Exhibit 99.1

|

Public Lenders' Presentation

Confidential

May 2011

1

|

|

Forward Looking Statements

Certain information in this presentation may be considered forward-looking

information within the definition of the Private Securities Litigation Reform

Act of 1995. This information is based on the Company's current expectations

and actual results could vary materially depending on risks and uncertainties

that may affect the Company's operations, markets, services, prices and other

factors as discussed in filings with the Securities and Exchange Commission.

These risks and uncertainties include, but are not limited to, general and

economic conditions and declines in the industries in which we participate.

There is no assurance that the Company's expectations will be realized. All

forward looking statements speak only as of the date of this presentation. All

subsequent written and oral forward-looking statements attributable to us or

any person acting on our behalf are qualified by the cautionary statements in

this section. The Company assumes no obligation to update any forward-looking

information contained in this presentation.

2

|

|

Table of Contents

I. Company Overview

Chuck Dawson

Chief Executive Officer

II. Key Credit Highlights

Chuck Dawson

Chief Executive Officer

III. Financial Overview

Peter Fera

Chief Financial Officer

IV. Transaction Terms and Timing

Credit Suisse

Appendix

3

|

|

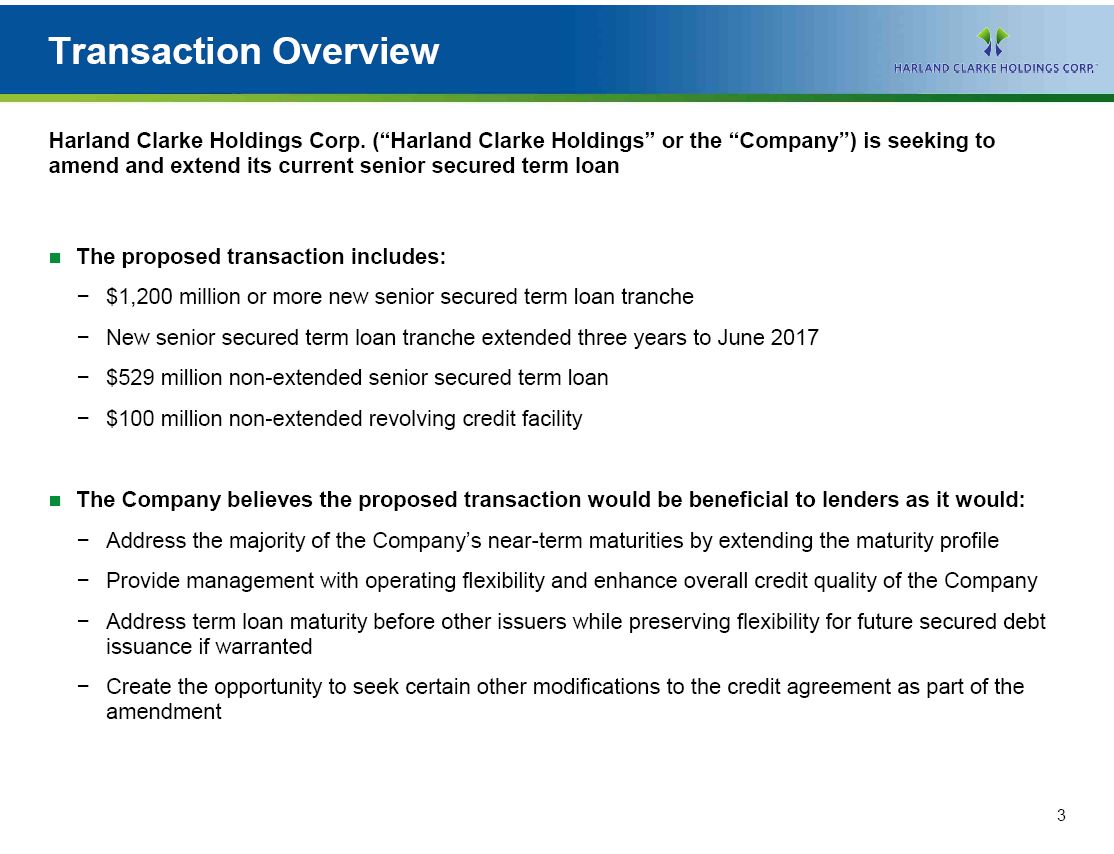

Transaction Overview

Harland Clarke Holdings Corp. ("Harland" or the "Company") is seeking to amend

and extend its

current senior secured term loan

[] The proposed transaction includes:

[] $1,200 million or more new senior secured term loan tranche

[] New senior secured term loan tranche extended three years to June 2017

[] $529 million non-extended senior secured term loan

[] $100 million non-extended revolving credit facility

[] The Company believes the proposed transaction would be beneficial to

lenders as it would:

[] Address the majority of the Company's near-term maturities by extending the

maturity profile

[] Provide management with operating flexibility and enhance overall credit

quality of the Company

[] Address term loan maturity before other issuers while preserving

flexibility for future secured debt issuance if warranted

[] Create the opportunity to seek certain other modifications to the credit

agreement as part of the amendment

4

|

|

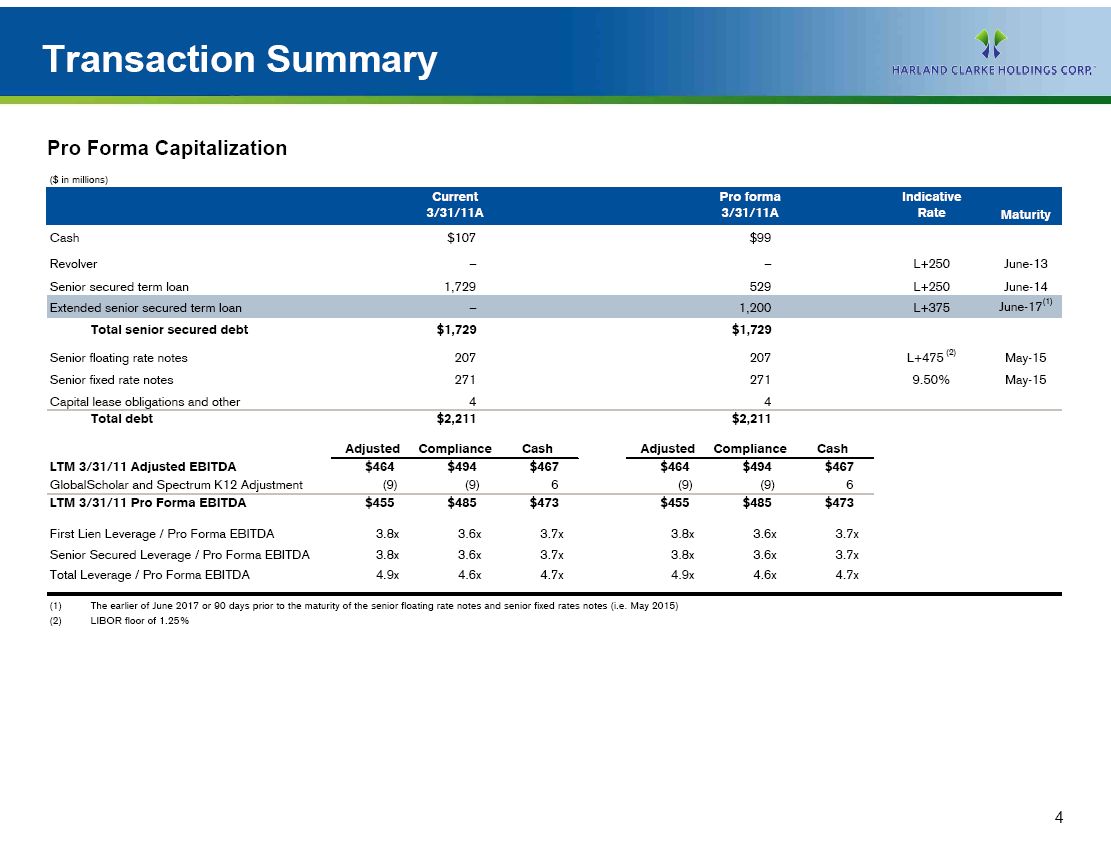

Transaction Summary

Pro Forma Capitalization

($ in millions)

=================================== ========== =========== =========== ===========

Current Pro forma Indicativ

3/31/11A 3/31/11A Rate Maturity

=================================== ========== =========== =========== ===========

Cash $107 $9

Revolver -- -- L+250 June-13

Senior secured term loan 1,729 529 L+250 June-14

(1)

June-17

Extended senior secured term loan -- 1,200 L+375

Total senior secured debt $1,729 $1,729

(2)

Senior floating rate notes 207 207 L+475 May-15

Senior fixed rate notes 271 271 9.50% May-15

Capital lease obligations and other 4 4

=================================== ========== =========== =========== ===========

Total debt $2,211 $2,21

Adjusted Compliance Cash Adjusted Compliance Cash

========== ============ ======= ========== ============ =======

LTM 3/31/11 Adjusted EBITDA $464 $494 $467 $464 $494 $46

GlobalScholar and Spectrum K12 Adjustment (9) (9) 6 (9) (9) 6

========================================== ========== ============ ======= ========== ============ =======

LTM 3/31/11 Pro Forma EBITDA $455 $485 $473 $455 $485 $47

First Lien Leverage / Pro Forma EBITDA 3.8x 3.6x 3.7x 3.8x 3.6x 3.7x

Senior Secured Leverage / Pro Forma EBITDA 3.8x 3.6x 3.7x 3.8x 3.6x 3.7x

Total Leverage / Pro Forma EBITDA 4.9x 4.6x 4.7x 4.9x 4.6x 4.7x

(1) The earlier of June 2017 or 90 days prior to the maturity of the senior

floating rate notes and senior fixed rates notes (i.e. May 2015)

(2) LIBOR floor of 1.25%

5

|

|

Management Presenters

Chuck Dawson

Chief Executive Officer

[] Over 34 years of experience in the financial services and security printing

industry

[] Over 18 years with Clarke American / Harland Clarke

[] Former Chief Executive Officer of Rocky Mountain Bank Note; began career at

IBM

[] B. A. in Marketing and an MBA from Lamar University

Peter Fera

Executive Vice President

and Chief Financial Officer

[] 17 years of experience with Harland Clarke, Honeywell, and GE in various

financial and operational leadership roles

[] Appointed Executive Vice President and Chief Financial Officer in May 2007

[] Former Chief Financial Officer of Honeywell's Aircraft Landing Systems

business from October 2003 to April 2005

[] B. A. in Mechanical Engineering from University of Pennsylvania, an M. A.

