SBT BANCORP, INC. AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Years Ended December 31, 2010 and 2009

NOTE 1 - NATURE OF OPERATIONS

On March 2, 2006, The Simsbury Bank & Trust Company, Inc. (the “Bank”) reorganized into a holding company structure. As a result, the Bank became a wholly-owned subsidiary of SBT Bancorp, Inc. (the “Company”) and each outstanding share of common stock of the Bank was converted into the right to receive one share of the common stock, no par value, of the Company. The Company files reports with the Securities and Exchange Commission and is supervised by the Board of Governors of the Federal Reserve System.

The Bank is a state chartered bank which was incorporated on April 28, 1992 and is headquartered in Simsbury, Connecticut. The Bank commenced operations on March 31, 1995 engaging principally in the business of attracting deposits from the general public and investing those deposits in securities, residential and commercial real estate, consumer and small business loans.

NOTE 2 - ACCOUNTING POLICIES

The accounting and reporting policies of the Company and its subsidiary conform to accounting principles generally accepted in the United States of America and predominant practices within the banking industry. The consolidated financial statements of the Company were prepared using the accrual basis of accounting. The significant accounting policies of the Company are summarized below to assist the reader in better understanding the consolidated financial statements and other data contained herein.

USE OF ESTIMATES:

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

BASIS OF PRESENTATION:

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiary the Bank and the Bank’s wholly-owned subsidiaries, SBT Investment Services, Inc. and NERE Holdings, Inc. SBT Investment Services, Inc. was established solely for the purpose of providing investment products, financial advice and services to its clients and the community. NERE Holdings, Inc. was established to hold real estate. All significant intercompany accounts and transactions have been eliminated in the consolidation.

CASH AND CASH EQUIVALENTS:

For purposes of reporting cash flows, cash and cash equivalents include cash on hand, cash items, due from banks, Federal Home Loan Bank interest-bearing demand and overnight deposits, Federal Reserve Bank interest-bearing demand deposits, money market mutual funds and federal funds sold.

Cash and due from banks as of December 31, 2010 and 2009 includes $4,070,000 and $3,127,000, respectively, which is subject to withdrawals and usage restrictions to satisfy the reserve requirements of the Federal Reserve Bank of Boston and Bankers’ Bank Northeast.

SECURITIES:

Investments in debt securities are adjusted for amortization of premiums and accretion of discounts computed so as to approximate the interest method. Gains or losses on sales of investment securities are computed on a specific identification basis.

The Company classifies debt and equity securities into one of three categories: held-to-maturity, available-for-sale, or trading. These security classifications may be modified after acquisition only under certain specified conditions. In general, securities may be classified as held-to-maturity only if the Company has the positive intent and ability to hold them to maturity. Trading securities are defined as those bought and held principally for the purpose of selling them in the near term. All other securities must be classified as available-for-sale.

| | -- | Held-to-maturity securities are measured at amortized cost in the consolidated balance sheets. Unrealized holding gains and losses are not included in earnings, or in a separate component of capital. They are merely disclosed in the notes to the consolidated financial statements. |

| | -- | Available-for-sale securities are carried at fair value on the consolidated balance sheets. Unrealized holding gains and losses are not included in earnings but are reported as a net amount (less expected tax) in a separate component of capital until realized. |

| | -- | Trading securities are carried at fair value on the consolidated balance sheets. Unrealized holding gains and losses for trading securities are included in earnings. |

For any debt security with a fair value less than its amortized cost basis, the Company will determine whether it has the intent to sell the debt security or whether it is more likely than not it will be required to sell the debt security before the recovery of its amortized cost basis. If either condition is met, the Company will recognize a full impairment charge to earnings. For all other debt securities that are considered other-than-temporarily impaired and do not meet either condition, the credit loss portion of impairment will be recognized in earnings as realized losses. The other-than-temporary impairment related to all other factors will be recorded in other comprehensive income.

Declines in marketable equity securities below their cost that are deemed other than temporary are reflected in earnings as realized losses.

As a member of the Federal Home Loan Bank (FHLB), the Company is required to invest in $100 par value stock of FHLB. The FHLB capital structure mandates that members must own stock as determined by their Total Stock Investment Requirement which is the sum of a member’s Membership Stock Investment Requirement and Activity-Based Stock Investment Requirement. The Membership Stock Investment Requirement is calculated as 0.35% of member’s Stock Investment Base, subject to a minimum investment of $10,000 and a maximum investment of $25,000,000. The Stock Investment Base is an amount calculated based on certain assets held by a member that are reflected on call reports submitted to applicable regulatory authorities. The Activity-Based Stock Investment Requirement is calculated as 4.5% of a member’s outstanding principal balances of FHLB advances plus a percentage of advance commitments, 4.5% of standby letters of credit issued by the FHLB and 4.5% of the value of intermediated derivative contracts. Management evaluates the Company’s investment in FHLB of Boston stock for other-than-temporary impairment at least on a quarterly basis and more frequently when economic or market conditions warrant such evaluation. Based on its most recent analysis of the FHLB of Boston as of December 31, 2010 management deems its investment in FHLB of Boston stock to be not other-than-temporarily impaired.

On December 8, 2008, the Federal Home Loan Bank of Boston announced a moratorium on the repurchase of excess stock held by its members. The moratorium will remain in effect indefinitely.

LOANS HELD-FOR-SALE:

Loans held-for-sale in the secondary market are carried at the lower of cost or estimated fair value in the aggregate. Net unrealized losses are provided for in a valuation allowance by charges to operations.

Interest income on mortgages held-for-sale is accrued currently and classified as interest on loans.

LOANS:

Loans receivable that management has the intent and ability to hold until maturity or payoff, are reported at their outstanding principal balances adjusted for amounts due to borrowers on unadvanced loans, any charge-offs, the allowance for loan losses and any deferred fees or costs on originated loans, or unamortized premiums or discounts on purchased loans.

Interest on loans is recognized on a simple interest basis.

Loan origination and commitment fees and certain direct origination costs are deferred, and the net amount amortized as an adjustment of the related loan's yield. The Company is amortizing these amounts over the contractual life of the related loans.

Residential real estate loans are generally placed on nonaccrual when reaching 90 days past due or in process of foreclosure. All closed-end consumer loans 90 days or more past due and any equity line in the process of foreclosure are placed on nonaccrual status. Secured consumer loans are written down to realizable value and unsecured consumer loans are charged-off upon reaching 120 or 180 days past due depending on the type of loan. Commercial real estate loans and commercial business loans and leases which are 90 days or more past due are generally placed on nonaccrual status, unless secured by sufficient cash or other assets immediately convertible to cash. When a loan has been placed on nonaccrual status, previously accrued and uncollected interest is reversed against interest on loans. A loan can be returned to accrual status when collectability of principal is reasonably assured and the loan has performed for a period of time, generally six months.

Cash receipts of interest income on impaired loans are credited to principal to the extent necessary to eliminate doubt as to the collectability of the net carrying amount of the loan. Some or all of the cash receipts of interest income on impaired loans is recognized as interest income if the remaining net carrying amount of the loan is deemed to be fully collectible. When recognition of interest income on an impaired loan on a cash basis is appropriate, the amount of income that is recognized is limited to that which would have been accrued on the net carrying amount of the loan at the contractual interest rate. Any cash interest payments received in excess of the limit and not applied to reduce the net carrying amount of the loan are recorded as recoveries of charge-offs until the charge-offs are fully recovered.

The Company has certain lending policies and procedures in place that are designed to maximize loan income with an acceptable level of risk. Management reviews and approves these policies and procedures on an annual basis. A reporting system is in place which provides management with frequent reports related to loan quality, loan production, loan delinquencies and non-performing or potential problem loans.

Commercial and industrial loans are underwritten after evaluating historical and projected profitability and cash flow to determine the borrower’s ability to repay their obligation as agreed. Underwriting standards are designed to promote relationship banking rather than transactional banking. Commercial and industrial loans are made primarily based on the identified cash flow of the borrower and secondarily on the underlying collateral supporting the loan facility. The cash flow of the borrower may not be as expected and the collateral supporting the loan may fluctuate in value. Most commercial and industrial loans are secured by the assets being financed or other business assets such as accounts receivable and inventory and may incorporate a personal guarantee. Some loans may be made on an unsecured basis. In the case of loans secured by accounts receivable, the availability of funds for the repayment of these loans may be substantially dependent upon the ability of the borrower to collect amounts due from its customers.

