SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 or 15d-16 OF

THE SECURITIES EXCHANGE ACT OF 1934

April 27, 2007

IBERDROLA, S.A.

(Exact name of registrant as specified in its charter)

Cardenal Gardoqui, 8

48008 Bilbao

Spain

(Address of principal executive offices)

Copies to:

Michael S. Immordino

Latham & Watkins

99 Bishopsgate

London EC2M 3XF

United Kingdom

Tel: +44 20 7710 1000

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F:

Form 20-F: x Form 40-F: ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes: ¨ No: x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): Not applicable

Exhibit Index

| Exhibit Number | Description | |

| Exhibit 99.1 | Press release regarding Iberdrola’s 2007 First Quarter Results | |

| Exhibit 99.2 | Iberdrola’s 2007 First Quarter Results | |

| Exhibit 99.3 | Presentation regarding Iberdrola’s 2007 First Quarter Results | |

| Exhibit 99.4 | Report on Iberdrola’s 2007 First Quarter Results | |

| Exhibit 99.5 | Iberdrola and Scottish Power Presentation: Introduction | |

| Exhibit 99.6 | Iberdrola and Scottish Power Presentation: Introduction to Scottish Power and its markets | |

| Exhibit 99.7 | Iberdrola and Scottish Power Presentation: Generation and Supply | |

| Exhibit 99.8 | Iberdrola and Scottish Power Presentation: Wind | |

| Exhibit 99.9 | Iberdrola and Scottish Power Presentation: Scottish Power -Transmission and Distribution | |

| Exhibit 99.10 | Iberdrola and Scottish Power Presentation: Scottish Power - North American Businesses | |

| Exhibit 99.11 | Iberdrola and Scottish Power Presentation: Scottish Power - Strategic Fit & Valuation Considerations | |

| Exhibit 99.12 | Annex to Iberdrola’s 2007 First Quarter Results - Significant Events | |

| Exhibit 99.13 | Other communications in connection with Iberdrola’s increase of its stake in Medgaz and CNE’s authorisation | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| IBERDROLA, S.A. | ||

| (Registrant) | ||

| By | /s/ JULIAN MARTINEZ-SIMANCAS SANCHEZ | |

| Name: Julián Martínez-Simancas Sánchez | ||

| Title: General Secretary | ||

Date: April 27, 2007

Exhibit 99.1

Birth of a world leader

PRESS RELEASE

| 26 April 2007 |  |

| Net profit rose 13.6% to €458.2 million in the first quarter of 2007 | |

IBERDROLA IS NOW ONE OF THE WORLD’S LARGEST ELECTRICITY COMPANIES WITH THE SCOTTISHPOWER OPERATION | ||

INTEGRATED GROUP | ||

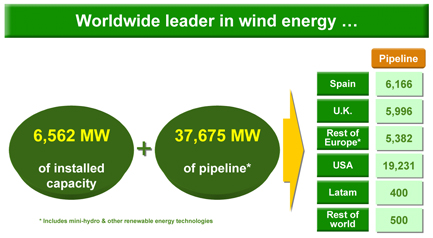

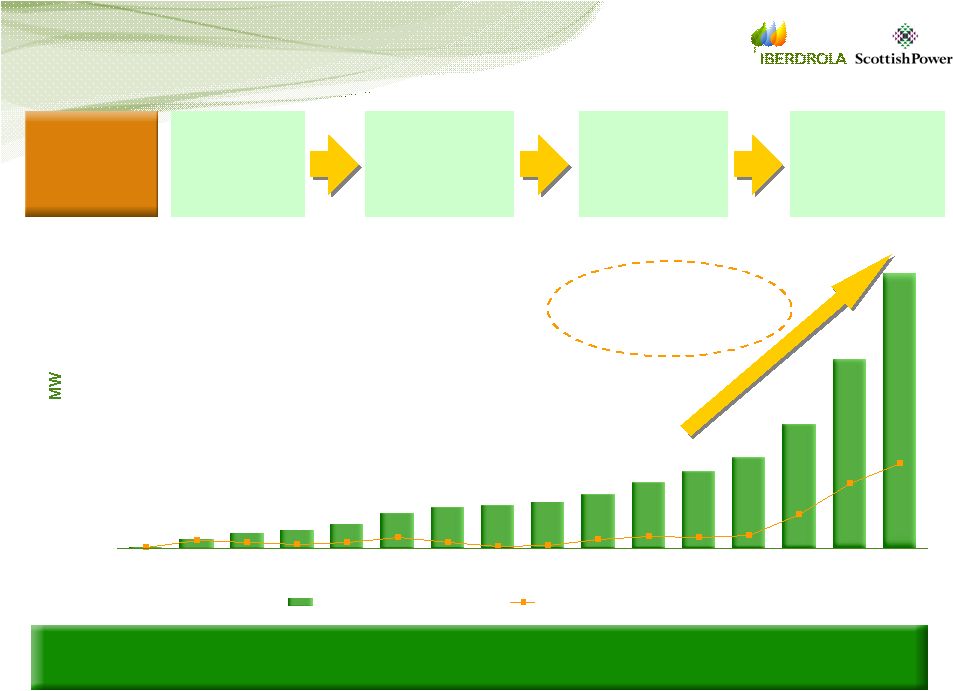

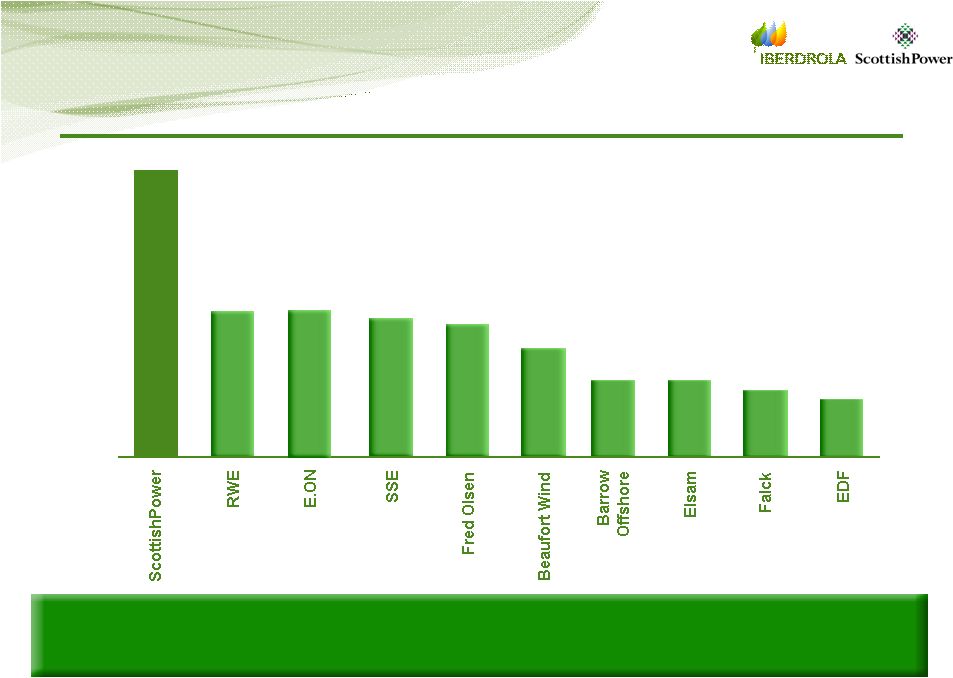

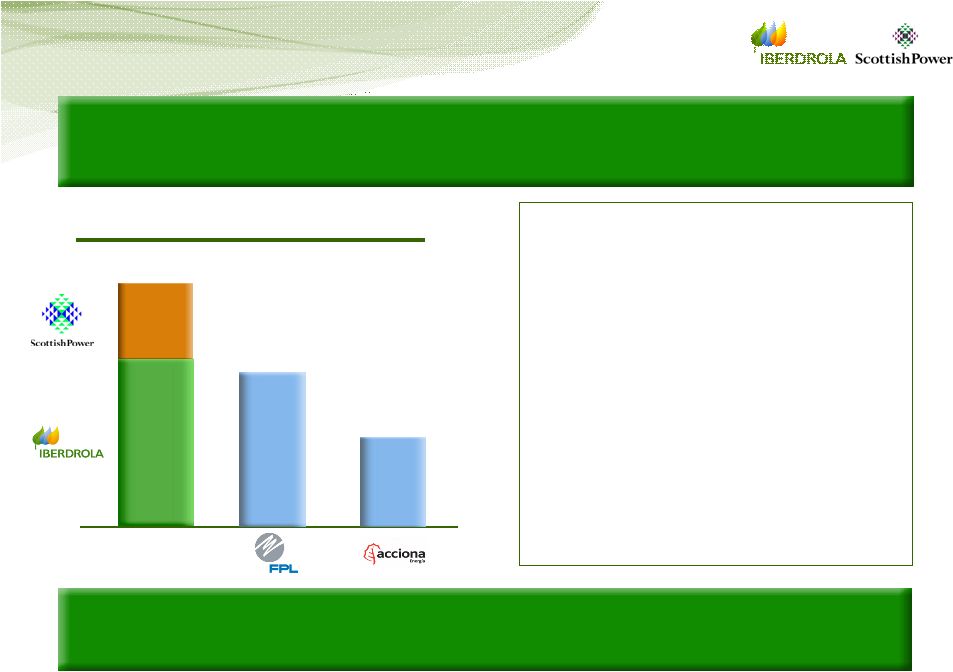

• GROWTH: With an enterprise value of more than €67 billion and a project pipeline in renewables of 37,700 MW, the combination of Iberdrola and ScottishPower represents a platform for future growth in Europe and the Americas | ||

