Exhibit 99.4

Multi-Line Reinsurance & Insurance Property / Property Catastrophe / Specialty Lines / Short-Tail Casualty Flagstone RE

SAFE HARBOUR STATEMENT This presentation may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934. All statements, other than statements of historical facts, included or referenced in this presentation which address activities, events or developments which we expect or anticipate will or may occur in the future are forward-looking statements. The words “will,” “believe,” “intend,” “expect,” “anticipate,” “project,” “estimate,” “predict” and similar expressions are also intended to identify forward-looking statements. These forward-looking statements include, among others, statements with respect to Flagstone’s: growth in book value per share or return on equity; business strategy; financial and operating targets or plans; incurred losses and the adequacy of its loss and loss adjustment expense reserves and related reinsurance; projections of revenues, income (or loss), earnings (or loss) per share, dividends, market share or other financial forecasts; expansion and growth of our business and operations; and future capital expenditures. These statements are based on certain assumptions and analyses made by Flagstone in light of its experience and perception of historical trends, current conditions and expected future developments, as well as other factors believed to be appropriate in the circumstances. However, whether actual results and developments will conform to our expectations and predictions is subject to a number of risks and uncertainties that could cause actual results to differ materially from expectations, including: the risks described in our Annual Report or Form 10-Q; claims arising from catastrophic events, such as hurricanes, earthquakes, floods or terrorist attacks; the continued availability of capital and financing; general economic, market or business conditions; business opportunities (or lack thereof) that may be presented to it and pursued; competitive forces, including the conduct of other property and casualty insurers and reinsurers; changes in domestic or foreign laws or regulations, or their interpretation, applicable to Flagstone, its competitors or its clients; an economic downturn or other economic conditions adversely affecting its financial position; recorded loss reserves subsequently proving to have been inadequate; other factors, most of which are beyond Flagstone’s control. Consequently, all of the forward-looking statements made in this presentation are qualified by these cautionary statements, and there can be no assurance that the actual results or developments anticipated by Flagstone will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, Flagstone or its business or operations. Flagstone assumes no obligation to publicly update any such forward-looking statements, whether as a result of new information, future events or otherwise.

Mark Byrne Executive Chairman 22 years industry experience Prior experience: Chairman: West End Capital Management Director: White Mountains, Terra Nova, Markel Significant Capital Markets experience – Salomon Brothers, Credit Suisse, Lehman Brothers David Brown Chief Executive Officer 26 years industry experience Prior experience: Chairman: Merastar Insurance CEO: Centre Solutions (Bermuda) Partner: Ernst & Young Gary Prestia Chief Underwriting Officer, North America 24 years industry experience Prior experience: CEO: Alea North America President: Converium North America Senior Vice President: Transatlantic Re

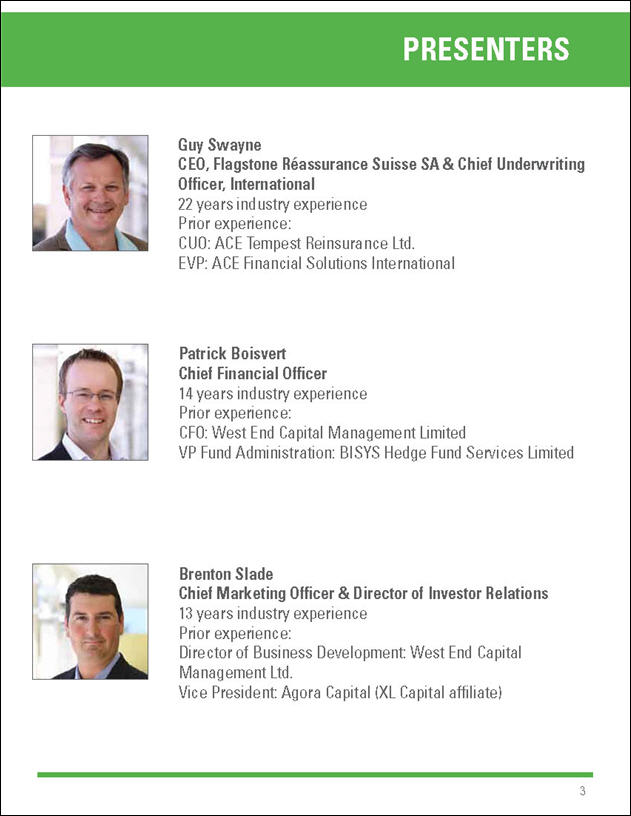

Presenters Guy Swayne CEO, Flagstone Réassurance Suisse SA & Chief Underwriting Officer, International 22 years industry experience Prior experience: CUO: ACE Tempest Reinsurance Ltd. EVP: ACE Financial Solutions International Patrick Boisvert Chief Financial Officer 14 years industry experience Prior experience: CFO: West End Capital Management Limited VP Fund Administration: BISYS Hedge Fund Services Limited Brenton Slade Chief Marketing Officer & Director of Investor Relations 13 years industry experience Prior experience: Director of Business Development: West End Capital Management Ltd. Vice President: Agora Capital (XL Capital affiliate)

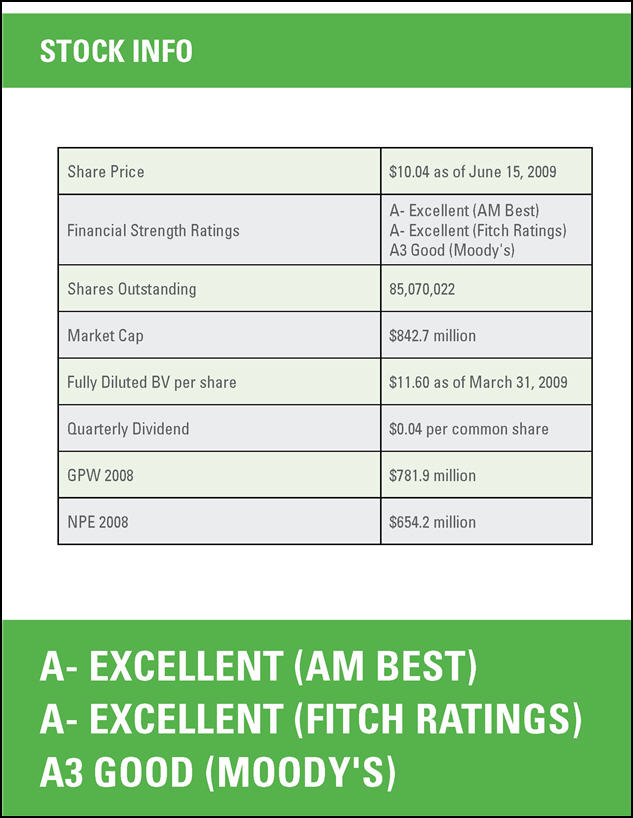

Stock Info Share Price $10.04 as of June 15, 2009 Financial Strength Ratings A- Excellent (AM Best) A- Excellent (Fitch Ratings) A3 Good (Moody’s) Shares Outstanding 85,070,022 Market Cap $842.7 million Fully Diluted BV per share $11.60 as of March 31, 2009 Quarterly Dividend $0.04 per common share GPW 2008 $781.9 million NPE 2008 $654.2 million A- Excellent (AM Best) A- Excellent (Fitch Ratings) A3 Good (Moody’s)

