Filed by SandRidge Energy, Inc.

pursuant to Rule 425 under the Securities

Act of 1933, as amended, and deemed filed

pursuant to Rule 14a-12 under the Securities

Exchange Act of 1934, as amended

Subject Company: Arena Resources, Inc.

Commission File No.: 001-31657

![]()

SandRidge Energy to acquire Arena Resources

SandRidge Energy to acquire Arena

Resources

Responses to selected Proxy Advisor issues

May 2010

SandRidge Energy to acquire Arena Resources

Responses to selected Proxy Advisor issues

Position SandRidge / Arena perspectives on position

Arena did not conduct a full process to solicit interest in acquiring the company

“We are concerned that the board of Arena failed to conduct a full review of strategic alternatives prior to entering into the proposed agreement” (Glass Lewis)

Arena has periodically engaged in a review of its strategic alternatives to ensure it maximizes shareholder value

Arena has, from time to time, engaged in discussions with third parties with a view of potentially pursuing strategic business combinations

In February 2009 and June 2009, Arena had preliminary discussions with third parties relating to a possible business combination

In both instances, the discussions led to the execution of a confidentiality agreement and limited due diligence, but no further discussions took place following the exchange of preliminary information

In the approximate 12-month period prior to the anticipated closing of the merger, Arena received one other indication of interest from a third party relating to a possible business combination

Arena and this company executed a confidentiality agreement in February 2010 but only preliminary discussions took place following the exchange of preliminary information

The merger agreement permits Arena to entertain any inbound expressions of interest

Over the past eight weeks, since the announcement of the transaction on April 4, 2010, no party has contacted Arena to express an interest in acquiring the Company

1

SandRidge Energy to acquire Arena Resources

Responses to selected Proxy Advisor issues

Position SandRidge / Arena perspectives on position

Strategic rationale for Arena to pursue a transaction with SandRidge

“Strategic rationale of the transaction is less intuitive from Arena’s perspective” (Risk Metrics)

Arena has consistently communicated a clear rationale for entering into a merger agreement with SandRidge. Selected reasons include:

Offer fully recognizes the value Arena has created for its shareholders to date

Arena’s stake in the combined company exceeds the percentage contribution from most operational metrics including daily production, proved reserves, proved developed reserves and EBITDA – transaction multiples at the high end of peer trading levels and precedent transactions range

Transaction allows Arena shareholders to participate in the upside potential offered through SandRidge equity

48% stake in the enlarged entity

Full participation in the unique synergies the combination offers – e.g. accelerated drilling, operational enhancements, SG&A synergies

Exposure to longer term gas price fundamentals and 550,000 acres of exploration upside in the West Texas Overthrust

Continued significant oil exposure through combined entity

57% of total proven reserves, 58% of Q1 revenue, 82% of PV-10

Creation of a leading Permian player with significant operational and basin expertise with 21.5 Mboe/d production and 183 MMboe reserves within a combined company with 57.8 Mboe/d production and reserves of 288 MMboe

Provides ownership in SandRidge’s recently acquired Forest Permian assets sought after by Arena

Combined 5,700 potential oil well drilling locations

Exposure to significant oil development potential from multiple assets

Creates ownership in SandRidge’s current gas production and significant upside potential from SandRidge’s significant resource base (over 11 Tcf of resource potential) through extensive planned drilling program

Accesses SandRidge’s extensive resource execution capabilities in area’s common to Arena’s assets

2

SandRidge Energy to acquire Arena Resources

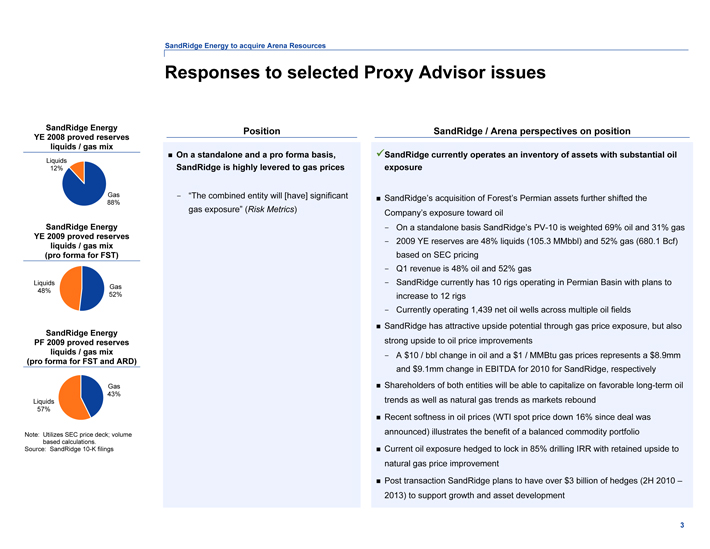

SandRidge Energy YE 2008 proved reserves liquids / gas mix

Liquids 12%

Gas 88%

SandRidge Energy YE 2009 proved reserves liquids / gas mix (pro forma for FST)

