Filed by Penn West Energy Trust

This communication is filed pursuant to Rule 425

under the Securities Act of 1933, as amended

Subject Company: Canetic Resources Trust

Commission File No.: 1-32728

Date: November 5, 2007

| [GRAPHIC] |

| Certain information regarding Penn West Energy Trust (“Penn West”) and Canetic Resources Trust (“Canetic”) and the transactions reviewed in this presentation including management’s assessment of future plans and operations, may constitute forward-looking statements under applicable securities law and necessarily involve risks, including, without limitation, risks associated with oil and gas exploration, development, exploitation, production, marketing and transportation, loss of markets, volatility of commodity prices, currency fluctuations, imprecision of reserve estimates, environmental risks, competition, incorrect assessment of the value of acquisitions, failure to realize the anticipated benefits of acquisitions and ability to access sufficient capital from internal and external sources; failure to obtain required regulatory approvals; including stock exchange listing approvals. As a consequence, actual results may differ materially from those anticipated in the forward-looking statements. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on these and other factors that could affect Penn West or Canetic’s operations or financial results are included in reports on file with Canadian securities regulatory authorities and may be accessed through the SEDAR website (www.sedar.com), at Penn West’s website (www.pennwest.com) or at Canetic’s website (www.canetictrust.com). Furthermore, the forward-looking statements contained in this presentation are made as of the date of this presentation, Neither Penn West nor Canetic undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be expressly required by applicable securities law. Where reserves or production are stated on a barrel of oil equivalent (BOE) basis, natural gas volumes have been converted to a barrel of oil equivalent (BOE) at a ratio of six thousand cubic feet of natural gas to one barrel of oil. This conversion ratio is based upon an energy equivalent conversion method primarily applicable at the burner tip and does not represent value equivalence at the wellhead. BOEs may be misleading, particularly if used in isolation. This presentation may contain references to non-GAAP terms. Penn West and Canetic use these measures to help evaluate their respective performance. These measures as presented do not have any standardized meaning prescribed by Canadian GAAP and therefore, they may not be comparable with calculations of similar measures for other companies or trusts. All references are to Canadian Dollars unless otherwise specified. IMPORTANT ADDITIONAL INFORMATION WILL BE FILED WITH THE SEC In connection with the proposed transaction, Penn West intends to, if required, file relevant materials with the Securities and Exchange Commission (the “SEC”) on a Registration Statement on Form F-10 (the “Registration Statement”) to register the Penn West Units (the “Units”) to be issued in connection with the proposed transaction. Investors and unitholders are urged to read the Registration Statement and any other relevant documents to be filed with the SEC when available because they will contain important information about Penn West and Canetic, the transaction and related matters. Investors and unitholders will be able to obtain free copies of the Registration Statement and other documents filed with the SEC by Penn West through the website maintained by the SEC at www.sec.gov. In addition, investors and unitholders will be able to obtain free copies of the Registration Statement and such other documents when they become available from Penn West by contacting Penn West Investor Relations at investor_relations@pennwest.com or by telephone at 1-888-770-2633. Advisory |

| Strategic Combination Creates $15 billion flagship energy trust Dominant light oil producer in Western Canada Significant portfolio of unconventional opportunities Scale will allow meaningful expansion both domestically and outside Canada Increased liquidity and enhanced financial strength Strong management team drawn from the combination DEAL RATIONALE |

| Strategic Combination On October 31, 2007, Penn West and Canetic announced a strategic business combination Exchange ratio of 0.515 units of Penn West for each Canetic unit (7.1% premium to Oct. 30 close, including special dist.) One-time special distribution of $0.09 CDN paid to Canetic unitholders on closing to equalize distributions for first six months following combination Initial Penn West distribution will be $0.34 CDN per unit per month The Combined Trust will continue to operate as Penn West Energy Trust and trade on the TSX (PWT.UN) and on the NYSE (PWE) TRANSACTION DETAILS |

| Strategic Combination Unanimous approval of Boards of Directors of Penn West and Canetic and resolution to recommend to unitholders Fairness opinions provided by respective advisors Plan of arrangement resulting in pro rata ownership of 67 percent Penn West and 33 percent Canetic Subject to approval of 66 2/3 percent of Canetic unitholders and customary exchange, court and regulatory approvals Information Circular to be mailed in December 2007 Canetic unitholder meeting to be held in January 2008 with anticipated closing in mid January TRANSACTION DETAILS (cont’d) |

