UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

Commission file number 001-33606

VALIDUS HOLDINGS, LTD.

(Exact name of registrant as specified in its charter)

|

| |

| BERMUDA | 98-0501001 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

29 Richmond Road, Pembroke, Bermuda HM 08

(Address of principal executive offices and zip code)

(441) 278-9000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class: | | Name of Each Exchange on Which Registered: |

| Common Shares, $0.175 par value per share | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | |

Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o (Do not check if a smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2012 was $2,077.0 million computed upon the basis of the closing sales price of the Common Shares on June 30, 2012. For the purposes of this computation, shares held by directors and officers of the registrant have been excluded. Such exclusion is not intended, nor shall it be deemed, to be an admission that such persons are affiliates of the registrant.

As of February 13, 2013, there were 107,468,544 outstanding Common Shares, $0.175 par value per share, of the registrant.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information from certain portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission within 120 days after the fiscal year ended December 31, 2012.

|

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| |

This Annual Report on Form 10-K contains “Forward-Looking Statements” as defined in the Private Securities Litigation Reform Act of 1995. A non-exclusive list of the important factors that could cause actual results to differ materially from those in such Forward-Looking Statements is set forth herein under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cautionary Note Regarding Forward-Looking Statements.”

PART I

All amounts presented in this part are in U.S. dollars except as otherwise noted.

Item 1. Business

Overview

Validus Holdings, Ltd. (the “Company”) was incorporated under the laws of Bermuda on October 19, 2005. Our initial investor, which we refer to as our founding investor, is Aquiline Capital Partners LLC, a private equity firm dedicated to investing in financial services companies. Other sponsoring investors included private equity funds managed by Goldman Sachs Capital Partners, Vestar Capital Partners, New Mountain Capital and Merrill Lynch Global Private Equity. The Company conducts its operations worldwide through three operating segments which have been determined under U.S. GAAP segment reporting, Validus Reinsurance, Ltd. (“Validus Re”), Talbot Holdings Ltd. (“Talbot”) and AlphaCat Managers, Ltd. ("AlphaCat"). The Company provides reinsurance, insurance and insurance linked securities management. Validus Re is a Bermuda based reinsurer focused on short tail lines of reinsurance. Talbot is the Bermuda parent of the specialty insurance group primarily operating within the Lloyd's insurance market through Syndicate 1183. AlphaCat is a Bermuda based investment adviser, managing third-party capital in insurance linked securities and other investments in the property catastrophe reinsurance space.

We seek to establish ourselves as a leader in the global insurance and reinsurance markets. Our principal operating objective is to use our capital efficiently by underwriting primarily short-tail insurance and reinsurance contracts with superior risk and return characteristics. Our primary underwriting objective is to construct a portfolio of short-tail insurance and reinsurance contracts which maximizes our return on equity subject to prudent risk constraints on the amount of capital we expose to any single event. We manage our risks through a variety of means, including contract terms, portfolio selection, diversification criteria, including geographic diversification criteria, and proprietary and commercially available third-party vendor catastrophe models.

Since our formation in 2005, we have been able to achieve substantial success in the development of our business. Selected examples of our accomplishments are as follows:

| |

| • | Raising approximately $1.0 billion of initial equity capital in December 2005 and underwriting $217.4 million in gross premiums written for the January 2006 renewal season; |

| |

| • | At the time of the Company’s formation an executive management team was assembled with an average of 20 years of industry experience and senior expertise spanning multiple aspects of the global insurance and reinsurance business; |

| |

| • | Building a risk analytics staff comprised of over 40 experts, many of whom have PhDs and Masters degrees in related fields; |

| |

| • | Developing Validus Capital Allocation and Pricing System (“VCAPS”), a proprietary computer-based system for modeling, pricing, allocating capital and analyzing catastrophe-exposed risks; |

| |

| • | Acquiring all of the outstanding shares of Talbot Holdings Ltd. on July 2, 2007; |

| |

| • | Completing an initial public offering (“IPO”) on July 30, 2007; |

| |

| • | Acquiring all of the outstanding shares of IPC Holdings Ltd. (“IPC”) on September 4, 2009; |

| |

| • | Raising $185.0 million of initial capital for AlphaCat Re 2011, Ltd. (“AlphaCat Re 2011”) on May 25, 2011 and a further $71.0 million of additional capital on December 23, 2011; |

| |

| • | Raising $500.0 million of capital for PaCRe, Ltd. ("PaCRe") a new Class 4 Bermuda reinsurer formed for the purpose of writing high excess property catastrophe reinsurance, on April 2, 2012; |

| |

| • | Raising $70.0 million of capital for AlphaCat Re 2012, Ltd. (“AlphaCat Re 2012”) on May 29, 2012; |

| |

| • | Acquiring all of the outstanding shares of Flagstone Reinsurance Holdings, S.A. ("Flagstone") on November 30, 2012; |

| |

| • | Raising $230.0 million of capital for Alpha Cat 2013, Ltd. ("AlphaCat 2013") on December 17, 2012 and receiving $219.4 million of third party subscriptions for AlphaCat Insurance Linked Securities ("ILS") Funds; |

| |

| • | Increasing the annual dividend by 20% from $1.00 to $1.20 per common share and per common share equivalent and announcing a $2.00 special dividend per common share and per common share equivalent on February 6, 2013; and |

| |

| • | Repurchasing approximately 43.7 million common shares for an aggregate purchase price of $1,227.1 million and paying and aggregate amount of $467.6 million in dividends from inception of the Company to February 13, 2013. |

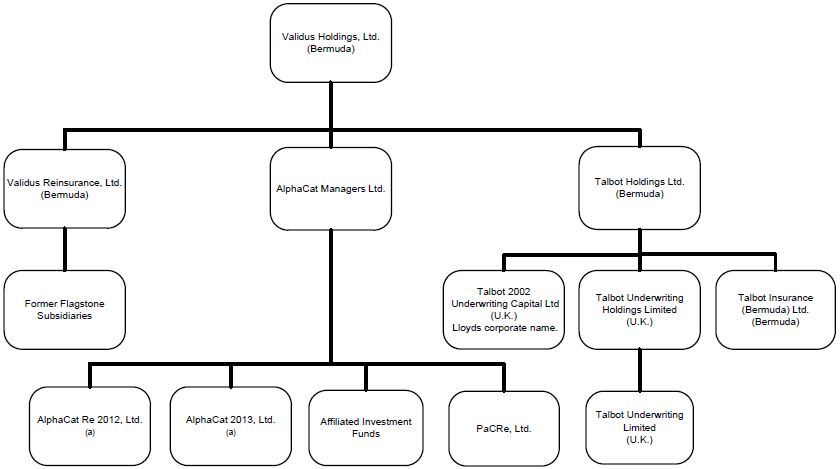

Our Operating Subsidiaries

The following chart shows how our Company and its principal operating subsidiaries are organized.

For a complete list of the Company’s subsidiaries, see Exhibit 21.

| |

| (a) | AlphaCat Re 2012 and AlphaCat 2013 are non-consolidated operating affiliates. |

Operating Segments

Validus Re: Validus Re, the Company’s principal reinsurance operating subsidiary, operates as a Bermuda-based provider of short-tail reinsurance products on a global basis. Validus Re concentrates on first-party risks, which are property risks and other reinsurance lines commonly referred to as short-tail in nature due to the relatively brief period between the occurrence and payment of a claim.

Validus Re was registered as a Class 4 insurer under The Insurance Act 1978 of Bermuda, amendments thereto and related regulations (the “Insurance Act”) in November 2005. It commenced operations with approximately $1.0 billion of equity capital and a balance sheet unencumbered by any historical losses relating to the 2005 hurricane season, the events of September 11, 2001, asbestos or other legacy exposures affecting our industry.

