Exhibit 99.1

August 11, 2006

Dear Sara Lee Stockholder:

I am pleased to inform you that on August 7, 2006, the Board of Directors of Sara Lee Corporation approved the spin off of Hanesbrands Inc., our wholly-owned subsidiary that operates our branded apparel business.

The spin off will separate the ownership and management of our business and that of Hanesbrands, which we think will better enable both companies to focus on their core businesses. Following the spin off, Sara Lee will become a more tightly focused company, focusing on its food, beverage and household products businesses. We are confident that the new Sara Lee will be well-positioned to achieve its long-term growth targets.

We will effect the spin off by distributing Hanesbrands’ common stock in a pro rata dividend to holders of our common stock as of August 18, 2006. The dividend will represent 100% of the common stock of Hanesbrands outstanding at the time of the spin off. We expect to distribute shares of Hanesbrands on or about September 5, 2006.

Stockholder approval for the spin off is not required, and you are not required to take any action to participate in the spin off. You do not need to pay any consideration or surrender or exchange your shares of Sara Lee common stock. Following the spin off, Sara Lee common stock will continue to trade on the New York Stock Exchange under the symbol “SLE,” and Hanesbrands common stock will trade on the New York Stock Exchange under the symbol “HBI.”

We intend for the spin off to be tax free for stockholders for U.S. federal income tax purposes. To that end, we have obtained a favorable ruling regarding the spin off from the Internal Revenue Service.

The enclosed information statement, which is being provided to all Sara Lee stockholders, describes the spin off in detail and contains important business and financial information about Hanesbrands.

I look forward to your continued support as a stockholder of both Sara Lee and Hanesbrands.

Sincerely,

Brenda C. Barnes

Chairman and Chief Executive Officer

August 11, 2006

Dear Hanesbrands Inc. Stockholder:

It is our pleasure to welcome you as a stockholder of our new company. Although we are a newly independent company, our product portfolio includes some of the most recognized apparel essentials brands in the United States, includingHanes, Champion, Playtex, Bali, Just My Size, barely thereandWonderbra. We design, manufacture, source and sell a broad range of products such as t-shirts, bras, panties, men’s underwear, kids’ underwear, socks, hosiery, casualwear and activewear. In fiscal 2005, we generated $4.7 billion in net sales and $359.5 million in income from operations. Our mission is to create value for you, our stockholders, and for our customers through effective supply chain management, competitive prices, high quality and service excellence. Our strong brands and dedicated employees will drive this value.

Our management team is excited about our spin off from Sara Lee Corporation, and is committed to realizing the potential that exists for us as an independent company focused on apparel essentials. We invite you to learn more about our company by reading the enclosed information statement and we look forward to updating you on our progress in realizing our vision and mission. We would like to thank you in advance for your support as a stockholder in our new company.

Sincerely,

| | |

Lee A. Chaden Executive Chairman | |

Richard A. Noll Chief Executive Officer |

INFORMATION STATEMENT

Hanesbrands Inc.

Common Stock

(Par Value $0.01)

Sara Lee Corporation is furnishing this information statement to its stockholders in connection with the spin off of our company. In the spin off, Sara Lee will transfer to us the assets and businesses which Sara Lee attributes to its branded apparel business and distribute on a pro rata basis to its stockholders all of the outstanding shares of our common stock.

For every eight shares of Sara Lee common stock held of record by you as of 5:00 p.m., New York City time, on August 18, 2006, the record date for the distribution, you will receive one share of our common stock. You will receive cash in lieu of any fractional shares of our common stock which you would have received after application of the above ratio. As discussed under “The Spin Off—Trading of Sara Lee Common Stock Between the Record Date and Distribution Date,” if you sell your shares of Sara Lee common stock in the “regular way” market after the record date and before the spin off, you also will be selling your right to receive shares of our common stock in connection with the spin off. We expect the shares of our common stock to be distributed by Sara Lee to you on or about September 5, 2006. We refer to the date of the distribution as the “distribution date.”

At the time of the spin off, each share of our common stock will have attached to it one preferred stock purchase right, the principal terms of which are described under “Description of Our Capital Stock—Common Stock—Preferred Stock Purchase Rights.” Where appropriate, references in this information statement to our common stock include the associated rights.

No vote of Sara Lee’s stockholders is required, and therefore you are not being asked for a proxy in connection with the spin off. You do not need to pay any consideration, exchange or surrender your existing shares of Sara Lee common stock or take any other action to receive your shares of our common stock.

There is no current trading market for our common stock, although we expect that a limited market, commonly known as a “when-issued” trading market, will develop on or shortly before the record date for the distribution, and we expect regular way trading of our common stock to begin on the first trading day following the completion of the spin off. Our common stock has been authorized for listing on the New York Stock Exchange under the symbol “HBI.”

In reviewing this information statement, you should carefully consider the matters described under the caption “Risk Factors” beginning on page 11.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this information statement is truthful or complete. Any representation to the contrary is a criminal offense.

This information statement does not constitute an offer to sell or the solicitation of an offer to buy any securities.

The date of this information statement is August 11, 2006

TABLE OF CONTENTS

Trademarks, Trade Names and Service Marks

We own or have rights to use the trademarks, service marks and trade names that we use in conjunction with the operation of our business. Some of the more important trademarks that we own or have rights to use that appear in this information statement include theHanes, Champion, C9 by Champion, Playtex, Bali, L’eggs, Just my Size, barely there, Wonderbra, Beefy-T, Outer Banks andDuofold marks, which may be registered in the United States and other jurisdictions. Each trademark, trade name or service mark of any other company appearing in this information statement is, to our knowledge, owned by such other company.

i

SUMMARY

The following is a summary of material information discussed in this information statement. This summary may not contain all the details concerning the spin off or other information that may be important to you. To better understand the spin off and our business and financial position, you should carefully review this entire information statement. Unless the context otherwise requires, references in this information statement to “Hanesbrands,” “we,” “our” and “us” mean the Sara Lee Branded Apparel Americas and Asia business which will be contributed in the spin off to Hanesbrands Inc., a Maryland corporation, and its subsidiaries. References in this information statement to “Sara Lee” mean Sara Lee Corporation, a Maryland corporation, and its subsidiaries, unless the context otherwise requires.

We describe in this information statement the businesses to be transferred to us by Sara Lee in the spin off as if the transferred businesses were our business for all historical periods described. References in this information statement to our historical assets, liabilities, products, businesses or activities of our business are generally intended to refer to the historical assets, liabilities, products, businesses or activities of the transferred businesses as the businesses were conducted as part of Sara Lee and its subsidiaries prior to the spin off.

Our Company

We are a consumer goods company with a portfolio of leading apparel brands, includingHanes, Champion, Playtex, Bali, Just My Size, barely thereandWonderbra. We design, manufacture, source and sell a broad range of apparel essentials such as t-shirts, bras, panties, men’s underwear, kids’ underwear, socks, hosiery, casualwear and activewear. Our brands hold either the number one or number two U.S. market position by sales in most product categories in which we compete.

| | | | | | | | |

| | | Industrywide

U.S. Retail Sales

(in billions)

2005 | | Compound Annual Growth

Rate Between 2003 and

2005 | | | Hanesbrands 2005 U.S.

