Filed Pursuant to Rule 424(b)(3)

Registration Nos. 333-192126

POWERSHARES DB G10 CURRENCY HARVEST FUND

SUPPLEMENT DATED NOVEMBER 28, 2014 TO

PROSPECTUS DATED DECEMBER 6, 2013

This Supplement dated November 28, 2014 updates certain information contained in the Prospectus dated December 6, 2013 (the “Prospectus”), as supplemented from time-to-time, of PowerShares DB G10 Currency Harvest Fund (the “Fund”). All capitalized terms used in this Supplement have the same meaning as in the Prospectus.

Prospective investors in the Fund should review carefully the contents of this Supplement and the Prospectus.

* * * * * * * * * * * * * * * * * * *

All information in the Prospectus is restated pursuant to this Supplement, except as updated hereby.

Neither the Securities and Exchange Commission nor any state or foreign securities commission has approved or disapproved of these securities or determined if this Supplement or the related Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED UPON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

DB COMMODITY SERVICES LLC

Managing Owner

| I. | Risk Factor (16) on page 22 of the Prospectus is hereby deleted and replaced, in its entirety, with the following: |

“(16) Price Volatility May Possibly Cause the Total Loss of Your Investment.

Futures contracts have a high degree of price variability and are subject to occasional rapid and substantial changes. Consequently, you could lose all or substantially all of your investment in the Fund.

The following table reflects various measures of volatility* of the Index as calculated on an excess return basis:

Volatility Type | Volatility | |||

Daily volatility over full history | 10.05 | % | ||

Average rolling 3-month daily volatility | 8.78 | % | ||

Monthly return volatility | 9.03 | % | ||

Average annual volatility | 9.08 | % | ||

The following table reflects the daily volatility on an annual basis of the Index:

| Year | Daily Volatility | |||||

| 1993** | 8.67 | % | ||||

| 1994 | 4.97 | % | ||||

| 1995 | 13.93 | % | ||||

| 1996 | 7.01 | % | ||||

| 1997 | 7.73 | % | ||||

| 1998 | 8.90 | % | ||||

| 1999 | 5.70 | % | ||||

| 2000 | 6.17 | % | ||||

| 2001 | 5.37 | % | ||||

| 2002 | 7.45 | % | ||||

| 2003 | 6.69 | % | ||||

| 2004 | 7.90 | % | ||||

| 2005 | 5.41 | % | ||||

| 2006 | 7.10 | % | ||||

| 2007 | 10.95 | % | ||||

| 2008 | 21.86 | % | ||||

| 2009 | 17.10 | % | ||||

| 2010 | 12.86 | % | ||||

| 2011 | 13.58 | % | ||||

| 2012 | 7.00 | % | ||||

| 2013 | 8.12 | % | ||||

| 2014*** | 5.32 | % | ||||

*Volatility, for these purposes, means the following:

Daily Volatility: The relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the daily change in price.

Monthly Return Volatility: The relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the monthly change in price.

2

Average Annual Volatility: The average of yearly volatilities for a given sample period. The yearly volatility is the relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the daily change in price for each business day in the given year.

**As of March 12, 1993.

***As of August 31, 2014.

Past Index results are not necessarily indicative of future changes, positive or negative, in the Index levels.”

| II. | Page 31 of the Prospectus is hereby deleted and replaced, in its entirety, with the following: |

“PERFORMANCE OF POWERSHARES DB G10 CURRENCY HARVEST FUND (TICKER: DBV)

Name of Pool:PowerShares DB G10 Currency Harvest Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:September 2006

Aggregate Gross Capital Subscriptions as of August 31, 20141: $1,358,540,794

Net Asset Value as of August 31, 20142: $94,175,937

Net Asset Value per Share as of August 31, 20143: $26.16

Worst Monthly Drawdown4: (6.72)% May 2010

Worst Peak-to-Valley Drawdown5: (36.85)% October 2007 – January 20096

Monthly Rate of Return | 2014(%) | 2013(%) | 2012(%) | 2011(%) | 2010(%) | 2009(%) | ||||||

January | (1.89) | 1.95 | 2.98 | 0.04 | (2.30) | (5.33) | ||||||

February | 1.60 | 0.08 | 4.24 | 0.55 | 0.35 | 3.09 | ||||||

March | 3.16 | 1.91 | (2.03) | 1.84 | 2.30 | 7.62 | ||||||

April | (0.23) | 0.85 | (0.92) | 3.21 | 2.47 | 0.39 | ||||||

May | (0.12) | (2.99) | (5.32) | (1.43) | (6.72) | 2.72 | ||||||

June | 0.27 | (4.40) | 4.85 | (0.28) | (2.71) | 1.66 | ||||||

July | (0.83) | (0.28) | 1.22 | (0.65) | 4.65 | 2.56 | ||||||

August | 0.99 | (2.01) | (0.04) | (1.06) | (5.04) | 1.36 | ||||||

September | 2.82 | 1.64 | (5.28) | 6.49 | 3.00 | |||||||

October | 0.82 | 0.28 | 6.36 | 0.82 | 0.61 | |||||||

November | (1.28) | 1.22 | (2.33) | (1.20) | (1.30) | |||||||

December | (0.04) | 1.63 | (0.13) | 2.64 | 3.02 | |||||||

Compound Rate of Return7 | 2.91% (8 months) | (2.79)% | 9.74% | 0.38% | 0.94% | 20.62% |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

Footnotes to Performance Information

1. “Aggregate Gross Capital Subscriptions” is the aggregate of all amounts ever contributed to the pool, including redeemed investments.