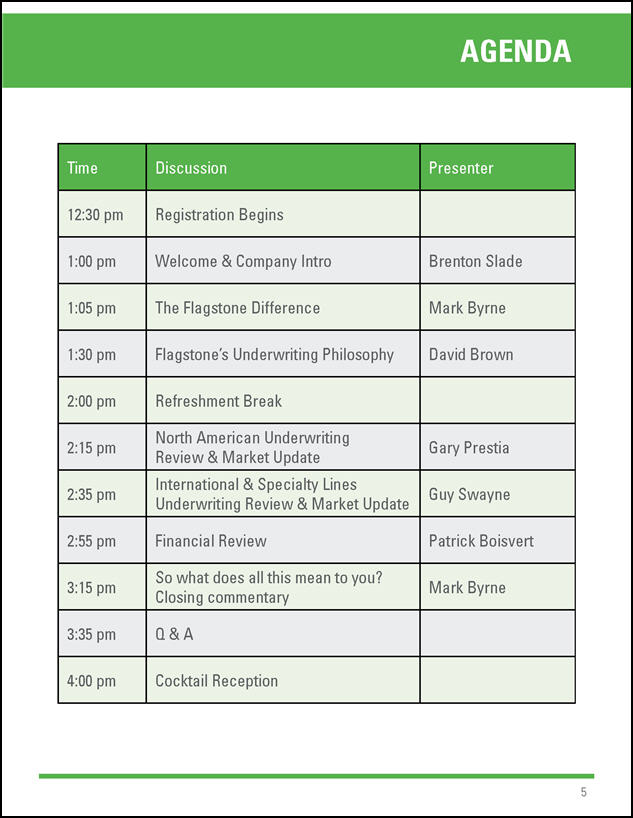

Agenda Time Discussion Presenter 12:30 pm Registration Begins 1:00 pm Welcome & Company Intro Brenton Slade 1:05 pm The Flagstone Difference Mark Byrne 1:30 pm Flagstone’s Underwriting Philosophy David Brown 2:00 pm Refreshment Break 2:15 pm North American Underwriting Review & Market Update Gary Prestia 2:35 pm International & Specialty Lines Underwriting Review & Market Update Guy Swayne 2:55 pm Financial Review Patrick Boisvert 3:15 pm So what does all this mean to you? Closing commentary Mark Byrne 3:35 pm Q & A 4:00 pm Cocktail Reception

Growth. Strength. Commitment

About Us Flagstone was formed in December 2005 in response to the market dislocation resulting from the historic catastrophe events of 2005. We grew successfully and rapidly and went public in April, 2007. Today, Flagstone is a multi-line reinsurer and insurer with over 500 talented employees in 13 offices and 12 countries around the globe dedicated to offering world-class service and the most comprehensive analysis of risk in the market. HISTORY Formed in Dec 05 IPO – April 07 Listed on NYSE & BSX ACQUISITIONS: Island Heritage Imperial Re/ FSR Africa Alliance Re/ FSR Alliance Lloyd’s – Syndicate 1861 TODAY: $1.3B Underwriting Capital 500+ employees 13 offices in 12 countries Operating Company and capital in Switzerland

Strategy & Objectives Flagstone fosters a strong service culture and continually pushes the boundaries of traditional modeling to provide better, richer data analysis in a shorter amount of time. We understand the need for prompt responses to quote and through the efficiency of our global platform and the utilization of proprietary technology, we can quickly respond to clients with informed, data driven risk analysis. OUR STRATEGY Leverage our global operating platform. Lead the industry in the utilization of proprietary analytics. Expand our strong broker and customer relationships through industry leading service. Employ our capital markets expertise to optimize our return and expand our opportunities. Communicate proactively and effectively with the investor community. Maintain an energetic culture that continuously challenges best practices. OUR OBJECTIVES Grow diluted book value per share. Obtain and maintain “A” level ratings from multiples agencies.

Clean. Value. Opportunity.

Our Current Position In 2008 we significantly grew our business and capabilities and have been able to capitalize on the difficulties being experienced by some major market participants. Our conservative investment portfolio, global platform, and preference for short-tail risks, position us to participate fully in the attractive markets 2009 is presenting. In October last year, we merged our wholly owned subsidiaries, Flagstone Reinsurance Limited of Bermuda and Flagstone Réassurance Suisse SA into one operating platform, based in Switzerland. The restructure of our operations to Switzerland gives us one single consolidated balance sheet with superior credit and better leverage of capital for the global underwriting platform. THE CURRENT FSR OPPORTUNITY Clean, conservative investment portfolio No exposure to potential casualty problems: D&O, E&O, Financial institutions Hard market for short-tail property, property cat & specialty lines Profit from problems of competitors Very scalable operating capabilities Ability to underwrite worldwide

Intelligent. Innovative. Different.

The Flagstone Difference From our world-class technology and analytics to our global team of highly qualified professionals. Growing and diversifying strategically, while keeping a steady eye on our long-term goals, making sure all our stakeholders – clients, shareholders, employees – benefit from the organization we’ve succeeded in creating and are committed to maintaining. OUR DIFFERENCE Global Platform Unique, efficient, and scalable Technology Cutting-edge analytics for superior risk analysis and industry leading customer service Diversification Balanced, conservative and strategic

Unique. Efficient. Scalable.

OUR GLOBAL PLATFORM Our unique global platform acknowledges the international nature of our operations. It allows us to allocate our capacity to the most attractive opportunities and to capitalize on the unique strengths of service and staffing available in distinct geographic locations. Through the efficiency of our global platform, we can source more business worldwide, undertaking the high quality, high volume and comprehensive risk analysis that helps set Flagstone apart. The result is an efficient, scalable, globally present operation that is rich in talent and specialized expertise. THROUGH THE EFFICIENCY OF OUR GLOBAL PLATFORM, FLAGSTONE IS ABLE TO: Source more risks, and be more selective in the risks we choose Offer fast, efficient service to clients 24 hours a day. Respond rapidly to submissions Penetrate local markets – source business that wouldn’t typically be directed to larger markets Retain more professional talent in comparison to companies several times our size Leverage low cost jurisdictions – cost efficiencies to analyze ALL risks.

Cutting-edge. Speed. Service.

TECHNOLOGY With the use of proprietary systems and analytical resources we can analyze more data, quicker, and with more comprehensive results. We are continually pushing the boundaries of traditional modeling to provide best in class service. Our innovative MOSAIC system gives our underwriters a proprietary view of risks. This cutting-edge technology, together with QUARTZ (our proprietary cat analysis tool), and CYCLONE (our high performance computing platform), allow us to analyze more risks, and make more informed underwriting decisions. These proprietary systems give us an additional view of risk that may differ from commercial models, and consider additional risk factors to provide higher quality risk analysis and exposure aggregation. WHERE TECHNOLOGY AND UNDERWRITING MEET Entire company integrated through technology Centralized underwriting systems and controls – single system Fully integrated work flow, underwriting & risk management system Combination of commercial models and in-house analytics to effectively control, monitor and analyze risks Real-time portfolio simulation and analysis Marginal pricing analysis & underwriting Assess capital adequacy relative to internal risk tolerance and regulatory criteria

Data Sources Proprietary Analytics RMS Mosaic Mosaic Pricing Risk Management Database Model (MPM) Solutions Engine AIR Mosaic Loss Portfolio (MLP) EQE Mosaic Dynamic Risk Model (MDRM) Investment Analysis Systems Comprehensive. Dynamic. Efficient.

Analytics MOSAIC. Our underwriting portfolio system - a large database and underwriting system. Loss portfolio analysis Optimization of exposures by risk Assess capital adequacy Risk tolerance and regulatory criteria QUARTZ. Our own proprietary CAT Models built due to discrepancies with existing vendor models. We also build models in markets without existing models. Additional proprietary view of risks Considers additional load factors CYCLONE. A massive computing platform to run all our suite of programs at an accelerated rate. Power to analyze large volumes of risk Quicker & more efficient results MOSAIC PRICING MODEL (MPM) Identify attractive opportunities by stand-alone pricing MOSAIC LOSS PORTFOLIO (MLP) Optimize exposures by risk zone from real-time marginal pricing simulations MOSAIC DYNAMIC RISK MODEL (MDRM) Firm-wide dynamic simulation ATTRACTIVE RISK

ADJUSTED RETURN ON CAPITAL

Design. Balance. Protect.