Market Position by

Sales |

T-shirts | | $ | 21.3 | | 8.4 | % | | #1 |

| | | |

Bras | | | 5.1 | | 4.5 | | | 2 |

| | | |

Fleece | | | 4.9 | | (2.7 | ) | | 1 |

| | | |

Socks | | | 4.7 | | 3.5 | | | 1 |

| | | |

Men’s Underwear | | | 3.0 | | 3.7 | | | 1 |

| | | |

Panties | | | 3.0 | | 3.1 | | | 2 |

| | | |

Sheer Hosiery | | | 1.0 | | (16.7 | ) | | 1 |

| | | |

Kids’ Underwear | | | 0.8 | | 5.4 | | | 1 |

Source: The NPD Group/Consumer Panel TrackSM, rolling year-end, as of December 2005.

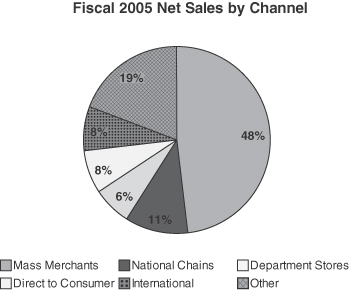

In fiscal 2005, we generated $4.7 billion in net sales and $359.5 million in income from operations. Our products are sold through multiple distribution channels. In fiscal 2005, 48% of our net sales were to mass merchants, 11% were to national chains, 6% were to department stores, 8% were direct to consumer, 8% were in our international segment and 19% were to other retail channels such as embellishers, specialty retailers, warehouse clubs and sporting goods stores. In addition to designing and marketing apparel essentials, we have a long history of operating a global supply chain which incorporates a mix of self-manufacturing, third-party contractors and third-party sourcing.

The apparel essentials segment of the apparel industry is characterized by frequently replenished items, such as t-shirts, bras, panties, men’s underwear, kids’ underwear, socks and hosiery. Growth and sales in the apparel

essentials industry are not primarily driven by fashion, in contrast to other areas of the broader apparel industry. Rather, we focus on the core attributes of comfort, fit and value, while remaining current with regard to consumer trends.

Our business is currently part of Sara Lee, and our assets and liabilities consist of those that Sara Lee attributes to its branded apparel business (excluding its European and U.K. operations, which have been sold by Sara Lee). Following the spin off, we will be an independent, publicly traded company, and Sara Lee will not retain any ownership interest in us. In connection with the spin off, we and Sara Lee will enter into a number of agreements that will govern our relationship following the spin off, including agreements pursuant to which we will provide each other with services during a transition period and indemnify each other against certain liabilities arising from our respective businesses and from the spin off. For a more detailed description of these agreements, see “Agreements with Sara Lee.”

Our business is subject to risks. For a more detailed description of these risks, see “Risk Factors.”

Our Competitive Strengths

Strong Brands with Leading Market Positions. Our brands have a strong heritage in the apparel essentials industry. According to The NPD Group/Consumer Panel TrackSM, or “NPD,” our brands possess either the number one or number two market position in the United States in most of the product categories in which we compete. Our brands enjoy high awareness among consumers according to a 2006 brand equity analysis by Millward Brown Market Research. According to a 2005 survey of consumer brand awareness by Women’s Wear Daily, we own three of the top five most recognized apparel and accessory brands among women in the United States, withHanes(number one), L’eggs (number three) and Hanes Her Way(number four) (now referred to asHanes). According to NPD, our largest brand,Hanes, is the top selling apparel brand in the United States by units sold. Our creative, focused advertising campaigns have been an important element in the continued success and visibility of our brands. We employ a multimedia marketing plan involving national television, radio, Internet, direct mail and in-store advertising, as well as targeted celebrity endorsements, to communicate the key features and benefits of our brands to consumers. We believe that these marketing programs reinforce and enhance our strong brand awareness across our product categories.

High-Volume, Core Essentials Focus.We sell high-volume, frequently replenished apparel essentials. The majority of our core styles continue from year to year, with variations only in color, fabric or design details, and are frequently replenished by consumers. For example, we believe the average U.S. consumer makes 3.5 trips to retailers to purchase men’s underwear and 4.5 trips to purchase panties annually. We believe that our status as a high-volume seller of core apparel essentials creates a more stable and predictable revenue base and reduces our exposure to dramatic fashion shifts often observed in the general apparel industry.

Significant Scale of Operations. We are the largest seller of apparel essentials in the United States as measured by sales. As an example of the scale of our operations, we manufactured and sold over 400 million t-shirts (innerwear and outerwear) and almost half a billion pairs of socks in fiscal 2005. Most of our products are sold to large retailers which have high-volume demands. We have met the demands of our customers by developing vertically integrated operations and an extensive network of owned facilities and third-party manufacturers over a broad geographic footprint. We believe that we are able to leverage our significant scale of operations to provide us with greater manufacturing efficiencies, purchasing power and product design, marketing and customer management resources than our smaller competitors.

Strong Customer Relationships. We sell our products primarily through large, high-volume retailers, including mass merchants, department stores and national chains. We have strong, long-term relationships withour top customers, including relationships of over ten years with each of our top ten customers. The size and operational scale of the high-volume retailers with which we do business require extensive category and product

2

knowledge and specialized services regarding the quantity, quality and planning of orders. In the late 1980s, we undertook a shift in our approach to our relationships with our largest customers when we sought to align significant parts of our organization with corresponding parts of their organizations. For example, we are organized into teams that sell to and service our customers across a range of functional areas, such as demand planning, replenishment and logistics. We also have entered into customer-specific programs such as the introduction in 2004 ofC9 by Champion products marketed and sold through Target stores. Through these efforts, we have become the largest apparel essentials supplier to many of our customers.

Significant Cash Flow Generation. Due to our strong brands and market position, our business has historically generated significant cash flow. In fiscal 2003, 2004 and 2005, we generated $416.7 million, $410.2 million and $446.8 million, respectively, of cash from operating activities net of cash used in investing activities. Our cash flow gives us the flexibility to create shareholder value by investing in our business, reducing debt and returning capital to our shareholders.

Strong Management Team. We have strengthened our management team through the addition of experienced executives in key leadership roles. Richard Noll, our Chief Executive Officer, has extensive management experience in the apparel and consumer products industries. During his 14-year tenure at Sara Lee, Mr. Noll led Sara Lee’s sock and hosiery businesses, Sara Lee Direct and Sara Lee Mexico (all of which are now part of our business), as well as the Sara Lee Bakery Group and Sara Lee Australia. Lee Wyatt, our Chief Financial Officer, has broad experience in executive financial management, including tenures as Chief Financial Officer at Sonic Automotive, a publicly traded automotive aftermarket supplier, and Sealy Corporation. Gerald Evans, our Chief Supply Chain Officer and Michael Flatow, our General Manager, Wholesale Americas, also add significant experience and leadership to our management team. The additions of Messrs. Noll and Wyatt complement the leadership and experience provided by Lee Chaden, our Executive Chairman, who has extensive experience within the apparel and consumer products industries.

Key Business Strategies

Historically, we have operated as part of Sara Lee, sharing services and capital with Sara Lee’s food, beverage and household products businesses. Following our spin off from Sara Lee, we will become a more tightly focused apparel essentials company. As an independent publicly traded company, we believe we will be better positioned to compete in the apparel essentials industry and to invest in and grow our business. Our mission is to grow earnings and cash flow by integrating our operations, optimizing our supply chain, increasing our brand leadership and leveraging and strengthening our retail relationships. Specifically, we intend to focus on the following strategic initiatives:

Create a More Integrated, Focused Company. Historically, we have had a decentralized operating structure, with many distinct operating units. We are in the process of consolidating functions, such as purchasing, finance, manufacturing/sourcing, planning, marketing and product development, across all of our product categories in the United States. We also are in the process of integrating our distribution operations and information technology systems. We believe that these initiatives will streamline our operations, improve our inventory management, reduce costs, standardize processes and allow us to distribute our products more effectively to retailers. We expect that our initiative to integrate our technology systems also will provide us with more timely information, increasing our ability to allocate capital and manage our business more effectively.