Validus Re entered the global reinsurance market in 2006 during a period of imbalance between the supply of underwriting capacity available for reinsurance on catastrophe-exposed property, marine and energy risks and demand for such reinsurance coverage.

On September 4, 2009, the Company acquired all of the outstanding shares of IPC. The primary lines in which IPC conducted business were property catastrophe reinsurance and, to a limited extent, property-per-risk excess, aviation (including satellite) and

other short-tail reinsurance on a worldwide basis. For segmental reporting purposes, the results of IPC’s operations since the acquisition date have been included within the Validus Re segment in the consolidated financial statements.

On November 30, 2012, the Company acquired all of the outstanding shares of Flagstone, strengthening the Company's leading property catastrophe reinsurance and short-tail specialty insurance platform. The primary lines in which Flagstone conducted business were property catastrophe reinsurance, property pro rata and per-risk excess and short tail specialty and casualty reinsurance such as aviation, energy, personal accident and health, satellite, marine and workers' compensation catastrophe. For segmental reporting purposes, the results of Flagstone’s operations since the acquisition date have been included within the Validus Re segment in the consolidated financial statements.

The following are the primary lines in which Validus Re conducts its business. Details of gross premiums written by line of business are provided below:

|

| | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, 2012 | | Year Ended December 31, 2011 | | Year Ended December 31, 2010 |

| (Dollars in thousands) | | Gross Premiums Written | | Gross Premiums Written (%) | | Gross Premiums Written | | Gross Premiums Written (%) | | Gross Premiums Written | | Gross Premiums Written (%) |

| Property | | $ | 771,617 |

| | 68.2 | % | | $ | 786,937 |

| | 70.6 | % | | $ | 778,794 |

| | 71.5 | % |

| Marine | | 257,469 |

| | 22.7 | % | | 232,401 |

| | 20.9 | % | | 227,135 |

| | 20.8 | % |

| Specialty | | 102,873 |

| | 9.1 | % | | 95,155 |

| | 8.5 | % | | 83,514 |

| | 7.7 | % |

| Total | | $ | 1,131,959 |

| | 100.0 | % | | $ | 1,114,493 |

| | 100.0 | % | | $ | 1,089,443 |

| | 100.0 | % |

Property: Validus Re underwrites property catastrophe reinsurance, property per risk reinsurance and property pro rata reinsurance.

Property catastrophe: Property catastrophe reinsurance provides reinsurance for insurance companies’ exposures to an accumulation of property and related losses from separate policies, typically relating to natural disasters or other catastrophic events. Property catastrophe reinsurance is generally written on an excess of loss basis, which provides coverage to primary insurance companies when aggregate claims and claim expenses from a single occurrence from a covered peril exceed a certain amount specified in a particular contract. Under these contracts, the Company provides protection to an insurer for a portion of the total losses in excess of a specified loss amount, up to a maximum amount per loss specified in the contract. In the event of a loss, most contracts provide for coverage of a second occurrence following the payment of a premium to reinstate the coverage under the contract, which is referred to as a reinstatement premium. The coverage provided under excess of loss reinsurance contracts may be on a worldwide basis or limited in scope to specific regions or geographical areas. Coverage can also vary from “all property” perils, which is the most expansive form of coverage, to more limited coverage of specified perils such as windstorm-only coverage. Property catastrophe reinsurance contracts are typically “all risk” in nature, providing protection against losses from earthquakes and hurricanes, as well as other natural and man-made catastrophes such as floods, tornadoes, fires and storms. The predominant exposures covered are losses stemming from property damage and business interruption coverage resulting from a covered peril. Certain risks, such as war or nuclear contamination may be excluded, partially or wholly, from certain contracts. Gross premiums written on property catastrophe business during the year ended December 31, 2012 were $598.0 million.

Property per risk: Property per risk reinsurance provides reinsurance for insurance companies’ excess retention on individual property and related risks, such as highly-valued buildings. Per risk excess of loss reinsurance protects insurance companies on their primary insurance risks on a “single risk” basis. A “risk” in this context might mean the insurance coverage on one building or a group of buildings or the insurance coverage under a single policy which the reinsured treats as a single risk. Coverage is usually triggered by a large loss sustained by an individual risk rather than by smaller losses which fall below the specified retention of the reinsurance contract. Such property per risk coverages are generally written on an excess of loss basis, which provides the reinsured protection beyond a specified amount up to the limit set within the reinsurance contract. Gross premiums written on property per risk business during the year ended December 31, 2012 were $59.3 million.

Property pro rata: Property pro rata contracts require that the reinsurer share the premiums as well as the losses and loss expenses in an agreed proportion with the cedant. Gross premiums written on property pro rata business during the year ended December 31, 2012 were $114.2 million.

Marine: Validus Re underwrites reinsurance on marine risks covering damage to or losses of marine vessels and cargo, third-party liability for marine accidents and physical loss and liability from principally offshore energy properties. Validus Re underwrites marine on an excess of loss basis and on a pro rata basis. Gross premiums written on marine business during the year ended December 31, 2012 were $257.5 million.

Specialty: Validus Re underwrites other lines of business depending on an evaluation of pricing and market conditions, which include aerospace and aviation, agriculture, financial lines of business, terrorism, life, accident & health, nuclear, workers’

compensation, crisis management, contingency, motor and technical lines. The Company seeks to underwrite other specialty lines with very limited exposure correlation with its property, marine and energy portfolios. With the exception of the aerospace line of business, which has a meaningful portion of its gross premiums written volume on a proportional basis, the Company’s other specialty lines are written on an excess of loss basis. Gross premiums written on specialty business during the year ended December 31, 2012 were $102.9 million.

AlphaCat: The AlphaCat segment manages strategic relationships that leverage the Company’s underwriting and investment expertise and earns management, performance and underwriting fees. AlphaCat Managers, Ltd. ("AlphaCat Managers"), formed in 2008, is a core element within the Validus Group strategic initiative to expand into capital market activities by participating in the market for Insurance Linked Securities ("ILS"). ILS are financial instruments whose fundamental value is determined by insurance losses caused by natural catastrophes such as major earthquakes and hurricanes. As the returns of ILS are primarily driven by natural catastrophes, when carefully structured, they are generally uncorrelated with the overall financial market, making ILS an attractive asset class for capital market investors.

AlphaCat helps investors take full advantage of this uncorrelated asset class through various funds and sidecars, accessing the market via AlphaCat Reinsurance Ltd., a Bermuda provider of fully collateralized property catastrophe reinsurance and retrocession capacity. AlphaCat invests in private reinsurance transactions, as well as catastrophe bonds, a common type of ILS issued by insurance and reinsurance companies. AlphaCat leverages the Validus Group’s extensive business sourcing, underwriting, research and analytic capabilities to construct ILS portfolios subject to prudent risk constraints.

During the first quarter of 2012, to better align the Company’s operating and reporting structure with its current strategy, there was a change in the Company's segment structure. This change included the AlphaCat group of companies as a separate operating segment. The AlphaCat segment was included as an additional segment and includes AlphaCat Re 2011, AlphaCat Re 2012, AlphaCat 2013, PaCRe and other affiliated investment funds. Prior period comparatives have been restated to reflect the change in segmentation.

Talbot: On July 2, 2007, the Company acquired all of the outstanding shares of Talbot. Talbot is the Bermuda parent of a specialty insurance group primarily operating within the Lloyd’s insurance market through Syndicate 1183. The acquisition of Talbot provided the Company with significant benefits in terms of product line and geographic diversification as well as offering the Company broader access to underwriting expertise. Similar to Validus Re, Talbot writes primarily short-tail lines of business but, as a complement to Validus Re, focuses mostly on insurance, as opposed to reinsurance risks, and on specialty lines where Validus Re currently has limited or no presence (e.g., war, financial institutions, contingency, accident and health). In addition, Talbot provides the Company with access to the Lloyd’s marketplace where Validus Re does not operate. As a London-based insurer, Talbot also writes the majority of its premiums on risks outside the United States. Talbot’s team of underwriters have, in many cases, spent most of their careers writing niche, short-tail business and bring their expertise to bear on expanding the Company’s short-tail insurance franchise.

