Risks Relating to our Business

In order to comply with PRC regulatory requirements, we operate our businesses through companies with which we have contractual relationships but in which we do not have controlling ownership. If the PRC government determines that our agreements with these companies are not in compliance with applicable regulations, our business in the PRC could be materially adversely affected.

We do not have direct or indirect equity ownership of HBOP which operates our main business in China. At the same time, however, we have entered into contractual arrangements with HBOP and its individual owners pursuant to which we received an economic interest in, and exert a controlling influence over HBOP, in a manner substantially similar to a controlling equity interest.

Although we believe the restructuring transaction and our current business operations are in compliance with the current laws in China, we cannot be sure that the PRC government would view our operating arrangements to be in compliance with PRC regulations that may be adopted in the future. If we are determined not to be in compliance, the PRC government could levy fines, revoke our business and operating licenses, require us to discontinue or restrict our operations, restrict our right to collect revenues, require us to restructure our business, corporate structure or operations, impose additional conditions or requirements with which we may not be able to comply, impose restrictions on our business operations or on our customers, or take other regulatory or enforcement actions against us that could be harmful to our business. As a result, our business in the PRC could be materially adversely affected.

We rely on contractual arrangements with HBOP for our operations, which may not be as effective in providing control over these entities as direct ownership.

Our operations and financial results are dependent on HBOP in which we have no equity ownership interest and must rely on contractual arrangements to control and operate the businesses of HBOP. These contractual arrangements are not as effective in providing control over HBOP as direct ownership. For example, HBOP may be unwilling or unable to perform their contractual obligations under our commercial agreements, including payment of consulting fees under the Exclusive Technical Service and Business Consulting Agreement as they become due. Consequently, we will not be able to conduct our operations in the manner currently planned. In addition, HBOP may seek to renew their agreements on terms that are disadvantageous to us. Although we have entered into a series of agreements that provide us with substantial ability to control HBOP, we may not succeed in enforcing our rights under them insofar as our contractual rights and legal remedies under Chinese law are inadequate. In addition, if we are unable to renew these agreements on favorable terms when these agreements expire, or to enter into similar agreements with other parties, our business may not be able to operate or expand, and our operating expenses may significantly increase.

The shareholders of HBOP may have potential conflicts of interests with us, which may adversely affect our business.

We operate our businesses in China though HBOP. Our chairman, CEO and 27.89% shareholder, Zhenyong Liu owns 93.26% of the equity interest in HBOP. Conflicts of interests between his duties to us and to HBOP may arise. We cannot assure you that when conflicts of interest arise, he will act in the best interests of our company or that any conflict of interest will be resolved in our favor. These conflicts may result in management decisions that could negatively affect our operations and potentially result in the loss of opportunities.

Our arrangements with HBOP and its shareholders may be subject to a transfer pricing adjustment by the PRC tax authorities which could have an adverse effect on our income and expenses.

We could face material and adverse tax consequences if the PRC tax authorities determine that our contracts with HBOP and its shareholders were not entered into based on arm’s length negotiations. Although our contractual arrangements are similar to other companies conducting similar operations in China, if the PRC tax authorities determine that these contracts were not entered into on an arm’s length basis, they may adjust our income and expenses for PRC tax purposes in the form of a transfer pricing adjustment. Such an adjustment may require that we pay additional PRC taxes plus applicable penalties and interest, if any.

The exercise of our option to purchase part or all of the equity interests in HBOP under the Call Option Agreement might be subject to approval by the PRC government. Our failure to obtain this approval may impair our ability to substantially control HBOP and could result in actions by HBOP that conflict with our interests.

Our Call Option Agreement with HBOP and its shareholders gives our Chinese subsidiary, Baoding Shengde or its designated entity or natural person, the option to purchase all or part of the equity interests in HBOP. The option may not be exercised by Baoding Shengde if the exercise would violate any applicable laws and regulations in China or cause any license or permit held by, and necessary for the operation of HBOP, to be cancelled or invalidated. Under the laws of China, if a foreign entity, through a foreign investment company that it invests in, acquires a domestic related company, China’s regulations regarding mergers and acquisitions may technically apply to the transaction. If these regulations apply, an examination and approval of the transaction by China’s Ministry of Commerce (“MOFCOM”), or its local counterparts would be required. In addition, an appraisal of the equity interest or the assets to be acquired would also be mandatory. Since the scope of business activities (making of digital photo paper and other cultural paper products) as defined in the business license of Baoding Shengde does not involve the MOFCOM approval and monitoring, we do not believe at this time that an approval or an appraisal is required for Baoding Shengde to exercise its option to acquire HBOP. In light of the different views on this issue, however, it is possible that the central MOFCOM office in Beijing will issue a standardized opinion imposing the approval and appraisal requirement. If we are not able to purchase the equity of HBOP, then we will lose a substantial portion of our ability to control HBOP and our ability to ensure that HBOP will act in our interests.

Our operating history may not serve as an adequate basis to judge our future prospects and results of operations.