| Benefits of Combination Combination will form largest conventional oil & gas trust in North America and create world-class Canadian platform Combined Trust will represent 23 percent of total production and 21 percent of market capitalization of conventional oil & gas trust sector Scale and enhanced financial strength Will assist the future development of non-conventional plays including multi-billion barrel Peace River Oil Sands project, CBM, shale gas and EOR Will allow expansion both domestically and outside Canada Geographic and play type diversity provides flexibility to adjust in changing economic, political and environmental conditions SIZE, STRENGTH, LIQUIDITY |

| Benefits of Combination Pro forma asset base rivals senior E&P companies and provides added flexibility in positioning for post 2010 Enhanced liquidity on TSX and NYSE - increased weighting in major indices including S&P TSX 60 Broader access to capital markets Safe harbour capacity for future expansion increased to $8.7 billion in 2008 and $15 billion in total Combined tax pools of over $5.5 billion CDN will ensure an efficient tax position well beyond 2011 FLEXIBILITY |

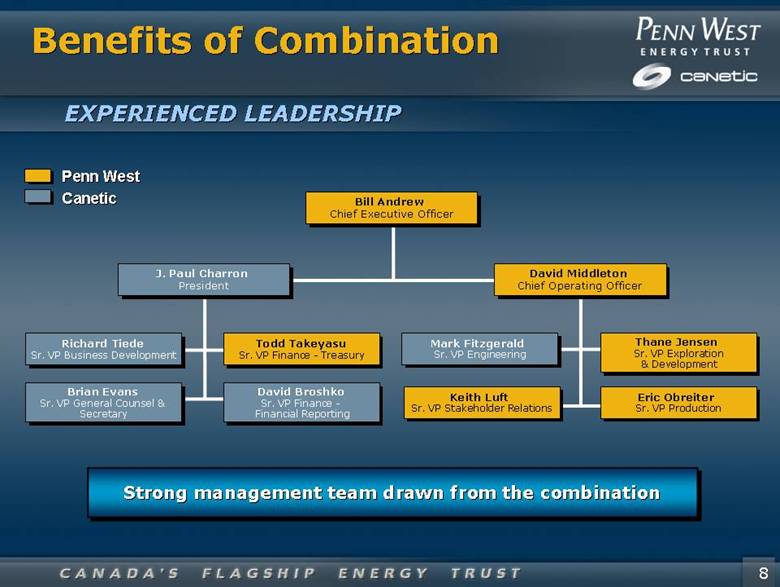

| J. Paul Charron President Richard Tiede Sr. VP Business Development Brian Evans Sr. VP General Counsel & Secretary Todd Takeyasu Sr. VP Finance - Treasury David Middleton Chief Operating Officer Bill Andrew Chief Executive Officer Thane Jensen Sr. VP Exploration & Development Eric Obreiter Sr. VP Production Penn West Canetic Mark Fitzgerald Sr. VP Engineering EXPERIENCED LEADERSHIP Strong management team drawn from the combination Benefits of Combination Keith Luft Sr. VP Stakeholder Relations David Broshko Sr. VP Finance - Financial Reporting |

