Legacy Reserves LP

RBC MLP Conference

November 15, 2007

Page 2

Forward-Looking Statements

Statements made by representatives of Legacy Reserves LP (the “Partnership”) during the course

of this presentation that are not historical facts are forward-looking statements. These statements

are based on certain assumptions made by the Partnership based on management’s experience

and perception of historical trends, current conditions, anticipated future developments and other

factors believed to be appropriate. Such statements are subject to a number of assumptions, risks

and uncertainties, many of which are beyond the control of the Partnership, which may cause actual

results to differ materially from those implied or expressed by the forward-looking statements. These

include risks relating to financial performance and results, availability of sufficient cash flow to pay

distributions and execute our business plan, prices and demand for oil a nd natural gas, our ability to

replace reserves and efficiently exploit our current reserves, our ability to make acquisitions on

economically acceptable terms, and other important factors that could cause actual results to differ

materially from those anticipated or implied in the forward-looking statements. Please see the

factors described in the Partnership’s Annual Report on Form 10-K in Item 1A under “Risk Factors”.

The Partnership undertakes no obligation to publicly update any forward-looking statements,

whether as a result of new information or future events.

Page 3

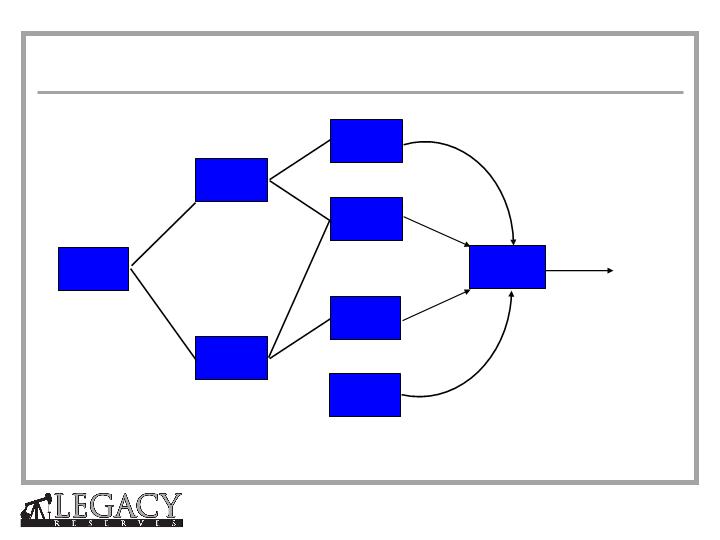

Other

Related

Entities

Dale Brown &

Jack McGraw

form

Partnership

Cary &

Dale Brown

form

Moriah

Formation Transaction

Through

Private Placement

1981

1991

2005

March

2006

January

2007

IPO

Brothers

Production

Company

Brothers

Moriah

Brothers

MBN

Moriah

Legacy

Kyle McGraw

&

Cary Brown

Assume

Management

Legacy History

Page 4

Name | Title | Years Experience in the Permian Basin | Years Experience in the Oil & Gas Industry |