Develop a Lower-Cost Efficient Supply Chain. As a provider of high-volume products, we are continually seeking to improve our cost-competitiveness and operating flexibility through supply chain initiatives. In this regard, we have recently launched two textile manufacturing projects outside of the United States—an owned textile manufacturing facility in the Dominican Republic, which began production in early 2006, and a strategic alliance with a third-party textile manufacturer in El Salvador, which began production in 2005. Over the

3

next several years, we will continue to transition additional parts of our supply chain from the United States to locations in Central America, the Caribbean Basin and Asia in an effort to optimize our cost structure. We intend to continue to self-manufacture core products where we can protect or gain a significant cost advantage through scale or in cases where we seek to protect proprietary processes and technology. We plan to continue to selectively source from third-party manufacturers product categories that do not meet these criteria. We expect that in future years our supply chain will become more balanced across the Eastern and Western Hemispheres. Our customers require a high level of service and responsiveness, and we intend to continue to meet these needs through a carefully managed facility migration process. We expect that these changes in our supply chain will result in significant cost efficiencies and increased asset utilization.

Increase the Strength of Our Brands with Consumers. Our advertising and marketing campaigns have been an important element in the success and visibility of our brands. We intend to increase our level of marketing support behind our key brands with targeted, effective advertising and marketing campaigns. For example, in fiscal 2005, we launched a comprehensive marketing campaign titled “Look Who We’ve Got Our Hanes on Now,” which we believe significantly increased positive consumer attitudes about theHanes brand in the areas of stylishness, distinctiveness and up-to-date products.

Our ability to react to changing customer needs and industry trends will continue to be key to our success. Our design, research and product development teams, in partnership with our marketing teams, drive our efforts to bring innovations to market. We intend to leverage our insights into consumer demand in the apparel essentials industry to develop new products within our existing lines and to modify our existing core products in ways that make them more appealing, addressing changing customer needs and industry trends. Examples of our success to date include:

| | • | | Tagless garments—where the label is embroidered or printed directly on the garment instead of attached on a tag—which we first released in t-shirts under ourHanes brand (2002), and subsequently expanded into other products such as outerwear tops (2003) and panties (2004). |

| | • | | “Comfort Soft” bands in our underwear and bra lines, which deliver to our consumers a softer, more comfortable feel with the same durable fit (2004 and 2005). |

| | • | | New versions of our Double Dry wicking products and Friction Free running products under ourChampion brand (2005). |

| | • | | The “no poke” wire which was successfully introduced to the market in ourBali brand bras (2004). |

Strengthen Our Retail Relationships. We intend to expand our market share at large, national retailers by applying our extensive category and product knowledge, leveraging our use of multi-functional customer management teams and developing new customer-specific programs such asC9 by Champion for Target. Our goal is to strengthen and deepen our existing strategic relationships with retailers and develop new strategic relationships. Additionally, we plan to expand distribution by providing manufacturing and production of apparel essentials products to specialty stores and other distribution channels, such as direct to consumer through the Internet.

We were incorporated in Maryland on September 30, 2005. Our principal executive offices are located at 1000 East Hanes Mill Road, Winston-Salem, North Carolina 27105. Our main telephone number is (336) 519-4400.

4

Questions and Answers Relating to the Spin Off

The following is a brief summary of the terms of the spin off. Please see “The Spin Off” for a more detailed description of the matters described below.

| A: | The spin off is the method through which Sara Lee will separate its existing businesses into two independent, publicly traded companies. In the spin off, Sara Lee will distribute to its stockholders all of the outstanding shares of our common stock. Following the spin off, we will be a separate company from Sara Lee, and Sara Lee will not retain any ownership interest in us. The number of shares of Sara Lee common stock you own will not change as a result of the spin off, although the value of shares of Sara Lee common stock may initially decline as a result of the spin off because the value of our business will no longer be part of the value of Sara Lee. |

| Q: | What is being distributed in the spin off? |

| A: | Approximately 95.1 million shares of our common stock will be distributed in the spin off, based upon the number of shares of Sara Lee common stock outstanding on July 28, 2006.The shares of our common stock to be distributed by Sara Lee will constitute all of the issued and outstanding shares of our common stock immediately after the spin off. Each share of our common stock will have attached to it one preferred stock purchase right. For more information on the shares being distributed in the spin off, see “Description of Our Capital Stock—Common Stock” and “Description of Our Capital Stock—Certain Provisions of Maryland Law and of Our Charter and Bylaws That Could Have the Effect of Delaying, Deferring or Preventing a Change in Control—Rights Agreement.” |

| Q: | What will I receive in the spin off? |

| A: | Holders of Sara Lee common stock will receive a pro rata dividend of one share of our common stock for every eight shares of Sara Lee common stock held by them on the record date and not subsequently sold in the “regular way” market. For more information on the shares being distributed in the spin off, see “Description of Our Capital Stock—Common Stock.” |

| Q: | What is the reason for the spin off? |

| A: | The following potential benefits were considered by Sara Lee’s board of directors in making the determination to approve the spin off: |

| | • | | enabling investors to invest directly in our business; |

| | • | | allowing both Sara Lee and us to focus on our respective core businesses; |

| | • | | creating more effective management incentives; and |

| | • | | providing our business with direct access to capital to further invest in our growth. |

| | For more information on the reasons for the spin off, see “The Spin Off—Reasons for the Spin Off.” |

| Q: | What do I have to do to participate in the spin off? |

| A: | Nothing. If you are a holder of record of Sara Lee common stock on the record date for the spin off you will not be required to pay any cash or deliver any other consideration, including any shares of Sara Lee common stock, in order to receive shares of our common stock in the spin off. As discussed under “The Spin Off—Trading of Sara Lee Common Stock Between the Record Date and Distribution Date,” if you sell your shares of Sara Lee common stock in the “regular way” market after the record date and before the spin |

5

| | off, you also will be selling your right to receive shares of our common stock in connection with the spin off. You are not being asked to provide a proxy with respect to any of your shares of Sara Lee common stock in connection with the spin off. |

| Q: | How will Sara Lee distribute shares of Hanesbrands common stock to me? |

| A: | Holders of shares of Sara Lee common stock on the record date that do not subsequently sell their shares in the “regular way” market will receive shares of our common stock through the transfer agent’s book-entry registration system. These shares will not be in certificated form. As such, instead of a share certificate, Sara Lee stockholders will receive a statement from our transfer agent that details their ownership interest and the method by which they may access their account. For more information, see “The Spin Off—Manner of Effecting the Spin Off.” |

| Q: | If I sell, on or before the distribution date, shares of Sara Lee common stock that I held on the record date, am I still entitled to receive shares of Hanesbrands common stock distributable with respect to the shares of Sara Lee common stock I sold? |

| A: | Shortly before the record date for the spin off, Sara Lee’s common stock will begin to trade in two markets on the NYSE: a “regular way” market and an “ex-distribution” market. If you are a holder of record of shares of Sara Lee common stock as of the record date for the spin off and sell those shares in the “regular way” market after the record date for the spin off and before the spin off, you also will be selling the right to receive the shares of our common stock in connection with the spin off. Conversely, if you are a holder of record of shares of Sara Lee common stock as of the record date for the spin off and sell those shares in the “ex-distribution” market after the record date for the spin off and before the spin off, you will still receive the shares of our common stock in the spin off. |

