Table of Contents

As filed with the Securities and Exchange Commission on October 25, 2007

Registration No. 333-144942

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

INTCOMEX, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 5045 | 65-0893400 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Intcomex, Inc. 3505 NW 107th Avenue

Miami, Florida 33178

(305) 477-6230

(Address including zip code, telephone number, including area code, of Registrant’s Principal Executive Offices)

Michael Shalom

Intcomex, Inc.

3505 NW 107th Avenue

Miami, Florida 33178

(305) 477-6230

(Name, address including zip code, telephone number, including area code, of agent for service)

Copies To:

Jeffrey D. Karpf, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 Telephone: (212) 225-2000 Telecopy: (212) 225-3999 | David Lefkowitz, Esq. Erika L. Weinberg, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, New York 10153 Telephone: (212) 310-8000 Telecopy: (212) 310-8007 |

Approximate date of commencement of proposed sale to the public:As soon as practicable after the effective date hereof.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 25, 2007.

P R O S P E C T U S

[LOGO]

Shares

Intcomex, Inc.

Common Stock

$ per share

We are selling shares of our common stock and the selling stockholder named in this prospectus is selling shares. We will not receive any proceeds from the sale of the shares by the selling stockholder. We and the selling stockholder have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

This is the initial public offering of our common stock. We currently expect the initial public offering price to be between $ and $ per share. We have applied to have the common stock listed on the Nasdaq Global Market under the symbol “ICMX.”

An affiliate of Citigroup Global Markets Inc., one of the underwriters in this offering, is the selling stockholder in this offering. The selling stockholder currently owns approximately % of our common stock on a fully diluted basis and will own approximately % of our common stock upon the completion of this offering (assuming the underwriters’ over-allotment option is not exercised). As a result of the selling stockholder’s current ownership interest in us, this offering is being conducted in accordance with the applicable provisions of the National Association of Securities Dealers, Inc. Conduct Rules. These rules require, among other things, that the initial public offering price of the common stock be no higher than that recommended by a “qualified independent underwriter” (as such term is defined by the rules). UBS Securities LLC is assuming the responsibilities of acting as the qualified independent underwriter in this offering.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 11.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

Public offering price | $ | $ | ||||

Underwriting discount | $ | $ | ||||

Proceeds to Intcomex, Inc. (before expenses) | $ | $ | ||||

Proceeds to the selling stockholder (before expenses) | $ | $ | ||||

The underwriters expect to deliver the shares to purchasers on or about , 2007.

| Citi | UBS Investment Bank |

Banc of America Securities LLC

Raymond James

Broadpoint.

, 2007

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any state where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

| Page | ||

| 1 | ||

| 11 | ||

| 25 | ||

| 26 | ||

| 27 | ||

| 28 | ||

| 30 | ||

| 31 | ||

Management’s Discussion and Analysis of Financial Condition | 33 | |

| 53 | ||

| 69 | ||

| 76 | ||

| 78 | ||

| 80 | ||

| 83 | ||

Certain United States Tax Consequences to Non-United States Holders | 87 | |

| 89 | ||

| 90 | ||

| 94 | ||

| 94 | ||

| 94 | ||

| 95 | ||

| 95 | ||

| F-1 | ||

Until , 2007 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. It does not contain all of the information that may be important to you. You should read the following summary together with the more detailed information regarding our company, the common stock offered and our audited and unaudited consolidated financial statements, including the notes to those statements, appearing elsewhere in this prospectus, before making an investment decision. Except as the context otherwise requires, all references in this prospectus to “Intcomex,” “we,” “us,” “our,” “our company” and similar terms refer to Intcomex, Inc. together with our consolidated subsidiaries and our predecessor companies.

Our Company

We believe we are the largest pure play value-added distributor of information technology, or IT, products focused solely on serving Latin America and the Caribbean. We distribute computer components, peripherals, software, computer systems, accessories, networking products and digital consumer electronics to more than 40,000 customers in 45 countries. We offer single source purchasing to our customers by providing an in-stock selection of more than 5,700 products from over 220 vendors, including many of the world’s leading IT product manufacturers.

Over the last 18 years, we have built an IT products distribution network in Latin America and the Caribbean that we believe is unmatched by any of our competitors in terms of the number of countries served through an in-country presence. We have achieved our regional market leadership position by offering our customers a wide and readily available product selection and excellent pre- and post-sale customer service, while providing our vendors with a multi-country distribution channel for their products. We believe our broad regional presence makes us more attractive to our vendors and customers, thereby enhancing our revenue growth and operating margins, and our geographic diversification reduces our operating risks.

We believe we have the broadest in-country presence of any distributor of IT products to Latin America and the Caribbean, in terms of the number of countries served through an in-country presence. From our headquarters and main distribution center in Miami, we support a network of in-country sales and distribution operations in 12 countries in Latin America and the Caribbean and a sales office in Brazil. As a result of our unique distribution platform, we have realized consistent organic revenue growth and strong operating margins. From 2001 to 2006, our revenue grew from $324.1 million to $889.8 million, representing a compound annual growth rate, or CAGR, of 22.4%, and our operating income grew from $11.2 million to $34.6 million, representing a CAGR of 25.2%. We believe these growth rates and our operating margins are higher than those of our public company competitors.

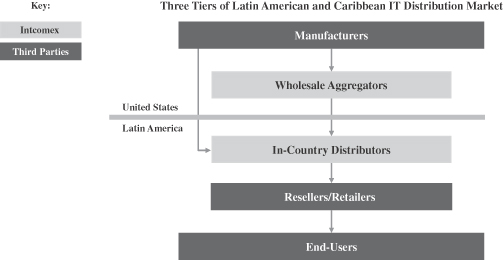

We serve the Latin American and Caribbean IT products markets using a dual distribution model:

| • | As a Miami-based wholesale aggregator, we sell primarily to: |

| - | third-party distributors, resellers and retailers of IT products based in countries in Latin America and the Caribbean where we do not have a local presence; |

| - | third-party distributors, resellers and retailers of IT products based in countries in Latin America and the Caribbean where we have a local presence but whose volumes are large enough to enable them to efficiently acquire products directly from U.S.-based wholesale aggregators; |

| - | other Miami-based exporters of IT products to Latin America and the Caribbean; and |

| - | our in-country operations. |

1

Table of Contents

For the six months ended June 30, 2007, revenue and operating income from our Miami operations (net of $148.7 million of revenue derived from sales to our in-country operations) were $146.6 million and $1.6 million, representing 29.4% and 12.3% of our consolidated revenue and operating income, respectively. For the year ended December 31, 2006, revenue and operating income from our Miami operations (net of $267.1 million of revenue derived from sales to our in-country operations) were $266.8 million and $13.0 million, representing 30.0% and 37.7% of our consolidated revenue and operating income, respectively.

| • | As an in-country distributor in 12 countries, we currently sell to over 40,000 local reseller and retailer customers, including value-added resellers (companies that sell, install and support IT products and personal computers, which we refer to as PCs), systems builders (companies that specialize in building complete computer systems by combining components from different vendors), smaller distributors and retailers. For the six months ended June 30, 2007, revenue and operating income from our in-country operations were $351.6 million and $11.5 million, representing 70.6% and 87.7% of our consolidated revenue and operating income, respectively. For the year ended December 31, 2006, revenue and operating income from our in-country operations were $623.0 million and $21.5 million, representing 70.0% and 62.3% of our consolidated revenue and operating income, respectively. |