Commercial real estate loans are subject to the underwriting standards and processes similar to commercial and industrial loans, in addition to those underwriting standards for real estate loans. These loans are viewed primarily as cash flow dependent and secondarily as loans secured by real estate. Commercial real estate lending typically involves higher principal balances and longer repayment periods. Repayment of these loans is generally dependent upon the successful operation of the property securing the loan or the principal business conducted on the property securing the loan. Commercial real estate loans may be adversely affected by conditions in the real estate markets or the economy in general. The properties securing the Company’s commercial real estate portfolio are diverse in terms of type and geographic location. This diversification reduces the exposure to adverse economic conditions that affect any single market or industry. Management monitors and evaluates commercial real estate loans based on collateral, geography and risk-rating criteria. The Company also utilizes third-party experts to provide environmental and market valuations, in addition to economic conditions and trends within a specific industry. The Company also tracks the level of owner occupied commercial real estate loans within its commercial real estate portfolio. At December 31, 2010, approximately 78.3% of the outstanding principal balance of the Company’s commercial real estate loans were secured by owner-occupied properties.

With respect to land developers and builders that are secured by non-owner-occupied properties that the Company may originate from time to time, the Company generally requires that the borrower have a proven record of success. Construction loans are underwritten based upon a financial analysis of the developers and property owners and construction cost estimates, in addition to independent appraisal valuations. These loans will rely on the value associated with the project upon completion. These cost and valuation estimates may be inaccurate. Construction loans generally involve the disbursement of substantial funds over a short period of time with repayment substantially dependent upon the success of the completed project. Sources of repayment of these loans would be permanent financing upon completion or sales of developed property. These loans are closely monitored by onsite inspections and are considered to be of a higher risk than other real estate loans due to their ultimate repayment being sensitive to general economic conditions, availability of long-term financing, interest rate sensitivity, and governmental regulation of real property.

The Company originates consumer loans utilizing a computer-based credit-scoring analysis to supplement the underwriting process. To monitor and manage consumer loan risk, policies and procedures are developed and modified, as needed, jointly by staff and management. This continual review, coupled with the high volume of borrowers of smaller dollar loans, minimizes risk. Additionally, trend and outlook reports are reviewed by management on a regular basis. Underwriting standards for home equity loans are heavily influenced by regulatory requirements, which include but are not limited to a maximum loan-to-value of 75%, collection remedies, the number of such loans that a borrower can have at one time, and documentation requirements.

The Company engages an independent loan review firm that reviews and validates the credit risk program on a periodic basis. Results of these reviews are presented to management and the Board of Directors. The loan review process complements and reinforces the risk identification process and assessment decisions made by the relationship managers and credit officer, as well as the Company’s policies and procedures.

ALLOWANCE FOR LOAN LOSSES:

The allowance for loan losses is established as losses are estimated to have occurred through a provision for loan losses charged to earnings. Loan losses are charged against the allowance when management believes the uncollectability of a loan balance is confirmed. Subsequent recoveries, if any, are credited to the allowance.

The allowance for loan losses is evaluated on a regular basis by management and is based upon management’s periodic review of the collectability of the loans in light of historical experience, the nature and volume of the loan portfolio, adverse situations that may affect the borrower’s ability to repay, estimated value of any underlying collateral and prevailing economic conditions. This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as more information becomes available.

General component:

The general component of the allowance for loan losses is based on historical loss experience adjusted for qualitative factors stratified by the following loan segments: residential real estate, commercial real estate, construction, commercial and consumer. Management uses a rolling average of historical losses based on a time frame appropriate to capture relevant loss data for each loan segment. This historical loss factor is adjusted for the following qualitative factors: levels/trends in delinquencies; trends in volume and terms of loans; effects of changes in risk selection and underwriting standards and other changes in lending policies, procedures and practices; experience/ability/depth of lending management and staff; and national and local economic trends and conditions. There were no changes in the Company’s policies or methodology pertaining to the general component of the allowance for loan losses during 2010.

The qualitative factors are determined based on the various risk characteristics of each loan segment. Risk characteristics relevant to each portfolio segment are as follows:

Residential real estate: The Company generally does not originate loans with a loan-to-value ratio greater than 80 percent without obtaining private mortgage insurance for any amounts over 80% and does not grant subprime loans. All loans in this segment are collateralized by owner-occupied residential real estate and repayment is dependent on the credit quality of the individual borrower. The overall health of the economy, including unemployment rates and housing prices, will have an effect on the credit quality in this segment.

Commercial real estate: Loans in this segment are primarily income-producing properties throughout the Farmington Valley in Connecticut. The underlying cash flows generated by the properties are adversely impacted by a downturn in the economy as evidenced by increased vacancy rates, which in turn will, have an effect on the credit quality in this segment. Management periodically obtains rent rolls annually and continually monitors the cash flows of these loans.

Construction loans: Loans in this segment primarily include speculative real estate development loans for which payment is derived from sale of the property. Credit risk is affected by cost overruns, time to sell at an adequate price, and market conditions.

Commercial loans: Loans in this segment are made to businesses and are generally secured by assets of the business. Repayment is expected from the cash flows of the business. A weakened economy, and resultant decreased consumer spending, will have an effect on the credit quality in this segment.

Consumer loans: Loans in this segment are generally unsecured and repayment is dependent on the credit quality of the individual borrower.

Allocated component:

The allocated component relates to loans that are classified as impaired. Impairment is measured on a loan-by-loan basis for commercial, commercial real estate and construction loans by either the present value of expected future cash flows discounted at the loan’s effective interest rate or the fair value of the collateral if the loan is collateral dependent. An allowance is established when the discounted cash flows (or collateral value) of the impaired loan is lower than the carrying value of that loan. Large groups of smaller balance homogeneous loans are collectively evaluated for impairment. Accordingly, the Company does not separately identify individual consumer and residential real estate loans for impairment disclosures, unless such loans are subject to a troubled debt restructuring agreement.

A loan is considered impaired when, based on current information and events, it is probable that the Company will be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement. Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length of the delay, the reasons for the delay, the borrower’s prior payment record, and the amount of the shortfall in relation to the principal and interest owed.

The Company periodically may agree to modify the contractual terms of loans. When a loan is modified and a concession is made to a borrower experiencing financial difficulty, the modification is considered a troubled debt restructuring ("TDR"). All TDRs are initially classified as impaired.

Unallocated component:

An unallocated component is maintained to cover uncertainties that could affect management’s estimate of probable losses. The unallocated component of the allowance reflects the margin of imprecision inherent in the underlying assumptions used in the methodologies for estimating allocated and general reserves in the portfolio.

PREMISES AND EQUIPMENT:

Premises and equipment are stated at cost, less accumulated depreciation and amortization. Cost and related allowances for depreciation and amortization of premises and equipment retired or otherwise disposed of are removed from the respective accounts with any gain or loss included in income or expense. Depreciation and amortization are calculated principally on the straight-line method over the estimated useful lives of the assets. Estimated lives are 3 to 20 years for furniture and equipment. Leasehold improvements are amortized over the lesser of the life of the lease or the estimated life of the improvements.

OTHER REAL ESTATE OWNED AND IN-SUBSTANCE FORECLOSURES:

Other real estate owned includes properties acquired through foreclosures and properties classified as in-substance foreclosures in accordance with ASC 310-40, “Receivables – Troubled Debt Restructuring by Creditors.” These properties are carried at the lower of cost or estimated fair value less estimated costs to sell. Any writedown from cost to estimated fair value required at the time of foreclosure or classification as in-substance foreclosure is charged to the allowance for loan losses. Expenses incurred in connection with maintaining these assets, subsequent writedowns, and gains or losses recognized upon sale are included in other expense.

In accordance with ASC 310-10-35, “Receivables – Overall – Subsequent Measurements,” the Company classifies loans as in-substance repossessed or foreclosed if the Company receives physical possession of the debtor’s assets regardless of whether formal foreclosure proceedings take place.

FAIR VALUES OF FINANCIAL INSTRUMENTS:

ASC 825,“ Financial Instruments,” requires that the Company disclose estimated fair values for its financial instruments. Fair value methods and assumptions used by the Company in estimating its fair value disclosures are as follows:

Cash and cash equivalents: The carrying amounts reported in the balance sheets for cash and cash equivalents approximate those assets' fair values.