Liquids 48%

Gas 52%

SandRidge Energy PF 2009 proved reserves liquids / gas mix (pro forma for FST and ARD)

Liquids 57%

Gas 43%

Note: Utilizes SEC price deck; volume based calculations. Source: SandRidge 10-K filings

Position SandRidge / Arena perspectives on position

On a standalone and a pro forma basis, SandRidge is highly levered to gas prices

“The combined entity will [have] significant gas exposure” (Risk Metrics)

SandRidge currently operates an inventory of assets with substantial oil exposure

SandRidge’s acquisition of Forest’s Permian assets further shifted the Company’s exposure toward oil

On a standalone basis SandRidge’s PV-10 is weighted 69% oil and 31% gas

2009 YE reserves are 48% liquids (105.3 MMbbl) and 52% gas (680.1 Bcf) based on SEC pricing

Q1 revenue is 48% oil and 52% gas

SandRidge currently has 10 rigs operating in Permian Basin with plans to increase to 12 rigs

Currently operating 1,439 net oil wells across multiple oil fields

SandRidge has attractive upside potential through gas price exposure, but also strong upside to oil price improvements

A $10 / bbl change in oil and a $1 / MMBtu gas prices represents a $8.9mm and $9.1mm change in EBITDA for 2010 for SandRidge, respectively

Shareholders of both entities will be able to capitalize on favorable long-term oil trends as well as natural gas trends as markets rebound

Recent softness in oil prices (WTI spot price down 16% since deal was announced) illustrates the benefit of a balanced commodity portfolio

Current oil exposure hedged to lock in 85% drilling IRR with retained upside to natural gas price improvement

Post transaction SandRidge plans to have over $3 billion of hedges (2H 2010 – 2013) to support growth and asset development

3

SandRidge Energy to acquire Arena Resources

Responses to selected Proxy Advisor issues

Position SandRidge / Arena perspectives on position

ARD’s share price has been dragged down by the underperformance of SandRidge

“Since SandRidge/Arena announced the merger, the selected peer group traded down about 3%. We note however, Arena shares are down about 11%, underperforming peers by additional 8%, dragged down by the underperformance of SandRidge” (Risk Metrics)

Since Arena announced Q1 earnings on May 10, 2010, both companies have performed broadly in line with the wider E&P space

SandRidge down 2%; Arena down 4% since immediately before Arena’s Q1 earnings announcement

Comparable to large cap, midcap, small and microcap E&P peer performance

Outperformed Oil (8%), the S&P 500 (4%) and the DJIA (4%)

Though SandRidge has traded down since ARD earnings announcement, so too have some of SandRidge’s closest peers – PXP (12%), APA (6%), NFX (6%), FST (4%)

Note: Share prices as of March 26, 2010 close.

4

SandRidge Energy to acquire Arena Resources

Responses to selected Proxy Advisor issues

Position SandRidge / Arena perspectives on position

Synergy potential with a combination

“Though both companies argue there could be significant operational synergies, they did not quantify it in public form” (Risk Metrics)

SandRidge and Arena believe that significant synergy potential can be realized as a result of the unique strategic fit of both companies

Complementary geographic overlap in the Permian Basin and extending into the West Texas Overthrust

Accelerated oil drilling potential on the Central Basin Platform of the Permian Basin

Center of SandRidge’s oil field service operations (Ft. Stockton) within ~60 miles of all major assets of both SandRidge and Arena

Ownership control and ability to move rigs as needed

SandRidge is currently one of the largest contractors in the region of pressure pumping, workover rigs, gas processing and storage, infrastructure requirements

Expected operational improvements

Combined company expects to achieve material oil production growth through improvement in process run-times, reliability and accelerated drilling of low risk, high return oil wells

SandRidge has strong infrastructure capabilities in place to handle recent Fuhrman Mascho operational challenges

Expected increase in rig program to drive incremental value creation

One incremental rig run for a year can create $5 million to $17 million in value(a)

SG&A reduction – potential future present value in excess of $100 million(b)