in Mechanical Engineering from MIT and an MBA in Management from MIT's

Sloan School of Management

6

|

|

I. Company Overview

Chuck Dawson, Chief Executive Officer

7

|

|

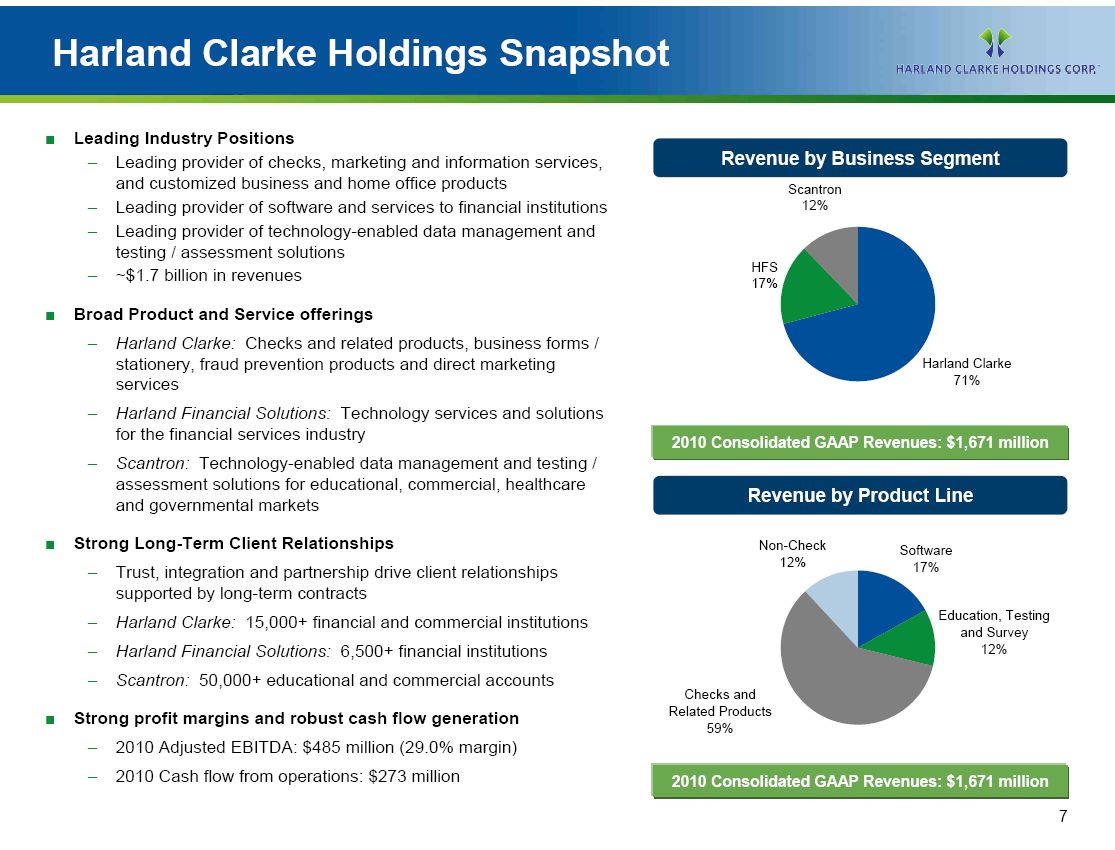

Harland Clarke Holdings Snapshot

[] Leading Industry Positions

-- Leading provider of checks, marketing and information services, and

customized business and home office products

-- Leading provider of software and services to financial institutions

-- Leading provider of technology-enabled data management and testing /

assessment solutions

-- $1.7 billion in revenues

[] Broad Product and Service offerings

-- Harland Clarke: Checks and related products, business forms / stationery,

fraud prevention products and direct marketing services

-- Harland Financial Solutions: Technology services and solutions for the

financial services industry

-- Scantron: Technology-enabled data management and testing / assessment

solutions for educational, commercial, healthcare and governmental markets

[] Strong Long-Term Client Relationships

-- Trust, integration and partnership drive client relationships supported by

long-term contracts

-- Harland Clarke: 15,000+ financial and commercial institutions

-- Harland Financial Solutions: 6,500+ financial institutions

-- Scantron: 50,000+ educational and commercial accounts

[] Strong profit margins and robust cash flow generation

-- 2010 Adjusted EBITDA: $485 million (29.0% margin)

-- 2010 Cash flow from operations: $273 million

Revenue by Business Segment

[GRAPHIC OMITTED]

2010 Consolidated GAAP Revenues: $1,671 million

Revenue by Product Line

[GRAPHIC OMITTED]

2010 Consolidated GAAP Revenues: $1,671 million

8

|

|

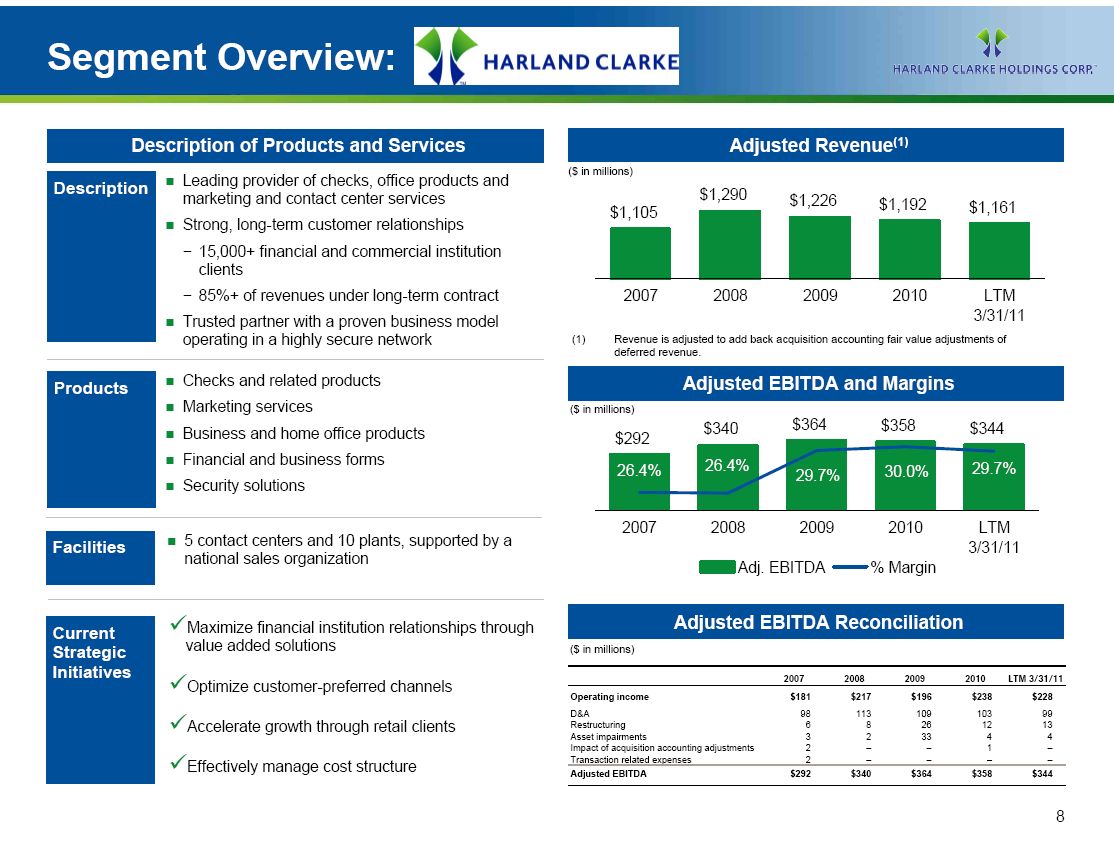

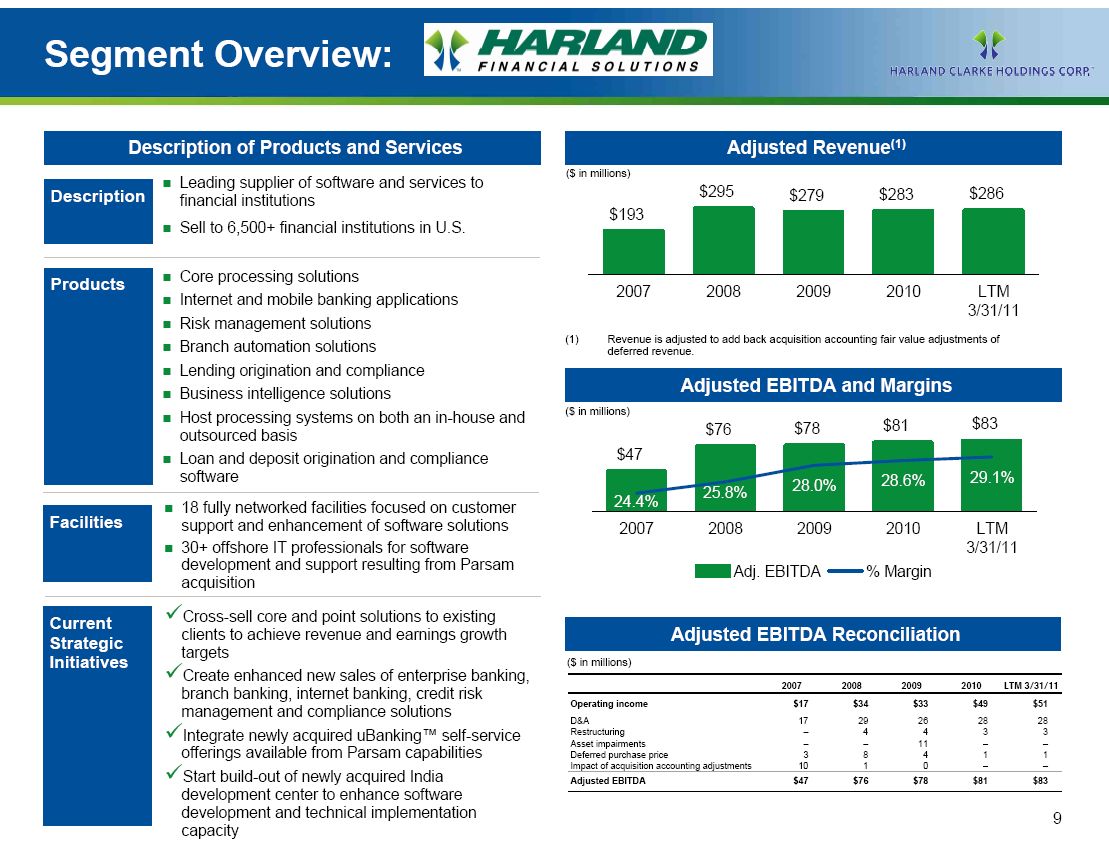

Segment Overview:

Description of Products and Services

Description

[] Leading provider of checks, office products and marketing and contact

center services

[] Strong, long-term customer relationships

[] 15,000+ financial and commercial institution clients

[] 85%+ of revenues under long-term contract

[] Trusted partner with a proven business model operating in a highly secure

network

Products

[] Checks and related products

[] Marketing services

[] Business and home office products

[] Financial and business forms

[] Security solutions

Facilities

[] 5 contact centers and 10 plants, supported by a national sales organization

Current Strategic Initiatives

[] Maximize financial institution relationships through value added solutions

[] Optimize customer-preferred channels

[] Accelerate growth through retail clients

[] Effectively manage cost structure

(1) Adjusted Revenue

($ in millions)

[GRAPHIC OMITTED]

(1) Revenue is adjusted to add back acquisition accounting fair value

adjustments of deferred revenue.

Adjusted EBITDA and Margins

($ in millions)

[GRAPHIC OMITTED]

Adjusted EBITDA Reconciliation

($ in millions)

-------------------------------------------- ----- ------ ------ ------ -----------

2007 2008 2009 2010 LTM 3/31/11

============================================ ===== ====== ====== ====== ===========

Operating income $181 $217 $196 $238 $22

D and A 98 113 109 103 99

Restructuring 6 8 26 12 13

Asset impairments 3 2 33 4 4

Impact of acquisition accounting adjustments 2 -- -- 1 --

Transaction related expenses 2 -- -- -- --

============================================ ===== ====== ====== ====== ===========

Adjusted EBITDA $292 $340 $364 $358 $34

9

|

|

Segment Overview:

Description of Products and Services

Description

[] Leading supplier of software and services to financial institutions

[] Sell to 6,500+ financial institutions in U. S.