The Company has expanded and diversified its business through Syndicate 1183’s access to Lloyd’s license agreements with regulators around the world. Talbot Underwriting Risk Services Ltd., Talbot Underwriting Services, (U.S.) Ltd., Talbot Underwriting (MENA) Ltd., Validus Reaseguros, Inc., Validus Re Chile S.A. and Talbot Risk Services Pte, Ltd., act as approved Lloyd’s coverholders for Syndicate 1183.

The following are the primary lines in which Talbot conducts its business. Details of gross premiums written by line of business are provided below:

|

| | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, 2012 | | Year Ended December 31, 2011 | | Year Ended December 31, 2010 |

| (Dollars in thousands) | | Gross Premiums Written | | Gross Premiums Written (%) | | Gross Premiums Written | | Gross Premiums Written (%) | | Gross Premiums Written | | Gross Premiums Written (%) |

| Property | | $ | 324,910 |

| | 30.2 | % | | $ | 306,317 |

| | 30.2 | % | | $ | 314,769 |

| | 32.1 | % |

| Marine | | 396,207 |

| | 36.7 | % | | 341,821 |

| | 33.7 | % | | 315,102 |

| | 32.1 | % |

| Specialty | | 357,519 |

| | 33.1 | % | | 365,984 |

| | 36.1 | % | | 351,202 |

| | 35.8 | % |

| Total | | $ | 1,078,636 |

| | 100.0 | % | | $ | 1,014,122 |

| | 100.0 | % | | $ | 981,073 |

| | 100.0 | % |

Property: The main sub-classes within property are international and North American direct and facultative contracts, onshore energy, lineslips and binding authorities together with a book of business written on a treaty reinsurance basis. The business written is mostly commercial and industrial insurance though there is a modest personal lines component. The business is short-tail with premiums for reinsurance and, direct and facultative business, substantially earned within 12 months and premiums for lineslips and binding authorities substantially earned within 12 months of the expiry of the contract. Gross premiums written on property business during the year ended December 31, 2012 were $324.9 million, including $86.3 million of treaty reinsurance.

Marine: The main types of business within marine are hull, cargo, energy, marine and energy liabilities, yachts and marinas and other treaty. Hull consists primarily of ocean going vessels and cargo and covers worldwide risks. Energy covers a variety of oil and gas industry risks. The marine and energy liability account provides cover for protection and indemnity clubs and a wide range of companies operating in the marine and energy sector. Each of the sub-classes within marine has a different profile of contracts written—some, such as energy, derive up to 36.1% of their business through writing facultative contracts while others, such as cargo, only derive 21.9% through this method. Each of the sub-classes also has a different geographical risk allocation. Most business written is short-tail enabling a quicker and more accurate picture of expected profitability than is the case for long-tail business. The marine and energy liability account, which makes up $60.3 million of the $396.2 million of gross premiums written during the year ended December 31, 2012, is the primary long-tail class in this line. The business written is mainly on a direct and facultative basis with a small element written on a reinsurance basis either as excess of loss reinsurance or proportional reinsurance.

Specialty: This class consists of war (comprising marine & aviation war, political risks and political violence, including war on land), financial institutions, contingency, bloodstock, accident and health, airlines and aviation treaty. With the exception of aviation treaty, most of the business written under the specialty accounts is written on a direct or facultative basis or under a binding authority through a coverholder. Gross premiums written on specialty business during the year ended December 31, 2012 were $357.5 million.

War: The marine & aviation war account covers physical damage to aircraft and marine vessels caused by acts of war and terrorism. The political risk account deals primarily with expropriation, contract frustration/trade credit, kidnap and ransom, and malicious and accidental product tamper. The political violence account mainly insures physical loss to property or goods anywhere in the world, caused by war, terrorism or civil unrest. This class is often written in conjunction with cargo, specie, property, energy, contingency and political risk. The period of the risks can extend up to 36 months and beyond. The attritional losses on the account are traditionally low but the account can be affected by large individual losses. Talbot is a market leader in the war and political violence classes. Gross premiums written on war business during the year ended December 31, 2012 were $184.7 million.

Financial Institutions: Talbot’s financial institutions team predominantly underwrites bankers blanket bond, professional indemnity and directors’ and officers’ coverage for various types of financial institutions and similar companies. Bankers blanket bond insurance products are specifically designed to protect against direct financial loss caused by fraud/criminal actions and mitigate the damage such activities may have on the asset base of the insured. Professional indemnity insurance protects businesses in the event that legal action is taken against them by third parties claiming professional negligence. Directors’ and officers’ insurance protects directors and officers against personal liability for losses incurred by a third party due to negligent performance by the director or officer. Gross premiums written on financial institutions business for the year ended December 31, 2012 were $35.8 million, comprising:

|

| | | | | | | |

| | | Year Ended December 31, 2012 |

| (Dollars in thousands) | | Gross Premiums Written | | Gross Premiums Written (%) |

| Bankers blanket bond | | $ | 20,933 |

| | 58.5 | % |

| Professional indemnity | | 12,887 |

| | 36.0 | % |

| Directors’ and Officers’ | | 1,986 |

| | 5.5 | % |

| Total | | $ | 35,806 |

| | 100.0 | % |

The risks covered in financial institutions are primarily fraud related and are principally written on an excess of loss basis. Talbot’s financial institutions account is concentrated on non-U.S. based clients, with 37.2% of gross premiums written in 2012 generated in Europe, 7.9% from the U.S. and 54.9% from other geographical regions. In addition, Talbot seeks to write regional accounts rather than global financial institutions with exposure in multiple jurisdictions and has only limited participation in exposures to publicly listed U.S. companies. As of December 31, 2012, the Company had gross reserves related to the financial institutions business of $157.9 million, comprised of $71.3 million, or 45.1% of incurred but not reported (“IBNR”) and $86.6 million, or 54.9% of case reserves. For comparison, as at December 31, 2011 the Company had gross reserves related to the financial institutions business of $176.7 million, comprising $69.5 million, or 39.4% of IBNR and $107.2 million, or 60.6% of case reserves. As of December 31, 2012, Talbot had minimal exposure to U.S. directors’ and officers’ risks.

Contingency: The main types of covers written under the contingency account are event cancellation and non-appearance business. Gross premiums written on contingency business during the year ended December 31, 2012 were $20.7 million.

Accident and Health: The accident and health account provides insurance in respect of individuals in both their personal and business activity together with corporations where they have an insurable interest relating to death or disability of employees

or those under contract. Gross premiums written on accident and health business during the year ended December 31, 2012 were $19.4 million.

Aviation: The aviation account insures major airlines, general aviation, aviation hull war and satellites. The coverage includes excess of loss treaties with medium to high attachment points. Gross premiums written on aviation business during the year ended December 31, 2012 were $95.7 million.

Enterprise Risk Management

The Company has implemented an Enterprise Risk Management (“ERM”) framework (the “Framework”) to identify, assess, quantify and manage risks and opportunities in order to protect our capital and maximize shareholder returns. This Framework is incorporated into the business activities of the Company and its strategic planning processes.

The Company’s Board of Directors has established a separate Risk Committee that is responsible for, among other things, approving the Company’s ERM Framework, working with management to ensure ongoing, effective implementation of the Framework and reviewing the Company’s specific risk limits as defined in the Framework, including limits for underwriting, investment, operational, business and other risks. The Company’s Chief Risk Officer prepares a quarterly presentation for the Risk Committee and communicates with the chairman of the Risk Committee on an informal basis periodically throughout the year.

