Invesco CurrencyShares Canadian Dollar Trust (FXC)

Filed: 1 Nov 18, 8:27am

Filed pursuant to Rule 424(b)(3)

Registration No. 333-227849

5,150,000 Shares

Canadian Dollar Shares

|

| |||

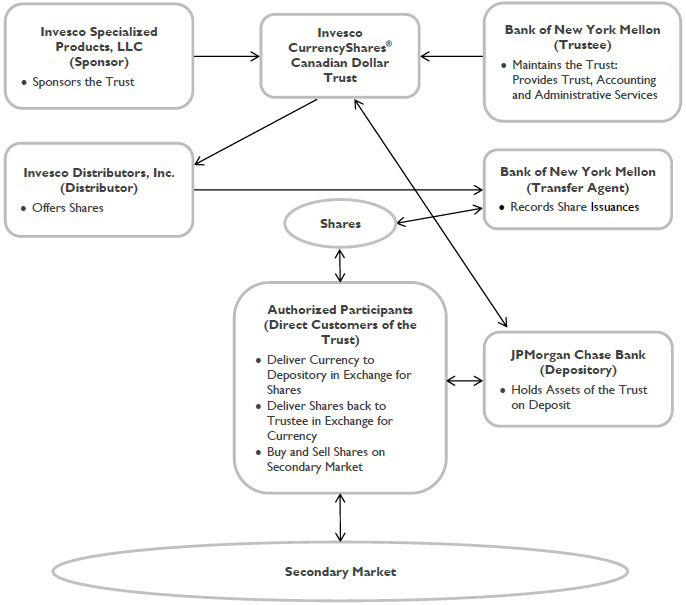

The Invesco CurrencyShares® Canadian Dollar Trust (Trust) issues Canadian Dollar Shares (Shares) that represent units of fractional undivided beneficial interest in, and ownership of, the Trust. Invesco Specialized Products, LLC is the sponsor of the Trust (Sponsor) and may be deemed the “issuer” of the Shares pursuant to Section 2(a)(4) of the Securities Act of 1933, as amended (the Securities Act). The Bank of New York Mellon is the trustee of the Trust (Trustee), JPMorgan Chase Bank, N.A., London Branch, is the depository for the Trust (Depository), and Invesco Distributors, Inc. is the distributor for the Trust (Distributor). The Trust intends to issue additional Shares on a continuous basis through the Trustee.

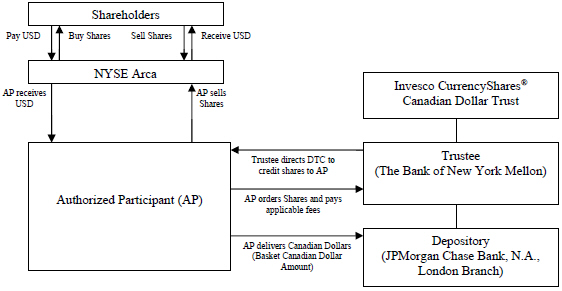

The Shares may be purchased from the Trust only in one or more blocks of 50,000 Shares, as described in “Creation and Redemption of Shares.” A block of 50,000 Shares is called a Basket. The Trust issues Shares in Baskets on a continuous basis to certain authorized participants (Authorized Participants) as described in “Plan of Distribution.” Each Basket, when created, is offered and sold to an Authorized Participant at a price in Canadian Dollars equal to the net asset value (NAV) of 50,000 Shares on the day that the order to create the Basket is accepted by the Trustee.

The Shares are offered and sold to the public by Authorized Participants at varying prices in U.S. Dollars (USD) determined by reference to, among other things, the market price of the Canadian Dollar and the trading price of the Shares on NYSE Arca, Inc. (NYSE Arca) at the time of each sale. Authorized Participants will not receive from the Trust, the Sponsor or any of their affiliates, any fee or other compensation in connection with the sale of Shares. Authorized Participants may receive commissions or fees from investors who purchase Shares through their commission- orfee-based brokerage accounts.

The Shares are listed and trade on NYSE Arca under the symbol “FXC.” The Shares may also trade in other markets, but the Sponsor has not sought to have the Shares listed by any other market.

Investing in the Shares involves significant risks. See “Risk Factors,” starting on page 6.

Neither the Securities and Exchange Commission (SEC) nor any state securities commission has approved or disapproved of the securities offered in this prospectus, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The Shares are neither interests in nor obligations of the Sponsor, the Trustee, the Depository or the Distributor.

Neither the Shares nor the Trust’s two deposit accounts maintained at the Depository and the Canadian Dollars deposited in them are deposits insured against loss by the Federal Deposit Insurance Corporation (FDIC), any other federal agency of the United States or the Financial Services Compensation Scheme of England.

The date of this prospectus is November 1, 2018.

This prospectus contains information you should consider when making an investment decision about the Shares. You may rely on the information contained in this prospectus or incorporated by reference in this prospectus. The Trust and the Sponsor have not authorized any person to provide you with different information and, if anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell the Shares in any jurisdiction where the offer or sale of the Shares is not permitted.

The Shares are not registered for public sale in any jurisdiction other than the United States.

| 1 | ||||

| 2 | ||||

| 6 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

| 13 | ||||

| 13 | ||||

| 15 | ||||

| 16 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 20 | ||||

Invesco CurrencyShares® Canadian Dollar Trust Organizational Chart | 21 | |||

| 22 | ||||

| 22 | ||||

| 24 | ||||

| 28 | ||||

| 34 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 40 | ||||

| 41 |

Authorized Participants may be subject to the prospectus delivery requirements of the Securities Act when effecting transactions in the Shares. See “Plan of Distribution.”

This prospectus summarizes certain documents and other information in a manner the Sponsor believes to be accurate. The information contained in the sections captioned “Overview of the Foreign Exchange Industry,” “The Canadian Dollar” and “Investment Attributes of the Trust” is based on information obtained from sources that the Sponsor believes to be reliable. In making an investment decision, you must rely on your own examination of the Trust, the foreign exchange market, the market for the Canadian Dollar, the terms of the offering and the Shares, including the merits and risks involved.

This is a summary of the prospectus. You should read the entire prospectus, including “Risk Factors” beginning on page 6 and the information incorporated by reference in this prospectus, before making an investment decision about the Shares. See “Glossary of Terms” beginning on page 11 for a description of certain terms used in this prospectus.

TRUST STRUCTURE

The Trust is a grantor trust formed under the laws of the State of New York pursuant to the Depositary Trust Agreement. The Trust holds Canadian Dollars and from time to time issues Baskets in exchange for deposits of Canadian Dollars and distributes Canadian Dollars in connection with redemptions of Baskets. The investment objective of the Trust is for the Shares to reflect the price in USD of the Canadian Dollar. Earning income for Shareholders is not the objective of the Trust. Whether investors earn income primarily depends on the relative value of the Canadian Dollar and the USD. If the Canadian Dollar appreciates relative to the USD and a Shareholder sells Shares, the Shareholder will earn income. If the Canadian Dollar depreciates relative to the USD and a Shareholder sells Shares, the Shareholder will incur a loss.

The Sponsor believes that, for many investors, the Shares represent a cost-effective investment in Canadian Dollars. The Shares represent units of fractional undivided beneficial interest in, and ownership of, the Trust. The Shares are listed and trade on NYSE Arca under the symbol “FXC.” The Shares may also trade in other markets, but the Sponsor has not sought to have the Shares listed by any other market.

The Sponsor, Invesco Specialized Products, LLC, a Delaware limited liability company, established the Trust and is responsible for registering the Shares. The Sponsor generally oversees the performance of the Trustee and the Trust’s principal service providers, but does not exerciseday-to-day oversight over the Trustee or the Trust’s service providers. The Sponsor may remove the Trustee if any of various events occur. See “Description of the Depositary Trust Agreement — The Trustee — Resignation, discharge or removal of trustee; successor trustees” for more information.

The Sponsor maintains a public website on behalf of the Trust containing information about the Trust and the Shares. The internet address of the Trust’s website is www.invesco.com/etfs. This internet address is provided here only as a convenience to you; the information contained on or connected to the Trust’s website is not considered part of this prospectus. The general role and responsibilities of the Sponsor are discussed further under “The Sponsor.”