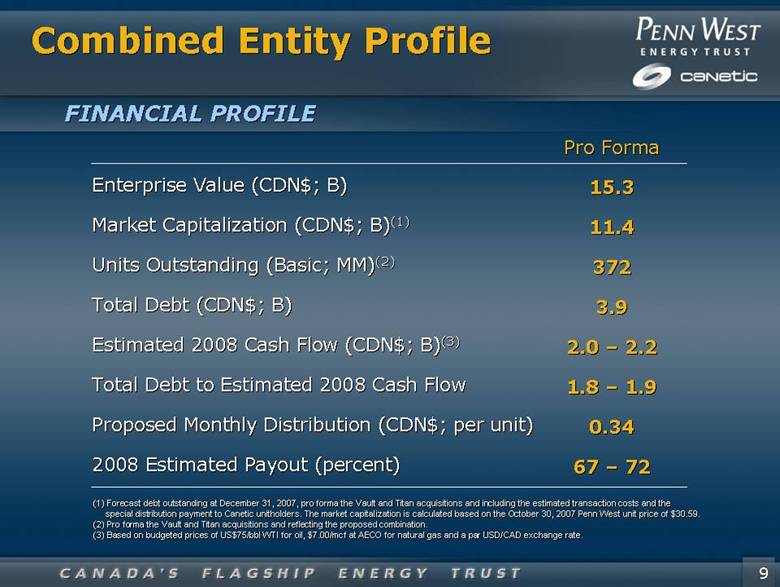

| Combined Entity Profile Enterprise Value (CDN$; B) Market Capitalization (CDN$; B)(1) Units Outstanding (Basic; MM)(2) Total Debt (CDN$; B) Estimated 2008 Cash Flow (CDN$; B)(3) Total Debt to Estimated 2008 Cash Flow Proposed Monthly Distribution (CDN$; per unit) 2008 Estimated Payout (percent) Pro Forma 15.3 11.4 372 3.9 2.0 – 2.2 1.8 – 1.9 0.34 67 – 72 FINANCIAL PROFILE (1) Forecast debt outstanding at December 31, 2007, pro forma the Vault and Titan acquisitions and including the estimated transaction costs and the special distribution payment to Canetic unitholders. The market capitalization is calculated based on the October 30, 2007 Penn West unit price of $30.59. (2) Pro forma the Vault and Titan acquisitions and reflecting the proposed combination. (3) Based on budgeted prices of US$75/bbl WTI for oil, $7.00/mcf at AECO for natural gas and a par USD/CAD exchange rate. |

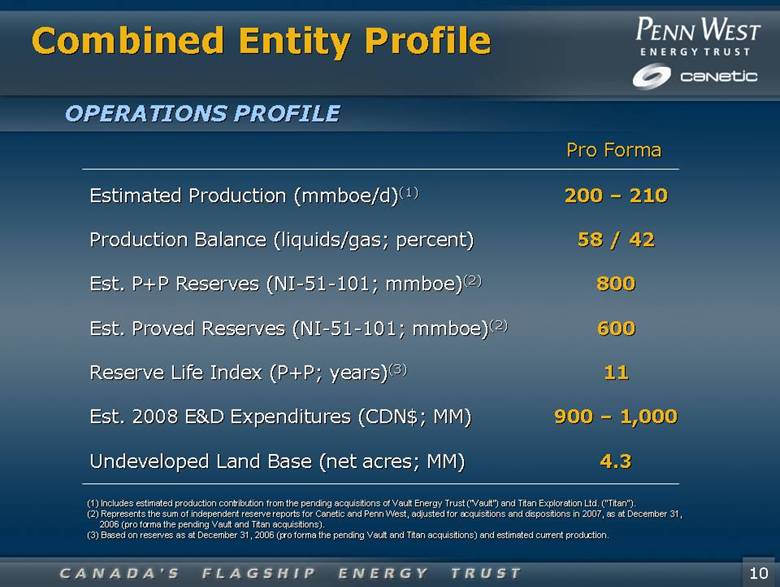

| Combined Entity Profile Estimated Production (mmboe/d)(1) Production Balance (liquids/gas; percent) Est. P+P Reserves (NI-51-101; mmboe)(2) Est. Proved Reserves (NI-51-101; mmboe)(2) Reserve Life Index (P+P; years)(3) Est. 2008 E&D Expenditures (CDN$; MM) Undeveloped Land Base (net acres; MM) Pro Forma OPERATIONS PROFILE 200 – 210 58 / 42 800 600 11 900 – 1,000 4.3 (1) Includes estimated production contribution from the pending acquisitions of Vault Energy Trust (“Vault”) and Titan Exploration Ltd. (“Titan”). (2) Represents the sum of independent reserve reports for Canetic and Penn West, adjusted for acquisitions and dispositions in 2007, as at December 31, 2006 (pro forma the pending Vault and Titan acquisitions). (3) Based on reserves as at December 31, 2006 (pro forma the pending Vault and Titan acquisitions) and estimated current production. |

