UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21897

Manager Directed Portfolios

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Scott M. Ostrowski, President

Manager Directed Portfolios

c/o U.S. Bank Global Fund Services

811 East Wisconsin Avenue, 8th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(414) 765-4339

Registrant's telephone number, including area code

Date of fiscal year end: October 31, 2021

Date of reporting period: October 31, 2021

Item 1. Reports to Stockholders.

| (a) |

Hardman Johnston

International Growth Fund

Retail Shares HJIRX

Institutional Shares HJIGX

Annual Report

October 31, 2021

Hardman Johnston International Growth Fund

Table of Contents

| Letter to Shareholders | 3 |

| Investment Highlights | 8 |

| Sector Allocation | 9 |

| Schedule of Investments | 10 |

| Statement of Assets and Liabilities | 12 |

| Statement of Operations | 13 |

| Statements of Changes in Net Assets | 14 |

| Financial Highlights | 16 |

| Notes to the Financial Statements | 18 |

| Report of Independent Registered Public Accounting Firm | 29 |

| Expense Example | 30 |

| Notice to Shareholders | 32 |

| Statement Regarding Liquidity Risk Management Program | 33 |

| Trustees and Officers | 34 |

| Notice of Privacy Policy & Practices | 37 |

Hardman Johnston International Growth Fund

| LETTER TO SHAREHOLDERS |

Dear Shareholders,

Since the Hardman Johnston International Growth Fund (“the Fund”), formerly Marmont Redwood International Equity Fund, inception date on February 14, 2018, the Fund generated a return of +12.25% (institutional Shares) for the period ending October 31, 2021. This performance compared to +6.30% for its benchmark, the MSCI AC World ex-USA Index (USD) for the same period. For the fiscal year ended October 31, 2021, the Fund generated a return of +30.87% (Institutional Shares). During the same period, the MSCI AC World ex-USA Index (USD) generated a +29.66% return. Hardman Johnston Global Advisors LLC became the sub-advisor to the Fund on January 1, 2020.

For the fiscal year ended October 31, 2021, the top five portfolio contributors for the portfolio were: ASML Holding NV, Atlassian Corp. Plc, ICICI Bank Ltd ADR, WuXi Biologics (Cayman) Inc., and Aptiv PLC. All five of the top contributors remained in the Fund at the end of the period. ASML Holding NV is a key beneficiary from the increased demand for semiconductor content across key end markets like smartphones, consumer electronics, data centers and autos. ASML is the monopoly-supplier of extreme ultraviolet (EUV) lithography equipment, which is the critical tool in the manufacturing of semiconductors on nodes at 7nm and smaller. Several major semiconductor manufacturers have increased capex plans for leading-edge equipment given the extremely tight supply situation in semiconductors, alongside robust demand driven by secular growth themes like 5G and the electrification of the vehicle. ASML remains a high conviction, long-term holding as demand remains very strong for their leading-edge equipment.

Atlassian Corp. followed a record-setting new customer result in its March 2021 quarter with an equally impressive June quarter result, where we saw its total customer base reach 236.1k as it finished its fiscal year. Atlassian’s successful penetration in large enterprise was evidenced by its 70% year over year growth of $1 million-plus customers as its unique, developer-led focus continues to scale its product offering throughout an organization’s technology stack. The company’s cloud migration strategy has exceeded expectations with 2x the number of customers migrating in FY21 over FY20. Atlassian should continue to benefit from continued conversions of its existing customer base to the cloud and new customer growth through its R&D-focused/product development go-to-market approach. This gives us confidence in the company’s mid-to-low 40% subscription growth guidance in FY22 and bolsters our conviction in the stock over the long-term.

Shares of ICICI Bank Limited responded to significantly better results than expected in early February 2021 with improved margins, better fee growth and strong deposit momentum. In addition, non-performing loans were much lower than expected which was a worry as a result of the pandemic. The bank gave an upbeat view at their investor day of their opportunities as the Indian economy continues to open which include: continuing improvement in ROE, better expense control, increased benefits from

3

Hardman Johnston International Growth Fund

technology investments, increased market share and better margins from higher fee products all as non-performing loans continue to normalize. WuXi Biologics Inc. has benefited as a manufacturing partner for COVID-19 vaccines. They have announced two additional partnered mRNA vaccines. The company reiterated their expectations of >50% growth over the next few years. We remain positive on WuXi Biologics as a leader in both China and global biologics manufacturing outsourcing.

Aptiv plc is a tier-one automotive supplier and a prime beneficiary of the industry’s two key megatrends, the electrification of the powertrain and active safety, including autonomous capabilities. As automobile functionality has increased over time, so too have the demands on the electrical systems with respect to increasing power and reliability needs, balanced against ongoing light-weighting efforts. Aptiv leverages its know-how to develop custom solutions through its Signal and Power Solutions segment, and in particular, benefits from electric vehicle (EV) proliferation as its EV-specific components represent 2-3x higher content per vehicle while already generating group level profitability. In the company’s Active Safety segment, Aptiv is a leading one-stop solution, providing Level 1-3 automated driver assistance systems (ADAS) safety features through its sensor and systems integration expertise, bolstered by its industry-leading software capabilities. The fast-growing ADAS business is also achieving group level profitability, with expectations of even higher margin potential in the medium term. As a result of these attributes, the company has consistently outgrown the industry, while maintaining double digit margins, which are feats seldom achieved among most auto suppliers. With significant runway left in EV and ADAS penetration, the company’s growth prospects are robust.

During the same period, the top five portfolio detractors for the portfolio were: Alibaba Health Information Technology Ltd., Melco Resorts & Entertainment, Alibaba Group Holding Ltd., Taiwan Semiconductor Manufacturing Co., and Tencent Holdings Ltd. Except for Alibaba Group Holding Ltd., the other portfolio detractors remained in the portfolio at the end of the period. Alibaba Group Holding Ltd. was sold in the first quarter of 2021. Alibaba Health Information Technology Ltd. fell sharply related to Chinese government societal plans on “common prosperity.” There have been no direct new regulations on healthcare, and we remain confident that internet healthcare will remain an agent for the government to improve healthcare access and quality. There is an upcoming regulatory rule finalization on internet prescriptions, but expectations are for modest changes in line with pre-published rule changes. We remain positive on Alibaba Health given their strong platform capabilities coupled with the large and growing need for healthcare efficiencies in China. Alibaba Health Information Technology Ltd. is China’s healthcare internet leader. They have a strong ecosystem to meet current demands and the ability to change with this expanding market. China has high unmet needs for improved healthcare delivery, creating a durable, high growth opportunity. Imbalances in age, facility utilization, online-to-offline and other system inefficiencies present a need and a long term market that the firm is well-positioned to capitalize on.

4

Hardman Johnston International Growth Fund

Shares of Melco Resorts & Entertainment Ltd. retracted as a result of travel restrictions and a new governmental framework on gaming license renewals. Travel restrictions were implemented following an outbreak of COVID-19 cases in China. We expect these restrictions to be recurring until China is fully vaccinated, or its policy regarding COVID-19 evolves vs. the current zero tolerance policy. Additionally, the Macau Government announced a proposed framework for renewing gaming licenses (expiring June 2022). The new framework envisions a larger role for the Government, more rules regarding capital deployment and repatriation, and more restrictions on the VIP Business. The Macau Government’s final version of the framework will become clearer in 2022. Travel will resume more freely likely around Q2-Q3 2022. However, the underlying role of Macau as a gaming destination has not and will not change.