The management committee of the Company that oversees risk management is the Group Risk Management Committee (“GRMC”). The GRMC is comprised of senior executives including among others; the Chief Executive Officer, Chief Financial Officer, Chief Risk Officer, Chief Actuary, Chief Operating Officer, Chief Executive Officer and Chief Risk Officer of Validus Re, Chief Executive Officer and Chief Risk Officer of Talbot and the Chief Executive Officer of Validus Research and AlphaCat.

To efficiently assess risks to the Company the GRMC has identified six key risk categories. Potential risks may span several or all of these key risk areas and as such risks are considered both within the context of these areas and the Company as a whole. The key risk areas are: Credit Risk, Market Risk, Liquidity Risk, Insurance Risk, Operational Risk and Group Risk.

Risk Appetite

The Group’s risk appetite sets a context within which all risks and opportunities are viewed. The risk appetite is proposed by management and approved by the Board of Directors, it represents the amount of risk the Company wants to take, within the constraints of capital resources, strategy, regulation and the rating agency environment.

Economic Capital Model

The Group uses economic capital modeling for capital adequacy assessment, risk-adjusted performance measurement and group-level and operating entity-level risk analysis.

Modeling

A pivotal factor in determining whether to found and fund the Company was the opportunity for differentiation based upon superior risk management expertise; specifically, managing catastrophe risk and optimizing our portfolio to generate attractive returns on capital while controlling our exposure to risk, and assembling a management team with the experience and expertise to do so. The Company’s proprietary models are current with emerging scientific trends. This has enabled the Company to gain a competitive advantage over those reinsurers who rely exclusively on commercial models for pricing and portfolio management. The Company has made a significant investment in expertise in the risk modeling area to capitalize on this opportunity. The Company has assembled an experienced group of professional experts who operate in an environment designed to allow them to use their expertise as a competitive advantage. While the Company uses both proprietary and commercial probabilistic models, catastrophe risk is ultimately subject to absolute aggregate limitations based on risk levels determined by the Risk Committee of the Board of Directors.

Vendor Models: The Company has global licenses for all three major commercial vendor models (RMS, AIR and EQECAT), to assess the adequacy of risk pricing and to monitor its overall exposure to risk in correlated geographic zones. Commencing in January 2012, the Company incorporated RMS version 11 into its vendor models. The Company models property exposures that could potentially lead to an over-aggregation of property risks (i.e., catastrophe-exposed business) using the vendor models. The vendor models enable the Company to aggregate exposures by correlated event loss scenarios, which are probability-weighted. This enables the generation of exceedance probability curves for the portfolio and major geographic areas. Once exposures are modeled using one of the vendor models, the other two models are used as a reasonability check and validation of the loss scenarios developed and reported by the first. The three commercial models each have unique strengths and weaknesses. For example, it is sometimes necessary to impose changes to frequency and severity ahead of changes made by the model vendors.

The Company’s review of market practice revealed a number of areas where quantitative expertise can be used to improve the reliability of the vendor model outputs:

| |

| • | Ceding companies may often report insufficient data and many reinsurers may not be sufficiently critical in their analysis of this data. The Company generally scrutinizes data for anomalies that may indicate insufficient data quality. These circumstances are addressed by either declining the program or, if the variances are manageable, by modifying the model output and pricing to reflect insufficient data quality; |

| |

| • | Prior to making overall adjustments for changes in climate variables, other variables are carefully examined (for example, demand surge, storm surge, and secondary uncertainty); and |

| |

| • | Pricing individual contracts frequently requires further adjustments to the three vendor models. Examples include bias in damage curves for commercial structures and occupancies and frequency of specific perils. |

In addition, many risks, such as second-event covers, aggregate excess of loss, or attritional loss components cannot be fully evaluated using the vendor models. In order to better evaluate and price these risks, the Company has developed proprietary analytical tools, such as VCAPS and other models and data sets.

Proprietary Models: In addition to making frequency and severity adjustments to the vendor model outputs, the Company has implemented a proprietary pricing and risk management tool, VCAPS, to assist in pricing submissions and monitoring risk aggregation.

To supplement the analysis performed using vendor models, VCAPS uses the gross loss output of catastrophe models to generate a 100,000-year simulation set, which is used for both pricing and risk management. This approach allows more precise measurement and pricing of exposures. The two primary benefits of this approach are:

| |

| • | VCAPS takes into account annual limits, event/franchise/annual aggregate deductibles, and reinstatement premiums. This allows for more accurate evaluation of treaties with a broad range of features, including both common (reinstatement premium and annual limits) and complex features (second or third event coverage, aggregate excess of loss, attritional loss components, covers with varying attachment across different geographical zones or lines of businesses and covers with complicated structures); and |

| |

| • | VCAPS use of 100,000-year simulations enables robust pricing of catastrophe-exposed business. This is possible in real-time operation because the Company has designed a computing hardware platform and software environment to accommodate the significant computing needs. |

In addition to VCAPS, the Company uses other proprietary models and other data in evaluating exposures. The Company cannot assure that the models and assumptions used by the software will accurately predict losses. Further, the Company cannot assure that the software is free of defects in the modeling logic or in the software code. In addition, the Company has not sought copyright or other legal protection for VCAPS.

Underwriting Risk Management

We underwrite and manage risk by paying close attention to risk selection and analysis. Through a detailed examination of contract terms, diversification criteria, contract experience and exposure, we aim to outperform our peers. We strive to provide our experienced underwriters with technically sound and objective information. We believe a strong working relationship between the underwriting, catastrophe modeling and actuarial disciplines is critical to long-term success and solid decision-making.

All of the Company’s underwriters are subject to a set of underwriting guidelines. At Validus Re, these guidelines are established by the Chief Executive Officer and approved by the Validus Re’s Board of Directors. At Talbot, the guidelines are established by executive management at Talbot and approved by their Board of Directors. These guidelines are then subject to review and approval by the Risk Committee of our Board of Directors. Underwriters are also issued letters of authority that specifically address the limits of their underwriting authority and their referral criteria. The Company’s current underwriting guidelines and letters of authority include:

| |

| • | lines of business that a particular underwriter is authorized to write; |

| |

| • | exposure limits by line of business; |

| |

| • | contractual exposures and limits requiring mandatory referrals to the Chief Executive Officer at Validus Re and the Chief Executive Officer at Talbot; and |

| |

| • | level of analysis to be performed by lines of business. |

In general, our underwriting approach is to:

| |

| • | seek high quality clients who have demonstrated superior performance over an extended period; |

| |

| • | evaluate our clients’ exposures and make adjustments where their exposure is not adequately reflected; |

| |

| • | apply the comprehensive knowledge and experience of our entire underwriting team to make progressive and cohesive decisions about the business they underwrite; |

| |

| • | employ our well-founded and carefully maintained market contacts within the group to enhance our robust distribution capabilities; and |

| |

| • | refer submissions to the Chief Underwriting Officer at Validus Re, the Chief Executive Officer at Talbot, Chief Executive Officer at Validus Re and the Risk Committee of our Board of Directors according to our underwriting guidelines. |

The underwriting guidelines are subject to waiver or change by the Chief Executive Officer at Validus Re or the Chief Executive Officer at Talbot subject to their authority as overseen by their respective Risk Committees.

Our underwriters have the responsibility to analyze all submissions and determine if the related potential exposures meet with both the Company’s risk profile line size and aggregate limitations, in line with the business plan. In order to ensure compliance, we run appropriate management information reports and all lines are subject to fully approved regulatory audits. Further, our treaty reinsurance operation has the authority limits of individual underwriters built into VCAPS while Talbot maintains separate compliance procedures to ensure that the appropriate policies and guidelines are followed.