| Q: | How will fractional shares be treated in the spin off? |

| A: | Sara Lee will not distribute fractional shares of our common stock in the spin off. The distribution agent will aggregate all of the fractional shares and sell them in the open market at then prevailing prices on behalf of our stockholders. You will then receive a cash payment in the amount of your proportionate share of the net sale proceeds, based on the average gross selling price per share of our common stock after making appropriate deductions for any required tax withholdings. For more information on fractional shares, see “The Spin Off—Treatment of Fractional Shares.” |

| Q: | What is the distribution date for the spin off? |

| A: | Shares of our common stock will be distributed by the distribution agent, on behalf of Sara Lee, on or about September 5, 2006. |

| Q: | What are the U.S. federal income tax consequences to me of the spin off? |

| A: | Other than with respect to fractional shares of our common stock, no gain or loss will be recognized by, and no amount will be included in the income of, a holder of Sara Lee common stock upon the receipt of shares of our common stock pursuant to the spin off. |

| | If you receive cash in lieu of a fractional share of our common stock as part of the spin off, you will be treated as though you first received a distribution of the fractional share in the spin off and then sold it for the amount of such cash. You generally will recognize capital gain or loss, provided that the fractional share is considered to be held as a capital asset, measured by the difference between the cash you receive for such fractional share and your tax basis in that fractional share. Such capital gain or loss will be a long-term capital gain or loss if your holding period for such fractional share is more than one year on the distribution date. |

| | Please see “The Spin Off—Material U.S. Federal Income Tax Consequences of the Spin Off” for more detail. |

6

| Q: | Does Hanesbrands intend to pay cash dividends? |

| A: | Effective upon the consummation of the distribution, we intend to adopt a policy of paying, subject to legally available funds, a modest quarterly cash dividend on outstanding shares of our common stock. Our board of directors is free to change our dividend policy at any time, including to increase, decrease or eliminate our dividend. For more information about our dividend policy, see “Dividend Policy.” |

| Q: | Who will manage Hanesbrands after the spin off? |

| A: | We benefit from a management team with an extensive background in both brand management in the consumer goods industry at Sara Lee as well as expertise in effectively executing product extensions and designing and building efficient manufacturing operations. Led by Lee Chaden, who will be our Executive Chairman after the spin off, and Richard Noll, who will be our Chief Executive Officer, our management team possesses deep knowledge of, and extensive experience in, our industry. For more information on our management, see “Management.” |

| Q: | What will the relationship be between Sara Lee and Hanesbrands following the spin off? |

| A: | After the spin off, Hanesbrands and Sara Lee will be independent, publicly traded companies, and Sara Lee will no longer have any ownership interest in us. We will, however, be parties to agreements that will define our ongoing relationship after the spin off. For example, under the terms of a master transition services agreement that we expect to enter into with Sara Lee prior to the consummation of the spin off, Hanesbrands and Sara Lee will provide to each other, for a fee, for a period of 12 months after the spin off, specified support services including human resources and payroll functions, financial and accounting functions and information technology. For more information on our relationship with Sara Lee after the spin off, see “Agreements with Sara Lee.” |

| Q: | Who is the distribution agent for the spin off? |

| A: | Computershare Investor Services, LLC is the distribution agent for the spin off. |

| Q: | Where will Hanesbrands common stock trade? |

| A: | Currently, there is no public market for our common stock. Our common stock has been authorized for listing on the New York Stock Exchange under the symbol “HBI.” |

| | We anticipate that trading will commence on a when-issued basis shortly before the record date. In the context of a spin off, when-issued trading refers to trading in our stock commencing two days before the record date for the distribution and made conditionally because the securities of the spun off entity have not yet been distributed. When-issued trades generally settle within three trading days after the distribution date. On the first trading day following the distribution date, any when-issued trading in respect of our common stock will end and regular way trading will begin. Regular way trading refers to trading after the security has been distributed and typically involves a trade that settles on the third full day following the date of distribution. Shares of our common stock generally will be freely tradable after the spin off. We cannot predict the trading prices for our common stock before or after the distribution date. |

| | For more information on the trading market for our shares, see “The Spin Off—Listing and Trading of Our Common Stock.” |

| Q: | Do I have appraisal rights? |

| A: | No. Holders of Sara Lee common stock have no appraisal rights in connection with the spin off. |

| Q: | Who is the transfer agent for your common stock? |

| A: | Computershare Investor Services, LLC is the transfer agent for our common stock. |

7

SUMMARY FINANCIAL AND OTHER DATA

The following table presents summary historical and pro forma financial data, as well as other data. The statements of income data for each of the fiscal years in the three fiscal years ended July 2, 2005 have been derived from our audited Combined and Consolidated Financial Statements included elsewhere in this information statement. The statements of income data for the thirty-nine weeks ended April 2, 2005 and April 1, 2006 and the balance sheet data as of April 1, 2006 have been derived from our Unaudited Interim Condensed Combined and Consolidated Financial Statements included elsewhere in this information statement. The Unaudited Interim Condensed Combined and Consolidated Financial Statements are not necessarily indicative of the results to be expected for any other interim period or for fiscal 2006 as a whole. However, in the opinion of management, the unaudited interim financial statements include all adjustments (consisting of normal recurring accruals) that are necessary for the fair presentation of the results for the interim period. The historical financial data should be read in conjunction with our historical financial statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Unaudited Pro Forma Combined and Consolidated Financial Statements” included elsewhere in this information statement.

The unaudited pro forma and pro forma as adjusted financial data have been derived from our historical financial statements and adjusted to give effect to the spin off and the related debt incurrence and the use of the proceeds therefrom. These adjustments are described under “Unaudited Pro Forma Combined and Consolidated Financial Statements.” Our historical and unaudited pro forma and pro forma as adjusted financial data are not necessarily indicative of our future performance or of what our financial position and results of operations would have been if we had operated as a separate, stand-alone entity during the periods shown.

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended | | | Thirty-nine Weeks Ended | |

| | | June 28, 2003 | | | July 3, 2004 | | | July 2, 2005 | | | April 2, 2005 | | | April 1, 2006 | |

| | | | | | | | | | | | (unaudited) | | | (unaudited) | |

| | | (in thousands, except per share data) | |

Statements of Income Data: | | | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 4,669,665 | | | $ | 4,632,741 | | | $ | 4,683,683 | | | $ | 3,528,333 | | | $ | 3,352,699 | |

Cost of sales | | | 3,010,383 | | | | 3,092,026 | | | | 3,223,571 | | | | 2,428,997 | | | | 2,248,828 | |

| | | | | | | | | | | | | | | | | | | | |

Gross profit | | | 1,659,282 | | | | 1,540,715 | | | | 1,460,112 | | | | 1,099,336 | | | | 1,103,871 | |

| | | | | |

Selling, general and administrative expenses | | | 1,126,065 | | | | 1,087,964 | | | | 1,053,654 | | | | 775,607 | | | | 749,236 | |

Charges for (income from) exit activities | | | (14,397 | ) | | | 27,466 | | | | 46,978 | | | | (815 | ) | | | 945 | |

| | | | | | | | | | | | | | | | | | | | |

Income from operations | | | 547,614 | | | | 425,285 | | | | 359,480 | | | | 324,544 | | | | 353,690 | |

Interest expense | | | 44,245 | | | | 37,411 | | | | 35,244 | | | | 18,458 | | | | 19,295 | |

