EXHIBIT 99.3

Ascend Acquisition Corp.

Acquisition of

e.PAK Resources (S) Pte. Ltd.

Cautionary Statements

THE ATTACHED SLIDESHOW WAS FILED ON AUGUST 13, 2007 WITH THE SECURITIES AND EXCHANGE COMMISSION AS PART OF THE AMMENDMENT NO. 1 TO FORM 8–K FILED BY ASCEND ACQUISITION CORP. ORIGINALLY FILED ON JULY 31, 2007 (“8–K”). ASCEND IS HOLDING PRESENTATIONS FOR CERTAIN OF ITS STOCKHOLDERS, AS WELL AS OTHER PERSONS WHO MIGHT BE INTERESTED IN PURCHASING ASCEND’S SECURITIES, REGARDING ITS ACQUISITION OF E.PAK RESOURCES (S) PTE. LTD., AS DESCRIBED IN THE 8–K AS AMENDED. THE ATTACHED SLIDESHOW, AS WELL AS THE 8–K AS AMENDED, ARE BEING DISTRIBUTED TO ATTENDEES OF THESE PRESENTATIONS. EARLYBIRDCAPITAL, INC. (“EBC”), THE MANAGING UNDERWRITER OF ASCEND’S INITIAL PUBLIC OFFERING (“IPO”) CONSUMMATED IN MAY 2006, IS ASSISTING ASCEND IN THESE EFFORTS AND WILL BE PAID A CASH FEE OF 1.5% OF CONSIDERATION PAID PLUS INDEBTEDNESS ASSUMED AND DEFERRED COMMISSIONS OF $925,000 AS THE UNDERWRITER OF THE IPO AT THE CLOSING OF THE ACQUISITION. ASCEND AND ITS DIRECTORS AND EXECUTIVE OFFICERS AND EBC MAY BE DEEMED TO BE PARTICIPANTS IN THE SOLICITATION OF PROXIES FOR THE SPECIAL MEETING OF STOCKHOLDERS TO BE HELD TO APPROVE THE ACQUISITION, AS WELL AS THE RELATED REDOMESTICATION OF ASCEND AS A BERMUDA PUBLIC COMPANY (“BERMUDA PUBCO”). STOCKHOLDERS OF ASCEND AND OTHER INTERESTED PERSONS ARE ADVISED TO READ, WHEN AVAILABLE, ASCEND’S PRELIMINARY PROSPECTUS AND FINAL PROSPECTUS IN CONNECTION WITH THE EXCHANGE OF BERMUDA PUBCO’S SHARES AND WARRANTS FOR THE OUTSTANDING SHARES AND WARRANTS OF ASCEND AND PRELIMINARY PROXY STATEMENT AND DEFINITIVE PROXY STATEMENT IN CONNECTION WITH ASCEND’S SOLICITATION OF PROXIES FOR THE SPECIAL MEETING BECAUSE THESE DOCUMENTS WILL CONTAIN IMPORTANT INFORMATION. SUCH PERSONS CAN ALSO READ ASCEND’S FINAL PROSPECTUS FROM THE IPO, DATED MAY 11, 2006, FOR A DESCRIPTION OF THE SECURITY HOLDINGS OF ASCEND’S OFFICERS AND DIRECTORS AND OF EBC AND THEIR RESPECTIVE INTERESTS IN THE SUCCESSFUL CONSUMMATION OF THIS BUSINESS COMBINATION. THE FINAL PROSPECTUS AND DEFINITIVE PROXY STATEMENT WILL BE MAILED TO STOCKHOLDERS AS OF A RECORD DATE TO BE ESTABLISHED FOR VOTING ON THE ACQUISITION. STOCKHOLDERS WILL ALSO BE ABLE TO OBTAIN A COPY OF THE FINAL PROSPECTUS AND DEFINITIVE PROXY STATEMENT, WITHOUT CHARGE, BY DIRECTING A REQUEST TO: ASCEND ACQUISITION CORP, 435 DEVON PARK DRIVE, BUILDING 400, WAYNE, PENNSYLVANIA 19087. THE PRELIMINARY AND FINAL PROSPECTUSES AND PRELIMINARY AND DEFINITIVE PROXY STATEMENTS, ONCE AVAILABLE, CAN ALSO BE OBTAINED, WITHOUT CHARGE, AT THE SECURITIES AND EXCHANGE COMMISSION’S INTERNET SITE (HTTP://WWW.SEC.GOV).