FIRST QUARTER: KEY DATA | ||

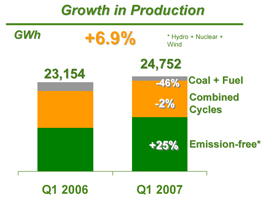

• HIGHER PRODUCTION: Electricity production rose 6.9% to 24,750 GWh; the increase in Spain is 2.5% compared to a fall of 0.5% for the rest of the sector | ||

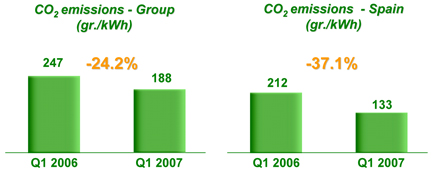

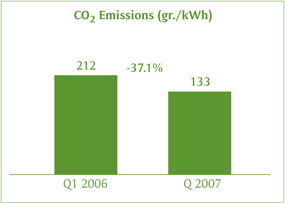

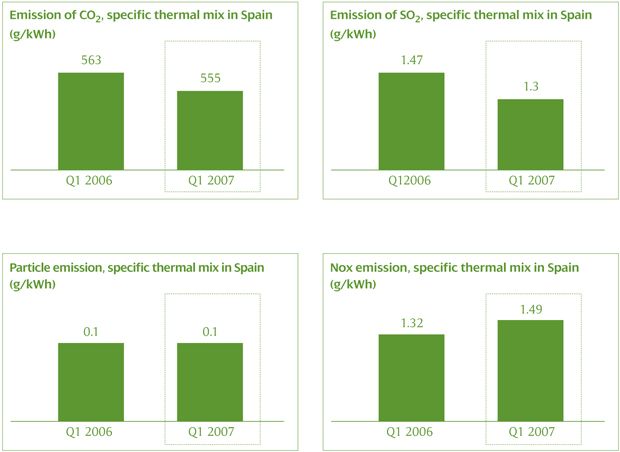

• LOWER EMISSIONS: CO2emissions per kWh were reduced by 37.1% in Spain from 212 to 133 grammes, increasing the ratio of clean energy production to 76% | ||

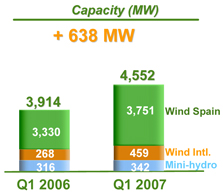

• WIND POWER: World leadership consolidated in this sector, with an operational capacity in renewables of 4,552 MW at the close of the quarter, of which 459 MW was outside Spain | ||

RESULTS | ||

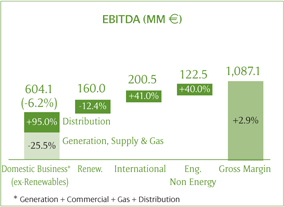

• FACTORS: Group EBITDA rose 2.9% in the period to €1,087.1 million, in a context of lower prices and lower energy demand in Spain | ||

• STRATEGY: International and non-energy businesses increased their contributions to gross operating profit by 41% and 40%, respectively |

| Ø | Communications |

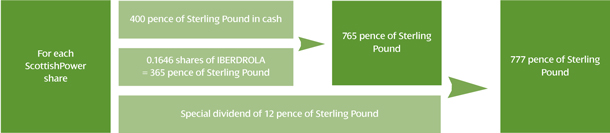

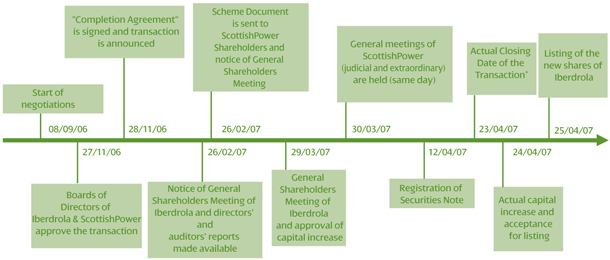

| IBERDROLA has become one of the largest electricity companies in the world having last Monday completed the transaction with ScottishPower for €17.1 billion, one of the biggest in Spanish corporate history. With an enterprise value of more than €67 billion, the combination of the two companies creates a platform for future growth in Europe and the Americas. | |

During the first quarter of the year, IBERDROLA has continued the strategy initiated in 2001 that has enabled it to successfully face this large-scale operation in record time. Net profit rose 13.6% to €458.2 million, in a difficult context of low electricity prices and lower energy demand in Spain. | ||

Completion of theIBERDROLA-ScottishPowertransaction, valued at €17.1 billion and announced in November 2006, is a milestone in the Company’s 100-year history. It creates a world electricity giant, leader in renewable energy and an enterprise value of more than €67 billion. | ||

This operation, in line with the strategy drawn up byIBERDROLA last October for the period 2007-09, will enable the group to accelerate planned growth, offer new long-term business opportunities, diversify risk and maintain financial strength with a view to creating value for shareholders. | ||

The operation, which is among the largest in Spanish business history, has been strongly endorsed by shareholders of both companies – 99.5% at theIBERDROLA Shareholders Meeting and 97.6% at theScottishPowerEGM – as well as by the markets. Between 27 November 2006 and April 23 more than €4 billion in value was created. | ||

| ||

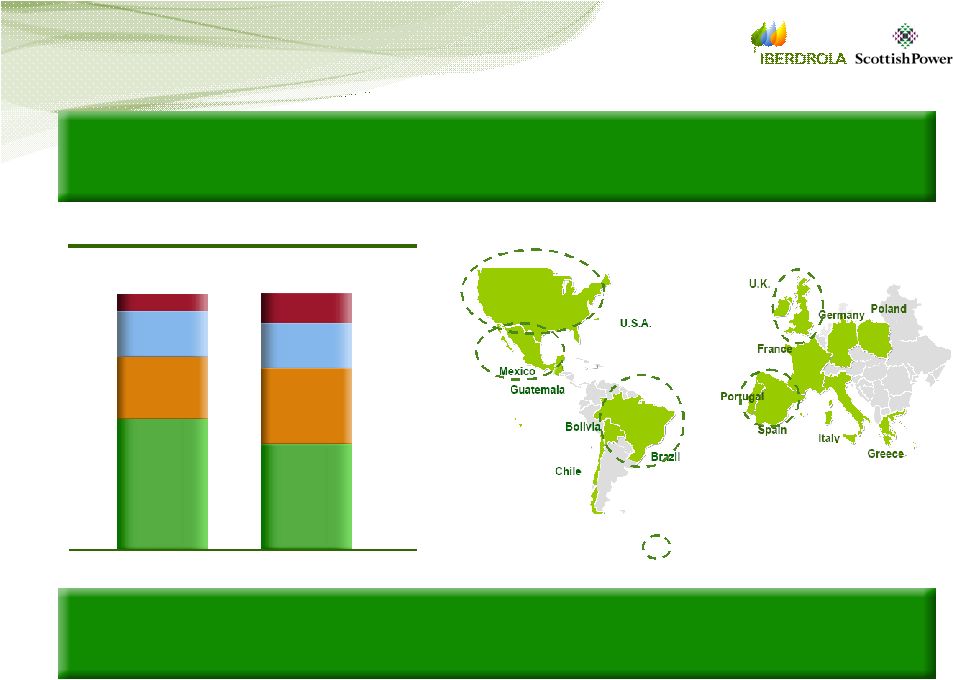

The geographical footprint ofIBERDROLA andScottishPower is now of significant proportions, creating an Atlantic platform. It has operations in Spain, the UK, the United States, Mexico, Brazil, Greece, Portugal, France, Germany, Italy, Poland, Guatemala, Bolivia and Chile. The group also has a substantial project pipeline that will enable it to continue growing in the future. |