Interest income | | | (46,631 | ) | | | (12,998 | ) | | | (21,280 | ) | | | (19,318 | ) | | | (7,783 | ) |

| | | | | | | | | | | | | | | | | | | | |

Income before income taxes | | | 550,000 | | | | 400,872 | | | | 345,516 | | | | 325,404 | | | | 342,178 | |

Income tax expense (benefit) | | | 121,560 | | | | (48,680 | ) | | | 127,007 | | | | 97,911 | | | | 78,970 | |

| | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 428,440 | | | $ | 449,552 | | | $ | 218,509 | | | $ | 227,493 | | | $ | 263,208 | |

| | | | | | | | | | | | | | | | | | | | |

Pro Forma: | | | | | | | | | | | | | | | | | | | | |

Net income per share basic (1) | | $ | 4.51 | | | $ | 4.73 | | | $ | 2.30 | | | $ | 2.39 | | | $ | 2.77 | |

Net income per share diluted (2) | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Other Data: | | | | | | | | | | | | | | | | | | | | |

EBITDA (3) | | $ | 656,269 | | | $ | 539,514 | | | $ | 477,371 | | | $ | 408,630 | | | $ | 436,014 | |

Cash flows from (used in): | | | | | | | | | | | | | | | | | | | | |

Operating activities | | | 493,986 | | | | 471,436 | | | | 506,871 | | | | 390,961 | | | | 460,140 | |

Investing activities | | | (77,296 | ) | | | (61,259 | ) | | | (60,080 | ) | | | (35,689 | ) | | | (71,416 | ) |

Financing activities | | | (233,082 | ) | | | (25,813 | ) | | | (41,377 | ) | | | (11,214 | ) | | | (1,015,812 | ) |

8

| | | | | | | | | | |

| | | April 1, 2006 | |

| | | Actual | | Pro Forma (4) | | Pro Forma as

Adjusted (5) | |

| | | (in thousands) | |

Balance Sheet Data: | | | | | | | | | | |

Cash and cash equivalents | | $ | 455,895 | | $ | — | | $ | 150,000 | |

Total assets | | | 4,205,112 | | | 3,233,372 | | | 3,430,172 | |

Noncurrent liabilities: | | | | | | | | | | |

Noncurrent capital lease obligations | | | 3,951 | | | 3,951 | | | 3,951 | |

Noncurrent deferred tax liabilities | | | 7,171 | | | 14,748 | | | 14,748 | |

Other noncurrent liabilities | | | 43,477 | | | 377,320 | | | 377,320 | |

Total noncurrent liabilities | | | 54,599 | | | 396,019 | | | 396,019 | |

Total long-term debt | | | — | | | — | | | 2,577,125 | |

Total parent companies’ equity | | | 2,662,193 | | | 1,746,739 | | | (206,461 | ) |

| (1) | The number of shares used to compute basic earnings per share is 95,016,942, which is the number of shares of our common stock assumed to be outstanding on the distribution date, based on a distribution ratio of one share of our common stock for every eight shares of Sara Lee common stock that was outstanding at April 1, 2006. |

| (2) | The number of shares used to compute diluted earnings per share will be based on the number of shares of our common stock described in (1) above used to compute basic earnings per share, plus the potential dilution that could occur if restricted stock units and options granted under the equity-based compensation arrangements were exercised or converted into common stock. There will be no potentially dilutive securities outstanding on the distribution date; however potentially dilutive securities will be outstanding shortly after the distribution date, and any resulting dilution could be significant. We have approved certain initial equity compensation awards to our executive officers and other employees, which approvals have been based on a specified dollar value for each award. The number of shares underlying these approved awards will be determined based on the fair market value per share of our common stock on the grant date, which is the 15th trading day after the distribution date. All action necessary to approve these awards has been taken; however, the number of shares subject to the awards cannot be computed until the grant date. |

| (3) | “EBITDA” represents net income before interest, income taxes and depreciation and amortization. EBITDA does not represent and should not be considered as an alternative to net income or net cash from operating activities, as determined by generally accepted accounting principles, or “GAAP,” and our calculation thereof may not be comparable to that reported by other companies. We present EBITDA because we understand that it is used by some investors and lenders to determine a company’s historical ability to service and/or incur indebtedness and to fund ongoing capital expenditures. This belief is based in part on our negotiations with our lenders, who have indicated that the amount of indebtedness we will be permitted to incur will be based, in part, on our EBITDA. EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are: |

| | • | | EBITDA does not reflect our capital expenditures or future requirements for capital expenditures or contractual commitments; |

| | • | | EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| | • | | EBITDA does not reflect the significant interest expense, or the cash requirement necessary to service interest or principal payments, on our debts; |

| | • | | Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and |

| | • | | Other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure. |

9

| | Because of these limitations, you should not consider EBITDA as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA only supplementally. The following is a reconciliation of net income to EBITDA for each of the applicable periods: |

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended | | | Thirty-nine Weeks Ended | |

| | | June 28, 2003 | | | July 3, 2004 | | | July 2, 2005 | | | April 2, 2005 | | | April 1, 2006 | |

Net income | | $ | 428,440 | | | $ | 449,552 | | | $ | 218,509 | | | $ | 227,493 | | | $ | 263,208 | |

Interest expense | | | 44,245 | | | | 37,411 | | | | 35,244 | | | | 18,458 | | | | 19,295 | |

Interest income | | | (46,631 | ) | | | (12,998 | ) | | | (21,280 | ) | | | (19,318 | ) | | | (7,783 | ) |

Income tax expense (benefit) | | | 121,560 | | | | (48,680 | ) | | | 127,007 | | | | 97,911 | | | | 78,970 | |

Depreciation | | | 101,420 | | | | 105,517 | | | | 108,791 | | | | 77,888 | | | | 75,797 | |

Amortization | | | 7,235 | | | | 8,712 | | | | 9,100 | | | | 6,198 | | | | 6,527 | |

| | | | | | | | | | | | | | | | | | | | |

Total EBITDA | | $ | 656,269 | | | $ | 539,514 | | | $ | 477,371 | | | $ | 408,630 | | | $ | 436,014 | |

| | | | | | | | | | | | | | | | | | | | |

See our statements of income data set forth in our historical financial statements included elsewhere in this information statement.

| (4) | Assumes that the spin off occurred as of April 1, 2006. |

| (5) | Assumes that the spin off and the related debt incurrence occurred as of April 1, 2006 and reflects the pro forma adjustments as described in the notes to our “Unaudited Pro Forma Combined and Consolidated Financial Statements,” as well as the incurrence of $1.65 billion of debt under a proposed new senior secured credit facility, $450.0 million of debt under a proposed new senior secured second lien credit facility and $500.0 million of debt under a proposed new bridge loan facility with an estimated blended interest rate of 8.0%, and the payment to Sara Lee of $2.4 billion from the proceeds of such debt incurrence. |

10

RISK FACTORS

You should carefully consider the following risks and other information in this information statement in evaluating our company and common stock. Any of the following risks, as well as additional risks and uncertainties not currently known to us or that we currently deem immaterial, could materially and adversely affect our business, results of operations or financial condition.

Risks Related to Our Business

A significant portion of our textile manufacturing operations are located in higher-cost locations, placing us at a product cost disadvantage to our competitors who have a higher percentage of their manufacturing operations in lower-cost, offshore locations.