Close proximity of Arena assets to Ft. Stockton

Corporate center rationalization

Technical knowledge sharing and midstream capabilities

Financial

Combined entity will have more capacity to hedge production and will have the opportunity to hedge an incremental $1.5 – $2 billion of future revenue

(a) Based on constant NYMEX oil prices varying between $70 and $85/bbl and $4.50/MMBtu NYMEX gas escalating to $6.00 in 2014. Impact based on hypothetical Fuhrman Mascho type curve. Assumes discount rate of 12%, $8.50/Boe operating costs, production and ad valorem taxes of 5.0% of revenue, production related SG&A of $1.50/Boe, oil differential of ($5.00)/Bbl and gas differential of $1.00/Mcf (due to liquids content). (b) Based on Q1 annualized G&A and a perpetuity discount rate of 11.5%.

5

SandRidge Energy to acquire Arena Resources

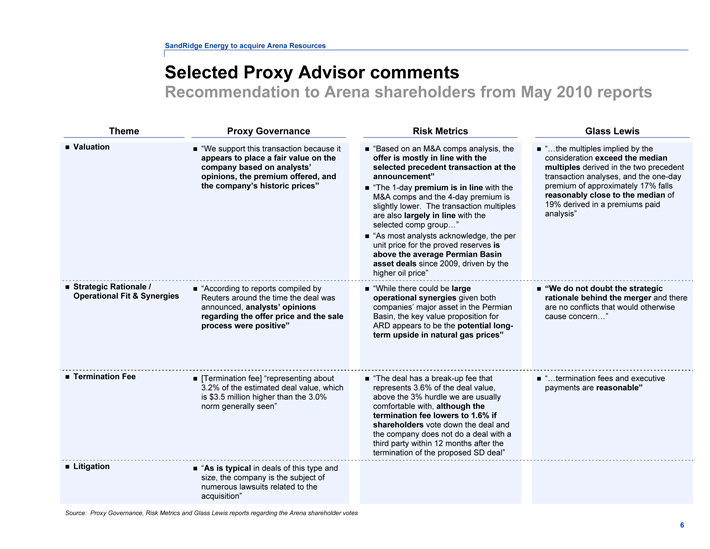

Selected Proxy Advisor comments Recommendation to Arena shareholders from May 2010 reports

Theme Proxy Governance Risk Metrics Glass Lewis

Valuation

“We support this transaction because it appears to place a fair value on the company based on analysts’ opinions, the premium offered, and the company’s historic prices”

“Based on an M&A comps analysis, the offer is mostly in line with the selected precedent transaction at the announcement”

“The 1-day premium is in line with the M&A comps and the 4-day premium is slightly lower. The transaction multiples are also largely in line with the selected comp group…”

“As most analysts acknowledge, the per unit price for the proved reserves is above the average Permian Basin asset deals since 2009, driven by the higher oil price”

“…the multiples implied by the consideration exceed the median multiples derived in the two precedent transaction analyses, and the one-day premium of approximately 17% falls reasonably close to the median of 19% derived in a premiums paid analysis”

Strategic Rationale / Operational Fit & Synergies

“According to reports compiled by Reuters around the time the deal was announced, analysts’ opinions regarding the offer price and the sale process were positive”

“While there could be large operational synergies given both companies’ major asset in the Permian Basin, the key value proposition for ARD appears to be the potential long-term upside in natural gas prices”

“We do not doubt the strategic rationale behind the merger and there are no conflicts that would otherwise cause concern…”

Termination Fee

[Termination fee] “representing about 3.2% of the estimated deal value, which is $3.5 million higher than the 3.0% norm generally seen”

“The deal has a break-up fee that represents 3.6% of the deal value, above the 3% hurdle we are usually comfortable with, although the termination fee lowers to 1.6% if shareholders vote down the deal and the company does not do a deal with a third party within 12 months after the termination of the proposed SD deal”

“…termination fees and executive payments are reasonable”

Litigation

“As is typical in deals of this type and size, the company is the subject of numerous lawsuits related to the acquisition”

Source: Proxy Governance, Risk Metrics and Glass Lewis reports regarding the Arena shareholder votes