Cary D. Brown, CPA | Chairman & CEO | 15 | 17 |

Steven H. Pruett | President & CFO | 18 | 23 |

Kyle A. McGraw | EVP, Business Development & Land | 24 | 24 |

Paul T. Horne | VP, Operations | 21 | 23 |

William M. Morris, CPA | VP, Controller & CAO | 25 | 26 |

William D. Sullivan

Former EVP

Anadarko Petroleum

G. Larry Lawrence

Former Controller

Pure Resources

Kyle D. Vann

Former CEO

Entergy - Koch, LP

Independent Board Members

Legacy Management Team

Page 5

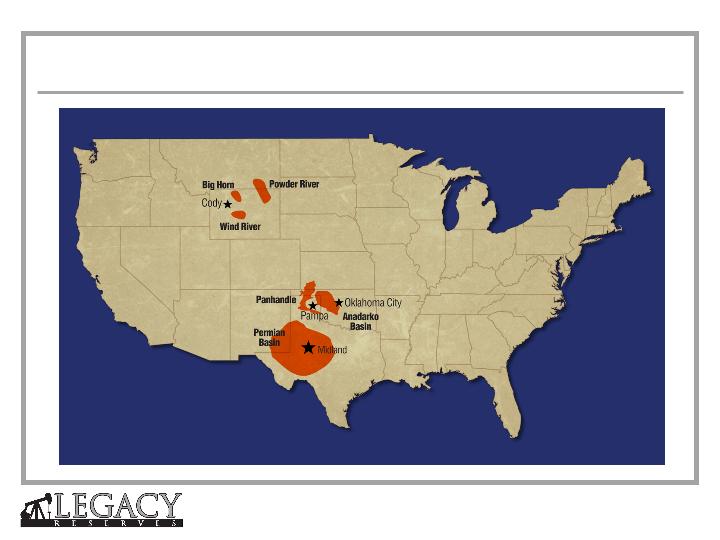

Asset Overview

Page 6

(1)Taken from reserve reports prepared by LaRoche Petroleum Consultants, Ltd. as of 12/31/06 for Legacy Reserves LP plus proved reserves from 2007 acquisitions from internal

reserve reports: Binger (4.1 MMBoe), TSF/Ameristate (1.4 MMBoe), Slaughter/Rocker A (1.0 MMBoe), Raven (1.2 MMBoe), TOC (4.0 MMBoe), Summit (0.7 MMBoe) and

Pan-Ellis/Mariner/SMB (0.77 MMBoe).

(2)Pro forma 2007 acquisitions of Binger, TSF, Ameristate, Slaughter/Rocker A, Raven, Samson, Carlow, TOC, Summit and Pan-Ellis/Mariner/SMB.

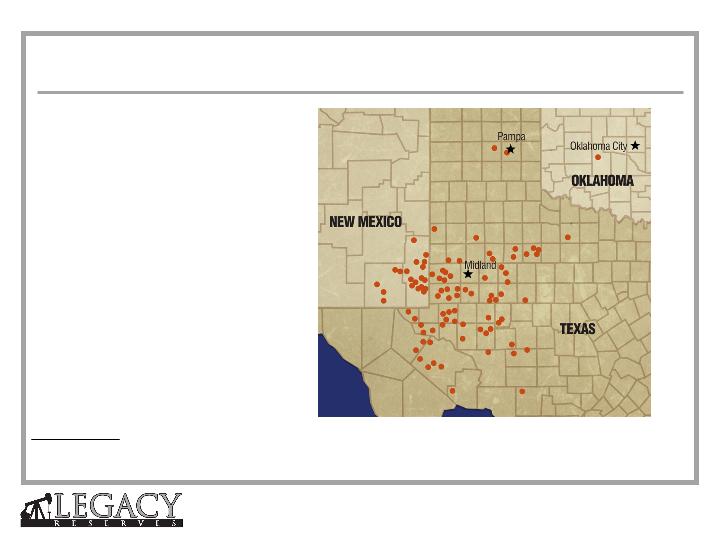

Legacy Base Asset Overview

q32.3 MMBoe of proved reserves (1)

qReserves-to-production ratio of over 15

years

qDiversified across over 3,000 wells

q70% operated

q6,100 net Boe per day (2)

q74% liquids

Page 7

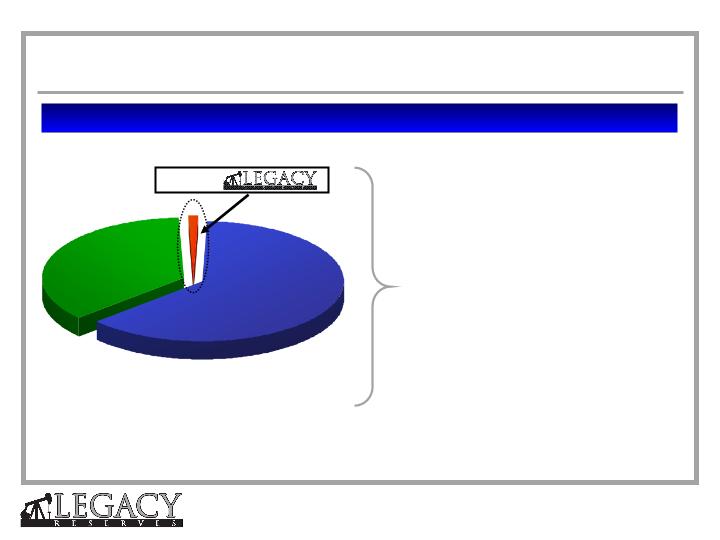

Top 5

Operators

1,700+

Operators

0.3%

(1) Ownership based on production. Permian Basin includes Texas Railroad Commission Districts 7C, 8, 8A and Lea and Eddy County, New Mexico.