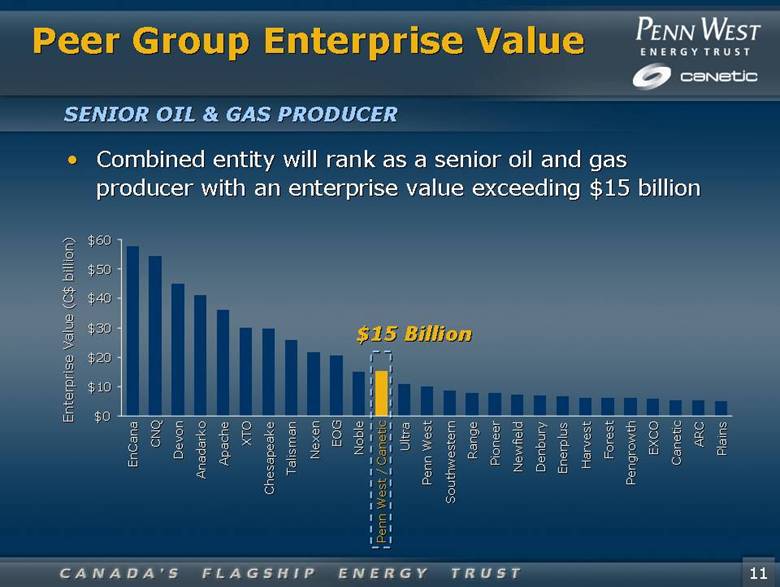

| Peer Group Enterprise Value SENIOR OIL & GAS PRODUCER Combined entity will rank as a senior oil and gas producer with an enterprise value exceeding $15 billion $0 $10 $20 $30 $40 $50 $60 EnCana CNQ Devon Anadarko Apache XTO Chesapeake Talisman Nexen EOG Noble Penn West / Canetic Ultra Penn West Southwestern Range Pioneer Newfield Denbury Enerplus Harvest Forest Pengrowth EXCO Canetic ARC Plains Enterprise Value (C$ billion) $15 Billion |

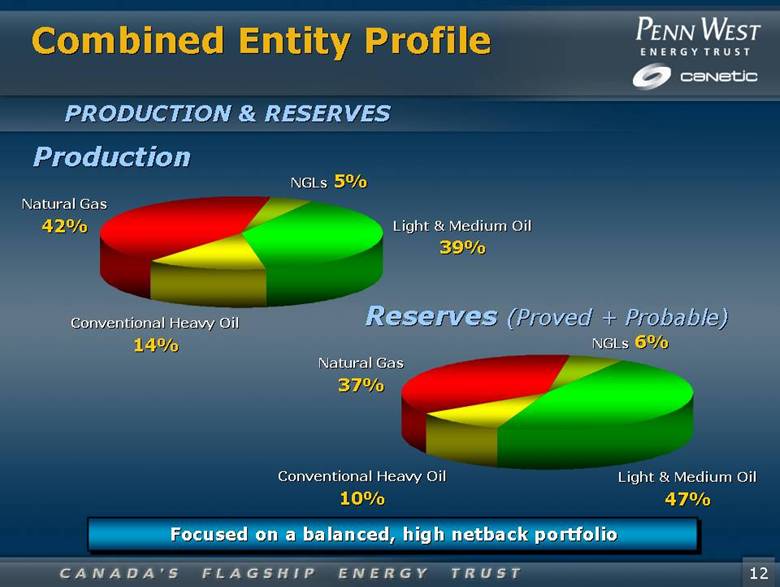

| PRODUCTION & RESERVES Combined Entity Profile Production Reserves (Proved + Probable) NGLs 5% Natural Gas 42% Light & Medium Oil 39% Conventional Heavy Oil 14% Natural Gas 37% Conventional Heavy Oil 10% Light & Medium Oil 47% NGLs 6% Focused on a balanced, high netback portfolio |