Interest-bearing time deposits with banks: The fair values of interest bearing time deposits with banks are estimated using discounted cash flow analyses using interest rates currently being offered for deposits with similar terms to investors.

Securities: Fair values for securities are based on quoted market prices, where available. If quoted market prices are not available, fair values are based on quoted market prices of comparable instruments.

Loans held-for-sale: Fair values for loans held-for-sale are estimated based on outstanding investor commitments, or in the absence of such commitments, are based on current investor yield requirements.

Loans receivable: For variable-rate loans that reprice frequently and with no significant change in credit risk, fair values are based on carrying values. The fair values for other loans are estimated by discounting the future cash flows, using interest rates currently being offered for loans with similar terms to borrowers of similar credit quality.

Accrued interest receivable: The carrying amount of accrued interest receivable approximates its fair value.

Deposit liabilities: The fair values disclosed for demand deposits, regular savings, NOW accounts, and money market accounts are equal to the amount payable on demand at the reporting date (i.e., their carrying amounts). Fair values for certificates of deposit are estimated using a discounted cash flow calculation that applies interest rates currently being offered on certificates to a schedule of aggregated expected monthly maturities on time deposits.

Federal Home Loan Bank advances: Fair values of Federal Home Loan Bank advances are estimated using discounted cash flow analyses based on the Company’s current incremental borrowing rates for similar types of borrowing arrangements.

Securities sold under agreements to repurchase: The carrying amounts of securities sold under agreements to repurchase approximate their fair values.

Due to broker: The carrying amount of due to broker approximates its fair value.

Off-balance sheet instruments: The fair value of commitments to originate loans is estimated using the fees currently charged to enter similar agreements, taking into account the remaining terms of the agreements and the present creditworthiness of the counterparties. For fixed-rate loan commitments and the unadvanced portion of loans, fair value also considers the difference between current levels of interest rates and the committed rates. The fair value of letters of credit is based on fees currently charged for similar agreements or on the estimated cost to terminate them or otherwise settle the obligation with the counterparties at the reporting date.

ADVERTISING:

The Company directly expenses costs associated with advertising as they are incurred.

INCOME TAXES:

The Company recognizes income taxes under the asset and liability method. Under this method, deferred tax assets and liabilities are established for the temporary differences between the accounting basis and the tax basis of the Company's assets and liabilities at enacted tax rates expected to be in effect when the amounts related to such temporary differences are realized or settled.

STOCK BASED COMPENSATION:

At December 31, 2010, the Company has a stock-based employee compensation plan which is described more fully in Note 17. The Company accounts for the plan under ASC 718-10, “Compensation – Stock Compensation – Overall.” During the years ended December 31, 2010 and 2009, $9,467 and $43,755, respectively, in stock-based employee compensation was recognized.

EARNINGS PER SHARE:

Basic earnings per share excludes dilution and is computed by dividing income available to common stockholders by the weighted-average number of common shares outstanding for the period. Diluted earnings per share reflects the potential dilution that could occur if securities or other contracts to issue common stock were exercised or converted into common stock or resulted in the issuance of common stock that then shared in the earnings of the entity.

RECENT ACCOUNTING PRONOUNCEMENTS:

In March 2010, the FASB issued ASU 2010-11, “Scope Exception Related to Embedded Credit Derivatives.” The ASU clarifies that certain embedded derivatives, such as those contained in certain securitizations, CDOs and structured notes, should be considered embedded credit derivatives subject to potential bifurcation and separate fair value accounting. The ASU allows any beneficial interest issued by a securitization vehicle to be accounted for under the fair value option at transition. At transition, the Company may elect to reclassify various debt securities (on an instrument-by-instrument basis) from held-to-maturity (HTM) or available-for-sale (AFS) to trading. The new rules are effective July 1, 2010. This ASU did not have a significant impact on the Company’s financial condition or results of operation.

In January 2010, the FASB issued ASU 2010-06, “Improving Disclosures about Fair Value Measurements.” The ASU requires disclosing the amounts of significant transfers in and out of Level 1 and 2 of the fair value hierarchy and describing the reasons for the transfers. The disclosures are effective for reporting periods beginning after December 15, 2009. The Company adopted ASU 2010-06 as of January 1, 2010. The required disclosures are included in Note 11. Additionally, disclosures of the gross purchases, sales, issuances and settlements activity in the Level 3 of the fair value measurement hierarchy will be required for fiscal years beginning after December 15, 2010.

In April 2010, the FASB issued ASU 2010-18, “Effect of a Loan Modification When the Loan is Part of a Pool That is Accounted for as a Single Asset.” As a result of this ASU, modifications of loans that are accounted for within a pool under Subtopic 310-30 do not result in the removal of those loans from the pool even if the modification of those loans would otherwise be considered a troubled debt restructuring. An entity will continue to be required to consider whether the pool of assets in which the loan is included is impaired if expected cash flows for the pool change. The amendments in this ASU are effective for modifications of loans accounted for within pools under Subtopic 310-30 occurring in the first interim or annual period ending on or after July 15, 2010. The amendments are to be applied prospectively. Early application is permitted.

In July 2010, the FASB issued ASU 2010-20, “Disclosures about the Credit Quality of Financing Receivables and the Allowance for Credit Losses.” This ASU is created to provide financial statement users with greater transparency about an entity’s allowance for credit losses and the credit quality of its financing receivables. This ASU is intended to provide additional information to assist financial statement users in assessing the entity’s

credit risk exposures and evaluating the adequacy of its allowance for credit losses. The amendments in this ASU are effective for public entities as of the end of a reporting period for interim and annual reporting periods ending on or after December 15, 2010. The disclosures about activity that occurs during a reporting period are effective for interim and annual reporting periods beginning on or after December 15, 2010. For nonpublic entities, the disclosures are effective for annual reporting periods ending on or after December 15, 2011.

In December 2010, the FASB issued ASU 2010-28, “Intangibles - Goodwill and Other.” This ASU is to addresses when to perform step 2 of the goodwill impairment test for reporting units with zero or negative carrying amounts. For public entities, the amendments in this ASU are effective for fiscal years, and interim periods beginning after December 15, 2010. For nonpublic entities, the amendments are effective for fiscal years and interim periods beginning after December 15, 2011.

In December 2010, the FASB issued ASU 2010-29, “Disclosure of Supplementary Pro Forma Information for Business Combinations.” This ASU addresses diversity in practice about the interpretation of the pro forma revenue and earnings disclosure requirements for business combinations. This ASU is effective prospectively for business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2010.

NOTE 3 - INVESTMENTS IN AVAILABLE-FOR-SALE SECURITIES

Debt and equity securities have been classified in the consolidated balance sheets according to management’s intent. The amortized cost of securities and their approximate fair values are as follows as of December 31:

| | | | | | | | | | | | | |

| | | Amortized

Cost

Basis | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair

Value | |

| December 31, 2010: | | | | | | | | | | | | |

| Debt securities issued by the U.S. Treasury and other U.S. government corporations and agencies | | $ | 10,749,626 | | | $ | 76,693 | | | $ | 35,297 | | | $ | 10,791,022 | |

| Obligations of states and municipalities | | | 11,607,144 | | | | 94,764 | | | | 135,763 | | | | 11,566,145 | |

| Corporate debt securities | | | 1,003,447 | | | | 21,281 | | | | 2,633 | | | | 1,022,095 | |

| Mortgage-backed securities | | | 21,026,171 | | | | 453,027 | | | | 172,085 | | | | 21,307,113 | |

| SBA loan pools | | | 1,459,431 | | | | 108,893 | | | | - | | | | 1,568,324 | |

| U.S. government sponsored enterprises perpetual/callable preferred stocks | | | 16,500 | | | | 17,998 | | | | - | | | | 34,498 | |

| Marketable equity securities | | | 8,342,967 | | | | - | | | | - | | | | 8,342,967 | |

| | | | 54,205,286 | | | | 772,656 | | | | 345,778 | | | | 54,632,164 | |

| Money market mutual funds included in cash and cash equivalents | | | (8,342,967 | ) | | | - | | | | - | | | | (8,342,967 | ) |

| Total available-for-sale securities | | $ | 45,862,319 | | | $ | 772,656 | | | $ | 345,778 | | | $ | 46,289,197 | |