Diversification In our industry, security and protection is a key concern for clients. Diversification provides security and protection. At Flagstone we diversify our business in several ways: geographically, through multiple lines of business, and in our risk choices. In addition we also limit our zonal exposures to protect our balance sheet against potential loss from large industry events. As part of our diversification strategy, we continue to grow our business into attractive complementary lines of business. (Q4 2008 was an example of this strategy as we acquired Alliance Re, and Marlborough Underwriting Agency Limited at Lloyd’s). These strategic acquisitions further diversify our global portfolio and complement our current book of business. They also provide us with local access and talent in growing and attractive markets. WE DIVERSIFY BY: Lines of Business Growing specialty lines Moving towards 50% Property Cat/50% Specialty Geographically New offices Talented teams Strategic acquisitions

Diversify. Strengthen. Prosper.

Underwriting Philosophy Flagstone has a unique underwriting philosophy that has positioned us as a best in class underwriter. Our global diversification allows us to write more business and source more risks than typical underwriters. This translates into increased premium leverage coupled with lower zonal risk exposures. The result is a superior annual loss ratio and the ability to withstand and prosper in times of severe loss events. Diversification globally Diversification allows for premium leverage Premium leverage lessens per event losses More frequent small losses but better annual loss ratio Allocate capital tactically Select best clients/blue chips LOB that we understand and can make use of our toolset SERVICE

Intelligent. Strategic. Selective.

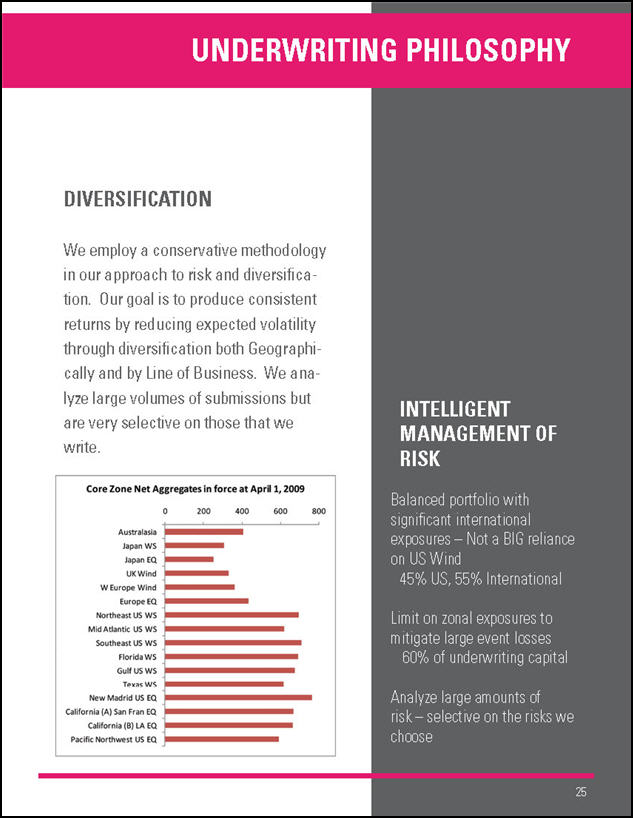

Underwriting Philosophy DIVERSIFICATION We employ a conservative methodology in our approach to risk and diversification. Our goal is to produce consistent returns by reducing expected volatility through diversification both Geographically and by Line of Business. We analyze large volumes of submissions but are very selective on those that we write. Core Zone Net Aggregates in force at April 1, 2009 0 200 400 600 800 Australasia Japan WS Japan EQ Uk Wind W Europe Wind Europe EQ Northeast US WS Mid Atlantic US WS Southeast US WS Florida WS Gulf US WS Texas WS New Madrid US EQ California (A) San Fran EQ California (B) LA EQ Pacific Northwest US EQ INTELLIGENT MANAGEMENT OF RISK Balanced portfolio with significant international exposures – Not a BIG reliance on US Wind 45% US, 55% International Limit on zonal exposures to mitigate large event losses 60% of underwriting capital Analyze large amounts of risk – selective on the risks we choose

Design. Balance. Protect.

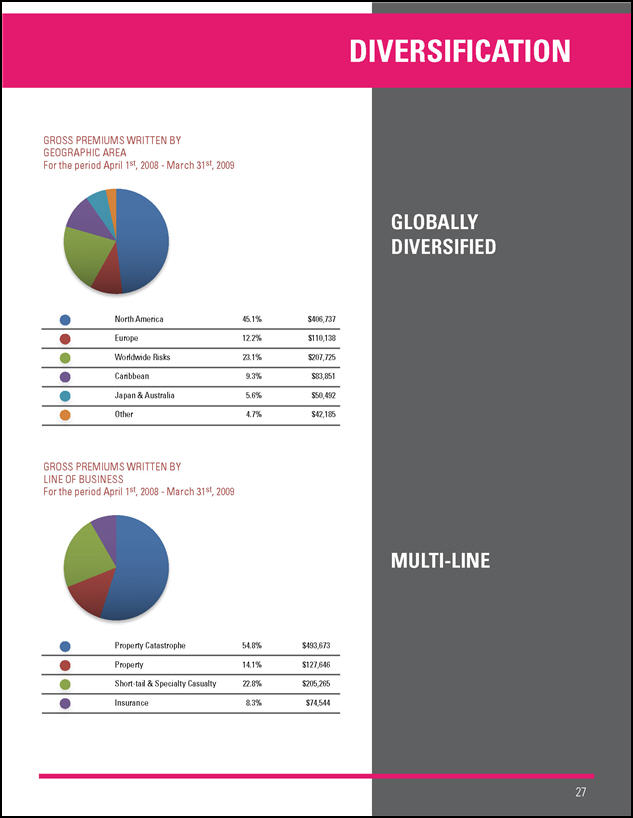

Diversification Gross Premiums Written by Geographic Area For the period April 1st, 2008 – March 31st, 2009 Globally Diversified North America 45.1% $406,737 Europe 12.2% $110,138 Worldwide Risks 23.1% $207,725 Caribbean 9.3% $83,851 Japan & Australia 5.6% $50,492 Other 4.7% $42,185 Gross Premiums Written by Line of Business For the period April 1st, 2008 – March 31st, 2009 Multi-Line Property Catastrophe 54.8% $493,673 Property 14.1%$127,646 Short-tail & Specialty Casualty 22.8% $205,265 Insurance 8.3% $74,544

Intelligent Risk Management

Underwriting Philosophy RISK MANAGEMENT ONE Underwriting System and pricing model for ALL underwriting team globally whether in Bermuda, Martigny, or Puerto Rico. Entire Company integrated through systems encompassing; workflow, underwriting, risk management, accounting, and auditing. Several layers of risk management to limit large, unexpected losses. Continual peer reviews to provide check on subjective risks and scaling levels of authority for binding. PROPRIETARY TECHNOLOGY TO EFFICIENTLY MANAGE RISK Monitor zonal loss limits as % of capital per zone Monitor exposures in adjacent combined zones Per risk (cedant/layer) Per event (1st event, 2nd event, aggregate) Per occurrence loss estimates Identifying potential loss scenarios Comparing & selecting risks Conservative Methodology as at March 31, 2009: 1 in 100 PML of $236M 1 in 250 PM L of $311M

Underwriting Philosophy SERVICE We have an award winning level of service We have won three awards in this industry for our outstanding level of service. That’s important not because it makes clients and brokers happy; when you finally decide after analysis which of the businesses you see you would like to write; it’s important to have a strong relationship with the client so you can actually get a preferred share of the business when you want it. Utilize proprietary technology and global talent to provide comprehensive risk analysis and support to clients Rapid turnaround and response Provide lead quote & price Extend large capacity for risks we like Visit frequently – local professionals

Technology. Integration. Efficiency.