2. “Net Asset Value” is the net asset value of the pool as of August 31, 2014.

3. “Net Asset Value per Share” is the Net Asset Value of the pool divided by the total number of Shares outstanding as of August 31, 2014.

4. “Worst Monthly Drawdown” is the largest single month loss sustained since inception of trading. “Drawdown” as used in this section of the Prospectus means losses experienced by the relevant pool over the specified period and is calculated on a rate of return basis, i.e., dividing net performance by beginning equity. “Drawdown” is measured on the basis of monthly returns only, and does not reflect intra-month figures. “Month” is the month of the Worst Monthly Drawdown.

3

5. “Worst Peak-to-Valley Drawdown” is the largest percentage decline in the Net Asset Value per Share over the history of the pool. This need not be a continuous decline, but can be a series of positive and negative returns where the negative returns are larger than the positive returns. “Worst Peak-to-Valley Drawdown” represents the greatest percentage decline from any month-end Net Asset Value per Share that occurs without such month-end Net Asset Value per Share being equaled or exceeded as of a subsequent month-end. For example, if the Net Asset Value per Share of a particular pool declined by $1 in each of January and February, increased by $1 in March and declined again by $2 in April, a “peak-to-valley drawdown” analysis conducted as of the end of April would consider that “drawdown” to be still continuing and to be $3 in amount, whereas if the Net Asset Value per Share had increased by $2 in March, the January-February drawdown would have ended as of the end of February at the $2 level.

6. The Worst Peak-to-Valley Drawdown from October 2007 – January 2009 includes the effect of the $0.80 per Share distribution made to Shareholders of record as of December 19, 2007, and the effect of the $0.27 per Share distribution made to Shareholders of record as of December 17, 2008.

7. “Compound Rate of Return” is calculated by multiplying on a compound basis each of the monthly rates of return set forth in the chart above and not by adding or averaging such monthly rates of return. For periods of less than one year, the results are year-to-date.”

| III. | Pages 39-46 of the Prospectus are hereby deleted and replaced, in their entirety, with the following: |

“DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – EXCESS RETURN

CLOSING LEVELS TABLE

Closing Level | ||||||||

| High1 | Low2 | Annual Index Changes3 |

Index Changes | |||||

19934 | 105.60 | 94.03 | -0.19% | -0.19% | ||||

1994 | 108.79 | 99.81 | 7.42% | 7.22% | ||||

1995 | 110.52 | 94.16 | 2.66% | 10.07% | ||||

1996 | 140.05 | 110.42 | 27.23% | 40.05% | ||||

1997 | 146.72 | 137.83 | 2.58% | 43.67% | ||||

1998 | 151.79 | 132.52 | -6.35% | 34.55% | ||||

1999 | 151.12 | 134.71 | 9.81% | 47.76% | ||||

2000 | 158.57 | 146.79 | 4.73% | 54.74% | ||||

2001 | 171.15 | 154.68 | 10.61% | 71.15% | ||||

2002 | 199.51 | 172.25 | 15.76% | 98.13% | ||||

2003 | 234.45 | 199.00 | 18.33% | 134.45% | ||||

2004 | 252.36 | 230.02 | 6.69% | 150.14% | ||||

2005 | 286.06 | 248.34 | 10.66% | 176.81% | ||||

2006 | 280.48 | 254.18 | 1.00% | 179.58% | ||||

2007 | 315.27 | 276.77 | 5.15% | 193.98% | ||||

2008 | 295.87 | 200.14 | -28.80% | 109.32% | ||||

2009 | 260.64 | 196.13 | 21.91% | 155.18% | ||||

2010 | 264.24 | 236.66 | 1.67% | 159.45% | ||||

2011 | 274.83 | 241.88 | 1.18% | 162.52% | ||||

2012 | 290.15 | 258.40 | 10.39% | 189.79% | ||||

2013 | 310.79 | 276.57 | -1.98% | 184.05% | ||||

20145 | 295.63 | 276.74 | 3.38% | 193.64% | ||||

THE FUND WILL TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – EXCESS RETURN OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