| | | | | | | | | | | | | |

| | | Amortized

Cost

Basis | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair

Value | |

| December 31, 2009: | | | | | | | | | | | | |

| Debt securities issued by the U.S. Treasury and other U.S. government corporations and agencies | | $ | 15,723,378 | | | $ | 56,246 | | | $ | 12,563 | | | $ | 15,767,061 | |

| Obligations of states and municipalities | | | 9,977,623 | | | | 159,024 | | | | 34,238 | | | | 10,102,409 | |

| Corporate debt securities | | | 508,673 | | | | 27,012 | | | | - | | | | 535,685 | |

| Mortgage-backed securities | | | 21,772,298 | | | | 322,668 | | | | 253,165 | | | | 21,841,801 | |

| SBA loan pools | | | 1,639,685 | | | | 67,480 | | | | - | | | | 1,707,165 | |

| U.S. government sponsored enterprises perpetual/callable preferred stocks | | | 16,500 | | | | 40,695 | | | | - | | | | 57,195 | |

| Marketable equity securities | | | 1,352,711 | | | | - | | | | - | | | | 1,352,711 | |

| | | | 50,990,868 | | | | 673,125 | | | | 299,966 | | | | 51,364,027 | |

| Money market mutual funds included in cash and cash equivalents | | | (1,352,711 | ) | | | - | | | | - | | | | (1,352,711 | ) |

| Total available-for-sale securities | | $ | 49,638,157 | | | $ | 673,125 | | | $ | 299,966 | | | $ | 50,011,316 | |

The scheduled maturities of securities were as follows as of December 31, 2010:

| | | | Fair

Value | |

| Due within one year | | $ | 497,536 | |

| Due after one year through five years | | | 12,319,807 | |

| Due after five years through ten years | | | 3,486,090 | |

| Due after ten years | | | 7,110,327 | |

| SBA loan pools | | | 1,568,324 | |

| Mortgage-backed securities | | | 21,307,113 | |

| | | $ | 46,289,197 | |

There were no sales of available-for-sale securities during the year ended December 31, 2010. During 2009, proceeds from sales of available-for-sale securities amounted to $1,170,316. Gross realized gains on those sales amounted to $39,491. The tax benefit applicable to these gross realized gains amounted to $15,382.

There were no securities of issuers whose aggregate carrying amount exceeded 10% of stockholders’ equity as of December 31, 2010.

As of December 31, 2010 and 2009, the total carrying amounts of securities pledged for securities sold under agreements to repurchase and public deposits were $16,587,463 and $11,037,829, respectively.

The aggregate fair value and unrealized losses of securities that have been in a continuous unrealized loss position for less than twelve months and for twelve months or more, and are not other than temporarily impaired, are as follows:

| | | Less than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | |

| December 31, 2010: | | | | | | | | | | | | | | | | | | |

Debt securities issued by the U.S. Treasury and other U.S. government corporations and agencies | | $ | 5,214,703 | | | $ | 35,297 | | | $ | - | | | $ | - | | | $ | 5,214,703 | | | $ | 35,297 | |

| Obligations of states and municipalities | | | 3,759,853 | | | | 135,763 | | | | - | | | | - | | | | 3,759,853 | | | | 135,763 | |

| Corporate debt securities | | | 496,130 | | | | 2,633 | | | | - | | | | - | | | | 496,130 | | | | 2,633 | |

| Mortgage-backed securities | | | 3,900,106 | | | | 61,665 | | | | 847,756 | | | | 110,420 | | | | 4,747,862 | | | | 172,085 | |

| Total temporarily impaired securities | | $ | 13,370,792 | | | $ | 235,358 | | | $ | 847,756 | | | $ | 110,420 | | | $ | 14,218,548 | | | $ | 345,778 | |

| | | Less than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | |

| December 31, 2009: | | | | | | | | | | | | | | | | | | |

Debt securities issued by the U.S. Treasury and other U.S. government corporations and agencies | | $ | 2,988,620 | | | $ | 12,563 | | | $ | - | | | $ | - | | | $ | 2,988,620 | | | $ | 12,563 | |

| Obligations of states and municipalities | | | 3,044,480 | | | | 34,238 | | | | - | | | | - | | | | 3,044,480 | | | | 34,238 | |

| Mortgage-backed securities | | | 2,227,512 | | | | 17,610 | | | | 1,317,233 | | | | 235,555 | | | | 3,544,745 | | | | 253,165 | |

| Total temporarily impaired securities | | $ | 8,260,612 | | | $ | 64,411 | | | $ | 1,317,233 | | | $ | 235,555 | | | $ | 9,577,845 | | | $ | 299,966 | |

The investments in the Company’s investment portfolio that are temporarily impaired as of December 31, 2010 consist of debt issued by states of the United States and political subdivisions of the states, U.S. corporations, and U.S. government corporations and agencies. Company management considers investments with an unrealized loss as of December 31, 2010 to be only temporarily impaired because the impairment is attributable to changes in market interest rates and current market inefficiencies. Company management anticipates that the fair value of securities that are currently impaired will recover to cost basis. As management has the ability to hold securities for the foreseeable future no declines are deemed to be other than temporary.

NOTE 4 - LOANS

Loans consisted of the following as of December 31:

| | | 2010 | | | 2009 | |

| Commercial, financial and agricultural | | $ | 13,568,271 | | | $ | 12,900,649 | |

| Real estate - construction and land development | | | 4,986,546 | | | | 6,744,569 | |

| Real estate - residential | | | 148,396,036 | | | | 138,408,956 | |

| Real estate - commercial | | | 31,293,763 | | | | 28,721,564 | |

| Municipal | | | 2,034,597 | | | | 2,015,318 | |

| Consumer | | | 4,512,092 | | | | 4,473,822 | |

| | | | 204,791,305 | | | | 193,264,878 | |

| Allowance for loan losses | | | (2,325,687 | ) | | | (2,211,301 | ) |

| Deferred costs, net | | | 326,859 | | | | 249,942 | |

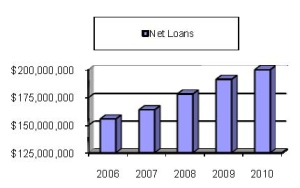

| Net loans | | $ | 202,792,477 | | | $ | 191,303,519 | |

Changes in the allowance for loan losses were as follows for the years ended December 31:

| | | 2010 | | | 2009 | |

| Balance at beginning of year | | $ | 2,211,301 | | | $ | 2,017,145 | |

| Provision for loan losses | | | 755,000 | | | | 547,000 | |

| Charge offs | | | (646,761 | ) | | | (358,097 | ) |

| Recoveries of loans previously charged off | | | 6,147 | | | | 5,253 | |

| Balance at end of year | | $ | 2,325,687 | | | $ | 2,211,301 | |

The following table sets forth information regarding the allowance for loan losses by portfolio segment as of December 31, 2010:

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Real Estate: | | | | | | | | | | | | | |

| | | Residential | | | Commercial | | | Construction and Land Development | | | Home Equity | | | Commerical

& Industrial | | | Consumer | | | Unallocated | | | Total | |

| Allowance: | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: | | | | | | | | | | | | | | | | | | | | | | | | |

| Individually evaluated for impairment | | $ | 79,000 | | | $ | - | | | $ | - | | | $ | 600 | | | $ | - | | | $ | - | | | $ | - | | | $ | 79,600 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Collectively evaluated for impairment | | | 759,321 | | | | 464,526 | | | | 67,655 | | | | 359,680 | | | | 410,355 | | | | 93,579 | | | | 90,971 | | | | 2,246,087 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total allowance | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| for loan lease loss ending balance | | $ | 838,321 | | | $ | 464,526 | | | $ | 67,655 | | | $ | 360,280 | | | $ | 410,355 | | | $ | 93,579 | | | $ | 90,971 | | | $ | 2,325,687 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Individually evaluated for impairment | | $ | 384,094 | | | $ | 326,406 | | | $ | 1,000,743 | | | $ | 7,802 | | | $ | - | | | $ | - | | | $ | - | | | $ | 1,719,045 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Collectively evaluated for impairment | | | 100,302,895 | | | | 30,997,736 | | | | 3,990,265 | | | | 47,927,571 | | | | 15,661,681 | | | | 4,518,971 | | | | - | | | | 203,399,119 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total loans | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ending balance | | $ | 100,686,989 | | | $ | 31,324,142 | | | $ | 4,991,008 | | | $ | 47,935,373 | | | $ | 15,661,681 | | | $ | 4,518,971 | | | $ | - | | | $ | 205,118,164 | |