Alibaba Group Holding Ltd. shares have been under pressure since late 2020 as they were the focus of Chinese antitrust regulators after the cancellation of the blockbuster, Ant Group, IPO in December 2020. Authorities are broadly examining markets across China Internet, especially e-commerce. While we do not expect near-term business trends for Alibaba to be significantly affected, we see a risk for Alibaba to be less dominant in the future. Additionally, we foresee an increasing need to invest in growing new markets, especially in lower tier cities. Lastly, we see more compelling opportunities elsewhere during this period of growth uncertainty and margin pressure. We decided to exit the position in February 2021.

We initiated a position in Taiwan Semiconductor Manufacturing Co., Ltd. (TSMC) during the first quarter due to its immense market leadership in foundry services for semiconductor manufacturing. TSMC has developed the highest standard of leading-edge manufacturing, particularly with the implementation of extreme ultraviolet (EUV) lithography, a tool primarily used to shrink patterns that manufacturers print onto semiconductors. TSMC is a critical supplier for many of the largest fabless chip designers and device manufacturers globally, including Apple, Qualcomm, AMD and NVIDIA. The company’s R&D efforts and expansion plans (emphasized in its first quarter earnings report with capex plans guided up to $28bn) solidify its leadership position in foundry, at a time where more and more end markets require semiconductor content. We take a long-term view on TSMC as one of the most critical suppliers in the technology supply chain.

China’s lock-down in 2020 gave Tencent Holdings Ltd.’s dominant gaming franchise a huge boost as stringently enforced stay-at-home orders left gamers with few entertainment options during the period. Subsequently, the Chinese government reminded the gaming firms that they need to limit game time for children and avoid what could be considered unfair competition and monopolies, comments that put pressure on all Chinese based internet companies. While regulatory challenges may weigh on the stock over the near term, we believe Tencent will be able to navigate these headwinds over time.

At the end of the period, the Fund held 25 stocks across various international regions and sectors. Relative to the benchmark, the Fund carried an overweight to Pacific Ex Japan and Japan, and a relative underweight to the Emerging Markets and North America.

5

Hardman Johnston International Growth Fund

Relative sector exposure to the benchmark, the Fund was overweight to information technology and industrials, and a relative underweight to financials and consumer staples.

OUTLOOK

Global growth momentum appears to have peaked following the economic boost supplied by reopening. We believe the recovery will stretch into 2022 as countries continue to deal with COVID-19 and the weaning of economies off fiscal and monetary support.

Supply chain bottlenecks, rising wages, and inflation could be a drag on growth in the near term. However, as the Federal Reserve and European Central Bank have indicated, the effects are likely to be only transitory. How long it will take to return to equilibrium is uncertain. And that equilibrium could be at a higher rate, with prices higher and labor more expensive than before the crisis. However, we don’t see the seeds of spiraling inflation. If anything, we believe the overarching drivers of disinflation, namely aging populations and increased penetration of technology that will automate industry and reduce costs, remain strong in developed economies.

Developed market central banks are likely to tread a cautious line in the face of inflation. The Fed has flagged the start of tapering and is expected to clamp down quickly should inflation accelerate; however, maintaining growth is likely to be its main focus. While a degree of tightening appears priced in, U.S. tax increases do not. A proposed hike in corporate tax rates could result in tepid earnings increases for many businesses next year. For this reason, we are focused on high-growth companies that can compound earnings at a higher rate. Opportunities will continue to arise across the tech and healthcare sectors, non-bank financials in certain markets, as well as industrials that may benefit from reshoring, automation and the application of technology to drive efficiency.

Many of the features that make emerging markets attractive will persist well past the impact of COVID-19. In our view, young populations and growing levels of wealth are long-term tailwinds that can help drive consumption and growth, particularly in Asia Pacific, and to a lesser extent Latin America. It is a similar story in China. Regulatory intervention does complicate the environment but cannot detract from China’s ever-increasing scale and global influence. The government is capitalizing on its lead in the global recovery to take steps to rebalance the economy, rein in excess, and address inequality. Where China differs from most is in its ability to take a sledgehammer to issues by acting immediately and unilaterally, rather than building political consensus over time. Across China, we continue to see a broad sweep of companies that have performed well and that have further runway for strong growth. For example, there are opportunities in the healthcare sector, which is on the right side of demographic and wealth trends, as well as the government’s priority to break down historic monopolies and drive more efficient, lower-cost services. Other areas still face competitive headwinds, such as China’s semiconductor manufacturing space. Although China is encouraging more domestic production for home-grown autos and technology, Chinese chip

6

Hardman Johnston International Growth Fund

sophistication still lags best-in-class international competitors by a significant distance. We believe that there are opportunities and ample room to maneuver for international investors who do their homework and adopt a bottom-up approach.

This material represents the manager’s assessment of the portfolio and market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

Fund holdings and/or sector allocations are subject to change at any time and should not be considered recommendations to buy or sell any security. Please see the Schedule of Investments in this report for a complete list of Fund holdings.

Mutual fund investing involves risk, including the loss of principal. Investments in foreign securities involve greater volatility and political, economic, and currency risks and differences in accounting methods. These risks are greater in emerging markets.

The Morgan Stanley Capital International All Country World Index Ex-U.S. (MSCI ACWI Ex-U.S.) is a market-capitalization-weighted index maintained by Morgan Stanley Capital International (MSCI). It is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI ACWI ExU.S. includes both developed and emerging markets.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Must be preceded or accompanied by a prospectus.

The Hardman Johnston International Growth Fund is distributed by Quasar Distributions, LLC.

You cannot invest directly into an index.

7

Hardman Johnston International Growth Fund

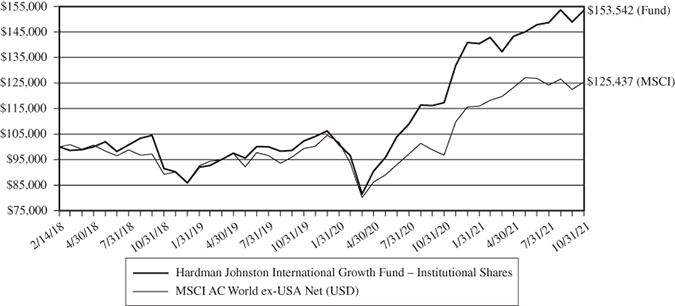

Investment Highlights (Unaudited)

Comparison of the Change in Value of a Hypothetical $100,000 Investment

in the Hardman Johnston International Growth Fund – Institutional Shares and

MSCI AC World ex-USA Net (USD)

| Average Annual Total Return Periods | Since Inception | ||

| Ended October 31, 2021: | 1 Year | 3 Year | (2/14/2018) |

| Hardman Johnston International Growth Fund – | |||

| Institutional Shares | 30.87% | 18.83% | 12.25% |

Retail Shares(1) | 30.45% | 18.90% | 12.26% |

| MSCI AC World ex-USA Net (USD) | 29.66% | 12.00% | 6.30% |

| Expense Ratios*: | Gross 6.49%; Net 1.01% (Institutional Shares); |

| Gross 7.31%; Net 1.26% (Retail Shares) |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-833-627-6668.

This chart illustrates the performance of a hypothetical $100,000 investment made in the Institutional Shares of the Fund on February 14, 2018. Returns reflect the reinvestment of dividends and capital gain distributions. The performance data and expense ratios shown reflect a contractual fee waiver made by the Adviser, currently, through February 28, 2023. In the absence of fee waivers, returns would be reduced. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. This chart does not imply any future performance.