Our Strengths

We have capitalized on our strengths to achieve a leadership position in the markets we serve. Our strengths include:

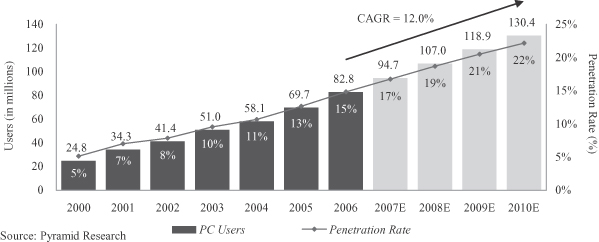

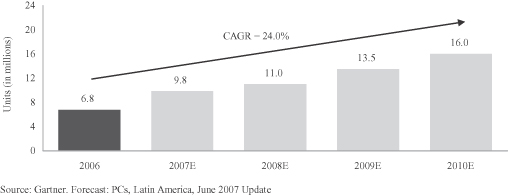

Pure play IT products distributor with leading positions in a large and growing market. We believe we are the largest pure play value-added distributor of IT products focused solely on Latin America and the Caribbean. We believe we hold the number one or number two market share position in each of the 12 countries in which we have an in-country distribution presence, except for Mexico and Colombia. According to IDC, spending on IT products (including hardware, packaged software and services) in Latin America and the Caribbean is projected to grow from $38.7 billion in 2006 to $60.4 billion in 2010, growing at an average of 11.8% per year. This is more than twice as fast as the expected growth rate in IT spending in the United States over the same period and nearly six times faster than the growth rate in IT spending in Latin America and the Caribbean from 2000 to 2006. Growth in these markets is expected to be driven primarily by increasing PC and Internet penetration rates as well as increasing demand for notebook computers. According to Pyramid Research, the Latin American and Caribbean PC penetration rate reached 14.8% in 2006 and is predicted to rise to 22.2% in 2010, which is still well below the U.S. and Canadian penetration rate of 83.0%. We expect that the higher growth in the market for PCs priced below $500 will drive a significant portion of this increase. We believe that we are well positioned in this market segment, which, according to Gartner, is expected to grow an average of 24.0% per year from 2006 to 2010. In addition, the rapid adoption of the Internet by Latin American and Caribbean consumers continues to fuel purchases of PCs. The number of Internet users is predicted by Pyramid Research to grow an average of 16.0% per year from 2006 to 2010, representing an increase in penetration rates from 15.7% to 27.0% over this period. Further, we expect to benefit from the accelerating growth in the notebook computers segment. Gartner expects notebook computer shipments to grow from 2.8 million units in 2006 to 11.5 million units in 2010, representing an average growth rate of 42.7% per year.

Unique business model creates industry-leading margins with significant barriers to entry. We operate both as a Miami-based wholesale aggregator and as an in-country distributor located in 12 countries throughout Latin America and the Caribbean. Our participation at two levels of the distribution chain (Miami and in-country), coupled with our extensive geographic footprint, creates a market presence that we believe is unmatched by any of our competitors and enables us to generate industry-leading margins among our public company competitors. Our dual distribution approach links a diversified set of vendors, primarily located in the

2

Table of Contents

United States and Asia, to a fragmented number of customers spread throughout Latin America and the Caribbean, and delivers value to both ends of the supply chain. To our vendors, we provide access to markets and customers that would be costly and inefficient for them to reach directly. To our customers, which are often small local resellers and retailers that lack the scale and access to buy directly from the United States and Asia, we provide broad and timely product availability, local staff, multi-vendor single source purchasing, technical support, customs management and local warranty service. Over the last 18 years, we have built a broad distribution infrastructure throughout our region and gained important business experience and relationships in each of our markets. We believe that the significant time and investment required to establish an efficient regional distribution infrastructure and the valuable services we provide to both our vendors and customers create significant barriers to entry in each of our markets.

Strong revenue growth and sustainable industry-leading profitability. From our founding in 1988 to the present, we have experienced consistent sales growth. From 2001 to 2006, we achieved a CAGR in revenue of 22.4%. During this period, we also maintained consistently strong operating profitability, with a CAGR in operating income of 25.2%. In 2006, we achieved an operating income margin of 3.9%, compared to the operating margins of 1.3% and 0.7% of our two largest competitors, Ingram Micro and Tech Data, respectively (excluding any goodwill impairment or restructuring charges). Our unique business model, our broad geographic footprint and our focus on higher-margin components, peripherals and software have been the main contributors to our strong margins. We believe these strong margins have helped us achieve what we believe to be an industry-leading return among our public company competitors on invested capital, or ROIC, which we define as net after-tax operating profit divided by average shareholders’ equity and net debt. We have consistently achieved an ROIC in the mid to high teens (17.2% in 2006). Our strong ROICs have also been driven by our focus on minimizing our cash conversion cycle with centralized purchasing, efficient managing of in-country inventory levels, establishing strict customer credit policies and carefully monitoring on-going inventory and demand.

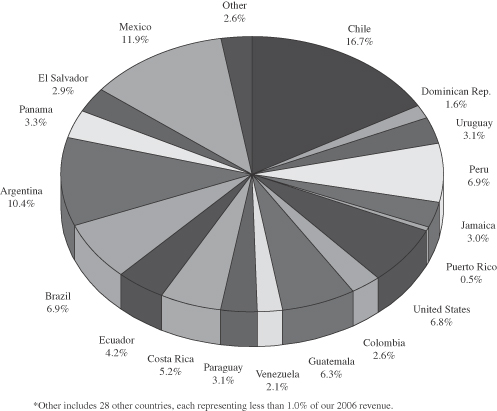

Highly diverse business across multiple geographies and customers. We believe we have the broadest in-country presence of any distributor of IT products to Latin America and the Caribbean, in terms of the number of countries served through an in-country presence. We distribute products to more than 40,000 customers in 45 countries. The diversification of our geographic presence and customer base contributes to our consistent organic revenue growth and reduces our dependence on any single country or customer. We believe our diverse geographic presence will allow us to maintain a strong pace of organic growth in our target markets, driven by attractive market share expansion opportunities as well as strong underlying market growth characteristics. We can also use our deep knowledge of local markets to assess local market conditions and adjust our market focus as necessary. Moreover, the regional expertise we have gained in our multiple local markets can be applied and transferred when we expand our distribution platform into new geographies. In 2006, no country contributed more than 10% of our revenue, except Chile (16.7%), Mexico (11.9%) and Argentina (10.4%). We have also established a strong brand and a reputation for providing excellent customer service that we believe builds customer loyalty and leads to recurring revenue. In addition, we offer customers a one-stop shop for purchasing a broad selection of products, which enables us to maintain a large and diverse group of customers and attract and maintain new customers. In 2006, no single customer represented more than 2.0% of our revenue on a consolidated basis.