Forward Looking Statements

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995: THIS PRESENTATION AND ACCOMPANYING ORAL REMARKS MAY CONTAIN FORWARD-LOOKING STATEMENTS THAT INVOLVE RISKS AND UNCERTAINTIES THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE DESCRIBED. SUCH FACTORS INCLUDE, BUT ARE NOT LIMITED TO, THE COMPANY’S ABILITY TO EFFECT A BUSINESS COMBINATION, EPAK’S ABILITY TO GROW FUTURE REVENUES AND EARNINGS, CHANGES IN DEMAND FOR EPAK’S PRODUCTS, MARKET ACCEPTANCE OF THE COMPANY’S PRODUCTS, CHANGES IN THE LAWS OF THE PEOPLE’S REPUBLIC OF CHINA THAT AFFECT THE COMPANY’S OPERATIONS, AND OTHER FACTORS DETAILED FROM TIME TO TIME IN THE COMPANY’S FILINGS WITH THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION AND OTHER REGULATORY AUTHORITIES INCLUDING THE PROSPECTUS AND PROXY STATEMENT TO BE FILED IN CONNECTION WITH THE PROPOSED ACQUISITION. THE COMPANY UNDERTAKES NO OBLIGATION TO PUBLICLY UPDATE OR REVISE ANY FORWARD-LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE. AS USED HEREIN, THE “COMPANY” MEANS THE COMBINED ENTITIES ASCEND ACQUISITION CORPORATION OR THE CONTINUING ENTITY RESULTING FROM ITS AMALGAMATION WITH A WHOLLY OWNED BERMUDA SUBSIDIARY AND EPAK RESOURCES (S) PTE LTD, FOLLOWING THE INTENDED ACQUISITION OF EPAK BY ASCEND. THIS PRESENTATION SUPERSEDES ANY PRIOR INVESTOR PRESENTATION REGARDING THE TRANSACTIONS DESCRIBED HEREIN. EPAK’S FINANCIAL INFORMATION AND DATA CONTAINED HEREIN IN THE EXHIBITS HERETO HAS BEEN PREPARED BY EPAK AS A PRIVATE COMPANY, AND WAS PREPARED IN ACCORDANCE WITH THE PUBLISHED RULES AND REGULATIONS OF THE SINGAPORE FINANCIAL REPORTING STANDARD AND HAS NOT BEEN AUDITED UNDER UNITED STATES GENERALLY ACCEPTED ACCOUNTING PRINCIPLES AND MAY NOT CONFORM TO SEC REGULATION S-X. ACCORDINGLY, SUCH INFORMATION AND DATA MAY BE ADJUSTED AND PRESENTED DIFFERENTLY IN ASCEND’S PROSPECTUS AND PROXY STATEMENT TO SOLICIT STOCKHOLDER APPROVAL OF THE ACQUISITION AND RELATED MATTERS. ALL FINANCIAL AMOUNTS PRESENTED HEREIN AND IN THE EXHIBITS HERETO ARE IN US DOLLARS UNLESS SPECIFICALLY NOTED OTHERWISE.