| Ø | Communications |

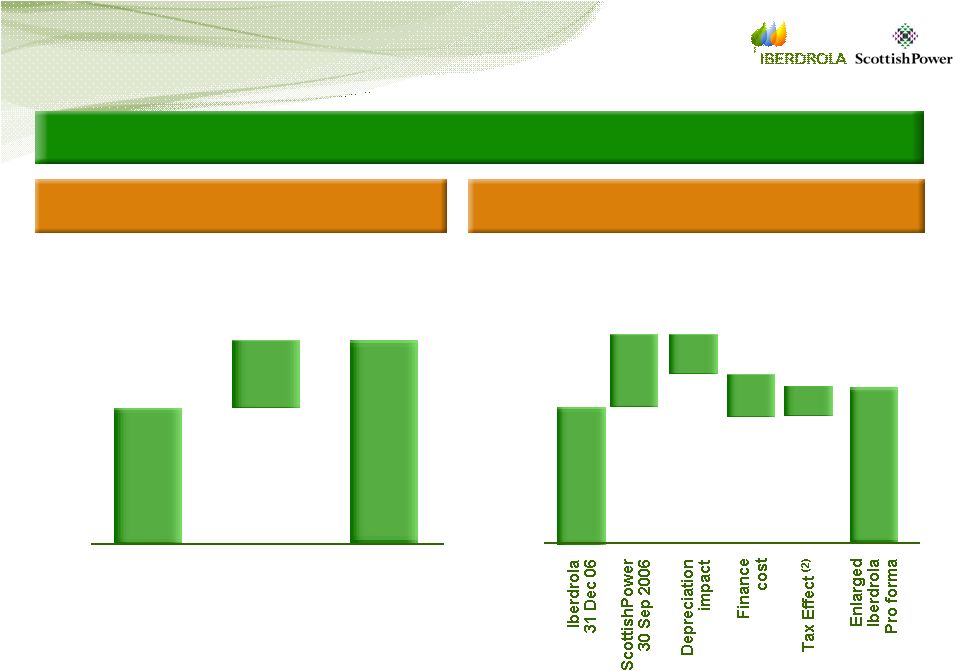

| The combined group has a total installed capacity of around 40,000 megawatts (MW) compared with the 30,500 MW ofIBERDROLA alone (a rise of 28%). Of this new capacity, 32,500 MW relates to conventional generation, an increase of 25% over IBERDROLA’s current level of 26,000 MW. | |

The new integrated group will consolidateIBERDROLA’s world leadership in renewable energy, especially in wind power. Added to the more than 4,500 MW ofIBERDROLA are over 2,000 MW fromScottishPower, mostly from U.S. company PPM, increasing capacity by 44% to 6,562 MW. | ||

The combined project pipeline ofIBERDROLAandScottishPowerin renewable energy stands at 37,675 MW: approximately 6,000 MW are in Spain and another 6,000 MW in the UK, nearly 5,400 MW in the rest of Europe, more than 19,200 MW in the United States, 400 MW in Latin America, and 500 MW in the rest of the world. | ||

The new Group has a significantly larger consumer base, with the 3.3 million customers ofScottishPower adding to the 18.4 million ofIBERDROLA to total 21.7 million in Europe and the Americas, a rise of 18%. | ||

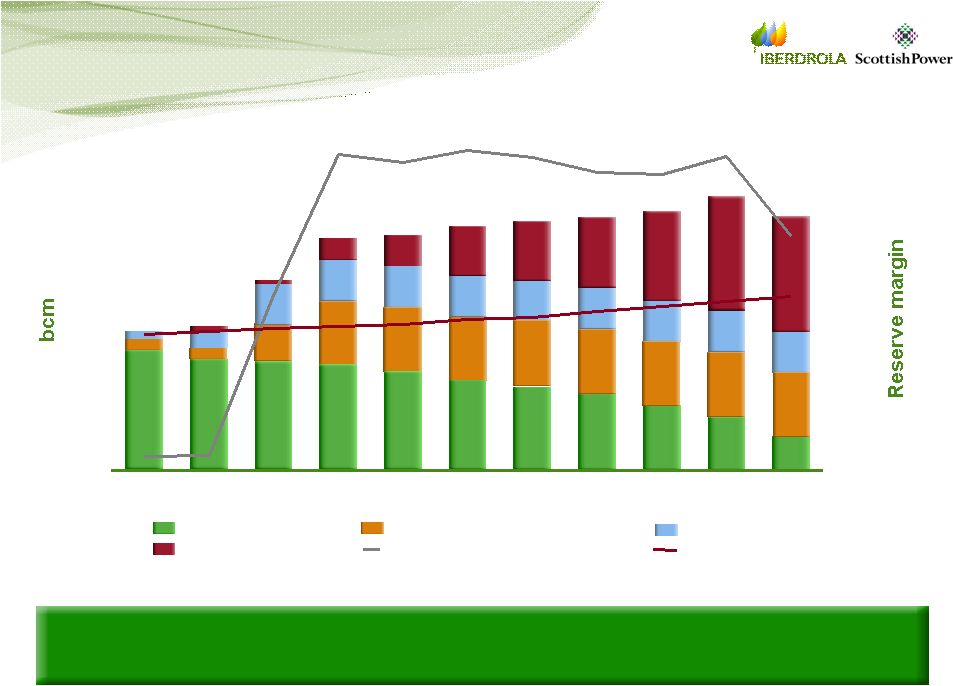

The Company now has 2.7 billion cubic metres of gas storage capacity in the UK and the United States, with significant expansion potential. | ||

| ||

The integration ofIBERDROLA andScottishPower also represents a strengthening of the commitment of both companies with shareholders, customers, employees and communities where they operate, thanks to their powerful business platform. The Group is a leader in renewable energy, with a balanced generation mix, low dependence on foreign supplies, excellent efficiency levels and financially sound. | ||

Net profit rose 13.6% in the first quarter | ||

IBERDROLA’sstrategic decision to invest in basic energy, and its progressive international expansion, have once again been reflected in results for the first quarter of 2007 with a double digit rise in net profit (13.6%) to €458.2 million, in line with expectations for the year as a whole. | ||

In a difficult context in Spain, with falling energy prices (-41%) and modest growth in electricity demand (1.8%), the Company has succeeded in increasing gross operating profit (EBITDA) by 2.9% €1,087.1 million. | ||

IBERDROLA has assigned the bulk of investments over the past few years to increasing electricity production capacity via combined cycles and wind farms. Over the past 12 months it has started up 2,607 megawatts (MW) to achieve |

3

| Ø | Communications |

| total capacity of 30,502 MW at March 31, of which 26,084 MW was in Spain (85.2% of the total). | |

TheIBERDROLA group has increased output in the first three months of the year by 6.9% to 24,752 million kWh, as a result of new capacity. In Spain, the Company generated 18,208 million kWh in the period, a rise of 2.5% over the same period of 2006. | ||

| ||

Increased output from clean energy technology has allowedIBERDROLA to substantially reduce its emissions during the period, both at Group level (24.2% less from 247 grammes of CO2 per kWh to 188 grammes) and in Spain (37.1% lower from 212 grammes of CO2 per kWh to 133 grammes, a third the level for the rest of the sector of 378 grammes. As a result, emission free production came to 76% of the total. | ||

These figures again underline that new investments in generation have not only allowedIBERDROLA to balance and diversify its production mix, placing a limit on traditional technologies, but also to continue contributing to meeting the goals of the Kyoto protocol, to which it is firmly committed. | ||

World leadership in wind power.The Company has continued to strengthen its leadership in renewable energy with new installations and a number of transactions outside Spain in the first three months of the year. | ||

| ||

The most significant of these was the acquisition of CPV Wind Ventures LLC of the United States por €55 million, in line withIBERDROLA’s plans to increase its presence in the wind power market in this country where it already has a project pipeline of 8,500 MW. It also signed an agreement in Italy with API Group to develop wind farms, increased its stake in Greek company Rokas to 52.7% and started work on two wind farms in France. | ||

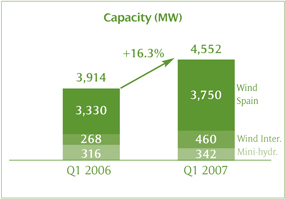

The Company incorporated 638 MW in new wind power capacity over the past 12 months, to a total of 4,552 MW, an increase of 16.3% over the 3,914 MW in |