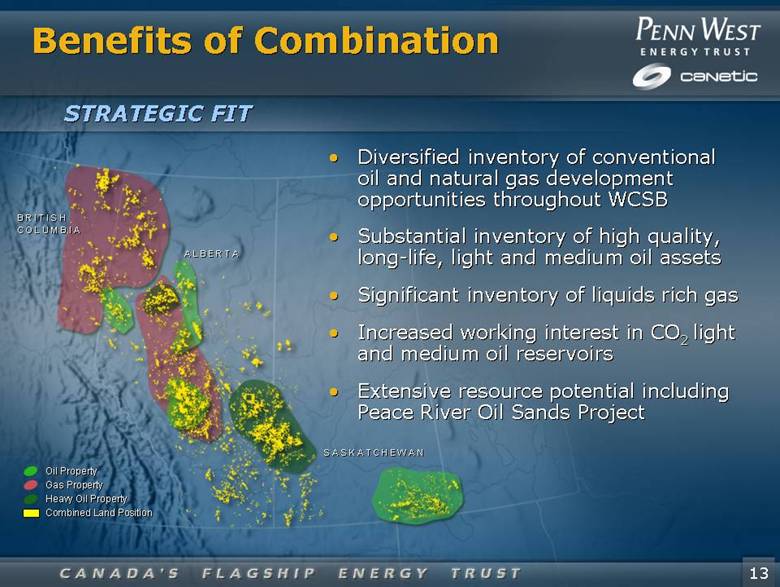

| Benefits of Combination Diversified inventory of conventional oil and natural gas development opportunities throughout WCSB Substantial inventory of high quality, long-life, light and medium oil assets Significant inventory of liquids rich gas Increased working interest in CO2 light and medium oil reservoirs Extensive resource potential including Peace River Oil Sands Project STRATEGIC FIT Oil Property Gas Property Heavy Oil Property Combined Land Position A L B E R T A S A S K A T C H E W A N B R I T I S H C O L U M B I A |

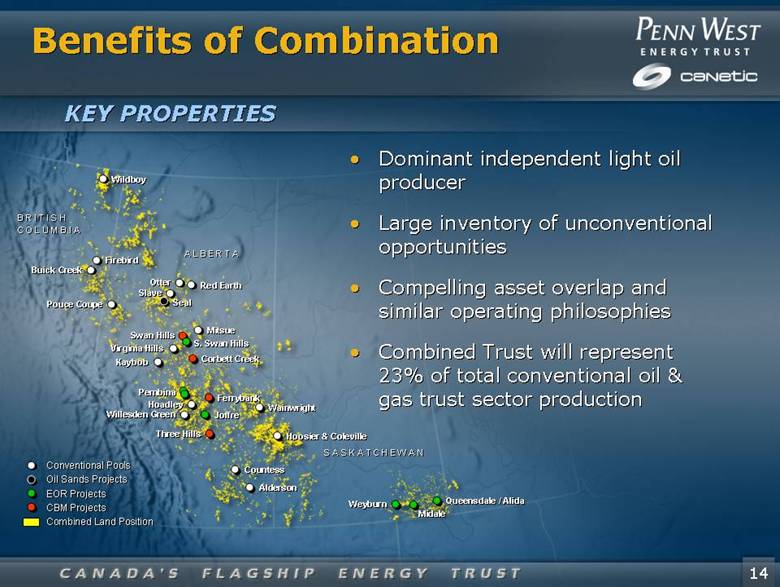

| Benefits of Combination KEY PROPERTIES A L B E R T A S A S K A T C H E W A N B R I T I S H C O L U M B I A Wildboy Firebird Red Earth Mitsue Virginia Hills Pembina Willesden Green Joffre Wainwright Hoosier & Coleville Midale Weyburn Swan Hills Kaybob Otter Slave Seal Three Hills Conventional Pools Oil Sands Projects EOR Projects CBM Projects Combined Land Position S. Swan Hills Buick Creek Dominant independent light oil producer Large inventory of unconventional opportunities Compelling asset overlap and similar operating philosophies Combined Trust will represent 23% of total conventional oil & gas trust sector production Pouce Coupe Corbett Creek Ferrybank Hoadley Alderson Countess Queensdale / Alida |

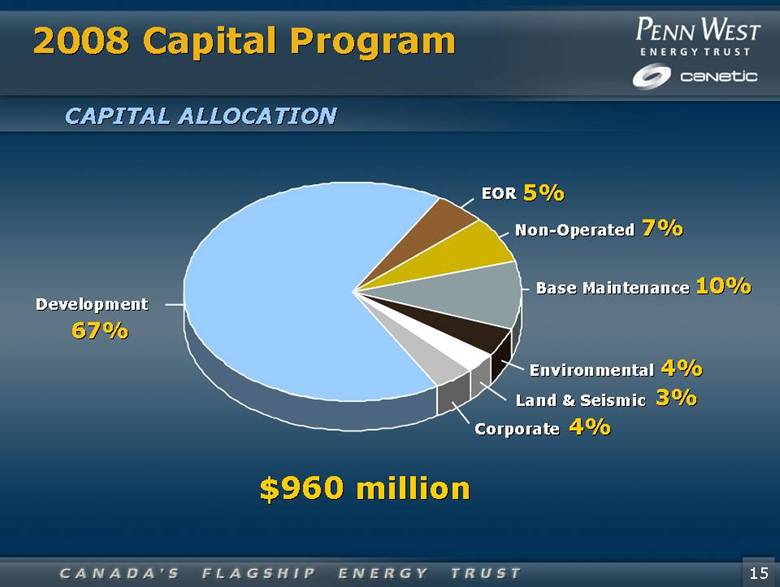

| 2008 Capital Program CAPITAL ALLOCATION $960 million Development 67% EOR 5% Non-Operated 7% Base Maintenance 10% Environmental 4% Land & Seismic 3% Corporate 4% |