Validus Re: Validus Re has established a referral process whereby business exceeding set exposure or premium limits is referred to the Chief Executive Officer for review. As the reviewer of such potential business, the Chief Executive Officer has the ability to determine if the business meets the Company’s overall desired risk profile. The Chief Executive Officer has defined underwriting authority for each underwriter, and risks outside of this authority must be referred to the Company’s Chief Executive Officer.

The Risk Committee of our Board of Directors reviews business that is outside the authority of the Chief Executive Officer.

AlphaCat: All of the investment companies managed by AlphaCat are subject to investment or underwriting guidelines. These guidelines are established in the offering documentation of the respective investment company. The AlphaCat management team manages investment portfolios in accordance with the guidelines, which are subject to oversight by the respective investment company's Board of Directors. AlphaCat leverages the Company's underwriting and analytical resources. However, all investment decisions are ultimately made by the AlphaCat management team. When services are provided to AlphaCat by the Company's underwriting teams, the applicable underwriting risk management framework outlined in this section applies.

Talbot: Talbot's risk review and control processes have been designed to ensure that all written risks comply with underwriting and risk control strategies. The workflow system is designed to automate the referral of risks to the relevant reviewer who has an appropriate level of authority to review the risk. These reviews are documented, monitored and reports are prepared on a regular basis.

Collectively, the various peer review procedures serve numerous objectives, including:

| |

| • | Validating that underwriting decisions are in accordance with risk appetite, authorities, agreed business plans and standards for type, quality and profitability of risk; |

| |

| • | Providing an experienced and suitably qualified second review of individual risks; |

| |

| • | Ensuring that risks identified as significant undergo the highest level of technical underwriting review; |

| |

| • | Elevating technical underwriting queries and/or need for remedial actions on a timely basis; and |

| |

| • | Improving data accuracy and coding for subsequent management reporting. |

The principal elements of the underwriting review process are as follows:

Underwriter review: The underwriting team must evidence data entry review by confirming review and agreement on the workflow system within a specified number of working days of entry being completed by the contracted third party.

Risk - based peer review: The majority of risks are peer reviewed by another underwriter within a specified number of working days of data entry being completed. There is an agreed matrix of underwriters authorized to peer review.

Class of business review: Risks written into a class by an underwriter other than the nominated class underwriter are subsequently forwarded to, and reviewed by, the nominated class underwriter.

Exceptions review: Risks that exceed a set of pre-determined criteria will also be referred to the Active Underwriter or the Director of Underwriting and Operations for review. Such risks are discussed by the underwriters at regular underwriting meetings in the presence of at least one of the above. In certain circumstances, some risks may be referred to the Insurance Management Committee or the Talbot Underwriting Ltd. (“TUL”) Board for final approval. These reviews also commonly include reports of risks renewed where there has been a large loss ratio in the recent past.

Insurance Management Committee: At its regular meetings, the Committee reviews a range of key performance indicators including: premium income written versus budget; movements in syndicate cash and investments; aggregate exposures; together with other highlighted exception reports. The Committee also reviews claim movements over a financial threshold.

Expert Review Committee (“ERC”): The ERC is a committee that meets regularly to review the underwriting activities of Syndicate 1183 and other related activities to provide assurance that the underwriting risks assumed are within the parameters of the business plan. This is achieved with the help of eight external expert reviewers who report their findings to the ERC.

The expert reviewers obtain and review a sample of risks underwritten in each class and report their findings to the quarterly meetings of the ERC. Findings range from general comments on approach and processes to specific points in respect of individual risks.

Within Talbot, the TUL Board is responsible for creating the environment and structures for risk management to operate effectively. The Talbot Chief Executive is responsible for ensuring the risk management process is implemented.

The TUL Board has several committees responsible for monitoring risk. The TUL Board approves the risk appetite as part of the syndicate business plan process which sets targets for premium volume, pricing, line sizes, aggregate exposures and retention by class of business.

The TUL Executive Committee is responsible for establishing and maintaining a comprehensive risk register and key controls for TUL. It is responsible for articulating Talbot's risk appetite for approval by the TUL Board.

The key focuses of each committee are as follows:

| |

| • | The TUL Executive Committee oversees the management of key risks with regard to strategy and reserves; |

| |

| • | The Insurance Management Committee oversees the management of insurance risks; |

| |

| • | The Operational Risk Committee oversees the management of risks related to people, processes, systems and external events; and |

| |

| • | The Financial Risk Committee oversees the management of credit risks associated with reinsurers, brokers, coverholders and investments, market risk and liquidity risk. |

Performance against underwriting targets is measured regularly throughout the year. Risks written are subject to peer review, an internal quality control process. Pricing is controlled by the monitoring of rate movements and the comparison of technical prices to actual prices. Controls over aggregation of claims exposures vary by class of business. They include limiting coastal risks, monitoring aggregation by county/region/blast zones and applying line size limits in all cases. Catastrophe modeling software and techniques are used to model expected loss outcomes for Lloyd’s Realistic Disaster Scenario returns and in-house catastrophe event scenarios. Reserves are reviewed for adequacy on a quarterly basis. The syndicate also purchases reinsurance, with an appropriate number of reinstatements, to arrive at an acceptable net retained risk.

Program Limits

Overall exposure to risk is controlled by limiting the amount of insurance or reinsurance underwritten in a particular program or contract. This helps to diversify risk within and across risk zones. The Risk Committee sets these limits, which may be exceeded only with its approval.

Geographic Diversification

The Company actively manages its aggregate exposures by geographic or risk zone (“zones”) to maintain a balanced and diverse portfolio of underlying risks. The coverage the Company is willing to provide for any risk located in a particular zone is limited to a predetermined level, thus limiting the net aggregate loss exposure from all contracts covering risks believed to be located in any zone. Contracts that have “worldwide” territorial limits have exposures in several geographic zones. Generally, if a proposed reinsurance program would cause the limit to be exceeded, the program would be declined, regardless of its desirability,

unless the Company buys retrocessional coverage, thereby reducing the net aggregate exposure to the maximum limit permitted or less. The following table summarizes our gross premiums written by geographic zone:

|

| | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, 2012 |

| | Gross Premiums Written |

| | Validus Re | | AlphaCat | | Talbot | | Corporate and Eliminations | | Total | | % |

| United States | $ | 468,730 |

| | $ | 18,774 |

| | $ | 120,086 |

| | $ | (7,285 | ) | | $ | 600,305 |

| | 27.7 | % |

| Worldwide excluding United States (a) | 40,168 |

| | — |

| | 263,597 |

| | (16,049 | ) | | 287,716 |

| | 13.3 | % |

| Europe | 90,673 |

| | 1,333 |

| | 50,262 |

| | (2,868 | ) | | 139,400 |

| | 6.4 | % |

| Latin America and Caribbean | 33,031 |

| | — |

| | 103,543 |

| | (6,164 | ) | | 130,410 |

| | 6.0 | % |

| Japan | 30,781 |

| | — |

| | 6,630 |

| | (396 | ) | | 37,015 |

| | 1.7 | % |

| Canada | 688 |

| | — |

| | 12,243 |

| | (690 | ) | | 12,241 |

| | 0.6 | % |

| Rest of the world (b) | 68,754 |

| | 496 |

| | — |

| | — |

| | 69,250 |

| | 3.2 | % |

| Sub-total, non United States | 264,095 |

| | 1,829 |

| | 436,275 |

| | (26,167 | ) | | 676,032 |

| | 31.2 | % |

| Worldwide including United States | 101,594 |

| | 1,000 |

| | 65,084 |

| | (3,552 | ) | | 164,126 |

| | 7.6 | % |

| Marine and Aerospace (c) | 297,540 |

| | — |

| | 457,191 |

| | (28,754 | ) | | 725,977 |

| | 33.5 | % |

| Total | $ | 1,131,959 |

| | $ | 21,603 |

| | $ | 1,078,636 |

| | $ | (65,758 | ) | | $ | 2,166,440 |

| | 100.0 | % |

| |

| (a) | Represents risks in two or more geographic zones. |

| |

| (b) | Represents risk in one geographic zone. |

| |

| (c) | Not classified by geographic area as marine and aerospace risks can span multiple geographic areas and are not fixed locations in some instances. |

The effectiveness of geographic zone limits in managing risk exposure depends on the degree to which an actual event is confined to the zone in question and on the Company’s ability to determine the actual location of the risks believed to be covered under a particular insurance or reinsurance program. Accordingly, there can be no assurance that risk exposure in any particular zone will not exceed that zone’s limits. Further control over diversification is achieved through guidelines covering the types and amount of business written in product classes and lines within a class.