HBOP commenced its current line of business operations in 1996 and received its initial Pollution Discharge Permit in September 1996, which must be renewed every year for HBOP to stay in business. Although we have never had problem renewing the Pollution Discharge Permit, we cannot guarantee automatic renewal every year. Our operating history may not provide a meaningful basis on which to evaluate its business. We cannot assure you that HBOP will maintain its profitability or that we will not incur net losses in the future. We expect that HBOP’s operating expenses will increase as it expands. Any significant failure to realize anticipated revenue growth could result in significant operating losses. We will continue to encounter risks and difficulties frequently experienced by companies at a similar stage of development, including our potential failure to:

| | • | raise adequate capital for expansion and operations; |

| | • | implement our business model and strategy and adapt and modify them as needed; |

| | • | increase awareness of our brand name, protect our reputation and develop customer loyalty; |

| | • | manage our expanding operations and service offerings, including the integration of any future acquisitions; |

| | • | maintain adequate control of our expenses; or |

| | • | anticipate and adapt to changing conditions in paper markets in which we operate as well as the impact of any changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. |

If we are not successful in addressing any or all of these risks, our business may be materially and adversely affected.

HBOP’s failure to compete effectively may adversely affect our ability to generate revenue.

Through HBOP, we compete in a highly developed market with companies that have significantly greater experience and history in our industry. If we do not compete effectively, we could lose market share and experience falling prices, adversely affecting our financial results. Our competitors will expand in the key markets and implement new technologies making them more competitive. There is also the possibility that competitors will be able to offer additional products, services, lower prices, or other incentives that we cannot or will not offer or that will make our products less profitable. We cannot assure you that we will be able to compete effectively with current or future competitors or that the competitive pressures we face will not harm our business.

Baoding Shengde does not have any operating history and has never competed in the digital photo paper market.

We conduct the digital photo paper business through our wholly-owned subsidiary Baoding Shengde, which has never had any experience competing in the Chinese digital photo paper market. Although we reasonably believe that we are able to compete effectively with our high quality digital photo paper products, Baoding Shengde has no industry experience in the past.

If HBOP fails to comply with covenants in its loan agreements, its lenders may allege a breach of a covenant and seek to accelerate the loan or exercise other remedies, which could strain our cash flow and harm our business, liquidity and financial condition.

HBOP received loans from commercial banks to fund its operations. Typically, these loans are made pursuant to customary loan agreements which contain representations and warranties about its business, financial covenants to which HBOP must adhere and other negative covenants in respect of its operations. Under some of these agreements, HBOP may be required to obtain the consent of its lenders prior to entering into its contractual arrangement with us but HBOP did not receive such prior consent. To date, our lenders have not given us any notice of default or otherwise objected to our contractual arrangements with HBOP. We intend to secure a waiver from our lenders in this regard, but cannot assure you that we will successfully do so. If we cannot obtain such a wavier and HBOP’s lenders declare it to be in default under the loan agreements, they may accelerate HBOP’s indebtedness to them which would negatively affect our cash flows and business operations.

We may not be able to effectively control and manage the growth of HBOP.

If HBOP’s business and markets grow and develop, it will be necessary for us to finance and manage expansion in an orderly fashion. An expansion would increase demands on existing management, workforce and facilities. Failure to satisfy such increased demands could interrupt or adversely affect our operations and cause delay in production and delivery of our paper products, as well as administrative inefficiencies.

We, through our subsidiaries, may engage in future acquisitions that could dilute the ownership interests of our stockholders and cause us to incur debt and assume contingent liabilities.

We, through our subsidiaries, may review acquisition and strategic investment prospects that we believe would complement the current product offerings of HBOP, augment its market coverage or enhance its technical capabilities, or otherwise offer growth opportunities. From time to time we review investments in new businesses and we, through our subsidiaries, expect to make investments in, and to acquire, businesses, products, or technologies in the future. We expect that when we raise funds from investors for any of these purposes we will be either the issuer or the primary obligor while the proceeds will be forwarded to HBOP. In the event of any future acquisitions, we could:

| | • | issue equity securities which would dilute current stockholders’ percentage ownership; |

| | • | assume contingent liabilities; or |

| | • | expend significant cash. |

These actions could have a material adverse effect on our operating results or the price of our common stock. Moreover, even if through our subsidiaries, we do obtain benefits in the form of increased sales and earnings, there may be a lag between the time when the expenses associated with an acquisition are incurred and the time when we recognize such benefits. Acquisitions and investment activities also entail numerous risks, including:

| | • | difficulties in the assimilation of acquired operations, technologies and/or products; |

| | • | unanticipated costs associated with the acquisition or investment transaction; |

| | • | the diversion of management’s attention from other business concerns; |

| | • | adverse effects on existing business relationships with suppliers and customers; |

| | • | risks associated with entering markets in which HBOP has no or limited prior experience; |

| | • | the potential loss of key employees of acquired organizations; and |

| | • | substantial charges for the amortization of certain purchased intangible assets, deferred stock compensation or similar items. |

We cannot ensure that we will be able to successfully integrate any businesses, products, technology, or personnel that we might acquire in the future and our failure to do so could have a material adverse effect on our and/or HBOP’s business, operating results and financial condition.