Though there has been a general industrywide migration of manufacturing operations to lower-cost locations, such as Central America, the Caribbean Basin and Asia, a significant portion of our textile manufacturing operations are still located in higher-cost locations, such as the United States. In addition, our competitors generally source or produce a greater portion of their textiles from regions with lower costs than us, placing us at a cost disadvantage. Our competitors are able to exert pricing pressure on us by using their manufacturing cost savings to reduce prices of their products, while maintaining higher margins than us. To remain competitive, we must, among other things, react to these pricing pressures by lowering our prices from time to time. We will continue to experience pricing pressure and remain at a cost disadvantage to our competitors unless we are able to successfully migrate a greater portion of our textile manufacturing operations to lower-cost locations. However, we cannot assure you that our migration plans, as executed, will relieve these pricing pressures and our cost disadvantage.

We are in the process of relocating a significant portion of our textile manufacturing operations to overseas locations and this process involves significant costs and the risk of operational interruption.

We are currently relocating and expect to continue to relocate a significant portion of our textile manufacturing operations to locations in Central America, the Caribbean Basin and Asia. The process of relocating significant portions of our textile manufacturing and production operations has resulted in and will continue to result in significant costs. This process may also result in operational interruptions, which may have an adverse effect on our business, results of operations and financial condition.

The integration of our information technology systems is complex, and any delay or problem with this integration may cause serious disruption or harm to our business.

As part of our efforts to consolidate our operations, we are in the process of integrating currently unrelated information technology systems across our company which have resulted in operational inefficiencies and in some cases increased our costs. This process involves the replacement of eight independent systems environments running on different technology platforms with a unified enterprise system, which will integrate all of our departments and functions onto common software that runs off a single database. We are subject to the risk that we will not able to absorb the level of systems change, commit the necessary resources or focus the management attention necessary for the implementation to succeed. Many key strategic initiatives of major business functions, such as our supply chain and our finance operations, depend on advanced capabilities enabled by the new systems and if we fail to properly execute or if we miss critical deadlines in the implementation of this initiative, we could experience serious disruption and harm to our business.

We operate in a highly competitive and rapidly evolving market, and our market share and results of operations could be adversely affected if we fail to compete effectively in the future.

The apparel essentials market is highly competitive and evolving rapidly. Competition is generally based upon price, brand name recognition, product quality, selection, service and purchasing convenience. Our businesses face competition today from other large corporations and foreign manufacturers. These competitors include Fruit of the Loom, Inc., Warnaco Group Inc., VF Corporation and Maidenform Brands, Inc. in our

11

innerwear business segment and Gildan Activewear, Inc., Russell Corporation and Fruit of the Loom, Inc. in our outerwear business segment. We also compete with many small companies across all of our business segments.

Additionally, department stores and other retailers, including many of our customers, market and sell apparel essentials products under private labels that compete directly with our brands. These customers may buy goods that are manufactured by others, which represents a lost business opportunity for us, or they may sell private label products manufactured by us, which have significantly lower gross margins than our branded products. We also face intense competition from specialty stores that sell private label apparel not manufactured by us, such as Victoria’s Secret, Old Navy and The Gap.

Increased competition may result in a loss of or a reduction in shelf space and promotional support and reduced prices, in each case decreasing our cash flows, operating margins and profitability. Our ability to remain competitive in the areas of price, quality, brand recognition, research and product development, manufacturing and distribution will, in large part, determine our future success. If we fail to compete successfully, our market share, results of operations and financial condition will be materially and adversely affected.

If we fail to manage our inventory effectively, we may be required to establish additional inventory reserves or we may not carry enough inventory to meet customer demands, causing us to suffer lower margins or losses.

We are faced with the constant challenge of balancing our inventory with our ability to meet marketplace needs. Excess inventory reserves can result from the complexity of our supply chain, a long manufacturing process and the seasonal nature of certain products. As a result, we are subject to high levels of obsolescence and excess stock. Based on discussions with our customers and internally generated projections, we produce, purchase and/or store raw material and finished goods inventory to meet our expected demand for delivery. However, we sell a large number of our products to a small number of customers, and these customers are generally not required by contract to purchase our goods. If, after producing and storing inventory in anticipation of deliveries, demand is lower than expected, we may have to hold inventory for extended periods or sell excess inventory at reduced prices, in some cases below our cost. There are inherent uncertainties related to the recoverability of inventory, and it is possible that market factors and other conditions underlying the valuation of inventory may change in the future and result in further reserve requirements. Excess inventory can reduce gross margins or result in operating losses, lowered plant and equipment utilization and lowered fixed operating cost absorption, all of which could have a material adverse effect on our business, results of operations or financial condition. For example, due in part to lower demand for some of our products in 2005 than forecasted, our total inventory reserve for fiscal 2005 was $116 million (which represented an increase of $25 million over fiscal 2004).

Conversely, we also are exposed to lost business opportunities if we underestimate market demand and produce too little inventory for any particular period. Because sales of our products are generally not made under contract, if we do not carry enough inventory to satisfy our customers’ demands for our products within an acceptable time frame, they may seek to fulfill their demands from one or several of our competitors and may reduce the amount of business they do with us. Any such action would have a material adverse effect on our business, results of operations and financial condition.

Sales of and demand for our products may decrease if we fail to keep pace with evolving consumer preferences and trends.

Our success depends on our ability to anticipate and respond effectively to evolving consumer preferences and trends and to translate these preferences and trends into marketable product offerings. If we are unable to successfully anticipate, identify or react to changing styles or trends or misjudge the market for our products, our sales may be lower than expected and we may be faced with a significant amount of unsold finished goods inventory. In response, we may be forced to increase our marketing promotions, provide mark-down allowances to our customers or liquidate excess merchandise, any of which could have a material adverse effect on our net

12

sales and profitability. Our brand image may also suffer if customers believe that we are no longer able to offer innovative products, respond to consumer preferences or maintain the quality of our products.

We rely on a relatively small number of customers for a significant portion of our sales, and the loss of or material reduction in sales to any of our top customers would have a material adverse effect on our business, results of operations and financial condition.

In fiscal 2005, our top ten customers accounted for 64% of our net sales and our top customer, Wal-Mart, accounted for 31% of our net sales. We expect that these customers will continue to represent a significant portion of our net sales in the future. In addition, our top ten customers are the largest market participants in our primary distribution channels across all of our product lines. Any loss of or material reduction in sales to any of our top ten customers, especially Wal-Mart, would be difficult to recapture, and would have a material adverse effect on our business, results of operations and financial condition.

We generally do not sell our products under contracts, and, as a result, our customers are generally not contractually obligated to purchase our products.

We generally do not enter into purchase agreements that obligate our customers to purchase our products, and as a result, most of our sales are made on a purchase order basis. For example, we have no agreements with Wal-Mart that obligate Wal-Mart to purchase our products. If any of our customers experiences a significant downturn in its business, or fails to remain committed to our products or brands, the customer is generally under no contractual obligation to purchase our products and, consequently, may reduce or discontinue purchases from us. In the past, such actions have resulted in a decrease in sales and an increase in our inventory and have had an adverse effect on our business, results of operations and financial condition. If such actions occur again in the future, our business, results of operations and financial condition will likely be similarly affected.

Further consolidation among our customer base and continued growth of our existing customers could result in increased pricing pressure, reduced floor space for our products and other changes that could be harmful to our business.

In recent years there has been a growing trend toward retailer consolidation. As a result of this consolidation, the number of retailers to which we sell our products continues to decline and, as such, larger retailers are now able to exercise greater negotiating power when purchasing our products. Continued consolidation in the retail industry could result in further price and other competition that may damage our business. Additionally, as our customers grow larger, they increasingly may require us to provide them with some of our products on an exclusive basis, which could cause an increase in the number of stock keeping units, or “SKUs,” we must carry and, consequently, increase our inventory levels and working capital requirements.