Reinsurance Management

Validus Re Retrocession: Validus Re monitors the opportunity to purchase retrocessional coverage on a continual basis and employs the VCAPS modeling system to evaluate the effectiveness of risk mitigation and exposure management relative to the cost. This coverage may be purchased on an indemnity basis as well as on an index basis (e.g., industry loss warranties (“ILWs”)). Validus Re also considers alternative retrocessional structures, including collateralized quota share (“sidecar”) and other capital markets products.

When Validus Re buys retrocessional coverage on an indemnity basis, payment is for an agreed upon portion of the losses actually suffered. In contrast, when Validus Re buys an ILW cover, which is a reinsurance contract in which the payout is dependent on both the insured loss of the policy purchaser and the measure of the industry-wide loss, payment is made only if both Validus Re and the industry suffer a loss, as reported by one of a number of independent agencies, in excess of specified threshold amounts. With an ILW, Validus Re bears the risk of suffering a loss while receiving no payment under the ILW if the industry loss was less than the specified threshold amount.

Validus Re may use capital markets instruments for risk management in the future (e.g., catastrophe bonds, sidecar facilities and other forms of risk securitization) where the pricing and terms are attractive.

AlphaCat: AlphaCat currently does not cede any premiums to third parties.

Talbot Ceded Reinsurance: Talbot enters into reinsurance agreements in order to mitigate its accumulation of loss, reduce its liability on individual risks and enable it to underwrite policies with higher limits. The ceding of the insurance does not legally discharge Talbot from its primary liability for the full amount of the policies, and Talbot is required to pay the loss and bear collection risk if the reinsurer fails to meet its obligations under the reinsurance agreement.

The following describes the Talbot Group’s process in the purchase and authorization of treaty reinsurance policies only. It does not cover the purchase of facultative reinsurance because these premiums are not significant.

The reinsurance program is reviewed by the reinsurance purchasing team on an on-going basis in line with the main business planning process. This process incorporates advice and analytical work from our brokers, actuarial and capital modeling teams.

The review and modification is based upon the following:

| |

| • | budgeted underwriting for the coming year; |

| |

| • | loss experience from prior years; |

| |

| • | loss information from the coming year’s individual capital assessment calculations; |

| |

| • | changes to risk limits and aggregation limits expected and any other changes to Talbot’s risk tolerance; |

| |

| • | changes to capital requirements; and |

| |

| • | Realistic Disaster Scenarios (“RDSs”) prescribed by Lloyd’s. |

The main type of reinsurance purchased is losses occurring; however, for a few lines of business, where the timing of the loss event is less easily verified or where such cover is available, risk attaching policies are purchased.

The type, quantity and cost of cover of the proposed reinsurance program is discussed and reviewed by the Chief Executive Officer of the Talbot group, and ultimately authorized by the TUL Board.

Once this has occurred, the reinsurance program is purchased in the months prior to the beginning of the covered period. All reinsurance contracts arranged are authorized for purchase by the Director of Underwriting and Operations. Slips are developed prior to inception to ensure that optimum cover is achieved. After purchase, cover notes are reviewed by the relevant class underwriters and presentations made to all underwriting staff to ensure they are aware of the boundaries of the cover.

Distribution

Although we conduct some business on a direct basis with our treaty and facultative reinsurance clients, most of our business is derived through insurance and reinsurance intermediaries (“brokers”), who access business from clients and coverholders. We are able to attract business through our recognized lead capability in most classes we underwrite, particularly in classes where such lead ability is rare.

Currently, our largest broker relationships, as measured by gross premiums written, are with Marsh & McLennan, Aon Benfield Group Ltd. and Willis Group Holdings Ltd. The following table sets forth the Company’s gross premiums written by broker:

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, 2012 |

| | | Gross Premiums Written |

| (Dollars in thousands) | | Validus Re | | AlphaCat | | Talbot | | Corporate and Eliminations | | Total | | % |

| Name of Broker | | | | | | | | | | | | |

| Marsh & McLennan | | $ | 399,325 |

| | $ | 7,426 |

| | $ | 244,776 |

| | $ | (14,809 | ) | | $ | 636,718 |

| | 29.4 | % |

| Aon Benfield Group Ltd. | | 400,018 |

| | 6,133 |

| | 180,234 |

| | (10,904 | ) | | 575,481 |

| | 26.5 | % |

| Willis Group Holdings Ltd. | | 187,353 |

| | 3,418 |

| | 167,249 |

| | (10,119 | ) | | 347,901 |

| | 16.1 | % |

| Sub-total | | 986,696 |

| | 16,977 |

| | 592,259 |

| | (35,832 | ) | | 1,560,100 |

| | 72.0 | % |

| All Others/Direct | | 145,263 |

| | 4,626 |

| | 486,377 |

| | (29,926 | ) | | 606,340 |

| | 28.0 | % |

| Total | | $ | 1,131,959 |

| | $ | 21,603 |

| | $ | 1,078,636 |

| | $ | (65,758 | ) | | $ | 2,166,440 |

| | 100.0 | % |

Reserve for losses and loss expenses

For insurance and reinsurance companies, a significant judgment made by management is the estimation of the reserve for losses and loss expenses. The Company establishes its reserve for losses and loss expenses to cover the estimated incurred liability for both reported and unreported claims.

The following tables show certain information with respect to the Company’s gross and net reserves:

|

| | | | | | | | | | | | |

| | | As at December 31, 2012 |

| (Dollars in thousands) | | Gross Case Reserves | | Gross IBNR | | Total Gross Reserve for Losses and Loss Expenses |

| Property | | $ | 930,553 |

| | $ | 892,227 |

| | $ | 1,822,780 |

|

| Marine | | 522,907 |

| | 477,948 |

| | 1,000,855 |

|

| Specialty | | 265,638 |

| | 428,300 |

| | 693,938 |

|

| Total | | $ | 1,719,098 |

| | $ | 1,798,475 |

| | $ | 3,517,573 |

|

|

| | | | | | | | | | | | |

| | | As at December 31, 2012 |

| (Dollars in thousands) | | Net Case Reserves | | Net IBNR | | Total Net Reserve for Losses and Loss Expenses |

| Property | | $ | 768,722 |

| | $ | 803,182 |

| | $ | 1,571,904 |

|

| Marine | | 465,080 |

| | 438,009 |

| | 903,089 |

|

| Specialty | | 230,584 |

| | 372,029 |

| | 602,613 |

|

| Total | | $ | 1,464,386 |

| | $ | 1,613,220 |

| | $ | 3,077,606 |

|

Loss reserves are established due to the significant periods of time that may lapse between the occurrence, reporting and payment of a loss. To recognize liabilities for unpaid losses and loss expenses, the Company estimates future amounts needed to pay claims and related expenses with respect to insured events. The Company’s reserving practices and the establishment of any particular reserve reflects management’s judgment concerning sound financial practice and does not represent any admission of liability with respect to any claim. Unpaid losses and loss expense reserves are established for reported claims (“case reserves”) and IBNR claims.

