Exhibit 99.1

Legacy Reserves LP

Executive Oil Conference

April 14, 2009

Page 2

Forward-Looking Statements

Statements made by representatives of Legacy Reserves LP (the “Partnership”) during the course

of this presentation that are not historical facts are forward-looking statements. These statements

are based on certain assumptions made by the Partnership based on management’s experience

and perception of historical trends, current conditions, anticipated future developments and other

factors believed to be appropriate. Such statements are subject to a number of assumptions, risks

and uncertainties, many of which are beyond the control of the Partnership, which may cause actual

results to differ materially from those implied or expressed by the forward-looking statements.

These include risks relating to financial performance and results, availability of sufficient cash flow

to pay distributions and execute our business plan, prices and demand for oil and natural gas, our

ability to replace reserves and efficiently exploit our current reserves, our ability to make

acquisitions on economically acceptable terms, and other important factors that could cause actual

results to differ materially from those anticipated or implied in the forward-looking statements.

Please see the factors described in the Partnership’s Annual Report on Form 10-K in Item 1A under

“Risk Factors”. The Partnership undertakes no obligation to publicly update any forward-looking

statements, whether as a result of new information or future events.

of this presentation that are not historical facts are forward-looking statements. These statements

are based on certain assumptions made by the Partnership based on management’s experience

and perception of historical trends, current conditions, anticipated future developments and other

factors believed to be appropriate. Such statements are subject to a number of assumptions, risks

and uncertainties, many of which are beyond the control of the Partnership, which may cause actual

results to differ materially from those implied or expressed by the forward-looking statements.

These include risks relating to financial performance and results, availability of sufficient cash flow

to pay distributions and execute our business plan, prices and demand for oil and natural gas, our

ability to replace reserves and efficiently exploit our current reserves, our ability to make

acquisitions on economically acceptable terms, and other important factors that could cause actual

results to differ materially from those anticipated or implied in the forward-looking statements.

Please see the factors described in the Partnership’s Annual Report on Form 10-K in Item 1A under

“Risk Factors”. The Partnership undertakes no obligation to publicly update any forward-looking

statements, whether as a result of new information or future events.

Page 3

Name | Title | Years Experience in the Permian Basin | Years Experience in the Oil & Gas Industry |

Cary D. Brown, CPA | Chairman & CEO | 17 | 19 |

Steven H. Pruett | President & CFO | 20 | 25 |

Kyle A. McGraw | EVP, Business Development & Land | 26 | 26 |

Paul T. Horne | EVP, Operations | 23 | 25 |

William M. Morris, CPA | VP, Controller & CAO | 27 | 28 |

Senior Management averages over 20 years of experience

William D. Sullivan

Former EVP

Anadarko Petroleum

G. Larry Lawrence

Former Controller

Pure Resources

Kyle D. Vann

Former CEO

Entergy - - Koch, LP

Independent Board Members

William R. Granberry

Former Pres & COO

Tom Brown, Inc.

Legacy Management Team

Page 4

q 30.8 MMBoe of Proved

Reserves (1)

Reserves (1)