4

DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – TOTAL RETURN

CLOSING LEVELS TABLE

Closing Level | ||||||||

| High1 | Low2 | Annual Index Changes3 |

Index Changes | |||||

19934 | 106.15 | 95.13 | 2.30% | 2.30% | ||||

1994 | 116.32 | 102.32 | 12.15% | 14.73% | ||||

1995 | 124.55 | 102.55 | 8.56% | 24.55% | ||||

1996 | 166.84 | 125.01 | 33.95% | 66.84% | ||||

1997 | 180.54 | 164.92 | 8.01% | 80.19% | ||||

1998 | 195.70 | 172.90 | -1.68% | 77.17% | ||||

1999 | 203.96 | 177.49 | 15.12% | 103.96% | ||||

2000 | 227.93 | 202.75 | 11.11% | 126.61% | ||||

2001 | 259.57 | 226.67 | 14.55% | 159.57% | ||||

2002 | 307.46 | 261.27 | 17.68% | 205.47% | ||||

2003 | 365.18 | 306.83 | 19.55% | 265.18% | ||||

2004 | 398.22 | 359.55 | 8.18% | 295.05% | ||||

2005 | 465.10 | 392.65 | 14.23% | 351.27% | ||||

2006 | 479.65 | 421.90 | 5.96% | 378.18% | ||||

2007 | 554.63 | 477.16 | 9.96% | 425.80% | ||||

2008 | 531.26 | 362.87 | -27.80% | 279.60% | ||||

2009 | 473.31 | 355.72 | 22.09% | 363.44% | ||||

2010 | 480.08 | 430.07 | 1.81% | 371.83% | ||||

2011 | 499.96 | 440.07 | 1.23% | 377.64% | ||||

2012 | 528.33 | 470.29 | 10.48% | 427.70% | ||||

2013 | 566.06 | 503.81 | -1.93% | 417.53% | ||||

20145 | 538.72 | 504.24 | 3.40% | 435.12% | ||||

THE FUND WILL NOT TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – TOTAL RETURN OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

5

INDEX CURRENCY WEIGHTS TABLE

DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – EXCESS RETURN

| USD | EUR | JPY | CAD | CHF | GBP | AUD | NZD | NOK | SEK | |||||||||||||||||||||||||||||||

| High1 | Low2 | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | |||||||||||||||||||||

19934 | -31.6% | -36.8% | 33.8% | 34.0% | -33.7% | -37.2% | 0.0% | -36.8% | 0.0% | 0.0% | 0.0% | 0.0% | -31.1% | 0.0% | 0.0% | 0.0% | 33.9% | 34.1% | 33.9% | 32.3% | ||||||||||||||||||||

1994 | 0.0% | -33.3% | -33.0% | 32.5% | -33.1% | -32.5% | 0.0% | -33.4% | -33.1% | 0.0% | 0.0% | 0.0% | 33.2% | 0.0% | 33.3% | 33.6% | 0.0% | 0.0% | 33.4% | 33.2% | ||||||||||||||||||||

1995 | 0.0% | 0.0% | -33.7% | -35.7% | -33.1% | -39.1% | 0.0% | 35.9% | -33.7% | -36.8% | 0.0% | 0.0% | 32.4% | 0.0% | 33.0% | 36.3% | 0.0% | 0.0% | 36.2% | 34.6% | ||||||||||||||||||||

1996 | 0.0% | 0.0% | 0.0% | -33.5% | -31.7% | -32.5% | -32.1% | 0.0% | -31.5% | -33.3% | 33.3% | 0.0% | 32.4% | 33.3% | 32.6% | 33.3% | 0.0% | 0.0% | 0.0% | 33.2% | ||||||||||||||||||||

1997 | 0.0% | 0.0% | 0.0% | 0.0% | -31.5% | -30.6% | -31.7% | -33.1% | -32.2% | -30.4% | 33.2% | 31.7% | 31.9% | 31.5% | 32.6% | 32.3% | 0.0% | 0.0% | 0.0% | 0.0% | ||||||||||||||||||||

1998 | 0.0% | 0.0% | -32.3% | -36.7% | -32.9% | -40.1% | 0.0% | 0.0% | -31.8% | -37.5% | 32.3% | 36.0% | 34.2% | 0.0% | 34.2% | 36.5% | 0.0% | 35.7% | 0.0% | 0.0% | ||||||||||||||||||||

1999 | 32.6% | 33.0% | -31.6% | -32.2% | -31.3% | -34.4% | 0.0% | 0.0% | -31.4% | -32.0% | 31.6% | 32.5% | 0.0% | 0.0% | 0.0% | 0.0% | 32.1% | 34.1% | 0.0% | 0.0% | ||||||||||||||||||||

2000 | 31.9% | 33.3% | -29.4% | -33.7% | -30.8% | -32.9% | 0.0% | 0.0% | -30.5% | -33.5% | 31.6% | 33.5% | 0.0% | 0.0% | 31.6% | 0.0% | 0.0% | 33.5% | 0.0% | 0.0% | ||||||||||||||||||||

2001 | -33.1% | 33.1% | 0.0% | 0.0% | -32.1% | -32.4% | 0.0% | 0.0% | -32.5% | -34.5% | 0.0% | 0.0% | 32.7% | 0.0% | 33.0% | 34.1% | 32.8% | 34.1% | 0.0% | -33.7% | ||||||||||||||||||||