Permian Basin data as of July 31, 2005; Legacy production data as of September 30, 2006.

63.6%

36.1%

Permian Basin Ownership Profile (1)

Consolidation Opportunities in the Permian Basin

qFragmented ownership provides numerous

acquisition opportunities

qAcquisition niche - large PDP component

qConnected in Permian Basin deal network

Page 8

$334 million of purchases

at an average cost of

$9.12 per Boe of proved

reserves in over 38 deals

13.4

20.2

36.7

6.8

13.4

6.8

13.4

16.5

Acquired Reserves (1999 - 2007)

Legacy & Predecessor Acquisition History

Page 9

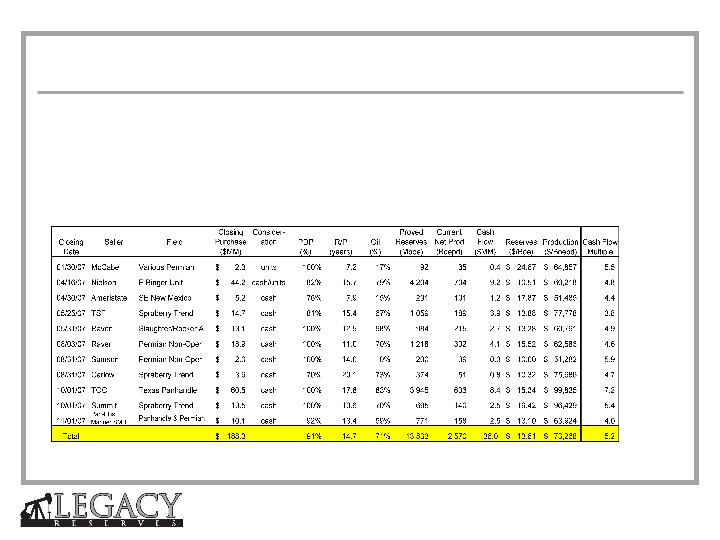

Legacy 2007 YTD Acquisitions

qClosed $188 million of acquisitions in 2007

qThirteen negotiated transactions averaging:

–$13.61 per Boe of proved reserves

–91% PDP, R/P ratio of 14.7 years

–$73,268 per Boepd

–5.2 times cash flow

Page 10

Financial Summary

Page 11

Financial and Operating Data - Latest Twelve Months

qThird Quarter earnings continue solid growth trend

–14.4% sequential volume growth over Q2

–Q3 production, revenue, distributable cash flow, and adjusted EBITDA exceeded analyst estimates

–Q3 does not include contribution from Panhandle, Summit and November acquisitions

(1)Please see pages 19 and 20

Consensus Analyst

($ in millions)

12-31-06

3-31-07

6-30-07

9-30-07

Estimates - Q3 2007

Production (Boe/d)

3,625

3,655

4,540

5,195

5,083

Revenue with realized hedges

$18.5

$18.4

$24.1

$29.8

$27.4

Distributable Cash Flow

$1.6

$6.8

$9.5

$14.5

$12.5

Distributable Cash Flow per Unit

$0.08

$0.36

$0.36

$0.56

$0.48

Adjusted EBITDA

(1)

$11.3

$11.1

$14.7

$18.9

$17.4

Quarter Ending

Summary Financial Information

Page 12

(1)Acquisitions closed subsequent to 9/30/2007, including cash flow adjustment paid to Legacy at deal closing.

(2)Excludes estimated offering expenses.