Underwriting Philosophy Our entire submission, underwriting, and accounting process is integrated through our proprietary system to provide seamless workflow and ultimately superior service and efficiency. INTEGRATED THROUGH TECHNOLOGY Entire submission, underwriting, and accounting process integrated in systems Rigorous peer reviews Differing levels of authorization Fully SOX compliant

Underwriting Philosophy QUALITY PORTFOLIO Our portfolio is built from the ground up, partnering with the best practitioners and insisting on the highest quality data possible. Insisting on high quality data and focusing on regional allocations, we have a clear understanding of our aggregate exposures and confidence in our ability to generate risk-adjusted returns. Partner with Blue Chip Companies Prefer regional exposures vs. national exposures Residential property vs. Commercial property Prefer XOL vs. Proportional Approx 86% XOL Generally conservative loss estimates Detailed cedant exposure: Detailed data resolution vs. aggregate resolution data 93% for US, 97.5% for Europe

Strategic Capacity Optimization

Underwriting Philosophy REINSURANCE Flagstone is not typically a large purchaser of retrocessional coverage. However, the events of 2008 made the availability of external capital extremely limited and therefore we acted early and purchased traditional retro in the Autumn of 2008 We prefer to diversify our retro via: Cat Bonds Sidecars Specific Retro Traditionally mainly net writer Current 80% net retention ratio Specific purchases to support business expansion Guideline on min rating of A- Collateralization if below A-

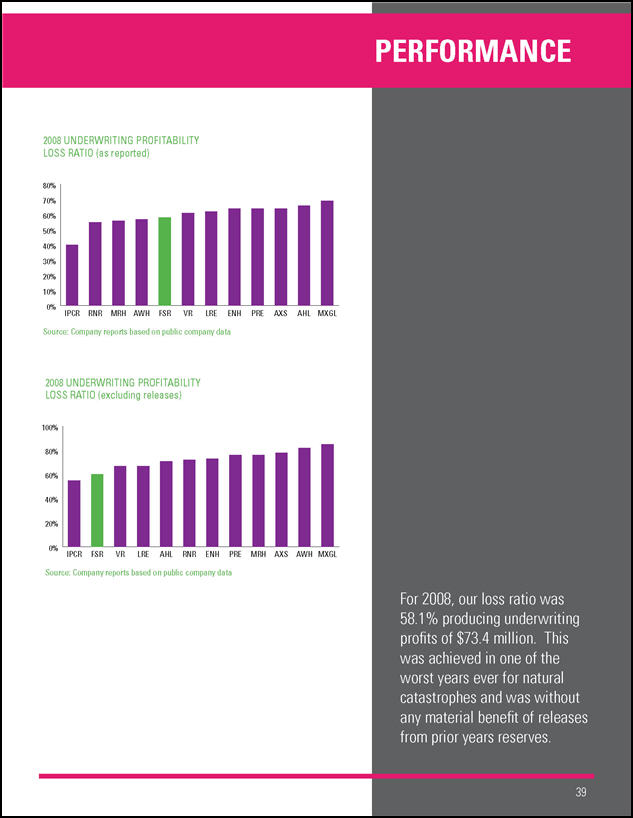

Performance 2008 Underwriting Profitability Loss Ratio (as reported) 80% 70% 60% 50% 40% 30% 20% 10% 0% IPCR RNR MRH AWH FSR VR LRE ENH PRE AXS AHL MXGL Source: Company reports based on public company data 2008 Underwriting Profitability Loss Ratio (excluding releases) 100% 80% 60% 40% 20% 0% IPCR FSR VR LRE AHL RNR ENH PRE MRH AXS AWH MXGL Source: Company reports based on public company data For 2008, our loss ratio was 58.1% producing underwriting profits of $73.4 million. This was achieved in one of the worst years ever for natural catastrophes and was without any material benefit of releases from prior years reserves.

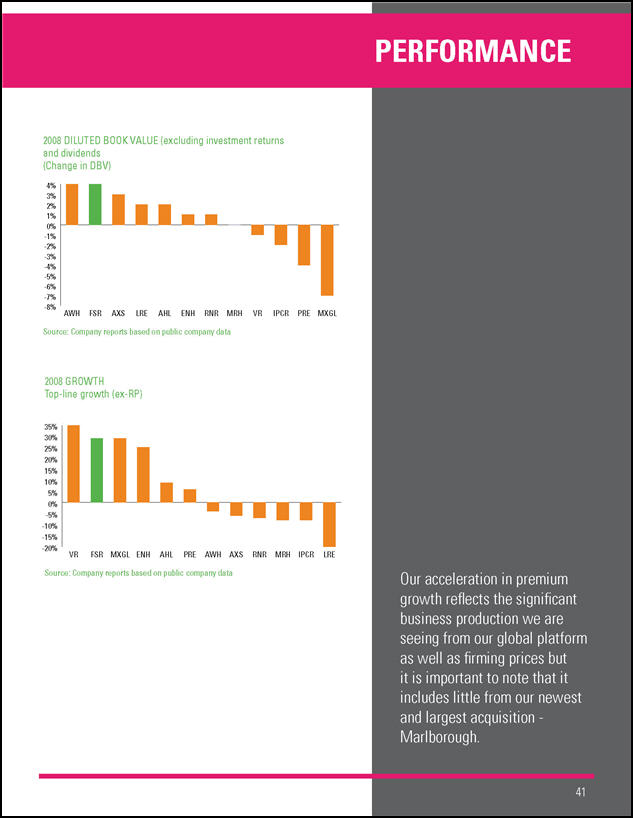

Performance 2008 Diluted Book Value (excluding investment returns and dividends) (Change in DBV) 4%3% 2% 1% 0% -1% -2% -3% -4% -5% -6% -7% -8% AWH FSR AXS LRE AHL ENH RNR MRH VR IPCR PRE MXGL Source: Company reports based on public company data 2008 Growth Top-line growth (ex-RP) 35% 30% 25% 20% 15% 10% 5% 0% -5% -10% - -15% -20% VR FSR MXGL ENH AHL PRE AWH AXS RNR MRH IPCR LRE Source: Company reports based on public company data Our acceleration in premium growth reflects the significant business production we are seeing from our global platform as well as firming prices but it is important to note that it includes little from our newest and largest acquisition - Marlborough.