2002 | -33.2% | -32.9% | 0.0% | 0.0% | -33.1% | -31.6% | 0.0% | 0.0% | -33.5% | -32.7% | 0.0% | 0.0% | 33.3% | 32.6% | 33.5% | 33.1% | 33.5% | 33.0% | 0.0% | 0.0% | ||||||||||||||||||||

2003 | -33.0% | -33.2% | 0.0% | 0.0% | -33.0% | -33.4% | 0.0% | 0.0% | -33.5% | -34.2% | 33.7% | 0.0% | 33.4% | 33.2% | 33.4% | 33.9% | 0.0% | 34.1% | 0.0% | 0.0% | ||||||||||||||||||||

2004 | 0.0% | -34.6% | 0.0% | 0.0% | -33.2% | -33.5% | 0.0% | 0.0% | -33.0% | -34.7% | 33.4% | 34.1% | 33.6% | 32.6% | 33.4% | 32.3% | -33.1% | 0.0% | 0.0% | 0.0% | ||||||||||||||||||||

2005 | 0.0% | 0.0% | 0.0% | 0.0% | -29.1% | -34.4% | 0.0% | 0.0% | -30.7% | -32.8% | 30.7% | 32.7% | 31.2% | 33.9% | 32.7% | 33.2% | 0.0% | -33.2% | -30.2% | 0.0% | ||||||||||||||||||||

2006 | 32.9% | 36.0% | 0.0% | 0.0% | -32.6% | -38.1% | 0.0% | 0.0% | -32.9% | -39.1% | 0.0% | 0.0% | 33.2% | 37.1% | 33.7% | 35.1% | 0.0% | 0.0% | -33.1% | -38.8% | ||||||||||||||||||||

2007 | 0.0% | 33.3% | 0.0% | 0.0% | -33.2% | -33.7% | 0.0% | 0.0% | -33.2% | -33.1% | 33.8% | 0.0% | 34.2% | 32.9% | 34.8% | 32.8% | 0.0% | 0.0% | -34.1% | -32.3% | ||||||||||||||||||||

2008 | 0.0% | -44.2% | 0.0% | 0.0% | -34.8% | -50.7% | 0.0% | 0.0% | -35.2% | -43.3% | 32.7% | 0.0% | 36.1% | 32.9% | 35.6% | 36.1% | 0.0% | 36.6% | -34.6% | 0.0% | ||||||||||||||||||||

2009 | -31.2% | -35.2% | 0.0% | 0.0% | -31.0% | -35.8% | 0.0% | 0.0% | -32.2% | -35.6% | 0.0% | 0.0% | 33.7% | 33.7% | 33.7% | 32.7% | 33.4% | 34.5% | 0.0% | 0.0% | ||||||||||||||||||||

2010 | -32.1% | -34.8% | 0.0% | 0.0% | -30.7% | -36.5% | 0.0% | 0.0% | -31.4% | 37.7% | 0.0% | 0.0% | 32.7% | 34.6% | 33.6% | 34.9% | 31.6% | 35.0% | 0.0% | 0.0% | ||||||||||||||||||||

2011 | -31.5% | -36.7% | 0.0% | 0.0% | -31.8% | -38.3% | 0.0% | 0.0% | -33.9% | -43.2% | 0.0% | 0.0% | 34.3% | 35.3% | 34.5% | 36.3% | 33.9% | 36.5% | 0.0% | 0.0% | ||||||||||||||||||||

2012 | 0.0% | -36.2% | -32.1% | 0.0% | -30.2% | -38.6% | 0.0% | 0.0% | -32.2% | -34.2% | 0.0% | 0.0% | 32.4% | 33.4% | 32.9% | 33.2% | 32.7% | 33.8% | 0.0% | 0.0% | ||||||||||||||||||||

2013 | 0.0% | 0.0% | -32.3% | -34.7% | -30.8% | -33.6% | 0.0% | 0.0% | -32.5% | -34.8% | 0.0% | 0.0% | 32.7% | 32.6% | 33.7% | 33.7% | 32.6% | 33.0% | 0.0% | 0.0% | ||||||||||||||||||||

20145 | 0.0% | 0.0% | 0.0% | -33.4% | -33.3% | -34.6% | 0.0% | 0.0% | -33.3% | -33.4% | 0.0% | 0.0% | 33.3% | 33.2% | 33.3% | 33.3% | 33.3% | 33.4% | 0.0% | 0.0% | ||||||||||||||||||||

THE FUND WILL TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – EXCESS RETURN OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

6

DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – TOTAL RETURN

| USD | EUR | JPY | CAD | CHF | GBP | AUD | NZD | NOK | SEK | |||||||||||||||||||||||||||||||

| High1 | Low2 | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | High | Low | |||||||||||||||||||||

19934 | -31.6% | -36.8% | 33.6% | 34.0% | -34.8% | -37.2% | 0.0% | -36.8% | 0.0% | 0.0% | 0.0% | 0.0% | -30.3% | 0.0% | 0.0% | 0.0% | 33.6% | 34.1% | 34.7% | 32.3% | ||||||||||||||||||||