Strong vendor relationships and broad portfolio of products. We distribute and market more than 5,700 products from over 220 vendors, enabling us to offer a wide variety of products, satisfy customer requirements for product availability and meet end-user demand for multi-vendor and multi-product IT configurations. The large number of resellers and retailers in the region, their relatively small size, and their geographic fragmentation make it cost effective for vendors to rely on wholesale distributors like us that can deliver a broad regional distribution channel, rather than distributing directly to numerous fragmented resellers and retailers. We provide vendors with extensive regional coverage, larger order sizes, simplified logistics, lower distribution costs

3

Table of Contents

than if they dealt with each of our affiliates independently and with quality pre- and post-sale marketing and technical support. We also eliminate the need for our vendors to handle issues such as local duty and tax arrangements, customer credit analysis and management of numerous small accounts. Consequently, we have established long-standing relationships with most of the leading manufacturers of IT products in the United States and Asia, who we believe value our ability to provide reliable and efficient access to the numerous and growing markets across Latin America and the Caribbean. In 2006, no single vendor’s products generated more than 14.8% of our revenue.

Experienced management team with significant equity ownership. Each of our two co-founders has more than 18 years of industry experience in Latin America and the Caribbean. Our senior managers have an average tenure of over 9 years with us and each has had substantial experience working in the region. In addition, the turnover rate among our senior managers has been low. Prior to this offering, our senior managers beneficially owned approximately 48.6% of our capital stock on a fully diluted basis and will own approximately % of our capital stock following the offering. As a result of their substantial equity interest, we believe that our management has significant incentive to continue to increase our revenue and margins.

Our Strategy

We intend to achieve future growth and profitability through the following strategies:

| • | Grow and strengthen our diverse customer base by leveraging our large selection of products and our comprehensive offering of value-added services, including product training and support, credit and financing and reverse logistics (i.e., handling returns to manufacturers of defective or unwanted parts and products). |

| • | Enhance our margins by maintaining close control over our operating expenses and realizing increased economies of scale in product purchasing and working capital management. |

| • | Build upon our comprehensive in-stock selection of more than 5,700 IT products by expanding our existing product categories to include additional products or vendors and by adding new product categories or subcategories for which there is growing consumer demand. |

| • | Grow our business through extensions of our existing capabilities (including further product diversification and targeting of new markets), increasing our customer base (by distributing products directly to retailers, including small non-traditional retailers), and expanding our product offering of private label and our own branded products. |

| • | Target selective acquisitions that we believe will expand our business into new markets or improve our distribution capabilities, while growing revenues and enhancing margins. |

Citigroup Venture Capital International

In August 2004, Citigroup Venture Capital International, or CVC International, acquired a controlling interest in us through its investment vehicle Co-Investment LLC VII (Intcomex). CVC International is a unit of Citigroup Inc. engaged in private equity investments in emerging markets. CVC International, an affiliate of one of the underwriters, is the selling stockholder in this offering. Following this offering, CVC International will own approximately % of our common stock on a fully diluted basis (approximately % if the underwriters’ overallotment option is exercised in full).

Our Corporate History, Principal Office and Website

Anthony Shalom and Michael Shalom founded our company as a small software retailer in South Florida in 1988. We were reincorporated in Delaware on August 13, 2004 in connection with the investment by CVC

4

Table of Contents

International. Our principal executive offices are located at 3505 NW 107th Avenue, Miami, Florida 33178. Our telephone number is (305) 477-6230. Our website is located at www.intcomex.com. None of the information that appears on or that is linked to or from our website is incorporated by reference into or is otherwise made a part of this prospectus.

Selected Risk Factors

We face risks in operating our business, including risks that may prevent us from achieving our business objectives or that may hurt our business, financial condition and operating results. You should consider these risks before investing in our company.

Some of the important risks to our business and of this offering include the following:

| • | Highly competitive environment. The IT products distribution industry in Latin America and the Caribbean is highly competitive and very fragmented. In certain markets, we compete against large multinational public companies that are significantly better capitalized than we are and potentially have greater bargaining power with vendors than we do. In all of our in-country markets, we also compete against a substantial number of locally-based distributors, many of which have a lower cost structure than we do. We refer to Ingram Micro, Tech Data, Bell Microproducts and SYNNEX in this prospectus as our public company competitors. |

| • | Challenge of establishing and maintaining sufficient management and financial reporting systems and internal and disclosure controls and hiring, retaining and training sufficient accounting and finance personnel. We rely on a variety of management and financial reporting systems and internal and disclosure controls to enable management to capitalize on business opportunities, identify unfavorable developments and risks at an early stage and to prepare accurate and timely financial information for our investors. As our business has grown rapidly in recent years and expanded into new geographic markets, the challenge of establishing and maintaining sufficient systems and controls and hiring, retaining and training sufficient accounting and finance personnel has intensified. |

| • | Dependence on IT products market in Latin America and the Caribbean. Historically, the strength of our business has been driven in large part by the growth of the IT products market in Latin America and the Caribbean. If the IT products market does not grow as quickly and in the manner we expect for any reason, including as a result of economic, political, social or legal developments in Latin America and the Caribbean, we may not be able to grow our business as expected. |

| • | Fluctuations in foreign currency exchange rates. A significant portion of our revenues from in-country operations is invoiced in currencies other than the U.S. dollar, and a significant amount of our in-country operating expenses are denominated in currencies other than U.S. dollars. In markets where we invoice in local currency, the appreciation of a local currency will reduce our gross profit and gross margins in U.S. dollar terms. In markets where books and records are prepared in currencies other than the U.S. dollar, the appreciation of a local currency will increase our operating expenses and decrease our operating margins in U.S. dollar terms. Large and sustained devaluations of local currencies can make many of our products more expensive in local currencies. This could result in our customers having difficulty paying those invoices and, in turn, result in decreases in revenue. Moreover, such devaluations may adversely impact demand for our products because our customers may be unable to afford them. |

| • | Restrictions in our debt agreements. The revolving credit facility agreement between our wholly-owned subsidiary Software Brokers of America, Inc., or SBA, and Comerica Bank as well as the indenture governing our 11 ¾% Second Priority Senior Secured Notes due 2011, which we refer to as the 11 ¾% Notes, impose significant operating and financial restrictions on us and SBA. |

| • | Credit exposure from customers. We extend credit for a significant portion of sales to our customers. We are subject to the risk that our customers fail to pay or delay payment for the products they purchase |

5

Table of Contents

from us, resulting in longer payment cycles, increased collection costs, defaults exceeding our expectations and an adverse impact on the cost or availability of financing. |

| • | Dependence on a relatively small number of vendors. A significant portion of our revenue is derived from products manufactured by a relatively small number of vendors. Due to intense competition in the IT products distribution industry, our key vendors can choose to work with other distributors and, pursuant to standard terms in our vendor agreements, may terminate their relationships with us on short notice. |

| • | Receiving adequate trade credit. Our business is working capital intensive and our vendors historically have been an important source of funding our business growth through the provision of trade credit. We expect to continue to rely on trade credit from our vendors to provide a significant amount of our working capital. If our vendors fail to provide us with sufficient trade credit, including larger amounts of trade credit, in a timely manner as our business grows, we may have to rely on other sources of financing, which may not be readily available or, if available, may not be on terms acceptable or favorable to us. |

| • | Concentration of stock ownership. After this offering, our executive officers, directors and principal stockholders will continue to be able to exercise control over all matters requiring stockholder approval, including the election of directors, amendment of our amended and restated certificate of incorporation and approval of significant corporate transactions and will have significant control over our management and policies. Their interests may not be aligned with your interests as a holder of our common stock. |

For a more detailed discussion of the these and other significant risks associated with our business, our industry and investing in our common stock, you should read the section entitled “Risk Factors” beginning on page 11 of this prospectus.