q Reserves-to-Production Ratio

of over 10 years

of over 10 years

q Diversified across 3,850

Producing Wells

Producing Wells

q 65% Operated Production

q 8,553 Net Boepd in Q4 2008

q 71% Oil & NGL Production

(1) 12-31-08 Reserves reported in the Legacy

Reserves 10-K based on flat prices of

$44.60/Bbl WTI and $5.62/MMBtu NYMEX

Henry Hub gas

Reserves 10-K based on flat prices of

$44.60/Bbl WTI and $5.62/MMBtu NYMEX

Henry Hub gas

Legacy Asset Overview

Page 5

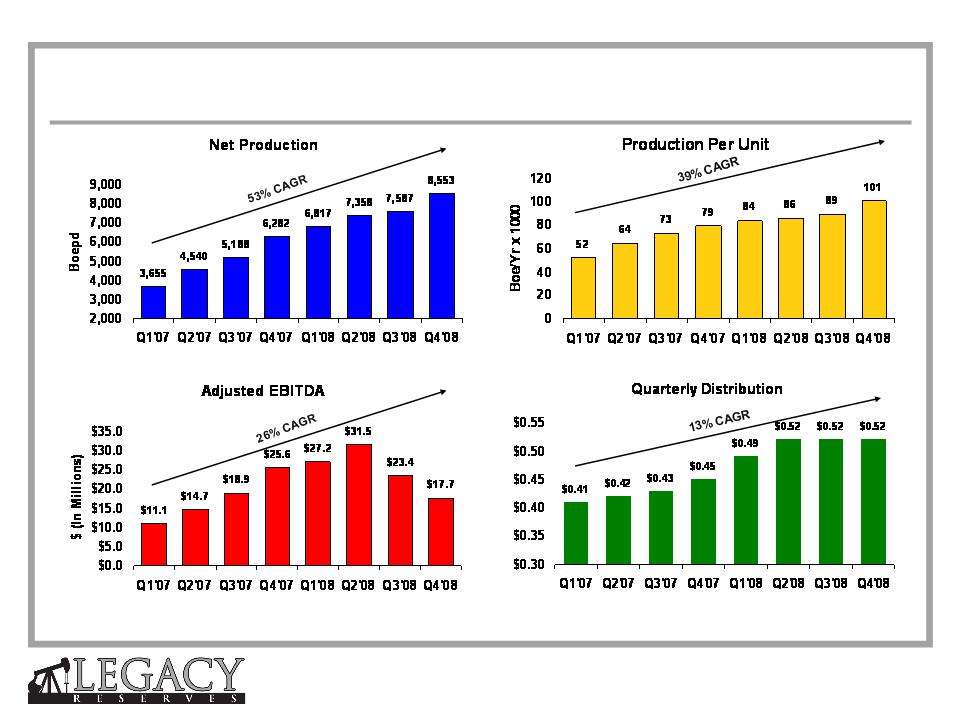

Note: CAGR = Compound Annual Growth Rate

Quarterly Production and Cash Flow Profile

Page 6

Equity Offering History

q March, 2006: $85 million raised through 144A Private Placement

q January, 2007: $131 million raised at Initial Public Offering - 85% retail placement

q November, 2007: $75 million raised from institutional investors (PIPE)