1994 | 0.0% | -33.3% | -33.1% | 32.5% | -33.1% | -32.5% | 0.0% | -33.4% | -33.1% | 0.0% | 0.0% | 0.0% | 33.2% | 0.0% | 33.3% | 33.6% | 0.0% | 0.0% | 33.4% | 33.2% | ||||||||||||||||||||

1995 | 0.0% | 0.0% | -33.5% | -35.7% | -32.9% | -39.1% | 0.0% | 35.9% | -33.6% | -36.8% | 0.0% | 0.0% | 33.4% | 0.0% | 33.4% | 36.3% | 0.0% | 0.0% | 33.2% | 34.6% | ||||||||||||||||||||

1996 | 0.0% | 0.0% | 0.0% | -33.5% | -31.7% | -32.5% | -32.1% | 0.0% | -31.5% | -33.3% | 33.3% | 0.0% | 32.4% | 33.3% | 32.6% | 33.3% | 0.0% | 0.0% | 0.0% | 33.2% | ||||||||||||||||||||

1997 | 32.4% | 0.0% | -32.1% | 0.0% | -30.0% | -30.6% | 0.0% | -33.1% | -32.8% | -30.4% | 34.0% | 31.7% | 0.0% | 31.5% | 31.3% | 32.3% | 0.0% | 0.0% | 0.0% | 0.0% | ||||||||||||||||||||

1998 | 0.0% | 0.0% | -32.3% | -36.7% | -32.9% | -40.1% | 0.0% | 0.0% | -31.8% | -37.5% | 32.3% | 36.0% | 34.2% | 0.0% | 34.2% | 36.5% | 0.0% | 35.7% | 0.0% | 0.0% | ||||||||||||||||||||

1999 | 33.1% | 33.0% | -32.5% | -32.2% | -32.9% | -34.4% | 0.0% | 0.0% | -32.4% | -32.0% | 32.8% | 32.5% | 0.0% | 0.0% | 0.0% | 0.0% | 32.8% | 34.1% | 0.0% | 0.0% | ||||||||||||||||||||

2000 | 32.9% | 33.3% | 0.0% | -33.7% | -32.3% | -32.9% | 0.0% | 0.0% | -33.7% | -33.5% | 0.0% | 33.5% | 0.0% | 0.0% | 34.0% | 0.0% | 33.4% | 33.5% | -33.0% | 0.0% | ||||||||||||||||||||

2001 | -33.1% | 33.1% | 0.0% | 0.0% | -32.1% | -32.4% | 0.0% | 0.0% | -32.5% | -34.5% | 0.0% | 0.0% | 32.7% | 0.0% | 33.0% | 34.1% | 32.8% | 34.1% | 0.0% | -33.7% | ||||||||||||||||||||

2002 | -33.2% | -32.9% | 0.0% | 0.0% | -33.1% | -31.6% | 0.0% | 0.0% | -33.5% | -32.7% | 0.0% | 0.0% | 33.3% | 32.6% | 33.5% | 33.1% | 33.5% | 33.0% | 0.0% | 0.0% | ||||||||||||||||||||

2003 | -33.0% | -33.2% | 0.0% | 0.0% | -33.0% | -33.4% | 0.0% | 0.0% | -33.5% | -34.2% | 33.7% | 0.0% | 33.4% | 33.2% | 33.4% | 33.9% | 0.0% | 34.1% | 0.0% | 0.0% | ||||||||||||||||||||

2004 | 0.0% | -34.2% | 0.0% | 0.0% | -33.5% | -33.2% | 0.0% | 0.0% | -33.8% | -33.8% | 33.7% | 33.6% | 33.8% | 32.6% | 33.8% | 32.4% | -33.7% | 0.0% | 0.0% | 0.0% | ||||||||||||||||||||

2005 | 0.0% | 0.0% | 0.0% | 0.0% | -29.7% | -33.8% | 0.0% | 0.0% | -30.9% | -32.7% | 30.8% | 32.7% | 31.1% | 33.8% | 32.4% | 33.1% | 0.0% | -33.0% | -30.4% | 0.0% | ||||||||||||||||||||

2006 | 33.1% | 35.7% | 0.0% | 0.0% | -32.9% | -38.0% | 0.0% | 0.0% | -33.1% | -38.6% | 0.0% | 0.0% | 33.2% | 37.3% | 33.7% | 34.9% | 0.0% | 0.0% | -33.4% | -38.4% | ||||||||||||||||||||

2007 | 0.0% | 33.0% | 0.0% | 0.0% | -33.4% | -32.7% | 0.0% | 0.0% | -33.9% | -33.0% | 34.2% | 0.0% | 34.4% | 33.3% | 34.9% | 33.7% | 0.0% | 0.0% | -34.9% | -33.3% | ||||||||||||||||||||

2008 | 0.0% | -24.4% | 0.0% | 0.0% | -19.4% | -28.0% | 0.0% | 0.0% | -19.6% | -23.9% | 18.2% | 0.0% | 20.1% | 18.1% | 19.8% | 19.9% | 0.0% | 20.2% | -19.3% | 0.0% | ||||||||||||||||||||