The following table presents the Company’s loans by risk rating as of December 31, 2010:

Credit quality indicators

| | | Real Estate | | | | | | | | | | |

| | | Residential | | | Commercial | | | Construction

and Land

Development | | | Home Equity | | | Commerical

and Industrial | | | Consumer | | | Total | |

| Grade: | | | | | | | | | | | | | | | | | | | | | |

| Pass | | $ | 99,658,355 | | | $ | 28,802,453 | | | $ | 3,650,310 | | | $ | 47,515,158 | | | $ | 14,392,933 | | | $ | 4,510,408 | | | $ | 198,529,617 | |

| Special Mention | | | 259,610 | | | | 1,797,703 | | | | 339,955 | | | | - | | | | 162,364 | | | | - | | | | 2,559,632 | |

| Substandard | | | 769,024 | | | | 723,986 | | | | 1,000,743 | | | | 420,215 | | | | 1,106,384 | | | | 8,563 | | | | 4,028,915 | |

| Total | | $ | 100,686,989 | | | $ | 31,324,142 | | | $ | 4,991,008 | | | $ | 47,935,373 | | | $ | 15,661,681 | | | $ | 4,518,971 | | | $ | 205,118,164 | |

Credit Quality Indicators: As part of the ongoing monitoring of the credit quality of the Company’s loan portfolio, management tracks certain credit quality indicators including trends related to (i) weighted average risk rating of commercial loans; (ii) the level of classified and criticized commercial loans; (iii) non performing loans; (iv) net charge-offs and (v) the general economic conditions within the State of Connecticut.

The Company utilizes a risk rating grading matrix to assign a risk grade to each of its commercial loans. Loans are graded on a scale of 1 to 7. A description of each rating class is as follows:

Risk Rating 1 (Superior) – This risk rating is assigned to loans secured by cash.

Risk Rating 2 (Good) – This risk rating is assigned to borrowers of high credit quality who have primary and secondary sources of repayment which are well defined and fully confirmed.

Risk Rating 3 (Satisfactory) – This risk rating is assigned to borrowers who are fully responsible for the loan or credit commitment, which has primary and secondary sources of repayment that are well defined and adequately confirmed. Most credit factors are favorable, and the credit exposure is managed through normal monitoring.

Risk Rating 3.5 (Bankable with Care) – This risk rating is assigned to borrowers who are fully responsible for the loan or credit commitment and the secondary sources of repayment are weak. These loans may require more than the average amount of attention from the relationship manager.

Risk Rating 4 (Special Mention) – This risk rating is assigned to borrowers which may be adequately protected by the present debt service capacity and tangible net worth of the borrower, but which have potential problems that could, if not checked or corrected, eventually weaken these assets or otherwise jeopardize the repayment of principal and interest as originally intended. Most credit factors are unfavorable, and the credit exposure requires immediate corrective action

Risk Rating 5 (Substandard) – This risk rating is assigned to borrowers who have inadequate cash flow or collateral to satisfy their loan obligations as originally defined in the loan agreement. Substandard loans may be placed on nonaccrual status if the conditions described above are generally met.

Risk Rating 6 (Doubtful) – This risk rating is assigned to a borrower or portion of a borrower’s loan with which the Company is no longer certain of its collectability. A specific reserve allocation is assigned to this portion of the loan.

Risk Rating 7 (Loss) – This risk rating is assigned to loans which have been charged off or the portion of the loan that has been charged down. “Loss” does not imply that the loan, or portion of, will never be paid, nor does it imply that there has been a forgiveness of debt.

An age analysis of past-due loans, segregated by class of loans, as of December 31, 2010 is as follows:

| | | 30-59 Days | | | 60-89 Days | | | Greater

than 90 Days | | | Total

Past Due | | | Recorded

Investment >

90 Days

and Accruing | |

| Real estate: | | | | | | | | | | | | | | | |

| Residential | | $ | 529,324 | | | $ | - | | | $ | 324,455 | | | $ | 853,779 | | | $ | - | |

| Commercial | | | - | | | | 254,548 | | | | 71,858 | | | | 326,406 | | | | - | |

| Construction and land development | | | - | | | | - | | | | 1,000,743 | | | | 1,000,743 | | | | - | |

| Commercial and industrial | | | - | | | | - | | | | 203,117 | | | | 203,117 | | | | - | |

| Consumer | | | 72,503 | | | | 526 | | | | 8,620 | | | | 81,649 | | | | - | |

| Total | | $ | 601,827 | | | $ | 255,074 | | | $ | 1,608,793 | | | $ | 2,465,694 | | | $ | - | |

The following table sets forth information regarding nonaccrual loans as of December 31, 2010:

| Real Estate: | | | |

| Residential | | $ | 541,969 | |

| Commercial | | | 326,406 | |

| Construction and land development | | | 1,000,743 | |

| Home equity | | | 420,215 | |

| Consumer | | | 17,183 | |

| Total nonaccrual loans | | $ | 2,306,516 | |

The following table sets forth information regarding nonaccrual loans and accruing loans 90 days or more overdue as of December 31, 2009:

| Total nonaccrual loans | | $ | 3,153,187 | |

| | | | | |

| Accruing loans which are 90 days or more overdue | | $ | 202,024 | |

Information about loans that meet the definition of an impaired loan in ASC 310-10-35 is as follows as of and for the year ended December 31, 2010.

| | | Recorded

Investment | | | Unpaid

Principal

Balance | | | Related

Allowance | |

| December 31, 2010: | | | | | | | | | |

| With no related allowance recorded: | | | | | | | | | |

| Real Estate: | | | | | | | | | |

| Commercial | | $ | 326,406 | | | $ | 325,340 | | | $ | - | |

| Construction and land development | | | 1,000,743 | | | | 1,000,838 | | | | - | |

| Total impaired with no related allowance | | | 1,327,149 | | | | 1,326,178 | | | | - | |

| | | | | | | | | | | | | |

| With an allowance recorded: | | | | | | | | | | | | |

| Real Estate: | | | | | | | | | | | | |

| Residential | | | 384,094 | | | | 400,747 | | | | 79,000 | |

| Home equity | | | 7,802 | | | | 7,703 | | | | 600 | |

| Total impaired with an allowance recorded | | | 391,896 | | | | 408,450 | | | | 79,600 | |

| Total: | | | | | | | | | | | | |

| Real Estate: | | | | | | | | | | | | |

| Residential | | | 384,094 | | | | 400,747 | | | | 79,000 | |

| Commercial | | | 326,406 | | | | 325,340 | | | | - | |

| Construction and land development | | | 1,000,743 | | | | 1,000,838 | | | | - | |

| Home equity | | | 7,802 | | | | 7,703 | | | | 600 | |

| | | $ | 1,719,045 | | | $ | 1,734,628 | | | $ | 79,600 | |

| | | Recorded | |

| | | Investment | |

| Average recorded investment in impaired loans | | | |

| during the year ended December 31, 2010 | | $ | 2,027,326 | |

| | | | | |

| Related amount of interest income recognized during the | | | | |

| time, in the year ended December 31, 2010 that the loans | | | | |

| were impaired | | | | |

| | | | | |

| Total recognized | | $ | 35,260 | |

| | | | | |

| Amount recognized using a cost-basis method of accounting | | $ | 34,380 | |

Information about loans that meet the definition of an impaired loan in ASC 310-10-35 is as follows as of and for the year ended December 31, 2009:

| | | 2009 | |

| | | Recorded

Investment

in Impaired

Loans | | | Related

Allowance

for Credit

Losses | |

| Loans for which there is a related allowance for credit losses | | $ | 353,613 | | | $ | 160,000 | |

| | | | | | | | | |

| Loans for which there is no related allowance for credit losses | | | 1,911,995 | | | | - | |

| | | | | | | | | |

| Totals | | $ | 2,265,608 | | | $ | 160,000 | |

| | | | | | | | | |

| Average recorded investment in impaired loans during the year ended December 31, 2009 | | $ | 1,215,532 | | | | | |

| | | | | | | | | |

| Related amount of interest income recognized during the time, in the year ended December 31, 2009 that the loans were impaired | | | | | | | | |

| Total recognized | | $ | 560 | | | | | |

| Amount recognized using a cash-basis method of accounting | | $ | - | | | | | |

NOTE 5 - PREMISES AND EQUIPMENT

The following is a summary of premises and equipment as of December 31:

| | | 2010 | | | 2009 | |

| Leasehold improvements | | $ | 1,178,612 | | | $ | 1,155,367 | |

| Furniture and equipment | | | 2,369,883 | | | | 2,302,763 | |

| | | | 3,548,495 | | | | 3,458,130 | |

| Accumulated depreciation and amortization | | | (2,986,782 | ) | | | (2,773,836 | ) |

| | | $ | 561,713 | | | $ | 684,294 | |

NOTE 6 - DEPOSITS

The aggregate amount of time deposit accounts in denominations of $100,000 or more as of December 31, 2010 and 2009 was $32,242,306 and $34,678,968, respectively.