($ in millions)

9/30/2007

Acquisition

PIPE Offering

9/30/2007

Actual

Adjustments

(1)

Adjustments

(2)

Pro Forma

(2)

Cash

5.1

$

6.7

$

-

$

11.8

$

Total Debt

93.0

$

82.0

$

(75.0)

$

100.0

$

Partners' Equity

244.5

-

75.0

319.5

Total Capitalization

342.6

$

88.7

$

-

$

431.3

$

Pro Forma Capitalization

Page 13

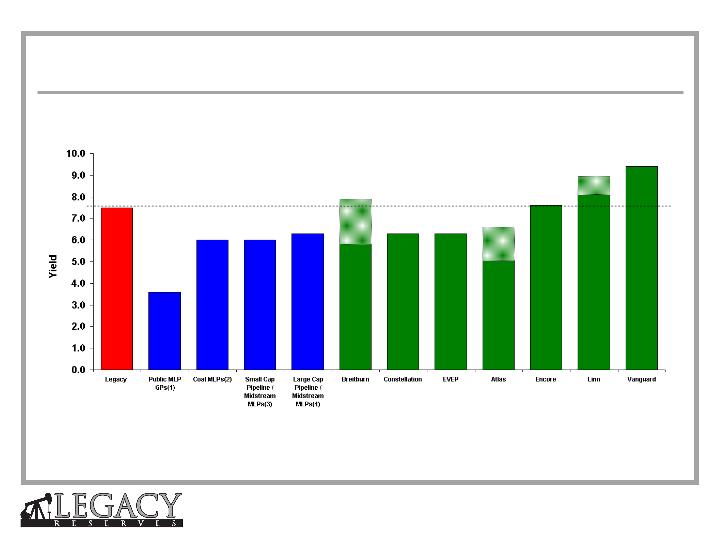

7.5%

3.6%

6.0%

6.0%

6.3%

5.8%

6.3%

6.3%

5.1%

8.1%

7.6%

Legacy as of 11/12/07. Other Energy MLP’s as of 11/8//07

As of 10/30/07:

(1) Includes General Partners of Alliance, Atlas, Buckeye, Crosstex, Energy Transfer, Enterprise, Hiland, Inergy, Magellan, Markwest, NuStar, Penn Virginia.

(2) Includes Alliance, Natural Resource Partners, Penn Virginia.

(3) Includes Atlas, Cheniere, Copano, Crosstex, DCP, Duncan, Eagle Rock, Genesis, Global, Hiland, Holly, Quicksilver, MarkWest, Martin, Regency, Sem Group, Spectra, Sunoco, Targa, TC, Transmontaigne, Williams.

(4) Includes Buckeye, Boardwalk, Enbridge, Energy Transfer, Enterprise, Kinder Morgan, Magellan, NuStar, Oneok, Plains, TEPPCO, NuStar.