We are responsible for the indemnification of our officers and directors.

Our Articles of Incorporation provides for the indemnification and/or exculpation of our directors, officers, employees, agents and other entities which deal with us to the maximum extent provided, and under the terms provided, by the laws and decisions of the courts of the state of Nevada. Although we do maintain professional error and omission insurance for the officers and directors, due to limitations of the insurance coverage these indemnification provisions could still result in substantial expenditures which we may be unable to recoup through the insurance and could adversely affect our business and financial conditions. Zhenyong Liu, our Chairman of the Board and Chief Executive Officer, Winston C. Yen, our Chief Financial Officer, Dahong Zhou, our Secretary, and Drew Bernstein, Wenbing Christopher Wang, Zhaofang Wang, and Fuzeng Liu, our directors, are key personnel with rights to indemnification under our Articles of Incorporation.

We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations.

Our success is, to a certain extent, attributable to the management, sales and marketing, and paper factory operational expertise of key personnel. Zhenyong Liu, our Chief Executive Officer and Chairman of the Board, Winston C. Yen, our Chief Financial Officer, Dahong Zhou, our Secretary, and Zhongmin Ma, HBOP’s General Engineer, Gengqi Yang, HBOP’s Vice President of Sales and Marketing, Fulai Huang, HBOP’s Vice President of Environmental Protection and Xiaodong Liu, Baoding Shengde’s General Manager, perform key functions in the operation of our business. There can be no assurance that Orient Paper or HBOP or Baoding Shengde will be able to retain these officers after the term of their employment contracts expire. The loss of these officers could have a material adverse effect upon our business, financial condition, and results of operations. We do not carry key man life insurance for any of our key personnel or personnel nor do we foresee purchasing such insurance to protect against a loss of key personnel and the key personnel.

We are dependent upon the services of Mr. Zhenyong Liu for the continued growth and operation of our company because of his experience in the industry and his personal and business contacts in the PRC. Although Mr. Liu has entered into an employment agreement with Baoding Shengde Paper Co., Ltd., our wholly owned subsidiary and a PRC company, and that we have no reason to believe that Mr. Liu will discontinue his services with us or HBOP, the interruption or loss of his services would adversely affect our ability to effectively run our business and pursue our business strategy as well as our results of operations.

We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire these personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected.

We must attract, recruit and retain a sizeable workforce of technically competent employees. Competition for senior management and senior personnel in the PRC is intense, the pool of qualified candidates in the PRC is very limited, and we may not be able to retain the services of our senior executives or senior personnel, or attract and retain high-quality senior executives or senior personnel in the future. This failure could materially and adversely affect our future growth and financial condition.

Our operating results may fluctuate as a result of factors beyond our control.

Our operating results may fluctuate significantly in the future as a result of a variety of factors, many of which are beyond our control. These factors include:

| | • | the costs of paper products and development; |

| | • | the relative speed and success with which we can obtain and maintain customers, merchants and vendors for our products; |

| | • | capital expenditure for equipment; |

| | • | marketing and promotional activities and other costs; |

| | • | changes in our pricing policies, suppliers and competitors; |

| | • | the ability of our suppliers to provide products in a timely manner to their customers; |

| | • | changes in operating expenses; |

| | • | increased competition in the paper markets; and |

| | • | other general economic and seasonal factors. |

We face risks related to product liability claims.

We presently do not maintain product liability insurance. We face the risk of loss because of adverse publicity associated with product liability lawsuits, whether or not such claims are valid. We may not be able to avoid such claims. Although product liability lawsuits in the PRC are rare, and we have not, to date, experienced significant failure of our products, there is no guarantee that we will not face such liability in the future. This liability could be substantial and the occurrence of such loss or liability may have a material adverse effect on our business, financial condition and prospects.

Our operating results also depend on the availability and pricing of energy and raw materials.