4

| Ø | Communications |

| March 2006. Of total installed capacity, 4,210 MW relates to wind power – 459 MW outside Spain – and 342 to mini hydro plants. | ||

Renewable energy plants achieved a production of 2,725 million kWh in the first three months (+21%), accounting for 11% of total output, with a significant (23.2%) increase in wind power to 2,578 million kWh. | ||

IBERDROLA envisages renewable energy capacity of 7,000 MW on stream in 2009, almost entirely wind power, and more than 10,000 MW in 2011. | ||

The largest combined cycle operator in Spain.Consistent with its focus on clean energy,IBERDROLA continues to build combined cycle gas plants in Spain and manages a total installed capacity of 5,600 MW. It has plans to bring the Castellón 4 combined cycle on stream this year with installed capacity of 800 MW. |

Project | Capacity (MW managed) | Startup | ||

Castellón | 800 | Operative 2002 | ||

Castejón | 400 | Operative 2003 | ||

Bahía Bizkaia Electricidad | 800 | Operative 2003 | ||

Tarragona | 400 | Operative 2003 | ||

Santurce | 400 | Operative 2004 | ||

Arcos Group I & II | 800 | Operative 2004 | ||

Aceca | 400 | Operative 2005 | ||

Arcos Group III | 800 | Operative 2005 | ||

Escombreras | 800 | Operative 2006 | ||

Total 2002-2005 | 5,600 | 2006 | ||

Castellón 4 | 800 | Projected 2007 | ||

Total 2002-2007 | 6,400 (5,600 owned) | 2007 |

| In this context, a contract was signed recently to acquire the site forIBERDROLA’S first combined cycle plant in Portugal (Figueira da Foz), with a capacity of 850 MW and which could start up operations in 2009. | |

At the same time, and meeting strategic goals of starting up power stations capable of covering increased demand,IBERDROLA has received approval from the Environment Ministry for two hydroelectric plants: a new complex at La Muela (Valencia) to double its capacity to 630 MW and a 175 MW expansion of the San Esteban plant in the Sil basin. | ||

Increase in international contributionFirst quarter results were supported substantially by the fruits of investments in business outside Spain, where EBITDA rose 41% to €200.5 million. | ||

Electricity production in Latin America rose 21.5% over the same period of 2006 to 6,544 million kWh (26.4% of Group total), with a significant contribution from combined cycles which generated 22.4% more to 6,161 million kWh |

5

| Ø | Communications |

| acccounting for 94.1% of electricity produced by the Company in the region. Energy distributed there byIBERDROLA increased 6.2% to 7,254 kWh.IBERDROLA confirmed its position as the number one privately owned energy producer in Mexico, with an installed capacity of 3,814 MW. In February, it began tests at the combined cycle plant at Tamazunchale (1,135 MW) in the State of San Luis Potosí, the largest to be put in operation in this country. | ||

| IBERDROLA THERMAL GENERATION PROJECTS IN MEXICO | ||

Project | Capacity (MW) | Status | ||

Enertek | 120 | 100% operative | ||

Monterrey III | 1,037 | 100% operative | ||

Altamira III y IV | 1,036 | 100% operative | ||

La Laguna II | 500 | 100% operative | ||

Altamira V | 1,121 | 100% operative | ||

Tamazunchale | 1,135 | Operational 2007 | ||

TOTAL | 4,949 | 2007 |

|

Progressive contribution from non-energy business. These businesses, in particular the engineering and construction along with the real estate subsidiaries, played an important part in the first quarter registering a 40% rise in EBITDA to €122.5 million. | |||||||

• Iberdrola Ingeniería y Construcción. The subsidiary has projects under way in more than 25 countries, and during the first quarter won a major contract worth 605 million dollars to modernise and increase capacity of the Laguna Verde nuclear plant in Mexico. | ||||||||

• Iberdrola Inmobiliaria. The company delivered 351 houses during the period and has a total of 16 housing projects under way (1,154 units) and another 20 under negotiation (1,498 homes). In the non-residential sector, it is promoted an office building in Málaga con 1,152 m2 and the Porta Firal project in Barcelona, with 91,111 m2 above street level and 42,363 m2 below street level, due to start construction this summer. | ||||||||

| Positive results in a difficult scenario | ||||||||

| Eur MM | Q1 2007 | Q1 2006 | Change% | |||||

Gross Margin | 1,572.4 | 1,493.9 | +5.3 | |||||

Net Op. Expenses | -439.3 | -391.2 | +12.3 | |||||

EBITDA | 1,087.1 | 1,056.6 | +2.9 | |||||

Operating Profit (EBIT) | 794.8 | 788.4 | +0.8 | |||||

Financial Result | -163.5 | -163.4 | +0.1 | |||||

Non-recurrent assets +Equity Income | 29.3 | 5.7 | N/M | |||||

Net Profit | 458.2 | 403.2 | +13.6 | |||||

| Ø | Communications |

| This communication does not constitute an offer to purchase, sell or exchange or the solicitation of an offer to purchase, sell or exchange any securities. The shares of Iberdrola, S.A. may not be offered or sold in the United States of America except pursuant to an effective registration statement under the Securities Act or pursuant to a valid exemption from registration. | |

FORWARD-LOOKING STATEMENTS | ||

This communication contains forward-looking information and statements about Iberdrola, S.A. and otherwise, including financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, capital expenditures, synergies, products and services, and statements regarding future performance. Forward-looking statements are statements that are not historical facts and are generally identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates” and similar expressions. | ||

Although Iberdrola, S.A. believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of Iberdrola, S.A. shares are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and generally beyond the control of Iberdrola, S.A., that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the public documents sent by Iberdrola, S.A. to theComisión Nacional del Mercado de Valores. | ||

Forward-looking statements are not guarantees of future performance. They have not been reviewed by the auditors of Iberdrola, S.A. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date they were made. All subsequent oral or written forward-looking statements attributable to Iberdrola, S.A. or any of its members, directors, officers, employees or any persons acting on its behalf are expressly qualified in their entirety by the cautionary statement above. All forward-looking statements included herein are based on information available to Iberdrola, S.A. on the date hereof. Except as required by applicable law, Iberdrola, S.A. does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. | ||

7

| Ø | Communications |

Exhibit 99.2

Income Statement

First Quarter 2007

(Unaudited)

Million Euros

| Q1 2007 | Q1 2006 | Change % | |||||||

NET SALES | 2,716.6 | 2,978.4 | (8.8 | ) | |||||

PROCUREMENTS | (1,136.1 | ) | (1,377.1 | ) | (17.5 | ) | |||

EMISSION ALLOWANCES | (8.0 | ) | (107.4 | ) | (92.6 | ) | |||

GROSS MARGIN | 1,572.5 | 1,493.9 | 5.3 | ||||||

EMISSION ALLOWANCES | 2.3 | 6.2 | (62.9 | ) | |||||

NET OPERATING EXPENSES | (439.4 | ) | (391.2 | ) | 12.3 | ||||

Net personnel expenses | (202.9 | ) | (211.4 | ) | (4.0 | ) | |||

Personnel | (243.2 | ) | (253.1 | ) | (3.9 | ) | |||

In-house work on fixed assets | 40.3 | 41.7 | -3.4 | ||||||

Net External Services | (236.5 | ) | (179.8 | ) | 31.5 | ||||

External services | (275.3 | ) | (222.5 | ) | 23.7 | ||||

Other operating revenues | 38.8 | 42.7 | -9.1 | ||||||

TAX | (48.3 | ) | (52.3 | ) | (7.6 | ) | |||

EBITDA | 1,087.1 | 1,056.6 | 2.9 | ||||||

AMORTISATION AND PROVISIONS | (292.3 | ) | (268.2 | ) | 9.0 | ||||

EBIT | 794.8 | 788.4 | .8 | ||||||

TOTAL FINANCIAL REVENUES | 65.8 | 40.7 | 61.7 | ||||||

Financial revenues | 41.9 | 19.4 | 116.0 | ||||||

Positive exchange rate differences | 8.1 | 1.3 | 523.1 | ||||||

Capitalised financial expenses | 15.8 | 20.0 | (21.0 | ) | |||||

TOTAL FINANCIAL EXPENSES | (229.2 | ) | (204.1 | ) | 12.3 | ||||

Interest expenses | (169.7 | ) | (152.4 | ) | 11.4 | ||||

Negative exchange rate differences | (11.4 | ) | (2.9 | ) | 293.1 | ||||

Pension funds | (8.4 | ) | (8.8 | ) | (4.5 | ) | |||

Change in provisions for short term financial investments | (.8 | ) | (.2 | ) | N/A | ||||