q $292 million of equity capital has been raised since 2006

Ш Used to fund approximately $523 million of acquisitions since forming Legacy

Ш Hedged 5 years of oil and gas prices when Legacy was formed

Ш Hedged acquisitions upon signing purchase agreement or at closing

Page 7

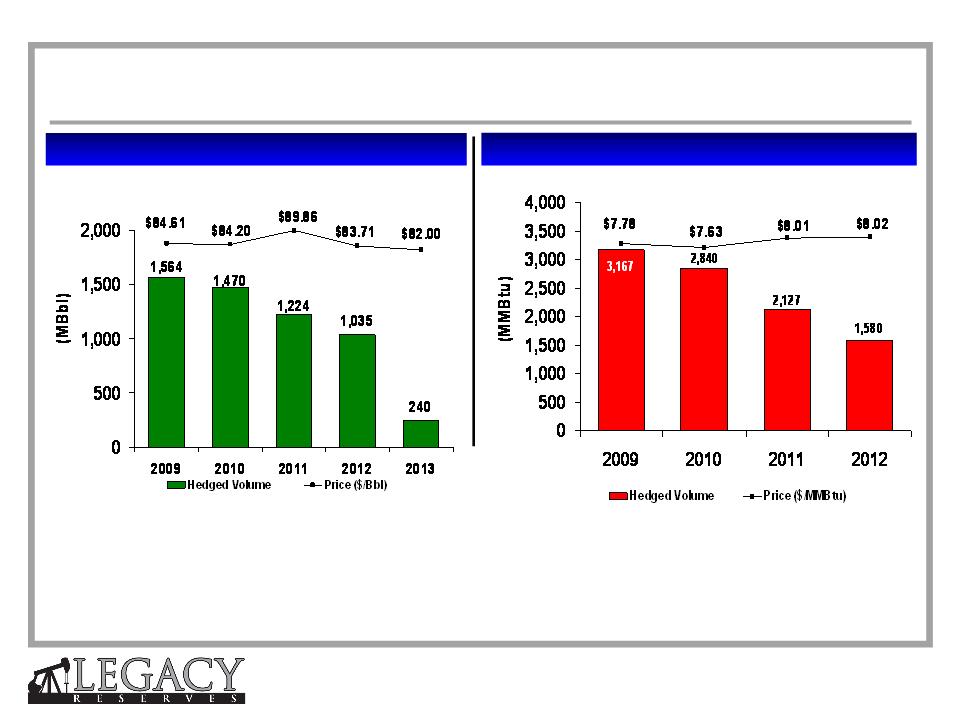

Oil

Natural Gas (1)

Hedges have been placed with Bank Group to avoid margin

calls and manage counterparty risk

calls and manage counterparty risk

(1)Natural gas is hedged near our gas sales points at Waha and

ANR-Oklahoma

ANR-Oklahoma

Oil and Gas Price Hedging Summary

Page 8

Borrowing Base Update

q Borrowing base decreased to $340 million in March from $410 million in the fall

q Increased Upfront Fees (112 bp) as well as wider LIBOR spreads resulting in higher