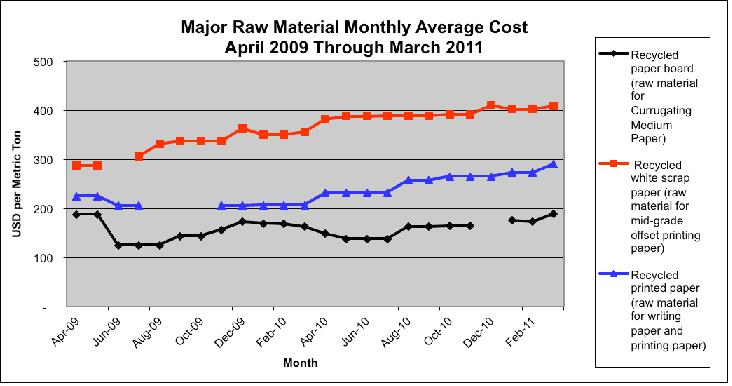

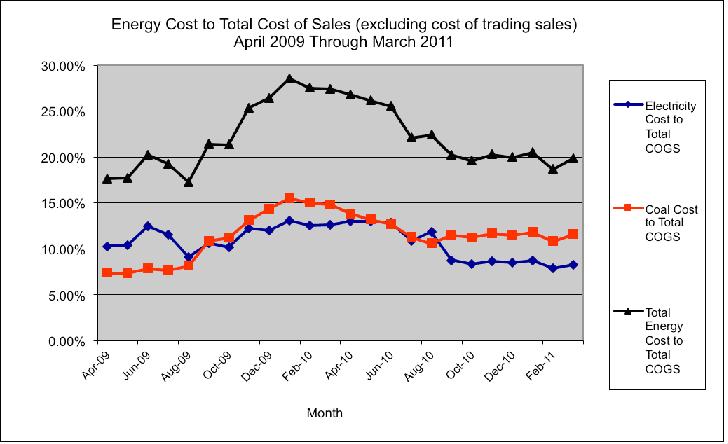

In addition to our dependence upon wood pulp, recycled white scrap paper and paperboard costs, our operating results depend on the availability and pricing of energy and other raw materials, including chemical agents and coal. An interruption in the supply of supplemental chemical agents could cause a material disruption at our mill in Baoding. In addition, an interruption in the supply of coal could cause a material disruption at our facilities in Baoding. At present, our raw materials including coal are purchased from a number of suppliers, of which the three largest suppliers account for over 72% of all purchases. If any of these contracts were to be terminated for any reason, or not renewed upon expiration, or if market conditions were to substantially change creating a significant increase in the price of coal and recycled paper, we may not be able to find alternative, comparable suppliers or suppliers capable of providing coal to us on terms or in amounts satisfactory to us. As a result of any of these events, our business, financial condition and operating results could suffer.

A material disruption at one of our manufacturing facilities could prevent us from meeting customer demand, reduce our sales, and/or negatively affect our net income.

Any of our manufacturing facilities, or any of our machines within an otherwise operational facility, could cease operations unexpectedly due to a number of events, including:

| | • | prolonged power failures; |

| | • | disruption in the supply of raw materials, such as wood fiber, energy, or chemicals; |

| | • | a chemical spill or release; |

| | • | closure because of environmental-related concerns; |

| | • | the effect of a drought or reduced rainfall on our water supply; |

| | • | disruptions in the transportation infrastructure, including roads, bridges, railroad tracks, and tunnels; |

| | • | fires, floods, earthquakes, hurricanes, or other catastrophes; |

| | • | terrorism or threats of terrorism; |

| | • | other operational problems. |

We have purchased property base insurance from Property Insurance and Casualty Company Limited, valid from March 2011 through March 2012. However, if any of the abovementioned events were to occur, we may be unable to meet customer demand, which may adversely affect our sales and net income.

Our certificates, permits, and licenses related to our papermaking operations are subject to governmental control and renewal and failure to obtain renewal will cause all or part of our operations to be terminated.

Due to the nature of the business, we are subject to environmental, health, and safety laws and regulations, including those related to the disposal of hazardous waste from our manufacturing processes. Compliance with existing and future environmental, health and safety laws could subject us to future costs or liabilities; impact our production capabilities; constrict our ability to sell, expand or acquire facilities; and generally impact our financial performance. Under the original factory land lease dated January 2, 2002, HBOP was obligated to return the land to the government to its original condition prior to the expiration of the lease. As such, Orient Paper would have to accrue the cost estimated to return the land to its prior condition over the 30-year life of the lease. However, on March 15, 2010, an amendment to the original January 2, 2002 lease was signed and removed the obligation of HBOP to return the land to its condition prior to the expiration of the lease. The management of the Company thus believes that no liabilities under the lease should be accrued as of December 31, 2010. Nevertheless, because of the uncertainties associated with environmental assessment and remediation activities, future expense to remediate any sites, which could be identified in the future for cleanup, could be higher than expected.

In 1988, the National Environmental Protection Bureau issued Interim Measures on the Administration of Water Pollutants Discharge Permits, requiring all companies discharging pollution into the water as a direct or indirect byproduct of production to adhere to certain caps on pollution discharge. Additionally, such companies were required to obtain and annually renew a Pollution Discharge Permit in order to conduct their operations. The PRC government has the authority to shut down a company’s operations for failure to maintain a valid permit. We renewed our Pollution Discharge Permit on March 12, 2010. Our latest permit is effective from March 12, 2010 through March 11, 2011. An application to renew has been filed with the local environment protection agency and the new license is expected to be issued shortly after March 11, 2011.

If we are unable to make necessary capital investments or respond to pricing pressures, our business may be harmed.