(1) | The inception date of the Retail Shares is September 17, 2018. Performance shown prior to the inception of the Retail Shares reflects the performance of the Institutional Shares and does not include expenses applicable to the Retail Shares, and are higher than, those of the Institutional Shares. The actual annualized performance during the period September 17, 2018 (Retail Share inception) through October 31, 2021 was 13.64% (annualized). |

| * | The expense ratios presented are from the most recent prospectus. |

8

Hardman Johnston International Growth Fund

| SECTOR ALLOCATION OF PORTFOLIO ASSETS |

| at October 31, 2021 (Unaudited) |

| COUNTRY ALLOCATION OF PORTFOLIO ASSETS |

| at October 31, 2021 (Unaudited) |

| United Kingdom | 16.3% |

| Japan | 15.8% |

| Netherlands | 12.2% |

| China | 11.0% |

| France | 6.2% |

| Denmark | 4.9% |

| Germany | 4.8% |

| India | 4.7% |

| Taiwan | 4.4% |

| Italy | 4.1% |

| Norway | 2.2% |

| Hong Kong | 2.1% |

| Ireland | 1.7% |

| Australia | 1.6% |

| Bermuda | 1.4% |

| Short-Term Investments and Other | 6.6% |

Percentages represent market value as a percentage of net assets.

9

Hardman Johnston International Growth Fund

| SCHEDULE OF INVESTMENTS |

| at October 31, 2021 |

| Number of | ||||||||

| COMMON STOCKS – 93.4% | Shares | Value | ||||||

| Communication Services – 2.3% | ||||||||

| Sea Ltd. – ADR (a) | 4,385 | $ | 1,506,554 | |||||

| Consumer Discretionary – 18.3% | ||||||||

| Aptiv Plc – ADR (a) | 21,625 | 3,738,746 | ||||||

| Kering SA | 1,395 | 1,046,999 | ||||||

| Meituan (a) | 29,800 | 1,014,053 | ||||||

| Melco Resorts & Entertainment Ltd. – ADR (a) | 156,060 | 1,690,130 | ||||||

| Prosus NV | 18,320 | 1,613,684 | ||||||

| Puma SE | 23,458 | 2,909,969 | ||||||

| 12,013,581 | ||||||||

| Financials – 6.9% | ||||||||

| AIA Group Ltd. | 123,950 | 1,389,109 | ||||||

| ICICI Bank Ltd. – ADR | 148,440 | 3,139,506 | ||||||

| 4,528,615 | ||||||||

| Health Care – 17.8% | ||||||||

| Alibaba Health Information Technology Ltd. (a) | 739,000 | 925,367 | ||||||

| Alkermes PLC – ADR (a) | 38,040 | 1,152,232 | ||||||

| AstraZeneca PLC | 26,690 | 3,338,957 | ||||||

| Genmab A/S (a) | 7,230 | 3,248,089 | ||||||

| Wuxi Biologics Cayman, Inc. (a) | 200,670 | 3,039,542 | ||||||

| 11,704,187 | ||||||||

| Industrials – 20.9% | ||||||||

| Airbus SE (a) | 24,985 | 3,205,134 | ||||||

| Daifuku Co., Ltd. | 24,925 | 2,294,582 | ||||||

| Nidec Corp. | 22,660 | 2,509,773 | ||||||

| Prysmian SpA | 71,705 | 2,711,106 | ||||||

| Safran SA | 22,695 | 3,054,522 | ||||||

| 13,775,117 | ||||||||

The accompanying notes are an integral part of these financial statements.

10

Hardman Johnston International Growth Fund

| SCHEDULE OF INVESTMENTS (Continued) |

| at October 31, 2021 |

| Number of | ||||||||

| COMMON STOCKS – 93.4% (Continued) | Shares | Value | ||||||

| Information Technology – 27.2% | ||||||||

| Afterpay Ltd. (a) | 10,990 | $ | 1,018,104 | |||||

| ASML Holding NV | 3,950 | 3,210,963 | ||||||

| Atlassian Corp PLC – ADR (a) | 8,009 | 3,669,163 | ||||||

| Keyence Corp. | 5,140 | 3,102,580 | ||||||

| Murata Manufacturing Co., Ltd. | 33,380 | 2,476,081 | ||||||

| Nordic Semiconductor ASA (a) | 48,907 | 1,453,037 | ||||||

| Taiwan Semiconductor Manufacturing Co., Ltd. | 139,000 | 2,949,623 | ||||||

| 17,879,551 | ||||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $52,966,085) | 61,407,605 | |||||||

| SHORT-TERM INVESTMENTS – 6.1% | ||||||||

| MONEY MARKET FUNDS – 6.1% | ||||||||

| First American Government | ||||||||

| Obligations Fund – Class X, 0.03% (b) | 4,008,936 | 4,008,936 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $4,008,936) | 4,008,936 | |||||||

| TOTAL INVESTMENTS | ||||||||

| (Cost $56,975,021) – 99.5% | 65,416,541 | |||||||

| Other Assets in Excess of Liabilities – 0.5% | 323,416 | |||||||

| TOTAL NET ASSETS – 100.00% | $ | 65,739,957 | ||||||

Percentages are stated as a percent of net assets.

ADR – American Depositary Receipt

PLC – Public Limited Company

| (a) | Non-income producing security. |

| (b) | The rate shown represents the fund’s 7-day yield as of October 31, 2021. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bank Global Fund Services.

The accompanying notes are an integral part of these financial statements.

11

Hardman Johnston International Growth Fund

| STATEMENT OF ASSETS AND LIABILITIES |

| at October 31, 2021 |

| Assets: | ||||

| Investments, at value (cost of $56,975,021) | $ | 65,416,541 | ||

| Receivables: | ||||

| Securities sold | 450,697 | |||

| Fund shares sold | 33,244 | |||

| Dividends and interest | 49,914 | |||

| Prepaid expenses | 25,323 | |||

| Total assets | 65,975,719 | |||

| Liabilities: | ||||

| Payables: | ||||

| Securities purchased | 132,075 | |||

| Administration and fund accounting fees | 31,360 | |||

| Advisory Fees | 16,045 | |||

| Custody Fees | 9,238 | |||

| Reports to shareholders | 9,965 | |||

| Transfer agent fees and expenses | 15,848 | |||

| Other accrued expenses | 21,231 | |||

| Total liabilities | 235,762 | |||

| Net assets | $ | 65,739,957 | ||

| Net assets consist of: | ||||

| Paid in capital | $ | 57,269,619 | ||

| Total accumulated earnings | 8,470,338 | |||

| Net assets | $ | 65,739,957 | ||

| Institutional Shares: | ||||

| Net assets applicable to outstanding Institutional Shares | $ | 64,978,575 | ||

| Shares issued (Unlimited number of beneficial | ||||

| interest authorized, $0.01 par value) | 4,469,377 | |||

| Net asset value, offering price and redemption price per share | $ | 14.54 | ||

| Retail Shares: | ||||

| Net assets applicable to outstanding Retail Shares | $ | 761,382 | ||

| Shares issued (Unlimited number of beneficial | ||||

| interest authorized, $0.01 par value) | 49,504 | |||

| Net asset value, offering price and redemption price per share | $ | 15.38 | ||

The accompanying notes are an integral part of these financial statements.