Products

[] Core processing systems

[] Internet and mobile banking applications

[] Risk management solutions

[] Branch automation solutions

[] Lending origination and compliance

[] Business intelligence solutions

[] Host processing systems on both an in-house and outsourced basis

[] Proprietary loan and deposit origination and compliance software

Facilities

[] 18 fully networked facilities focused on customer support and enhancement

of software solutions

[] 30+ offshore IT professionals for software development and support

resulting from Parsam acquisition

Current Strategic Initiatives

[] Cross-sell core and point solutions to existing clients to achieve revenue

and earnings growth targets

[] Create enhanced new sales of enterprise banking, branch banking, internet

banking, credit risk management and compliance solutions

[] Integrate newly acquired uBanking[] self-service offerings available from

Parsam capabilities

[] Start build-out of newly acquired India development center to enhance

software development and technical implementation capacity

(1)

Adjusted Revenue

[GRAPHIC OMITTED]

Adjusted EBITDA and Margins

[GRAPHIC OMITTED]

Adjusted EBITDA Reconciliation

($ in millions)

-------------------------------------------- ------ ------ ----- ------ -----------

2007 2008 2009 2010 LTM 3/31/11

============================================ ====== ====== ===== ====== ===========

Operating income $17 $34 $33 $49 $5

D and A 17 29 26 28 28

Restructuring -- 4 4 3 3

Asset impairments -- -- 11 -- --

Deferred purchase price 3 8 4 1 1

Impact of acquisition accounting adjustments 10 1 0 -- --

============================================ ====== ====== ===== ====== ===========

Adjusted EBITDA $47 $76 $78 $81 $8

10

|

|

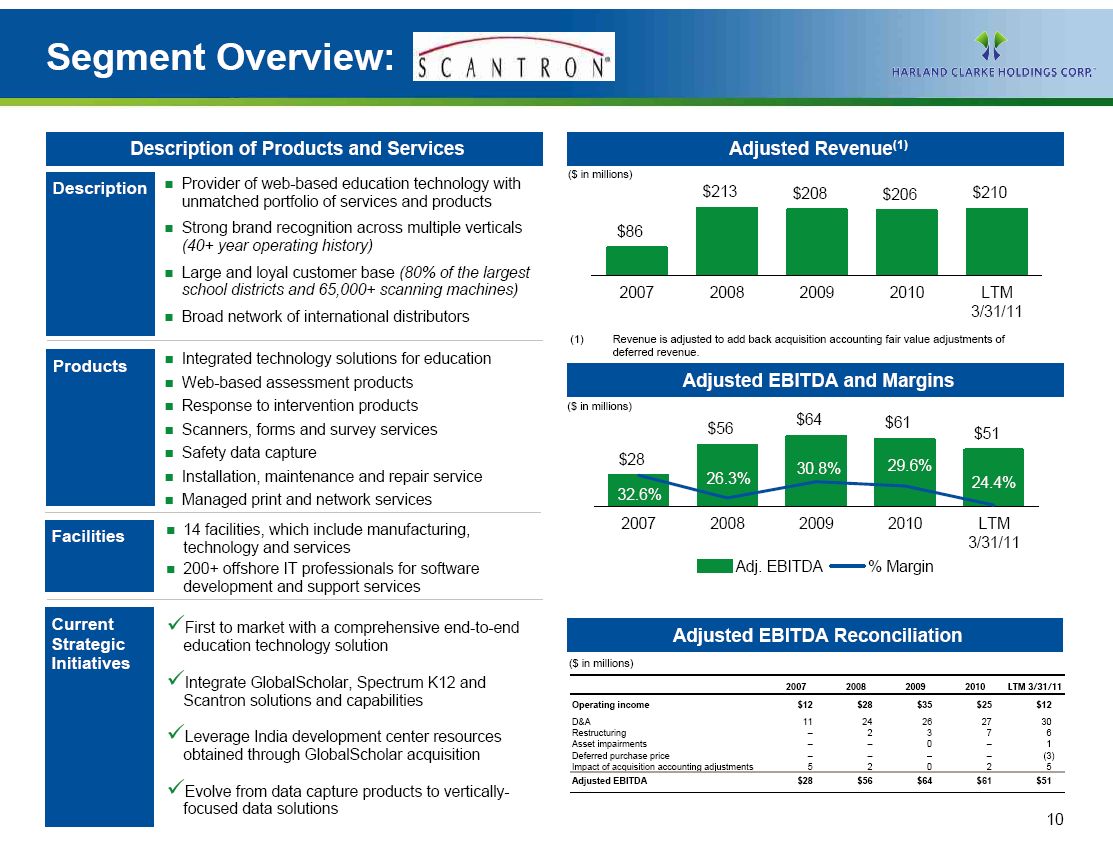

Segment Overview:

Description of Products and Services

Description

[] Provider of web-based education technology with unmatched portfolio of

services and products

[] Strong brand recognition across multiple verticals (40+ year operating

history)

[] Large and loyal customer base (80% of the largest school districts and

65,000+ scanning machines)

[] Broad network of international distributors

Products

[] Integrated technology solutions for education

[] Web-based assessment products

[] Response to intervention products

[] Scanners, forms and survey services

[] Safety data capture

[] Installation, maintenance and repair service

[] Managed print and network services

Facilities

[] 14 facilities, which include manufacturing, technology and services

[] 200+ offshore IT professionals for software development and support

services

Current Strategic Initiatives

[] First to market with a comprehensive end-to-end education technology

solution

[] Integrate GlobalScholar, Spectrum K12 and

Scantron solutions and capabilities

[] Leverage Indian development center resources obtained through GlobalScholar

acquisition

[] Evolve from data capture products to vertically- focused data solutions

(1)

Adjusted Revenue

[GRAPHIC OMITTED]

Adjusted EBITDA and Margins

[GRAPHIC OMITTED]

Adjusted EBITDA Reconciliation

($ in millions)

-------------------------------------------- ------ ------ ------ ------ -----------

2007 2008 2009 2010 LTM 3/31/11

============================================ ====== ====== ====== ====== ===========

Operating income $12 $28 $35 $25 $1

D and A 11 24 26 27 30

Restructuring -- 2 3 7 6

Asset impairments -- -- 0 -- 1

Deferred purchase price -- -- -- -- (3)

Impact of acquisition accounting adjustments 5 2 0 2 5

============================================ ====== ====== ====== ====== ===========

Adjusted EBITDA $28 $56 $64 $61 $5

11

|

|

Segment Overview:

Acquisition of GlobalScholar

Business description

GlobalScholar delivers the technical innovations that meet the needs of today's

evolving data-driven educational system

[] Dedicated to building a bridge to change for education by offering

powerful, leading edge solutions and viable transformational opportunities

at all levels of the education community

[] End-to-end solution, Pinnacle Suite[], increases teacher effectiveness,

improves communication and empowers educators to transform practices that

improve student learning

[] Customers that benefit from the GlobalScholar solution:

[] K-12 and Higher Education -- benefit from learning-centric tools

integrating all the data sources for each student -- student information,

standards-based curriculum, assessment and gradebook

[] Professional Development -- improves teacher effectiveness, develops 21st

Century teaching skills, delivers research-based practices on school

improvement, and brings real value to the hands of teachers

[] Tutoring and Test Preparation -- provide tutoring companies and

institutions of all sizes with an end-to-end, web-based solution for

efficiently managing existing tutoring services and expanding their

business into an online/offline/hybrid education vertical

Transaction Rationale

[] GlobalScholar's instructional management platform supports all aspects of

managing education at K-12 schools

[] Complements Scantron's testing and assessment, response to intervention,

student achievement management and special education software solutions

[] Adding GlobalScholar's product offering and customer base to a larger,

well-run company like Scantron creates significant revenue and cost

synergies

On January 3, 2011 Scantron completed the acquisition of GlobalScholar

12

|

|

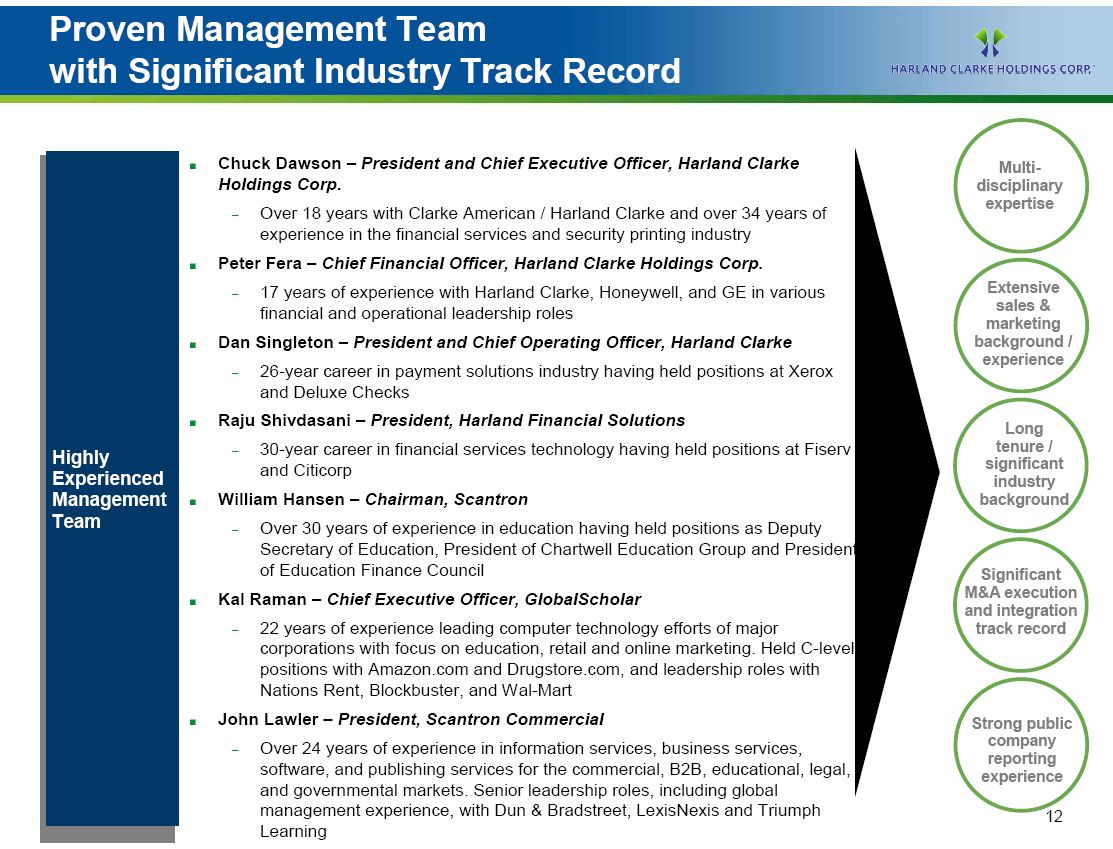

Proven Management Team with Significant Industry Track Record

[GRAPHIC OMITTED]

[] Chuck Dawson -- President and Chief Executive Officer, Harland Clarke

Holdings Corp.

-- Over 18 years with Clarke American / Harland Clarke and over 34 years of

experience in the financial services and security printing industry

[] Peter Fera -- Chief Financial Officer, Harland Clarke Holdings Corp.

