Credit Suisse 2008 Global

Leveraged Finance Conference

March 25, 2008

Forward looking statements

Certain information in this presentation may be considered forward-looking information within the definition of the Private Securities Litigation Reform Act of 1995. This information is based on the Company's current expectations and actual results could vary materially depending on risks and uncertainties that may affect the Company's operations, markets, services, prices and other factors as discussed in filings with the Securities and Exchange Commission. These risks and uncertainties include, but are not limited to, general and economic conditions, failure to complete, integrate and/or realize the cost savings from our acquisition of Harland, and declines in the market in which we participate. There is no assurance that the Company's expectations will be realized. All forward looking statements speak only as of the date of this presentation. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are qualified by the cautionary statements in this section. The Company assumes no obligation to update any forward-looking information contained in this presentation.

2

Introductions

Over 32 years of experience in the financial services and security printing industry

Over 15 years with Clarke American / Harland Clarke

Former Chief Executive Officer of Rocky Mountain Bank Note

Spent 16 years at Harland

Marketing representative for IBM out of graduate school

Chuck Dawson

President & CEO,

Harland Clarke Holdings

15 years of experience with Harland Clarke, Honeywell, and GE in various financial and operations leadership roles

Former Chief Financial Officer of Honeywell’s Aircraft Landing Systems business

Peter Fera

EVP & CFO,

Harland Clarke Holdings

3

World class

operations

Leading market

presence

Diversified,

blue-chip

client portfolio

A leading provider of checks & office products and marketing & contact center services

A leading provider of software and services to financial institutions

A leading provider of testing and survey technologies

$1.7 billion in combined revenues in 2007

Over 14,000 financial institutions clients such as:

Harland Clarke: 5 contact centers and 15 plants, supported by a national sales organization

Harland Financial Solutions: 17 fully networked facilities focused on customer support and enhancement of software solutions

Scantron: 6 facilities, 4 related to our recent acquisition, which are in the process of being fully networked to connect a breadth of businesses which include manufacturing, technology and services

2001 Malcolm Baldrige National Quality Award winner

Strong, long-

term client

relationships

Trusted, integrated relationships with clients

Provider of mission-critical software products

Strong partnerships with long-term contracts – 80% of revenue under long-term contract

