Exhibit 99.2 |

2 Safe Harbor Language on Forward Looking Statements: This presentation includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements express a belief, expectation or intention and are generally accompanied by words that convey projected future events or outcomes. The forward-looking statements include statements relating to the impact SandRidge Energy, Inc. expects the proposed merger with Arena Resources, Inc. to have on the combined entity's operations, financial condition, and financial results, and SandRidge Energy, Inc.’s expectations about its ability to successfully integrate the combined businesses and the amount of cost savings and overall operational efficiencies SandRidge Energy, Inc. expects to realize as a result of the proposed merger. The forward-looking statements also include statements about SandRidge Energy, Inc.’s future operations, estimates of reserve and resource volumes, reserve values, future drilling locations, costs, cash flow, hedging transactions, and anticipated timing for filings with regulatory agencies, shareholder meetings and closing of the proposed merger. We have based these forward-looking statements on our current expectations and assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate under the circumstances. However, whether actual results and developments will conform with our expectations and predictions is subject to a number of risks and uncertainties, including the ability to obtain governmental approvals of the merger on the proposed terms and schedule, the failure of SandRidge Energy, Inc. or Arena Resources, Inc. stockholders to approve the merger, the risk that the businesses will not be integrated successfully, the risk that the cost savings and any synergies from the merger may not be fully realized or may take longer to realize than expected, disruption from the merger making it more difficult to maintain relationships with customers, employees or suppliers, the volatility of natural gas and oil prices, our success in discovering, estimating, and developing natural gas and oil reserves, the availability and terms of capital, our timely execution of hedge transactions, credit conditions of global capital markets, changes in economic conditions, regulatory changes, including those related to carbon dioxide and greenhouse gas emissions, and other factors, many of which are beyond our control. We refer you to the discussion of risk factors in Part I, Item 1A - “Risk Factors” of our Annual Report on Form 10-K for the year ended December 31, 2009 and the Annual Report on Form 10-K filed by Arena Resources, Inc. and in comparable “risk factors” sections of our and Arena Resources, Inc.’s Quarterly Reports on Form 10-Q filed after the date of this presentation. All of the forward-looking statements made in this presentation are qualified by these cautionary statements. The actual results or developments anticipated may not be realized or, even if substantially realized, they may not have the expected consequences to or effects on our company or our business or operations. Such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. We undertake no obligation to update or revise any forward-looking statements. The SEC permits oil and natural gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves, as each is defined by the SEC. At times we use the term "EUR" (estimated ultimate recovery) to provide estimates that the SEC’s guidelines prohibit us from including in filings with the SEC. In addition, this presentation includes a table demonstrating the sensitivity of proved oil and natural gas reserves to price fluctuations by comparing the reserves calculated under the price assumptions required by current U.S. Securities and Exchange Commission (“SEC”) rules to (1) spot prices at December 31, 2009, and (2) the 10-year average NYMEX strip prices as of December 31, 2009. The reserves presented under these alternative price assumptions are not calculated in accordance with current SEC rules, and they have not been reviewed by independent petroleum engineers. These estimates are by their nature more speculative than estimates of proved, probable or possible reserves and, accordingly, are subject to substantially greater risk of being actually realized by the company. For a discussion of the company’s proved reserves, as calculated under current SEC rules, we refer you to the company’s Annual Report on Form 10-K referenced above, which is available on our website at www.sandridgeenergy.com and on the SEC's website at www.sec.gov. Disclaimer (Page 1 of 2) |