12

Hardman Johnston International Growth Fund

| STATEMENT OF OPERATIONS |

| For the Year Ended October 31, 2021 |

| Investment income: | ||||

| Dividends (net of foreign taxes withheld of $31,306) | $ | 237,111 | ||

| Interest | 485 | |||

| Total investment income | 237,596 | |||

| Expenses: | ||||

| Investment advisory fees (Note 4) | 459,234 | |||

| Administration and fund accounting fees (Note 4) | 126,880 | |||

| Distribution fees (Note 5) | ||||

| Distribution fees – Retail Shares | 1,700 | |||

| Transfer agent fees and expenses | 65,421 | |||

| Federal and state registration fees | 48,835 | |||

| Audit fees | 18,298 | |||

| Compliance expense | 16,010 | |||

| Legal fees | 32,295 | |||

| Reports to shareholders | 10,030 | |||

| Trustees’ fees and expenses | 11,897 | |||

| Custody fees | 64,195 | |||

| Other | 10,928 | |||

| Total expenses before reimbursement from advisor | 865,723 | |||

| Expense reimbursement from advisor (Note 4) | (406,289 | ) | ||

| Net expenses | 459,434 | |||

| Net investment loss | (221,838 | ) | ||

| Realized and unrealized gain (loss) on investments: | ||||

| Net realized gain (loss) on transactions from: | ||||

| Investments | 858,964 | |||

| Foreign currency related transactions | (3,335 | ) | ||

| Net change in unrealized gain (loss) on: | ||||

| Investments | 6,712,828 | |||

| Foreign currency related transactions | (1,815 | ) | ||

| Net realized and unrealized gain on | ||||

| investments and foreign currency | 7,566,642 | |||

| Net increase in net assets resulting from operations | $ | 7,344,804 | ||

The accompanying notes are an integral part of these financial statements.

13

Hardman Johnston International Growth Fund

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Year Ended | |||||||

| October 31, 2021 | October 31, 2020 | |||||||

| Operations: | ||||||||

| Net investment loss | $ | (221,838 | ) | $ | (28,873 | ) | ||

| Net realized gain on investments | ||||||||

| and foreign currency | 855,629 | 794,313 | ||||||

| Net change in unrealized gain on | ||||||||

| investments and foreign currency | 6,711,013 | 773,600 | ||||||

| Net increase in net assets | ||||||||

| resulting from operations | 7,344,804 | 1,539,040 | ||||||

| Distributions to Shareholders From: | ||||||||

| Net investment income | ||||||||

| Investor class shares | — | — | ||||||

| Institutional shares | — | (84,081 | ) | |||||

| Total distributions | — | (84,081 | ) | |||||

| Capital Share Transactions: | ||||||||

| Proceeds from shares sold | ||||||||

| Retail shares | 483,884 | 277,898 | ||||||

| Institutional shares | 42,464,294 | 17,916,065 | ||||||

| Proceeds from shares issued to holders | ||||||||

| in reinvestment of dividends | ||||||||

| Retail shares | — | — | ||||||

| Institutional shares | — | 84,081 | ||||||

| Cost of shares redeemed | ||||||||

| Retail Shares | (186,899 | ) | (2,459,859 | ) | ||||

| Institutional shares | (2,022,130 | ) | (9,164,582 | ) | ||||

| Net increase in net assets | ||||||||

| from capital share transactions | 40,739,149 | 6,653,603 | ||||||

| Total increase in net assets | 48,083,953 | 8,108,562 | ||||||

| Net Assets: | ||||||||

| Beginning of year | 17,656,004 | 9,547,442 | ||||||

| End of year | $ | 65,739,957 | $ | 17,656,004 | ||||

The accompanying notes are an integral part of these financial statements.

14

Hardman Johnston International Growth Fund

| STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| Year Ended | Year Ended | |||||||

| October 31, 2021 | October 31, 2020 | |||||||

| Changes in Shares Outstanding: | ||||||||

| Shares sold | ||||||||

| Retail shares | 34,099 | 23,926 | ||||||

| Institutional shares | 3,057,943 | 1,792,699 | ||||||

| Proceeds from shares issued to holders | ||||||||

| in reinvestment of dividends | ||||||||

| Retail shares | — | — | ||||||

| Institutional shares | — | 8,536 | ||||||

| Shares redeemed | ||||||||

| Retail shares | (12,381 | ) | (239,065 | ) | ||||

| Institutional shares | (147,661 | ) | (932,959 | ) | ||||

| Net increase in shares outstanding | 2,932,000 | 653,137 | ||||||

The accompanying notes are an integral part of these financial statements.

15

Hardman Johnston International Growth Fund

| FINANCIAL HIGHLIGHTS |

For a capital share outstanding throughout each period

Institutional Shares

| February 14, | ||||||||||||||||

| Year Ended | Year Ended | Year Ended | 2018* through | |||||||||||||

| October 31, | October 31, | October 31, | October 31, | |||||||||||||

| 2021 | 2020 | 2019 | 2018 | |||||||||||||

| Net Asset Value – | ||||||||||||||||

| Beginning of Period | $ | 11.11 | $ | 10.23 | $ | 9.15 | $ | 10.00 | ||||||||

| Income from | ||||||||||||||||

| Investment Operations: | ||||||||||||||||

Net investment income/(loss)1 | (0.07 | ) | (0.05 | ) | 0.09 | — | 2 | |||||||||

| Net realized and unrealized | ||||||||||||||||

| gain (loss) on investments | 3.50 | 1.48 | 0.99 | (0.85 | ) | |||||||||||

| Total from investment operations | 3.43 | 1.43 | 1.08 | (0.85 | ) | |||||||||||

| Less Distributions: | ||||||||||||||||

| Dividends from net investment income | — | (0.55 | ) | — | — | |||||||||||

| Total distributions | — | (0.55 | ) | — | — | |||||||||||

| Net Asset Value – End of Period | $ | 14.54 | $ | 11.11 | $ | 10.23 | $ | 9.15 | ||||||||

| Total Return | 30.87 | % | 14.68 | % | 11.80 | % | (8.50 | )%^ | ||||||||

| Ratios and Supplemental Data: | ||||||||||||||||

| Net assets, end of | ||||||||||||||||

| period (thousands) | $ | 64,979 | $ | 17,329 | $ | 7,069 | $ | 9,580 | ||||||||

| Ratio of operating expenses | ||||||||||||||||

| to average net assets: | ||||||||||||||||

| Before reimbursements | 1.88 | % | 6.48 | % | 4.57 | % | 11.31 | %+ | ||||||||

| After reimbursements | 1.00 | % | 1.00 | % | 1.00 | % | 1.00 | %+ | ||||||||

| Ratio of net investment income | ||||||||||||||||

| to average net assets: | ||||||||||||||||

| Before reimbursements | (1.36 | )% | (5.94 | )% | (2.63 | )% | (10.25 | )%+ | ||||||||

| After reimbursements | (0.48 | )% | (0.46 | )% | 0.94 | % | 0.06 | %+ | ||||||||

Portfolio turnover rate3 | 46 | % | 224 | % | 81 | % | 53 | %^ | ||||||||

| * | Commencement of operations for Institutional Shares was February 14, 2018. |

+ | Annualized |

| ^ | Not Annualized |

1 | The net investment income per share was calculated using the average shares outstanding method. |

2 | Amount is less than $0.01 per share. |

3 | Portfolio turnover was calculated on the basis of the Fund as a whole. |

The accompanying notes are an integral part of these financial statements.