| Near Term Development Emphasis on exploitation of assets Exploit operational efficiencies and economies of scale Leverage control and ownership of infrastructure Further consolidation in core areas Long Term Development Oil Sands CO2 Enhanced Oil Recovery Coalbed Methane Tight Gas / Shale Gas Future Growth Consolidator of Western Canadian Sedimentary Basin Expansion outside of Canada Increased unconventional development STRATEGIC FOCUS Moving Forward |

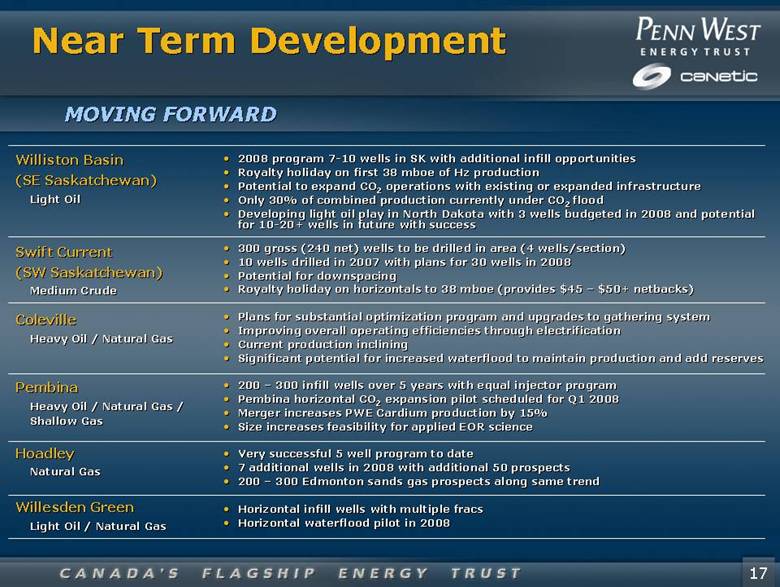

| Near Term Development MOVING FORWARD Williston Basin (SE Saskatchewan) Light Oil Swift Current (SW Saskatchewan) Medium Crude Coleville Heavy Oil / Natural Gas Pembina Heavy Oil / Natural Gas / Shallow Gas Hoadley Natural Gas Willesden Green Light Oil / Natural Gas 2008 program 7-10 wells in SK with additional infill opportunities Royalty holiday on first 38 mboe of Hz production Potential to expand CO2 operations with existing or expanded infrastructure Only 30% of combined production currently under CO2 flood Developing light oil play in North Dakota with 3 wells budgeted in 2008 and potential for 10-20+ wells in future with success 300 gross (240 net) wells to be drilled in area (4 wells/section) 10 wells drilled in 2007 with plans for 30 wells in 2008 Potential for downspacing Royalty holiday on horizontals to 38 mboe (provides $45 – $50+ netbacks) Plans for substantial optimization program and upgrades to gathering system Improving overall operating efficiencies through electrification Current production inclining Significant potential for increased waterflood to maintain production and add reserves 200 – 300 infill wells over 5 years with equal injector program Pembina horizontal CO2 expansion pilot scheduled for Q1 2008 Merger increases PWE Cardium production by 15% Size increases feasibility for applied EOR science Very successful 5 well program to date 7 additional wells in 2008 with additional 50 prospects 200 – 300 Edmonton sands gas prospects along same trend Horizontal infill wells with multiple fracs Horizontal waterflood pilot in 2008 |