For time deposits as of December 31, 2010, the scheduled maturities for years ended December 31 are:

| 2011 | | $ | 55,664,340 | |

| 2012 | | | 13,405,673 | |

| 2013 | | | 2,653,084 | |

| 2014 | | | 2,954,258 | |

| 2015 | | | 3,054,984 | |

| Total | | $ | 77,732,339 | |

NOTE 7 - SECURITIES SOLD UNDER AGREEMENTS TO REPURCHASE

Securities sold under agreements to repurchase consist of funds borrowed from customers on a short-term basis secured by portions of the Company's investment portfolio. The securities which were sold have been accounted for not as sales but as borrowings. The securities consisted of debt securities issued by the U.S. Treasury and other U.S. government sponsored enterprises, corporations and agencies and states and municipalities. The securities were held in safekeeping by Morgan Stanley, under the control of the Company. The purchasers have agreed to sell to the Company substantially identical securities at the maturity of the agreements. The agreements mature generally within three months from date of issue.

NOTE 8 - FEDERAL HOME LOAN BANK ADVANCES

Advances consist of funds borrowed from the Federal Home Loan Bank (FHLB). There were no FHLB advances outstanding as of December 31, 2010 and 2009.

Borrowings from the FHLB are secured by a blanket lien on qualified collateral, consisting primarily of loans with first mortgages secured by one to four family properties and other qualified assets.

The Company has a line of credit with the FHLB in the amount of $1,525,000 at December 31, 2010 and 2009. At December 31, 2010 and 2009, there were no advances outstanding under this line of credit.

NOTE 9 - INCOME TAX EXPENSE

The components of income tax expense are as follows for the years ended December 31:

| | | 2010 | | | 2009 | |

| Current: | | | | | | |

| Federal | | $ | 262,551 | | | $ | 184,014 | |

| State | | | 99,543 | | | | 61,452 | |

| | | | 362,094 | | | | 245,466 | |

| Deferred: | | | | | | | | |

| Federal | | | (1,469 | ) | | | (30,352 | ) |

| State | | | 1,469 | | | | 12,599 | |

| | | | - | | | | (17,753 | ) |

| Total income tax expense | | $ | 362,094 | | | $ | 227,713 | |

The reasons for the differences between the statutory federal income tax rate and the effective tax rates are summarized as follows for the years ended December 31:

| | | 2010 | | | 2009 | |

| | | % of | | | % of | |

| | | Income | | | Income | |

| Federal income tax at statutory rate | | | 34.0 | % | | | 34.0 | % |

| Increase (decrease) in tax resulting from: | | | | | | | | |

| Tax-exempt income | | | (15.5 | ) | | | (20.0 | ) |

| Other | | | 1 | | | | 3.3 | |

| Stock-based compensation | | | 0.2 | | | | 1.6 | |

| State tax expense, net of federal benefit | | | 4.3 | | | | 5.2 | |

| Effective tax rates | | | 24.0 | % | | | 24.1 | % |

The Company had gross deferred tax assets and gross deferred tax liabilities as follows as of December 31:

| | | 2010 | | | 2009 | |

| Deferred tax assets: | | | | | | |

| Allowance for loan losses | | $ | 798,326 | | | $ | 803,109 | |

| Deferred compensation | | | 88,146 | | | | 61,350 | |

| Other | | | - | | | | 24,456 | |

| Impairment of operating lease | | | 78,988 | | | | 96,221 | |

| Write-down of equity securities | | | 772,573 | | | | 772,573 | |

| Alternative minimum tax carryforward | | | 115,662 | | | | 83,375 | |

| Gross deferred tax assets | | | 1,853,695 | | | | 1,841,084 | |

| | | | | | | | | |

| Deferred tax liabilities: | | | | | | | | |

| Depreciation | | | (15,181 | ) | | | (34,475 | ) |

| Deferred loan costs/fees | | | (127,313 | ) | | | (97,351 | ) |

| Other | | | (1,943 | ) | | | - | |

| Net unrealized holdings gain on available-for-sale securities | | | (166,269 | ) | | | (145,345 | ) |

| Gross deferred tax liabilities | | | (310,706 | ) | | | (277,171 | ) |

| Net deferred tax asset | | $ | 1,542,989 | | | $ | 1,563,913 | |

Deferred tax assets as of December 31, 2010 and 2009 have not been reduced by a valuation allowance because management believes that it is more likely than not that the full amount of deferred taxes will be realized.

As of December 31, 2010, the Company had no operating loss carryovers for income tax purposes.

It is the Company’s policy to provide for uncertain tax positions and the related interest and penalties based upon management’s assessment of whether a tax benefit is more likely than not to be sustained upon examination by tax authorities. As of December 31, 2010 and 2009, there were no material uncertain tax positions related to federal and state income tax matters. The Company is currently open to audit under the statute of limitations by the Internal Revenue Service and state taxing authorities for the years ended December 31, 2007 through December 31, 2010.

NOTE 10 - COMMITMENTS AND CONTINGENT LIABILITIES

As of December 31, 2010 the Company was obligated under non-cancelable operating leases for bank premises and equipment expiring between March 2011 and May 2016. The total minimum rental due in future periods under these existing agreements is as follows as of December 31, 2010:

| 2011 | | $ | 501,903 | |

| 2012 | | | 458,524 | |

| 2013 | | | 446,966 | |

| 2014 | | | 385,082 | |

| 2015 | | | 282,491 | |

| Thereafter | | | 47,839 | |

Total | | $ | 2,122,805 | |

Certain leases contain provisions for escalation of minimum lease payments contingent upon percentage increases in the consumer price index. Total rental expense amounted to $600,343 and $597,445 for the years ended December 31, 2010 and 2009, respectively.

On November 28, 2008, the Company entered into an agreement with its data processing servicer which ends in five years, and automatically continues for three years, unless terminated by either party with notice. Under the agreement, the Company must pay a termination fee as described in the agreement if the Company terminates the agreement with notice, before the end of the agreement.

NOTE 11 - FAIR VALUE MEASUREMENTS

ASC 820-10, “Fair Value Measurements and Disclosures,” provides a framework for measuring fair value under generally accepted accounting principles. This guidance also allows an entity the irrevocable option to elect fair value for the initial and subsequent measurement for certain financial assets and liabilities on a contract-by-contract basis.

In accordance with ASC 820-10, the Company groups its financial assets and financial liabilities measured at fair value in three levels, based on the markets in which the assets and liabilities are traded and the reliability of the assumptions used to determine fair value.

Level 1 - Valuations for assets and liabilities traded in active exchange markets, such as the New York Stock Exchange. Level 1 also includes U.S. Treasury, other U.S. Government and agency mortgage-backed securities that are traded by dealers or brokers in active markets. Valuations are obtained from readily available pricing sources for market transactions involving identical assets or liabilities.

Level 2 - Valuations for assets and liabilities traded in less active dealer or broker markets. Valuations are obtained from third party pricing services for identical or comparable assets or liabilities.

Level 3 - Valuations for assets and liabilities that are derived from other methodologies, including option pricing models, discounted cash flow models and similar techniques, are not based on market exchange, dealer, or broker traded transactions. Level 3 valuations incorporate certain assumptions and projections in determining the fair value assigned to such assets and liabilities.

A financial instrument’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The Company did not have any significant transfers of assets between Level 1 and Level 2 of the fair value hierarchy during the year ended December 31, 2010.