Other financial expenses | (38.9 | ) | (39.8 | ) | (2.3 | ) | |||

RESULTS OF COMPANIES CARRIED BY EQUITY METHOD | 19.9 | 4.1 | 385.4 | ||||||

INCOME FROM NON-CURRENT ASSETS | 9.3 | 1.6 | 481.3 | ||||||

PROFIT BEFORE TAXES | 660.6 | 630.7 | 4.7 | ||||||

Corporate income tax | (193.8 | ) | (221.6 | ) | (12.5 | ) | |||

Minorities | (8.6 | ) | (5.9 | ) | 45.8 | ||||

NET PROFIT | 458.2 | 403.2 | 13.6 |

Balance Sheet

First Quarter 2007

(Unaudited)

Million Euros

| March 2007 | December 2006 | Change | |||||||

FIXED ASSETS | 25,532 | 25,188 | 344 | ||||||

Tangible fixed assets | 21,737 | 21,564 | 173 | ||||||

Intangible fixed assets | 967 | 900 | 67 | ||||||

Long-term financial investments | 2,828 | 2,724 | 104 | ||||||

DEFERRED TAX | 1,133 | 1,222 | (89 | ) | |||||

NON-CURRENT ACCOUNTS RECEIVABLE | 884 | 833 | 51 | ||||||

CURRENT ASSETS | 6,453 | 5,818 | 635 | ||||||

Nuclear fuel | 243 | 238 | 5 | ||||||

Inventories | 1,340 | 1,193 | 147 | ||||||

Accounts receivable | 2,759 | 2,791 | (32 | ) | |||||

Taxes receivable | 789 | 602 | 187 | ||||||

Short temp. Financial Investments | 310 | 289 | 21 | ||||||

Cash & equivalents | 1,012 | 705 | 307 | ||||||

| TOTAL ASSETS | 34,002 | 33,061 | 941 | ||||||

| March 2007 | December 2006 | Change | |||||||

SHAREHOLDERS’ EQUITY | 10,564 | 10,567 | (3 | ) | |||||

Capital Stock | 2,705 | 2,705 | |||||||

Reserves and other | 7,298 | 6,100 | 1,198 | ||||||

Profit and Loss | 458 | 1,660 | (1,202 | ) | |||||

Treasury Stock | (3 | ) | (3 | ) | |||||

Exchange differentials | (50 | ) | (44 | ) | (6 | ) | |||

Minority interest | 156 | 149 | 7 | ||||||

LONG TERM PROVISIONS | 1,658 | 1,718 | (60 | ) | |||||

DEFERRED INCOME | 864 | 818 | 46 | ||||||

FINANCIAL DEBT | 14,599 | 14,352 | 247 | ||||||

OTHER LONG-TERM DEBT | 5,217 | 4,541 | 676 | ||||||

OTHER SHORT TERM DEBT | 957 | 847 | 110 | ||||||

PAYABLE TO CO. ACCOUNTED BY EQUITY METHOD | 143 | 218 | (75 | ) | |||||

| TOTAL LIABILITIES | 34,002 | 33,061 | 941 | ||||||

Results by Business

First Quarter 2007

(Unaudited)

Million Euros

| Domestic Energy | International Business | Engineering & Non- Energy | |||||||

Net sales | 1,635.1 | 611.4 | 470.0 | ||||||

Procurements | (506.7 | ) | (344.9 | ) | (284.5 | ) | |||

Emission allowances | (8.0 | ) | |||||||

Gross Margin | 1,120.4 | 266.5 | 185.5 | ||||||

Emission allowances | 2.3 | ||||||||

Net operating expenses | (314.5 | ) | (63.7 | ) | (61.0 | ) | |||

Net personnel expenses | (149.5 | ) | (24.4 | ) | (29.0 | ) | |||

Personnel | (177.0 | ) | (27.8 | ) | (38.4 | ) | |||

In-house work on fixed assets | 27.5 | 3.4 | 9.4 | ||||||

Net External Services | (165.0 | ) | (39.3 | ) | (32.0 | ) | |||

External services | (193.8 | ) | (44.5 | ) | (36.9 | ) | |||

Other operating revenues | 28.8 | 5.2 | 4.9 | ||||||

TAX | (44.0 | ) | (2.3 | ) | (2.0 | ) | |||

EBITDA | 764.2 | 200.5 | 122.5 | ||||||

Amortisation and provisions | (230.1 | ) | (43.6 | ) | (18.6 | ) | |||

EBIT / Operating Profit | 534.1 | 156.9 | 103.9 | ||||||

Financial Result | (142.6 | ) | (21.1 | ) | .1 | ||||

Companies using equity method | .7 | 1.4 | 17.8 | ||||||

Income from non-current assets | 9.8 | (.3 | ) | (.1 | ) | ||||

PROFIT BEFORE TAXES | 402.0 | 136.9 | 121.7 | ||||||

Corporate tax & minorities | (131.1 | ) | (39.1 | ) | (32.3 | ) | |||

Net Profit | 270.9 | 97.8 | 89.4 | ||||||

| First Quarter 2006 | |||||||||

| Million Euros | |||||||||

| Domestic Energy | International Business | Engineering & Non- Energy | |||||||

Net sales | 2,048.6 | 584.6 | 345.2 | ||||||

Procurements | (795.7 | ) | (388.7 | ) | (192.6 | ) | |||

Emission allowances | (107.4 | ) | |||||||

Gross Margin | 1,145.5 | 195.9 | 152.6 | ||||||

Emission allowances | 6.2 | ||||||||

Net operating expenses | (276.0 | ) | (51.8 | ) | (63.5 | ) | |||

Net personnel expenses | (156.2 | ) | (17.9 | ) | (37.3 | ) | |||

Personnel | (181.7 | ) | (21.6 | ) | (49.7 | ) | |||

In-house work on fixed assets | 25.5 | 3.7 | 12.4 | ||||||

Net External Services | (119.8 | ) | (33.9 | ) | (26.2 | ) | |||

External services | (142.7 | ) | (46.1 | ) | (33.8 | ) | |||

Other operating revenues | 22.9 | 12.2 | 7.6 | ||||||

TAX | (48.7 | ) | (1.9 | ) | (1.6 | ) | |||

EBITDA | 827.0 | 142.2 | 87.5 | ||||||

Amortisation and provisions | (211.8 | ) | (40.0 | ) | (16.3 | ) | |||

EBIT / Operating Profit | 615.2 | 102.2 | 71.2 | ||||||

Financial Result | (131.9 | ) | (27.5 | ) | (3.9 | ) | |||

Companies using equity method | (1.5 | ) | 2.8 | 2.7 | |||||

Income from non-current assets | 2.6 | (.6 | ) | (.5 | ) | ||||

PROFIT BEFORE TAXES | 484.4 | 76.9 | 69.5 | ||||||

Corporate tax & minorities | (191.6 | ) | (18.0 | ) | (17.9 | ) | |||

Net Profit | 292.8 | 58.9 | 51.6 | ||||||

Domestic Energy Busines

First Quarter 2007

(Unaudited)

Million Euros

| GENER | RENEW | DISTRIB | SUPPLY | CORP. | |||||||||||

Net sales | 848.9 | 203.4 | 373.1 | 445.4 | (235.7 | ) | |||||||||

Procurements | (316.9 | ) | (1.9 | ) | (419.9 | ) | 232.0 | ||||||||

Emission allowances | (8.0 | ) | |||||||||||||

Gross Margin | 524.0 | 203.4 | 371.2 | 25.5 | (3.7 | ) | |||||||||

Emission allowances | 2.3 | ||||||||||||||

Net operating expenses | (139.0 | ) | (41.1 | ) | (114.0 | ) | (12.4 | ) | (8.0 | ) | |||||

Net personnel expenses | (49.2 | ) | (10.3 | ) | (44.9 | ) | (5.3 | ) | (39.7 | ) | |||||

Personnel | (54.7 | ) | (12.4 | ) | (63.7 | ) | (5.3 | ) | (40.8 | ) | |||||

In-house work on fixed assets | 5.5 | 2.1 | 18.8 | 1.1 | |||||||||||

Net External Services | (89.8 | ) | (30.8 | ) | (69.1 | ) | (7.1 | ) | 31.7 | ||||||

External services | (98.8 | ) | (35.3 | ) | (86.5 | ) | (7.1 | ) | 33.9 | ||||||

Other operating revenues | 9.0 | 4.5 | 17.4 | (2.2 | ) | ||||||||||

TAX | (18.6 | ) | (2.3 | ) | (30.6 | ) | 8.6 | (1.1 | ) | ||||||

EBITDA | 368.7 | 160.0 | 226.6 | 21.7 | (12.8 | ) | |||||||||

Amortisation and provisions | (117.5 | ) | (53.9 | ) | (50.3 | ) | (1.0 | ) | (7.5 | ) | |||||