The Trustee is The Bank of New York Mellon, a banking corporation formed under the laws of the State of New York with trust powers. The Trustee is generally responsible for theday-to-day administration of the Trust. This includes calculating the NAV of the Trust and the NAV per Share each business day, paying the Trust’s expenses (which are accrued daily but paid monthly), including withdrawing the Trust’s Canadian Dollars, if needed, receiving and processing orders from Authorized Participants to create and redeem Baskets and coordinating the processing of such orders with the Depository and DTC. The general role, responsibilities and regulation of the Trustee are further described under “The Trustee.”

The Depository is JPMorgan Chase Bank, N.A., London Branch. The Depository and the Trustee have elected the laws of England to govern the Deposit Account Agreement between them. The Depository accepts Canadian Dollars deposited with it by Authorized Participants in connection with the creation of Baskets. The Depository facilitates the transfer of Canadian Dollars into and out of the Trust through the two deposit accounts maintained with it by the Trust. The Depository may pay interest on the primary deposit account but does not pay interest on the secondary deposit account. Interest on the primary deposit account, if any, accrues daily and is paid monthly. The material terms of the Depositary Trust Agreement are discussed in greater detail in “Description of the Depositary Trust Agreement.” The general role, responsibilities and regulation of the Depository and the two deposit accounts are further described under “The Depository” and “Description of the Deposit Account Agreement.”

Detailed descriptions of certain specific rights and duties of the Trustee and the Depository are set forth under “Description of the Shares,” “Description of the Depositary Trust Agreement” and “Description of the Deposit Account Agreement.”

The Distributor, Invesco Distributors, Inc., is a corporation formed under the laws of the State of Delaware. The Distributor assists the Sponsor in marketing the Shares. Specifically, the Distributor prepares marketing materials regarding the Shares, including the content of the Trust’s website, executes the marketing plan for the Trust and provides strategic and tactical research on the foreign exchange markets, in each case in compliance with applicable laws and regulations. The Distributor and the Sponsor are affiliates of one another. There is no written agreement between them, and no compensation is paid by the Sponsor to the Distributor in connection with services performed by the Distributor for the Trust. See “The Distributor” for more information.

1

INVESTMENT ATTRIBUTES OF THE TRUST

The investment objective of the Trust is for the Shares to reflect the price in USD of the Canadian Dollar. The Shares are intended to provide institutional and retail investors with a simple, cost-effective means of gaining investment benefits similar to those of holding Canadian Dollars. The costs of purchasing Shares should not exceed the costs associated with purchasing any other publicly-traded equity securities. The Shares are an investment that is:

Easily Accessible. Investors are able to access the market for Canadian Dollars through a traditional brokerage account. The Shares are bought and sold on NYSE Arca like any other exchange-listed security.

Exchange-Traded. Because they are traded on NYSE Arca, the Shares will provide investors with an efficient means of implementing investment tactics and strategies that involve Canadian Dollars. NYSE Arca-listed securities are eligible for margin accounts. Accordingly, investors are able to purchase and hold Shares with borrowed money to the extent permitted by law.

Transparent. The Shares are backed by the assets of the Trust, which does not hold or use derivative products. The value of the holdings of the Trust is reported on the Trust’s website, www.invesco.com/etfs, every business day.

Investing in the Shares will not insulate the investor from price volatility or other risks. Further, the ratio of Canadian Dollars to Shares may decrease due to withdrawals made to pay Trust expenses in the event that the interest income of the Trust is not sufficient to cover the entirety of the Trust expenses. See “Risk Factors” and “The Depository.”

PRINCIPAL OFFICES

The principal offices of the Sponsor and the Trust are the offices of Invesco Specialized Products, LLC at 3500 Lacey Road, Suite 700, Downers Grove, Illinois 60515, and the principal offices of the Distributor are the offices of Invesco Distributors, Inc. at 11 Greenway Plaza, Suite 1000, Houston, Texas 77046. The telephone number of Invesco Specialized Products, LLC at its address is (800)983-0903. None of the Sponsor, the Trust or the Distributor owns or leases any other real estate. The Trustee has an office at 2 Hanson Place, Brooklyn, New York 11217. The Depository is located at 125 London Wall, London, EC2Y 5AJ, United Kingdom.

| Offering | The Shares represent units of fractional undivided beneficial interest in, and ownership of, the Trust. | |

| Use of proceeds | The proceeds received by the Trust from the issuance and sale of Baskets are Canadian Dollars. In accordance with the Depositary Trust Agreement, during the life of the Trust these proceeds will only be (1) owned by the Trust and held by the Depository, (2) disbursed or sold as needed to pay the Trust’s expenses and (3) distributed to Authorized Participants upon the redemption of Baskets. | |

| NYSE Arca symbol | FXC | |

| CUSIP | 46138T104 | |

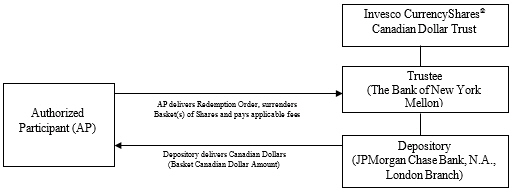

| Creation and redemption | The Trust creates and redeems the Shares on a continuous basis, but only in Baskets. A Basket is a block of 50,000 Shares. The creation and redemption of Baskets requires the delivery to the Trust or the distribution by the Trust of the amount of Canadian Dollars represented by the Baskets being created or redeemed, the amount of which is based on the combined NAV per Share of the number of Shares included in the Baskets being created or redeemed. The amount of Canadian Dollars required to create a Basket or to be delivered | |

2

| upon the redemption of a Basket may gradually decrease over time if the Trust’s Canadian Dollars are withdrawn to pay the Trust’s expenses. See “Investment Attributes of the Trust — Trust Expenses.” Baskets may be created or redeemed only by Authorized Participants. Authorized Participants pay a transaction fee for each order to create or redeem Baskets and may sell to other investors the Shares included in the Baskets that they create. See “Creation and Redemption of Shares” for more details. | ||

| Interest on deposits | JPMorgan Chase Bank, N.A., London Branch, maintains two Canadian Dollar-denominated, demand deposit accounts for the Trust: a primary deposit account that may earn interest and a secondary deposit account that does not earn interest. The secondary deposit account is used to account for interest received and paid on creations and redemptions of Baskets. The secondary deposit account is also used to account for interest that may be earned on the primary deposit account, if any, to pay Trust expenses and to distribute any excess interest to Shareholders on a monthly basis. Interest on the primary deposit account, if any, accrues daily and is paid monthly. The Depository may change the rate at which interest accrues, including reducing the interest rate to zero or below zero, based upon changes in market conditions or the Depository’s liquidity needs. The Depository will notify the Sponsor of the interest rate applied each business day after the close of such business day.

The Sponsor discloses the interest rate on the Trust’s website. If the Sponsor believes that the interest rate paid by the Depository is not competitive, the Sponsor’s sole recourse will be to remove the Depository by terminating the Deposit Account Agreement and closing the accounts. See “Description of the Deposit Account Agreement.” Neither the Trustee nor the Sponsor has the power or authority to deposit the Trust’s Canadian Dollars with any other person, entity or account. Interest earned on the deposited Canadian Dollars, if any, is used to pay the Trust’s expenses. Any excess interest will be distributed to Shareholders monthly. Such interest is not expected to form a significant part of the Shareholders’ investment return. If the Trust’s expenses exceed interest earned, the Trustee will withdraw Canadian Dollars held by the Trust to pay the excess, thereby reducing the number of Canadian Dollars per Share. The payment of expenses by the Trust is a taxable event to Shareholders. See “United States Federal Tax Consequences — Taxation of U.S. Shareholders.”