3 IMPORTANT ADDITIONAL INFORMATION WILL BE FILED WITH THE SEC This communication is being made in respect of the proposed business combination involving SandRidge Energy, Inc. and Arena Resources, Inc. In connection with the proposed transaction, SandRidge Energy, Inc. plans to file with the Securities and Exchange Commission (the “SEC”) a Registration Statement on Form S-4 containing a Joint Proxy Statement/Prospectus, and each of SandRidge Energy, Inc. and Arena Resources, Inc. may file with the SEC other documents regarding the proposed transaction. The definitive Joint Proxy Statement/Prospectus will be mailed to stockholders of SandRidge Energy, Inc. and Arena Resources, Inc. Investors and security holders of SandRidge Energy, Inc. and Arena Resources, Inc. are urged to read the Joint Proxy Statement/Prospectus and other documents filed with the SEC carefully in their entirety when they become available because they will contain important information about the proposed transaction. Investors and security holders will be able to obtain free copies of the Registration Statement and the Joint Proxy Statement/Prospectus (when available) and other documents filed with the SEC by SandRidge Energy, Inc. and Arena Resources, Inc. through the web site maintained by the SEC at www.sec.gov. Free copies of the Registration Statement and the Joint Proxy Statement/Prospectus (when available) and other documents filed with the SEC can also be obtained by directing a request to SandRidge Energy, Inc., 123 Robert S. Kerr Avenue, Oklahoma City, Oklahoma 73102, Attention: Investor Relations, or by directing a request to Arena Resources, Inc., 6555 South Lewis Avenue, Tulsa, Oklahoma 74136, Attention: Investor Relations. SandRidge Energy, Inc., Arena Resources, Inc. and their respective directors and executive officers and other persons may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information regarding SandRidge Energy, Inc.’s directors and executive officers is available in its Annual Report on Form 10-K for the year ended December 31, 2009, which was filed with the SEC on March 1, 2010, and its proxy statement for its 2009 annual meeting of stockholders, which was filed with the SEC on April 22, 2009, and information regarding Arena Resources, Inc.’s directors and executive officers is available in its Annual Report on Form 10-K for the year ended December 31, 2009, which was filed with the SEC on March 1, 2010 and its proxy statement for its 2009 annual meeting of stockholders, which was filed with the SEC on October 29, 2009. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the Joint Proxy Statement/Prospectus and other relevant materials to be filed with the SEC when they become available. Disclaimer (Page 2 of 2) |

4 Transaction – Summary Strategy: Why Arena? Increases exposure to oil (8,500 Boepd – 86% Oil) Single asset focus in the Central Basin Platform • Low risk drilling (2,700 locations) • Shallow vertical wells (less than 6,000 feet) • Proven production history (discovered in 1930) Seamless integration by SandRidge • Extensive existing operations in Permian Basin • Close proximity to Ft. Stockton service base (33 rigs) • Long term cost control with rig ownership SandRidge post acquisition plans to have over $3.0 billion of hedges • Hedges for 2H10 - 2013 • Natural Gas upside for 2011 and beyond Transaction: $1.6 billion acquisition yields post acquisition SandRidge value of $6.2 billion 191 MM new SandRidge shares issued, no assumed debt Post acquisition 58% of SandRidge will be owned by current shareholders Relative PV-10 (debt adjusted) supports ownership percentage Accretive to cash flow per share in 2011 Expected closing June/July 2010 |