A description of the valuation methodologies used for instruments measured at fair value, as well as the general classification of such instruments pursuant to the valuation hierarchy, is set forth below. These valuation methodologies were applied to all of the Company’s financial assets and financial liabilities carried at fair value for December 31, 2010 and 2009.

The Company’s cash instruments are generally classified within Level 1 or Level 2 of the fair value hierarchy because they are valued using quoted market prices, broker or dealer quotations, or alternative pricing sources with reasonable levels of price transparency.

The Company’s investment in obligations of states and municipalities, mortgage-backed securities and other debt securities available-for-sale are generally classified within Level 2 of the fair value hierarchy. For these securities, we obtain fair value measurements from independent pricing services. The fair value measurements consider observable data that may include dealer quotes, market spreads, cash flows, the U.S. treasury yield curve, trading levels, market consensus prepayment speeds, credit information, and the instrument’s terms and conditions.

Level 3 is for positions that are not traded in active markets or are subject to transfer restrictions, valuations are adjusted to reflect illiquidity and/or non-transferability, and such adjustments are generally based on available market evidence. In the absence of such evidence, management’s best estimate is used. Subsequent to inception, management only changes Level 3 inputs and assumptions when corroborated by evidence such as transactions in similar instruments, completed or pending third-party transactions in the underlying investment or comparable entities, subsequent rounds of financing, recapitalization and other transactions across the capital structure, offerings in the equity or debt markets, and changes in financial ratios or cash flows.

The Company’s impaired loans are reported at the fair value of the underlying collateral if repayment is expected solely from the collateral. Collateral values are estimated using Level 2 inputs based upon appraisals of similar properties obtained from a third party. For Level 3 inputs, fair values are based on management estimates.

Other real estate owned values are estimated using Level 2 inputs based upon appraisals of similar properties obtained from a third party. For Level 3 inputs, fair values are based on management estimates.

The following summarizes assets measured at fair value for the period ending December 31, 2010 and 2009.

ASSETS MEASURED AT FAIR VALUE ON A RECURRING BASIS

| | | Fair Value Measurements at Reporting Date Using: | |

| | | | | | Quoted Prices in | | | Significant | | | Significant | |

| | | | | | Active Markets for | | | Other Observable | | | Unobservable | |

| | | | | | Identical Assets | | | Inputs | | | Inputs | |

| | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

| December 31, 2010: | | | | | | | | | | | | |

| Securities available-for-sale | | $ | 46,289,197 | | | $ | 34,498 | | | $ | 46,254,699 | | | $ | - | |

| Totals | | $ | 46,289,197 | | | $ | 34,498 | | | $ | 46,254,699 | | | $ | - | |

| | | | | | | | | | | | | | | | | |

| December 31, 2009: | | | | | | | | | | | | | | | | |

| Securities available-for-sale | | $ | 50,011,316 | | | $ | 57,195 | | | $ | 49,954,121 | | | $ | - | |

| Totals | | $ | 50,011,316 | | | $ | 57,195 | | | $ | 49,954,121 | | | $ | - | |

Under certain circumstances we make adjustments to fair value for our assets and liabilities although they are not measured at fair value on an ongoing basis. The following table presents the financial instruments carried on the consolidated balance sheet by caption and by level in the fair value hierarchy, at December 31, 2010 and 2009, for which a nonrecurring change in fair value has been recorded:

ASSETS MEASURED AT FAIR VALUE ON A NONRECURRING BASIS

| | | Fair Value Measurements at Reporting Date Using: | |

| | | | | | Quoted Prices in | | | Significant | | | Significant | |

| | | | | | Active Markets for | | | Other Observable | | | Unobservable | |

| | | | | | Identical Assets | | | Inputs | | | Inputs | |

| | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

| December 31, 2010: | | | | | | | | | | | | |

| Impaired loans | | $ | 312,296 | | | $ | - | | | $ | - | | | $ | 312,296 | |

| Totals | | $ | 312,296 | | | $ | - | | | $ | - | | | $ | 312,296 | |

| | | | | | | | | | | | | | | | | |

| December 31, 2009: | | | | | | | | | | | | | | | | |

| Impaired loans | | $ | 193,613 | | | $ | - | | | $ | 193,613 | | | $ | - | |

| Totals | | $ | 193,613 | | | $ | - | | | $ | 193,613 | | | $ | - | |

| | | Fair Value Measurements | |

| | | Using Significant Unobservable Inputs | |

| | | Level 3 | |

| | | Impaired Loans | |

| Beginning balance, December 31, 2009 | | $ | - | |

| Transfers in and/or out of Level 3 | | | 312,296 | |

| Ending balance, December 31, 2010 | | $ | 312,296 | |

The estimated fair values of the Company’s financial instruments, all of which are held or issued for purposes other than trading, are as follows as of December 31:

| | | 2010 | | | 2009 | |

| | | Carrying | | | Fair | | | Carrying | | | Fair | |

| | | Amount | | | Value | | | Amount | | | Value | |

| Financial assets: | | | | | | | | | | | | |

| Cash and cash equivalents | | $ | 30,871,344 | | | $ | 30,871,344 | | | $ | 17,089,409 | | | $ | 17,089,409 | |

| Interest-bearing time deposits with other banks | | | 5,963,426 | | | | 6,257,000 | | | | 5,488,037 | | | | 5,690,000 | |

| Available-for-sale securities | | | 46,289,197 | | | | 46,289,197 | | | | 50,011,316 | | | | 50,011,316 | |

| Federal Home Loan Bank stock | | | 659,600 | | | | 659,600 | | | | 630,700 | | | | 630,700 | |

| Loans, net | | | 202,792,477 | | | | 204,841,000 | | | | 191,303,519 | | | | 193,185,000 | |

| Accrued interest receivable | | | 904,896 | | | | 904,896 | | | | 977,350 | | | | 977,350 | |

| Financial liabilities: | | | | | | | | | | | | | | | | |

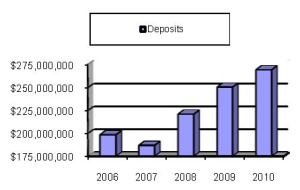

| Deposits | | | 269,279,026 | | | | 270,082,000 | | | | 250,445,682 | | | | 251,268,000 | |

| Securities sold under agreements to repurchase | | | 3,235,083 | | | | 3,235,083 | | | | 912,849 | | | | 912,849 | |

The carrying amounts of financial instruments shown in the above table are included in the consolidated balance sheets under the indicated captions. Accounting policies related to financial instruments are described in Note 2.

NOTE 12 - FINANCIAL INSTRUMENTS

The Company is party to financial instruments with off-balance sheet risk in the normal course of business to meet the financing needs of its customers. These financial instruments include commitments to originate loans, unadvanced funds on loans and standby letters of credit. The instruments involve, to varying degrees, elements of credit risk in excess of the amount recognized in the balance sheets. The contract amounts of those instruments reflect the extent of involvement the Company has in particular classes of financial instruments.

The Company's exposure to credit loss in the event of nonperformance by the other party to the financial instrument for loan commitments is represented by the contractual amounts of those instruments. The Company uses the same credit policies in making commitments and conditional obligations as it does for on-balance sheet instruments.

Commitments to originate loans are agreements to lend to a customer provided there is no violation of any condition established in the contract. Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee. Since many of the commitments are expected to expire without being drawn upon, the total commitment amounts do not necessarily represent future cash requirements. The Company evaluates each customer's creditworthiness on a case-by-case basis. The amount of collateral obtained, if deemed necessary by the Company upon extension of credit, is based on management's credit evaluation of the borrower. Collateral held varies, but may include secured interests in mortgages, accounts receivable, inventory, property, plant and equipment and income-producing properties.

Standby letters of credit are conditional commitments issued by the Company to guarantee the performance by a customer to a third party. The credit risk involved in issuing letters of credit is essentially the same as that involved in extending loan facilities to customers. As of December 31, 2010 and 2009, the maximum potential amount of the Company’s obligation was $233,400 and $337,000, respectively for financial and standby letters of credit. The Company’s outstanding letters of credit generally have a term of less than one year. If a letter of credit is drawn upon, the Company may seek recourse through the customer’s underlying line of credit. If the customer’s line of credit is also in default, the Company may take possession of the collateral, if any, securing the line of credit.