cost of borrowing

cost of borrowing

q New maturity date of April 1, 2012

q $300 million of debt drawn

q Goal in 2009 is debt reduction

Page 9

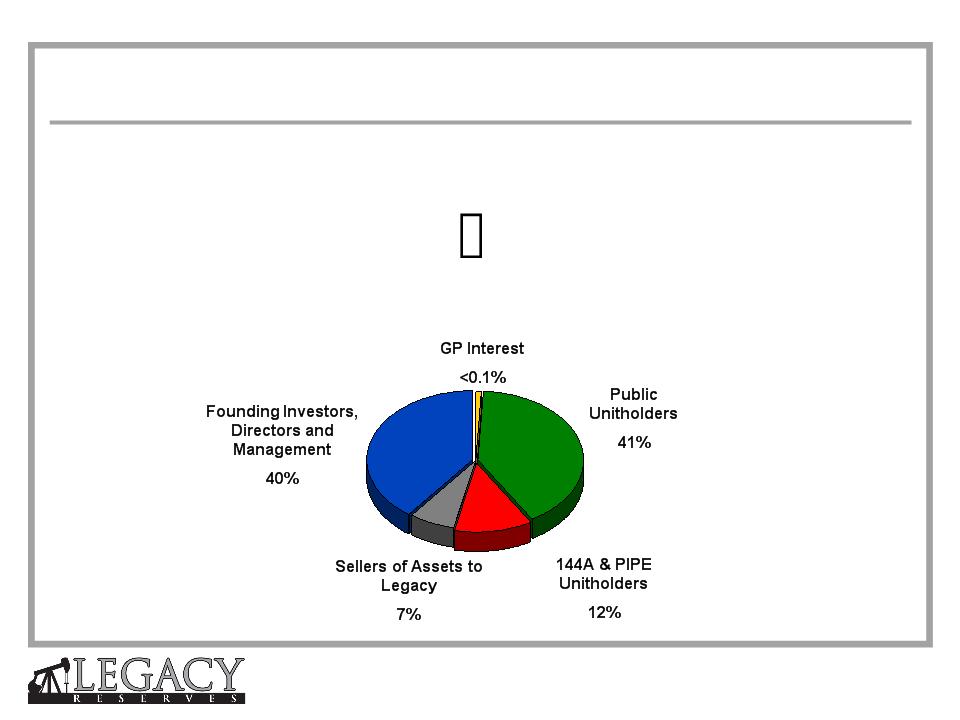

Ticker: LGCY

Exchange: NASDAQ

Unit Price (4/9/09): $13.00 per unit

Quarterly Distribution: $0.52 per unit

Yield: 16%