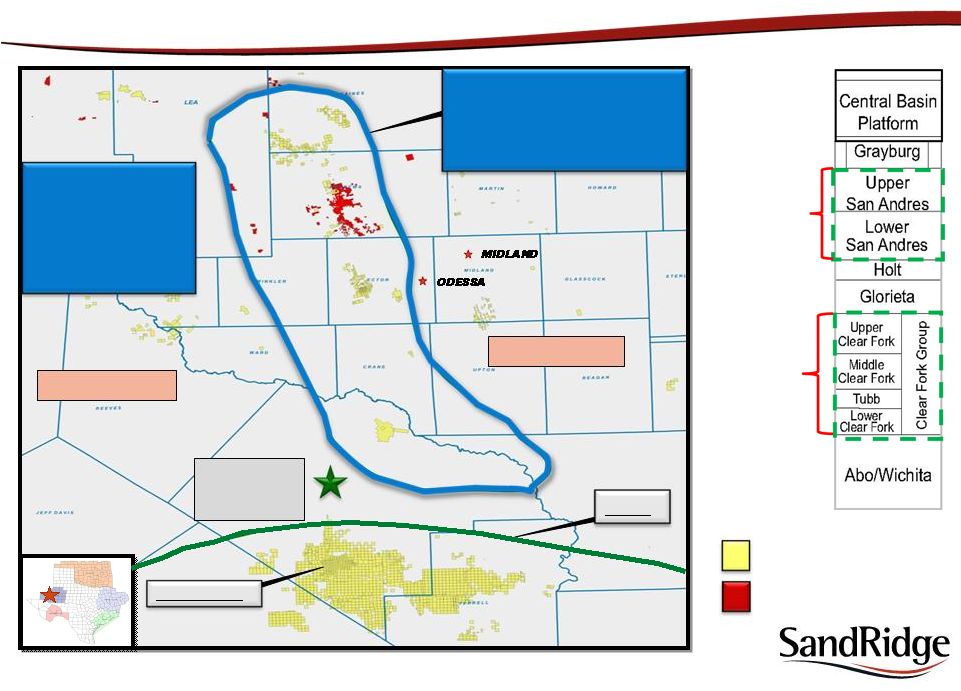

5 Transaction – Arena Key Attributes Production/Reserves 86% Oil Concentrated, operated oil-weighted Permian Basin position March 2 disclosed net production 8,500 Boepd with significant growth potential 69.3 Mmboe proven reserves YE 2009 Permian Basin Oil Approximately 67,600 Net Acres (85% Permian Basin) • High Working Interests ( 95% WI) Predictable Production Growth (from 200 to 8,500 Boepd in 5 years) Value Generation Driven by developing low risk San Andres wells @ 4,300’ • Large, multi-year inventory with over 2,700 San Andres locations Clear Fork potential @ 6,000’ Future Secondary and Tertiary Potential |

6 Concentrated West Texas Asset Base SandRidge Arena Ft. Stockton Service Base (33 drilling rigs) WTO Combined West Texas Net Acreage Position ˜ 770,000 acres CENTRAL BASIN PLATFORM San Andres / Clear Fork Formations Midland Basin PIÑON FIELD Delaware Basin San Andres (4,300’) Clear Fork (6,000’) |

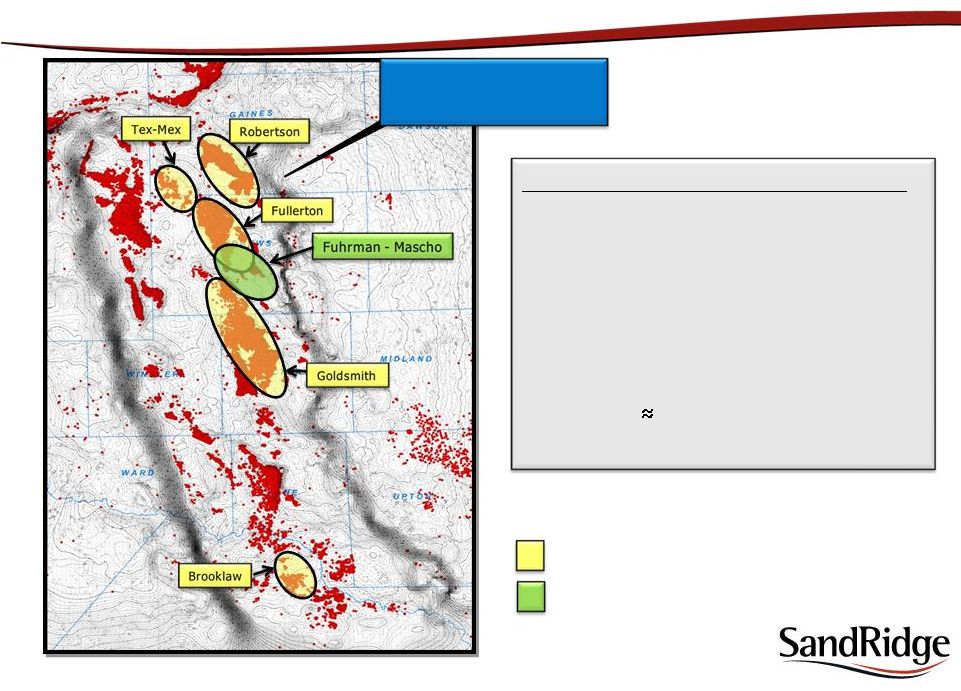

7 Permian Basin (Fuhrman – Mascho Field) Fuhrman-Mascho / San Andres • 2,700 low risk, 10 acre locations • 35 Mboe gross per primary location • 94.5 Mmboe EUR gross • 950 Producing Wells • 700 Wells Drilled Since 2005 • Well Costs $500,000 • Average Well Depth – 4,300 feet SandRidge Arena CENTRAL BASIN PLATFORM San Andres / Clear Fork Formations |