In order to remain competitive, we need to invest in research and development, manufacturing, customer service and support, and marketing. From time to time we also have to adjust the prices of our products to remain competitive. We may not have available sufficient financial or other resources to continue to make investments necessary to maintain our competitive position.

If we fail to introduce enhancements to our existing products or to develop new products, our business and results of operations could be adversely affected.

We believe our future success depends in part on our ability to enhance our existing products and develop new products in order to continue to meet customer demands. Our failure to introduce new or enhanced products on a timely and cost-competitive basis, or the development of processes that make our existing products obsolete, could harm our business and results of operations.

Risks Related To Doing Business in the PRC

Changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the PRC and the profitability of such business.

Our business operations may be adversely affected by the current and future political environment in the PRC. The PRC has operated as a socialist state since the middle of the 20th century and is controlled by the Communist Party of China. The Chinese government exerts substantial influence and control over the manner in which we must conduct our business activities. The PRC has only permitted provincial and local economic autonomy and private economic activities since 1978. The government of the PRC has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy, including the paper industry, through regulation and state ownership. Our ability to operate in the PRC may be adversely affected by changes in Chinese laws and regulations, including those relating to taxation, import and export tariffs, raw materials, environmental regulations, land use rights, property and other matters. Under its current leadership, the government of the PRC has been pursuing economic reform policies that encourage private economic activity and greater economic decentralization. There is no assurance, however, that the government of the PRC will continue to pursue these policies, or that it will not significantly alter these policies from time to time without notice.

The PRC’s economy is in a transition from a planned economy to a market oriented economy subject to five-year and annual plans adopted by the government that set national economic development goals. Policies of the PRC government can have significant effects on the economic conditions of the PRC. The PRC government has confirmed that economic development will follow the model of a market economy. Under this direction, we believe that the PRC will continue to strengthen its economic and trading relationships with foreign countries and business development in the PRC will follow market forces. While we believe that this trend will continue, there can be no assurance that this will be the case.

A change in policies by the PRC government could adversely affect our interests by, among other factors: changes in laws, regulations or the interpretation thereof, confiscatory taxation, restrictions on currency conversion, imports or sources of supplies, or the expropriation or nationalization of private enterprises. Although the PRC government has been pursuing economic reform policies for more than two decades, there is no assurance that the government will continue to pursue such policies or that such policies may not be significantly altered, especially in the event of a change in leadership, social or political disruption, or other circumstances affecting the PRC’s political, economic and social life.

The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Any changes in such PRC laws and regulations may harm our business.

The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. The PRC’s legal system is a civil law system based on written statutes, in which system decided legal cases have little value as precedents unlike the common law system prevalent in the United States. There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including but not limited to the laws and regulations governing our business, the enforcement and performance of our contractual arrangements with our affiliated Chinese entity, HBOP, and its shareholders, or the enforcement and performance of our arrangements with customers in the event of the imposition of statutory liens, death, bankruptcy and criminal proceedings. The Chinese government has been developing a comprehensive system of commercial laws, and considerable progress has been made in introducing laws and regulations dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade. However, because these laws and regulations are relatively new, and because of the limited volume of published cases and judicial interpretation and their lack of force as precedents, interpretation and enforcement of these laws and regulations involve significant uncertainties. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. Our major operating entity, HBOP, conducts its operations in China, and as a result, we are required to comply with PRC laws and regulations. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future PRC laws or regulations. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business. If the relevant authorities find that we are in violation of PRC laws or regulations, they would have broad discretion in dealing with such a violation, including, without limitation:

| | • | revoking HBOP’s business and other licenses; |

| | • | requiring that we restructure our ownership or operations; and |

| | • | requiring that we discontinue any portion or all of our business. |

Among the material laws that we are subject to are the Price Law of The People’s Republic of China, Measurement Law of The People’s Republic of China, Tax Law, Environmental Protection Law, Contract Law, Patent Law, Accounting Laws and Labor Law.

Our contractual arrangements with HBOP and its shareholders may not be as effective in providing control over HBOP as direct ownership.

Since the law of the PRC limits foreign equity ownership in companies in China, we operate our business through HBOP. We have no equity ownership interest in HBOP and rely on contractual arrangements to control and operate its business. These contractual arrangements may not be effective in providing control over HBOP as direct ownership. For example, HBOP could fail to take actions required for our business despite its contractual obligation to do so. If HBOP fails to perform under their agreements with us, we may have to incur substantial costs and resources to enforce such arrangements and may have to rely on legal remedies under the law of the PRC, which may not be effective. In addition, we cannot assure you that the HBOP’s shareholders would always act in our best interests.

Because we may rely on the consulting services agreement with HBOP for essentially all of our revenue and cash flows, any difficulty for HBOP to pay consulting fees to Baoding Shengde under the consulting agreement may have a material adverse effect on our operations.