6

Table of Contents

The Offering

Common stock offered by us | shares |

Common stock offered by the selling stockholder | shares |

Common stock to be outstanding immediately after this offering | shares |

Option to purchase additional shares of common stock | We and the selling stockholder have granted to the underwriters an option, exercisable for 30 days from the date of this prospectus, to purchase up to additional shares of common stock at the public offering price less the underwriting discount. The underwriters may exercise the option solely for the purpose of covering over-allotments, if any, in connection with this offering. To the extent the option is exercised, each underwriter must purchase a number of additional shares approximately proportionate to that underwriter’s initial purchase commitment. |

Use of proceeds | We intend to use $ million of our net proceeds from this offering to redeem or repurchase a portion of our 11 3/4% Notes. We intend to use the remainder of our net proceeds from this offering for general corporate purposes. |

We will not receive any proceeds from the sale of the shares by the selling stockholder. The selling stockholder will receive all of the proceeds from the sale of its shares in the offering. Citigroup Global Markets Inc. (“Citi”), one of the underwriters, is an affiliate of the selling stockholder, CVC International. Because the selling stockholder currently owns approximately % of our common stock on a fully diluted basis, this offering is being conducted in accordance with the applicable provisions of the National Association of Securities Dealers, Inc. Conduct Rules (the “NASD Rules”). The NASD Rules require, among other things, that the initial public offering price of the common stock be no higher than that recommended by a “qualified independent underwriter” (as such term is defined by the NASD Rules). UBS Securities LLC (“UBS”) is assuming the responsibilities of acting as the qualified independent underwriter in this offering. See “Risk Factors—Risks Relating to Our Common Stock and This Offering—Citigroup Global Markets Inc. may have a conflict of interest with respect to this offering” and “Underwriting.”

Dividends | We do not anticipate paying any cash dividends in the foreseeable future. |

Proposed Nasdaq Global Market symbol | “ICMX.” |

Risk factors | Investing in our shares involves a high degree of risk. See “Risk Factors” beginning on page 11 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

7

Table of Contents

Except as otherwise noted, all information in this prospectus:

| • | assumes that the underwriters do not exercise their option to purchase up to additional shares of common stock from us and the selling stockholder; |

| • | assumes the exchange by the holders of the 2,182 shares of our Class B non-voting common stock (which we issued in connection with the re-acquisition of Centel S.A. de C.V. (“Centel”), our Mexican subsidiary) for 2,182 shares of our voting common stock prior to or simultaneously with the completion of this offering; |

| • | assumes that the initial offering price is per share, the midpoint of the range set forth on the cover of this prospectus; |

| • | assumes our receipt of net proceeds of from the offering and the application of the proceeds as described under “Use of Proceeds;” |

| • | reflects a for one split of our common stock in the form of a stock dividend to our existing stockholders prior to or simultaneously with the completion of this offering; |

| • | excludes 1,540 shares of common stock issuable upon exercise of outstanding stock options granted prior to this offering to certain of our officers and directors with a weighted average exercise price of $1,077 per share, none of which were vested as of June 30, 2007; and |

| • | excludes restricted stock grants of 64 shares of common stock with a vesting period of one year for each third of such shares that we intend to grant to two independent directors at the initial public offering price. |

8

Table of Contents

Summary Historical Consolidated Financial and Other Data

The following table presents summary financial and other data as of and for the years ended December 31, 2004, 2005 and 2006 and the three months ended March 31, 2006 and 2007. We derived the statement of operations and other data set forth below for the years ended December 31, 2004, 2005 and 2006 and the balance sheet data as of December 31, 2005 and 2006 from our audited consolidated financial statements (together with the notes thereto) that are included elsewhere in this prospectus. We derived the balance sheet and other data as of December 31, 2004 from our audited consolidated financial statements with respect to such date that are not included in this prospectus. The statement of operations data for the six months ended June 30, 2007 and 2006 and the balance sheet data as of June 30, 2007 were derived from our unaudited condensed consolidated financial statements for these periods (together with the notes thereto) that are included elsewhere in this prospectus. They include all adjustments consisting of normal recurring adjustments that management considers necessary for a fair presentation of the financial position and results of operations for these periods. The results for any interim period are not necessarily indicative of the results that may be expected for the full year.

You should read the following summary information in conjunction with “Selected Financial Information and Other Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited and unaudited consolidated financial statements (together with the notes thereto) that are included elsewhere in this prospectus.

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||

| 2004 | 2005(1) | 2006 | 2006 | 2007 | ||||||||||||||||

(audited) | (unaudited) | |||||||||||||||||||

| (in thousands, except per share data and number of shares) | ||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||

Revenue | $ | 554,345 | $ | 716,440 | $ | 889,779 | $ | 427,299 | $ | 498,147 | ||||||||||

Cost of revenue | 495,536 | 642,737 | 797,665 | 383,181 | 448,045 | |||||||||||||||

Gross profit | 58,809 | 73,703 | 92,114 | 44,118 | 50,102 | |||||||||||||||

Operating expenses | 33,815 | 43,343 | 57,537 | 27,318 | 36,931 | |||||||||||||||

Operating income | 24,994 | 30,360 | 34,577 | 16,800 | 13,171 | |||||||||||||||

Other (income) expense | ||||||||||||||||||||

Interest expense | 3,429 | 16,805 | 16,233 | 8,060 | 8,445 | |||||||||||||||

Interest income | (153 | ) | (456 | ) | (876 | ) | (500 | ) | (283 | ) | ||||||||||

Other (income) expense, net | (196 | ) | 600 | 164 | 4 | 27 | ||||||||||||||

Foreign exchange (gain) loss | (986 | ) | (1,407 | ) | 1,099 | 2,570 | (968 | ) | ||||||||||||

Total other (income) expense | 2,094 | 15,542 | 16,620 | 10,134 | 7,221 | |||||||||||||||

Income before taxes and minority interest | 22,900 | 14,818 | 17,957 | 6,666 | 5,950 | |||||||||||||||

Income tax provision | 6,417 | 2,755 | 4,894 | 2,169 | 1,897 | |||||||||||||||

Income before minority interest | 16,483 | 12,063 | 13,063 | 4,497 | 4,053 | |||||||||||||||

Minority interest(2) | 314 | — | — | — | — | |||||||||||||||

Net income | $ | 16,169 | $ | 12,063 | $ | 13,063 | $ | 4,497 | $ | 4,053 | ||||||||||

Net income per common share (basic and diluted) | $ | 277.48 | $ | 119.28 | $ | 127.84 | $ | 44.01 | $ | 39.66 | ||||||||||

Weighted average number of shares used in per share calculation (basic and diluted)(3) | 58,270 | 101,133 | 102,182 | 102,182 | 102,182 | |||||||||||||||

9

Table of Contents

| As of December 31, | As of June 30, | ||||||||||||

| 2004 | 2005(1) | 2006 | 2007 | ||||||||||

| (audited) | (unaudited) | ||||||||||||

| (in thousands) | |||||||||||||

Balance Sheet Data: | |||||||||||||

Cash and cash equivalents | $ | 6,902 | $ | 12,964 | $ | 20,482 | $ | 18,034 | (4) | ||||