8 SandRidge Combined Asset Analysis (1) 2009 SEC 12 month average; $3.87/Mcf, $57.65/Bbl (2) Dec. 31, 2009 spot prices; $5.79/Mcf, $79.34/Bbl (3) Average 10 year NYMEX strip; $6.94/Mcf, $92.24/Bbl (4) Dec. 2009 average for SD, Mar. 2, 2010 for ARD Post-Acquisition Total Proven Reserves (MMBoe) 219 69 288 Proved Developed % 63% 37% 57% Proven Oil Value % 69% 99% 82% Current Production (MBoepd) 49.3 8.5 57.8 PV10 PROVEN (SEC) $MM 1,561 $ 1,121 $ 2,682 $ PV10 PROVEN (12/31 SPOT) $MM 3,590 $ 1,820 $ 5,410 $ PV10 PROVEN (NYMEX 10 yr avg) $MM 5,240 $ 2,234 $ 7,474 $ (1) (1) (1) (4) (1) (2) (3) |

9 SandRidge Permian Progression (1) SandRidge: February 2010 Permian average; Arena: March 2, 2010 (2) 2009 SEC 12 month average; $3.87/Mcf, $57.65/Bbl (3) Dec 31, 2009 spot prices; $5.79/Mcf, $79.34/Bbl (4) Average 10 year NYMEX strip; $6.94/Mcf, $92.24/Bbl Permian Production (MBoepd) 4.3 13.0 21.5 Net Acres (M Acres) 56 148 205 Total Proven Reserves (MMBoe) 43 117 183 Drilling Locations ( # ) 740 2,694 5,700 PV10 PROVEN (SEC) $MM 424 $ 990 $ 2,053 $ PV10 PROVEN (12/31 SPOT) $MM 778 $ 1,823 $ 3,557 $ PV10 PROVEN (NYMEX 10 yr avg) $MM 1,025 $ 2,414 $ 4,546 $ Permian Metrics as of YE 2009 (2) (2) (1) (3) (4) |

10 Acquisition Financial Review Goals of Transaction Increase exposure to oil Hedge significant amount of production through 2013 Cash flow per share accretion Balance sheet improvement Major Steps to Complete File S-4 File HSR Shareholder Vote (both SD and ARD) Expected Closing: June/July |

11 Transaction – Hedge Review Q3 & Q4 2H10 -2013 2010 TOTAL Current SandRidge Crude Oil (Mmbo) 2.3 14.8 Price $82.08 $85.88 Natural Gas (Bcf) 40.0 40.0 Price $7.76 $7.76 Total Revenue Hedged $499 $1,578 Arena Crude Oil (Mmbo) 0.6 0.6 Price (Floor) $66.67 $66.67 Natural Gas (Bcf) 0.9 0.9 Price (Floor) $4.00 $4.00 Total Revenue Hedged $40 $40 Revenue Hedged $540 $1,619 Revenue To Be Hedged $59 $1,416 Total Revenue Hedged $599 $3,034 |

12 Transaction – Share Analysis SandRidge SandRidge Pre-Acquisition Arena Post-Acquisition SD Shares Outstanding - March 26, 2010 210,797,254 SD 8.5% Preferred Stock 33,083,645 SD 6.0% Preferred Stock 18,416,206 Total SD Fully Diluted 262,297,105 262,297,105 ARD Shares Outstanding - March 15, 2010 39,018,737 ARD Options/Restricted Grants (1) 954,224 Total ARD Fully Diluted 39,972,961 Merger Conversion Ratio (2) 4.7771x Total ARD Merger Fully Diluted 190,953,633 190,953,633 New SandRidge Fully Diluted 453,250,738 (1) Assumes options settled cashless (2) Merger Conversion Ratio: $37.50/$7.85 = 4.7771x |

13 (as of December 31, 2009) SandRidge Estimated SandRidge Pre-Acquisition Arena Adjustments Post-Acquisition Cash $7.9 $63.6 -$15.0 $56.5 Debt Bank Debt $0.0 $0.0 $100.0 $100.0 Other Senior Debt 35.3 35.3 Floating Senior Notes 350.0 350.0 8.625% Senior Notes 650.0 650.0 9.875% Senior Notes 351.0 351.0 8.0% Senior Notes 750.0 750.0 8.75% Senior Notes 442.6 442.6 Total Debt $2,578.9 $0.0 $100.0 $2,678.9 Equity -$195.9 $522.7 $976.3 $1,303.1 Total Capitalization $2,390.9 $586.3 $1,061.3 $4,038.5 Transaction – Balance Sheet |

|