Notional amounts of financial instrument liabilities with off-balance-sheet credit risk are as follows as of December 31:

| | | 2010 | | | 2009 | |

| Commitments to originate loans | | $ | 2,701,250 | | | $ | 1,498,580 | |

| Standby letters of credit | | | 233,400 | | | | 337,000 | |

| Unadvanced portions of loans: | | | | | | | | |

| Construction | | | 4,321,442 | | | | 3,473,939 | |

| Commercial lines of credit | | | 7,857,538 | | | | 7,743,686 | |

| Consumer | | | 735,355 | | | | 701,361 | |

| Home equity | | | 24,119,575 | | | | 24,231,520 | |

| | | $ | 39,968,560 | | | $ | 37,986,086 | |

There is no material difference between the notional amounts and the estimated fair values of the above off-balance sheet liabilities.

NOTE 13 - RELATED PARTY TRANSACTIONS

Certain directors and executive officers of the Company and companies in which they have significant ownership interest were customers of the Bank during 2010. Total loans to such persons and their companies amounted to $4,700,867 as of December 31, 2010. During the year ended December 31, 2010 principal payments totaled $2,695,414 and advances amounted to $2,740,101.

Deposits from related parties held by the Company as of December 31, 2010 and 2009 amounted to $4,408,009 and $3,434,620, respectively.

During 2010 and 2009, the Company paid $56,711 and $65,420, respectively, for rent and related expenses of the Company’s Granby branch office to a company of which a bank director is a principal. The rent expense for the Granby branch included in Note 10 amounted to $43,078 in 2010 and $44,935 in 2009.

NOTE 14 - SIGNIFICANT GROUP CONCENTRATIONS OF CREDIT RISK

Most of the Company's business activity is with customers located within the state. There are no concentrations of credit to borrowers that have similar economic characteristics. The majority of the Company's loan portfolio is comprised of loans collateralized by real estate located in the state of Connecticut.

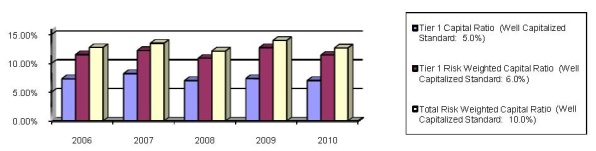

NOTE 15 - REGULATORY MATTERS

The Bank is subject to various regulatory capital requirements administered by the federal banking agencies. Failure to meet minimum capital requirements can initiate certain mandatory and possibly additional discretionary actions by regulators that, if undertaken, could have a direct material effect on the Bank’s financial statements. Under capital adequacy guidelines and the regulatory framework for prompt corrective action, the Bank must meet specific capital guidelines that involve quantitative measures of its assets, liabilities, and certain off-balance-sheet items as calculated under regulatory accounting practices. The Bank’s capital amounts and classification are also subject to qualitative judgments by the regulators about components, risk weightings and other factors.

Quantitative measures established by regulation to ensure capital adequacy require the Bank to maintain minimum amounts and ratios (set forth in the table below) of total and Tier 1 capital (as defined in the regulations) to risk-weighted assets (as defined), and of Tier 1 capital (as defined) to average assets (as defined). Management believes, as of December 31, 2010 and 2009, that the Bank meets all capital adequacy requirements to which it is subject.

As of December 31, 2010, the most recent notification from the Federal Deposit Insurance Corporation categorized the Bank as well capitalized under the regulatory framework for prompt corrective action. To be categorized as well capitalized the Bank must maintain minimum total risk-based, Tier 1 risk-based and Tier 1 leverage ratios as set forth in the table. There are no conditions or events since that notification that management believes have changed the institution's category.

The Bank’s actual capital amounts and ratios are also presented in the table.

| | | | | | | | | | | | | To Be Well |

| | | | | | | | | | | | | Capitalized Under |

| | | | | | | | | For Capita | | Prompt Corrective |

| | | Actual | | | Adequacy Purposes | | Action Provisions |

| | | Amount | | | Ratio | | | Amount | | Ratio | | Amount | | Ratio |

| | | (Dollar amounts in thousands) |

| As of December 31, 2010: |

| Total Capital (to Risk Weighted Assets): | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | $ | 23,150 | | | | 12.66 | % | | $ | 14,624 | | > 8.0% | | $ | 18,280 | | > 10.0% |

| Tier 1 Capital (to Risk Weighted Assets): | | | | | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | | 20,864 | | | | 11.41 | | | | 7,312 | | > 4.0 | | | 10,968 | | > 6.0 |

| Tier 1 Capital (to Average Assets): | | | | | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | | 20,864 | | | | 7.00 | | | | 11,921 | | > 4.0 | | | 14,901 | | > 5.0 |

| | | | | | | | | | | | | | | | | | | |

| As of December 31, 2009: |

| Total Capital (to Risk Weighted Assets): | | | | | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | | 22,512 | | | | 13.97 | | | | 12,896 | | >8.0 | | | 16,119 | | >10.0 |

| Tier 1 Capital (to Risk Weighted Assets): | | | | | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | | 20,495 | | | | 12.71 | | | | 6,448 | | >4.0 | | | 9,672 | | >6.0 |

| Tier 1 Capital (to Average Assets): | | | | | | | | | | | | | | | | | | |

| Simsbury Bank & Trust Company, Inc. | | | 20,495 | | | | 7.35 | | | | 11,156 | | >4.0 | | | 13,945 | | >5.0 |

The declaration of cash dividends is dependent on a number of factors, including regulatory limitations, and the Company's operating results and financial condition. The stockholders of the Company will be entitled to dividends only when, and if, declared by the Company's Board of Directors out of funds legally available therefore. The declaration of future dividends will be subject to favorable operating results, financial conditions, tax considerations, and other factors.

Under Connecticut law, the Bank may pay dividends only out of net profits. The Connecticut Banking Commissioner’s approval is required for dividend payments which exceed the current year’s net profits and retained net profits from the preceding two years. As of December 31, 2010, the Bank is restricted from declaring dividends to the Company in an amount greater than $350,644.

NOTE 16 - EMPLOYEE BENEFITS

The Company sponsors a 401(k) savings and retirement plan. Employees who were 21 years of age and employed on the plan's effective date were immediately eligible to participate in the plan. Other employees who have attained age 21 are eligible for membership on the first day of the month following completion of 90 days of service.

The provisions of the 401(k) plan allow eligible employees to contribute subject to IRS limitations. The Company's matching contribution will be determined at the beginning of the plan year. The Company's expense under this plan was $87,089 in 2010 and $75,755 in 2009.

The Company entered into Supplemental Executive Retirement Agreements with current and former executive officers. The agreements require the payment of specified benefits upon retirement over specified periods as described in each agreement. The total liability for the agreements included in other liabilities was $226,305 at December 31, 2010 and $157,510 at December 31, 2009. Expenses under these agreements amounted to $73,796 and $13,939, respectively, for the years ended December 31, 2010 and 2009.

The Company entered into employment agreements (the “Agreements”) with the Executive Officers of the Company. The Agreements provide for severance benefits upon termination following a change in control as defined in the agreements in amounts equal to cash compensation as defined in the agreements, and fringe benefits that the Executive(s) would have received if the Executive(s) would have continued working for an additional two or five years.

NOTE 17 - STOCK OPTION PLAN

The Simsbury Bank & Trust Company, Inc. 1998 Stock Plan (“Plan”) provides for the granting of options to purchase shares of common stock or the granting of shares of restricted stock up to an aggregate amount of 142,000 shares of common stock of the Company. Options granted under the Plan may be either Incentive Stock Options (“ISOs”) within the meaning of Section 422 of the Internal Revenue Code or non-qualified options which do not qualify as ISOs (“NQOs”). Effective March 17, 2009, no additional restricted stock awards or stock options may be granted under the Plan.

The exercise price for shares covered by an ISO may not be less than 100% of the fair market value of common stock on the date of grant. The exercise price for shares covered by a NQO may not be less than 50% of the fair market value of common stock at the date of grant. All options must expire no later than ten years from the date of grant. The Plan also provides the Board with authority to make grants that will provide that options will become exercisable and restricted awards will become fully vested upon a change in control of the Company.

In accordance with the Plan each non-employee director is granted a NQO to purchase 1,000 shares of common stock at the fair market value of the common stock on the grant date. These options will become exercisable in two equal installments beginning on the first anniversary of the date of grant.