Working capital(5) | 51,843 | 92,846 | 98,222 | 104,267 | |||||||||

Total assets | 172,522 | 248,311 | 292,575 | 344,449 | |||||||||

Long-term debt (including capital leases) | 60,274 | 119,628 | 120,209 | 120,703 | |||||||||

Total debt | 70,045 | 125,041 | 137,862 | 144,585 | |||||||||

Total shareholders’ equity | 30,189 | 25,567 | 38,337 | 45,633 | |||||||||

Other Data: | |||||||||||||

Cash dividends per common share(6) | $ | 0.00 | $ | 197.76 | $ | 0.00 | $ | 0.00 | |||||

| (1) | In 1990, we formed Centel. In September 2001, we exchanged with the management of Centel our interest in Centel for the Intcomex shares held by the management of Centel. We re-acquired all interests in Centel on June 23, 2005 and, as a result, the financial and other data for the year ended December 31, 2005 includes the financial information for Centel commencing on the date of its re-acquisition. |

| (2) | Represents minority shareholders’ interests in Intcomex Costa Rica Mayorista en Equipo de Computo, S.A., Intcomex Ecuador, S.A. and Intcomex Jamaica, Ltd. We acquired all of the outstanding common stock held by those minority shareholders on August 30, 2004 subsequent to the CVC International investment in our company. |

| (3) | In 2004, the weighted average number of shares used in per share calculations reflects the impact of the recapitalization of our company as of August 31, 2004 in connection with the CVC International investment in our company. In 2005, the weighted average number of shares used in per share calculations reflects the issuance of 2,182 shares of Class B non-voting common stock to the sellers of Centel in connection with our re-acquisition of Centel on June 23, 2005. |

| (4) | Includes $47 of certificates of deposit-restricted as of June 30, 2007. |

| (5) | Working capital is defined as current assets less current liabilities. |

(6) | In August 2005, we paid a one-time cash dividend of $20.0 million, or $197.76 per share, to all of our then existing stockholders. The dividend was paid out of proceeds of the offering of our 11 3/4% Notes that was completed in August 2005. The per common share amount is based on 102,182 shares outstanding as of August 25, 2005. |

10

Table of Contents

Any investment in our common stock involves a high degree of risk. You should carefully consider the material risks described below together with all of the other information included in this prospectus before making an investment decision. If any of the following risks actually occurs, our business, results of operations or financial condition would likely suffer. In such an event, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Relating to Our Business

We operate in a highly competitive environment and, as a result, we may not be able to compete effectively or maintain or increase our sales, market share or margins.

The IT products distribution industry in Latin America and the Caribbean is highly competitive. The factors on which IT distributors compete include:

| • | price; |

| • | availability and quality of products and services; |

| • | terms and conditions of sale; |

| • | availability of credit and credit terms; |

| • | timeliness of delivery; |

| • | flexibility in tailoring specific solutions to customers’ needs; |

| • | effectiveness of marketing and sales programs; |

| • | availability of technical and product information; and |

| • | availability and effectiveness of warranty programs. |

The IT products distribution industry in Latin America and the Caribbean is very fragmented. In certain markets, we compete against large multinational public companies (including Ingram Micro, Tech Data, SYNNEX and Bell Microproducts) that are significantly better capitalized than we are and potentially have greater bargaining power with vendors than we do. In addition, our main competitor in Mexico, Ingram Micro, has a significantly larger market share than we do in that country. In all of our in-country markets, we also compete against a substantial number of locally-based distributors, many of which have a lower cost structure than we do, in some cases because they operate in the gray market and the local “informal” economy. Due to intense competition in our industry, we may not be able to compete effectively against our existing competitors or against new entrants to the industry, or to maintain or increase our sales, market share or margins.

Our relatively high margins, together with improving regional economic conditions, may attract new competitors into our markets, which could result in the loss of our market share and may cause our results of operations to decline.

Historically, we have had relatively high margins as compared to our public company competitors. Our relatively high margins may attract new competition into our markets, including competition from companies employing alternate business models such as manufacturer direct sales. Improvements in economic conditions in countries in which we operate, including an increase in per capita income levels, will likely lead to an increase in demand for IT products in these countries, thereby making our business more attractive to our competitors. Loss of existing or future market share to new competitors and increased price competition could hurt our results of operations.

11

Table of Contents

Our management and financial reporting systems, internal and disclosure controls and finance and accounting personnel may not be sufficient to meet our management and reporting needs.

We rely on a variety of management and financial reporting systems and internal controls to provide management with accurate and timely information about our business and operations. This information is important to enable management to capitalize on business opportunities and identify unfavorable developments and risks at an early stage. We also rely on these management and financial reporting systems and internal and disclosure controls to enable us to prepare accurate and timely financial information for our investors.

The challenge of establishing and maintaining sufficient systems and controls and hiring, retaining and training sufficient accounting and finance personnel has intensified as our business has grown rapidly in recent years and expanded into new geographic markets. As a result, we have identified the need to expand our finance and accounting staff and enhance internal controls at both the corporate and in-country levels, and to enhance the training of in-country management personnel regarding internal controls and management reporting, to meet our current needs. This process is ongoing. For example, although we expect our new company-wide financial reporting system Sentai to enhance the control of daily operating functions by our senior management, Sentai has yet to be implemented in three out of 12 countries in which we have operations. In addition, although we have recently hired a corporate controller with responsibility for our SEC reporting as well as two controllers for our subsidiaries in Argentina and Guatemala, we are still seeking to add personnel to our finance and accounting staff. In addition, we are enhancing existing controls and instituting new controls at our consolidated and subsidiary operating levels.

Although we believe our current management and financial reporting systems, internal and disclosure controls and finance and accounting personnel are sufficient to enable us to effectively manage our business, identify unfavorable developments and risks at an early stage and produce financial information in an accurate and timely manner, we cannot be sure this will be the case. In addition, a control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that its objectives are met. Its inherent limitations include the realities that judgments in decision-making can be faulty and failures can occur because of a simple mistake. Moreover, controls can be circumvented by the acts of an individual, collusion of two or a group of people or by management’s decision to override the existing controls. For example, although immaterial in amount, two employees of our Panama subsidiary colluded to commit check fraud which went undetected from mid-2002 to early 2006.

Deficiencies in our controls may have contributed to the circumstances that led to our recent settlements following a tax audit with the Uruguayan tax and customs authorities. These settlements resulted in a net pretax charge of $3.8 million to the company in the second quarter of 2007 as described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Uruguay Tax Audit.” Moreover, a targeted review of various internal controls in our in-country operations related to certain key components of our financial statements initiated as a follow up to the Uruguay tax audit indicated various areas in which controls should be improved. We have implemented, or are implementing, control improvements to address these issues.

We believe that we will also need to continue to expand our finance and accounting staff and enhance internal controls at both the corporate and in-country levels, and to enhance the training of in-country management personnel regarding internal controls and management reporting, to meet our future needs as a result of our anticipated or future growth. We cannot be sure that we will be able to take all necessary actions in a timely manner in order to keep pace with our anticipated growth.