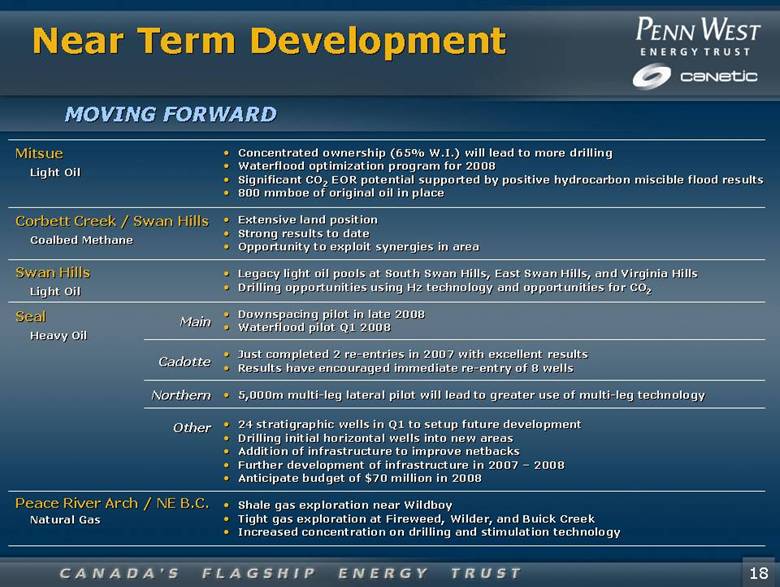

| Near Term Development MOVING FORWARD Mitsue Light Oil Corbett Creek / Swan Hills Coalbed Methane Swan Hills Light Oil Seal Heavy Oil Peace River Arch / NE B.C. Natural Gas Concentrated ownership (65% W.I.) will lead to more drilling Waterflood optimization program for 2008 Significant CO2 EOR potential supported by positive hydrocarbon miscible flood results 800 mmboe of original oil in place Extensive land position Strong results to date Opportunity to exploit synergies in area Legacy light oil pools at South Swan Hills, East Swan Hills, and Virginia Hills Drilling opportunities using Hz technology and opportunities for CO2 Downspacing pilot in late 2008 Waterflood pilot Q1 2008 Just completed 2 re-entries in 2007 with excellent results Results have encouraged immediate re-entry of 8 wells 5,000m multi-leg lateral pilot will lead to greater use of multi-leg technology 24 stratigraphic wells in Q1 to setup future development Drilling initial horizontal wells into new areas Addition of infrastructure to improve netbacks Further development of infrastructure in 2007 – 2008 Anticipate budget of $70 million in 2008 Shale gas exploration near Wildboy Tight gas exploration at Fireweed, Wilder, and Buick Creek Increased concentration on drilling and stimulation technology Main Cadotte Northern Other |

| Long Term Development FUTURE GROWTH Oil Sands - Seal CO2 Enhanced Oil Recovery Coalbed Methane Tight Gas / Shale Gas |

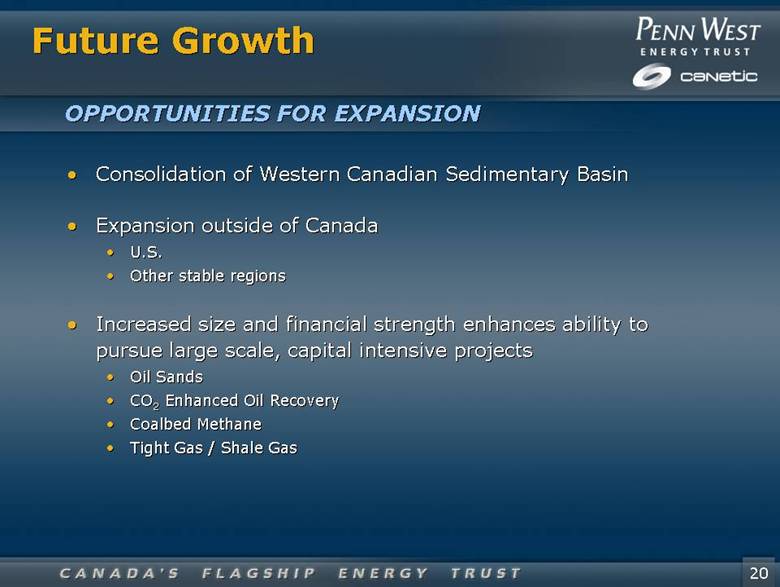

| Consolidation of Western Canadian Sedimentary Basin Expansion outside of Canada U.S. Other stable regions Increased size and financial strength enhances ability to pursue large scale, capital intensive projects Oil Sands CO2 Enhanced Oil Recovery Coalbed Methane Tight Gas / Shale Gas Future Growth OPPORTUNITIES FOR EXPANSION |