Moreover, as our customers consolidate and grow larger they may increasingly seek markdown allowances, incentives and other forms of economic support which reduce our gross margins and affect our profitability. Our financial performance is negatively affected by these pricing pressures when we are forced to reduce our prices without being able to correspondingly reduce our production costs.

Our customers generally purchase our products on credit, and as a result, our results of operations and financial condition may be adversely affected if our customers experience financial difficulties.

During the past several years, various retailers, including some of our largest customers, have experienced significant difficulties, including restructurings, bankruptcies and liquidations. This could adversely affect us because our customers generally pay us after goods are delivered. Adverse changes in our customers’ financial position could cause us to limit or discontinue business with that customer, require us to assume more credit risk relating to that customer’s future purchases or limit our ability to collect accounts receivable relating to previous purchases by that customer, all of which could have a material adverse effect on our business, results of operations and financial condition.

13

International trade regulations may increase our costs or limit the amount of products that we can import from suppliers in a particular country.

Because a significant amount of our manufacturing and production operations are in, or our products are sourced from, overseas locations, we are subject to international trade regulations. The international trade regulations to which we are subject or may become subject include tariffs, safeguards or quotas. These regulations could limit the countries from which we produce or source our products or significantly increase the cost of operating in or obtaining materials originating in certain countries. Restrictions imposed by international trade regulations can have a particular impact on our business when, after we have moved our operations to a particular location, new unfavorable regulations are enacted in that area or favorable regulations currently in effect are changed. The countries in which our products are manufactured or into which they are imported may from time to time impose additional new regulations, or modify existing regulations, including:

| | • | | additional duties, taxes, tariffs and other charges on imports, including retaliatory duties or other trade sanctions, which may or may not be based on World Trade Organization, or “WTO,” rules, and which would increase the cost of products purchased from suppliers in such countries; |

| | • | | quantitative limits that may limit the quantity of goods which may be imported into the United States from a particular country, including the imposition of further “safeguard” mechanisms by the U.S. government or governments in other jurisdictions, limiting our ability to import goods from particular countries, such as China; |

| | • | | changes in the classification of products that could result in higher duty rates than we have historically paid; |

| | • | | modification of the trading status of certain countries; |

| | • | | requirements as to where products are manufactured; |

| | • | | creation of export licensing requirements, imposition of restrictions on export quantities or specification of minimum export pricing; or |

| | • | | creation of other restrictions on imports. |

Adverse international trade regulations, including those listed above, would harm our business.

Significant fluctuations and volatility in the price of cotton and other raw materials we purchase may have a material adverse effect on our business, results of operations and financial condition.

Cotton is the primary raw material used in the manufacture of many of our products. Our costs for cotton yarn and cotton-based textiles vary based upon the fluctuating and often volatile cost of cotton, which is affected by weather, consumer demand, speculation on the commodities market, the relative valuations and fluctuations of the currencies of producer versus consumer countries and other factors that are generally unpredictable and beyond our control. In addition, fluctuations in crude oil or petroleum prices may also influence the prices of related items used in our business, such as chemicals, dyestuffs, polyester yarn and foam.

We are not always successful in our efforts to protect our business from the volatility of the market price of cotton, through short-term supply agreements and hedges, and our business can be adversely affected by dramatic movements in cotton prices. For example, we estimate that, excluding the impact of futures contracts, a change of $0.01 per pound in cotton prices would affect our annual raw material costs by $3.5 million, at current levels of production. The ultimate effect of this change on our earnings cannot be quantified, as the effect of movements in cotton prices on industry selling prices are uncertain, but any dramatic increase in the price of cotton would have a material adverse effect on our business, results of operations and financial condition.

14

We are incurring substantial indebtedness in connection with the spin off, which will subject us to various restrictions and could decrease our profitability and otherwise adversely affect our business.

We are incurring substantial indebtedness in connection with the spin off and will have total debt of approximately $2.6 billion after giving effect to such incurrence. We will be subject to significant financial and operating restrictions contained in the credit agreements and similar instruments governing our indebtedness after the spin off. These restrictions will affect, and in some cases significantly limit or prohibit, among other things, our ability to:

| | • | | pay dividends or make other distributions; |

| | • | | engage in transactions with affiliates; or |

| | • | | create liens on our assets. |

In addition, some of the credit agreements to which we will become subject will require us to maintain financial ratios. If we fail to comply with the covenant restrictions contained in these credit agreements, that failure could result in a default that accelerates the maturity of the indebtedness under such agreements.

Our substantial leverage also could put us at a significant competitive disadvantage compared to our competitors which are less leveraged. These competitors could have greater financial flexibility to pursue strategic acquisitions, secure additional financing for their operations by incurring additional debt, expend capital to expand their manufacturing and production operations to lower-cost areas and apply pricing pressure on us. In addition, because many of our customers rely on us to fulfill a substantial portion of their apparel essentials demand, any concern these customers may have regarding our financial condition may cause them to reduce the amount of products they purchase from us. Our substantial leverage could also impede our ability to withstand downturns in our industry or the economy in general.

After giving effect to our significant debt incurrence, we may not have sufficient funding for our operations and capital requirements.

We expect to pay $2.4 billion of the proceeds of the borrowings we are incurring in connection with the spin off to Sara Lee, and as a result, those proceeds will not be available for our business needs, such as funding working capital or the expansion of our operations. In addition, the restrictions contained in our credit agreements and similar instruments governing our debt obligations may restrict our ability to obtain additional capital in the future to:

| | • | | fund capital expenditures or acquisitions; |

| | • | | meet our debt payment obligations and capital commitments; |

| | • | | fund any operating losses or future development of our business affiliates; |

| | • | | obtain lower borrowing costs that are available from secured lenders or engage in advantageous transactions that monetize our assets; or |

| | • | | conduct other necessary or prudent corporate activities. |

We may need to incur additional debt or issue equity in order to fund working capital and capital expenditures or to make acquisitions and other investments. We cannot assure you that debt or equity financing will be available to us on acceptable terms or at all. If we are not able to obtain sufficient financing, we may be unable to maintain or expand our business. It may be more expensive for us to raise funds through the issuance of additional debt than it was while we were part of Sara Lee.

If we raise funds through the issuance of debt or equity, any debt securities or preferred stock issued will have rights, preferences and privileges senior to those of holders of our common stock in the event of a liquidation, and the terms of the debt securities may impose restrictions on our operations. If we raise funds through the issuance of equity, the issuance would dilute your ownership interest.

15

To service our substantial debt obligations we may need to increase the portion of the income of our foreign subsidiaries that is expected to be remitted to the United States, which could significantly increase our income tax expense.

We pay U.S. federal income taxes on that portion of the income of our foreign subsidiaries that is expected to be remitted to the United States and be taxable. The amount of the income of our foreign subsidiaries we remit to the United States may significantly impact our U.S. federal income tax rate. In order to service our substantial debt obligations, we may need to increase the portion of the income of our foreign subsidiaries that we expect to remit to the United States, which may significantly increase our income tax expense. Consequently, we believe that our tax rate in future periods is likely to be higher, on average, than our historical income tax rates.

If we fail to meet our payment or other obligations under the senior secured credit facility, the lenders could foreclose on, and acquire control of, substantially all of our assets.