ePAK Investment Merits

Leading full service supplier of semiconductor transfer and handling products

Central, PRC-based operations led by veteran semiconductor industry team

Accelerating revenue and earnings growth

Advanced low cost manufacturing

Consistent market growth, low volatility

Multiple opportunities for large scale growth

ePAK Focus

Semiconductor & Electronics

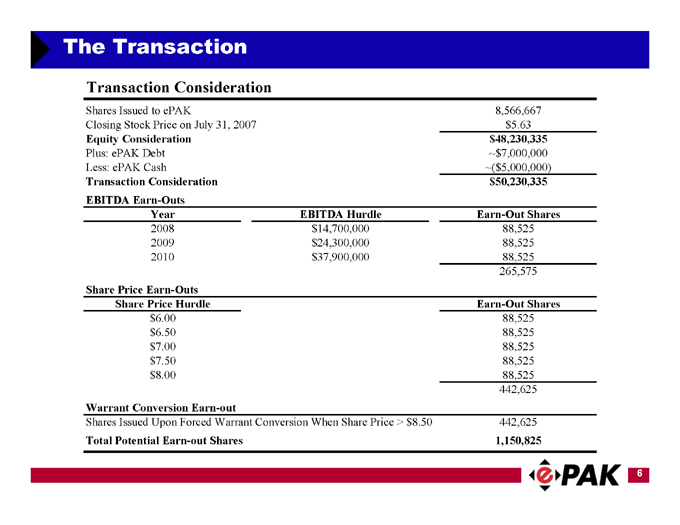

The Transaction

Transaction Consideration

Shares Issued to Epak | 8,566,667 | ||||

Closing Stock Price on July 31, 2007 | $5.63 | ||||

Equity Consideration | $48,230,335 | ||||

Plus: ePAK Debt | ~$7,000,000 | ||||

Less: ePAK Cash | ~($5,000,000) | ||||

Transaction Consideration | $50,230,335 | ||||

EBITDA Earn-Outs | |||||

Year |

| EBITDA Hurdle | Earn-Out Shares | ||

2008 | $ | 14,700,000 | 88,525 | ||

2009 | $ | 24,300,000 | 88,525 | ||

2010 | $ | 37,900,000 | 88,525 | ||

265,575 | |||||

Share Price Earn-Outs | |||||

Share Price Hurdle | Earn-Out Shares | ||||

$6.00 | 88,525 | ||||

$6.50 | 88,525 | ||||

$7.00 | 88,525 | ||||

$7.50 | 88,525 | ||||

$8.00 | 88,525 | ||||

442,625 | |||||

Warrant Conversion Earn-out | |||||

Shares Issued Upon Forced Warrant Conversion When Share Price > $8.50 | 442,625 | ||||

Total Potential Earn-out Shares | 1,150,825 |

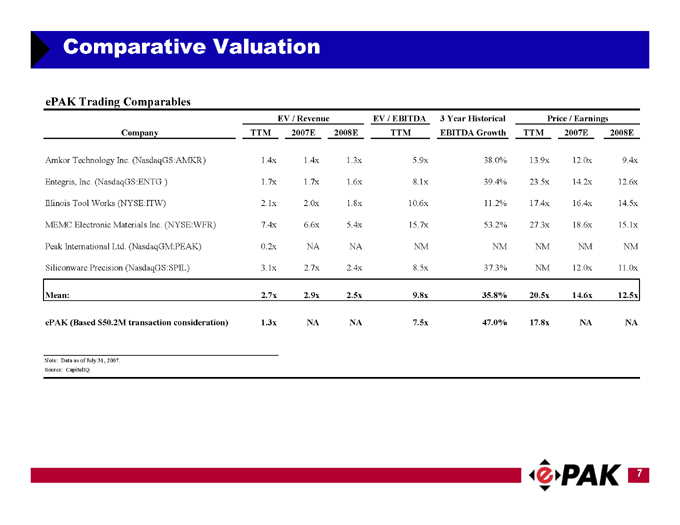

Comparative Valuation

ePAK Trading Comparables | |||||||||||||||||

EV / Revenue | EV /EBITDA | 3 Year Historical |

| Price / Earnings | |||||||||||||

Company | TTM | 2007E | 2008E | TTM | EBITDA Growth |

| TTM | 2007E | 2008E | ||||||||

Amkor Technology Inc. (NasdaqGS:AMKR) | 1.4x | 1.4x | 1.3x | 5.9x | 38.0 | % | 13.9x | 12.0x | 9.4x | ||||||||

Entegris, Inc. (NasdaqGS:ENTG ) | 1.7x | 1.7x | 1.6x | 8.1x | 39.4 | % | 23.5x | 14.2x | 12.6x | ||||||||

Illinois Tool Works (NYSE:ITW) | 2.1x | 2.0x | 1.8x | 10.6x | 11.2 | % | 17.4x | 16.4x | 14.5x | ||||||||

MEMC Electronic Materials Inc. (NYSE:WFR) | 7.4x | 6.6x | 5.4x | 15.7x | 53.2 | % | 27.3x | 18.6x | 15.1x | ||||||||

Peak International Ltd. (NasdaqGM:PEAK) | 0.2x | NA | NA | NM | NM |

| NM | NM | NM | ||||||||

Siliconware Precision (NasdaqGS:SPIL) | 3.1x | 2.7x | 2.4x | 8.5x | 37.3 | % | NM | 12.0x | 11.0x | ||||||||

Mean: | 2.7x | 2.9x | 2.5x | 9.8x | 35.8 | % | 20.5x | 14.6x | 12.5x | ||||||||

ePAK (Based $50.2M transaction consideration) | 1.3x | NA | NA | 7.5x | 47.0 | % | 17.8x | NA | NA | ||||||||

Note: Data as of July 31, 2007.