Harland Clarke Holdings

4

Harland Clarke

Checks and office

products and marketing

and contact center

services for financial and

commercial institutions

Scantron

Testing, data collection

and surveys for

schools, healthcare and

other commercial

businesses

Harland Financial

Solutions

Software and services

for banks, credit unions

and thrifts

What we do

5

Harland & Clarke: A compelling strategic combination

Diversified business and product lines

Diversified and expanded client relationships with long-term contracts

Significant cost savings

Strong management team

Strong free cash flow generation

6

Diversified business and product lines

Combined business has four major product lines

Checks and office products

Marketing and contact center services

Software and related services

Testing and survey solutions

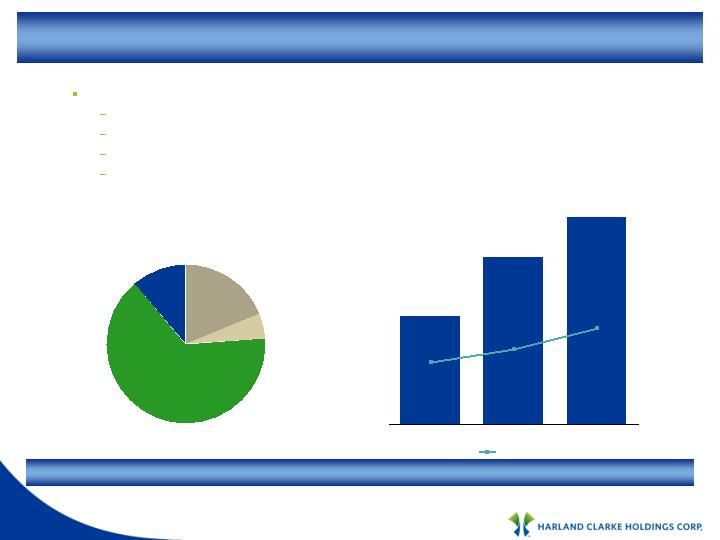

$1.7 billion

Checks

and Office

Products

64%

Testing and

Survey

5%

Software

19%

Cash Management, Forms &

Marketing

Services

12%

2007 Revenue

$623M

$378M

45%

36%

29%

2002

2007

5 Year Target

% of Total Sales

Revenue for Non-Check Products

Value proposition is more than a “check provider” for financial institutions

7

Diversified and expanded client relationships

Approximately 80% of revenue is under long-term contracts

8

Cost savings originally planned

Facilities $15.5 million

Procurement $9.8 million

Shared services $22.7 million

Other SG&A $64.6 million

Total savings $112.6 million

$59.7 million in actions taken in first eight months since acquisition

$30.0 million in EBITDA impact realized in 2007

Facilities

14%

Procurement

9%

Shared Services

20%

Other SG&A

57%

On target to achieve $112.6 million in synergies

Cost savings

9

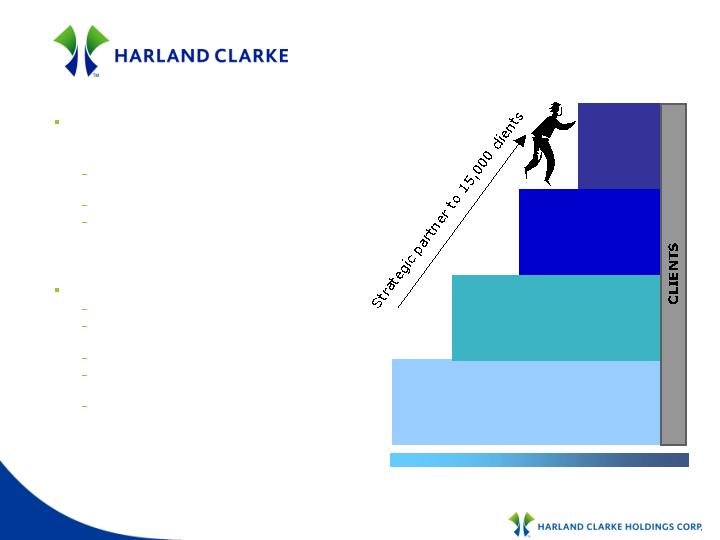

A leading provider of checks and office

products and marketing and contact

center services

15,000 financial and commercial institution

clients

85% of revenues under long-term contract

More than 20 million annual direct customer

contacts through contact centers and

websites

Diverse product and service offerings

Personal and business checks

Address labels, self-inking stamps,

checkbook covers, registers

Financial and business forms

Deposit products including deposit tickets,

security bags, cash straps, coin wraps

Marketing services including onboarding,

direct mail, contact center and agency

solutions

Strategic

partner

Partner

Supplier

Vendor

10

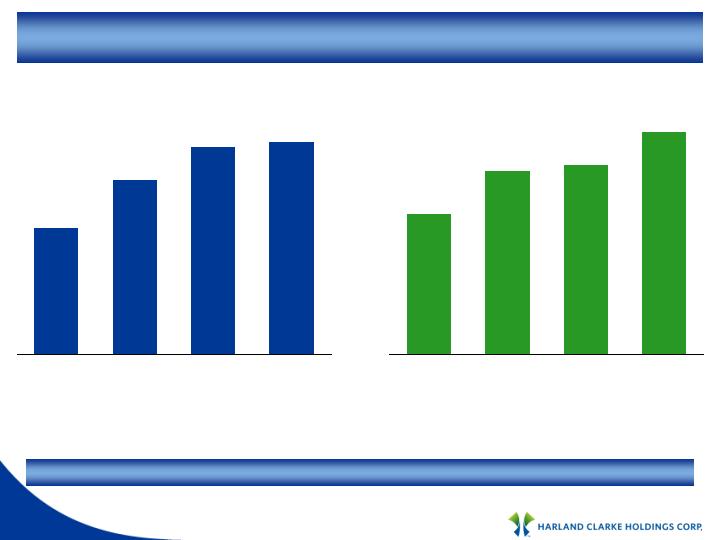

$1,088

$1,234

$1,274

$1,319

2004

2005

2006

2007

$229

$271

$293

$340

2004

2005

2006

2007

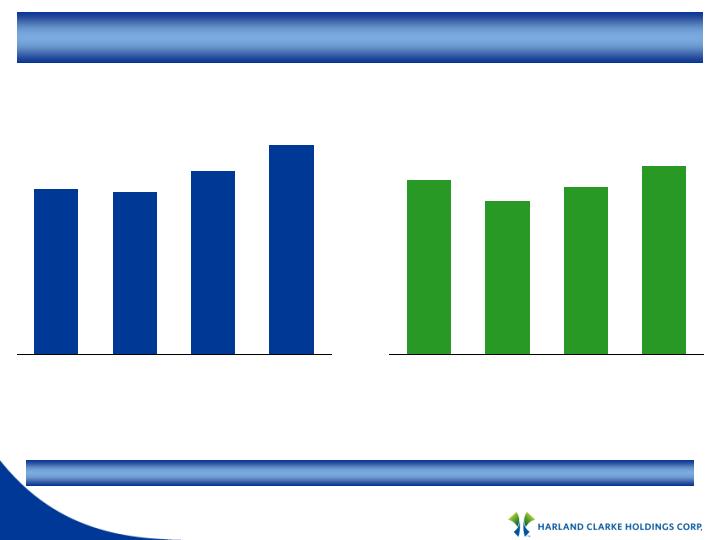

Harland Clarke financial performance

(1) Combined revenue is the sum of the revenues of the Harland Clarke segment (which consists of only Clarke American revenues prior to May 1, 2007), plus revenues of Harland’s Printed Products