The nature of the Company’s high excess of loss liability and catastrophe business can result in loss payments that are both irregular and significant. Such loss payments are part of the normal course of business for the Company. Adjustments to reserves for individual years can also be irregular and significant. Conditions and trends that have affected development of liabilities in the past may not necessarily occur in the future. Accordingly, it is inappropriate to extrapolate future redundancies or deficiencies based upon historical experience. See Part I, Item 1A, “Risk Factors” and Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cautionary Note Regarding Forward-Looking Statements.”

The tables below present the development of the Company’s unpaid losses and loss expense reserves on both a net and gross basis. The cumulative redundancy (deficiency) calculated on a net basis differs from that calculated on a gross basis. As different reinsurance programs cover different underwriting years, net and gross loss experience will not develop proportionately. The top line of the tables shows the estimated liability, net and gross of reinsurance recoveries, as at the year end balance sheet date for each of the indicated years. This represents the estimated amounts of losses and loss expenses, including IBNR, arising in the current and all prior years that are unpaid at the year end balance sheet date of the indicated year. The tables also show the re-estimated amount of the previously recorded reserve liability based on experience as of the year end balance sheet date of each succeeding year. The estimate changes as more information becomes known about the frequency and severity of claims for individual years. The cumulative redundancy (deficiency) represents the aggregate change with respect to that liability originally estimated. The lower portion of each table also reflects the cumulative paid losses relating to these reserves. Conditions and trends that have affected development of liabilities in the past may not necessarily occur in the future. Accordingly, it is not appropriate to extrapolate redundancies or deficiencies into the future, based on the tables below. See Part I, Item 1A, “Risk Factors” and Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cautionary Note Regarding Forward-Looking Statements.”

Analysis of Losses and Loss Expense Reserve Development Net of Recoveries

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Years Ended December 31, |

| (Dollars in thousands) | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 (b) |

| Estimated liability for unpaid losses and loss expense, net of reinsurance recoverable | | $ | 77,363 |

| | $ | 791,713 |

| | $ | 1,096,507 |

| | $ | 1,440,369 |

| | $ | 1,752,839 |

| | $ | 2,258,658 |

| | $ | 3,077,606 |

|

| Liability—estimated as of: | | | | | | | | | | | | | | |

| One year later | | 60,106 |

| | 722,010 |

| | 1,018,930 |

| | 1,283,759 |

| | 1,596,720 |

| | 2,083,378 |

| | |

| Two years later | | 54,302 |

| | 670,069 |

| | 937,696 |

| | 1,181,987 |

| | 1,451,448 |

| | | | |

| Three years later | | 50,149 |

| | 606,387 |

| | 902,161 |

| | 1,085,664 |

| | | | | | |

| Four years later | | 46,851 |

| | 584,588 |

| | 847,935 |

| | | | | | | | |

| Five years later | | 45,946 |

| | 547,965 |

| | | | | | | | | | |

| Six years later | | 45,199 |

| | | | | | | | | | | | |

| Cumulative redundancy (deficiency)(a) | | 32,164 |

| | 243,748 |

| | 248,572 |

| | 354,705 |

| | 301,391 |

| | 175,280 |

| | |

| Cumulative paid losses, net of reinsurance recoveries, as of: | | | | | | | | | | | | | | |

| One year later | | $ | 27,180 |

| | $ | 216,469 |

| | $ | 353,476 |

| | $ | 384,828 |

| | $ | 476,779 |

| | $ | 631,889 |

| | |

| Two years later | | 34,935 |

| | 320,803 |

| | 562,831 |

| | 634,041 |

| | 741,940 |

| | | | |

| Three years later | | 39,520 |

| | 350,521 |

| | 662,319 |

| | 744,324 |

| | | | | | |

| Four years later | | 41,746 |

| | 374,788 |

| | 722,652 |

| | | | | | | | |

| Five years later | | 41,901 |

| | 390,895 |

| | | | | | | | | | |

| Six years later | | 43,571 |

| | | | | | | | | | | | |

| |

| (a) | See Part II Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further discussion. |

| |

| (b) | The reserves for losses and loss expenses or Flagstone are consolidated only from the November 30, 2012 date of acquisition. |

Analysis of Losses and Loss Expense Reserve Development Gross of Recoveries

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Years Ended December 31, |

| (Dollars in thousands) | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 (b) |

| Estimated gross liability for unpaid losses and loss expense | | $ | 77,363 |

| | $ | 926,117 |

| | $ | 1,305,303 |

| | $ | 1,622,134 |

| | $ | 2,035,973 |

| | $ | 2,631,143 |

| | $ | 3,517,573 |

|

| Liability—estimated as of: | | | | | | | | | | | | | | |

| One year later | | 60,106 |

| | 846,863 |

| | 1,223,018 |

| | 1,484,646 |

| | 1,854,565 |

| | 2,422,343 |

| | |

| Two years later | | 54,302 |

| | 791,438 |

| | 1,164,923 |

| | 1,385,533 |

| | 1,705,995 |

| | | | |

| Three years later | | 50,149 |

| | 745,624 |

| | 1,134,043 |

| | 1,288,915 |

| | | | | | |

| Four years later | | 46,851 |

| | 721,730 |

| | 1,079,842 |

| | | | | | | | |

| Five years later | | 45,946 |

| | 675,884 |

| | | | | | | | | | |

| Six years later | | 46,104 |

| | | | | | | | | | | | |

| Cumulative redundancy (deficiency)(a) | | 31,259 |

| | 250,233 |

| | 225,461 |

| | 333,219 |

| | 329,978 |

| | 208,800 |

| | |

| Cumulative paid losses, gross of reinsurance recoveries, as of: | | | | | | | | | | | | | | |

| One year later | | $ | 27,180 |

| | $ | 245,240 |

| | $ | 437,210 |

| | $ | 455,182 |

| | $ | 557,894 |

| | $ | 807,296 |

| | |

| Two years later | | 34,935 |

| | 394,685 |

| | 706,249 |

| | 709,309 |

| | 878,406 |

| | | | |

| Three years later | | 39,520 |

| | 452,559 |

| | 825,159 |

| | 864,918 |

| | | | | | |

| Four years later | | 41,746 |

| | 480,277 |

| | 898,338 |

| | | | | | | | |

| Five years later | | 41,901 |

| | 496,511 |

| | | | | | | | | | |

| Six years later | | 43,571 |

| | | | | | | | | | | | |

| |

| (a) | See Part II Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further discussion. |

| |

| (b) | The reserves for losses and loss expenses or Flagstone are consolidated only from the November 30, 2012 date of acquisition. |

The following table presents an analysis of the Company’s paid, unpaid and incurred losses and loss expenses and a reconciliation of beginning and ending unpaid losses and loss expenses for the years indicated:

|

| | | | | | | | | | | | |

| | | Years Ended December 31, |

| (Dollars in thousands) | | 2012 | | 2011 | | 2010 |

| Reserve for losses and loss expenses, beginning of year | | $ | 2,631,143 |

| | $ | 2,035,973 |

| | $ | 1,622,134 |

|

| Losses and loss expenses recoverable | | (372,485 | ) | | (283,134 | ) | | (181,765 | ) |

| Net reserves for losses and loss expenses, beginning of year | | 2,258,658 |

| | 1,752,839 |

| | 1,440,369 |

|

| Net loss reserves acquired in Flagstone acquisition | | 639,641 |

| | — |

| | — |

|

| Increase (decrease) in net losses and loss expenses incurred in respect of losses occurring in: | | | | | | |

| Current year | | 1,174,415 |

| | 1,400,520 |

| | 1,144,196 |

|

| Prior years | | (174,969 | ) | | (156,119 | ) | | (156,610 | ) |

| Total incurred losses and loss expenses | | 999,446 |

| | 1,244,401 |

| | 987,586 |

|

| Less net losses and loss expenses paid in respect of losses occurring in: | | | | | | |