16

Hardman Johnston International Growth Fund

| FINANCIAL HIGHLIGHTS |

For a capital share outstanding throughout each period

Retail Shares

| September 17, | ||||||||||||||||

| Year Ended | Year Ended | Year Ended | 2018* through | |||||||||||||

| October 31, | October 31, | October 31, | October 31, | |||||||||||||

| 2021 | 2020 | 2019 | 2018 | |||||||||||||

| Net Asset Value – | ||||||||||||||||

| Beginning of Period | $ | 11.79 | $ | 10.20 | $ | 9.15 | $ | 10.32 | ||||||||

| Income from | ||||||||||||||||

| Investment Operations: | ||||||||||||||||

Net investment income/(loss)1 | (0.11 | ) | (0.08 | ) | 0.07 | (0.01 | ) | |||||||||

| Net realized and unrealized | ||||||||||||||||

| gain (loss) on investments | 3.70 | 1.67 | 0.98 | (1.16 | ) | |||||||||||

| Total from investment operations | 3.59 | 1.59 | 1.05 | (1.17 | ) | |||||||||||

| Net Asset Value – End of Period | $ | 15.38 | $ | 11.79 | $ | 10.20 | $ | 9.15 | ||||||||

| Total Return | 30.45 | % | 15.59 | % | 11.48 | % | (11.34 | )%^ | ||||||||

| Ratios and Supplemental Data: | ||||||||||||||||

| Net assets, end of period (thousands) | $ | 761 | $ | 327 | $ | 2,479 | $ | 2,390 | ||||||||

| Ratio of operating expenses | ||||||||||||||||

| to average net assets: | ||||||||||||||||

| Before reimbursements | 2.18 | % | 7.30 | % | 4.88 | % | 4.43 | %+ | ||||||||

| After reimbursements | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | %+ | ||||||||

| Ratio of net investment income | ||||||||||||||||

| to average net assets: | ||||||||||||||||

| Before reimbursements | (1.68 | )% | (6.84 | )% | (2.87 | )% | (3.99 | )%+ | ||||||||

| After reimbursements | (0.75 | )% | (0.79 | )% | 0.76 | % | (0.81 | )%+ | ||||||||

Portfolio turnover rate2 | 46 | % | 224 | % | 81 | % | 53 | %^ | ||||||||

| * | Commencement of operations for Retail Shares was September 17, 2018. |

+ | Annualized |

| ^ | Not Annualized |

1 | The net investment income/(loss) per share was calculated using the average shares outstanding method. |

2 | Portfolio turnover was calculated on the basis of the Fund as a whole. |

The accompanying notes are an integral part of these financial statements.

17

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS |

| at October 31, 2021 |

NOTE 1 – ORGANIZATION

The Hardman Johnston International Growth Fund (the “Fund”) is a series of Manager Directed Portfolios (the “Trust”). The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and was organized as a Delaware statutory trust on April 4, 2006. The Fund is an open-end investment management company and is a non-diversified series of the Trust. The Fund’s Institutional Shares commenced operations on February 14, 2018. The Fund’s Retail Shares commenced operations on September 17, 2018. Each class of shares differs principally in its respective distribution expenses. Each class of shares has identical rights to earnings, assets and voting privileges, except for class-specific expenses and exclusive rights to vote on matters affecting only individual classes. Dakota Investments LLC (the “Advisor”) serves as the investment advisor to the Fund. Hardman Johnston Global Advisors LLC (the “Sub-Advisor”) serves as the sub-advisor to the Fund. Redwood Investments, LLC (“Redwood”) served as the International Growth Fund’s sub-advisor from the Fund’s inception to December 31, 2019. Effective January 1, 2020, Hardman Johnston replaced Redwood as the International Growth Fund’s sub-advisor. As an investment company, the Fund follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services – Investment Companies. The investment objective of the Fund is to seek long term capital appreciation.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund. These policies are in conformity with U.S. generally accepted accounting principles (“GAAP”).

| A. | Security Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3. | |

| B. | Federal Income Taxes: It is the Fund’s policy to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Therefore, no federal income or excise tax provisions are required. | |

| The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions to be taken or expected to be taken on a tax return. The tax returns for the Fund for the prior three fiscal years are open for examination. The Fund identifies its major tax jurisdictions as U.S. Federal and the state of Delaware. | ||

| C. | Securities Transactions, Income and Distributions: Securities transactions are accounted for on the trade date. Realized gains and losses on securities sold are |

18

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

| determined on the basis of identified cost. Interest income is recorded on an accrual basis. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Discounts and premiums on fixed income securities are amortized using the effective interest method. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. | ||

| The Fund distributes substantially all of its net investment income, if any, and net realized capital gains, if any, annually. Distributions from net realized gains for book purposes may include short-term capital gains. All short-term capital gains are included in ordinary income for tax purposes. The amount of dividends and distributions to shareholders from net investment income and net realized capital gains is determined in accordance with federal income tax regulations, which differ from GAAP. To the extent these book/tax differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax treatment. | ||

| The Fund is charged for those expenses that are directly attributable to it, such as investment advisory, custody and transfer agent fees. Expenses that are not attributable to a Fund are typically allocated among the funds in the Trust proportionately based on allocation methods approved by the Board of Trustees (the “Board”). Common expenses of the Trust are typically allocated among the funds in the Trust based on a fund’s respective net assets, or by other equitable means. | ||

| D. | Use of Estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets during the reporting period. Actual results could differ from those estimates. | |

| E. | Redemption Fees: The Fund does not charge redemption fees to shareholders. | |

| F. | Reclassification of Capital Accounts: GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. | |

| G. | Foreign Currency: Values of investments denominated in foreign currencies are converted into U.S. dollars using the spot market rate of exchange at the time of valuation. Purchases and sales of investments and income are translated into U.S. dollars using the spot market rate of exchange prevailing on the respective dates of such transactions. The Fund does not isolate the portion of the results of operations resulting from fluctuations in foreign exchange rates on investments from fluctuations resulting from changes in the market prices of securities held. Such fluctuations are included with the net realized and unrealized gain/loss on investments. Foreign investments present additional risks due to currency fluctuations, economic and political factors, lower liquidity, government regulations, differences in accounting standards, and other factors. |

19

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

| H. | Events Subsequent to the Fiscal Year End: In preparing the financial statements as of October 31, 2021 and through the date the financial statements were available to be issued, management considered the impact of subsequent events for potential recognition or disclosure in the financial statements and had concluded that no additional disclosures are necessary. | |

| I. | Recent Accounting Pronouncements and Rule Issuances: In October 2020, the SEC adopted new regulations governing the use of derivatives by registered investment companies (“Rule 18f-4”). Rule 18f-4 will impose limits on the amount of derivatives a Fund can enter into, eliminate the asset segregation framework currently used by funds to comply with Section 18 of the 1940 Act, and require funds whose use of derivatives is greater than a limited specified amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. Funds will be required to comply with Rule 18f-4 by August 19, 2022. It is not currently clear what impact, if any, Rule 18f-4 will have on the availability, liquidity or performance of derivatives. Management is currently evaluating the potential impact of Rule 18f-4 on the Fund. When fully implemented, Rule 18f-4 may require changes in how a Fund uses derivatives, adversely affect the Fund’s performance and increase costs related to the Fund’s use of derivatives. | |

| In December 2020, the SEC adopted a new rule providing a framework for fund valuation practices (“Rule 2a-5”). Rule 2a-5 establishes requirements for determining fair value in good faith for purposes of the 1940 Act. Rule 2a-5 will permit fund boards to designate certain parties to perform fair value determinations, subject to board oversight and certain other conditions. Rule 2a-5 also defines when market quotations are “readily available” for purposes of the 1940 Act and the threshold for determining whether a fund must fair value a security. In connection with Rule 2a-5, the SEC also adopted related recordkeeping requirements and is rescinding previously issued guidance, including with respect to the role of a board in determining fair value and the accounting and auditing of fund investments. The Funds will be required to comply with the rules by September 8, 2022. Management is currently assessing the potential impact of the new rules on the Funds’ financial statements. |