-- 17 years of experience with Harland Clarke, Honeywell, and GE in various

financial and operations leadership roles

[] Dan Singleton -- President and Chief Operating Officer, Harland Clarke

-- 26-year career in payment solutions industry having held positions at Xerox

and Deluxe Checks

[] Raju Shivdasani -- President, Harland Financial Solutions

-- 30-year career in financial services technology having held positions at

Fiserv and Citicorp

[] William Hansen -- Chairman, Scantron

-- Over 30 years of experience in education having held positions as Deputy

Secretary of Education, President of Chartwell Education Group and President of

Education Finance Council

[] Kal Raman -- Chief Executive Officer, GlobalScholar

-- 22 years of experience leading computer technology efforts of major

corporations with focus on education, retail and online marketing. Held

C-level positions with Amazon. com and Drugstore. com, and leadership roles

with Nations Rent, Blockbuster, and Wal-Mart

[] John Lawler -- President, Scantron Commercial

-- Over 24 years of experience in information services, business services,

software, and publishing services for the commercial, B2B, educational, legal,

and governmental markets. Senior leadership roles, including global management

experience, with Dun and Bradstreet, LexisNexis and Triumph Learning

Multi-disciplinary expertise

Extensive sales and marketing background / experience

Long tenure / significant industry background

Significant M and A execution and integration track record

Strong public company reporting experience

13

|

|

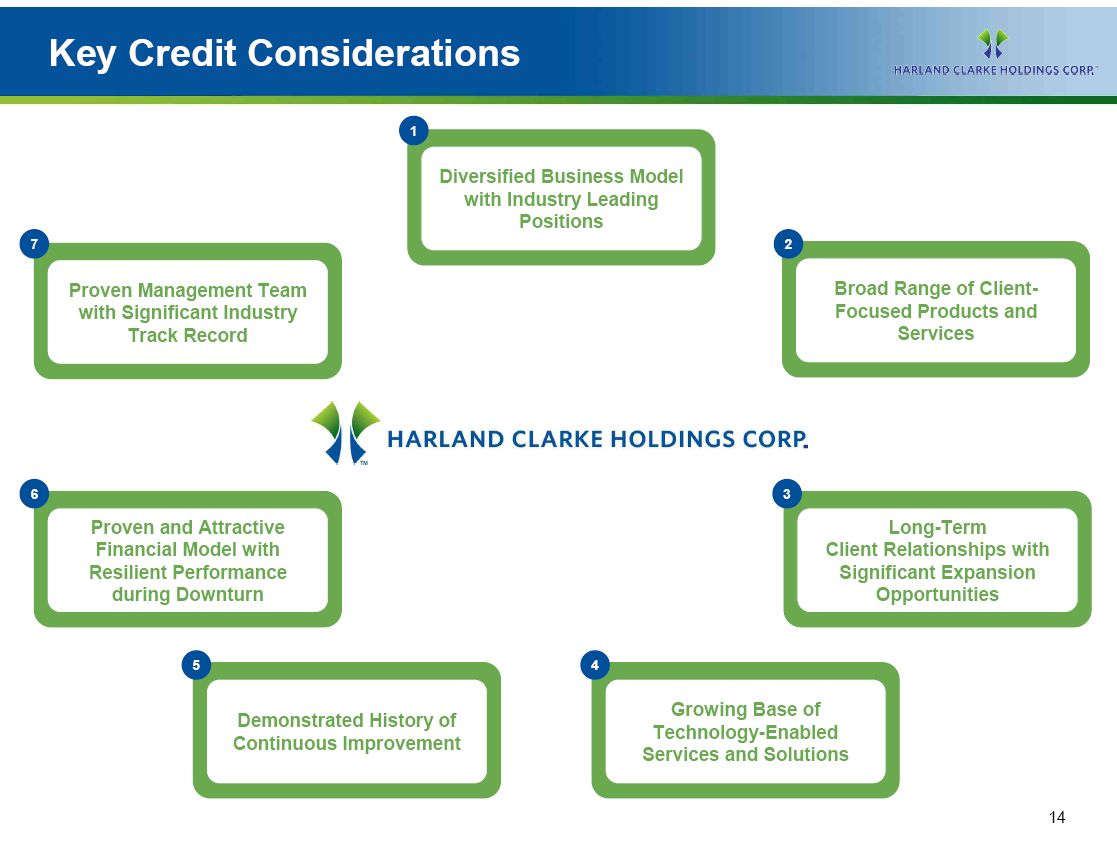

II. Key Credit Highlights

Chuck Dawson, Chief Executive Officer

14

|

|

[GRAPHIC OMITTED]

Diversified Business Model with Industry Leading Positions

Broad Range of Client-Focused Products and Services

Long-Term Client Relationships with Significant Expansion

Opportunities

Growing Base of Technology-Enabled Services and Solutions

Demonstrated History of

Continuous Improvement

Proven and Attractive Financial Model with Resilient Performance during

Downturn

Proven Management Team with Significant Industry Track Record

15

|

|

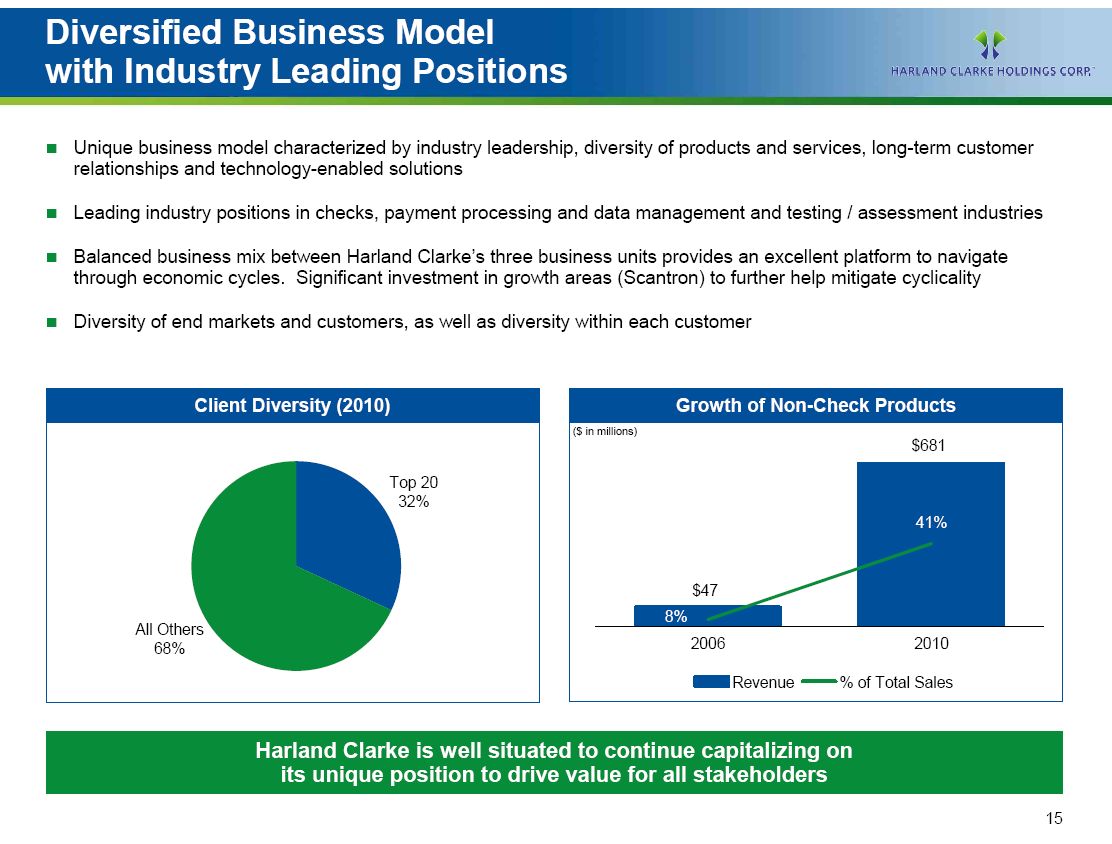

Diversified Business Model

with Industry Leading Positions

[] Unique business model characterized by industry leadership, diversity of

products and services, long-term customer relationships and

technology-enabled solutions

[] Leading industry positions in checks, payment processing and data

management and testing / assessment industries

[] Balanced business mix between Harland Clarke's three business units

provides an excellent platform to navigate through economic cycles.

Significant investment in growth areas (Scantron) to further help mitigate

cyclicality

[] Diversity of end markets and customers, as well as diversity within each

customer

Client Diversity (2010)

[GRAPHIC OMITTED]

Growth of Non-Check Products

[GRAPHIC OMITTED]

Harland Clarke is well situated to continue capitalizing on

its unique position to drive value for all stakeholders

16

|

|

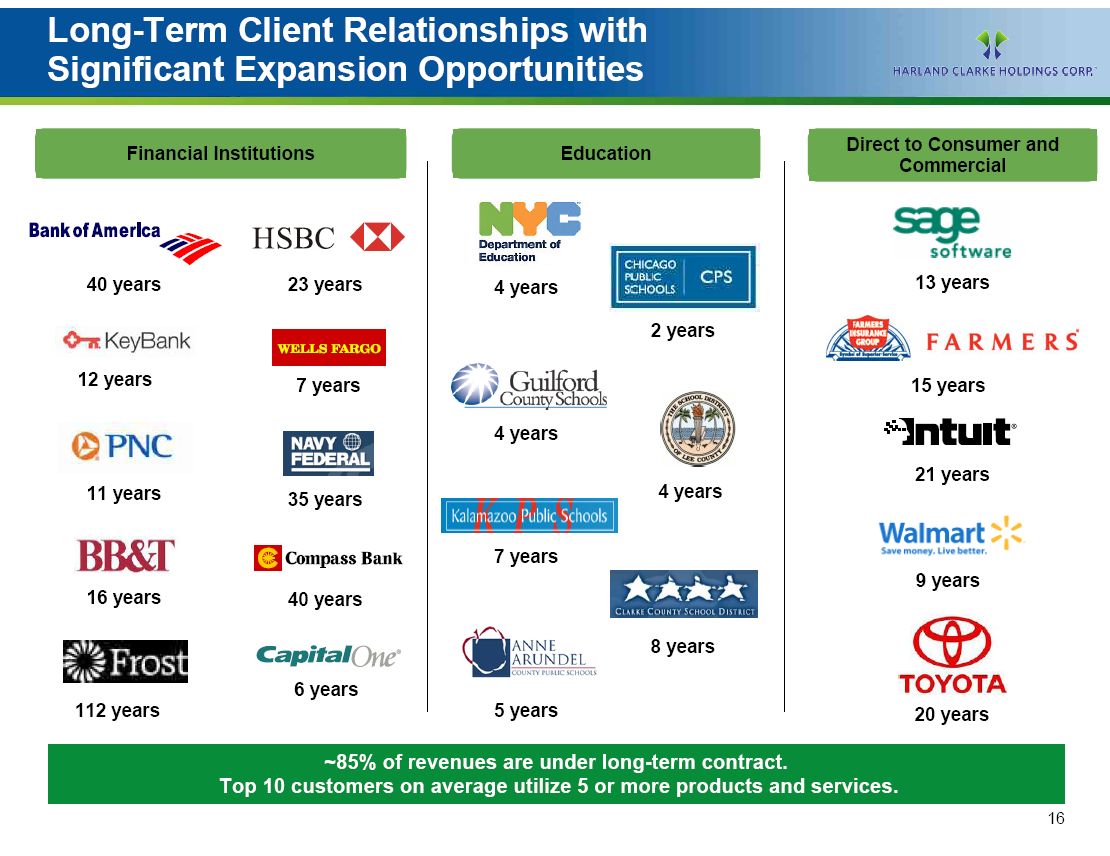

Long-Term Client Relationships with

Significant Expansion Opportunities

Financial Institutions

[GRAPHIC OMITTED]

Education

[GRAPHIC OMITTED]

Direct to Consumer and

Commercial

[GRAPHIC OMITTED]

~85% of revenues are under long-term contracts.

Top 10 customers on average utilize 5 or more products and services.