We are a holding company and currently do not conduct any business operations other than the contractual arrangements between Baoding Shengde and HBOP. As a result, we may rely entirely for our revenues on dividend payments from Baoding Shengde for any payment from HBOP pursuant to the consulting services agreement which forms a part of the contractual arrangements between Baoding Shengde and HBOP. Since Baoding Shengde is not a legal shareholder of HBOP under PRC statutes, the arrangement for HBOP to pay a substantial portion of its net income to Baoding Shengde may be challenged by the PRC government, which could prevent us from issuing dividends to our shareholders or making required payments to some of our service providers.

A slowdown, inflation or other adverse developments in the PRC economy may harm our customers and the demand for our services and products.

All of our operations are conducted in the PRC and all of our revenue is generated from sales in the PRC. Although the PRC economy has grown significantly in recent years, we cannot assure you that this growth will continue. A slowdown in overall economic growth, an economic downturn, a recession or other adverse economic developments in the PRC could significantly reduce the demand for our products and harm our business.

While the PRC economy has experienced rapid growth, such growth has been uneven among various sectors of the economy and in different geographical areas of the country. Rapid economic growth could lead to growth in the money supply and rising inflation. If prices for our products rise at a rate that is insufficient to compensate for the rise in the costs of supplies, it may harm our profitability. In order to control inflation in the past, the PRC government has imposed controls on bank credit, limits on loans for fixed assets and restrictions on state bank lending. Such an austere policy can lead to a slowing of economic growth. In January 2010, the People’s Bank of China, the PRC’s central bank, raised interest rates for the first time in nearly five months. Repeated rises in interest rates by the central bank would likely slow economic activity in the PRC which could, in turn, materially increase our costs and also reduce demand for our products.

Governmental control of currency conversion may affect the value of your investment.

The PRC government imposes controls on the convertibility of Renminbi into foreign currencies and, in certain cases, the remittance of currency out of the PRC. We receive substantially all of our revenue in Renminbi, which is currently not a freely convertible currency. Shortages in the availability of foreign currency may restrict our ability to remit sufficient foreign currency to pay dividends, or otherwise satisfy foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from the transaction, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate governmental authorities is required where Renminbi is to be converted into foreign currency and remitted out of the PRC to pay capital expenses such as the repayment of bank loans denominated in foreign currencies.

The PRC government may also in the future restrict access to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay certain of our expenses as they come due.

The fluctuation of the Renminbi may harm your investment.

The value of the Renminbi against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in the PRC’s political and economic conditions. According to the Financial Management website fms.treas.gov/intn.html, as of December 31, 2010, $1 = 6.6700 Yuan (RMB). As we rely entirely on revenues earned in the PRC, any significant revaluation of the Renminbi may materially and adversely affect our cash flows, revenues and financial condition. For example, to the extent that we need to convert U.S. dollars we receive from an offering of our securities into Renminbi for HBOP’s operations, appreciation of the Renminbi against the U.S. dollar would diminish the value of the proceeds of the offering and this could harm our business, financial condition and results of operations because it would reduce the proceeds available to us for capital investment in proportion to the appreciation of the Renminbi. Thus if we raise 1,000,000 dollars and the Renminbi appreciates against the U.S. dollar by 15%, then the proceeds will be worth only RMB5,669,500 as opposed to RMB 6,670,000 prior to the appreciation. Conversely, if we decide to convert our Renminbi into U.S. dollars for the purpose of making payments for dividends on our common shares or for other business purposes and the U.S. dollar appreciates against the Renminbi, the U.S. dollar equivalent of the Renminbi we convert would be reduced in proportion to the amount the U.S. dollar appreciates. In addition, the depreciation of significant RMB denominated assets could result in a charge to our income statement and a reduction in the dollar value of these assets. Thus if HBOP has RMB1,000,000 in assets and Renminbi is depreciated against the U.S. dollar by 15%, then the assets will be valued at $130,370 as opposed to $149,925 prior to the depreciation.

On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the Renminbi to the U.S. dollar. Under the new policy, the Renminbi is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. This change in policy has resulted in an approximately 19.44% appreciation of the Renminbi against the U.S. dollar as of December 31, 2010. While the international reaction to the Renminbi revaluation has generally been positive, there remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the Renminbi against the U.S. dollar.

Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may materially adversely affect us.

In October 2005, the PRC State Administration of Foreign Exchange, or SAFE, issued the Notice on Relevant Issues in the Foreign Exchange Control over Financing and Round-Trip Investment Through Special Purpose Companies by Residents Inside China, generally referred to as Circular 75. The policy announced in this notice required PRC residents to register with the relevant SAFE branch before establishing or acquiring control over an offshore special purpose company, or SPV, for the purpose of engaging in an equity financing outside of China on the strength of domestic PRC assets originally held by those residents. Internal implementing guidelines issued by SAFE, which became public in May 2007 (known as Notice 106), expanded the reach of Circular 75. In the case of an SPV which was established, and which acquired a related domestic company or assets, before the implementation date of Circular 75, a retroactive SAFE registration was required to have been completed before March 31, 2006; this date was subsequently extended indefinitely by Notice 106, which also required that the registrant establish that all foreign exchange transactions undertaken by the SPV and its affiliates were in compliance with applicable laws and regulations. Failure to comply with the requirements of Circular 75, as applied by SAFE in accordance with Notice 106, may result in fines and other penalties under PRC laws for evasion of applicable foreign exchange restrictions. Any such failure could also result in the SPV’s affiliates being impeded or prevented from distributing their profits and the proceeds from any reduction in capital, share transfer or liquidation to the SPV, or from engaging in other transfers of funds into or out of China.