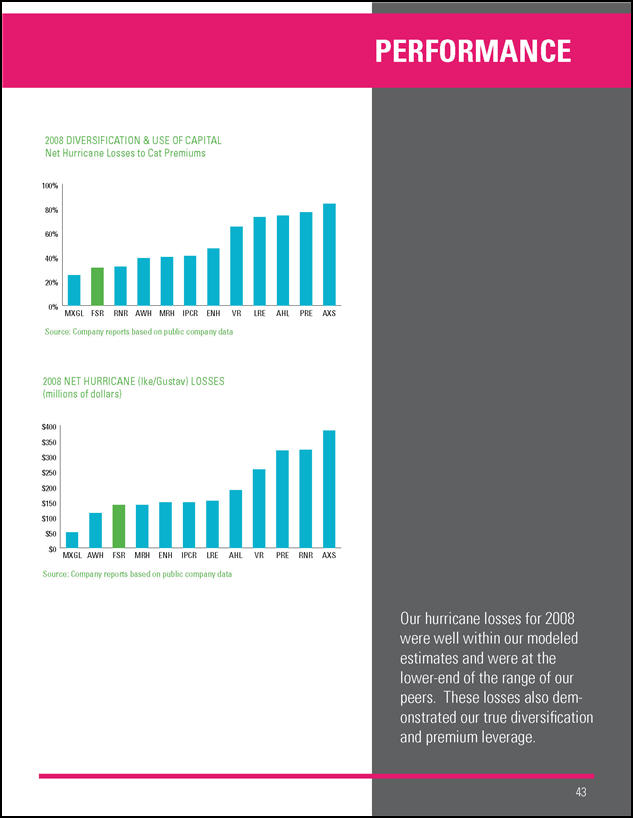

Performance 2008 Diversification & Use of Capital Net Hurricane Losses to Cat Premiums 100% 80% 60% 40% 20% 0% MXGL FSR RNR AWH MRH IPCR ENH VR LRE AHL PRE AXS Source: Company reports based on public company data 2008 Net Hurricane (Ike/Gustav) Losses (millions of dollars) $400 $350 $300 $250 $200 $150 $100 $50 $0 MXGL AWH FSR MRH ENH IPCR LRE AHL VR PRE RNR AXS Source: Company reports based on public company data Our hurricane losses for 2008 were well within our modeled estimates and were at the lower-end of the range of our peers. These losses also demonstrated our true diversification and premium leverage.

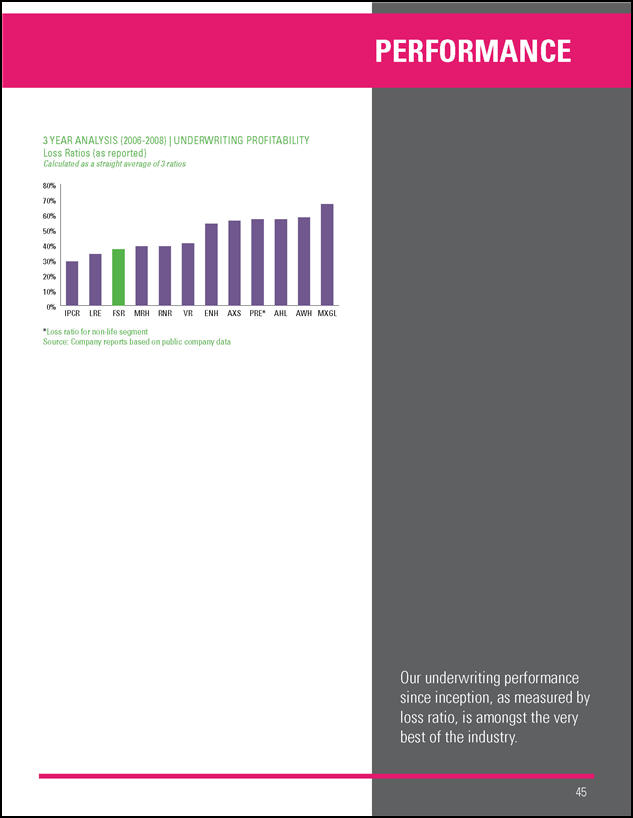

Performance 3 Year Analysis (2006-2008) / Underwriting Profitability Loss Ratios (as reported) Calculated as a straight average of 3 ratios 80% 70% 60% 50% 40% 30% 20% 10% 0% IPCR LRE FSR MRH RNR VR ENH AXS PRE* AHL AWH MXGL *Loss ratio for non-life segment

Source: Company reports based on public company data Our underwriting performance since inception, as measured by loss ratio, is amongst the very best of the industry.

Strong Strategic Performance

NA Underwriting Philosophy At Flagstone we employ a high-touch model. We promote frequent interaction with clients and brokers so that we fully understand our clients’ business. We underwrite the quality of our clients; their underwriting and claims expertise and loss history . . . an approach that produces superior results based on industry data. This combined with our own comprehensive data analysis, cat modeling and marginal pricing analysis provides for a quality book of business. Underwrite NA Cat in Bermuda - one team, highly coordinated Selectively deploy capital in most attractive market - US Property Cat Understand our clients business Favour long term clients – reinsurance purchase “must buy” vs. “opportunistic buy” Quality book - underwrite for profit margin/ROE, not premium Industry leading service fosters satisfaction, loyalty/ sustainability

Clear. Consistent. Knowledgeable.

NA Underwriting Approach Our aim is to be the top choice of brokers and clients and produce industry-leading results. Become top choice of brokers & clients by providing: High level of technical expertise in risks we write Rapid & informed quoting Large capacity within our Underwriting guidelines on the high quality clients we target Clear and timely response on submissions of business we will & will not write – a quick “no” is appreciated Consistent approach – know what to expect from us Favorable broker feedback - within a tight range of final pricing on business we quote

Clients. Quality. Capacity.

NA Portfolio We were very pleased with Q1’s strong-renewal book and addition of new clients. Rate increases were at the top end of our expectations with US premiums up approximately 32% and related aggregate exposure approximately the same as 2008. The mid-year business is important for us as we favor regional exposures vs. nationwide exposures. We plan to deploy capital to take advantage of the market opportunities and provide significant capacity for quality clients. Profitable results since inception Q1 09 NA Premiums up by 31.6% Strong 6/1 renewals High teens increase in rates at June 1 North American portfolio – aggregate exposures similar to 08 Expect solid 7/1 renewals

Capacity. Demand. Supply.

NA Market Update We’ve seen a hardening market due to continued adverse development of IKE losses and the severity of the global financial crisis. Based on the Florida Hurricane Cat Fund’s decision to reduce the TICL layer (by $2bn for 2009 and for the next 5 years) as well a Texas Windstorm Insurance Association’s increased industry assessment potential these factors will likely cause a demand/supply imbalance for US CAT reinsurance into 2010. Hardening US Property cat reinsurance market first half of 2009 due to: IKE development Severity of global financial crisis and investment results Difficulties of major market participants – desire to syndicate placement Rating agency pressures FHCF’s $2bn reduction in TICL = growth in Florida demand TWIA Assessment = greater exposure to Texas companies Reduced sidecar and hedge fund capacity

NA Opportunities To date we have developed a profitable and maturing US Property portfolio. The opportunity now exists to refine and optimize the mix by program and focus on expanding and leveraging our relationships to see additional lines of business and new submissions. Developed profitable & maturing US Property portfolio Opportunity to refine and optimize mix by program Re-evaluate core clients and brokers Meet with clients prior to renewal Remain nimble in accessing market opportunities “Live cat” and post-event covers Continue to profitably grow as we have done for the past 3 1/2 years

Technology Driven Underwriting

International Underwriting OUR APPROACH We focus on providing high quality service to brokers and clients in order to see large amounts of business and gain preferential shares on quality programs. Quick turnaround time and clear appetites for submissions – service is key! Combining technology driven underwriting with experienced judgment and focusing on clients who value risk management has produced excellent year over year results. Targeted core clients = foundation for portfolio Focus on service level to brokers and clients Leveraged Bermuda Cat business to expand other relationships and develop Specialty Lines Focus on territories and LOB with best returns Internal coordination

Strong Analytical Knowledge

Location, Teams and LOB BERMUDA INTERNATIONAL CATASTROPHE TEAM We have a strong International Cat team – we swear the team was together in a previous life! We have strong analytical and model knowledge and recognize the importance of understanding the models - not relying on them. We set a clear plan in 2006 to target top percentile companies in respective regions and our plan has worked. Strong analytical and model knowledge - understand the models - not rely on them Strong relationship = targeted business Quoting market status with superior technical response plus large capacity Private deals enhance relationships with improved returns Consistent approach - well received by clients and brokers

Experience. Relationships. Service.