Market Capitalization: $404 million

Enterprise Value $704 million

Note: Estimated Ownership as of 12/01/08

Legacy Ownership

Page 10

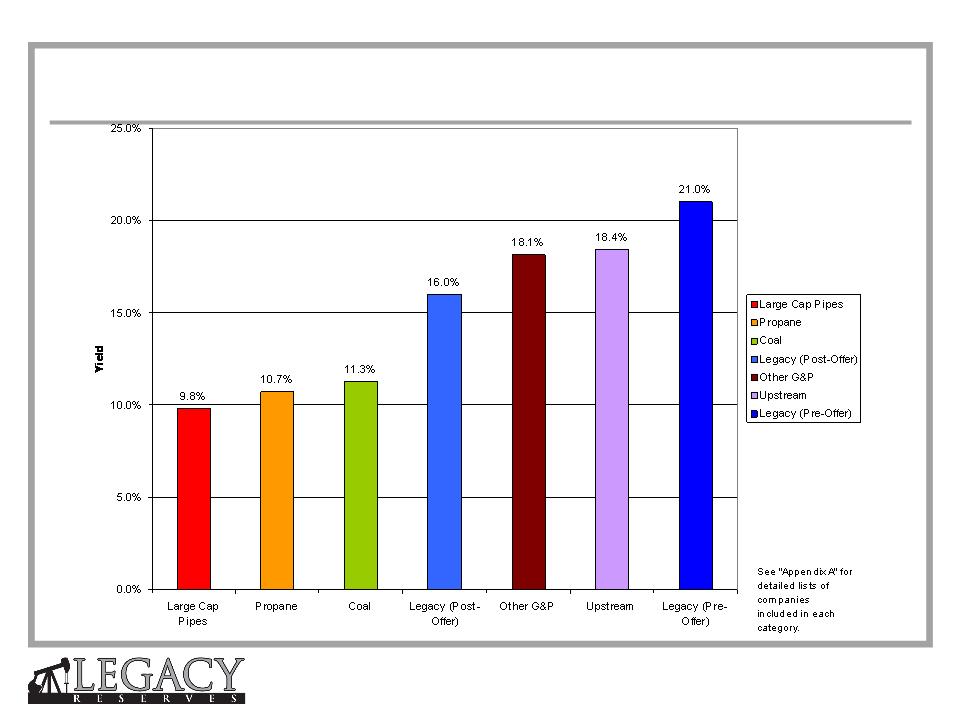

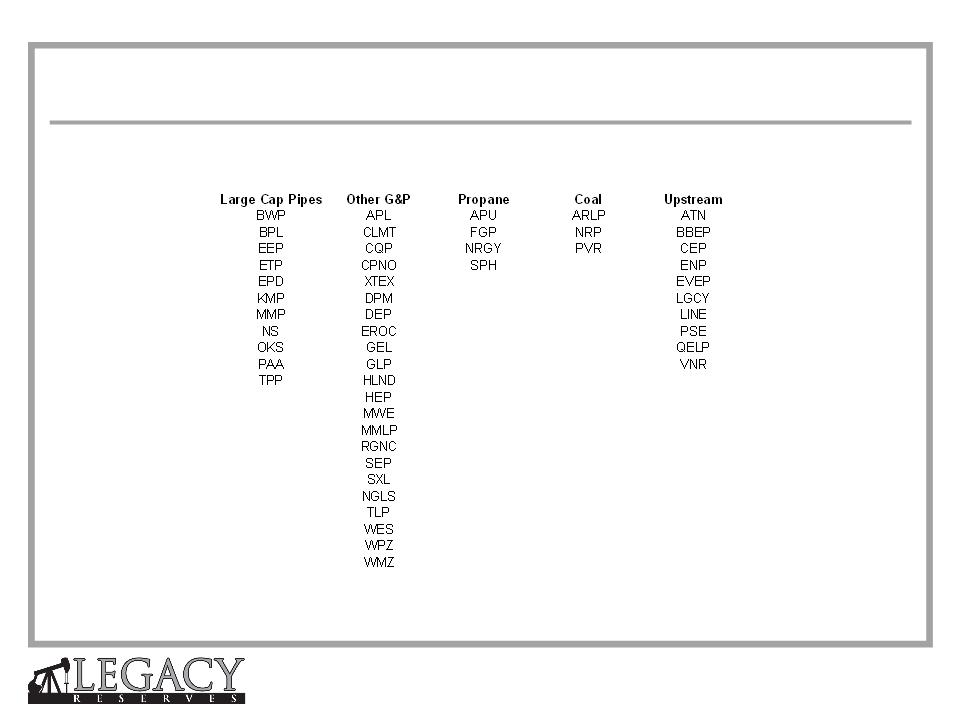

MLP Yields by Sector

Page 11

Page 12

Page 13

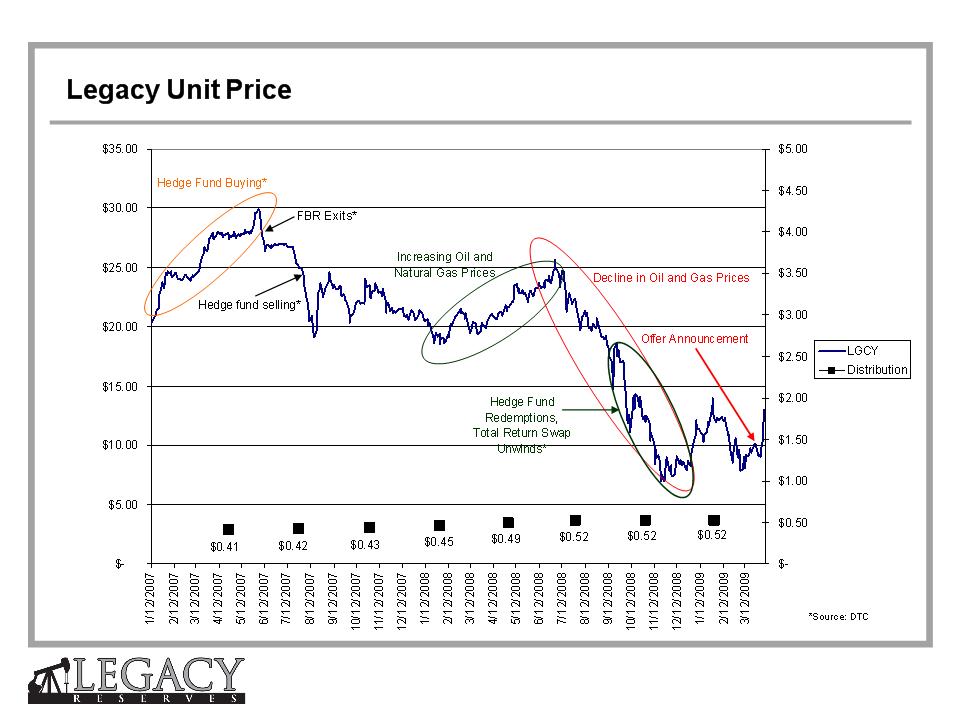

Hedge fund buying*