2009 | -17.2% | -19.4% | 0.0% | 0.0% | -17.1% | -19.7% | 0.0% | 0.0% | -17.7% | -19.6% | 0.0% | 0.0% | 18.6% | 18.6% | 18.6% | 18.0% | 18.4% | 19.0% | 0.0% | 0.0% | ||||||||||||||||||||

2010 | -17.7% | -19.2% | 0.0% | 0.0% | -16.9% | -20.1% | 0.0% | 0.0% | -17.3% | -20.7% | 0.0% | 0.0% | 18.0% | 19.0% | 18.5% | 19.2% | 17.4% | 19.3% | 0.0% | 0.0% | ||||||||||||||||||||

2011 | -17.3% | -20.2% | 0.0% | 0.0% | -17.5% | -21.0% | 0.0% | 0.0% | -18.7% | -23.8% | 0.0% | 0.0% | 18.9% | 19.4% | 18.9% | 19.9% | 18.6% | 20.1% | 0.0% | 0.0% | ||||||||||||||||||||

2012 | 0.0% | -19.9% | -17.6% | 0.0% | -16.6% | -21.2% | 0.0% | 0.0% | -17.7% | -18.8% | 0.0% | 0.0% | 17.8% | 18.3% | 18.1% | 18.3% | 17.9% | 18.6% | 0.0% | 0.0% | ||||||||||||||||||||

2013 | 0.0% | 0.0% | -17.8% | -19.1% | -16.9% | -18.5% | 0.0% | 0.0% | -17.9% | -19.1% | 0.0% | 0.0% | 18.0% | 17.9% | 18.5% | 18.5% | 17.9% | 18.1% | 0.0% | 0.0% | ||||||||||||||||||||

20145 | 0.0% | 0.0% | 0.0% | -18.3% | -18.3% | -19.0% | 0.0% | 0.0% | -18.3% | -18.4% | 0.0% | 0.0% | 18.3% | 18.2% | 18.3% | 18.3% | 18.3% | 18.3% | 0.0% | 0.0% | ||||||||||||||||||||

THE FUND WILL NOT TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK G10 CURRENCY FUTURE HARVEST INDEX® – TOTAL RETURN OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

7

All Statistics based on data from March 12, 1993 to August 31, 2014.

| VARIOUS STATISTICAL MEASURES* | INDEX-TR6,7 | INDEX-ER7,8 | DXY9 | EFFAS US Treasuries10 | S&P 500 TR11 | DBLCI12 | ||||||

Annualized Changes to Index Level13 | 8.9% | 4.9% | -0.5% | 6.6% | 5.6% | 9.5% | ||||||

Average rolling 3-month daily volatility14 | 8.8% | 8.8% | 7.8% | 4.6% | 16.8% | 19.7% | ||||||

Sharpe Ratio15 | 0.60 | 0.56 | -0.52 | 0.64 | 0.12 | 0.30 | ||||||

% of months with positive change | 67% | 64% | 47% | 63% | 65% | 56% | ||||||

Average monthly positive return change | 2.1% | 1.9% | 1.9% | 1.2% | 3.3% | 4.8% | ||||||

Average monthly negative return change | -2.1% | -2.2% | -1.7% | -0.8% | -3.7% | -4.2% | ||||||

| CORRELATION OF MONTHLY INDEX LEVELS*,16 | INDEX-TR | INDEX-ER | DXY | EFFAS US Treasuries | S&P 500 TR | DBLCI | ||||||

Index TR | 100% | 100% | -20% | -10% | 45% | 37% | ||||||

Index-ER | 100% | -20% | -11% | 45% | 37% | |||||||

DXY | 100% | -11% | -23% | -38% | ||||||||

EFFAS US Treasuries | 100% | -17% | -7% | |||||||||

S&P 500 TR | 100% | 26% | ||||||||||

DBLCI | 100% |

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN DECEMBER 2005, CERTAIN INFORMATION RELATING TO THE INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD MARCH 1993 THROUGH NOVEMBER 2005, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX METHODOLOGY, AND SELECTION OF INDEX CURRENCIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE CURRENCIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK THE INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF THE INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUND AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

8

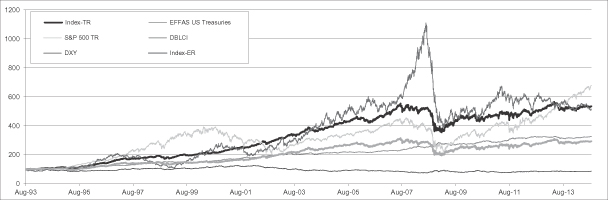

COMPARISON OF THE INDICES WITH CERTAIN GENERAL MARKET INDICES REPRESENTING CURRENCIES, BONDS, STOCKS AND COMMODITIES

(MARCH 12, 1993 – AUGUST 31, 2014)*

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

Each of the Index-TR, EFFAS US Treasuries, S&P 500 TR, DBLCI and DXY are indices and do not reflect actual trading.