Location, Teams and LOB FLAGSTONE RÉASSURANCE SUISSE SA - MARTIGNY The underwriting group in Martigny is a high quality team with enormous experience in Europe. The team was structured to provide great balance between relationship underwriters with extensive experience in the market and technical underwriters with advanced quantitative and analytical skills. Embracing the overall Flagstone underwriting philosophy, the team is highly active in their marketing efforts and strive to touch our clients on a more frequent basis that our competitors. Furthermore, responding rapidly with informed decisions to submissions is changing the paradigm of service in Europe and winning substantial business. WE TARGET CLIENTS RATHER THAN MARKET SHARE AND FOCUS ON COUNTRIES WITH ADEQUATE MARGINS 2008 established as European Reinsurer 2009 excellent development: Improved service level Noticeable breakthrough in German direct market Complements BDA with focus on proportional, risk and local markets Current offer to bind ratio of approximately 15% or less Optimistic for next year’s renewals with Competitor problems driving greater Reinsurer diversification

Focused. Experienced. Strong.

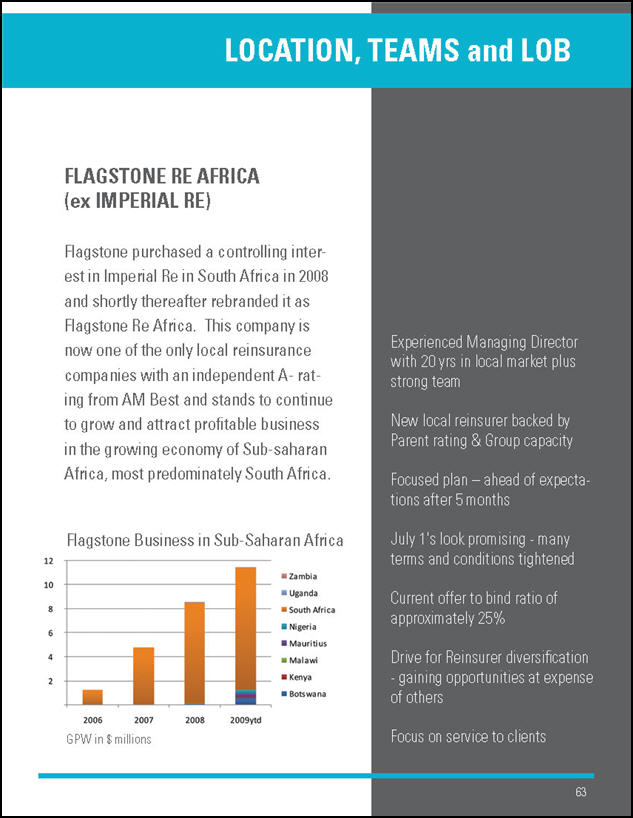

Location, Teams and LOB FLAGSTONE RE AFRICA (ex IMPERIAL RE) Flagstone purchased a controlling interest in Imperial Re in South Africa in 2008 and shortly thereafter rebranded it as Flagstone Re Africa. This company is now one of the only local reinsurance companies with an independent A- rating from AM Best and stands to continue to grow and attract profitable business in the growing economy of Sub-saharan Africa, most predominately South Africa. Flagstone Business in Sub-Saharan Africa 12 10 8 6 4 2 2006 2007 2008 2009ytd Zambia Uganda South Africa Nigeria Mauritius Malawi Kenya Botswana Experienced Managing Director with 20 yrs in local market plus strong team New local reinsurer backed by Parent rating & Group capacity Focused plan – ahead of expectations after 5 months July 1’s look promising - many terms and conditions tightened Current offer to bind ratio of approximately 25% Drive for Reinsurer diversification - gaining opportunities at expense of others Focus on service to clients

Experienced Technical Professionals

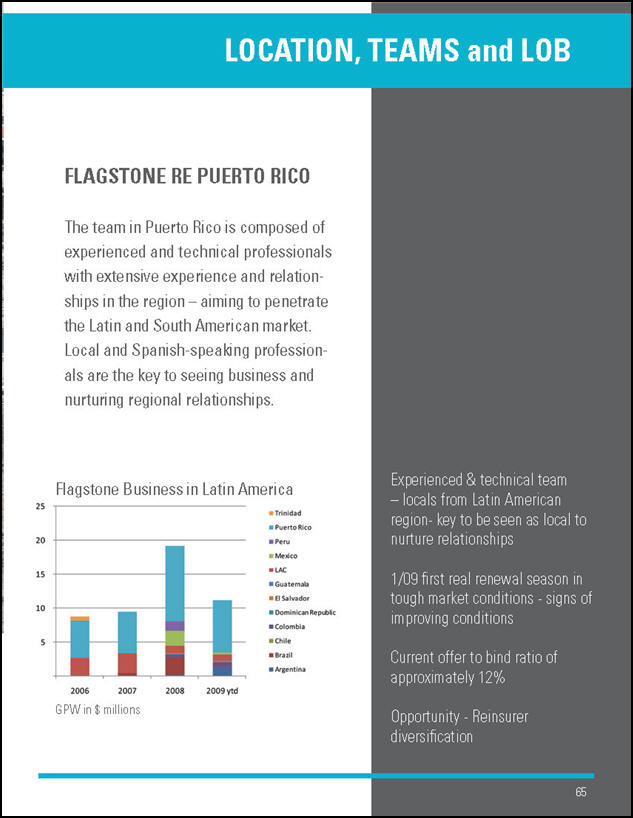

Location, Teams and LOB FLAGSTONE RE PUERTO RICO The team in Puerto Rico is composed of experienced and technical professionals with extensive experience and relationships in the region – aiming to penetrate the Latin and South American market. Local and Spanish-speaking professionals are the key to seeing business and nurturing regional relationships. Flagstone Business in Latin America 25 20 15 10 5 2006 2007 2008 2009 ytd Trinidad Puerto Rico Peru Mexico LAC Guatemala El Salvador Dominican Republic Colombia Chile Brazil Argentina GPW in $ millions Experienced & technical team – locals from Latin American region- key to be seen as local to nurture relationships 1/09 first real renewal season in tough market conditions - signs of improving conditions Current offer to bind ratio of approximately 12% Opportunity - Reinsurer diversification

Attractive Growing Economy

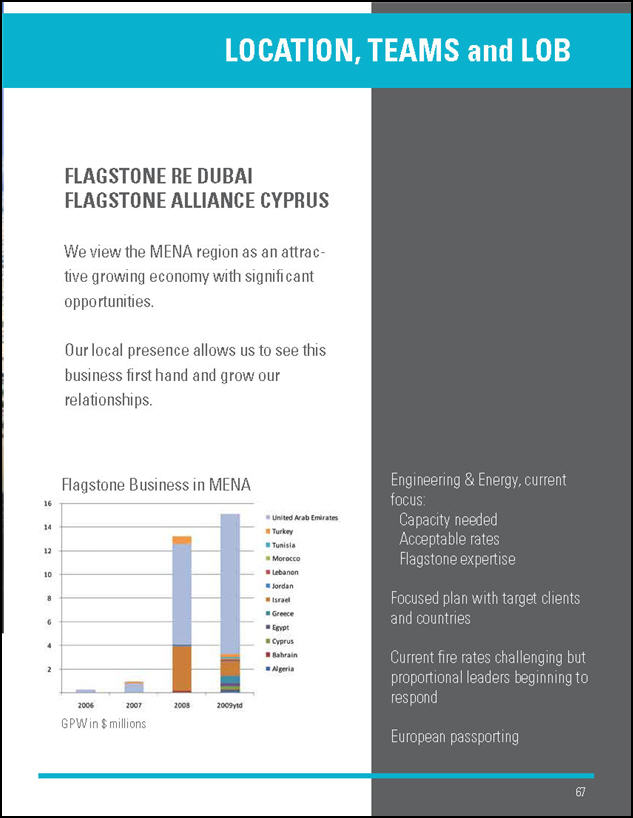

Location, Teams and LOB FLAGSTONE RE DUBAI FLAGSTONE ALLIANCE CYPRUS We view the MENA region as an attractive growing economy with significant opportunities. Our local presence allows us to see this business first hand and grow our relationships. Flagstone Business in MENA 16 14 12 10 8 6 4 2 2006 2007 2008 2009ytd United Arab Emirates Turkey Tunisia Morocco Lebanon Jordan Israel Greece Egypt Cyprus Bahrain Algeria GPW in $ millions Engineering & Energy, current focus: Capacity needed Acceptable rates Flagstone expertise Focused plan with target clients and countries Current fire rates challenging but proportional leaders beginning to respond European passporting

MARGINS. RENEWALS. OPPORTUNITIES.