Hedge fund selling*

*Source: DTC

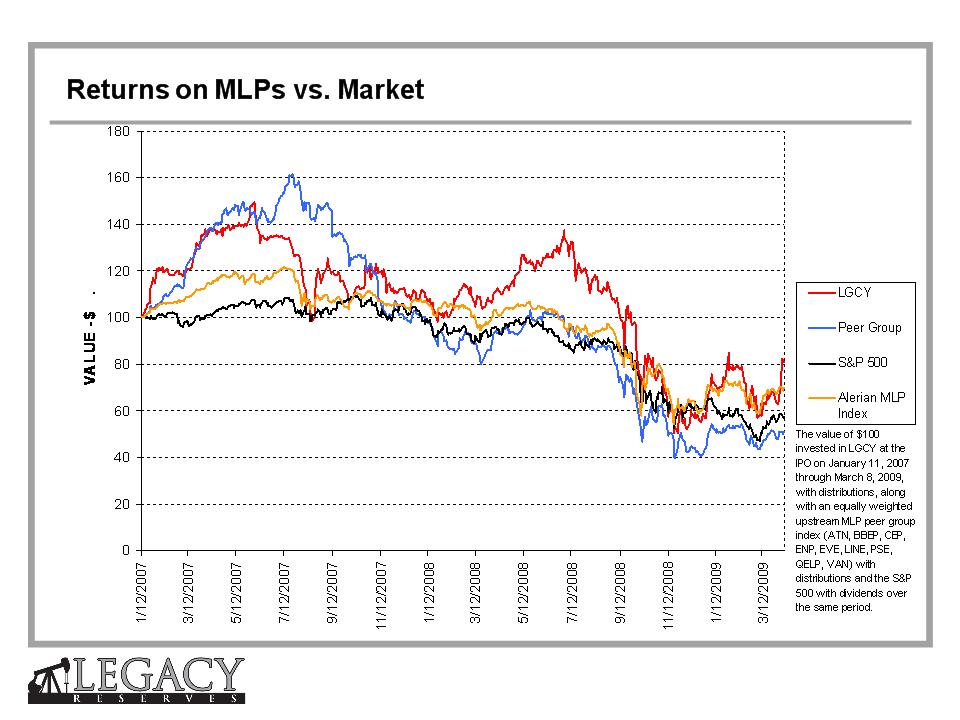

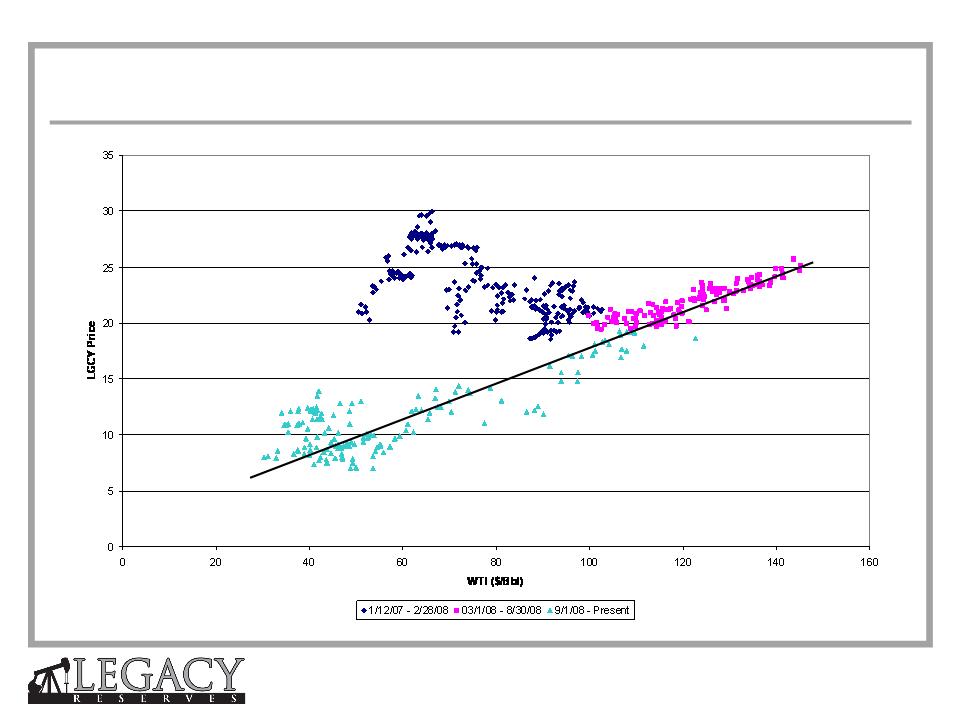

LGCY Unit Price vs. Oil Price

Page 14

“Take Private” Proposal

q Apollo Management VII, LP, a $14.7B private equity fund, has offered $14 per unit,

less future cash distributions, to buy all units outstanding.