segment for periods prior to the completion of the Harland Acquisition on May 1, 2007, plus an adjustment to add back $0.6 million of purchase accounting fair value adjustments of deferred revenue for

2007, minus revenue from inter-segment transactions.

(2) Combined Adjusted EBITDA is the sum of the operating income of the Harland Clarke segment (which consists of only Clarke American operating income prior to May 1, 2007), plus the operating

income of Harland’s Printed Products segment for periods prior to the completion of the Harland Acquisition on May 1, 2007, plus combined depreciation and amortization (other than amortization of

upfront contract payments), plus adjustments to add back (i) purchase accounting fair value adjustments of inventory and deferred revenue, (ii) Harland Acquisition-related expenses, (iii) intangible

asset impairment, (iv) a contingent earn-out payment and (v) restructuring expenses.

2007 revenue and adjusted EBITDA up 3.5% and 16.0%, respectively

$ in millions

Combined Revenue(1)

$ in millions

Margin 21.0% 22.0% 23.0% 25.8%

Combined Adjusted EBITDA(2)

11

Harland Clarke

The table below presents a reconciliation of (x) the combined operating income of the Harland Clarke segment and John H. Harland Company's printed products segment to (y) combined adjusted EBITDA for 2004, 2005, 2006 and 2007.

(1) For periods prior to May 1, 2007, consists of only the operating income of Clarke American Corp.

(2) Consists of the operating income of the printed products segment of John H. Harland Company for periods prior to May 1, 2007

($ in millions)

Harland Clarke

2004

2005

2006

2007

Harland Clarke operating income (1)

$ 107.0

$ 78.3

$ 87.0

$ 181.1

Harland Printed Products segment operating income (2)

63.6

98.4

111.7

24.4

Combined operating income

170.6

176.7

198.7

205.5

D&A (other than upfront contract payments amort)

52.0

85.2

89.0

108.4

Purchase accounting related fair value adjustments

-

4.9

1.3

2.0

Harland Acquisition expenses

-

-

-

15.4

Intangible asset impairment costs

-

-

-

3.1

Contingent earnout payment

-

1.9

1.1

-

Restructuring expenses

6.5

2.4

3.3

5.6

Combined adjusted EBITDA

$ 229.1

$ 271.0

$ 293.4

$ 340.0

12

7%

4%

11%

30%

48%

A leading supplier of software and services

to financial institutions

Core processing

Retail solutions (branch, teller, call center)

Lending compliance

Mortgage origination

High switching costs associated with

switching integrated software providers

Contracts: license (33%); subscriptions

(37%); service (30%)

Sell to 40% of all financial institutions in the

U.S.

Top 20 customers < 6% of revenue

Recurring revenue for 75% of sales

Customer Mix

Banks

4,011

Credit Unions

2,490

Thrifts

579

Mortgage Co.

339

Total 8,327

Revenue growth is primarily driven by the growth of financial institutions’ assets

Other

908

13

$235

$287

$322

$327

2004

2005

2006

2007

$45

$59

$61

$71

2004

2005

2006

2007

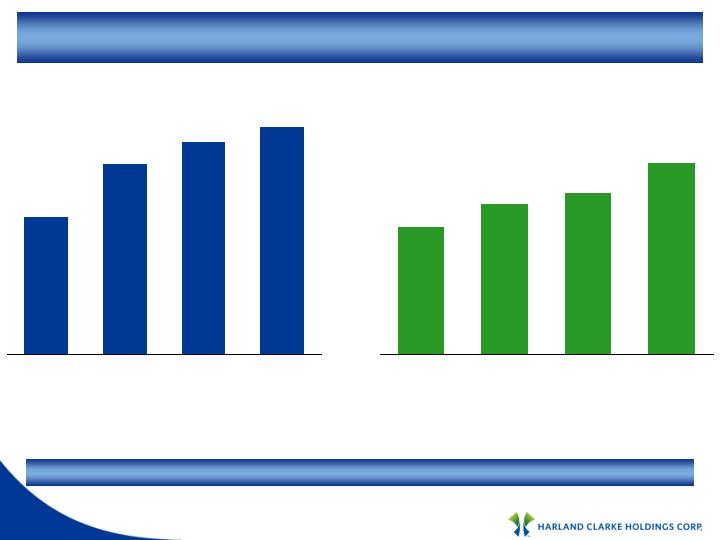

HFS financial performance

$ in millions

Revenue(1)