Neither the Shares nor the Deposit Accounts and the Canadian Dollars deposited in them are deposits insured against loss by the FDIC, any other federal agency of the United States or the Financial Services Compensation Scheme of England. | |

| Net Asset Value | The NAV of the Trust is the aggregate value, expressed in USD, of the Trust’s assets, less its liabilities (which include estimated accrued but unpaid fees and expenses). The Trustee calculates, and the Sponsor publishes, the Trust’s net asset value (NAV) each business day. To calculate the NAV, the Trustee adds to the amount of Canadian Dollars in the Trust at the end of the preceding business day accrued but unpaid interest, if any, Canadian Dollars receivable under pending purchase orders and the value of other Trust assets, and subtracts the accrued but unpaid Sponsor’s fee, Canadian Dollars payable under pending redemption orders and other Trust expenses and liabilities, if any. The NAV is expressed in USD based on the Closing Spot Rate as determined by The WM Company at 4:00 PM (London time / London fixing) on each day that NYSE Arca is open for regular trading. If, on a particular evaluation day, the Closing Spot Rate has not been determined and announced by 6:00 PM (London time), then the most recent determination of the Closing Spot Rate by The WM Company shall be used to determine the NAV of the Trust unless the Trustee, in consultation with the Sponsor, determines that such price is inappropriate to use as the basis for such valuation. | |

3

| In the event that the Trustee and the Sponsor determine that the most recent determination of the Closing Spot Rate is not an appropriate basis for valuation of the Trust’s Canadian Dollars, the Trustee and the Sponsor shall determine an alternative basis for such evaluation to be employed by the Trustee. Such an alternative basis may include reference to otherexchange-traded securities that reflect the value of the Canadian Dollar relative to the USD. The use of any alternative basis to determine NAV would be disclosed on the Trust’s website. The Trustee also determines the NAV per Share, which equals the NAV of the Trust divided by the number of outstanding Shares. The Sponsor publishes the NAV and NAV per Share on each day that NYSE Arca is open for regular trading on the Trust’s website, www.invesco.com/etfs. | ||

| Trust expenses | The Trust’s only ordinary recurring expense is the Sponsor’s fee. The Sponsor is obligated under the Depositary Trust Agreement to assume and pay the following administrative and marketing expenses of the Trust: the Trustee’s monthly fee, typical maintenance and transaction fees of the Depository, SEC registration fees, printing and mailing costs, audit fees and expenses, up to $100,000 per annum in legal fees and expenses, applicable license fees and NYSE Arca listing fees. The Trust may incur additional expenses in certain other circumstances. These additional expenses include expenses not assumed by the Sponsor, expenses resulting from negative interest rates, taxes and governmental charges, expenses and costs of any extraordinary services performed by the Trustee or the Sponsor on behalf of the Trust or action taken by the Trustee or the Sponsor to protect the Trust or the interests of Shareholders, indemnification of the Sponsor under the Depositary Trust Agreement and legal fees and expenses in excess of $100,000 per year. If these additional expenses are incurred, the Trust will be required to pay these expenses by withdrawing deposited Canadian Dollars and the amount of Canadian Dollars represented by a Share will decline at such time. Accordingly, the Shareholders will effectively bear the cost of these other expenses, if incurred. Although the Sponsor cannot definitively state the frequency or magnitude of such expenses, the Sponsor predicts that they will occur infrequently, if at all. See “Description of the Depositary Trust Agreement — Expenses of the Trust.”

The Sponsor’s fee accrues daily at an annual nominal rate of 0.40% of the Canadian Dollars in the Trust (including all unpaid interest but excluding unpaid fees, each as accrued through the immediately preceding day) and is paid monthly. To pay the Sponsor’s fee and any other Trust expenses that have been incurred each month, the Trustee first withdraws Canadian Dollars the Trust has earned as interest, if any.

If that is not sufficient to pay the Trust’s expenses, then the Trustee will withdraw deposited Canadian Dollars as needed. See “Investment Attributes of the Trust — Trust Expenses” and “Description of the Depositary Trust Agreement — Expenses of the Trust.” The payment of expenses in Canadian Dollars and the conversion of Canadian Dollars to USD, if required to pay expenses of the Trust, are generally taxable events to U.S. Shareholders. See “United States Federal Tax Consequences — Taxation of U.S. Shareholders.” The Sponsor does not anticipate anynon-ordinary recurring expenses that will be paid from the Trust. | |

4

| Termination events | The Trustee will terminate the Trust if any of the following events occur:

• the Sponsor has given notice of resignation or is unable to perform its duties or becomes bankrupt or insolvent and the Trustee does not appoint a successor sponsor or agree to act as sponsor;

• Shareholders holding at least 75% of the outstanding Shares notify the Trustee that they elect to terminate the Trust;

• the Depository resigns or is removed; or

• the Trustee receives notice from the IRS or from counsel for the Trust or the Sponsor that the Trust fails to qualify for treatment, or will not be treated, as a grantor trust under the Internal Revenue Code of 1986, as amended (Internal Revenue Code).

The Sponsor may, in its sole discretion, direct the Trustee to terminate the Trust if any of the following events occur:

• the Shares are delisted from NYSE Arca and are not listed for trading on another U.S. national securities exchange within five business days from the date the Shares are delisted;

• the SEC determines that the Trust is an investment company under the Investment Company Act;

• the NAV of the Trust remains less than $100 million for 30 consecutive business days;

• all of the Trust’s assets are sold;

• the aggregate market capitalization of the Trust, based on the closing price for the Shares, remains less than $300 million for five consecutive trading days; or

• DTC stops providing book-entry settlement services for the Shares.

If the Trustee notifies the Sponsor of the Trustee’s election to resign and the Sponsor does not appoint a successor trustee within 60 days, the Trustee may terminate the Trust.

The Trust will terminate on June 8, 2046 if it has not been terminated prior to that date.

Upon termination of the Trust and surrender of Shares by the Shareholders, Shareholders will receive the amount of Canadian Dollars represented by their Shares. If, however, a Shareholder surrenders its Shares 90 days or more after the termination of the Trust, it will receive a distribution in USD after the Trustee has sold the Trust’s Canadian Dollars and has paid or made provision for the Trust’s liabilities. See “Description of the Trust Agreement — Termination of the Trust.” | |

| Authorized Participants | An Authorized Participant is a DTC Participant that is a registered broker-dealer or other securities market participant such as a bank or other financial institution that is not required to register as a broker-dealer to engage in securities transactions and has entered into a Participant Agreement with the Trustee. Only Authorized Participants may place orders to create or redeem Baskets. The Participant Agreement provides the procedures for the creation and redemption of Baskets and for the delivery of Canadian Dollars required for creation or redemption. A list of the current Authorized Participants can be obtained from the Trustee or the Sponsor. See “Creation and Redemption of Shares” for more details. | |

| Shareholders trading via NYSE Arca | A Shareholder who buys or sells Shares from, to, or through a broker-dealer should expect to be charged a commission by the broker-dealer for effecting the transaction. Investors are encouraged to review the terms of their brokerage accounts for details on applicable commissions or charges. | |

| Clearance and settlement | All Shares are evidenced by one or more global certificates issued by the Trustee to DTC. The Shares are available only in book-entry form. Shareholders may hold their Shares through DTC, if they are DTC Participants, or through Authorized Participants or Indirect Participants. | |

5

You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included in this prospectus, including the Trust’s financial statements and the related notes. See “Glossary of Terms” beginning on page 11 for a description of certain terms used in this prospectus.

The value of the Shares relates directly to the value of the Canadian Dollars held by the Trust. Fluctuations in the price of the Canadian Dollar could materially and adversely affect the value of the Shares.

The Shares are designed to reflect the price of the Canadian Dollar, plus accumulated interest, if any, less the Trust’s expenses. Several factors may affect the price of the Canadian Dollar, including:

| • | Sovereign debt levels and trade deficits; |

| • | Domestic and foreign inflation rates and interest rates and investors’ expectations concerning those rates; |

| • | Currency exchange rates; |

| • | Investment and trading activities of mutual funds, hedge funds and currency funds; and |

| • | Global or regional political, economic or financial events and situations. |

In addition, the Canadian Dollar may not maintain its long-term value in terms of purchasing power in the future. When the price of the Canadian Dollar declines, the Sponsor expects the price of a Share to decline as well.

The USD/Canadian Dollar exchange rate, like foreign exchange rates in general, can be volatile and difficult to predict. This volatility could materially and adversely affect the performance of the Shares.