NOTE 3 – SECURITIES VALUATION

The Fund has adopted authoritative fair value accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion of changes in valuation techniques and related inputs during the period, and expanded disclosure of valuation levels for major security types. These inputs are summarized in the three broad levels listed below:

20

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

| Level 1 – | Unadjusted, quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the date of measurement. | |

| Level 2 – | Other significant observable inputs (including, but not limited to, quoted prices in active markets for similar instruments, quoted prices in markets that are not active for identical or similar instruments, and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets, such as interest rates, prepayment speeds, credit risk curves, default rates, and similar data). | |

| Level 3 – | Significant unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

Following is a description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis.

Equity Securities: Equity securities, including common stocks, preferred stocks, foreign-issued common stocks, exchange-traded funds, closed-end mutual funds and real estate investment trusts (REITs), that are primarily traded on a national securities exchange shall be valued at the last sale price on the exchange on which they are primarily traded on the day of valuation or, if there has been no sale on such day, at the mean between the bid and asked prices. Securities primarily traded in the NASDAQ Global Market System for which market quotations are readily available shall be valued using the NASDAQ Official Closing Price (“NOCP”). If the NOCP is not available, such securities shall be valued at the last sale price on the day of valuation, or if there has been no sale on such day, at the mean between the bid and asked prices. Over-the-counter securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter market. Over-the-counter securities which are not traded in the NASDAQ Global Market System shall be valued at the mean between the bid and asked prices. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy. Securities traded on foreign exchanges generally are not valued at the same time the Fund calculates its net asset value (“NAV”) because most foreign markets close well before such time. The earlier close of most foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim. In certain circumstances, it may be determined that a security needs to be fair valued because it appears that the value of the security might have been materially affected by an event (a “Significant Event”) occurring after the close of the market in which the security is principally traded, but before the time the Fund calculates its NAV. A Significant Event may relate to a single issuer or to an entire market sector, or even occurrences not tied directly to the securities markets, such as natural disasters, armed conflicts, or significant government actions.

21

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

Registered Investment Companies: Investments in registered investment companies (e.g., mutual funds) are generally priced at the ending NAV provided by the applicable registered investment company’s service agent and will be classified in Level 1 of the fair value hierarchy.

Short-Term Debt Securities: Debt securities, including short-term debt instruments having a maturity of less than 60 days, are valued at the evaluated mean price supplied by an approved pricing service. Pricing services may use various valuation methodologies including matrix pricing and other analytical pricing models as well as market transactions and dealer quotations. In the absence of prices from a pricing service, the securities will be priced in accordance with the procedures adopted by the Board. Short-term securities are generally classified in Level 1 or Level 2 of the fair market hierarchy depending on the inputs used and market activity levels for specific securities.

The Board has delegated day-to-day valuation issues to a Valuation Committee of the Trust which, as of October 31, 2021, was comprised of officers of the Trust. The function of the Valuation Committee is to value securities where current and reliable market quotations are not readily available, or the closing price does not represent fair value, by following procedures approved by the Board. These procedures consider many factors, including the type of security, size of holding, trading volume, news events and significant events such as those described previously. All actions taken by the Valuation Committee are subsequently reviewed and ratified by the Board.

Depending on the relative significance of the valuation inputs, fair valued securities may be classified in either level 2 or level 3 of the fair value hierarchy.

The fair valuation of foreign securities may be determined with the assistance of a pricing service using correlations between the movement of prices of such securities and indices of domestic securities and other appropriate indicators, such as closing market prices of relevant American Depositary Receipts or futures contracts. The Fund uses ICE Data Services (“ICE”) as a third-party fair valuation vendor. ICE provides a fair value for foreign securities in the Fund based on certain factors and methodologies applied by ICE in the event that there is a movement in the U.S. markets that exceeds a specific threshold established by the Valuation Committee. The effect of using fair value pricing is that the Fund’s NAV will reflect the affected portfolio securities’ values as determined by the Board or its designee instead of being determined by the market. Using a fair value pricing methodology to price a foreign security may result in a value that is different from the foreign security’s most recent closing price and from the prices used by other investment companies to calculate their NAVs and are generally classified in Level 2 of the fair valuation hierarchy. Because the Fund may invest in foreign securities, the value of the Fund’s portfolio securities may change on days when you will not be able to purchase or redeem your shares.

22

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the fair valuation hierarchy of the Fund’s securities as of October 31, 2021:

| Common Stocks | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Communication Services | $ | 1,506,554 | $ | — | $ | — | $ | 1,506,554 | ||||||||

| Consumer Discretionary | 5,428,876 | 6,584,705 | — | 12,013,581 | ||||||||||||

| Financials | 3,139,506 | 1,389,109 | — | 4,528,615 | ||||||||||||

| Health Care | 1,152,232 | 10,551,955 | — | 11,704,187 | ||||||||||||

| Industrials | — | 13,775,117 | — | 13,775,117 | ||||||||||||

| Information Technology | 3,669,163 | 14,210,388 | — | 17,879,551 | ||||||||||||

| Total Common Stocks | 14,896,331 | 46,511,274 | — | 61,407,605 | ||||||||||||

| Short-Term Investments | 4,008,936 | — | — | 4,008,936 | ||||||||||||

| Total Investments in Securities | $ | 18,905,267 | $ | 46,511,274 | $ | — | $ | 65,416,541 | ||||||||

NOTE 4 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

For the year ended October 31, 2021, the Advisor provided the Fund with investment management services under an Investment Advisory Agreement. The Advisor furnishes all investment advice, office space, and facilities, and provides most of the personnel needed by the Fund. As compensation for its services, the Advisor is entitled to a monthly fee at an annual rate of 1.00% of the average daily net assets of the Fund. For the year ended October 31, 2021, the Fund incurred $459,234 in advisory fees. The Advisor has hired Hardman Johnston Global Advisors LLC as a sub-advisor to the Fund. The Advisor pays the Sub-Advisor fee for the Fund from its own assets and these fees are not an additional expense of the Fund.

The Fund is responsible for its own operating expenses. The Advisor has contractually agreed to waive its management fees and/or absorb expenses of the Fund to ensure that the total annual operating expenses [excluding Acquired Fund Fees and Expenses, taxes, brokerage commissions, interest and extraordinary expenses (collectively, “Excludable Expenses”)] do not exceed the following amounts of the average daily net assets for each class of shares:

| Hardman Johnston International Growth Fund | |||

| Institutional Shares | 1.00% | ||

| Retail Shares | 1.25% | ||

For the year ended October 31, 2021, the Advisor reduced its fees and absorbed Fund expenses in the amount of $406,289 for the Fund. The waivers and reimbursements will remain in effect through February 28, 2023 unless terminated sooner by, or with the consent of, the Board.