Because of uncertainty over the interpretation of Circular 75, we cannot assure you that, if challenged by government agencies, the structure of our organization has fully complied with all applicable registrations or approvals required by Circular 75. Moreover, because of uncertainty over how Circular 75 will be interpreted and implemented, and how or whether SAFE will apply it to us, we cannot predict how it will affect our business operations or future strategies. A failure by such PRC resident beneficial holders or future PRC resident stockholders to comply with Circular 75 and Notice 106, if SAFE requires it, could subject these PRC resident beneficial holders to fines or legal sanctions, restrict our overseas or cross-border investment activities, limit our subsidiaries’ ability to make distributions or pay dividends or affect our ownership structure, which could adversely affect our business and prospects.

The PRC’s legal and judicial system may not adequately protect our business and operations and the rights of foreign investors.

The PRC legal and judicial system may negatively impact foreign investors. In 1982, the National People’s Congress amended the Constitution of China to authorize foreign investment and guarantee the “lawful rights and interests” of foreign investors in the PRC. However, the PRC’s system of laws is not yet comprehensive. The legal and judicial systems in the PRC are still rudimentary, and enforcement of existing laws is inconsistent. Many judges in the PRC lack the depth of legal training and experience that would be expected of a judge in a more developed country. Because the PRC judiciary is relatively inexperienced in enforcing the laws that do exist, anticipation of judicial decision-making is more uncertain than would be expected in a more developed country. It may be impossible to obtain swift and equitable enforcement of laws that do exist, or to obtain enforcement of the judgment of one court by a court of another jurisdiction. The PRC’s legal system is based on the civil law regime, that is, it is based on written statutes; a decision by one judge does not set a legal precedent that is required to be followed by judges in other cases. In addition, the interpretation of Chinese laws may be varied to reflect domestic political changes.

The trend of legislation over the last 20 years has significantly enhanced the protection of foreign investment and allowed for more control by foreign parties of their investments in Chinese enterprises. However, the promulgation of new laws, changes to existing laws and the pre-emption of local regulations by national laws may adversely affect foreign investors. A change in leadership, social or political disruption, or unforeseen circumstances affecting the PRC’s political, economic or social life, may affect the PRC government’s ability to continue to support and pursue these reforms. Such a shift could have a material adverse effect on our business and prospects.

The practical effect of the PRC legal system on our business operations in the PRC can be viewed from two separate but intertwined considerations. First, as a matter of substantive law, the foreign invested enterprise laws provide significant protection from government interference. In addition, these laws guarantee the full enjoyment of the benefits of corporate articles and contracts to foreign invested enterprise participants. These laws, however, do impose standards concerning corporate formation and governance, which are qualitatively different from the general corporation laws of the United States. Similarly, the PRC accounting laws mandate accounting practices, which are not consistent with U.S. generally accepted accounting principles. PRC’s accounting laws require that an annual “statutory audit” be performed in accordance with PRC accounting standards and that the books of account of foreign invested enterprises are maintained in accordance with Chinese accounting laws. Article 14 of the People’s Republic of China Wholly Foreign-Owned Enterprise Law requires a wholly foreign-owned enterprise to submit certain periodic fiscal reports and statements to designated financial and tax authorities, at the risk of business license revocation. While the enforcement of substantive rights may appear less clear than United States procedures, foreign invested enterprises and wholly foreign-owned enterprises are Chinese registered companies, which enjoy the same status as other Chinese registered companies in business-to-business dispute resolution. Any award rendered by an arbitration tribunal is enforceable in accordance with the United Nations Convention on the Recognition and Enforcement of Foreign Arbitral Awards (1958). Therefore, as a practical matter, although no assurances can be given, the Chinese legal infrastructure, while different in operation from its United States counterpart, should not present any significant impediment to the operation of foreign invested enterprises

Any recurrence of Severe Acute Respiratory Syndrome, or SARS, or another widespread public health problem, could harm our operations.

A renewed outbreak of SARS or another widespread public health problem (such as bird flu) in the PRC, where all of our revenues are derived, could significantly harm our operations. Our operations may be impacted by a number of health-related factors, including quarantines or closures of any of our two locations in the city of Baoding that would adversely disrupt our operations. Any of the foregoing events or other unforeseen consequences of public health problems could significantly harm our operations.

Because our principal assets are located outside of the United States and most of our directors and officers reside outside of the United States, it may be difficult for you to enforce your rights based on U.S. federal securities laws against us and our officers or to enforce U.S. court judgment against us or them in the PRC.