Foreign exchange rates are influenced by the factors identified in the preceding risk factor and may also be influenced by: changing supply and demand for a particular currency; monetary policies of governments (including exchange control programs, restrictions on local exchanges or markets and limitations on foreign investment in a country or on investment by residents of a country in other countries); changes in balances of payments and trade; trade restrictions; and currency devaluations and revaluations. Also, governments from time to time intervene in the currency markets, directly and by regulation, in order to influence prices directly. These events and actions are unpredictable. The resulting volatility in the USD/Canadian Dollar exchange rate could materially and adversely affect the performance of the Shares.

Changes to United States tariff and trade policies may increase the volatility of foreign exchange rates. This volatility could materially and adversely affect the performance of the Shares.

There have been ongoing discussions and commentary regarding potential significant changes to United States trade policies, treaties and tariffs. The current administration, along with Congress, has created significant uncertainty about the future relationship between the United States and other countries with respect to trade policies, treaties and tariffs. These developments, or the perception that any of them could occur, may have a material adverse effect on global economic conditions and the stability of global financial markets, and may increase the volatility of foreign exchange rates, including the USD/Canadian Dollar exchange rate. The resulting volatility could materially and adversely affect the performance of the Shares.

6

If interest earned by the Trust does not exceed the Trust’s expenses, the Trustee will withdraw Canadian Dollars from the Trust to pay these excess expenses, which will reduce the amount of Canadian Dollars represented by each Share on an ongoing basis and may result in adverse tax consequences for Shareholders.

Each outstanding Share represents a fractional, undivided interest in the Canadian Dollars held by the Trust. Recently, the amount of interest earned by the Trust has not exceeded the Trust’s expenses; accordingly, the Trustee has been required to withdraw Canadian Dollars from the Trust to pay these excess expenses. As long as the amount of interest earned does not exceed expenses, the amount of Canadian Dollars represented by each Share will gradually decline over time. This is true even if additional Shares are issued in exchange for additional deposits of Canadian Dollars into the Trust, as the amount of Canadian Dollars required to create Shares will proportionately reflect the amount of Canadian Dollars represented by the Shares outstanding at the time of creation. Assuming a constant Canadian Dollar price, if expenses exceed interest earned, the trading price of the Shares will gradually decline relative to the price of the Canadian Dollar as the amount of Canadian Dollars represented by the Shares gradually declines. In this event, the Shares will only maintain their original price if the price of the Canadian Dollar increases. There is no guarantee that interest earned by the Trust in the future will exceed the Trust’s expenses.

Investors should be aware that a gradual decline in the amount of Canadian Dollars represented by the Shares may occur regardless of whether the trading price of the Shares rises or falls in response to changes in the price of the Canadian Dollar. The estimated ordinary operating expenses of the Trust, which accrue daily, are described in “Investment Attributes of the Trust – Trust Expenses.”

The payment of expenses by the Trust will result in a taxable event to Shareholders. To the extent Trust expenses exceed interest paid to the Trust, a gain or loss may be recognized by Shareholders depending on the tax basis of the tendered Canadian Dollars. See “United States Federal Tax Consequences – Taxation of U.S. Shareholders” for more information.

The interest rate paid by the Depository, if any, may not be the best rate available. If the Sponsor determines that the interest rate is inadequate, then its sole recourse is to remove the Depository and terminate the Deposit Accounts.

The Depository is committed to endeavor to pay a competitive interest rate on the balance of Canadian Dollars in the primary deposit account of the Trust, but there is no guarantee of the amount of interest that will be paid, if any, on this account. Interest on the primary deposit account, if any, accrues daily and is paid monthly. The Depository may change the rate at which interest accrues, including reducing the interest rate to zero or below zero, based upon changes in market conditions or the Depository’s liquidity needs. The Depository notifies the Sponsor of the interest rate applied each business day after the close of such business day. The Sponsor discloses the current interest rate on the Trust’s website. If the Sponsor believes that the interest rate paid by the Depository is not adequate, the Sponsor’s sole recourse is to remove the Depository and terminate the Deposit Accounts. The Depository is not paid a fee for its services to the Trust; rather, it generates income or loss based on its ability to earn a “spread” or “margin” over the interest it pays to the Trust by using the Trust’s Canadian Dollars to make loans or in other banking operations. For these reasons, you should not expect that the Trust will be paid the best available interest rate at any time or over time.

If the Trust incurs expenses in USD, the Trust would be required to sell Canadian Dollars to pay these expenses. The sale of the Trust’s Canadian Dollars to pay expenses in USD at a time of low Canadian Dollar prices could adversely affect the value of the Shares.

The Trustee will sell Canadian Dollars held by the Trust to pay Trust expenses, if any, incurred in USD, irrespective of then-current Canadian Dollar prices. The Trust is not actively managed and no attempt will be made to buy or sell Canadian Dollars to protect against or to take advantage of fluctuations in the price of the Canadian Dollar. Consequently, if the Trust incurs expenses in USD, the Trust’s Canadian Dollars may be sold at a time when the Canadian Dollar price is low, resulting in a negative effect on the value of the Shares.

The Deposit Accounts are not entitled to payment at any office of JPMorgan Chase Bank, N.A. located in the United States.

The federal laws of the United States prohibit banks located in the United States from paying interest on unrestricted demand deposit accounts. Therefore, payments out of the Deposit Accounts will be payable only at the London branch of JPMorgan Chase Bank, N.A., located in England. The Trustee will not be entitled to demand payment of these accounts at any office of JPMorgan Chase Bank, N.A. that is located in the United States. JPMorgan Chase Bank, N.A. will not be required to repay the deposit if its London branch cannot repay the deposit due to an act of war, insurrection or civil strife or an action by a foreign government or instrumentality (whether de jure or de facto) in England.

7

Shareholders do not have the protections associated with ownership of a demand deposit account insured in the United States by the Federal Deposit Insurance Corporation or the protection provided for bank deposits under English law.

Neither the Shares nor the Deposit Accounts and the Canadian Dollars deposited in them are deposits insured against loss by the FDIC, any other federal agency of the United States or the Financial Services Compensation Scheme of England.

If the Depository becomes insolvent, its assets may not be adequate to satisfy a claim by the Trust or any Authorized Participant. In addition, in the event of the insolvency of the Depository, the U.S. bank of which it is a branch or any local cash correspondent holding the currency on deposit for the benefit of the Trust, there may be a delay and costs incurred in recovering the Canadian Dollars held in the Deposit Accounts.

Canadian Dollars deposited in the Deposit Accounts by an Authorized Participant are commingled with Canadian Dollars deposited by other Authorized Participants and are held by the Depository in either the primary deposit account or the secondary deposit account of the Trust. Canadian Dollars held in the Deposit Accounts are not segregated from the Depository’s other assets.

The Trust has no proprietary rights in or to any specific Canadian Dollars held by the Depository and will be an unsecured creditor of the Depository with respect to the Canadian Dollars held in the Deposit Accounts in the event of the insolvency of the Depository or the U.S. bank of which it is a branch. In the event the Depository, the U.S. bank of which it is a branch or any local cash correspondent holding the currency on deposit for the benefit of the Trust becomes insolvent, the Depository’s assets might not be adequate to satisfy a claim by the Trust or any Authorized Participant for the amount of Canadian Dollars deposited by the Trust or the Authorized Participant and, in such event, the Trust and any Authorized Participant will generally have no right in or to assets other than those of the Depository.

In the case of insolvency of the Depository or JPMorgan Chase Bank, N.A., the U.S. bank of which the Depository is a branch, a liquidator may seek to freeze access to the Canadian Dollars held in all accounts by the Depository, including the Deposit Accounts. In the case of insolvency of a local cash correspondent, a liquidator may seek to freeze access to the Canadian Dollars held in all accounts by such local cash correspondent, including the Deposit Accounts held by such cash correspondent. The Trust and the Authorized Participants could incur expenses and delays in connection with asserting their claims. These problems would be exacerbated by the fact that the Deposit Accounts are not held in the U.S. but instead are held at the London branch of a U.S. national bank or with a local cash correspondent, where they are subject to English and Canadian insolvency law. Further, under U.S. law, in the case of the insolvency of JPMorgan Chase Bank, N.A., the claims of creditors in respect of accounts (such as the Trust’s Deposit Accounts) that are maintained with an overseas branch of JPMorgan Chase Bank, N.A. or with a local cash correspondent will be subordinate to claims of creditors in respect of accounts maintained with JPMorgan Chase Bank, N.A. in the U.S., greatly increasing the risk that the Trust and the Trust’s beneficiaries would suffer a loss.