Our failure to establish and maintain sufficient management and financial reporting systems and internal and disclosure controls, to hire, retain and train sufficient accounting and finance personnel, and to enhance the training of in-country management personnel regarding internal controls and management reporting could impair our ability to prepare accurate and timely financial information, hinder our growth and have a material adverse effect on our current or future business, results of operations and financial condition.

12

Table of Contents

We are exposed to increased costs associated with complying with the Sarbanes-Oxley Act of 2002 and other corporate governance and disclosure standards. Compliance efforts could divert management time from revenue-generating activities to compliance activities and failures to comply could cause reputational harm, a decline of the trading price of our securities and additional costs to remedy shortcomings.

The Sarbanes-Oxley Act of 2002, or SOX, as well as rules implemented by the SEC and the Nasdaq Global Market, require us to adopt various corporate governance practices and implement various internal controls when we become a public company. Our efforts to comply with evolving laws, regulations and standards applicable to public companies have resulted in, and are likely to continue to result in, increased expenses and a diversion of management time from revenue-generating activities to compliance activities.

In particular, Section 404 of SOX requires our management to annually review and evaluate our internal controls over financial reporting and attest to the effectiveness of these controls beginning with our fiscal year ended December 31, 2007. Our independent registered public accounting firm is required by SOX to attest to managements’ assessment beginning with our fiscal year ended December 31, 2008. We are currently working towards ensuring that adequate resources and expertise, both internal and external, are put in place to meet this requirement. To date, our ongoing efforts to comply with Section 404 have required the commitment of significant financial and managerial resources. Though we are currently making efforts to become compliant with Section 404 requirements in a timely manner, we may be unable to achieve compliance by the required dates. In the event that our Chief Executive Officer, Chief Financial Officer or independent registered public accounting firm determines that our controls over financial reporting are not effective as required by Section 404 of SOX at any time in the future, investor perceptions of us and our reputation may be adversely affected, the trading price of our securities may decline and we may incur significant additional costs to remedy shortcomings in our internal controls.

If the IT products market in Latin America and the Caribbean does not grow as we expect, we may not be able to maintain or increase our present growth rate and our results of operations and financial condition could be affected.

Historically, the growth of our business has been driven in large part by the growth of the IT products market in Latin America and the Caribbean. In particular, we have benefited from rapid growth in PC and Internet penetration rates. We expect that our future growth will also depend in large part on further growth in the IT market including growth in PC and Internet penetration rates and increasing demand for notebook computers. If the IT products market does not grow as quickly and in the manner we expect for any reason, including as a result of economic, political, social or legal developments in Latin America and the Caribbean, we may not be able to maintain or grow our business as expected which could have an impact on our results of operations and financial condition.

Economic, political, social or legal developments in Latin America and the Caribbean could hurt our results of operations and financial condition.

Historically, sales to Latin America and the Caribbean have accounted for almost all of our consolidated revenues. As a result, our financial results are particularly sensitive to the performance of the economies of countries in Latin America and the Caribbean. If local, regional or worldwide developments adversely affect the economies of any of the countries in which we do business, our results of operations and financial condition could be hurt. Our results are also impacted by political and social developments in the countries in which we do business and changes in the laws and regulations affecting our business in those regions. Changes in local laws and regulations could, among other things, make it more difficult for us to sell our products in the affected countries, restrict or prevent our receipt of cash from our customers, result in longer payment cycles, impair our collection of accounts receivable and make it more difficult for us to repatriate capital and dividends from our foreign subsidiaries to the ultimate U.S. parent company.

The economic, political, social and legal risks we are subject to in Latin America and the Caribbean include but are not limited to:

| • | deteriorating economic, political or social conditions; |

13

Table of Contents

| • | additional tariffs, import and export controls or other trade barriers that restrict our ability to sell products into countries in Latin America and the Caribbean; |

| • | changes in local tax regimes, including the imposition of significantly increased withholding or other taxes or an increase in value added tax or sales tax on products we sell; |

| • | changes in laws and other regulatory requirements governing foreign capital transfers and the repatriation of capital and dividends; |

| • | increases in costs for complying with a variety of different local laws, trade customs and practices; |

| • | delays in shipping and delivering products to us or customers across borders for any reason, including more complex and time-consuming customs procedures; and |

| • | fluctuations of local currencies. |

Any adverse economic, political, social or legal developments in the countries in which we do business could harm our results of operations and financial condition.

Fluctuations in foreign currency exchange rates could reduce our gross profit and gross margins and increase our operating expenses in U.S. dollar terms.

We generally do not engage in foreign currency hedging arrangements because either we do not believe it is cost-effective or it is not available to us for certain foreign currencies. Consequently, foreign currency fluctuations may adversely affect our results of operations, including our gross margins and operating margins.

A significant portion of our revenues from in-country operations is invoiced in currencies other than the U.S. dollar, and a significant amount of our in-country operating expenses are denominated in currencies other than U.S. dollars. In markets where we invoice in local currency, including Argentina, Chile, Colombia, Costa Rica, Guatemala, Jamaica, Mexico, Peru and Uruguay, the appreciation of a local currency will reduce our gross profit and gross margins in U.S. dollar terms. In markets where our books and records are prepared in currencies other than the U.S. dollar, the appreciation of a local currency will increase our operating expenses and decrease our operating margins in U.S. dollar terms.

Large and sustained devaluations of local currencies, like those that occurred in Brazil in 2000 and Argentina in 2001, can make many of our products more expensive in local currencies. This could result in our customers having difficulty paying those invoices and, in turn, result in decreases in revenue. Moreover, such devaluations may adversely impact demand for our products because our customers may be unable to afford them.

For a more detailed discussion of the effect of foreign currency fluctuations on our results of operations, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures About Market Risks—Foreign exchange risk.”

We could experience difficulties in staffing and managing our foreign operations, which could result in reduced revenues and difficulties in realizing our growth strategy.

We have many sales and distribution centers in multiple countries, which requires us to attract managers of our business in each of those locations. In establishing and developing many of our in-country sales and distribution operations, we have relied in large part on the local market knowledge and entrepreneurial skills of a limited number of local managers in those markets. We have no employment agreements with any of our in-country managers. The loss of the services of any of these managers could adversely impact our results of operations in the market in which the manager is located. Further, it may prove difficult to find and attract new talent (including accounting and finance personnel) in our existing markets or any new markets we enter in Latin America and the Caribbean who possess the expertise required to successfully manage and operate our in-country sales and distribution operations. If we fail to recruit highly qualified candidates, we may experience greater difficulty realizing our growth strategy, which could hurt our results of operations.

14

Table of Contents

If we lose the services of our key executive officers, we may not succeed in implementing our business strategy.

We are currently managed by certain key executive officers, including both of our founders, Anthony Shalom and Michael Shalom. These individuals have extensive experience and knowledge of our industry and the many local markets in which we operate. They also have been integral in establishing and expanding some of our most significant customer relationships and building our unique distribution platform. The loss of the services of these key executive officers could adversely affect our ability to implement our business strategy, and new members of management may not be able to successfully replace them. With the exception of an employment agreement with our Chief Financial Officer, we have no employment agreements with any of our key executive officers.

We are dependent on a variety of IT and telecommunications systems and are subject to additional risks, as we are in the process of implementing a new company-wide reporting system, and any disruptions in our existing systems or delays in implementing our new system could adversely impact our ability to effectively manage our business and prepare accurate and timely financial information.