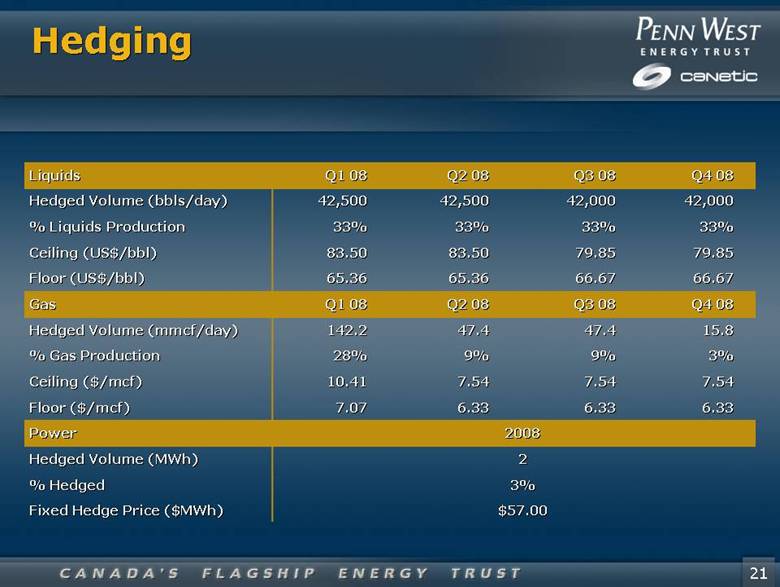

| Hedging Liquids Hedged Volume (bbls/day) % Liquids Production Ceiling (US$/bbl) Floor (US$/bbl) Gas Hedged Volume (mmcf/day) % Gas Production Ceiling ($/mcf) Floor ($/mcf) Power Hedged Volume (MWh) % Hedged Fixed Hedge Price ($MWh) Q1 08 42,500 33% 83.50 65.36 Q1 08 142.2 28% 10.41 7.07 Q2 08 42,500 33% 83.50 65.36 Q2 08 47.4 9% 7.54 6.33 Q3 08 42,000 33% 79.85 66.67 Q3 08 47.4 9% 7.54 6.33 Q4 08 42,000 33% 79.85 66.67 Q4 08 15.8 3% 7.54 6.33 2008 2 3% $57.00 |

| Change of: Impact on Cash Flow* Impact on Net Income* $1.00 CAD per bbl of liquids price Per trust unit (basic) 36.8 0.10 25.7 0.07 1,000 bbls per day in liquids production Per trust unit (basic) 14.4 0.04 4.8 0.01 $0.10 CAD per mcf of natural gas price Per trust unit (basic) 15.1 0.04 10.5 0.03 10 mmcf per day in natural gas production Per trust unit (basic) 12.4 0.03 - - 1% in effective interest rate Per trust unit (basic) 31.5 0.08 22.0 0.06 $0.01 in $CAD/$USD exchange rate Per trust unit (basic) 27.6 0.07 19.2 0.05 * $ millions, except per unit amounts. Cash Flow represents EBITDA less interest and cash taxes and is prior to all non-cash revenues and expenses. The impact on cash flow and net income is computed based on 2007 forecast commodity prices and production volumes. The impact on net income further assumes that the distribution levels are not adjusted for changes in cash flow thus reducing the incremental tax rate. These sensitivities are subject to known or unknown risks and uncertainties that could cause actual results to differ materially from those anticipated or implied in the forward looking statements. Sensitivity analysis assumes that none of the Trust’s production is hedged. Combined Sensitivities – 2008 Forecast Pro Forma 2008 |

| Contact Stock Exchange Toronto: PWT.UN New York: PWE Penn West Energy Trust 2200, 425 – 1st Street SW Calgary, Alberta, Canada T2P 3L8 Bill Andrew President & CEO Telephone: (403) 777-2502 Fax: (403) 777-2699 Stock Exchange Toronto: CNE.UN New York: CNE Canetic Resources Trust 1900, 255 – 5th Avenue SW Calgary, Alberta, Canada T2P 3G6 Paul Charron President & CEO Telephone: (403) 539-6330 Fax: (403) 539-5900 |