EBIT / Operating Profit | 251.2 | 106.1 | 176.3 | 20.7 | (20.3 | ) | |||||||||

Financial Result | (33.8 | ) | (31.3 | ) | (23.3 | ) | .1 | (54.2 | ) | ||||||

Companies using equity method | .2 | .7 | (.1 | ) | |||||||||||

Income from non-current assets | (.1 | ) | 7.4 | 2.4 | |||||||||||

PROFIT BEFORE TAXES | 217.5 | 74.8 | 161.1 | 20.7 | (72.1 | ) | |||||||||

Corporate tax & minorities | (69.7 | ) | (27.9 | ) | (51.8 | ) | (6.7 | ) | 25.0 | ||||||

Net Profit | 147.8 | 46.9 | 109.3 | 14.0 | (47.1 | ) | |||||||||

| First Quarter 2006 | |||||||||||||||

| Million Euros | |||||||||||||||

| GENER | RENEW | DISTRIB | SUPPLY | CORP. | |||||||||||

Net sales | 1,345.8 | 215.2 | 265.5 | 618.8 | (396.8 | ) | |||||||||

Procurements | (556.6 | ) | (628.9 | ) | 389.8 | ||||||||||

Emission allowances | (107.4 | ) | |||||||||||||

Gross Margin | 681.8 | 215.2 | 265.5 | (10.1 | ) | (7.0 | ) | ||||||||

Emission allowances | 6.2 | ||||||||||||||

Net operating expenses | (118.5 | ) | (30.6 | ) | (124.9 | ) | (13.6 | ) | 11.6 | ||||||

Net personnel expenses | (53.1 | ) | (5.3 | ) | (51.3 | ) | (11.1 | ) | (35.4 | ) | |||||

Personnel | (57.8 | ) | (6.5 | ) | (69.5 | ) | (11.1 | ) | (36.8 | ) | |||||

In-house work on fixed assets | 4.7 | 1.2 | 18.2 | 1.4 | |||||||||||

Net External Services | (65.4 | ) | (25.3 | ) | (73.6 | ) | (2.5 | ) | 47.0 | ||||||

External services | (73.1 | ) | (27.7 | ) | (90.3 | ) | (9.2 | ) | 57.6 | ||||||

Other operating revenues | 7.7 | 2.4 | 16.7 | 6.7 | (10.6 | ) | |||||||||

TAX | (18.0 | ) | (1.9 | ) | (24.4 | ) | (3.6 | ) | (.9 | ) | |||||

EBITDA | 551.5 | 182.7 | 116.2 | (27.3 | ) | 3.7 | |||||||||

Amortisation and provisions | (96.4 | ) | (41.7 | ) | (64.7 | ) | (2.1 | ) | (6.9 | ) | |||||

EBIT / Operating Profit | 455.1 | 141.0 | 51.5 | (29.4 | ) | (3.2 | ) | ||||||||

Financial Result | (20.0 | ) | (21.2 | ) | (18.1 | ) | 1.0 | (73.6 | ) | ||||||

Companies using equity method | (2.0 | ) | .6 | ||||||||||||

Income from non-current assets | .3 | 2.2 | |||||||||||||

PROFIT BEFORE TAXES | 433.4 | 119.8 | 34.0 | (28.4 | ) | (74.6 | ) | ||||||||

Corporate tax & minorities | (146.9 | ) | (44.0 | ) | (10.9 | ) | 10.1 | .2 | |||||||

Net Profit | 286.5 | 75.8 | 23.1 | (18.3 | ) | (74.4 | ) | ||||||||

STATEMENT OF SOURCES & USES OF FUNDS

First Quarter 2007

(Unaudited)

Million Euros

| Jan - March 2007 | Jan - March 2006 | Difference | |||||||

EBIT | 795.0 | 788.0 | 7.0 | ||||||

Amortisation | 284.0 | 249.0 | 35.0 | ||||||

Provisions | 9.0 | 19.0 | (10.0 | ) | |||||

Provision for the pension funds | (11.0 | ) | 10.0 | (21.0 | ) | ||||

Operating Cash Flow | 1,077.0 | 1,066.0 | 11.0 | ||||||

Interest paid | (183.0 | ) | (195.0 | ) | 12.0 | ||||

Interest received | 39.0 | 41.0 | (2.0 | ) | |||||

Dividends received from affiliates | .0 | 5.0 | (5.0 | ) | |||||

Minority interests | (9.0 | ) | (6.0 | ) | (3.0 | ) | |||

Tax | (193.0 | ) | (221.0 | ) | 28.0 | ||||

Gross Cash Flow | 731.0 | 690.0 | 41.0 | ||||||

Dividends paid | (406.0 | ) | (331.0 | ) | (75.0 | ) | |||

Retained Cash Flow | 325.0 | 359.0 | (34.0 | ) | |||||

Investments | (506.0 | ) | (435.0 | ) | (71.0 | ) | |||

Fixed asset disposals | (9.0 | ) | 2.0 | (11.0 | ) | ||||

Financial asset disposals | .0 | .0 | .0 | ||||||

Taxes on investment activities | (1.0 | ) | (1.0 | ) | .0 | ||||

Pension payments & other | (56.0 | ) | (54.0 | ) | (2.0 | ) | |||

Total Cash Flow Applications | (572.0 | ) | (488.0 | ) | (84.0 | ) | |||

Capital subsidies received | 43.0 | 29.0 | 14.0 | ||||||

Change in working capital | (38.0 | ) | (450.0 | ) | 412.0 | ||||

Change in debt | 242.0 | 549.0 | (307.0 | ) | |||||

Change in consolidation perimeter | 4.0 | 2.0 | 2.0 | ||||||

| .0 | |||||||||

Change in Gross Debt | 246.0 | 551.0 | (305.0 | ) |

1 First Quarter 2007 First Quarter 2007 Results Results 26 26 th April 2007 April 2007 Exhibit 99.3 |

2 DISCLAIMER This document has been prepared by Iberdrola, S.A. (the “Company”) solely for use during the presentation corresponding to the First Quarter 2007 Results. The information and any forward looking statements contained in this document have not been independently verified and no representation or warranty express of implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. None of the Company, or any of its advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document. This document does not constitute an offer or invitation to purchase or subscribe for any securities in accordance with the Spanish Securities Market Law (Law 24/1988, as amended), Royal Decree Law 5/2005 and/or Royal Decree 1310/2005 and the rules and regulations made there under. Furthermore, this document does not constitute an offer to purchase, sell or exchange or the solicitation of an offer to purchase, sell or exchange any securities or the solicitation of any vote or approval in any other jurisdiction. Neither this document nor any part of it shall form the basis of or be relied in connection with any contract or commitment whatsoever. Legal Note |

3 Legal Note IMPORTANT INFORMATION This communication does not constitute an offer to purchase, sell or exchange or the solicitation of an offer to purchase, sell or exchange any securities. The shares of Iberdrola, S.A. may not be offered or sold in the United States of America except pursuant to an effective registration statement under the Securities Act or pursuant to a valid exemption from registration. FORWARD-LOOKING STATEMENTS This communication contains forward-looking information and statements about Iberdrola, S.A. and otherwise, including financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, capital expenditures, synergies, products and services, and statements regarding future performance. Forward-looking statements are statements that are not historical facts and are generally identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates” and similar expressions. Although Iberdrola, S.A. believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of Iberdrola, S.A. shares are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and generally beyond the control of Iberdrola, S.A., that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the public documents sent by Iberdrola, S.A. to the Comisión Nacional del Mercado de Valores. Forward-looking statements are not guarantees of future performance. They have not been reviewed by the auditors of Iberdrola, S.A. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date they were made. All subsequent oral or written forward-looking statements attributable to Iberdrola, S.A. or any of its members, directors, officers, employees or any persons acting on its behalf are expressly qualified in their entirety by the cautionary statement above. All forward-looking statements included herein are based on information available to Iberdrola, S.A. on the date hereof. Except as required by applicable law, Iberdrola, S.A. does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. |

4 Agenda Highlights of the Period Highlights of the Period Analysis of Results Analysis of Results Conclusion Conclusion Consolidated Consolidated By Business By Business |