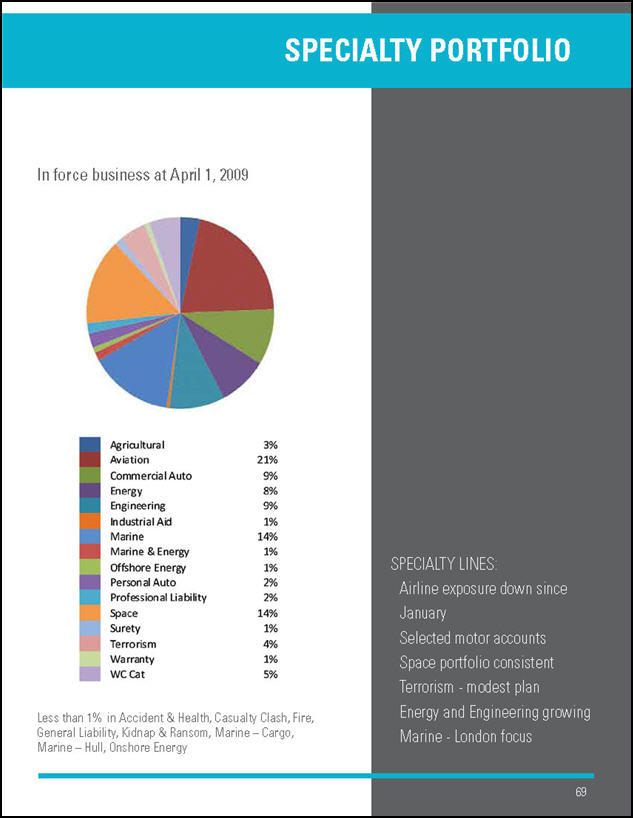

Specialty Portfolio In force business at April 1, 2009 Agricultural 3% Aviation 21% Commercial Auto 9% Energy 8% Engineering 9% Industrial Aid 1% Marine 14% Marine & Energy 1% Offshore Energy 1% Personal Auto 2% Professional Liability 2% Space 14% Surety 1% Terrorism 4% Warranty 1% WC Cat 5% Less than 1% in Accident & Health, Casualty Clash, Fire, General Liability, Kidnap & Ransom, Marine – Cargo, Marine – Hull, Onshore Energy SPECIALTY LINES: Airline exposure down since January Selected motor accounts Space portfolio consistent Terrorism - - modest plan Energy and Engineering growing Marine - London focus

Short-Tail Specialist Portfolio

Lloyd’s Platform Marlborough Underwriting Agency Limited (“MUAL”) is the managing agent for Syndicate 1861 purchased by Flagstone in Q4 2008. MUAL writes a Specialist portfolio of short-tail insurance & reinsurance such as marine, energy, aviation and XOL reinsurance. BENEFITS: Global distribution & licenses Lloyd’s branding A+ Rating Further diversifying short-tail specialty lines Extended market reach Scalable platform Experienced team with deep relationships Efficient capital structure

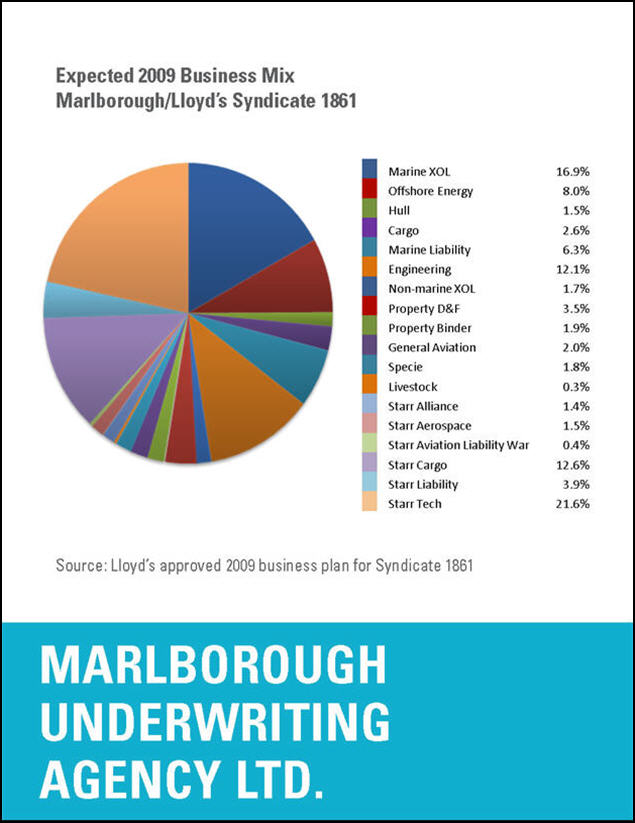

Expected 2009 Business Mix Marlborough/Lloyd’s Syndicate 1861 Marine XOL 16.9% Offshore Energy 8.0% Hull 1.5% Cargo 2.6% Marine Liability 6.3% Engineering12.1% Non-marine XOL 1.7% Property D&F 3.5% Property Binder 1.9% General Aviation 2.0% Specie 1.8% Livestock 0.3% Starr Alliance 1.4% Starr Aerospace 1.5% Starr Aviation Liability War 0.4% Starr Cargo 12.6% Starr Liability 3.9% Starr Tech 21.6% Source: Lloyd’s approved 2009 business plan for Syndicate 1861 Marlborough Underwriting Agency Ltd.

Lloyd’s Platform Flagstone purchased MUAL with no legacy business and as a result, the portfolio will take several quarters to contribute. Specialist portfolio, short-tail insurance & reinsurance: marine, energy, aviation and XOL reinsurance Fee based services – Frameworks, Insurance Admin and Turnkey No legacy business 2008 – GPW of GBP 80m ($119m) 2009 – New Business for FSR Expect GPW of GBP 100m ($130/$140) Currency benefit – strengthening of $

2009 & 2010 Prospects We are seeing increased volumes of submissions and expect opportunities to continue to present themselves as cedants look to diversify their risk amongst Reinsurers. Flagstone is well positioned to capitalize as opportunities develop, and we expect that the remainder of 2009 and 2010 will see us continue to strengthen the quality of our book of business. Global reach & high level of marketing activities Building solid reputation Seeing high volume of submissions Reinsurance rates improving Some regions & LOB already increased Cedants diversifying Reinsurer panel Already seeing benefits in Europe, Latin America & South Africa

Ratios. Metrics. Results.