Most of our directors and officers reside outside of the United States. In addition, our operating company is located in the PRC and substantially all of our assets are located outside of the United States. It may therefore be difficult for investors in the United States to enforce their legal rights based on the civil liability provisions of the U.S. Federal securities laws against us in the courts of either the U.S. or the PRC and, even if civil judgments are obtained in U.S. courts, to enforce such judgments in PRC courts. Further, it is unclear if extradition treaties now in effect between the United States and the PRC would permit effective enforcement against us or our officers and directors of criminal penalties, under the U.S. Federal securities laws or otherwise.

The relative lack of public company experience of our management team may put us at a competitive disadvantage.

Our management team lacks public company experience, which could impair our ability to comply with legal and regulatory requirements such as those imposed by Sarbanes-Oxley Act of 2002. The individuals who now constitute our senior management have never had responsibility for managing a publicly traded company. Such responsibilities include complying with federal securities laws and making required disclosures on a timely basis. Our senior management may not be able to implement programs and policies in an effective and timely manner that adequately responds to such increased legal, regulatory compliance and reporting requirements. Our failure to comply with all applicable requirements could lead to the imposition of fines and penalties and distract our management from attending to the growth of our business.

We may be required to broaden the coverage of the mandatory social security insurance programs under the New Labor Law of the PRC

The PRC New Labor Law, effective January 1, 2008, requires that employers enroll in the following social security insurance programs and offer certain employer-sponsored premium benefits to eligible employees: (1) retirement endowment, (2) healthcare insurance, (3) unemployment insurance, (4) workers’ compensation insurance, and (5) pregnancy insurance. Of these insurance programs, the retirement endowment fund requires employee withholdings of 4% to 8% of the gross compensation, while the employer’s matching contribution varies from 16% to 20% of such compensation. While the Company is enrolled in the retirement endowment fund and is withholding employees’ portion and the employer’s portion of the endowment contribution, many of the Company’s employees have elected to waive their coverage under these mandatory social security insurance programs in favor of certain other low-cost, local government-sponsored social security insurance programs for residents in non-urban districts. Although we have verified with the local government agencies for the validity of the employee waivers and reasonably believe that we are not required to cover the employees who waived the benefits, the local government may change its policy and ask us to broaden our insurance coverage to those who have specifically waived their rights.

Risks Related to Our Common Stock

Our officers and directors control us through their positions and stock ownership and their interests may differ from other stockholders.

As of December 31, 2010, there were 18,344,811 shares of our common stock issued and outstanding. Our officers and directors beneficially own approximately 27.98% of our common stock. Mr. Zhenyong Liu, our Chief Executive Officer, beneficially owns approximately 27.89% of our common stock. As a result, he is able to influence the outcome of stockholder votes on various matters, including the election of directors and extraordinary corporate transactions including business combinations. Yet Mr. Liu’s interests may differ from those of other stockholders. Furthermore, ownership of 27.98% of our common stock by our officers and directors reduces the public float and liquidity, and may affect the market price, of our common stock as traded on the NYSE Amex.

We are not likely to pay cash dividends in the foreseeable future.

We intend to retain any future earnings for use in the operation and expansion of our business. We do not expect to pay any cash dividends in the foreseeable future but will review this policy as circumstances dictate. Should we decide in the future to do so, as a holding company, our ability to pay dividends and meet other obligations depends upon the receipt of dividends or other payments from our operating subsidiaries. In addition, our operating subsidiaries, from time to time, may be subject to restrictions on their ability to make distributions to us, including restrictions on the conversion of local currency into U.S. dollars or other hard currency and other regulatory restrictions.

If we fail to comply with Section 404 of the Sarbanes-Oxley Act of 2002 in a timely manner, our business could be harmed and our stock price could decline.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of U.S. public companies’ internal control over financial reporting, and attestation of this assessment by their independent registered public accountants. The standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. While there has not been any detected significant deficiency or material weakness in our internal control and with respect to the assessment of the internal control for the year ended December 31, 2010, we cannot guarantee the implementation of controls and procedures in future years to be without any significant deficiency or material weakness.

Our common stock may be affected by limited trading volume and may fluctuate significantly.

Our common stock is traded on the NYSE Amex. Although an active trading market has developed for our common stock, there can be no assurance that an active trading market for our common stock will be sustained. Failure to maintain an active trading market for our common stock may adversely affect our shareholders’ ability to sell our common stock in short time periods, or at all. Our common stock has experienced, and may experience in the future, significant price and volume fluctuations, which could adversely affect the market price of our common stock.

Future financings may dilute stockholders or impair our financial condition.

In the future, we may need to raise additional funds through public or private financing, which might include the sale of equity securities. The issuance of equity securities could result in financial and voting dilution to our existing stockholders. The issuance of debt could result in effective subordination of stockholders’ interests to the debt, create the possibility of default, and limit our financial and business alternatives.