7.9%

6.6%

9.0%

9.4%

Comparable Company Trading Yields

Page 14

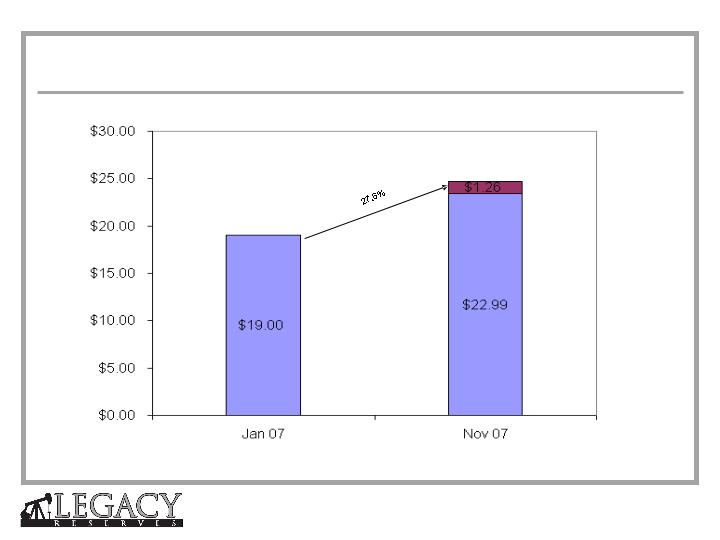

Note: Reflects closing price of 11/12/07

Legacy Unit Returns 2007 YTD

Page 15

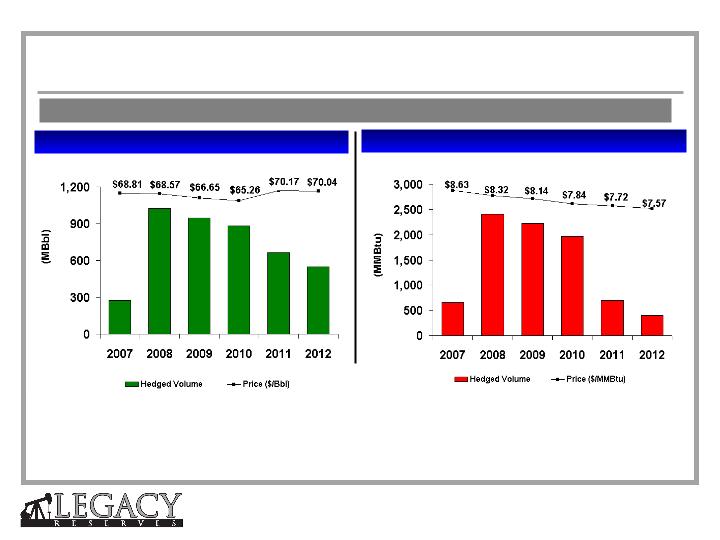

(1)WTI oil swaps used to hedge NGL production in 2009 (85,200 Bbls), 2010 (84,600 Bbls), 2011 (78,000 Bbls) and 2012 (75,600 Bbls).

(2)Includes NYMEX and Waha / ANR-OK swaps, where the latter indexes trade at a discount to NYMEX Henry Hub but better reflect what Legacy is paid for its

natural gas.

656 *

2,403

2,217

1,963

274 *

1,025

948

883

550

665

Oil (1)

Natural Gas (2)

Over 74% of forecasted production hedged for 2007-08 and over 60% hedged through 2010.

694

* 4th Quarter 2007 Volumes

404

Commodity Price Hedging Summary

Page 16

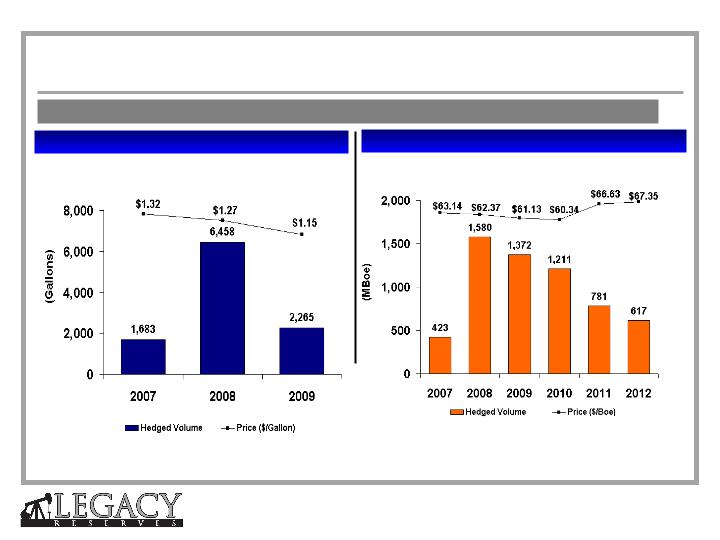

*

*

NGL’s

BOE’s

Over 74% of forecasted production hedged for 2007-08 and over 60% hedged through 2010.