Shareholders do not have the protections associated with ownership of shares in an investment company registered under the Investment Company Act.

The Investment Company Act is designed to protect investors by preventing: insiders from managing investment companies to their benefit and to the detriment of public investors; the issuance of securities having inequitable or discriminatory provisions; the management of investment companies by irresponsible persons; the use of unsound or misleading methods of computing earnings and asset value; changes in the character of investment companies without the consent of investors; and investment companies from engaging in excessive leveraging. To accomplish these ends, the Investment Company Act requires the safekeeping and proper valuation of fund assets, restricts greatly transactions with affiliates, limits leveraging, and imposes governance requirements as a check on fund management.

The Trust is not registered as an investment company under the Investment Company Act and is not required to register under that act. Consequently, Shareholders do not have the regulatory protections afforded to investors in registered investment companies.

8

Shareholders do not have the rights enjoyed by investors in certain other financial instruments.

As interests in a grantor trust, the Shares have none of the statutory rights normally associated with the ownership of shares of a business corporation, including, for example, the right to bring “oppression” or “derivative” actions. Apart from the rights afforded to them by federal and state securities laws, Shareholders have only those rights relative to the Trust, the Trust property and the Shares that are set forth in the Depositary Trust Agreement. In this connection, the Shareholders have limited voting and distribution rights. They do not have the right to elect directors. See “Description of the Shares” for a description of the limited rights of the Shareholders.

The Shares may trade at a price which is at, above, or below the NAV per Share.

The NAV per Share fluctuates with changes in the market value of the Trust’s assets. The market price of Shares can be expected to fluctuate in accordance with changes in the NAV per Share, but also in response to market supply and demand. As a result, the Shares might trade at prices at, above or below the NAV per Share.

The Depository owes no fiduciary duties to the Trust or the Shareholders, is not required to act in their best interest and could resign or be removed by the Sponsor, which would trigger early termination of the Trust.

The Depository is not a trustee for the Trust or the Shareholders. As stated above, the Depository is not obligated to maximize the interest rate paid to the Trust. In addition, the Depository has no duty to continue to act as the depository of the Trust. The Depository can terminate its role as depository for any reason whatsoever upon 90 days’ notice to the Trust. If directed by the Sponsor, the Trustee must terminate the Depository. Such a termination might result, for example, if the Sponsor determines that the interest rate paid by the Depository is inadequate. In the event that the Depository was to resign or be removed, the Trust will be terminated.

Shareholders may incur significant fees upon the termination of the Trust.

The occurrence of any one of several events would either require the Trust to terminate or permit the Sponsor to terminate the Trust. For example, if the Depository were to resign or be removed, then the Sponsor would be required to terminate the Trust. Shareholders tendering their Shares within 90 days of the Trust’s termination will receive the amount of Canadian Dollars represented by their Shares. Shareholders may incur significant fees if they choose to convert the Canadian Dollars they receive to USD. See “Description of the Depositary Trust Agreement — Termination of the Trust” for more information about the termination of the Trust, including when the termination of the Trust may be triggered by events outside the direct control of the Sponsor, the Trustee or the Shareholders.

Redemption orders are subject to rejection by the Trustee under certain circumstances.

The Trustee will reject a redemption order if the order is not in proper form as described in the Participant Agreement or if the fulfillment of the order, in the opinion of its counsel, might be unlawful. Any such rejection could adversely affect a redeeming Shareholder. For example, the resulting delay would adversely affect the value of the Shareholder’s redemption distribution if the NAV were to decline during the delay. See “Creation and Redemption of Shares — Redemption Procedures — Suspension or rejection of redemption orders.” In the Depositary Trust Agreement, the Sponsor and the Trustee disclaim any liability for any loss or damage that may result from any such rejection.

Substantial sales of Canadian Dollars by the official sector could adversely affect an investment in the Shares.

The official sector consists of central banks, other governmental agencies and multi-lateral institutions that buy, sell and hold Canadian Dollars as part of their reserve assets. The official sector holds a significant amount of Canadian Dollars that can be mobilized in the open market. In the event that future economic, political or social conditions or pressures require members of the official sector to sell their Canadian Dollars simultaneously or in an uncoordinated manner, the demand for Canadian Dollars might not be sufficient to accommodate the sudden increase in the supply of Canadian Dollars to the market. Consequently, the price of the Canadian Dollar could decline, which would adversely affect an investment in the Shares.

Shareholders that are not Authorized Participants may only purchase or sell their Shares in secondary trading markets.

Only Authorized Participants may create or redeem Baskets through the Trust. All other investors that desire to purchase or sell Shares must do so through NYSE Arca or in other markets, if any, in which the Shares are traded.

9

The liability of the Sponsor and the Trustee under the Depositary Trust Agreement is limited and, except as set forth in the Depositary Trust Agreement, they are not obligated to prosecute any action, suit or other proceeding in respect of any Trust property.

The Depositary Trust Agreement provides that neither the Sponsor nor the Trustee assumes any obligation or is subject to any liability under the Trust Agreement to any Shareholder, except that they each agree to perform their respective obligations specifically set forth in the Depositary Trust Agreement without negligence or bad faith. Additionally, neither the Sponsor nor the Trustee is obligated to, although each may in its respective discretion, prosecute any action, suit or other proceeding in respect of any Trust property. The Depositary Trust Agreement does not confer upon Shareholders the right to prosecute any such action, suit or other proceeding.

The Depositary Trust Agreement may be amended to the detriment of Shareholders without their consent.

The Sponsor and the Trustee may amend most provisions (other than those addressing core economic rights) of the Depositary Trust Agreement without the consent of any Shareholder. Such an amendment could impose or increase fees or charges borne by the Shareholders. Any amendment that increases fees or charges (other than taxes and other governmental charges, registration fees or other expenses), or that otherwise prejudices any substantial existing rights of Shareholders, will not become effective until 30 days after written notice is given to Shareholders.

The License Agreement with The Bank of New York Mellon may be terminated by The Bank of New York Mellon in the event of a material breach. Termination of the License Agreement might lead to early termination and liquidation of the Trust.

The Bank of New York Mellon and the Sponsor have entered into a License Agreement granting the Sponsor anon-exclusive, personal andnon-transferable license to certain patent applications made by The Bank of New York Mellon covering systems and methods for securitizing a commodity for the life of such patents and patent applications. The license grant is solely for the purpose of allowing the Sponsor to establish, operate and market a currency-based securities product based solely on the securitization, in whole or in part, of a singlenon-U.S. currency. The License Agreement provides that either party may provide notice of intent to terminate the License Agreement in the event the other party commits a material breach. If the License Agreement is terminated and one or more of The Bank of New York Mellon’s patent applications issue as patents, then The Bank of New York Mellon may claim that the operation of the Trust violates its patent or patents and seek an injunction forcing the Trust to cease operation and the Shares to cease trading. In that case, the Trust might be forced to terminate and liquidate, which would adversely affect Shareholders.

Current discussions between the SEC and PricewaterhouseCoopers LLP regarding PricewaterhouseCoopers LLP’s independence could have potentially adverse consequences for the Trust.

PricewaterhouseCoopers LLP informed the Trust that it has identified an issue related to its independence under Rule2-01(c)(1)(ii)(A) of RegulationS-X (referred to as the Loan Rule). The Loan Rule prohibits accounting firms, such as PricewaterhouseCoopers LLP, from being deemed independent if they have certain financial relationships with their audit clients or certain affiliates of those clients. The Trust is required under various securities laws to have its financial statements audited by an independent accounting firm.