Source: CapitalIQ.

ePAK Overview

Dedicated to servicing the semiconductor and electronics industry

Global headquarters: Austin, TX

Large central manufacturing: Shenzhen, PRC

Founded in 1999

9 sales offices central to semiconductor industry

Over 500 customers

1,500 employees

100+ English-speaking engineering and technical staff

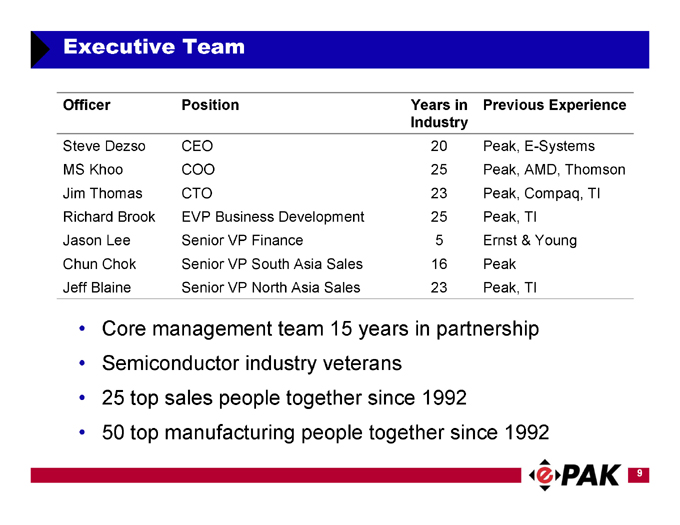

Executive Team

Officer | Position | Years in | Previous Experience | |||

Industry | ||||||

Steve Dezso | CEO | 20 | Peak, E-Systems | |||

MS Khoo | COO | 25 | Peak, AMD, Thomson | |||

Jim Thomas | CTO | 23 | Peak, Compaq, TI | |||

Richard Brook | EVP Business Development | 25 | Peak, TI | |||

Jason Lee | Senior VP Finance | 5 | Ernst & Young | |||

Chun Chok | Senior VP South Asia Sales | 16 | Peak | |||

Jeff Blaine | Senior VP North Asia Sales | 23 | Peak, TI |

Core management team 15 years in partnership

Semiconductor industry veterans

25 top sales people together since 1992

50 top manufacturing people together since 1992

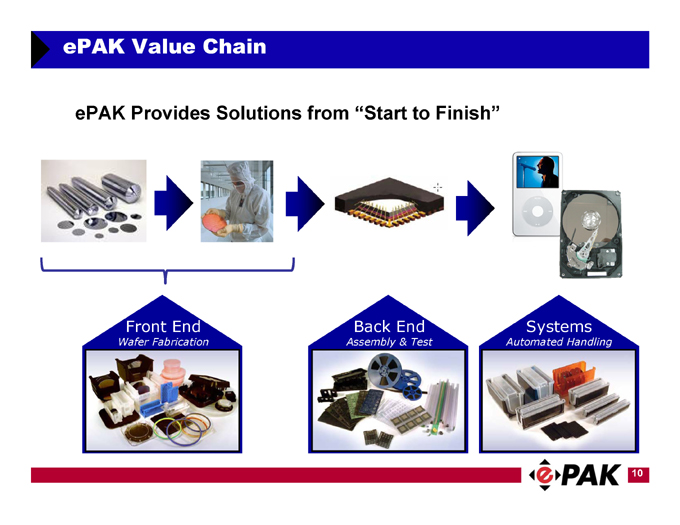

ePAK Value Chain

ePAK Provides Solutions from “Start to Finish”