17

|

|

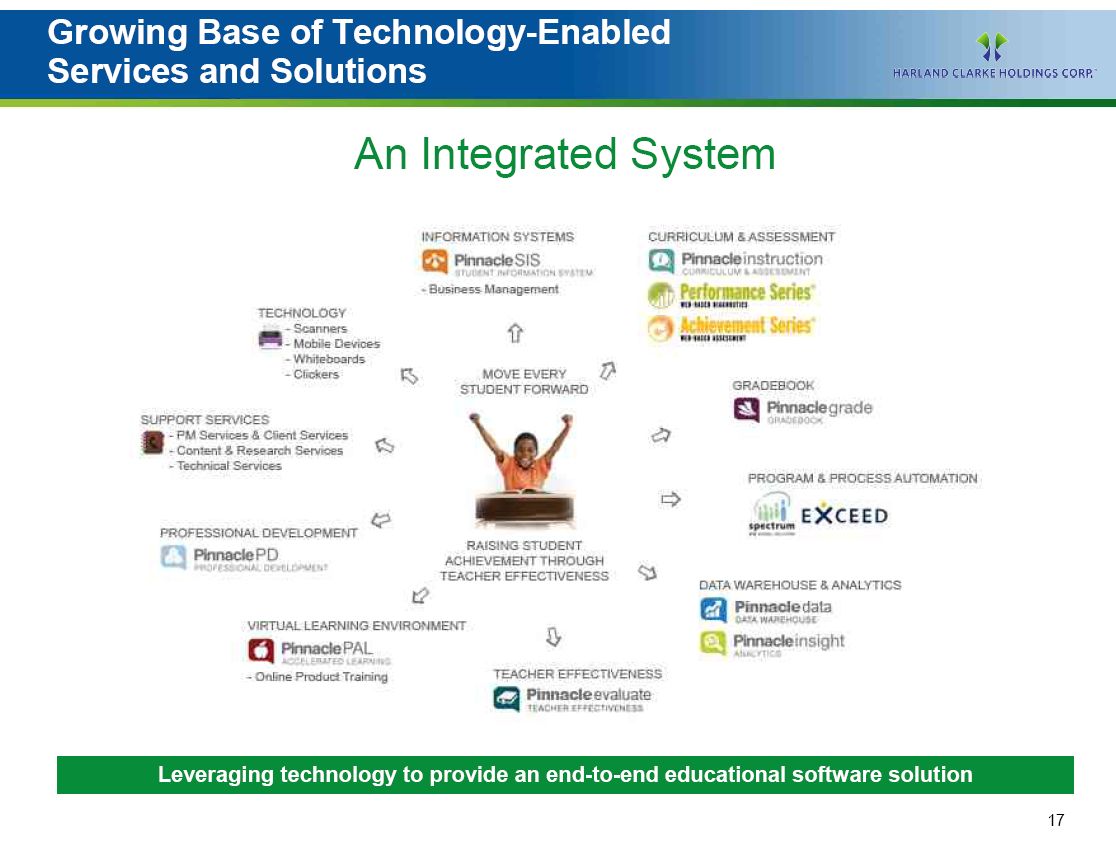

Growing Base of Technology-Enabled

Services and Solutions

An Integrated System

Leveraging technology to provide an end-to-end educational software solution

18

|

|

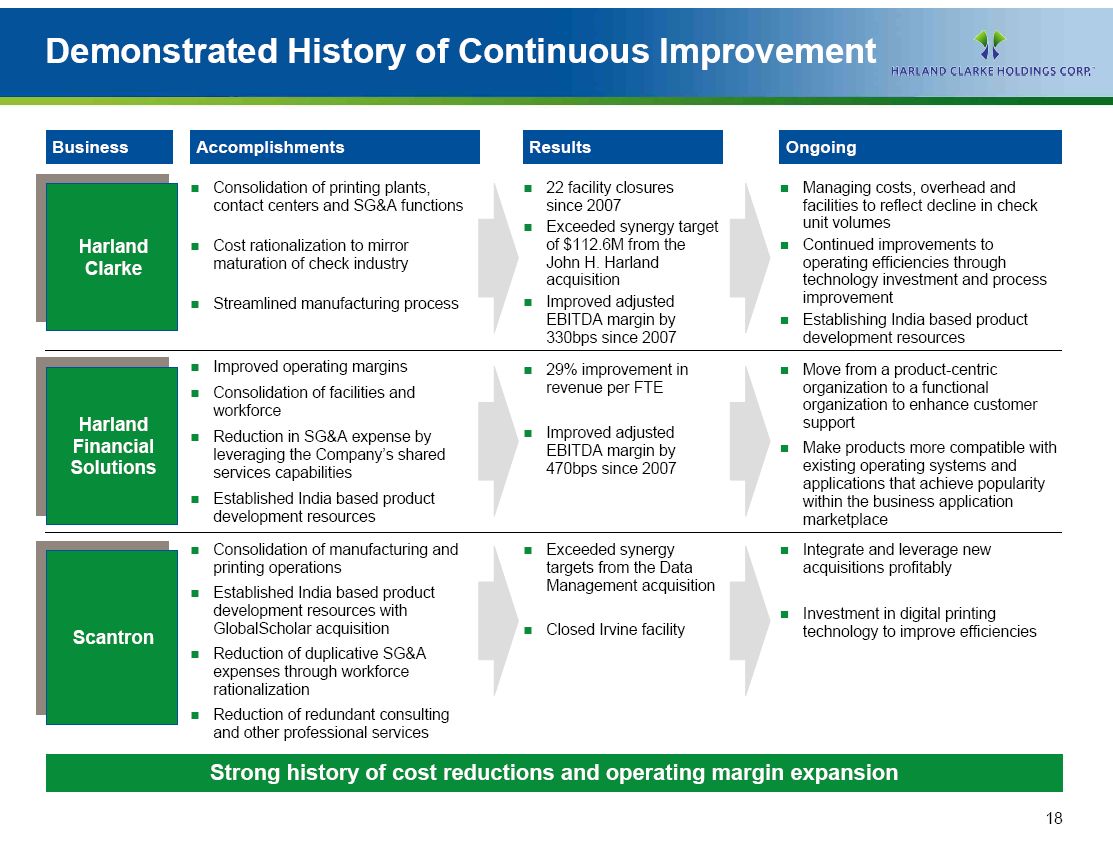

Demonstrated History of Continuous Improvement

Business Accomplishments Results Ongoing

============= -------------------------------------- --------------------------- ------------------------------------------

[] [] []

Consolidation of printing plants, 22 facility closures Managing costs, overhead and

contact centers and SG and A functions since 2007 facilities to reflect decline in check

[] unit volumes

Exceeded synergy target

[] []

Cost rationalization to mirror of $112.6M from the Continued improvements to

Harland

maturation of check industry John H. Harland operating efficiencies through

Clarke

acquisition technology investment and process

[] improvement

[] Improved adjusted

Streamlined manufacturing process

[]

EBITDA margin by Establishing India based product

330bps since 2007 development resources

============= -------------------------------------- --------------------------- ------------------------------------------

[] Improved operating margins [] []

29% improvement in Move from a product-centric

[] revenue per FTE organization to a functional

Consolidation of facilities and

organization to enhance customer

workforce

support

Harland

[]

[] Improved adjusted

Reduction in SG and A expense by

[]

Financial Make products more compatible with

EBITDA margin by

leveraging the Company's shared

existing operating systems and

Solutions 470bps since 2007

services capabilities

applications that achieve popularity

[]

Established India based product

within the business application

development resources

marketplace

============= -------------------------------------- --------------------------- ------------------------------------------

[] [] []

Consolidation of manufacturing and Exceeded synergy Integrate and leverage new

printing operations targets for Data acquisitions profitably

Management acquisition

[]

Established India based product

development resources with []

Investment in digital printing

[]

GlobalScholar acquisition Closed Irvine facility technology to improve efficiencies

Scantron

[]

Reduction of duplicative SG and A

expenses through workforce

rationalization

[]

Reduction of redundant consulting

and other professional services

Strong history of cost reductions and operating margin expansion

19

|

|

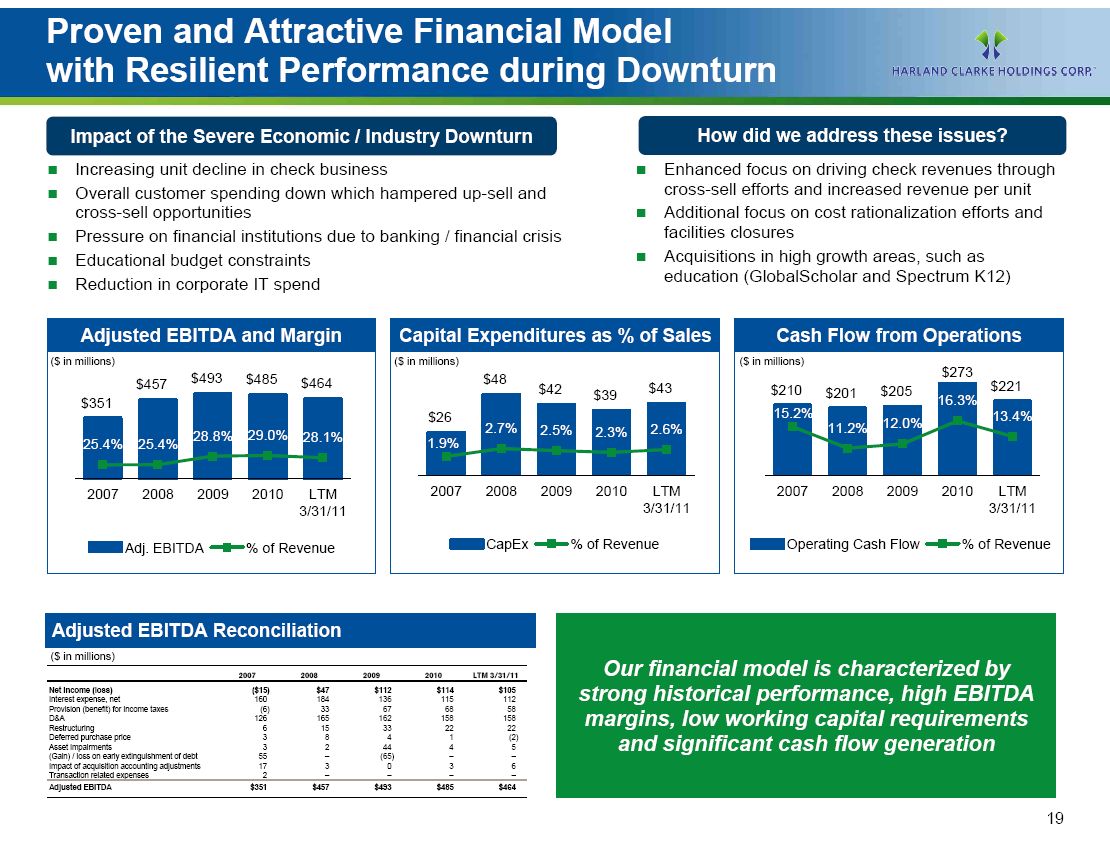

Proven and Attractive Financial Model

with Resilient Performance during Downturn

Impact of the Severe Economic / Industry Downturn

[] Increasing unit decline in check business

[] Overall customer spending down which hampered up-sell and

cross-sell opportunities

[] Pressure on financial institutions due to banking / financial crisis

[] Educational budget constraints

[] Reduction in corporate IT spend

How did we address these issues?

[] Enhanced focus on driving check revenues through

cross-sell efforts and increased revenue per unit

[] Additional focus on cost rationalization efforts and

facilities closures

[] Acquisitions in high growth areas, such as

education (GlobalScholar and Spectrum K12)

Adjusted EBITDA and Margin

[GRAPHIC OMITTED]

Capital Expenditures as % of Sales

[GRAPHIC OMITTED]

Cash Flow from Operations

[GRAPHIC OMITTED]

Adjusted EBITDA Reconciliation

($ in millions)

--------------------------------------------- ------- ------ ------- ------ -----------

2007 2008 2009 2010 LTM 3/31/11

============================================= ======= ====== ======= ====== ===========

Net income (loss) ($15) $47 $112 $114 $10

Interest expense, net 160 184 136 115 112

Provision (benefit) for income taxes (6) 33 67 68 58

D and A 126 165 162 158 158

Restructuring 6 15 33 22 22

Deferred purchase price 3 8 4 1 (2)

Asset impairments 3 2 44 4 5

(Gain) / loss on early extinguishment of debt 55 -- (65) -- --

Impact of acquisition accounting adjustments 17 3 0 3 6

Transaction related expenses 2 -- -- -- --

============================================= ======= ====== ======= ====== ===========

Adjusted EBITDA $351 $457 $493 $485 $46

Our financial model is characterized by strong historical performance, high

EBITDA margins, low working capital requirements and significant cash flow

generation

20

|

|

III. Financial Overview

Peter Fera, Chief Financial Officer

21

|

|

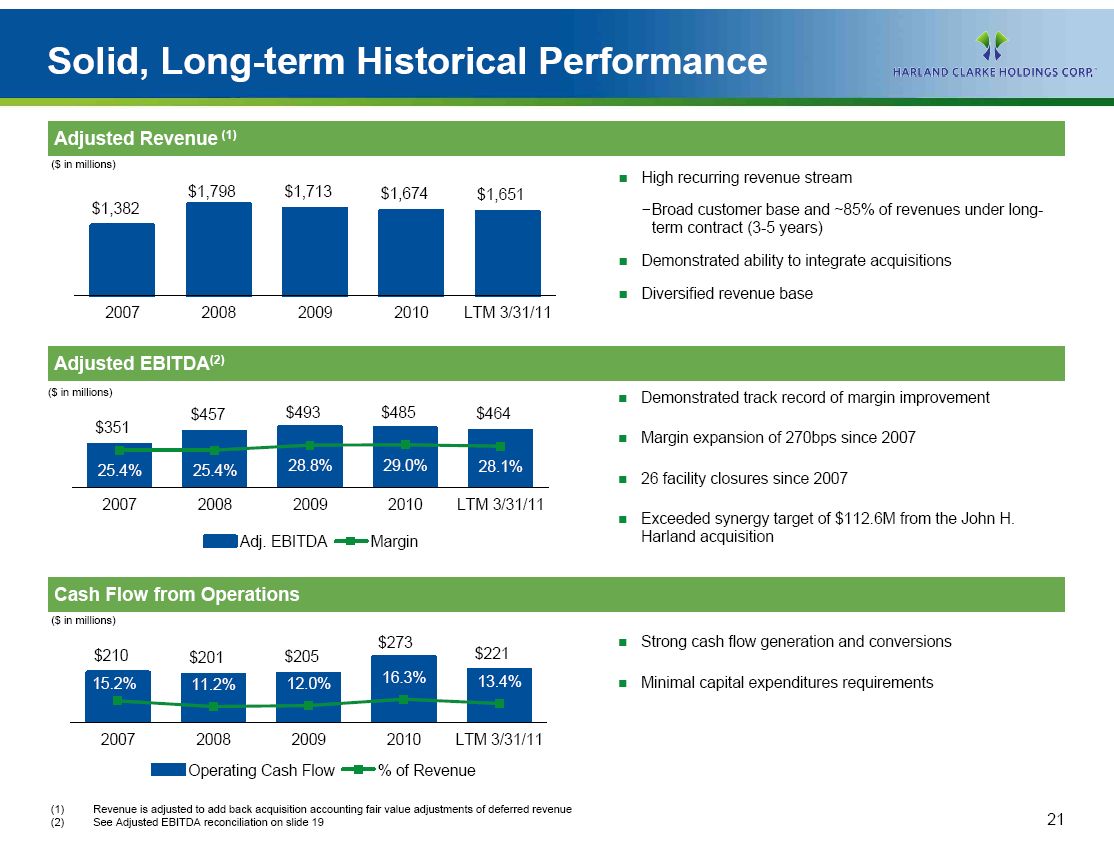

Solid, Long-term Historical Performance

[GRAPHIC OMITTED]

[GRAPHIC OMITTED]

[] High recurring revenue stream

[]Broad customer base and ~85% of revenues under long-

term contract (3-5 years)

[] Demonstrated ability to integrate acquisitions

[] Diversified revenue base

(2) Adjusted EBITDA

[GRAPHIC OMITTED]

[] Demonstrated track record of margin improvement

[] Margin expansion of 270bps since 2007

[] 26 facility closures since 2007

[] Exceeded synergy target of $112.6M from the John H.