In connection with our incurrence of indebtedness under the senior secured credit facility, the lenders will receive a pledge of substantially all of our existing and future direct and indirect subsidiaries, with certain customary or agreed-upon exceptions for foreign subsidiaries and certain other subsidiaries. Additionally, these lenders generally will have a lien on substantially all of our assets and the assets of our subsidiaries, with certain customary or agreed-upon exceptions. As a result of these pledges and liens, if we fail to meet our payment or other obligations under the senior secured credit facility, the lenders will be entitled to foreclose on substantially all of our assets and, at their option, liquidate these assets.

Our supply chain is reliant on an extensive network of foreign operations and any disruption to or adverse impact on our foreign operations may adversely affect our business, results of operations and financial condition.

We have an extensive global supply chain in which a significant portion of our products are manufactured in or sourced from locations in Central America, the Caribbean Basin, Mexico and Asia. Potential events that may disrupt our foreign operations include:

| | • | | political instability and acts of war or terrorism; |

| | • | | disruptions in shipping and freight forwarding services; |

| | • | | increases in oil prices, which would increase the cost of shipping; |

| | • | | interruptions in the availability of basic services and infrastructure, including power shortages; |

| | • | | fluctuations in foreign currency exchange rates resulting in uncertainty as to future asset and liability values, cost of goods and results of operations that are denominated in foreign currencies; |

| | • | | extraordinary weather conditions or natural disasters, such as hurricanes, earthquakes or tsunamis; and |

| | • | | the occurrence of an epidemic, the spread of which may impact our ability to obtain products on a timely basis. |

Disruptions to our foreign operations have an adverse impact on our supply chain which can result in production and sourcing interruptions, increases in our cost of sales and delayed deliveries of our products to our customers, all of which can have an adverse affect on our business, results of operations and financial condition.

The loss of one or more of our suppliers of finished goods or raw materials may interrupt our supplies and materially harm our business.

We purchase all of the raw materials used in our products and approximately 15% of the apparel designed by us from a limited number of third-party suppliers and manufacturers. Our ability to meet our customers’ needs depends on our ability to maintain an uninterrupted supply of raw materials and finished products from our third-party suppliers and manufacturers. Our business, financial condition or results of operations could be adversely

16

affected if any of our principal third-party suppliers or manufacturers experience production problems, lack of capacity or transportation disruptions. The magnitude of this risk depends upon the timing of the changes, the materials or products that the third-party manufacturers provide and the volume of production.

Our dependence on third parties for raw materials and finished products subjects us to the risk of supplier failure and customer dissatisfaction with the quality of our products. Quality failures by our third-party manufacturers or changes in their financial or business condition which affect their production could disrupt our ability to supply quality products to our customers and thereby materially harm our business.

We may suffer negative publicity if we or our third-party manufacturers violate labor laws or engage in practices that are viewed as unethical or illegal.

We cannot fully control the business and labor practices of our third-party manufacturers, the majority of whom are located in Central America, the Caribbean Basin and Asia. If one of our own manufacturing operations or one of our third-party manufacturers violates or is accused of violating local or international labor laws or other applicable regulations, or engages in labor or other practices that would be viewed in any market in which our products are sold as unethical, we could suffer negative publicity which could tarnish our brands’ image or result in a loss of sales. In addition, if such negative publicity affected one of our customers, it could result in a loss of business for us.

We have approximately 50,000 employees worldwide, and our business operations and financial performance could be adversely affected by changes in our relationship with our employees or changes to U.S. or foreign employment regulations.

We have approximately 50,000 employees worldwide. This means we have a significant exposure to changes in domestic and foreign laws governing our relationships with our employees, including wage and hour laws and regulations, fair labor standards, minimum wage requirements, overtime pay, unemployment tax rates, workers’ compensation rates, citizenship requirements and payroll taxes, changes which would likely have a direct impact on our operating costs. We have approximately 35,500 employees outside of the United States. A significant increase in minimum wage or overtime rates in such countries could have a significant impact on our operating costs and may require that we relocate those operations or take other steps to mitigate such increases, all of which may cause us to incur additional costs, expend resources responding to such increases, and lower our margins.

In addition, some of our employees are members of labor organizations or are covered by collective bargaining agreements. If there were a significant increase in the number of our employees who are members of labor organizations or become parties to collective bargaining agreements, we would become vulnerable to a strike, work stoppage or other labor action by these employees that could have an adverse effect on our business.

Due to the extensive nature of our foreign operations, fluctuations in foreign currency exchange rates could negatively impact our results of operations.

We sell a majority of our products in transactions denominated in U.S. dollars; however, we purchase many of our products, pay a portion of our wages and make other payments in our supply chain in foreign currencies. As a result, if the U.S. dollar were to weaken against any of these currencies, our cost of sales could increase substantially. We are also exposed to gains and losses resulting from the effect that fluctuations in foreign currency exchange rates have on the reported results in our consolidated financial statements due to the translation of operating results and financial position of our foreign subsidiaries. In addition, currency fluctuations can impact the price of cotton, the primary raw material we use in our business.

We have significant unfunded employee benefit liabilities: if assumptions underlying our calculation of these liabilities prove incorrect, the amount of these liabilities could increase or we could be required to make contributions to these plans in excess of our current expectations, both of which could have a negative impact on our cash flows, liquidity and results of operations.

We will assume significant unfunded employee benefit liabilities for pension, postretirement and other retirement benefit qualified and nonqualified plans from Sara Lee in connection with the spin-off. These

17

unfunded liabilities are expected to be approximately $348.6 million. Included in these unfunded liabilities are pension obligations which have not been reflected in our historical financial statements, because these obligations have historically been obligations of Sara Lee. The pension obligations we are assuming are projected to be approximately $266.0 million more than the corresponding pension assets we are acquiring, which will result in our pension plans being underfunded. In addition, we could be required to make contributions to the pension plans in excess of our current expectations if financial conditions change or if the assumptions we have used to calculate our pension costs and obligations turn out to be inaccurate. A significant increase in our funding obligations could have a negative impact on our cash flows, liquidity and results of operations. See “Unaudited Pro Forma Combined and Consolidated Financial Statements.”

Due to restrictions imposed on us related to Sara Lee’s sale of its European branded apparel business, we are prohibited from selling ourWonderbraandPlaytex intimate apparel products in the European Union, as well as certain other countries in Europe and South Africa.

In February 2006, Sara Lee sold its European branded apparel business to an affiliate of Sun Capital. In connection with the sale, Sun Capital received an exclusive, perpetual, royalty-free license to sell and distribute apparel products under theWonderbra andPlaytex trademarks in the member states of the European Union, or the “EU,” as well as Russia, South Africa, Switzerland and certain other nations in Europe (together with the EU, the “Covered Nations”). Due to the exclusive license, we are not permitted to sellWonderbra andPlaytex branded products in the Covered Nations and Sun Capital is not permitted to sellWonderbra andPlaytex branded products outside of the Covered Nations. We are also not permitted to distribute or sell certain apparel products, not includingHanes products, in the Covered Nations until February 2007. Consequently, we will not be able to take advantage of business opportunities that may arise relating to the sale ofWonderbra andPlaytex products in the Covered Nations. In addition, any misuse of theWonderbra andPlaytex brands by Sun Capital could result in bad press and a loss of sales for our products under these brands, any of which may have a material adverse effect on our business, results of operations or financial condition. For more information on these sales restrictions see “Description of Our Business—Intellectual Property.”

The success of our business is tied to the strength and reputation of our brands, including brands which we license to other parties. If other parties take actions that weaken, harm the reputation of, or cause confusion with our brands, our business, and consequently our sales and results of operations, may be adversely affected.