Front End

Wafer Fabrication

Back End

Assembly & Test

Systems

Automated Handling

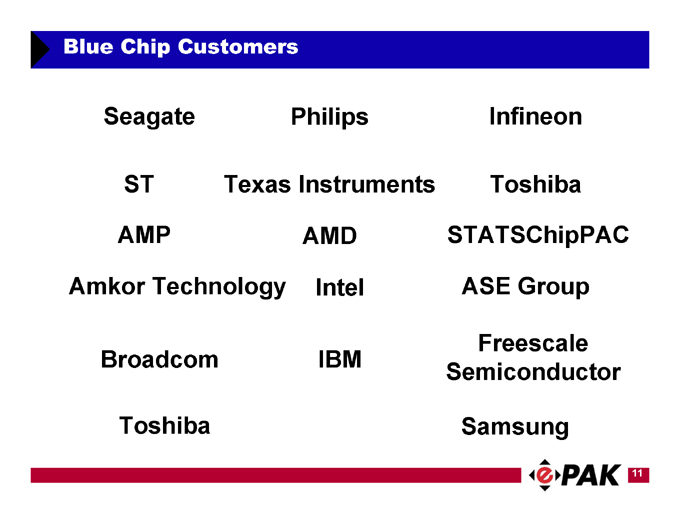

Blue Chip Customers

Seagate | Philips | Infineon | ||

ST | Texas Instruments | Toshiba | ||

AMP | AMD | STATSChipPAC | ||

Amkor Technology | Intel | ASE Group | ||

Freescale | ||||

Broadcom | IBM | |||

Semiconductor | ||||

Toshiba | Samsung |

Favorable Market Environment

Global semiconductor market is highly fragmented

ePAK’s products represent a small percentage of customers’ total cost

Customer demand driven by semiconductor unit volumes

– Consistent YOY growth

– Not subject to cyclical semiconductor capital equipment volatility

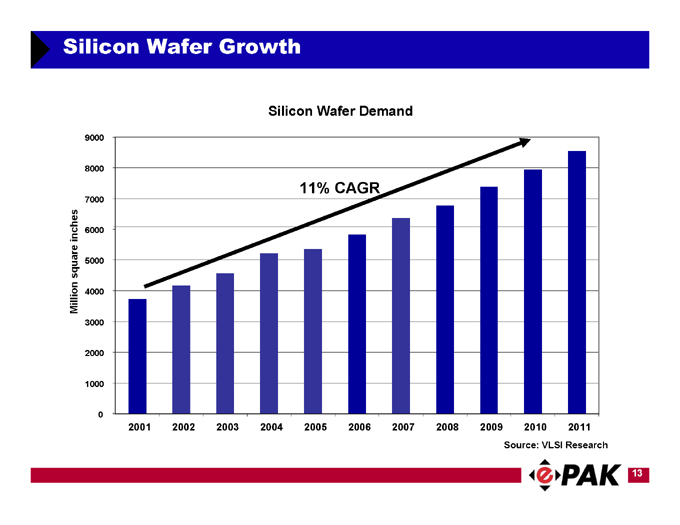

Silicon Wafer Growth

Silicon Wafer Demand

Million square inches

11% CAGR

9000

8000

7000

6000

5000

4000

3000

2000

1000

0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: VLSI Research

The ePAK Way

Customer problem = ePAK Opportunity

Design Solutions

ePAK is outsourced engineering for customer

Engineered solutions improve customer yield

Results in proprietary products for ePAK

Service solutions

Flexible vendor-managed inventory

Barriers to competition

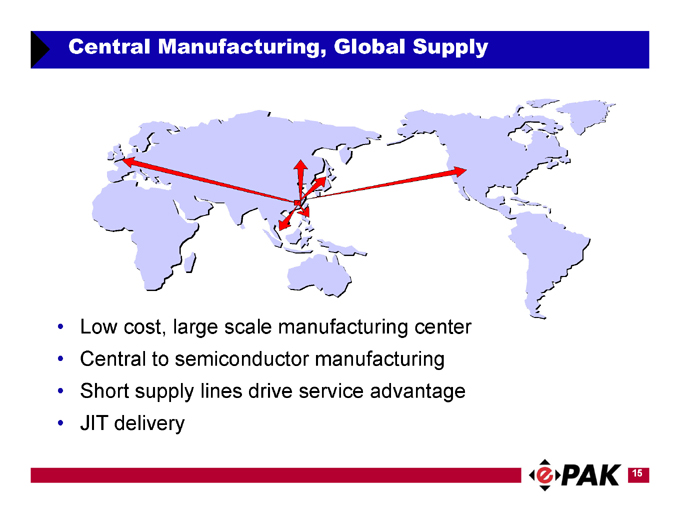

Central Manufacturing, Global Supply

Low cost, large scale manufacturing center

Central to semiconductor manufacturing

Short supply lines drive service advantage

JIT delivery

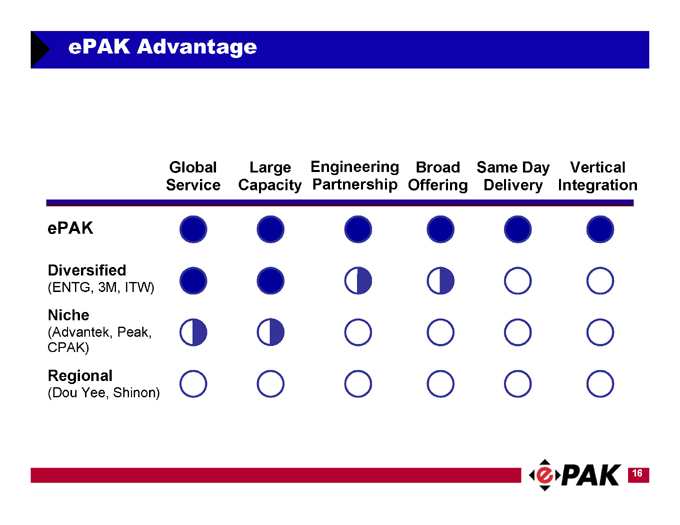

ePAK Advantage

Global | Large | Engineering | Broad | Same Day | Vertical | |||||

Service | Capacity | Partnership | Offering | Delivery | Integration |

ePAK

Diversified

(ENTG, 3M, ITW)