Each of the indices, except DXY, are calculated on a total return basis and does not reflect any fees or expenses.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN DECEMBER 2005, CERTAIN INFORMATION RELATING TO THE INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD MARCH 1993 THROUGH NOVEMBER 2005, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX METHODOLOGY, AND SELECTION OF INDEX CURRENCIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE CURRENCIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK THE INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF THE INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUND AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

| 9 |

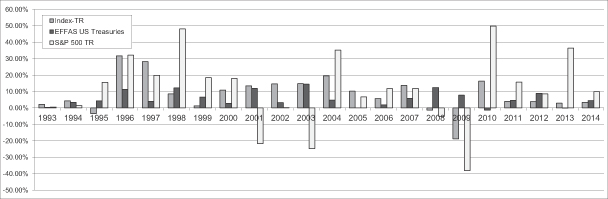

COMPARISON OF ANNUAL PERCENTAGE CHANGE IN THE INDICES WITH CERTAIN GENERAL MARKET INDICES REPRESENTING BONDS AND STOCKS

(MARCH 12, 1993 – AUGUST 31, 2014)*

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

Each of the Index-TR, EFFAS US Treasuries, S&P 500 TR, DBLCI and DXY are indices and do not reflect actual trading.

Each of the indices, except DXY, are calculated on a total return basis and does not reflect any fees or expenses.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN DECEMBER 2005, CERTAIN INFORMATION RELATING TO THE INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD MARCH 1993 THROUGH NOVEMBER 2005, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX METHODOLOGY, AND SELECTION OF INDEX CURRENCIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE CURRENCIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK THE INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF THE INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUND AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

| 10 |

NOTES AND LEGENDS:

1. “High” reflects the highest closing level of the Index during the applicable year.

2. “Low” reflects the lowest closing level of the Index during the applicable year.

3. “Annual Index Changes” reflect the change to the Index level on an annual basis as of December 31 of each applicable year.

4. Closing levels as of inception on March 12, 1993.

5. Closing levels as of August 31, 2014.

6. “INDEX-TR” is Deutsche Bank G10 Currency Future Harvest Index® — Total Return. The Deutsche Bank G10 Currency Future Harvest Index® is calculated on both an excess return basis and total return. The Index-TR calculation is funded and reflects the change in market value of both the underlying index currencies and the interest income from a hypothetical basket of fixed income securities. The sponsor of the Index, or the Index Sponsor, is Deutsche Bank AG London. Deutsche Bank G10 Currency Future Harvest Index® is a registered trademark of Deutsche Bank AG. All rights reserved.

7. If the Fund’s interest income from its holdings of fixed income securities were to exceed the Fund’s fees and expenses, the total return on an investment in the Fund is expected to outperform the INDEX-ER (as such term is defined in the following footnote) and underperform the INDEX-TR. The only difference between the INDEX-ER and the INDEX-TR is that the INDEX-ER does not include interest income from a hypothetical basket of fixed income securities while the INDEX-TR does include such a component. The difference between the INDEX-ER and the INDEX-TR is attributable entirely to the hypothetical interest income from this hypothetical basket of fixed income securities. If the Fund’s interest income from its holdings of fixed-income securities exceeds the Fund’s fees and expenses, the amount of such excess is expected to be distributed periodically. The market price of the Shares is expected closely to track the INDEX-ER. The total return on an investment in the Fund over any period is the sum of the capital appreciation or depreciation of the Shares over the period, plus the amount of any distributions during the period. Consequently, the Fund’s total return is expected to outperform the INDEX-ER by the amount of the excess, if any, of its interest income over its fees and expenses but, as a result of the Fund’s fees and expenses, the total return on the Fund is expected to underperform the INDEX-TR. If the Fund’s fees and expenses were to exceed the Fund’s interest income from its holdings of fixed income securities, the total return on an investment in the Fund is expected to underperform the INDEX-ER.

8. “INDEX-ER” is the Deutsche Bank G10 Currency Future Harvest Index® — Excess Return. The excess return calculation is unfunded and reflects the change in market value of the underlying index currencies.

9. “DXY” is U.S. Dollar Index®. The U.S. Dollar Index® provides a general indication of the international value of the USD by averaging the exchange rates between the USD and the following six major world currencies: Euro, Japanese Yen, British Pound, Canadian Dollar, Swedish Krona and Swiss Franc. U.S. Dollar Index® is a registered service mark of ICE Futures U.S.

10. “EFFAS US Treasuries” is Bloomberg/EFFAS Index of U.S. Treasuries. The Bloomberg/EFFAS indices are designed as transparent benchmarks for government bond markets. Indices are grouped by country and maturity sectors. Bloomberg computes daily values and index characteristics for each sector. The Bloomberg/EFFAS Index of U.S. Treasuries includes treasuries with more than one year prior to maturity and is representative of the bond market.