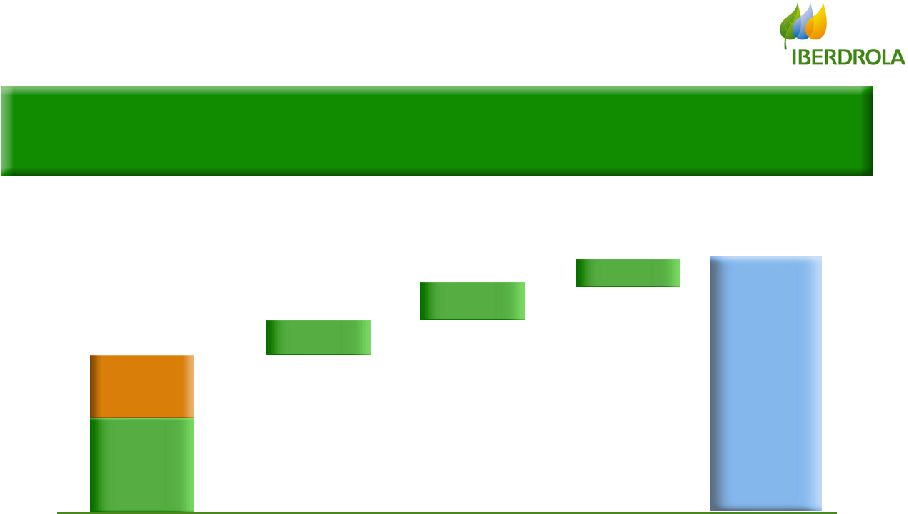

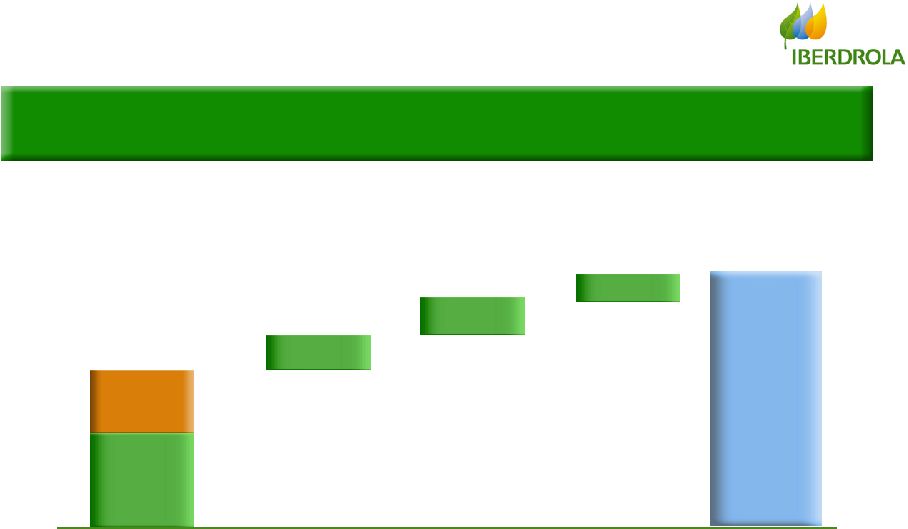

5 Highlights of the period Net Profit up 13.6% to Eur 458.2 MM Higher production (+6.9%) with low cost & emissions-free technologies … in a difficult scenario of low prices & moderate demand growth Efficient management to provide positive results … New transactions in wind energy expansion in the US & Europe Successful closing of ScottishPower transaction 99.5% and 97.6% of the attending capital of Iberdrola and ScottishPower, respectively, voted in favour |

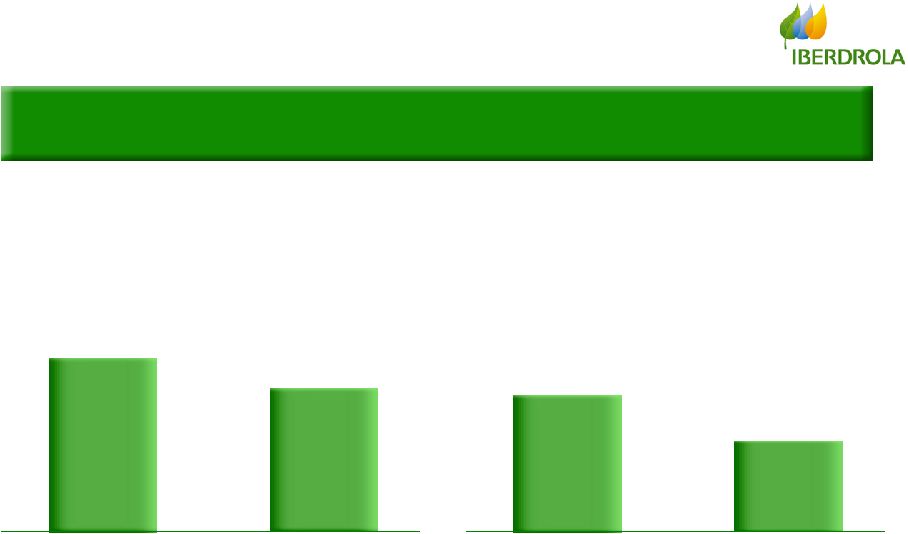

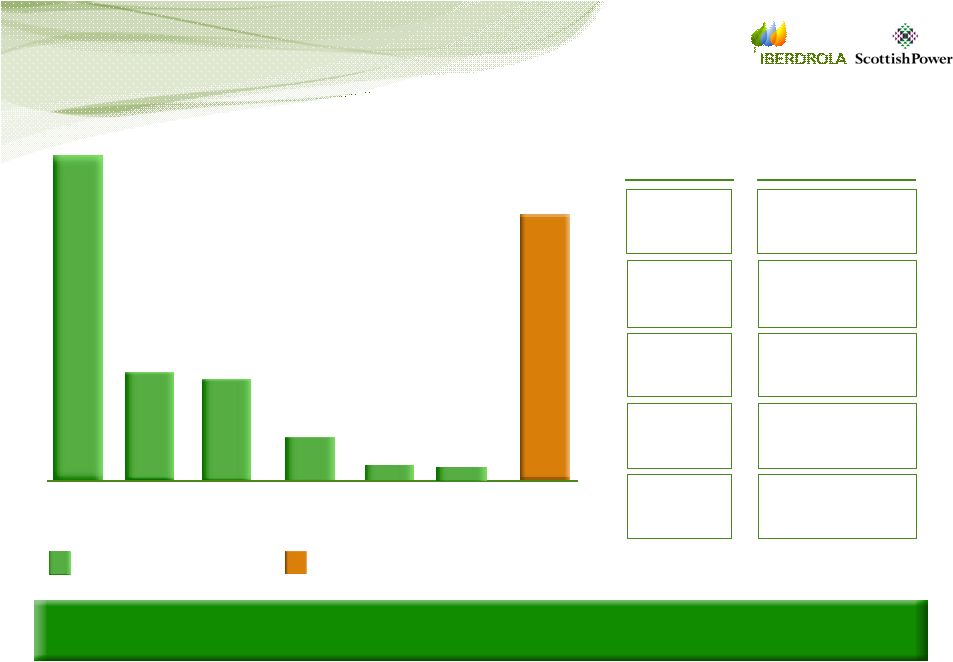

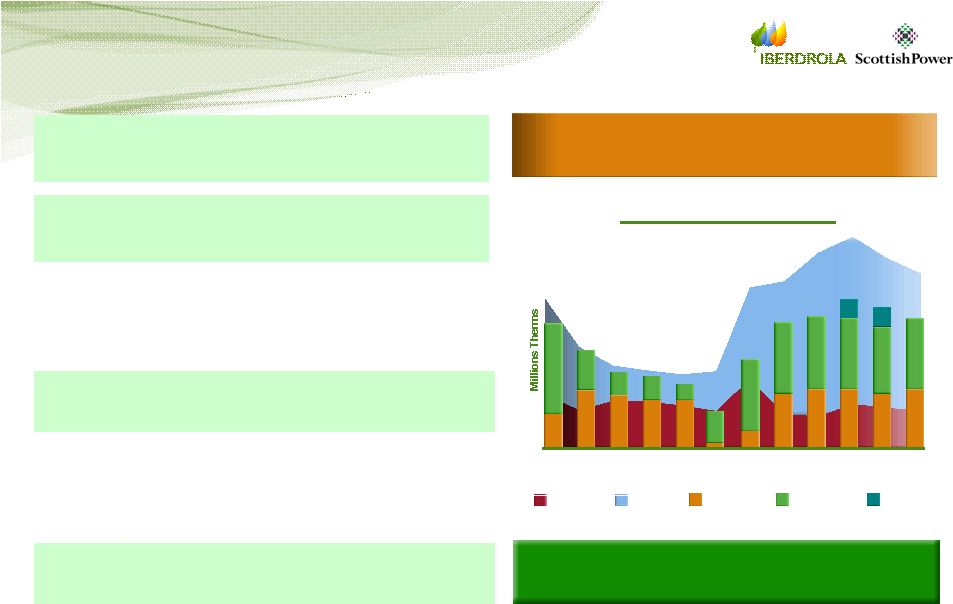

6 24,752 GWh (+6.9%) Production Mix Q1 2007 Production Mix Q1 2007 Nuclear Nuclear 26% 26% Comb. Comb. Cycles Cycles 36% 36% Coal 5% Coal 5% Fuel Fuel 0% 0% Hydro Hydro 20% 20% Wind Wind 11% 11% Cogen. 2% Cogen. 2% . 2% Production - Group Q1 2006 Q1 2007 Combined Combined Cycles Cycles Emission-free* 24,752 24,752 23,154 23,154 Growth in Production Growth in Production -2% -2% -2% +25% +25% +25% +6.9% +6.9% … … boosted by low emission technologies … boosted by low emission technologies … -46% -46% -46% 46% Coal + Fuel Coal + Fuel * Hydro + Nuclear + Wind GWh GWh |