$ in millions

Margin 19.1% 20.6% 18.9% 21.7%

Adjusted EBITDA(2)

2007 revenue and adjusted EBITDA up 1.6% and 16.4%, respectively

(1) Revenue is adjusted to add back $10.2 million of purchase accounting fair value adjustments of deferred revenue for 2007, minus revenue from inter-segment transactions.

(2) Adjusted EBITDA consists of operating income, plus combined depreciation and amortization, plus adjustments to add back (i) the effect of purchase accounting fair value adjustments of inventory

and deferred revenue and (ii) Harland Acquisition-related expenses.

14

HFS

The table below presents a reconciliation of the operating income of the Harland Financial Solutions segment to adjusted EBITDA for 2004, 2005, 2006 and 2007.

($ in millions)

Harland Financial Solutions

2004

2005

2006

2007

Operating income

$ 32.6

$ 42.4

$ 42.9

$ 12.2

D&A

12.4

16.4

17.9

24.6

Purchase accounting related fair value adjustments

-

-

-

10.2

Harland Acquisition expenses

-

-

-

24.3

Adjusted EBITDA

$ 45.0

$ 58.8

$ 60.8

$ 71.3

15

Strong brand recognition

A leading testing provider for over 40 years

Razor blade model

Provide patent protected scanner to school

Sales of forms create annuity-like revenue

stream

Large installed base

80%+ of all public schools

45,000+ scanning machines

Customer diversification

100,000+ accounts

Largest account approximately 4% of

revenue

Focus on being a leading provider of

enterprise-wide testing and surveying

technology

School Forms and Testing

Surveys, Forms, and Processing

16

Data Management acquisition

$225 million acquisition of Data Management, a business of Pearson plc,

funded with cash on hand

Data Management products and services include:

Printed forms

Scanners and related software

Survey consulting

Tracking services

Revenues of $114 million and operating profit of $25 million in 2007

Significant synergy opportunities

Projected to be accretive to earnings in 2008

Will be operated by and integrated with Scantron

17

$75

$74

$78

$82

2004

2005

2006

2007

$26

$23

$25

$28

2004

2005

2006

2007

Scantron financial performance

2007 revenue and adjusted EBITDA up 5.1% and 12.0%, respectively

$ in millions

Revenue(1)

$ in millions

Margin 34.7% 31.1% 32.1% 34.1%

Adjusted EBITDA(2)

(1) Revenue is adjusted to add back $1.4 million of purchase accounting fair value adjustments of deferred revenue for 2007, minus revenue from inter-segment transactions.

(2) Adjusted EBITDA consists of operating income, plus combined depreciation and amortization, plus adjustments to add back (i) the effect of purchase accounting fair value adjustments of inventory

and deferred revenue and (ii) Harland Acquisition-related expenses.

18

Scantron

The table below presents a reconciliation of the operating income of the Scantron segment to adjusted EBITDA for 2004, 2005, 2006 and 2007.

($ in millions)

Scantron

2004

2005

2006

2007

Operating income

$ 22.7

$ 20.3

$ 21.9

$ 8.5

D&A

3.5

2.9

3.3

10.2

Purchase accounting related fair value adjustments

-

-

-

4.5

Harland Acquisition expenses

-

-

-

5.1

Adjusted EBITDA

$ 26.2

$ 23.2

$ 25.2

$ 28.3

19

Harland Clarke Holdings financial highlights

Strong historical financial performance

High EBITDA margins

Low working capital requirements

Efficient deployment of capital

Significant cash flow generation

20

(1) As reported; includes results of Harland since May 1, 2007, the date of the acquisition.

(2) Adjustments to EBITDA are net of upfront contract payment amortization and adds back purchase accounting related fair value adjustments to inventory and deferred revenue, restructuring expense,

transaction-related expense, intangible asset impairment, and a contingent earn-out payment related to a prior transaction. Adjusted EBITDA for these periods is reconciled in Harland Clarke Holdings

8-K dated February 29, 2008.