The Loan Rule specifically provides that an accounting firm would not be independent if it or certain affiliates and covered persons receives a loan from a lender that is a record or beneficial owner of more than ten percent of an audit client’s equity securities (referred to as a “more than ten percent owner”). For purposes of the Loan Rule, audit clients include the Trust as well as all registered investment companies advised by the Sponsor and its affiliates, including other subsidiaries of the Sponsor’s parent company, Invesco Ltd. (collectively, the Invesco Fund Complex). PricewaterhouseCoopers LLP informed the Trust it and certain affiliates and covered persons have relationships with lenders who hold, as record owner, more than ten percent of the shares of certain funds within the Invesco Fund Complex, which may implicate the Loan Rule.

On June 20, 2016, the SEC Staff issued a“no-action” letter to another mutual fund complex (see Fidelity Management & Research Company et al.,No-Action Letter) related to the audit independence issue described above. In that letter, the SEC confirmed that it would not recommend enforcement action against a fund that relied on audit services performed by an audit firm that was not in compliance with the Loan Rule in certain specified circumstances. On May 2, 2018, the SEC proposed amendments to the Loan Rule that, if adopted as proposed, would address many of the issues that led to issuance of the no-action letter. In connection with prior independence determinations, PricewaterhouseCoopers LLP communicated, as contemplated by theno-action letter, that it believes that it remains objective and impartial and that a reasonable investor possessing all the facts would conclude that PricewaterhouseCoopers LLP is able to exhibit the requisite objectivity and impartiality to report on the Trust’s financial statements as the independent registered public accounting firm. PricewaterhouseCoopers LLP also represented that it has complied with PCAOB Rule 3526(b)(1) and (2), which are conditions to the Trust relying on theno-action letter, and affirmed that it is an independent accountant within the meaning of PCAOB Rule 3520. Therefore, the Sponsor, the Trust and PricewaterhouseCoopers LLP concluded that PricewaterhouseCoopers LLP could continue as the Trust’s independent registered public accounting firm. The Invesco Fund Complex relied upon theno-action letter in reaching this conclusion.

10

If in the future the independence of PricewaterhouseCoopers LLP is called into question under the Loan Rule by circumstances that are not addressed in the SEC’sno-action letter, the Trust will need to take other action in order for the Trust’s filings with the SEC containing financial statements to be deemed compliant with applicable securities laws. Such additional actions could result in additional costs, impair the ability of the Trust to issue new shares or have other material adverse effects on the Trust. The SECno-action relief was initially set to expire 18 months from issuance but has been extended by the SEC without an expiration date, except that theno-action letter will be withdrawn upon the effectiveness of any amendments to the Loan Rule designed to address the concerns expressed in the letter.

In this prospectus, each of the following terms has the meaning assigned to it here:

“Authorized Participant” — A DTC Participant that is a registered broker-dealer or other securities market participant such as a bank or other financial institution that is not required to register as a broker-dealer to engage in securities transactions and that has entered into a Participant Agreement with the Sponsor and the Trustee. Only Authorized Participants may place orders to create or redeem Baskets.

“Basket Canadian Dollar Amount” — The deposit required to create one or more Baskets pursuant to a purchase order. This deposit will be an amount of Canadian Dollars bearing the same proportion to the number of Baskets to be created as the total assets of the Trust (net of estimated accrued but unpaid expenses) bears to the number of Baskets outstanding on the date that the order to purchase is accepted by the Trustee.

“Canadian Dollar” — The official currency of Canada.

“Closing Spot Rate” — The USD/Canadian Dollar exchange rate as determined by The WM Company at 4:00 PM (London time / London fixing) on each day that NYSE Arca is open for regular trading.

“Deposit Account Agreement” — The agreements, including the Account Application and the JPMorgan Chase Bank, N.A. Global Account Terms, between the Trustee and the Depository establishing the Deposit Accounts with the Depository.

“Deposit Accounts” — The primary (interest-bearing) and secondary(non-interest bearing) Canadian Dollar-denominated, demand accounts of the Trust established with the Depository by the Deposit Account Agreement. The Deposit Accounts hold the Canadian Dollars deposited with the Trust.

“Depositary Trust Agreement” — The agreement between the Trustee and the Sponsor establishing and governing the operations of the Trust.

“DTC” — The Depository Trust Company. DTC is a limited purpose trust company organized under the laws of the State of New York, a member of the U.S. Federal Reserve System and a clearing agency registered with the SEC. DTC acts as the securities depository for the Shares.

“DTC Participant” — Participants in DTC, such as banks, brokers, dealers and trust companies.

“Foreign exchange” — The exchange of one currency for another.

“Indirect Participants” — Those banks, brokers, dealers, trust companies and others that maintain, either directly or indirectly, a custodial relationship with a DTC Participant.

“Internal Revenue Code” — The Internal Revenue Code of 1986, as amended.

“Investment Company Act” — The Investment Company Act of 1940, as amended.

“NAV” — Net asset value. The Trustee calculates, and the Sponsor publishes, the Trust’s NAV each business day as soon as practicable after The WM Company announces the Closing Spot Rate. To calculate the NAV, the Trustee adds to the amount of Canadian Dollars in the Trust at the end of the preceding day accrued but unpaid interest, if any, Canadian Dollars receivable under pending purchase orders and the value of other Trust assets, and subtracts the accrued but unpaid Sponsor’s fee, Canadian Dollars payable under pending redemption orders and other Trust expenses and liabilities, if any.

11

“Participant Agreement” — An agreement entered into by each Authorized Participant with the Sponsor and the Trustee that states the procedures for the creation and redemption of Baskets and for the delivery of Canadian Dollars required for creation and redemption.

“Securities Act” — The Securities Act of 1933, as amended.

“Securities Exchange Act” — The Securities Exchange Act of 1934, as amended.

“Shareholder” — Any owner of a Share (whether such owner owns through DTC, a DTC Participant or an Indirect Participant).

“Sponsor Indemnified Party” — The Sponsor, its members, officers, employees and agents.

“SWIFT” — Society for Worldwide Interbank Financial Telecommunication.

“The Bank of New York Mellon” — The Bank of New York Mellon, a banking corporation organized under the laws of the State of New York with trust powers. The Bank of New York Mellon is the trustee of the Trust.

“The WM Company” — A joint venture of The WM Company PLC and Thomson Reuters.

“USD” or “$” — United States Dollar or Dollars.

Statement Regarding Forward-Looking Statements

This prospectus and information incorporated by reference in this prospectus includes “forward-looking statements” which generally relate to future events or future performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or the negative of these terms or other comparable terminology. All statements (other than statements of historical fact) included in this prospectus or incorporated by reference in this prospectus that address activities, events or developments that will or may occur in the future, including such matters as changes in currency prices and market conditions (for the Canadian Dollar and the Shares), the Trust’s operations, the Sponsor’s plans and references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially. These statements are based upon certain assumptions and analyses the Sponsor made, based on its perceptions of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including the special considerations discussed in this prospectus, general economic, market and business conditions, changes in laws and regulations, including those concerning taxes, made by governmental authorities and regulatory bodies and other world economic and political developments. See “Risk Factors.” Consequently, all forward-looking statements made in this prospectus or incorporated by reference in this prospectus are qualified by these cautionary statements, and there can be no assurance that the actual results or developments that the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Shares. Moreover, neither the Sponsor nor any other person assumes responsibility for the accuracy or completeness of the forward-looking statements. Neither the Trust nor the Sponsor is under a duty to update any of the forward-looking statements to conform such statements to actual results or to reflect a change in the Sponsor’s expectations or predictions.

The proceeds received by the Trust from the issuance and sale of Baskets are Canadian Dollars. Such proceeds are deposited into the Deposit Accounts. In accordance with the Depositary Trust Agreement, during the life of the Trust these proceeds will only be (1) owned by the Trust and held by the Depository, (2) disbursed or sold as needed to pay the Trust’s expenses, and (3) distributed to Authorized Participants upon the redemption of Baskets.