less future cash distributions, to buy all units outstanding.

q The proposed price represents a 42% premium over the April 2, 2009 closing price

prior to the announcement and a 51% premium to the prior 30 day average closing

price.

prior to the announcement and a 51% premium to the prior 30 day average closing

price.

q Legacy’s Conflicts Committee (composed entirely of independent directors) has

engaged Tudor Pickering Holt to evaluate the fairness of the proposal and consider

other alternatives.

engaged Tudor Pickering Holt to evaluate the fairness of the proposal and consider

other alternatives.

q It is expected that management and employees would remain in place should the

proposed transaction be approved.

proposed transaction be approved.

q If approved by the Board of Directors, Legacy management has indicated that it will

support the transaction, rolling a significant portion of its holdings into the private

partnership with Apollo.

support the transaction, rolling a significant portion of its holdings into the private

partnership with Apollo.

Note: There can be no assurance that any definitive offer will be made, any agreement will be executed or that any

transaction will be approved or consummated.

transaction will be approved or consummated.

Page 15

Upstream MLP Issues

q Sustainability of Distributions

– Distribution security impacted by liquidity

– Variable vs. Managed

q Judicious Approach to Acquisitions

– Opportunities for acquisition should become compelling if capital

remains scarce; companies selling off production to fund drilling

remains scarce; companies selling off production to fund drilling

– Reductions in Borrowing Base

q Lack of Access to Equity Markets

Page 16

Hunker Down or Act?

q The longer prices remain depressed, the more dramatic the recovery due to

deferral and cancellation of LT capital projects and demand stimulus.

deferral and cancellation of LT capital projects and demand stimulus.

q Costs are resetting with stacking of iron and layoffs, input costs declining with

global recession (iron, cement, power).

global recession (iron, cement, power).

q Opportunistic selling during 2007-08 replaced with distressed selling by the fall.

q Availability of good projects and acreage has never been better as companies

are overcommitted with expiring leases.

are overcommitted with expiring leases.

q Capital markets will start to function ahead of the global recovery.

q Patience is warranted, as we are relatively early in what is expected to be a

deep cycle, but be positioned to act.

deep cycle, but be positioned to act.