Harland acquisition

Cash Flow from Operations

[GRAPHIC OMITTED]

[] Strong cash flow generation and conversions

[] Minimal capital expenditures requirements

(1) Revenue is adjusted to add back acquisition accounting fair value

adjustments of deferred revenue

(2) See Adjusted EBITDA reconciliation on slide 19

22

|

|

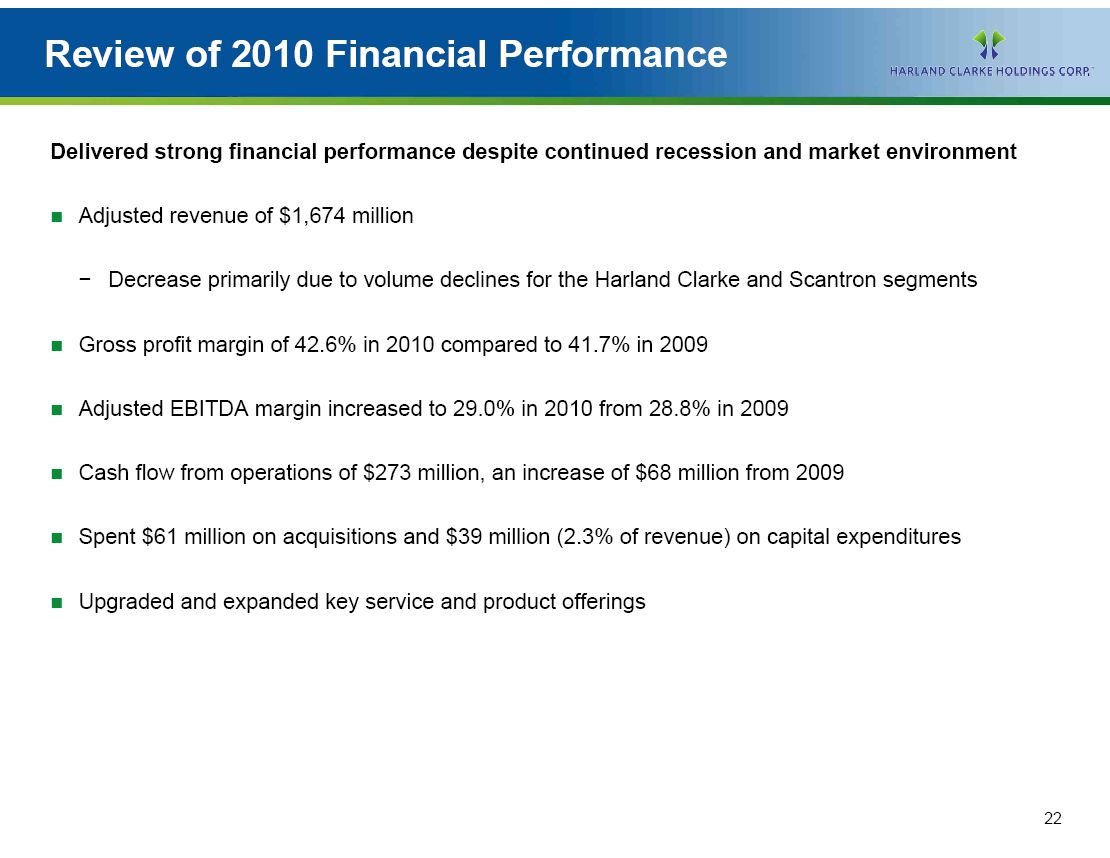

Review of 2010 Financial Performance

Delivered strong financial performance despite continued recession and market

environment

[] Adjusted revenue of $1,674 million

[] Decrease primarily due to volume declines for the Harland Clarke and

Scantron segments

[] Gross profit margin of 42.6% in 2010 compared to 41.7% in 2009

[] Adjusted EBITDA margin increased to 29.0% in 2010 from 28.8% in 2009

[] Cash flow from operations of $273 million, an increase of $68 million from

2009

[] Spent $61 million on acquisitions and $39 million (2.3% of revenue) on

capital expenditures

[] Upgraded and expanded key service and product offerings

23

|

|

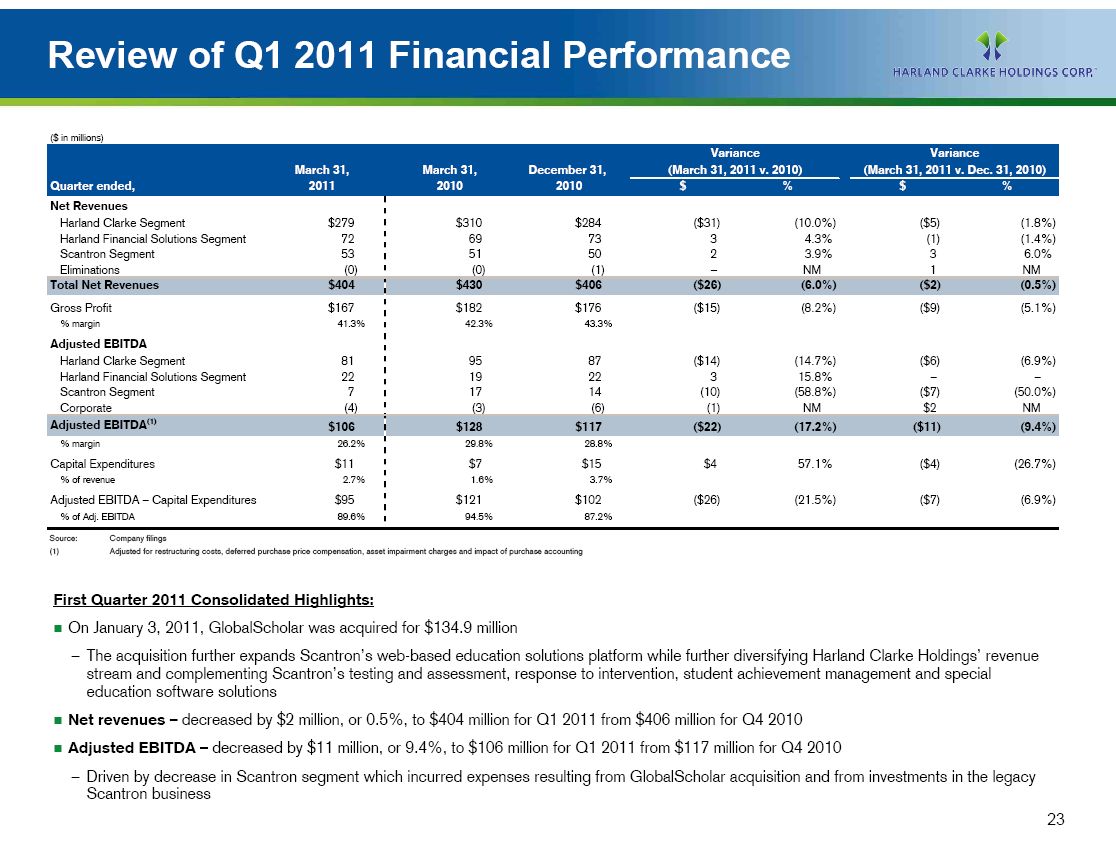

Review of Q1 2011 Financial Performance

Variance Variance

(March 31, 2011 v.

March 31, March 31, December 31, (March 31, 2011 v. 2010) Dec. 31, 2010)

Quarter ended, 2011 2010 2010 $ % $ %

Net Revenues

Harland Clarke Segment $279 $310 $284 ($31) (10.0%) ($5) (1.8%)

Harland Financial

Solutions Segment 72 69 73 3 4.3% (1) (1.4%)

Scantron Segment 53 51 50 2 3.9% 3 6.0%

Eliminations (0) (0) (1) -- NM 1 NM

Total Net Revenues $404 $430 $406 ($26) (6.0%) ($2) (0.5%)

Gross Profit $167 $182 $176 ($15) (8.2%) ($9) (5.1%)

% margin 41.3% 42.3% 43.3%

Adjusted EBITDA

Harland Clarke Segment 81 95 87 ($14) (14.7%) ($6) (6.9%)

Harland Financial

Solutions Segment 22 19 22 3 15.8% -- --

Scantron Segment 7 17 14 (10) (58.8%) ($7) (50.0%)

Corporate (4) (3) (6) (1) NM $2 NM

Adjusted EBITDA (1)

$106 $128 $117 ($22) (17.2%) ($11) (9.4%)

% margin 26.2% 29.8% 28.8%

Capital Expenditures $11 $7 $15 $4 57.1% ($4) (26.7%)

% of revenue 2.7% 1.6% 3.7%

Adjusted EBITDA -- Capital Expenditures $95 $121 $102 ($26) (21.5%) ($7)

(6.9%) % of Adj. EBITDA 89.6% 94.5% 87.2%

Source: Company filings

(1) Adjusted for restructuring costs, deferred purchase price compensation,

asset impairment charges and impact of purchase accounting

First Quarter 2011 Consolidated Highlights:

[] On January 3, 2011, GlobalScholar was acquired for $134.9 million

[] The acquisition further expands Scantron's web-based education solutions

platform while diversifying Harland Clarke's revenue stream and complementing

Scantron's testing and assessment, response to intervention, student

achievement management and special education software solutions

[] Net revenues -- decreased by $2 million, or 0.5%, to $404 million for Q1 2011

from $406 million for Q4 2010

[] Adjusted EBITDA -- decreased by $11 million, or 9.4%, to $106 million for Q1

2011 from $117 million for Q4 2010

[] Driven by decrease in Scantron segment which incurred expenses resulting

from GlobalScholar acquisition and from investments in the legacy

Scantron business

24

|

|

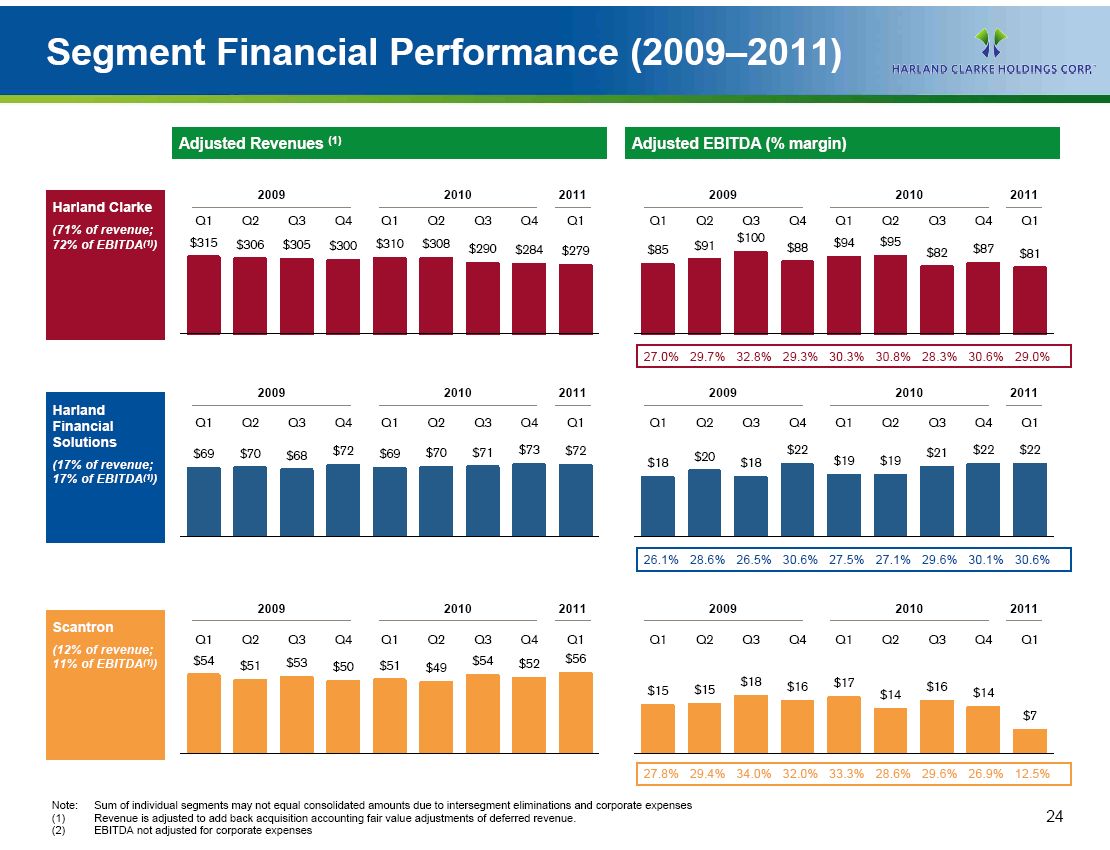

Segment Financial Performance (2009--2011)

(1)

Adjusted Revenues

Harland Clarke

(71% of revenue;

(1)

72% of EBITDA )

[GRAPHIC OMITTED]

Harland Financial Solutions

(17% of revenue;

(1)

17% of EBITDA )

[GRAPHIC OMITTED]

Scantron

(12% of revenue;

(1)

11% of EBITDA )

[GRAPHIC OMITTED]

Adjusted EBITDA (% margin)

[GRAPHIC OMITTED]

[GRAPHIC OMITTED]

[GRAPHIC OMITTED]

Note: Sum of individual segments may not equal consolidated amounts due to

intersegment eliminations and corporate expenses

(1) Revenue is adjusted to add back acquisition accounting fair value

adjustments of deferred revenue.

(2) EBITDA not adjusted for corporate expenses

25

|

|

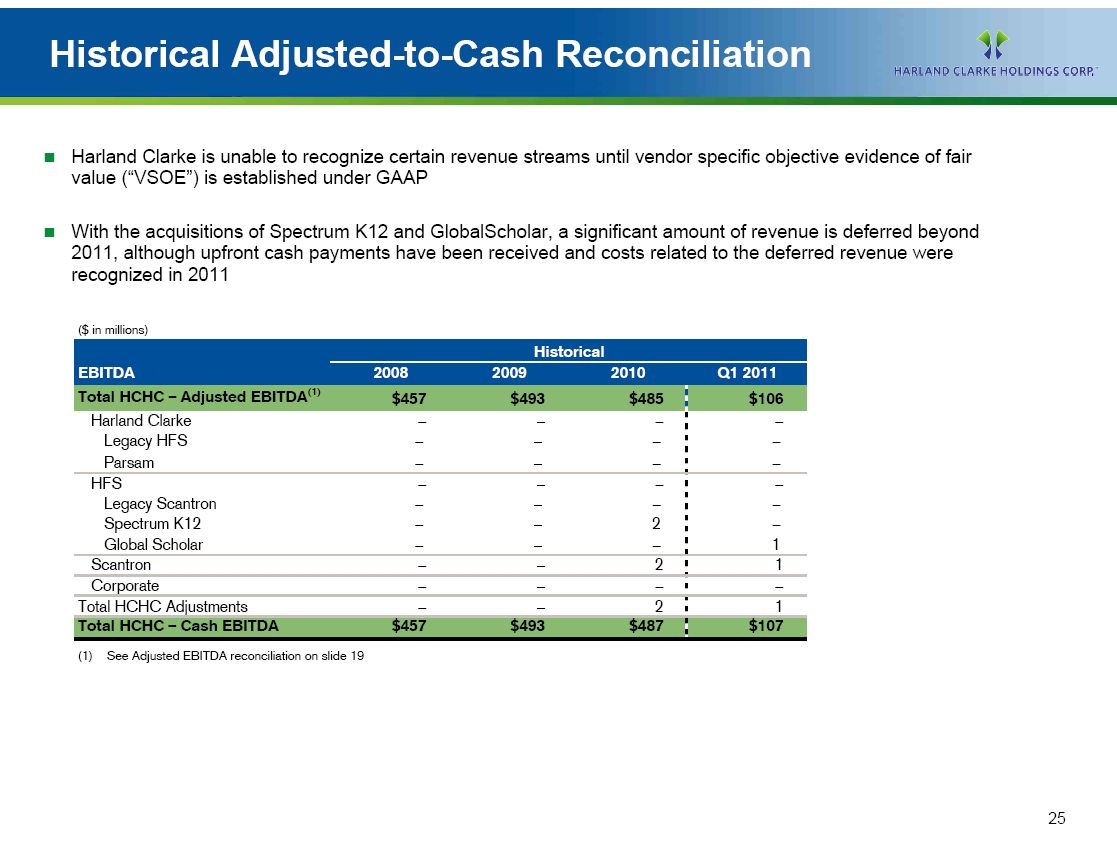

Historical Adjusted-to-Cash Reconciliation

[]

Harland Clarke is unable to recognize certain revenue streams until vendor

specific objective evidence of fair

value ("VSOE") is established under GAAP

[]

With the acquisitions of Spectrum K12 and GlobalScholar, a significant amount

of revenue is deferred beyond 2011, although upfront cash payments have been

received and costs related to the deferred revenue were recognized in 2011

($ in millions)

Historical

EBITDA 2008 2009 2010 Q1 2011

============================= === ========== ================== ========== =============

(1

Total HCHC -- Adjusted EBITDA

$457 $493 $485 $106

Harland Clarke -- -- -- --

Legacy HFS -- -- -- --

Parsam -- -- -- --

============================= === ========== ================== ========== =============

HFS -- -- -- -

Legacy Scantron -- -- -- --

Spectrum K12 -- -- 2 1

Global Scholar -- -- -- 1

============================= === ========== ================== ========== =============

Scantron -- -- 2

============================= === ========== ================== ========== =============

Corporate -- -- -- -

============================= === ========== ================== ========== =============

Total HCHC Adjustments -- -- 2 1

============================= === ========== ================== ========== =============

Total HCHC -- Cash EBITDA $457 $493 $487 $107

(1) See Adjusted EBITDA reconciliation on slide 19

26

|

|

IV. Transaction Terms and Timing

Credit Suisse

27

|

|

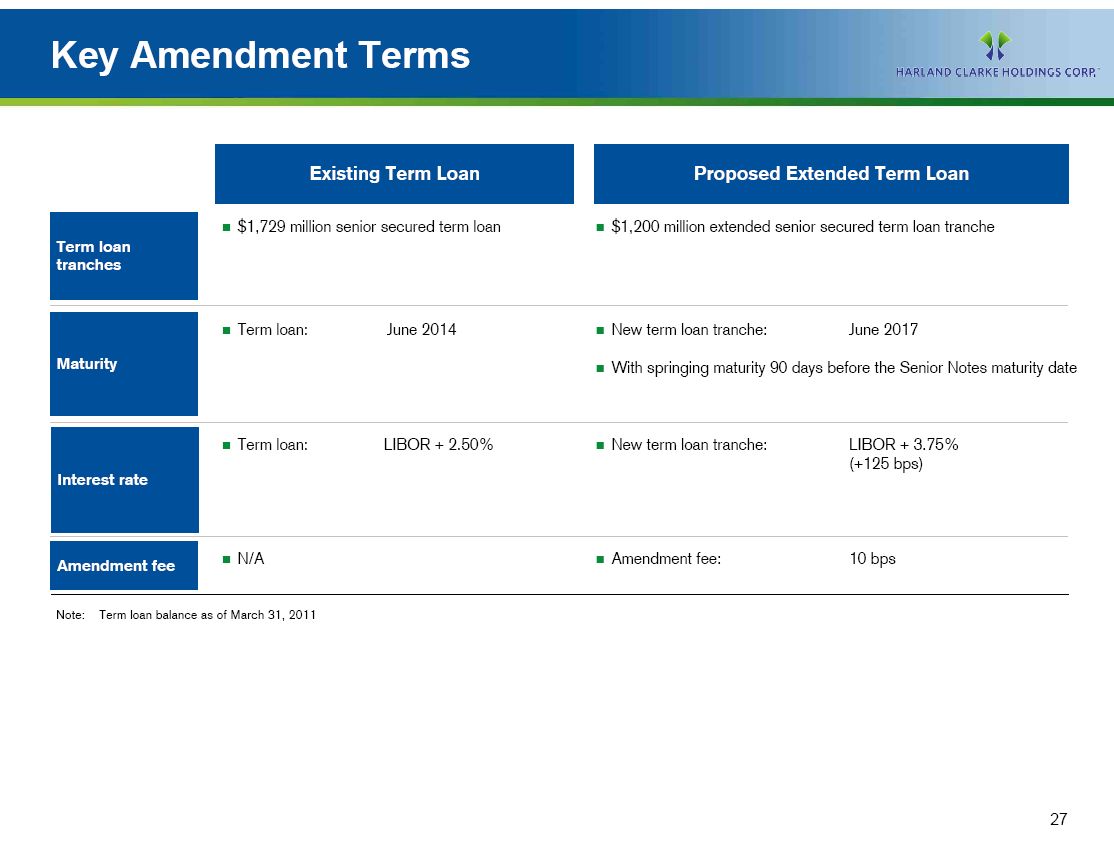

Key Amendment Terms

Existing Term Loan Proposed Extended Term Loan

------------- ------------- ---------------------------- ------------------------------------------------------------------------

[] []

$1,729 million senior secured term loan $1,200 million extended senior secured term loan tranche

Term loan

tranches

============= ------------- ---------------------------- ------------------------- ----------------------------------------------

[] []

Term loan: June 2014 New term loan tranche: June 2017

Maturity []

With springing maturity 90 days before the Senior Notes maturity date

============= ------------- ---------------------------- ------------------------------------------------------------------------

[] []

Term loan: LIBOR + 2.50% New term loan tranche: LIBOR + 3.75%

(+125 bps)

Interest rate

============= ------------- ---------------------------- ------------------------- ----------------------------------------------

[] []

N/A Amendment fee: 10 bps

Amendment fee

Note: Term loan balance as of March 31, 2011

28

|

|

Key Amendment Terms (cont'd)

Proposed Amendment

to Existing Credit Facilities

Other terms

[] Add incremental term loan capacity to be used to repay the non-extended term

loan, subject to 50 bps MFN

[] Provide the ability to complete revolver extensions in the future

[] Provide the ability to incur 2nd Lien Debt or Unsecured Debt so long as

proceeds are used to repay term loans

[] Refresh the $25mm general restricted payments basket

[] Increase the annual restricted payments basket from $20mm to $25mm

[] Permit an EBITDA add-back for earnings deferred as a result of the Vendor

Specific Objective Evidence ("VSOE") method for revenue recognition. Revenue

for multi-element contracts at Scantron due to Spectrum K12 and GlobalScholar

operations are deferred until VSOE is established. The proposed add-back will

modify the credit agreement definition of EBITDA to reflect Cash EBITDA amounts

for Scantron versus GAAP EBITDA

[] Modify the definition of Similar Businesses (for purposes of investments and

acquisitions) to reflect the current diversification of the Company's business lines

[] Allow for borrower debt buybacks through tender offers to prepay, subject to

customary restrictions including, but not limited to: [] All loans prepaid are

immediately cancelled [] The revolver is undrawn at the time of the buyback

29

|

|

Summary Amendment Timetable

[GRAPHIC OMITTED]