12

Overview of the Foreign Exchange Industry

There are three major kinds of transactions in the traditional foreign exchange markets: spot transactions, outright forwards and foreign exchange swaps. “Spot” trades are foreign exchange transactions that settle typically within two business days with the counterparty to the trade. “Forward” trades are transactions that settle on a date beyond spot and “swap” transactions are transactions in which two parties exchange two currencies on one or more specified dates over an agreed period and exchange them again when the period ends. There also are transactions in currency options, which trade bothover-the-counter and, in the U.S., on the Philadelphia Stock Exchange. Currency futures are transactions in which an institution buys or sells a standardized amount of foreign currency on an organized exchange for delivery on one of several specified dates. Currency futures are traded in a number of regulated markets, including the International Monetary Market division of the Chicago Mercantile Exchange, the Singapore Exchange Derivatives Trading Limited (formerly the Singapore International Monetary Exchange, or SIMEX) and the London International Financial Futures Exchange (LIFFE).

Participants in the foreign exchange market have various reasons for participating. Multinational corporations and importers need foreign currency to acquire materials or goods from abroad. Banks and multinational corporations sometimes require specific wholesale funding for their commercial loan or other foreign investment portfolios. Some participants hedge open currency exposure throughoff-balance-sheet products.

The primary market participants in foreign exchange are banks (including government-controlled central banks), investment banks, money managers, multinational corporations and institutional investors. The most significant participants are the major international commercial banks that act both as brokers and as dealers. In their dealer role, these banks maintain long or short positions in a currency and seek to profit from changes in exchange rates. In their broker role, the banks handle buy and sell orders from commercial customers, such as multinational corporations. The banks earn commissions when acting as agent. They profit from the spread between the rates at which they buy and sell currency for customers when they act as principal.

Much of the foregoing information is taken fromA Foreign Exchange Primer by Shani Shamah (John Wiley & Sons Ltd., 2003) andTrading in the Global Currency Markets by Cornelius Luca (New York Institute of Finance, 2d ed., 2000).

The Canadian Dollar is the national currency of Canada and the currency of the accounts of the Bank of Canada, the Canadian central bank. The official currency code for the Canadian Dollar is “CAD.” As with U.S. currency, 100 Canadian cents are equal to one Canadian Dollar.

The Canadian Dollar was introduced in 1858. Initially, the Canadian Dollar was redeemable for gold, but the gold standard was suspended at times and abandoned officially in 1933. In 1934, Canada’s official central bank, the Bank of Canada, was established. During World War II, the Canadian Dollar was pegged to the USD and the British Pound by the Canadian government. In 1950, Canada abolished the fixed rates of exchange for the Canadian Dollar into USD and British Pounds. In 1962, Canada again established fixed rates of exchange based primarily on the USD. In 1970, the Canadian government decided to allow the value of the Canadian Dollar to float; as a result, its value now depends almost entirely on market forces. The source of this information is James Powell’s book, A History of the Canadian Dollar (2005).

Investment Attributes of the Trust

The investment objective of the Trust is for the Shares to reflect the price in USD of the Canadian Dollar. The Sponsor believes that, for many investors, the Shares represent a cost-effective investment relative to traditional means of investing in the foreign exchange market. As the value of the Shares is tied to the value of the Canadian Dollars held by the Trust, it is important in understanding the investment attributes of the Shares to first understand the investment attributes of the Canadian Dollar.

REASONS FOR INVESTING IN THE CANADIAN DOLLAR

All forms of investment carry some degree of risk. Although the Shares have certain unique risks described in “Risk Factors,” generally these are the same risks as investing directly in the Canadian Dollar. Moreover, investment in the Shares may help to balance a portfolio or protect against currency swings, thereby reducing overall risk.

Investors may wish to invest in the Canadian Dollar in order to take advantage of short-term tactical or long-term strategic opportunities. From a tactical perspective, an investor that believes that the USD is weakening relative to the Canadian Dollar may choose to buy Shares in order to capitalize on the potential movement. An investor that believes that the Canadian Dollar is overvalued relative to the USD may choose to sell Shares. Sales may also include short sales that are permitted under SEC and exchange regulations.

13

From a strategic standpoint, since currency movements can affect returns on cross-border investments and businesses, both individual investors and businesses may choose to hedge their currency risk through the purchase or sale of Canadian Dollars. For example, in the case where a U.S. investor has a portfolio consisting of Canadian equity and fixed income securities, the investor may decide to hedge the currency exposure that exists within the Canadian portfolio by selling an appropriate amount of Shares. Again, such sales may include short sales in accordance with applicable SEC regulations. In doing this, the U.S. investor may be able to mitigate the impact that changes in exchange rates have on the returns associated with Canadian equity and fixed income components of the portfolio.

Similarly, a business that has currency exposure because it manufactures or sells its products abroad is exposed to exchange rate risk. Buying or selling Shares in appropriate amounts can reduce the business’s exchange rate risk.

More generally, investors that wish to diversify their investment portfolios with a wider range ofnon-correlative investments may desire to invest in foreign currencies.Non-correlative asset classes, such as foreign currencies, are often used to enhance investment portfolios by making them more consistent and less volatile. Less volatility means lower risk and closer proximity to an expected return.

COST-EFFICIENT PARTICIPATION IN THE MARKET FOR THE CANADIAN DOLLAR

The Shares are intended to provide institutional and retail investors with a simple, cost-effective means of gaining investment benefits similar to those of holding Canadian Dollars. The costs of purchasing Shares should not exceed the costs associated with purchasing any other publicly-traded equity securities. The Shares are an investment that is:

Easily Accessible. Investors are able to access the market for the Canadian Dollar through a traditional brokerage account. The Shares are bought and sold on NYSE Arca like any other exchange-listed security.

Exchange-Traded. Because they are traded on NYSE Arca, the Shares provide investors with an efficient means of implementing investment tactics and strategies that involve Canadian Dollars. NYSE Arca-listed securities are eligible for margin accounts. Accordingly, investors are able to purchase and hold Shares with borrowed money to the extent permitted by law.

Transparent. The Shares are backed by the assets of the Trust, which does not hold or use derivative products. The value of the holdings of the Trust is reported on the Trust’s website, www.invesco.com/etfs, every business day.

Investing in the Shares will not insulate the investor from price volatility or other risks. See “Risk Factors.”

INTEREST ON DEPOSITED CANADIAN DOLLARS

JPMorgan Chase Bank, N.A., London Branch, maintains two deposit accounts for the Trust: a primary deposit account that may earn interest and a secondary deposit account that does not earn interest. Interest on the primary deposit account, if any, accrues daily and is paid monthly. The Depository may change the rate at which interest accrues, including reducing the interest rate to zero or below zero, based upon changes in market conditions or the Depository’s liquidity needs. The Depository notifies the Sponsor of the interest rate applied each business day after the close of such business day. The Sponsor discloses the current interest rate on the Trust’s website. If the Sponsor believes that the interest rate paid by the Depository is not competitive, the Sponsor’s sole recourse will be to remove the Depository by terminating the Deposit Account Agreement and closing the accounts.

The secondary deposit account is used to account for any interest that may be received and paid on creations and redemptions of Baskets. The secondary deposit account is also used to account for interest earned on the primary deposit account, if any, pay Trust expenses and distribute any excess interest to Shareholders on a monthly basis. In the event that the interest deposited exceeds the sum of the Sponsor’s fee for the prior month plus other Trust expenses, if any, then the Trustee will direct that the excess be converted into USD at a prevailing market rate and the Trustee will distribute the USD as promptly as practicable to Shareholders on apro-rata basis (in accordance with the number of Shares that they own).

TRUST EXPENSES

The Trust’s only ordinary recurring expense is the Sponsor’s fee. The Sponsor is responsible for payment of the following administrative and marketing expenses of the Trust: the Trustee’s monthly fee, typical maintenance and transaction fees of the Depository, NYSE Arca listing fees, SEC registration fees, printing and mailing costs, audit fees and expenses, up to $100,000 per annum in legal fees and expenses, and applicable license fees. The Sponsor’s

14

fee accrues daily at an annual nominal rate of 0.40% of the Canadian Dollars in the Trust. Each month, the Trust first withdraws Canadian Dollars the Trust has earned as interest, if any, to pay the Sponsor’s fee and any other Trust expenses that have been incurred. If that interest is not sufficient to fully pay the Sponsor’s fee and other Trust expenses, then the Trustee will withdraw Canadian Dollars as needed from the primary deposit account to pay these expenses. Shareholders do not have the option of choosing to pay their proportionate share of the excess expenses in lieu of having their share of expenses paid by withdrawing Canadian Dollars from the primary deposit account. If the Trust were to incur expenses in USD (which is not anticipated), Canadian Dollars will be converted to USD at a prevailing market rate at the time of conversion to pay these expenses. The payment of expenses in Canadian Dollars and the conversion of Canadian Dollars to USD, if required to pay expenses of the Trust, are taxable events to Shareholders. See “United States Federal Tax Consequences — Taxation of U.S. Shareholders.”