6

SandRidge Energy to acquire Arena Resources

IMPORTANT ADDITIONAL INFORMATION WILL BE FILED WITH THE SEC Portions of this communication are being made in respect of the proposed business combination involving SandRidge Energy, Inc. and Arena Resources, Inc. In connection with the proposed transaction, SandRidge Energy, Inc. has filed with the Securities and Exchange Commission (the “SEC”) a Registration Statement on Form S-4 containing a Joint Proxy Statement/Prospectus (Registration No. 333-166141), and each of SandRidge Energy, Inc. and Arena Resources, Inc. may file with the SEC other documents regarding the proposed transaction. The definitive Joint Proxy Statement/Prospectus was mailed to stockholders of SandRidge Energy, Inc. and Arena Resources, Inc. Investors and security holders of SandRidge Energy, Inc. and Arena Resources, Inc. are urged to read the Joint Proxy Statement/Prospectus and other documents filed with the SEC carefully in their entirety when they become available because they contain important information about the proposed transaction. Investors and security holders may obtain free copies of the Registration Statement and the Joint Proxy Statement/Prospectus and other documents filed with the SEC by SandRidge Energy, Inc. and Arena Resources, Inc. through the web site maintained by the SEC at www.sec.gov. Free copies of the Registration Statement and the Joint Proxy Statement/Prospectus and other documents filed with the SEC can also be obtained by directing a request to SandRidge Energy, Inc., 123 Robert S. Kerr Avenue, Oklahoma City, Oklahoma 73102, Attention: Investor Relations, or by directing a request to Arena Resources, Inc., 6555 South Lewis Avenue, Tulsa, Oklahoma 74136, Attention: Investor Relations. SandRidge Energy, Inc., Arena Resources, Inc and their respective directors and executive officers and other persons may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information regarding SandRidge Energy, Inc.’s directors and executive officers is available in its Annual Report on Form 10-K for the year ended December 31, 2009, which was filed with the SEC on March 1, 2010, and its proxy statement for its 2010 annual meeting of stockholders, which was filed with the SEC on April 26, 2010, and information regarding Arena Resources, Inc.’s directors and executive officers is available in its Annual Report on Form 10-K for the year ended December 31, 2009, which was filed with the SEC on March 1, 2010 and its proxy statement for its 2009 annual meeting of stockholders, which was filed with the SEC on October 29, 2009. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the Joint Proxy Statement/Prospectus and other relevant materials to be filed with the SEC when they become available.

7

SandRidge Energy to acquire Arena Resources

Safe Harbor Language on Forward Looking Statements: This communication includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements express a belief, expectation or intention and are generally accompanied by words that convey projected future events or outcomes. The forward-looking statements include statements relating to when the companies expect to close the proposed transaction. We have based these forward-looking statements on our current expectations and assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate under the circumstances. However, whether actual results and developments will conform with our expectations and predictions is subject to a number of risks and uncertainties, including the failure of SandRidge Energy, Inc. or Arena Resources, Inc. stockholders to approve the merger, the risk that the businesses will not be integrated successfully, credit conditions of global capital markets, changes in economic conditions, regulatory changes, and other factors, many of which are beyond our control. We refer you to the discussion of risk factors in Part I, Item 1A - “Risk Factors” of the Annual Report on Form 10-K filed by SandRidge Energy, Inc. with the SEC on March 1, 2010; Part II, Item 1A – “Risk Factors” of the Quarterly Report on Form 10-Q for the quarter ended March 31, 2010 filed by SandRidge Energy, Inc. with the SEC on May 7, 2010; and Part I, Item Safe Harbor Language on Forward Looking Statements: 1A - “Risk Factors” of the Annual Report on Form 10-K filed by Arena Resources, Inc. with the SEC on March 1, 2010. All of the forward-looking statements made in this press release are qualified by these cautionary statements. The actual results or developments anticipated may not be realized or, even if substantially realized, they may not have the expected consequences to or effects on our company or our business or operations. Such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. We undertake no obligation to update or revise any forward-looking statements.

8

SandRidge Energy to acquire Arena Resources

The SEC permits oil and natural gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves, as each is defined by the SEC. Under SEC rules, proved reserve estimates are considered reasonably certain. Probable reserve estimates are as likely as not to be achieved and possible reserve estimates might be achieved but only under more favorable circumstances than are likely, making each of them inherently less certain than proved reserve estimates and subject to greater risk of being actually realized by the company. At times this presentation uses the term “resource potential” and other descriptions of hydrocarbon volumes potentially recoverable through additional drilling or recovery techniques to provide estimates that the SEC’s guidelines prohibit us from including in filings with the SEC. These estimates are by their nature more speculative than estimates of proved, probable or possible reserves and, accordingly, are subject to substantially greater risk of being actually realized by the company. For a discussion of SandRidge’s proved reserves, as calculated under current SEC rules, you are referred to SandRidge’s Annual Report on Form 10-K referenced above, which is available on our website at www.sandridgeenergy.com and on the SEC’s website at www.sec.gov.

9