Harland Clarke Holdings 3 months and year ended

($ in millions)

3 months ended

12/31/06

3 months ended

12/31/07

Year ended

12/31/06

Year ended

(1)

12/31/07

Revenue

149.5

$

432.9

$

623.9

$

1,369.9

$

Adjusted EBITDA

(2)

34.1

$

110.7

$

147.1

$

347.6

$

Margin

22.8%

25.6%

23.6%

25.4%

21

$1,398

$1,595

$1,674

$1,728

2004

2005

2006

2007

$273

$323

$345

$409

2004

2005

2006

2007

Harland Clarke Holdings financial performance

2007 revenue and adjusted EBITDA up 3.2% and 18.6%, respectively

Combined Revenue(1)

$ in millions

$ in millions

Combined Adjusted EBITDA(2)

(1) Combined revenue is the sum of the revenues of Harland Clarke Holdings (which consists of only Clarke American revenues prior to May 1, 2007), plus revenues of John H. Harland Company for

periods prior to the completion of the Harland Acquisition on May 1, 2007, plus an adjustment to add back $12.2 million purchase accounting fair value adjustments of deferred revenue for 2007.

(2) Combined Adjusted EBITDA is the sum of the consolidated net income of Harland Clarke Holdings (which consisted only of Clarke American’s net income prior to May 1, 2007) plus the consolidated

net income of John H. Harland Company for periods prior to the completion of the Harland Acquisition on May 1, 2007, before combined net interest expense, combined income taxes and combined

depreciation and amortization (other than amortization related to upfront contract payments), plus adjustments to add back (i) purchase accounting fair value adjustments of inventory and deferred

revenue, (ii) Harland Acquisition-related expenses, (iii) intangible asset impairment, (iv) a contingent earn-out payment and (v) restructuring expenses.

Margin 19.5% 20.3% 20.6% 23.7%

22

Harland Clarke Holdings Corp.

The table below presents a reconciliation of (x) the combined consolidated net income of Harland Clarke Holdings and John H. Harland Company to (y) combined adjusted EBITDA for 2004, 2005, 2006 and 2007.

($ in millions)

(1) For periods prior to May 1, 2007, consists of the consolidated net income of Clarke American Corp.

(2) Consists of the consolidated net income of John H. Harland Company for periods prior to May 1, 2007.

Harland Clarke Holdings Corp

2004

2005

2006

2007

Harland Clarke Holdings consolidated net income (1)

$ 64.4

$ 40.7

$ 19.5

$ (15.4)

John H. Harland consolidated net income (2)

55.1

75.5

68.1

(50.9)

Combined consolidated net income

119.5

116.2

87.6

(66.3)

Combined net interest expense

23.2

20.8

76.1

164.3

Combined Income tax expense

56.2

73.0

49.2

(30.5)

Loss on early extingushment of debt

-

-

-

54.6

Other expenses

(0.9)

(0.4)

3.8

0.5

Combined D&A (other than upfront contract payments amort)

68.2

104.5

110.3

143.3

Purchase accounting related fair value adjustments

-

4.9

1.3

16.6

Harland Acquisition expenses

-

-

12.6

118.3

Intangible asset impairment costs

-

-

-

3.1

Contingent earnout payment

6.5

1.9

1.1

-

Restructuring expenses

-

2.4

3.3

5.6

Combined adjusted EBITDA

$ 272.7

$ 323.3

$ 345.3

$ 409.5

23

Harland Clarke Holdings credit strength

YTD cash flow from operations(1) $210.0 million

Cash on hand(2) &nbs p; $239.7 million

Net debt(3) &nb sp; $2,170.2 million

2007 Full Synergies Combined Adjusted EBITDA(4) $492.1 million

Net debt / 2007 full synergies adj. EBITDA 4.4x

2007 full synergies adj. EBITDA / PF interest(5) 2.5x

12/31/2007

(1) As reported; includes results of Harland since May 1, 2007, the date of the acquisition.

(2) Cash on hand as of the date of this presentation is substantially lower due to $225.0 million used for the Data Management acquisition.

(3) Net debt equals total debt of $2,409.9 million less cash and equivalents as of December 31, 2007, as reported; cash and equivalents are substantially lower now than at year-end as a result of the Data Management acquisition.

(4) Combined Adjusted EBITDA for Harland Clarke Holdings Corp. plus an adjustment to reflect the full $112.6 million of annual run-rate synergies described previously. No

pro forma adjustments were made.

(5) PF Interest of $193.2 million reflects one year of interest on total debt as of 12/31/2007.

24