11. “S&P 500 TR” is the Standard & Poor’s index calculated on a total return basis. Widely regarded as the benchmark gauge of the U.S. equities market, this index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 focuses on the large cap segment of the market, with over 80% coverage of U.S. equities, it also serves as a proxy for the total market. The total return calculation provides investors with a price plus gross cash dividend return. Gross cash dividends are applied on the ex date of the dividend.

12. “DBLCI” is the Deutsche Bank Liquid Commodity Index — Total Return™. This Index is intended to reflect the change in market value of the following commodities: Light, Sweet Crude Oil, Heating Oil, Aluminum, Gold, Corn and Wheat. The notional amounts of each index commodity included in this index are broadly in proportion to historical levels of the world’s

11

production and stocks of the index commodities. The sponsor of the Index, or the Index Sponsor, is Deutsche Bank AG London. Deutsche Bank Liquid Commodity Index® – Total Return is a registered trade mark of Deutsche Bank AG and is the subject of Community Trade Mark Number 3054996.

13. “Annualized Changes to Index Level” reflects the change to the level of the applicable index on an annual basis as of December 31 of each applicable year.

14. “Average rolling 3-month daily volatility.” The daily volatility reflects the relative rate at which the price of the applicable index moves up and down, which is found by calculating the annualized standard deviation of the daily change in price. In turn, an average of this value is calculated on a 3-month rolling basis.

15. “Sharpe Ratio” compares the annualized rate of return minus the annualized risk-free rate of return to the annualized variability — often referred to as the “standard deviation” — of the monthly rates of return. A Sharpe Ratio of 1:1 or higher indicates that, according to the measures used in calculating the ratio, the rate of return achieved by a particular strategy has equaled or exceeded the risks assumed by such strategy. The risk-free rate of return that was used in these calculations was assumed to be 3.64%.

16. “Correlation of Monthly Index Levels.” Every investment asset, by definition, has a correlation coefficient of 1.0 with itself; 1.0 indicates 100% positive correlation. Two investments that always move in the opposite direction from each other have a correlation coefficient of -1.0; -1.0 indicates 100% negative correlation. Two investments that perform entirely independently of each other have a correlation coefficient of 0; 0 indicates 100% non-correlation.

* For the period from March 12, 1993 to August 31, 2014.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN DECEMBER 2005, CERTAIN INFORMATION RELATING TO THE INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD MARCH 1993 THROUGH NOVEMBER 2005, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX METHODOLOGY, AND SELECTION OF INDEX CURRENCIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE CURRENCIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK THE INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF THE INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUND AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

ALTHOUGH THE INDEX SPONSOR WILL OBTAIN INFORMATION FOR INCLUSION IN OR FOR USE IN THE CALCULATION OF THE INDEX FROM SOURCE(S) WHICH THE INDEX SPONSOR CONSIDERS RELIABLE, THE INDEX SPONSOR WILL NOT INDEPENDENTLY VERIFY SUCH INFORMATION AND DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE INDEX OR ANY DATA INCLUDED THEREIN. THE INDEX SPONSOR WILL NOT BE LIABLE (WHETHER IN NEGLIGENCE OR OTHERWISE) TO ANY PERSON FOR ANY ERROR IN THE INDEX AND THE INDEX SPONSOR IS UNDER NO OBLIGATION TO ADVISE ANY PERSON OF ANY ERROR THEREIN.

12

UNLESS OTHERWISE SPECIFIED, NO TRANSACTION RELATING TO THE INDEX IS SPONSORED, ENDORSED, SOLD OR PROMOTED BY THE INDEX SPONSOR AND THE INDEX SPONSOR MAKES NO EXPRESS OR IMPLIED REPRESENTATIONS OR WARRANTIES AS TO (A) THE ADVISABILITY OF PURCHASING OR ASSUMING ANY RISK IN CONNECTION WITH ANY SUCH TRANSACTION, (B) THE LEVELS AT WHICH THE INDEX STANDS AT ANY PARTICULAR TIME ON ANY PARTICULAR DATE, (C) THE RESULTS TO BE OBTAINED BY THE ISSUER OF ANY SECURITY OR ANY COUNTERPARTY OR ANY SUCH ISSUER’S SECURITY HOLDERS OR CUSTOMERS OR ANY SUCH COUNTERPARTY’S CUSTOMERS OR COUNTERPARTIES OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE INDEX OR ANY DATA INCLUDED THEREIN IN CONNECTION WITH ANY LICENSED RIGHTS OR FOR ANY OTHER USE, OR (D) ANY OTHER MATTER. THE INDEX SPONSOR MAKES NO EXPRESS OR IMPLIED REPRESENTATIONS OR WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE INDEX OR ANY DATA INCLUDED THEREIN.

WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL THE INDEX SPONSOR HAVE ANY LIABILITY (WHETHER IN NEGLIGENCE OR OTHERWISE) TO ANY PERSON FOR ANY DIRECT, INDIRECT, SPECIAL, PUNITIVE, CONSEQUENTIAL OR ANY OTHER DAMAGES (INCLUDING LOST PROFITS) EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.”

13