| Current year | | (182,146 | ) | | (266,247 | ) | | (288,594 | ) |

| Prior years | | (653,874 | ) | | (476,779 | ) | | (384,828 | ) |

| Total net paid losses | | (836,020 | ) | | (743,026 | ) | | (673,422 | ) |

| Foreign exchange | | 15,881 |

| | 4,444 |

| | (1,694 | ) |

| Net reserve for losses and loss expenses, end of year | | 3,077,606 |

| | 2,258,658 |

| | 1,752,839 |

|

| Losses and loss expenses recoverable | | 439,967 |

| | 372,485 |

| | 283,134 |

|

| Reserve for losses and loss expenses, end of year | | $ | 3,517,573 |

| | $ | 2,631,143 |

| | $ | 2,035,973 |

|

Validus Re and AlphaCat: Validus Re and AlphaCat’s loss reserves are established based upon an estimate of the total cost of claims that have been incurred, including estimates of unpaid liability on known individual claims, the costs of additional case reserves on claims reported but not considered to be adequately reserved in such reporting (“ACRs”) and amounts that have been incurred but not yet reported. ACRs are used in certain cases and may be calculated based on management’s estimate of the required case reserve on an individual claim less the case reserves reported by the client. The Validus Re Loss Reserve Committee follows material catastrophe event ultimate loss reserve estimation procedures for the investigation, analysis, estimation and approval of ultimate loss reserving resulting from any material catastrophe event. U.S. GAAP does not permit the establishment of loss reserves until an event occurs that gives rise to a loss.

For reported losses, Validus Re and AlphaCat establish case reserves within the parameters of the coverage provided in the impacted reinsurance contracts. Where there is a reported claim for which the reported case reserve is determined to be insufficient, Validus Re and AlphaCat may book an ACR or individual claim IBNR estimate that is adjusted as claims notifications are received. Information may be obtained from various sources including brokers, proprietary and third party vendor models and internal data regarding reinsured exposures related to the geographic location of the event, as well as other sources. Validus Re and AlphaCat use generally accepted actuarial techniques in its IBNR estimation process. Validus Re and AlphaCat also use historical insurance industry loss emergence patterns, as well as estimates of future trends in claims severity, frequency and other factors, to aid it in establishing loss reserves.

Loss reserves represent estimates, including actuarial and statistical projections at a given point in time, of the expectations of the ultimate settlement and administration costs of claims incurred. Such estimates are not precise in that, among other things, they are based on predictions of future developments and estimates of future trends in loss severity and frequency and other variable factors such as inflation, litigation and tort reform. This uncertainty is heightened by the short time in which Validus Re has operated, thereby providing limited claims loss emergence patterns that directly pertain to Validus Re’s operations. This has necessitated the use of industry loss emergence patterns in deriving IBNR, which despite management’s and our actuaries’ care in selecting them, will differ from actual experience. Further, expected losses and loss ratios are typically developed using vendor and proprietary computer models and these expected losses and loss ratios are a significant component in the calculation deriving IBNR. Finally, the uncertainty surrounding estimated costs is greater in cases where large, unique events have been reported and the associated claims are in early stages of resolution. As a result of these uncertainties, it is likely that the ultimate liability will differ from such estimates, perhaps materially.

For disclosure purposes, only those loss events which aggregate to over $15.0 million on a consolidated basis ("notable losses") are disclosed separately and included in the reserve for notable loss events and reserve for development on events tables. Notable loss events are first determined at the respective operating segments based on segment thresholds and are then aggregated and disclosed if it is determined that they reach the consolidated threshold for notable loss disclosure.

During 2010 and 2011, given the complexity and severity of notable loss events in the year, an explicit reserve for potential development on 2010 and 2011 notable loss events ("RDE") was included within the Company’s IBNR reserving process. As uncertainties surrounding initial estimates on notable loss events have developed, this reserve has been and will continue to be allocated to specific notable loss events. No RDE was established for 2012 notable losses.

The requirement for a reserve for potential development on notable loss events in a quarter is a function of (a) the number of significant events occurring in that quarter and (b) the complexity and volatility of those events. Complexity and volatility factors considered are as follows:

• Contract complexity;

• Nature and number of perils arising from an event;

• Limits and sub limits exposed;

• Quality, timing and flow of information received from each loss;

• Timing of receipt of information to the Company;

• Information regarding retrocessional covers;

• Assumptions, both explicit and implicit, regarding future paid and reported loss development patterns;

• Frequency and severity trends;

• Claims settlement practices; and

• Potential changes in the legal environment.

Each of these factors may lead to associated volatility for each notable loss event as well as consideration of the total reserve for loss events in the aggregate. Consequently, all of these factors are considered in the aggregate for the events occurring in the quarter, recognizing that it is more likely that one or some of the events may deteriorate significantly, rather than all deteriorating proportionately. The establishment of each quarter’s requirement for a reserve for potential development on notable loss events takes place as part of the quarterly evaluation of the Company’s overall reserve requirements. It is not directly linked in isolation to any one significant/notable loss in the quarter. The reserve for potential development on notable loss events is evaluated by our in-house actuaries as part of their normal process in setting of indicated reserves for the quarter. In ensuing quarters senior management and the in-house actuaries revisit and re-estimate certain events previously considered in the catastrophe loss event process as well as events that have subsequently emerged in the current quarter. To the extent that there has been adverse development on a notable loss event, if there is RDE remaining from that accident year, an allocation from the respective accident year RDE will be made to the notable loss event. If there is no remaining RDE relating to the accident year of the loss, then adverse development will be recorded for the notable loss event through the Statements of Comprehensive Income.

Changes to the reserve for potential development on notable loss events will be considered in light of changes to previous loss estimates from notable losses in this re-estimation process.To the extent that there are continued complexity and volatility factors relating to notable loss events in the aggregate, additions to the RDE may be established for a specific accident year, as illustrated in the RDE roll forward table which can be found in Item. 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations."

Loss reserves are reviewed regularly and adjustments to reserves, if any, will be recorded in earnings in the period in which they are determined. Even after such adjustments, the ultimate liability may exceed or be less than the revised estimates.

Talbot: Talbot’s loss reserves are established based upon an estimate of the total cost of claims that have been incurred, including case reserves and IBNR. Talbot uses generally accepted actuarial techniques in its IBNR estimation process. ACRs are not generally used.

Talbot performs internal assessments of liabilities on a quarterly basis. Talbot’s loss reserving process involves the assessment of actuarial estimates of gross ultimate losses on both an ultimate basis (i.e., ignoring the period during which premium earns) and an earned basis, split by underwriting year and class of business, and generally also between attritional, large and catastrophe losses. These estimates are made using a variety of generally accepted actuarial projection methodologies, as well as additional qualitative consideration of future trends in frequency, severity and other factors. The gross estimates are used to estimate ceded reinsurance recoveries, which are in turn used to calculate net ultimate losses as the difference between gross and ceded. These figures are subsequently used by Talbot’s management to help it assess its best estimate of gross and net ultimate losses.

As with Validus Re and AlphaCat, Talbot’s loss reserves represent estimates, including actuarial and statistical projections at a given point in time, of the expectations of the ultimate settlement and administration costs of claims incurred. Such estimates are not precise in that, among other things, they are based on predictions of future developments and estimates of future trends in loss severity and frequency and other variable factors such as inflation, litigation and tort reform. The uncertainty surrounding estimated costs is also greater in cases where large, unique events have been reported and the associated claims are in the early stages of resolution. As a result of these uncertainties, it is likely that the ultimate liability will differ from such estimates, perhaps materially.

Talbot’s loss reserves are reviewed regularly and adjustments to reserves, if any, will be recorded in earnings in the period in which they are determined. Even after such adjustments, the ultimate liability may exceed or be less than the revised estimates. See Part I, Item 1A, “Risk Factors” and Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cautionary Note Regarding Forward-Looking Statements.”

Investment Management