The Advisor may request recoupment of previously waived fees and paid expenses in any subsequent month in the three-year period from the date of the management fee

23

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

reduction and expense payment if the aggregate amount actually paid by the Fund toward the operating expenses for such fiscal year (taking into account the reimbursement) will not cause the Fund to exceed the lesser of: (1) the expense limitation in place at the time of the management fee reduction and expense payment; or (2) the expense limitation in place at the time of the reimbursement. Any such reimbursement is also contingent upon Board of Trustees review and approval at the time the reimbursement is made. Such reimbursement may not be paid prior to the Fund’s payment of current ordinary operating expenses. Cumulative expenses subject to recapture pursuant to the aforementioned conditions expire as follows:

10/31/2022 | 10/31/2023 | 10/31/2024 | Total | ||

| $346,262 | $332,022 | $406,289 | $1,084,573 |

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services, LLC (“Fund Services” or the “Administrator”) acts as the Fund’s Administrator under an Administration Agreement. The Administrator prepares various federal and state regulatory filings, reports and returns for the Fund; prepares reports and materials to be supplied to the Trustees; monitors the activities of the Fund’s custodian, transfer agent and accountants; coordinates the preparation and payment of the Fund’s expenses and reviews the Fund’s expense accruals. Fund Services also serves as the fund accountant and transfer agent to the Fund. Vigilant Compliance, LLC serves as the Chief Compliance Officer to the Fund. U.S. Bank N.A., an affiliate of Fund Services, serves as the Fund’s custodian. For the year ended October 31, 2021, the Fund incurred the following expenses for administration, fund accounting, transfer agency and custody fees:

| Administration & fund accounting | $126,880 | ||

| Custody | $ 64,195 | ||

Transfer agency(a) | $ 45,625 | ||

(a) Does not include out-of-pocket expenses. |

At October 31, 2021, the Fund had payables due to Fund Services for administration, fund accounting and transfer agency fees and to U.S. Bank N.A. for custody fees in the following amounts:

| Administration & fund accounting | $31,360 | ||

| Custody | $ 9,238 | ||

Transfer agency(a) | $11,315 | ||

(a) Does not include out-of-pocket expenses. |

Quasar Distributors, LLC (the “Distributor”) acts as the Fund’s principal underwriter in a continuous public offering of the Fund’s shares. On July 7, 2021, Foreside Financial Group, LLC (“Foreside”), the parent company of Quasar Distributors, LLC (“Quasar”), the Fund’s distributor, announced that it had entered into a definitive purchase and sale agreement with Genstar Capital (“Genstar”) such that Genstar would acquire a majority stake in Foreside. The transaction closed at the end of the third quarter of 2021. Quasar will remain the Fund’s distributor.

24

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

Certain officers of the Fund are employees of the Administrator and are not paid any fees by the Fund for serving in such capacities.

NOTE 5 – DISTRIBUTION AGREEMENT AND PLAN

The Fund has adopted a Distribution Plan pursuant to Rule 12b-1 (the “Plan”). The Plan permits the Fund to pay for distribution and related expenses at an annual rate of up to 0.25% of the average daily net assets of the Fund’s Retail Shares. The expenses covered by the Plan may include costs in connection with the promotion and distribution of shares and the provision of personal services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, and the printing and mailing of sales literature. Payments made pursuant to the Plan will represent compensation for distribution and service activities, not reimbursements for specific expenses incurred. For the year ended October 31, 2021, the Hardman Johnston International Growth Fund incurred distribution expenses on its Retail Shares of $1,700.

NOTE 6 – SECURITIES TRANSACTIONS

For the year ended October 31, 2021, the cost of purchases and the proceeds from sales of securities, excluding short-term securities, were as follows:

Purchases | Sales | ||

| International Growth Fund | $60,095,984 | $20,355,254 |

There were no purchases or sales of long-term U.S. Government securities.

NOTE 7 – INCOME TAXES AND DISTRIBUTIONS TO SHAREHOLDERS

As of October 31, 2021, the components of accumulated earnings/(losses) on a tax basis were as follows:

Cost of investments(a) | $ | 57,384,994 | |||

| Gross unrealized appreciation | 11,667,886 | ||||

| Gross unrealized depreciation | (3,636,339 | ) | |||

| Net unrealized appreciation | 8,031,547 | ||||

| Undistributed ordinary income | — | ||||

| Undistributed long-term capital gain | 686,288 | ||||

| Total distributable earnings | 686,288 | ||||

| Other accumulated gains/(losses) | (247,497 | ) | |||

| Total accumulated earnings/(losses) | $ | 8,470,338 |

(a) | The difference between the book basis and tax basis net unrealized appreciation and cost is attributable primarily to wash sales, and the mark-to-market of passive foreign investment companies. |

As of October 31, 2021, the Fund had no long-term or short-term tax basis loss carryforwards.

25

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

At October 31, 2021, the Fund deferred, on a tax basis, post-October losses of:

Capital | Ordinary Late Year Loss | |

| $ — | $246,554 |

The tax character of distributions paid during the year ended October 31, 2021 and the year ended October 31, 2020 was as follows:

| Year Ended | Year Ended | ||||||||

| October 31, 2021 | October 31, 2020 | ||||||||

| Ordinary income | $ | — | $ | 84,081 | |||||

| Long-term capital gains | — | — | |||||||

| $ | — | $ | 84,081 | ||||||

NOTE 8 – PRINCIPAL RISKS

Below are summaries of some, but not all, of the principal risks of investing in the Fund, each of which could adversely affect the Fund’s NAV, market price, yield, and total return. Further information about investment risks is available in the Fund’s prospectus and Statement of Additional Information.

Equity Market Risk: Equity securities are susceptible to general stock market fluctuations due to economic, market, political and issuer-specific considerations and to potential volatile increases and decreases in value as market confidence in and perceptions of their issuers change.

Foreign Securities and Currency Risk: Foreign securities are subject to risks relating to political, social and economic developments abroad and differences between U.S. and foreign regulatory requirements and market practices. Those risks are increased for investments in emerging markets. Securities that are denominated in foreign currencies are subject to further risk that the value of the foreign currency will fall in relation to the U.S. dollar and/or will be affected by volatile currency markets or actions of U.S. and foreign governments or central banks. Income earned on foreign securities may be subject to foreign withholding taxes.

Management Risk: The ability of the Fund to meet its investment objective is directly related to the Advisor’s and Sub-Advisor’s management of the Fund. The value of your investment in the Fund may vary with the effectiveness of the Advisor’s research, analysis and asset allocation among portfolio securities. If the investment strategies do not produce the expected results, the value of your investment could be diminished or even lost entirely.

General Market Risk; Recent Market Events: The value of the Fund’s shares will fluctuate based on the performance of the Fund’s investments and other factors affecting the securities markets generally. Certain investments selected for the Fund’s portfolio may be worth less than the price originally paid for them, or less than they were worth at an earlier time. The value of the Fund’s investments may go up or down, sometimes

26

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

dramatically and unpredictably, based on current market conditions, such as real or perceived adverse political or economic conditions, inflation, changes in interest rates, lack of liquidity in the fixed income markets or adverse investor sentiment.