Niche

(Advantek, Peak,

CPAK)

Regional

(Dou Yee, Shinon)

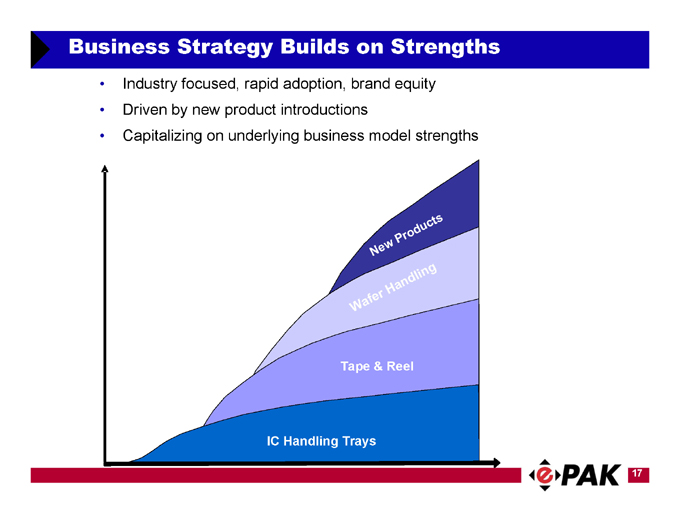

Business Strategy Builds on Strengths

Industry focused, rapid adoption, brand equity

Driven by new product introductions

Capitalizing on underlying business model strengths

New Products

Wafer Handling

Tape & Reel

IC Handling Trays

Latest Growth Driver, Wafer Handling

Entered in 2005

5% of TAM

Largest ePAK performance driver

Sales: 2005 = 12%, 2006 = 22%, Q1 2007 = 38%

50 |

| - 60% gross margin range |

Historically dominated by Entegris (80% of TAM)

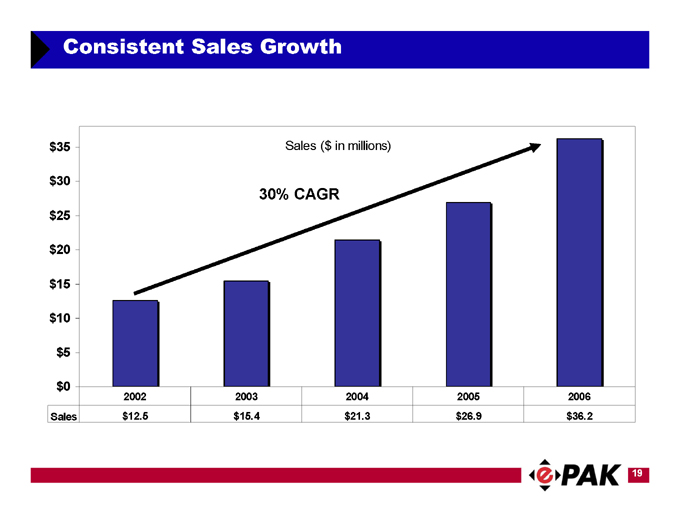

Consistent Sales Growth

$35 Sales ($ in millions)

$30

30% CAGR

$25

$20

$15

$10

$5

$0

2002 2003 2004 2005 2006

Sales $12.5 $15.4 $21.3 $26.9 $36.2

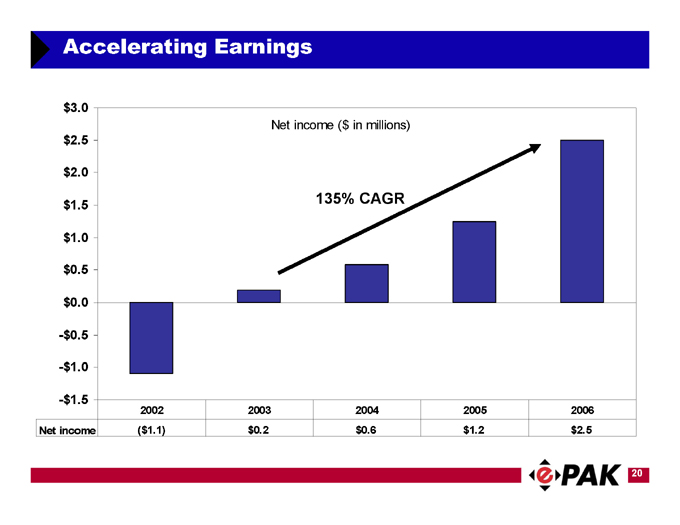

Accelerating Earnings

$3.0

Net income ($ in millions)