We are dependent on a variety of IT and telecommunications systems, including systems for managing our inventories, accounts receivable, accounts payable, order processing, shipping and accounting. In addition, our ability to price products appropriately and the success of our expansion plans depend to a significant degree upon our IT and telecommunications systems. We are in the process of installing Sentai, a new company-wide financial reporting system. Sentai is a scalable IT system that enables simultaneous decentralized decision-making by our employees involved in sales and purchasing while permitting control of daily operating functions by our senior management. We are also using the Sentai logistics and inventory management system in order to better adapt to higher shipping volumes. The system has been implemented in eight of our 12 in-country locations and in our Miami location. We expect to complete implementation in the remaining locations by year-end 2008. Our experience with this new platform is limited and each new installation requires the training of our local employees. In addition, new installations may require further modifications in order to handle the different accounting requirements in each of the countries in which it is installed. Any delay in installation or temporary or long-term failure of these systems, once installed, could adversely impact our ability to effectively manage our business and prepare accurate and timely financial information. Also, our failure to adapt and upgrade our systems to keep pace with our future development and expansion could hurt our results of operations.

Our substantial debt could limit the cash flow available for our operations, which could adversely affect our business.

We have now and will continue to have a substantial amount of debt, which requires significant interest and principal payments. As of June 30, 2007, we had $144.6 million of total debt outstanding (consisting of $119.4 million outstanding under our 11 3/4% Notes, net of discount, a portion of which we intend to redeem or repurchase with the proceeds from this offering, $19.6 million outstanding under the revolving credit facility of SBA, $5.1 million of outstanding debt of our foreign subsidiaries and $0.5 million of capital leases). Subject to the limits contained in the indenture governing our 11 3/4% Notes and our other debt instruments, we may be able to incur additional debt from time to time to finance working capital, capital expenditures, investments or acquisitions, or for other purposes. If we incur additional debt, the risks related to our high level of debt could intensify. Specifically, our high level of debt could have important consequences to the holders of our common stock, including the following:

| • | limiting our ability to obtain additional financing to fund future working capital, capital expenditures, acquisitions or other general corporate requirements; |

| • | requiring a substantial portion of our cash flows to be dedicated to debt service payments instead of other purposes; |

| • | increasing our vulnerability to general adverse economic and industry conditions; |

| • | limiting our flexibility in planning for and reacting to changes in the industry in which we compete; |

15

Table of Contents

| • | placing us at a disadvantage compared to other, less leveraged competitors; and |

| • | increasing our cost of borrowing. |

The indenture governing our 11 3/4% Notes and the credit agreement governing SBA’s revolving credit facility impose significant operating and financial restrictions on our company and our subsidiaries, which may prevent us from capitalizing on business opportunities.

The indenture governing our 11 3/4% Notes imposes significant operating and financial restrictions on us. These restrictions limit our ability (and the ability of our subsidiaries) to, among other things:

| • | incur additional indebtedness or enter into sale and leaseback obligations; |

| • | pay certain dividends or make certain distributions on our capital stock or repurchase our capital stock; |

| • | make certain investments or other restricted payments; |

| • | place restrictions on the ability of subsidiaries to pay dividends or make other payments to us; |

| • | engage in transactions with shareholders or affiliates; |

| • | sell certain assets or merge with or into other companies; |

| • | guarantee indebtedness; and |

| • | create liens. |

SBA’s revolving credit facility limits SBA’s ability, among other things, to:

| • | incur additional indebtedness; |

| • | make certain capital expenditures; |

• | guarantee obligations, other than SBA’s guarantee of our 11 3/4% Notes; |

• | create or allow liens on assets, other than liens securing our 11 3/4% Notes; |

| • | make investments, loans or advances; |

| • | pay dividends, make distributions and undertake stock and other equity interest buybacks; |

| • | make certain acquisitions; |

| • | engage in mergers, consolidations or sales of assets; |

| • | use proceeds of the revolving credit facility for certain purposes; |

| • | enter into certain lease obligations; |

| • | enter into transactions with affiliates on non-arms’ length terms; |

| • | sell or securitize receivables; |

| • | make certain payments on subordinated indebtedness; or |

| • | create or acquire subsidiaries. |

In addition, SBA’s revolving credit facility requires SBA to:

| • | maintain a tangible effective net worth (tested quarterly) of at least $37.0 million, which minimum level shall decline from the end of the third fiscal quarter of 2006 to the end of the third fiscal quarter of 2007 to $25.0 million and remain at $25.0 million thereafter; |

16

Table of Contents

| • | maintain a ratio of senior debt to tangible effective net worth (tested quarterly) of not more than 2.5 to 1.0; |

| • | maintain for the fiscal year ending December 31, 2007, net income of not less than $7.5 million; and |

| • | maintain as of the last day of each fiscal year, commencing with the fiscal year ending December 31, 2008, a fixed charge coverage ratio of not less than 1.0 to 1.0. |

As a result of these covenants and restrictions, we are limited in how we conduct our business and we may be unable to raise additional debt financing to compete effectively or to take advantage of new business opportunities. The terms of any future indebtedness we may incur could include more restrictive or additional covenants.

We may not be able to maintain compliance with our current debt covenants or any additional covenants in the future and our failure to do so could adversely impact our liquidity.

In 2006, SBA was in default under its revolving credit facility with Comerica Bank as a result of SBA’s repayment of a portion of the outstanding principal under our intercompany loan to SBA. SBA was prohibited from repaying any principal under the intercompany loan pursuant to a subordination agreement with the lender under the revolving credit facility. The lender granted a waiver of the default and amended the revolving credit facility and related subordination agreement to allow SBA to repay the principal under the intercompany loan ($22.6 million of which remains outstanding), which amounts we expect to use to pay interest and a portion of the sinking funds payments due under our 11 3/4% Notes. As of March 31, 2007, SBA was in default on its capital expenditure covenant under its revolving credit facility with Comerica Bank due to a delay in the relocation of our main warehouse and headquarters in Miami and a resulting delay in the timing of capital expenditures. On May 14, 2007, SBA requested and received a waiver from Comerica Bank on the covenant default and on May 15, 2007 an amendment to the revolving credit facility was signed increasing the facility to $27.5 million from $25.0 million and raising the 2007 capital expenditure limit to $2.5 million from $1.0 million.

We may not be able to maintain compliance with our current covenants or any additional covenants in the future and, if we fail to do so, we may not be able to obtain waivers from the lenders or amend any such covenants on acceptable terms or at all. If we fail to obtain such waivers or a replacement facility, we may not have resources sufficient at our parent company level or otherwise to meet our anticipated debt service requirements, capital expenditures and working capital needs.

Our and SBA’s failure to comply with the restrictive covenants described above could result in an event of default, which, if not cured or waived, could result in either of us having to repay our respective borrowings before their respective due dates. If we or SBA is forced to refinance these borrowings on less favorable terms, our results of operations or financial condition could be harmed. In addition, if we are in default under any of our existing or future debt facilities, we also will not be able to borrow additional amounts under those facilities to the extent they would otherwise be available and may not be able to repay our existing indebtedness.

We have significant credit exposure to our customers. If we are unable to effectively manage our accounts receivable, it could result in longer payment cycles, increased collection costs and defaults exceeding our expectations and adversely impact the cost or availability of our financing.