Date Event

May 12th Announce transaction

May 13th Lenders' Call

May 13th Distribute amendment documentation

May 20th Deadline for consents

May 27th Amendment becomes effective

30

|

|

Transaction Contacts

Title Phone E-mail

Harland Clarke

Peter Fera Executive Vice President and Chief Financial Officer (210) 697-1208 peter.fera@harlandclarke.com

Martin Wexler Vice President and Treasurer (210) 697-6251 martin.wexler@harlandclarke.com

Credit Suisse

David Miller Managing Director, (212) 538-7443 david.miller@credit-suisse.com

Co-Head of U.S. Leveraged Finance Capital Markets

Co Head of U.S. Syndicated Loan Group

Carly Baxter Director, (212) 538-3933 carly.baxter@credit-suisse.com

Syndicated Loan Group

Robert Hetu Managing Director, (212) 325-4542 robert.hetu@credit-suisse.com

Corporate Banking

Michael Spaight Associate, (212) 325-7039 michael.spaight@credit-suisse.com

Corporate Banking

31

|

|

Conclusion

32

|

|

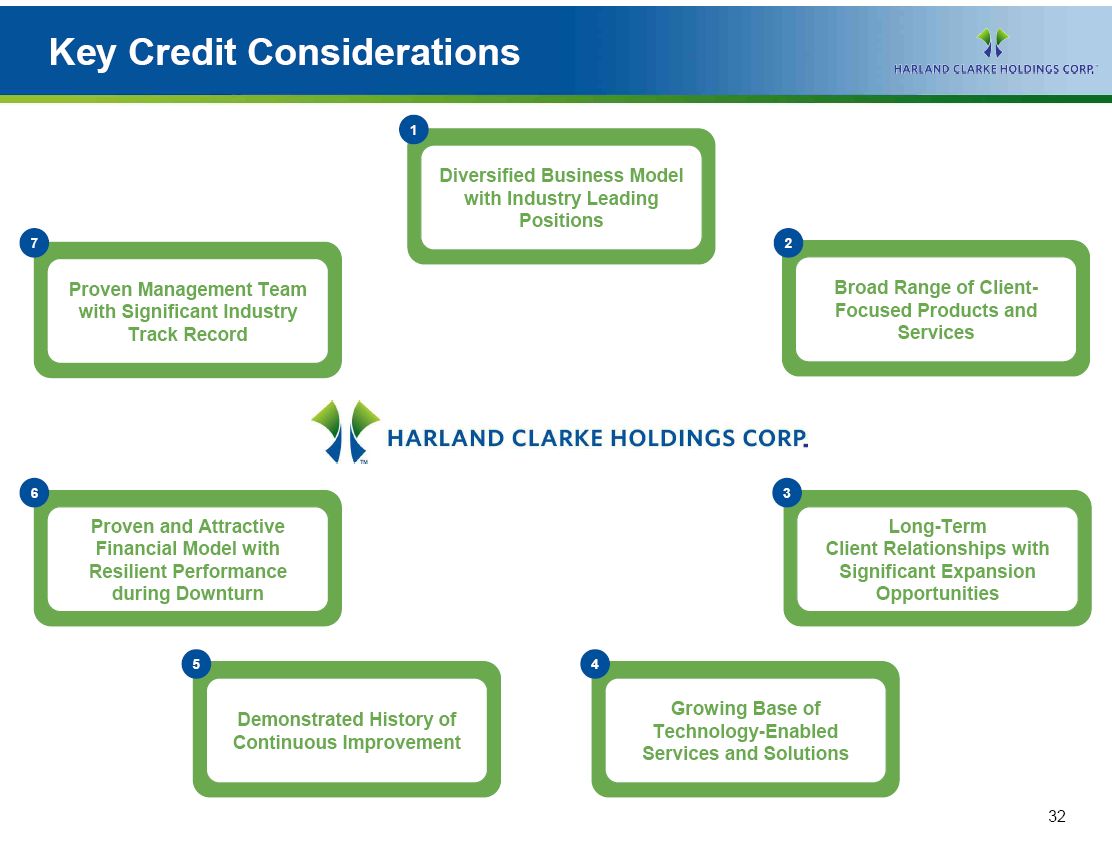

Key Credit Considerations

Diversified Business Model with Industry Leading Positions

Broad Range of Client-Focused Products and Services

Long-Term Client Relationships with Significant Expansion

Opportunities

Growing Base of Technology-Enabled Services and Solutions

Demonstrated History of

Continuous Improvement

Proven and Attractive Financial Model with Resilient Performance during

Downturn

Proven Management Team with Significant Industry Track Record

33

|

|

Public Q and A

34

|

|

Appendix

35

|

|

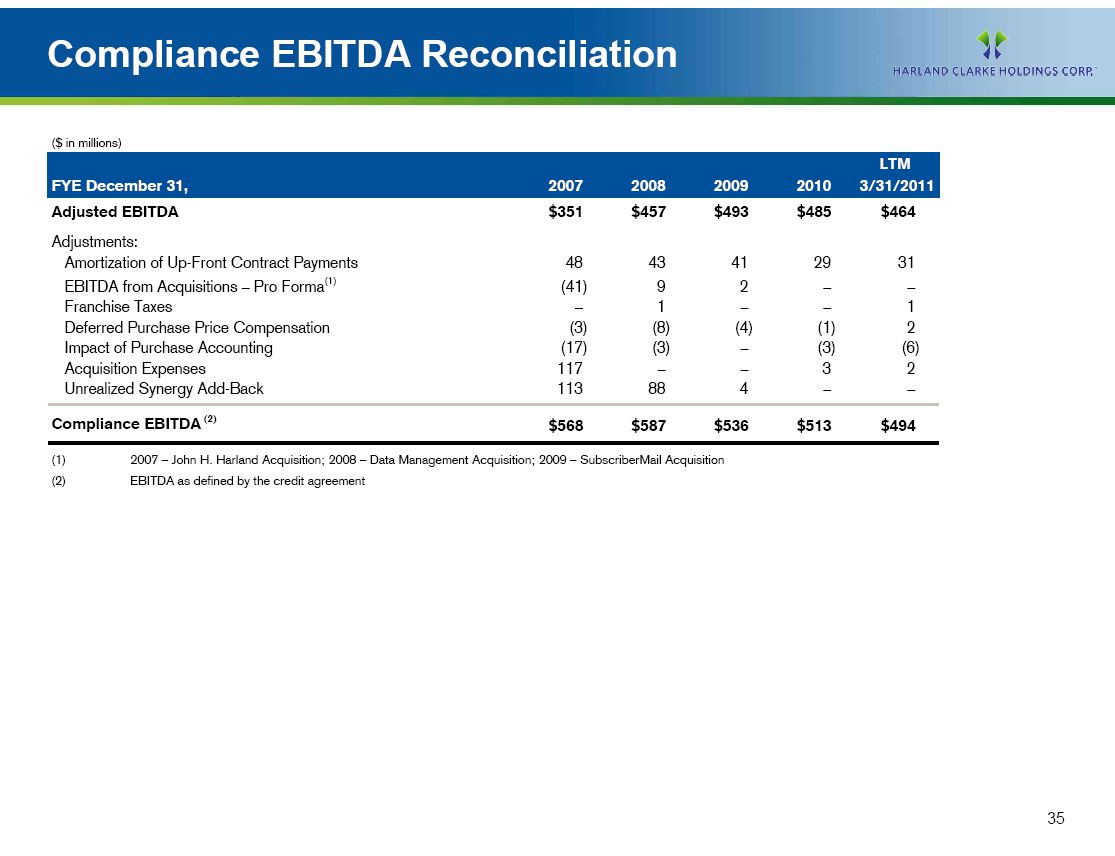

Compliance EBITDA Reconciliation

($ in millions)

========================================================= ======= ======= ======= ======= ===========

LT

FYE December 31, 2007 2008 2009 2010 3/31/2011

========================================================= ======= ======= ======= ======= ===========

Adjusted EBITDA $351 $457 $493 $485 $46

Adjustments:

Amortization of Up-Front Contract Payments (1) 48 43 41 29 31

EBITDA from Acquisitions -- Pro Forma (41) 9 2 -- --

Franchise Taxes -- 1 -- -- 1

Deferred Purchase Price Compensation (3) (8) (4) (1) 2

Impact of Purchase Accounting (17) (3) -- (3) (6)

Acquisition Expenses 117 -- -- 3 2

Unrealized Synergy Add-Back 113 88 4 -- --

========================================================= ======= ======= ======= ======= ===========

Compliance EBITDA (2) $568 $587 $536 $513 $494

(1) 2007 -- John H. Harland Acquisition; 2008 -- Data Management Acquisition;

2009 -- SubscriberMail Acquisition

(2) EBITDA as defined by the credit agreement

36

|

|

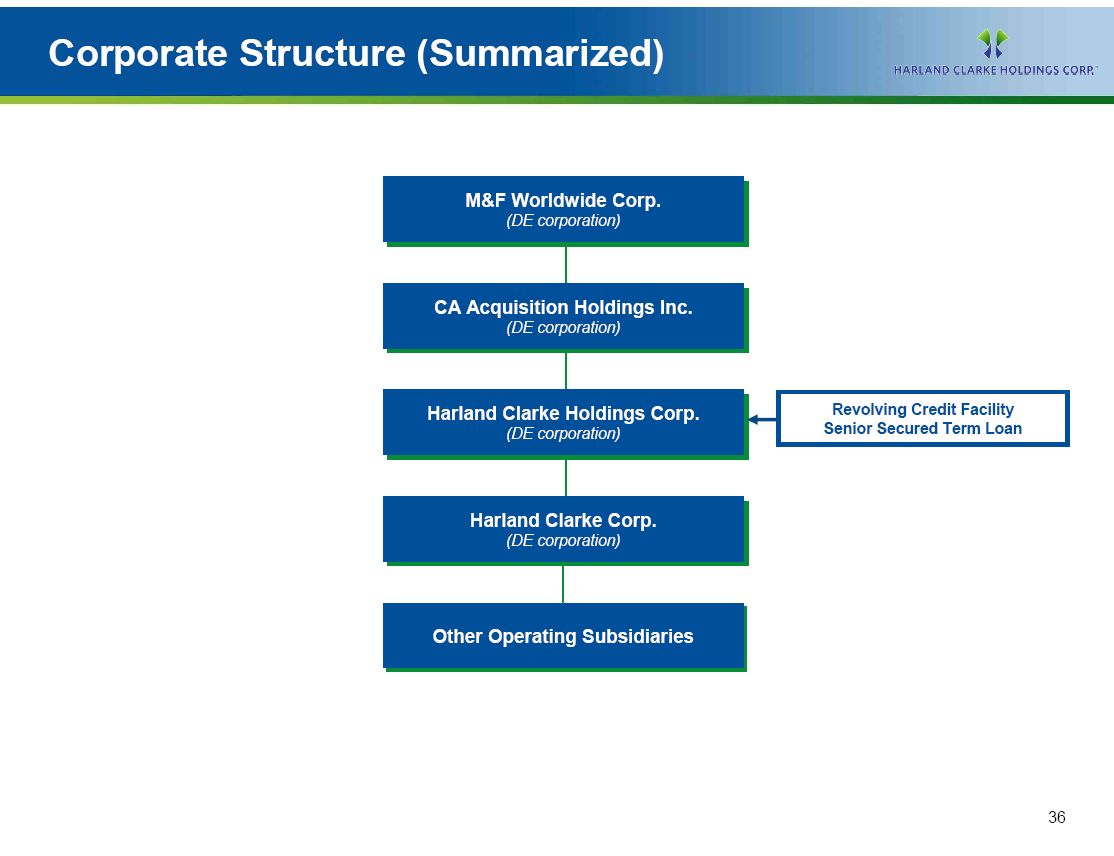

Corporate Structure (Summarized)

M and F Worldwide Corp.

(DE corporation)

CA Acquisition Holdings Inc.

(DE corporation)

Harland Clarke Holdings Corp.

(DE corporation)

Revolving Credit Facility

Senior Secured Term Loan

Harland Clarke Corp.

(DE corporation)

Other Operating Subsidiaries

37

|

|

[HARLAND CLARKE HOLDINGS CORP.]

|