U.S. and international markets have experienced volatility in recent months and years due to a number of economic, political and global macro factors, including the impact of the coronavirus (COVID-19) global pandemic, which has resulted in a public health crisis, business interruptions, growth concerns in the U.S. and overseas, layoffs, rising unemployment claims, changed travel and social behaviors and reduced consumer spending. The effects of COVID-19 may lead to a substantial economic downturn or recession in the U.S. and global economies, the recovery from which is uncertain and may last for an extended period of time.

New Fund Risk: There can be no assurance that the Fund will grow to or maintain an economically viable size, in which case the Board may determine to liquidate the Fund. Liquidation of the Fund can be initiated without shareholder approval by the Board if it determines that liquidation is in the best interest of shareholders. As a result, the timing of the Fund’s liquidation may not be favorable.

Emerging and Frontier Markets Risk: Countries in emerging markets are generally more volatile and can have relatively unstable governments, social and legal systems that do not protect shareholders, economies based on only a few industries, and securities markets that trade a small number of issues. Frontier market countries generally have smaller economies and even less developed capital markets than emerging markets. As a result, the risks of investing in emerging markets are magnified in frontier markets, and include potential for extreme price volatility and illiquidity; government ownership or control of parts of private sector and of certain companies; trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures; and relatively new and unsettled securities laws.

Large Capitalization Risk: Larger, more established companies may be unable to respond quickly to new competitive challenges such as changes in technology and consumer tastes. Larger companies also may not be able to attain the high growth rates of successful smaller companies.

Medium and Small Capitalization Risk: Investing in medium and small capitalization companies may involve special risks because those companies may have narrower product lines, more limited financial resources, fewer experienced managers, dependence on a few key employees, and a more limited trading market for their stocks, as compared with larger companies. Securities of medium and smaller capitalization issuers may be subject to greater price volatility and may decline more significantly in market downturns than securities of larger companies.

27

Hardman Johnston International Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at October 31, 2021 |

NOTE 9 – GUARANTEES AND INDEMNIFICATIONS

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

NOTE 10 – CONTROL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of the fund, under Section 2(a)(9) of the 1940 Act. As of October 31, 2021, TD Ameritrade Inc. held 21% of the outstanding shares of the Fund, Charles Schwab & Co. Inc. held 56% of the outstanding shares of the Fund and National Financial Services held 16% of the outstanding shares of the Fund. The Fund has no knowledge as to whether all or any portion of the shares owned of record by TD Ameritrade Inc., Charles Schwab & Co. Inc. or National Financial Services are also beneficially owned.

28

Hardman Johnston International Growth Fund

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Board of Trustees of Manager Directed Portfolios

and the Shareholders of Hardman Johnston International Growth Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Hardman Johnston International Growth Fund, a series of shares of beneficial interest in Manager Directed Portfolios (the “Fund”), including the schedule of investments, as of October 31, 2021, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the three-year period then ended and for the period from commencement of operations (February 14, 2018 for Institutional Shares and September 17, 2018 for Retail Shares) to October 31, 2018, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of October 31, 2021, and the results of its operations, the changes in its net assets and its financial highlights for the periods presented above, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2021 by correspondence with the custodian, brokers, or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Manager Directed Portfolios since 2007.

Philadelphia, Pennsylvania

December 28, 2021

29

Hardman Johnston International Growth Fund

| EXPENSE EXAMPLE |

| October 31, 2021 (Unaudited) |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs including sales charges (loads) and redemption fees, if applicable; and (2) ongoing costs, including management fees; distribution and/or service (12b-1 fees); and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period indicated and held for the entire period from May 1, 2021 to October 31, 2021 for the Institutional and Retail Shares.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the row entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. There are some account fees that are charged to certain types of accounts, such as Individual Retirement Accounts (generally, a $15 fee is charged to the account annually) that would increase the amount of expenses paid on your account. The example below does not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under generally accepted accounting principles.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. As noted above, there are some account fees that are charged to certain types of accounts that would increase the amount of expense paid on your account.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the information under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

30

Hardman Johnston International Growth Fund

| EXPENSE EXAMPLE (Continued) |

| April 30, 2021 (Unaudited) |

| Beginning | Ending | Expenses Paid | |

| Account Value | Account Value | During Period(1) | |

5/1/21 | 10/31/21 | 5/1/21 – 10/31/21 | |

| Actual | |||

| Institutional Shares | $1,000.00 | $1,071.50 | $5.22 |

| Retail Shares | $1,000.00 | $1,069.50 | $6.52 |

| Hypothetical (5% return | |||

| before expenses) | |||

| Institutional Shares | $1,000.00 | $1,020.16 | $5.09 |

| Retail Shares | $1,000.00 | $1,018.90 | $6.36 |

(1) | Expenses are equal to the Institutional and Retail Shares’ annualized expense ratio of 1.00% and 1.25%, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the period). |

31

Hardman Johnston International Growth Fund

| NOTICE TO SHAREHOLDERS |

| at April 30, 2021 (Unaudited) |

How to Obtain a Copy of the Fund’s Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-833-627-6668 or on the U.S. Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

How to Obtain a Copy of the Fund’s Proxy Voting Records for the most recent 12-Month Period Ended June 30

Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available no later than August 31 without charge, upon request, by 1-833-627-6668. Furthermore, you can obtain the Fund’s proxy voting records on the SEC’s website at http://www.sec.gov.

Quarterly Filings on Form N-PORT

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Part F of Form N-PORT. The Fund’s Part F of Form N-PORT is available on the SEC’s website at http://www.sec.gov. Information included in the Fund’s Part F of Form N-PORT is also available, upon request, by calling 1-833-627-6668.

Householding

In an effort to decrease costs, the Fund intends to reduce the number of duplicate prospectuses and annual and semi-annual reports you receive by sending only one copy of each to those addresses shared by two or more accounts and to shareholders the Transfer Agent reasonably believes are from the same family or household. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 1-833-627-6668 to request individual copies of these documents. Once the Transfer Agent receives notice to stop householding, the Transfer Agent will begin sending individual copies thirty days after receiving your request. This policy does not apply to account statements.

32

Hardman Johnston International Growth Fund

| STATEMENT REGARDING LIQUIDITY RISK MANAGEMENT PROGRAM |

In accordance with Rule 22e-4 under the Investment Company Act of 1940, as amended, the Fund, a series of Manager Directed Portfolios (the “Trust”), has adopted and implemented a liquidity risk management program tailored specifically to the Fund (the “Program”). The Program seeks to promote effective liquidity risk management for the Fund and to protect Fund shareholders from dilution of their interests. The Board has designated the Fund’s investment adviser to serve as the administrator of the Program (the “Program Administrator”). Personnel of the Fund’s investment adviser conduct the day-to-day operation of the Program pursuant to policies and procedures administered by the Program Administrator. The Program Administrator is required to provide a written annual report to the Board and the chief compliance officer of the Trust regarding the adequacy and effectiveness of the Program, including the operation of the Fund’s highly liquid investment minimum, and any material changes to the Program.

Under the Program, the Program Administrator manages the Fund’s liquidity risk, which is the risk that the Fund could not meet shareholder redemption requests without significant dilution of remaining shareholders’ interests in the Fund. The Program assesses liquidity risk under both normal and reasonably foreseeable stressed market conditions. This risk is managed by monitoring the degree of liquidity of the Fund’s investments, limiting the amount of the Fund’s illiquid investments, and utilizing various risk management tools and facilities available to the Fund for meeting shareholder redemptions, among other means. The Program Administrator’s process of determining the degree of liquidity of the Fund’s investments is supported by one or more third-party liquidity assessment vendors.