$2.5

$2.0

$1.5 135% CAGR

$1.0

$0.5

$0.0

-$0.5

-$1.0

-$1.5

2002 2003 2004 2005 2006

Net income($1.1) $0.2 $0.6 $1.2 $2.5

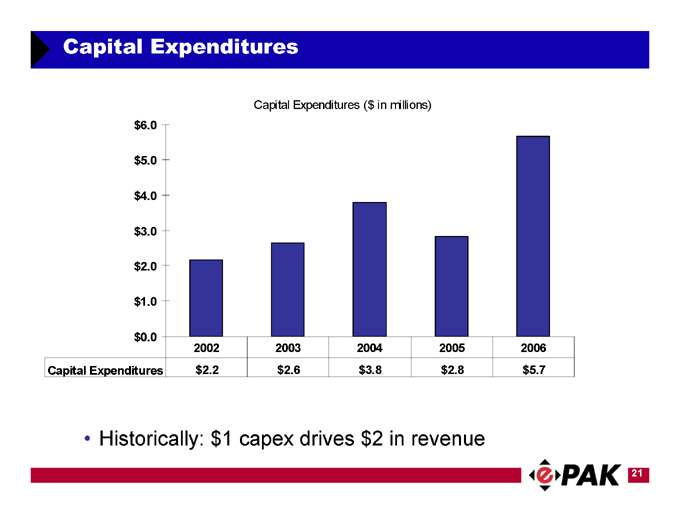

Capital Expenditures

Capital Expenditures ( $ in millions)

$6.0

$5.0

$4.0

$3.0

$2.0

$1.0

$0.0

2002 2003 2004 2005 2006

Capital Expenditures $2.2 $2.6 $3.8 $2.8 $5.7

Historically: $1 capex drives $2 in revenue

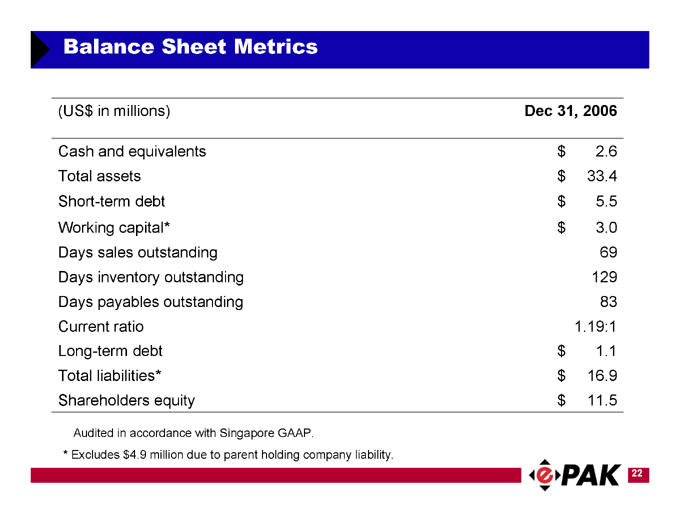

Balance Sheet Metrics

(US$ in millions) |

| Dec 31, 2006 | |

Cash and equivalents | $ | 2.6 | |

Total assets | $ | 33.4 | |

Short-term debt | $ | 5.5 | |

Working capital* | $ | 3.0 | |

Days sales outstanding |

| 69 | |

Days inventory outstanding |

| 129 | |

Days payables outstanding |

| 83 | |

Current ratio |

| 1.19:1 | |

Long-term debt | $ | 1.1 | |

Total liabilities* | $ | 16.9 | |

Shareholders equity | $ | 11.5 |

Audited in accordance with Singapore GAAP.

* Excludes $4.9 million due to parent holding company liability.