Financial Snapshot Q1 Financial Highlights (in millions of U.S. dollars) Q1 2009 Q1 2008 Loss ratio 44% 29% Combined ratio 80% 67% Diluted Book value Growth 3.00% 1.80% Diluted Book value Growth ex-investments 3.20% 1.40% Net Premiums written to surplus 28% 18% Gross Premiums Written by LOB: Property Cat $209 $165 Property 43 19 Specialty 52 40 Lloyds 49 Insurance 17 19 Total GPW $370 $243 Global platform continues to generate quality premiums Loss Ratio (though higher than last year) - within long run expectations Premium leverage contributed to strong book value growth Recent acquisitions contribution to GPW: Lloyd’s $49M Alliance & Africa $24M

Annualized Value Creation

Key Metric – Growth in DBV $16 $15 $14 $13 $12 $11 $10 $9 $8 +20.5% +16.8% -17.4% +3.0% 9.86 11.94 0.08 13.87 0.24 11.3 0.28 11.6 12/31/2005 12/31/2006 12/31/2007 12/31/2008 3/31/2009 Diluted Book Value per share Cumulative Dividends Annualized value creation since inception of 5.9% while suffering concurrently one of the worst investment years and one of the worst catastrophe years in history. Our Key metric is Growth in Diluted Book Value per share Represents the value creation Board sets the growth target annually

Strong Underwriting Platform

Key Metric - Underwriting Contribution Diluted Book Value Growth (Ex-Investments) 36% 32% 28% 24% 20% 16% 12% 8% 4% 0% -4% -8% -12% -16% 16.3 24.9 28.9 32.1 16.3 8.6 4.0 3.2 12.8 12.8 11.4 2.3 2.0 2006 2007 2008 q1 2009 FSR Peers: Axis, Endurance, IPC Re, Lancashire, Montpellier, Ren Re, Validus Source: Company Reports Despite being only a “class of 2005” (therefore having a “ramp-up lag”) and without having any benefits of KRW reserves releases, we have outperformed our peers and believe this is a true reflection of the underwriting platform we have built. Better measure than combined ratio – factors premium leverage Superior core business results to our peers since inception due to: Diversification benefits

Premiums/capital management Better risk calls

Strong. Clean. Transparent.

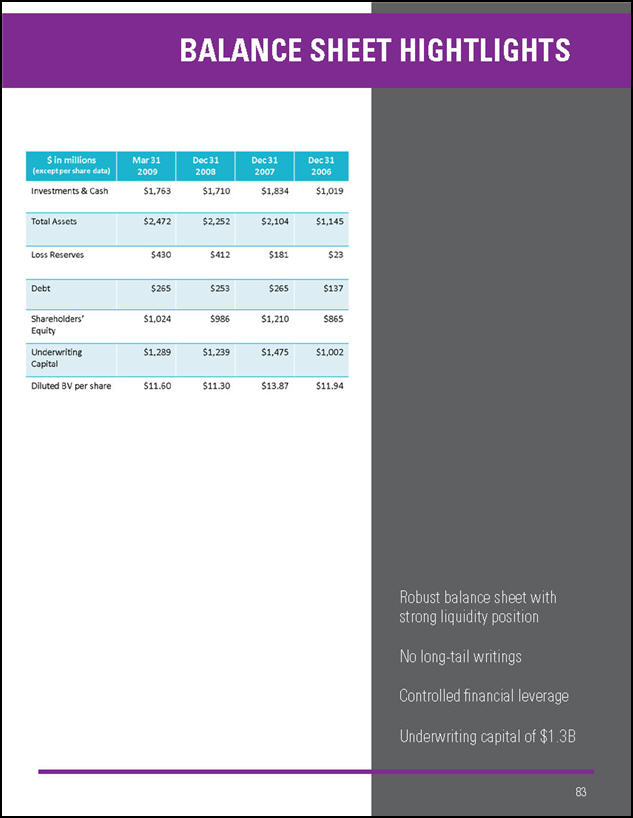

Balance Sheet Highlights $ in millions Mar 31 Dec 31 Dec 31 Dec 31 (except per share data) 2009 2008 2007 2006 Investments & Cash $1,763 $1,710 $1,834 $1,019Total Assets $2,472 $2,252 $2,104 $1,145 Loss Reserves $430 $412 $181 $23 Debt $265 $253 $265 $137 Shareholders’ Equity $1,024 $986 $1,210 $865 Underwriting Capital $1,289 $1,239 $1,475 $1,002 Diluted BV per share $11.60 $11.30 $13.87 $11.94 Robust balance sheet with strong liquidity position No long-tail writings Controlled financial leverage Underwriting capital of $1.3B

Current Allocation - Invested Assets Cash & Cash Equivalents 4.6% Commodities 3.1% Others 1.6% UST-Tips 20.6% ABS / MBS 9.8% Agencies 10.8% UST (Ex-Tips) 13.9% Corporates 15.5% *Sovereign bonds 16.5% Global Inflation Bonds Ex US 3.6% *Sovereign Bonds – Ex-US & Supranationals Average duration: 2.4 years Average credit rating: AA+ Clean. Conservative. Transparent.

Investments We recognized that the capital markets were in turmoil and not likely to quickly recover. We therefore reduced our asset risk and now have 94% in high grade fixed income and cash for a clean, transparent balance sheet. Although we expect lower returns from the asset allocation, this provides us with a stable capital base from which to underwrite. As such we expect to stay with this allocation for 2009 as we focus on producing superior underwriting performance. October 2008 - de-risked the portfolio Conservative portfolio – expect to stay here for 2009 At 3/31/09 - 94% of our assets in high grade fixed income securities & cash No material exposure to sub prime or Alt A securities Lower current returns – focus on underwriting Stable capital base with which to underwrite

Clean. Value. Opportunity.

The FSR Opportunity Business continues to be attractive and we are building franchise value and strong client support. The quality global platform we have built is producing strong underwriting results and we have all key systems in place and operating efficiently. We have a strong management team that shares one vision and has the determination to be the best at what we do. We are ideally positioned to take advantage of the opportunities in the market. Ideally positioned to take advantage of opportunities in the market High Quality book of business Adequate capital & strong balance sheet Systems, global locations & teams to provide: SHAREHOLDER VALUE (Investors) SERVICE (clients/brokers)

Commitments. Prospects. Opportunities.

Going Forward We are placed in the most attractive sectors of the market and the opportunities are significant. New opportunities have come out of crisis and Flagstone is well positioned to capitalize on them. We will continue to stay as strong as ever in our commitment to industry leading analytics and service. We are acquiring a reputation and image that differentiates us from our peers, and we think the prospects for the industry and for Flagstone are bright. ATTRACTIVE OPPORTUNITIES Business continues to be attractive Hardening market 2009 Growth Plan: Renewals Increase participation on programs Develop new clients especially with Marlborough Expand specialty business Global expansion Brazil

Multi-line. Global. Diversified.

Contact Us We diversify our portfolio exposure geographically and across multiple lines of business. Lines of Business: Property Property Catastrophe Specialty Lines Agribusiness Motor Aviation Personal Accident & Life Catastrophe Casualty Clash Property Specialty Energy Short-tail Casualty Engineering Space Kidnap & Ransom Structured Risk Live Cat Terrorism Marine Workers’ Compensation Catastrophe Subsidiaries: Flagstone Reinsurance Africa A wholly owned subsidiary specializing in short-tail property reinsurance in Sub-Saharan Africa, possessing independent A- rating from AM Best. Flagstone Alliance A wholly owned subsidiary providing A- rated insurance paper via European passporting rights, opening up new avenues for opportunity. Island Heritage Caribbean Property Insurer domiciled in Grand Cayman. Marlborough Underwriting Agency Lloyd’s of London Syndicate 1861; a specialist syndicate currently focused on marine, energy and aviation risks. Flagstone Reinsurance Holdings Limited 23 Church Street Hamilton HM 11 Bermuda Phone: 1 (441) 278 4300 Fax: 1 (441) 296 9879 info@flagstonere.bm Flagstone Réassurance Suisse SA Rue du Collège, 1 CH-1920 Martigny Switzerland Phone: +41 27 721 00 10 Fax: +41 27 721 00 11 infoch@flagstonere.bm

www.flagstonere.com FLAGSTONE RE