We extend credit for a significant portion of sales to our customers. We are subject to the risk that if our customers fail to pay or delay payment for the products they purchase from us, it could result in longer payment cycles, increased collection costs, defaults exceeding our expectations and an adverse impact on the cost or availability of financing. These risks may be exacerbated by a variety of factors, including adverse economic conditions, decreases in demand for our products and negative trends in the businesses of our customers.

17

Table of Contents

We have a number of credit facilities under which the amount we are able to borrow is based on the value and quality of our accounts receivable. The value and quality of our accounts receivable is affected by several factors, including:

| • | the collectibility of our accounts receivable; |

| • | general and regional industry and economic conditions; and |

| • | our and our customers’ financial condition and creditworthiness. |

Any reduction in our borrowing capacity under these credit facilities could adversely affect our ability to finance our working capital and other needs.

Although we obtain credit insurance against the failure to pay or delay in payment for our products by some of the customers of our Miami operations, our results of operations and liquidity could be hurt by a loss for which we do not have insurance or that is subject to an exclusion or that exceeds our applicable policy limits. In addition, increasing insurance premiums could adversely affect our results of operations. Moreover, failure to obtain credit insurance may have a negative impact on the amount of borrowing capacity available to our Miami-based operations under SBA’s revolving credit facility.

Our expansion into new markets may present additional risks, which may limit our success in those markets and could hurt our results of operations.

We currently have in-country sales and distribution operations in 12 Latin American and Caribbean countries and a sales office in Brazil. We expect to enter into new geographic markets both within the countries where we already conduct operations and in new countries where we have no prior operating or distribution experience. In new markets, we will face challenges such as customers’ lack of awareness of our brand, difficulties in hiring personnel and our unfamiliarity with local markets. New markets may also have different competitive conditions from our existing markets and may generate lower margins. Any failure on our part to recognize or effectively respond to these differences may limit the success of our operations in those markets, and could hurt our results of operations.

We depend on a relatively small number of vendors for products that make up a significant portion of our revenue and the loss of a relationship with any of our key vendors may hurt our results of operations.

A significant portion of our revenue is derived from products manufactured by a relatively small number of vendors. For the six months ended June 30, 2007 and the years ended December 31, 2006 and 2005, our top ten vendors manufactured products that accounted for 65.0%, 63.8% and 64.0% of our revenue, respectively, and the products of one top vendor accounted for 16.8% of our revenue in the six months ended June 30, 2007, the products of the same top vendor accounted for 14.8% of our revenue in 2006 and the products of a different top vendor accounted for 14.8% of our revenue in 2005. We expect that we will continue to obtain most of our products from a relatively small number of vendors and that the portion of our revenue that we obtain from such vendors may continue to increase in the future. Due to intense competition in the IT products distribution industry, our key vendors can choose to work with other distributors and, pursuant to standard terms in our vendor agreements, may terminate their relationships with us on short notice. The loss of a relationship with any of our key vendors may hurt our results of operations.

If we are unable to obtain sufficient trade credit from our vendors or other sources in a timely manner and on reasonable terms, our results of operations could be adversely affected and our growth inhibited.

Our business is working capital intensive and our vendors historically have been an important source of funding our business growth through the provision of trade credit. We expect to continue to rely on trade credit from our vendors to provide a significant amount of our working capital. If our vendors fail to provide us with sufficient trade credit, including larger amounts of trade credit, in a timely manner as our business grows, we

18

Table of Contents

may have to rely on other sources of financing, which may not be readily available or, if available, may not be on terms acceptable or favorable to us. If we are unable to obtain sufficient trade credit from our vendors or other sources in a timely manner, our results of operations could be adversely affected and our growth inhibited.

In addition, our ability to pay for products is largely dependent on our principal vendors providing us with payment terms that facilitate the efficient use of our capital. The payment terms we receive from our vendors are based on several factors, including (i) our recent operating results, financial position (including our level of indebtedness) and cash flows; (ii) our payment history with the vendor; (iii) the vendor’s credit granting policies (including any contractual restrictions to which it is subject), our creditworthiness (as determined by various entities) and general industry conditions; (iv) prevailing interest rates; and (v) the vendors’ ability to obtain credit insurance in respect of amounts that we owe. Adverse changes in any of these factors, many of which are not within our control, could increase the costs to us of financing our inventory and may limit or eliminate our ability to obtain vendor financing and hurt our results of operations and financial condition.

Our vendors generally can unilaterally change the terms of the sales agreements for future orders and if they adversely change the terms, our results of operations could be hurt.

The sales agreements provided by our vendors are generally at will agreements that have short terms. Generally, each vendor has the ability to unilaterally change the terms and conditions of its sales agreements for future orders, including by reducing the level of purchase discounts, rebates and marketing programs available to us. If we are unable to pass the impact of these changes through to our reseller and retailer customers (usually through increased prices), our results of operations could be hurt.

We are dependent on vendors to maintain adequate inventory levels and oversupplies may adversely affect our margins and product shortages may adversely affect our revenues and costs.

We depend on our vendors to maintain adequate inventory. Our inventory levels may vary from period to period, due primarily to the anticipated and actual sales levels and our purchasing levels. The IT industry occasionally experiences an oversupply of IT products, which vendors then sell on the market at reduced prices. The most recent example of such an oversupply that affected us was the excess supply of Intel processors at the end of 2005 and during the first half of 2006, which resulted in us selling Intel processors at prices below our cost. Although we continued buying and distributing Intel processors during that period to maintain our relationship with Intel, our margins were adversely affected despite rebates we received from Intel at the end of 2006. If similar oversupplies occur in the future, our results of operations could be adversely affected again.

The IT industry is also characterized by periods of severe product shortages due to vendors’ difficulties in projecting demand for certain products distributed by us. When such product shortages occur, we typically receive an allocation of products from the vendor. Our vendors may not be able to maintain an adequate supply of products to fulfill all of our customer orders on a timely basis and the costs of these products to us may increase. Any supply shortages or delays (some or all of which are beyond our control) could cause us to be unable to service customers on a timely basis. If the decline in sales or increased costs due to product shortages is not offset by higher margins, this could hurt our results of operations.

We are subject to the risk that our inventory values may decline, which could adversely affect our results of operations.

The IT products distribution industry is subject to rapid technological change, new and enhanced product specification requirements and evolving industry standards. These factors may cause a substantial decline in the value of our inventory or may render all or substantial portions of our inventory obsolete. Changes in customs or security procedures in the countries through which our inventory is shipped, as well as other logistical difficulties that slow the movement of our products to our customers, can also exacerbate the impact of these factors. While some of our vendors offer us limited protection against the decline in value of our inventory due to technological

19

Table of Contents

change or new product developments in the form of credit or partial refunds, these protective policies are largely subject to the discretion of our vendors and change from time to time. In addition, we distribute private label products for which price protection and rights of return are not customarily contractually available, and for which we bear increased risks. In any event, the protective terms of our vendor agreements may not adequately cover declines in our inventory value and these vendors may discontinue providing these terms at any time in the future. Any decline in the value of our inventory not offset by vendor credits or refunds could adversely affect our results of operations.

If our vendors fail to respond quickly to technological changes and innovations and our product offerings fail to satisfy consumers’ tastes or respond to changes in consumer preferences, our revenues may decline and our competitors may gain additional market share.