Page 17

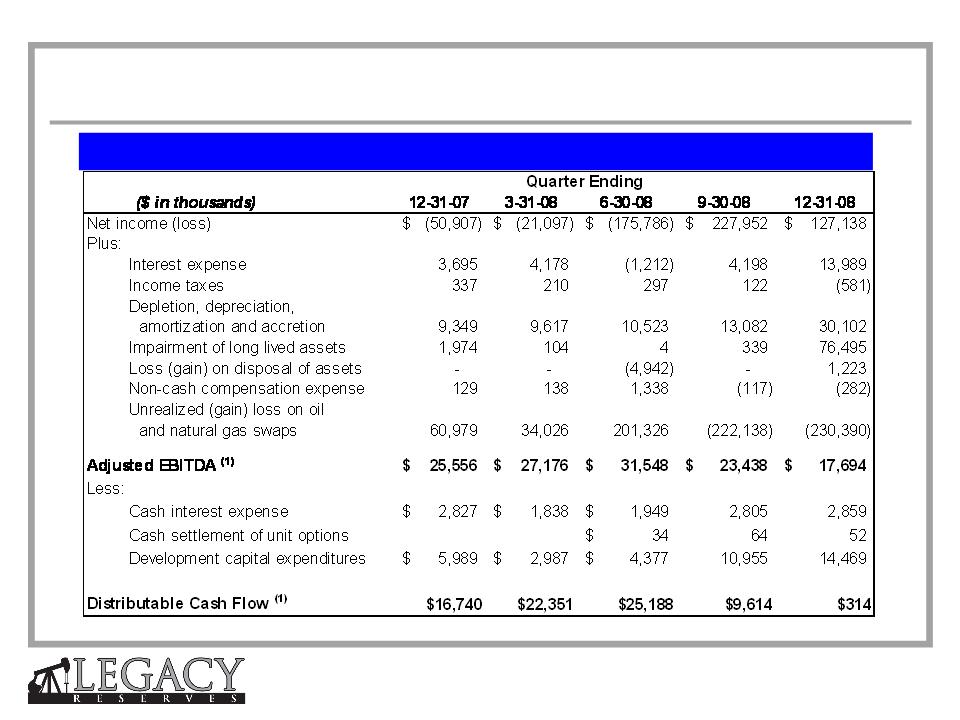

Adjusted EBITDA & Distributable Cash Flow Reconciliation

This presentation, the financial tables and other supplemental information, including the reconciliations

of certain non-generally accepted accounting principles ("non-GAAP") measures to their nearest

comparable generally accepted accounting principles ("GAAP") measures, may be used periodically by

management when discussing Legacy's financial results with investors and analysts and they are also

available on Legacy's website under the Investor Relations tab. Adjusted EBITDA is defined in our

revolving credit facility as net income (loss) plus interest expense; income taxes; depletion,

depreciation, amortization and accretion; impairment of long-lived assets; (gain) loss on sale of

partnership investment; (gain) loss on sale of assets; equity in (income) loss of partnerships; non-cash

compensation expense and unrealized (gain) loss on oil and natural gas swaps. Adjusted EBITDA and

Distributable Cash Flow is presented as management believes it provides additional information and

metrics relative to the performance of Legacy's business, such as the cash distributions we expect to

pay to our unitholders, as well as our ability to meet our debt covenant compliance tests. Management

believes that these financial measures indicate to investors whether or not cash flow is being generated

at a level that can sustain or support an increase in our quarterly distribution rates. Adjusted EBITDA

and Distributable Cash Flow may not be comparable to a similarly titled measure of other publicly

traded limited partnerships or limited liability companies because all companies may not calculate

Adjusted EBITDA and Distributable Cash Flow in the same manner.

of certain non-generally accepted accounting principles ("non-GAAP") measures to their nearest

comparable generally accepted accounting principles ("GAAP") measures, may be used periodically by

management when discussing Legacy's financial results with investors and analysts and they are also

available on Legacy's website under the Investor Relations tab. Adjusted EBITDA is defined in our

revolving credit facility as net income (loss) plus interest expense; income taxes; depletion,

depreciation, amortization and accretion; impairment of long-lived assets; (gain) loss on sale of

partnership investment; (gain) loss on sale of assets; equity in (income) loss of partnerships; non-cash

compensation expense and unrealized (gain) loss on oil and natural gas swaps. Adjusted EBITDA and

Distributable Cash Flow is presented as management believes it provides additional information and

metrics relative to the performance of Legacy's business, such as the cash distributions we expect to

pay to our unitholders, as well as our ability to meet our debt covenant compliance tests. Management

believes that these financial measures indicate to investors whether or not cash flow is being generated

at a level that can sustain or support an increase in our quarterly distribution rates. Adjusted EBITDA

and Distributable Cash Flow may not be comparable to a similarly titled measure of other publicly

traded limited partnerships or limited liability companies because all companies may not calculate

Adjusted EBITDA and Distributable Cash Flow in the same manner.

Page 18

(1) Adjusted EBITDA and Distributable Cash Flow are non-GAAP financial measures.

Reconciliation of Net Income to Adjusted EBITDA & Distributable Cash Flow

Adjusted EBITDA and DCF Reconciliation

Page 19

MLP Yields by Sectors Listed Below (see page 10)

Appendix A