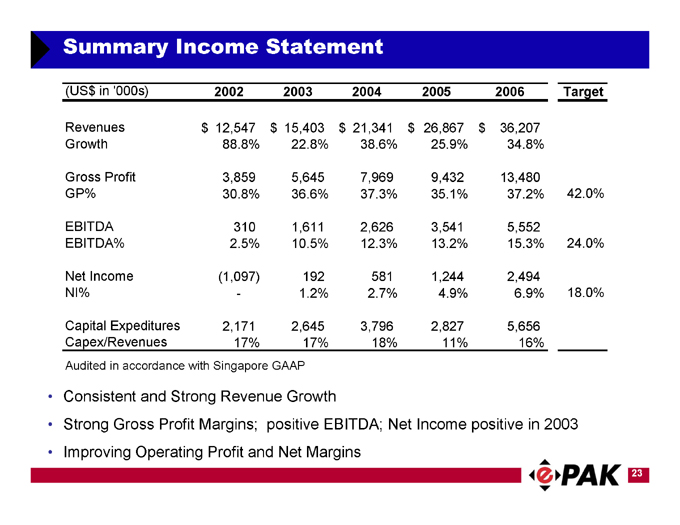

Summary Income Statement

(US$ in ‘000s) |

| 2002 |

|

| 2003 |

|

| 2004 |

|

| 2005 |

|

| 2006 |

| Target |

| ||||||

Revenues | $ | 12,547 |

| $ | 15,403 |

| $ | 21,341 |

| $ | 26,867 |

| $ | 36,207 |

| ||||||||

Growth |

| 88.8 | % |

| 22.8 | % |

| 38.6 | % |

| 25.9 | % |

| 34.8 | % | ||||||||

Gross Profit |

| 3,859 |

|

| 5,645 |

|

| 7,969 |

|

| 9,432 |

|

| 13,480 |

| ||||||||

GP% |

| 30.8 | % |

| 36.6 | % |

| 37.3 | % |

| 35.1 | % |

| 37.2 | % | 42.0 | % | ||||||

EBITDA |

| 310 |

|

| 1,611 |

|

| 2,626 |

|

| 3,541 |

|

| 5,552 |

| ||||||||

EBITDA% |

| 2.5 | % |

| 10.5 | % |

| 12.3 | % |

| 13.2 | % |

| 15.3 | % | 24.0 | % | ||||||

Net Income |

| (1,097 | ) |

| 192 |

|

| 581 |

|

| 1,244 |

|

| 2,494 |

| ||||||||

NI% |

| — |

|

| 1.2 | % |

| 2.7 | % |

| 4.9 | % |

| 6.9 | % | 18.0 | % | ||||||

Capital Expeditures |

| 2,171 |

|

| 2,645 |

|

| 3,796 |

|

| 2,827 |

|

| 5,656 |

| ||||||||

Capex/Revenues |

| 17 | % |

| 17 | % |

| 18 | % |

| 11 | % |

| 16 | % |

Audited in accordance with Singapore GAAP

Consistent and Strong Revenue Growth

Strong Gross Profit Margins; positive EBITDA; Net Income positive in 2003

Improving Operating Profit and Net Margins

Use of Proceeds

Increase capacity to accelerate growth

New product development

– High purity silicon handling

– High density disk drive

– Customer driven

Acquisition candidates

– Semi materials space: $24B, highly fragmented

– Targets: inefficient business models, high cost structures

Amalgamation/Redomicile in Bermuda

Surviving company ePAK International Limited

Bermuda registered corporation

All common stock and warrants outstanding exchanged 1:1

Tax efficient corporate structure

Preserves capital and retained earnings where they are most efficiently deployed

Nasdaq listed, prospective ticker EPAK

Investment Summary

Leading full service supplier of semiconductor transfer and handling products

Central, PRC-based operations led by veteran semiconductor industry team

Accelerating revenue and earnings growth

Advanced low cost manufacturing

Consistent market growth, low volatility

Multiple opportunities for large scale growth

Contact Information

Ascend Acquisition Corporation

Don K. Rice, Chairman and CEO

435 Devon Park Drive, Bldg. 400

Wayne, PA 19087

Phone: 610-519-1336

don@ascendgrowth.com

www.ascendgrowth.com

e.PAK Resources (S) Pte. Ltd.

Steve Dezso, CEO

4926 Spicewood Springs, #200

Austin, TX 78759

Phone: 512-231-8083

steve.dezso@epak.com

www.epak.com

Investor Relations

Crocker Coulson, President

CCG Elite

1325 Avenue of the Americas, Suite 2800

New York, NY 10019

Phone: 646-213-1915

crocker.coulson@ccgir.com

www.ccgir.com