* 4th Quarter 2007 volumes

Commodity Price Hedging Summary

Page 17

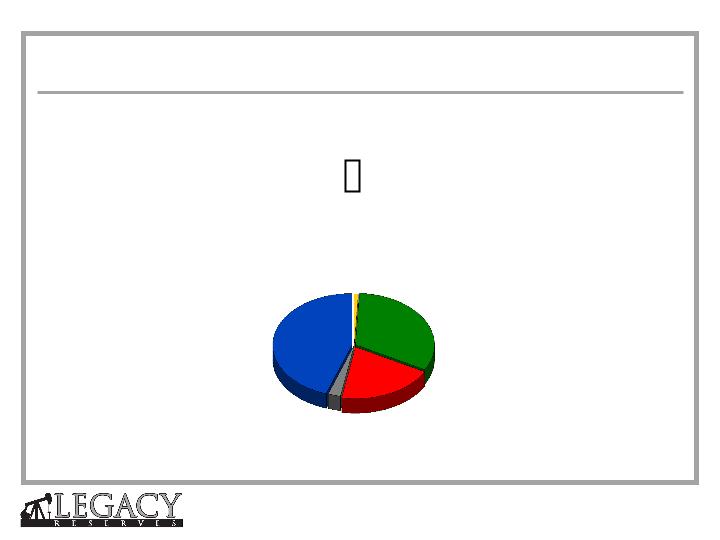

GP Interest

<0.1%

Public

Unitholders

32.4%

144A & PIPE

Unitholders

20%

Sellers of Assets to

Legacy

2.5%

Founding Investors,

Directors and Management

45%

Ticker:LGCY

Exchange:NASDAQ

Unit Price (11/12/07):$22.99 per unit

Quarterly Distribution:$0.43 per unit

Yield:7.5%

Market Capitalization:$683 million

Note: Ownership as of 11/12/07

Legacy Ownership

Page 18

Legacy Summary

qOnly MLP focused on the oil-weighted Permian Basin and Mid-continent regions

qExperienced management team with significant equity ownership

qSignificant organic and external growth opportunities

qLong-lived, diversified multi-pay properties

qDemonstrated reserve replacement capability

qLong-term hedges in place

qTax advantaged yield

qLow level of debt

qMLP structure with no IDRs

Page 19

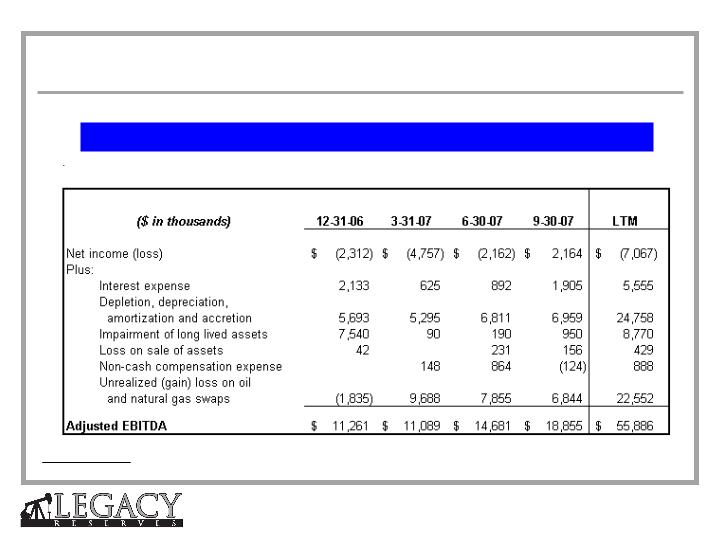

Adjusted EBITDA Reconciliation

This presentation, the financial tables and other supplemental information, including the reconciliations

of certain non-generally accepted accounting principles ("non-GAAP") measures to their nearest

comparable generally accepted accounting principles ("GAAP") measures, may be used periodically

by management when discussing Legacy's financial results with investors and analysts and they are

also available on Legacy's website under the Investor Relations tab. Adjusted EBITDA is defined in

our revolving credit facility as net income (loss) plus interest expense; depletion, depreciation,

amortization and accretion; impairment of long-lived assets; (gain) loss on sale of partnership

investment; (gain) loss on sale of assets; equity in (income) loss of partnerships; non-cash

compensation expense and unrealized (gain) loss on oil and natural gas swaps. Adjusted EB ITDA is

presented as management believes it provides additional information and metrics relative to the

performance of Legacy's business, such as the cash distributions we expect to pay to our unitholders,

as well as our ability to meet our debt covenant compliance tests. Management believes that these

financial measures indicate to investors whether or not cash flow is being generated at a level that can

sustain or support an increase in our quarterly distribution rates. Adjusted EBITDA may not be

comparable to a similarly titled measure of other publicly traded limited partnerships or limited liability

companies because all companies may not calculate Adjusted EBITDA in the same manner.

Page 20

Note: Adjusted EBITDA is a non-GAAP financial measure.

Reconciliation of Net Income to Adjusted EBITDA

Adjusted EBITDA Reconciliation

Legacy Reserves LP