In certain exceptional cases the Trust will pay for some expenses in addition to the Sponsor’s fee. These exceptions include expenses not assumed by the Sponsor, expenses resulting from negative interest rates, taxes and governmental charges, expenses and costs of any extraordinary services performed by the Trustee or the Sponsor on behalf of the Trust or action taken by the Trustee or the Sponsor to protect the Trust or the interests of Shareholders, indemnification of the Sponsor under the Depositary Trust Agreement, and legal expenses in excess of $100,000 per year.

In the event that none of the extraordinary expenses described in the immediately preceding paragraph are charged to the Trust, an investment of $10,000 in Shares will incur an annual fee of approximately $40, or approximately $200 over five years. Additionally, investors should expect to pay customary brokerage fees and expenses for each purchase or sale of Shares. An Authorized Participant will pay transaction fees to the Trustee, which will not be contributed to the Trust, for each creation or redemption order.

The Trust was formed under the laws of the State of New York on June 8, 2006. The Shares commenced trading on the New York Stock Exchange under the ticker symbol “FXC” on June 26, 2006. The Trust holds Canadian Dollars and, from time to time, issues Baskets in exchange for deposits of Canadian Dollars and distributes Canadian Dollars in connection with redemptions of Baskets. The investment objective of the Trust is for the Shares to reflect the price in USD of the Canadian Dollar. The material terms of the Depositary Trust Agreement are discussed under “Description of the Depositary Trust Agreement.” The Shares represent units of fractional undivided beneficial interest in, and ownership of, the Trust. The Trust is not managed like a business corporation or an active investment vehicle. The Canadian Dollars held by the Trust will only be sold (1) if needed to pay Trust expenses, (2) in the event the Trust terminates and liquidates its assets or (3) as otherwise required by law or regulation. The payment of expenses in Canadian Dollars and the conversion of Canadian Dollars to USD, if necessary to pay expenses of the Trust, are taxable events to Shareholders. See “United States Federal Tax Consequences — Taxation of U.S. Shareholders.”

The Trust is not registered as an investment company under the Investment Company Act and is not required to register under such Act.

The Trust creates and redeems Shares from time to time, but only in whole Baskets. A Basket is a block of 50,000 Shares. The number of Shares outstanding is expected to increase and decrease from time to time as a result of the creation and redemption of Baskets. Authorized Participants pay for Baskets with Canadian Dollars. Shareholders pay for Shares with USD.

The creation and redemption of Baskets requires the delivery to the Trust or the distribution by the Trust of the amount of Canadian Dollars represented by the Baskets being created or redeemed. This amount is based on the total Canadian Dollars represented by the number of Shares included in the Baskets being created or redeemed. Baskets may be created or redeemed only by Authorized Participants. Authorized Participants will pay transaction fees for each order to create or redeem Baskets. See “Creation and Redemption of Shares.” Authorized Participants may sell to other investors all or part of the Shares included in the Baskets that they purchase from the Trust. See “Plan of Distribution.”

The Trustee calculates, and the Sponsor publishes, the Trust’s NAV each business day. To calculate the NAV, the Trustee adds to the amount of Canadian Dollars in the Trust at the end of the preceding day accrued but unpaid interest, if any, Canadian Dollars receivable under pending purchase orders and the value of other Trust assets, and subtracts the accrued but unpaid Sponsor’s fee, Canadian Dollars payable under pending redemption orders and other Trust expenses and liabilities, if any. The NAV is expressed in USD based on the Closing Spot Rate. The Trustee also determines the NAV per Share, which equals the NAV of the Trust divided by the number of outstanding Shares. See “Description of the Depositary Trust Agreement — Valuation of Canadian Dollars; Definition of Net Asset Value” for a more detailed description of how the NAV of the Trust and the NAV per Share are calculated.

15

The Trust’s assets consist only of Canadian Dollars on demand deposit in two Canadian Dollar-denominated accounts at JPMorgan Chase Bank, N.A., London Branch: a primary deposit account that may earn interest and anon-interest bearing secondary account. The Trust does not hold any derivative products. Each Share represents a proportional interest, based on the total number of Shares outstanding, in the Canadian Dollars owned by the Trust, plus accrued and unpaid interest, if any, less accrued but unpaid expenses (both asset-based andnon-asset based) of the Trust. The Sponsor expects that the price of a Share will fluctuate in response to fluctuations in the price of the Canadian Dollar and that the price of a Share will reflect accumulated interest as well as the estimated accrued but unpaid expenses of the Trust.

Investors may obtain, 24 hours a day, foreign exchange pricing information based on the spot price of the Canadian Dollar from various financial information service providers. Current spot prices are also generally available with bid/ask spreads from foreign exchange dealers. In addition, the Trust’s website, www.invesco.com/etfs, provides ongoing pricing information for Canadian Dollar spot prices and the Shares. Market prices for the Shares are available from a variety of sources, including brokerage firms, information websites and other information service providers. One such website is hosted by Bloomberg, https://www.bloomberg.com/markets/currencies/americas, and it regularly reports current foreign exchange pricing information. The NAV of the Trust is published by the Sponsor on each day that NYSE Arca is open for regular trading and is posted on the Trust’s website.

The Trust will terminate upon the occurrence of any of the termination events listed in the Depositary Trust Agreement and will otherwise terminate on June 8, 2046. See “Description of the Depositary Trust Agreement — Termination of the Trust.”

The Sponsor of the Trust is Invesco Specialized Products, LLC, a Delaware limited liability company. The principal offices of the Sponsor and the Trust are the offices of Invesco Specialized Products at 3500 Lacey Road, Suite 700, Downers Grove, Illinois 60515, and the Sponsor does not own or lease any other property.

The Invesco CurrencyShares® Euro Trust (NYSE Arca: FXE), sponsored by Invesco Specialized Products, was the first exchange-traded product limited solely to particular foreign currency,. In addition to the Invesco CurrencyShares® Euro Trust and the Trust, Invesco Specialized Products sponsors seven other exchange-traded products limited solely to particular foreign currency, as follows: Invesco CurrencyShares® Australian Dollar Trust (NYSE Arca: FXA); Invesco CurrencyShares® British Pound Sterling Trust (NYSE Arca: FXB); Invesco CurrencyShares® Chinese Renminbi Trust (NYSE Arca: FXCH); Invesco CurrencyShares® Japanese Yen Trust (NYSE Arca: FXY); Invesco CurrencyShares® Singapore Dollar Trust (NYSE Arca: FXSG); Invesco CurrencyShares® Swedish Krona Trust (NYSE Arca: FXS); and Invesco CurrencyShares® Swiss Franc Trust (NYSE Arca: FXF).

The following executive officers of the Sponsor serve in the capacities specified for them:

Name | Capacity | |

| Daniel Draper | Chief Executive Officer and Principal Executive Officer; Board of Managers | |

| Kelli Gallegos | Principal Financial and Accounting Officer – Investment Pools | |

| Annette J. Lege | Chief Financial Officer | |

| Melanie Zimdars | Chief Compliance Officer | |

| David C. Warren | Board of Managers | |

| John M. Zerr | Board of Managers | |

The Sponsor is managed by a Board of Managers. The Board of Managers is composed of Messrs. Draper, Warren and Zerr.

Daniel Draper (50) currently serves as Chief Executive Officer and Principal Executive Officer of the Sponsor, and also serves as a member of the Sponsor’s Board of Managers. He has served in such capacities since April 6, 2018. In his role, he has general oversight responsibilities for all of the Sponsor’s business. Mr. Draper also serves as Chief Executive Officer of Invesco Capital Management (“Invesco Capital Management”), an affiliate of the Sponsor, and

16