7 Increasing production in Spain by +1.8% with low cost & emissions-free technologies … Production - Spain … … vs. -1.6% of the rest of the sector* vs. -1.6% of the rest of the sector* * Excluding Iberdrola Ordinary Regime -0.6% Special Regime +16.3% +2,442 Hydro -1,339 Nuclear -153 -485 Coal -551 Fuel +349 Wind + Mh +55 Cogeneration C. Cycles GWh GWh |

8 Increasing hydro reserves … Production - Spain 64% 55% 6,170 GWh 7,193 GWh Q1 2006 As of today … … points out for sustainable results in Generation points out for sustainable results in Generation +17% +17% |

9 Q1 2006 CO CO 2 2 emissions - emissions - Group Group (gr./kWh) (gr./kWh) Emissions 76% of Q1 ’07 production in Spain is emissions-free Q1 2007 1/3 of the emissions compared to 1/3 of the emissions compared to the rest of the sector (378* gr/kWh) the rest of the sector (378* gr/kWh) Q1 2006 Q1 2007 CO CO 2 2 emissions - emissions - Spain Spain (gr./kWh) (gr./kWh) 247 188 -24.2% -24.2% 212 133 -37.1% -37.1% * Excluding Iberdrola |

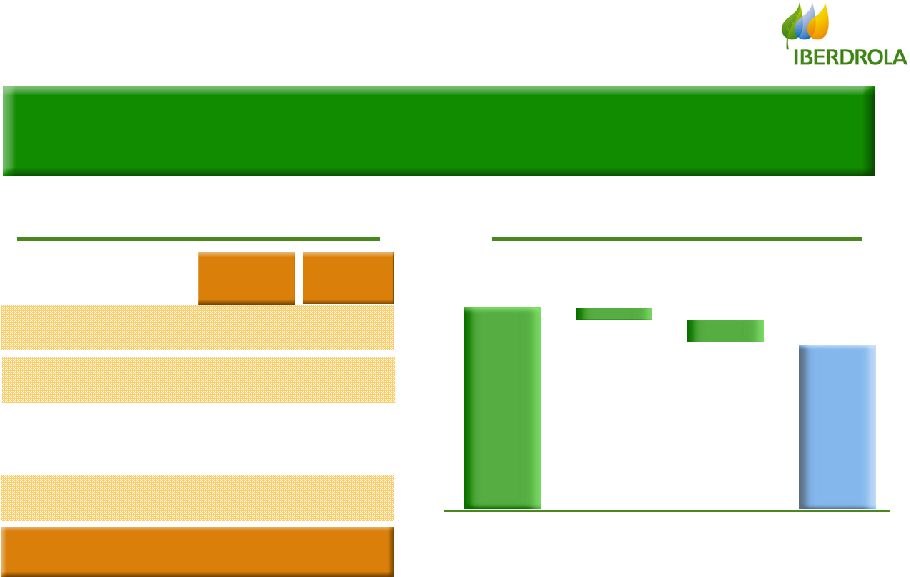

10 Q1 2007 Results Efficient management of assets … Hydro assets + Provides Iberdrola with a balanced generation mix Wind energy assets + Flexibility of gas contracts … … to optimize results in all scenarios to optimize results in all scenarios |

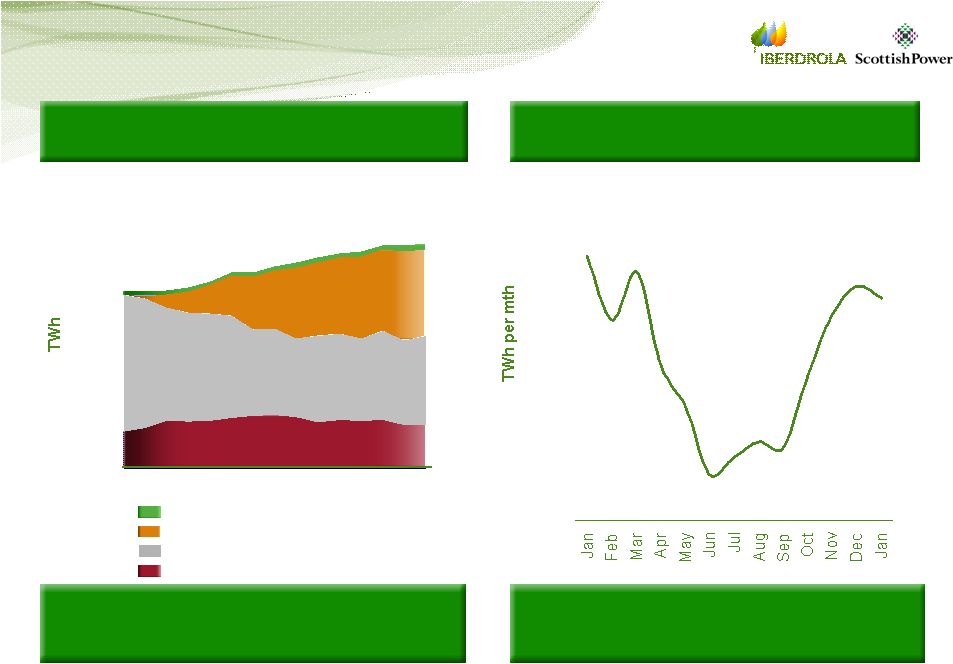

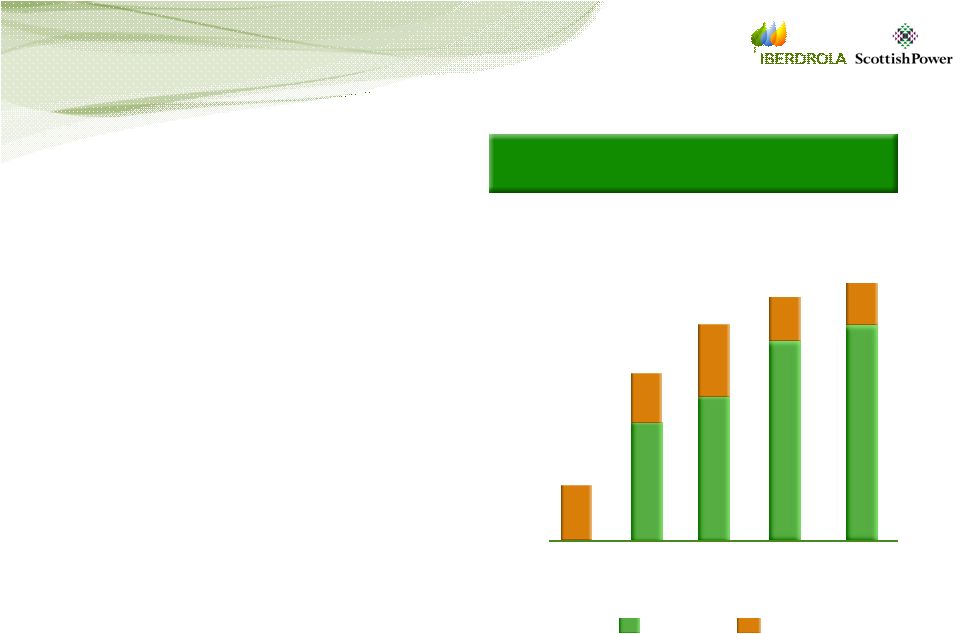

11 EBITDA - Group EBITDA up 2.9% to Eur 1,087.1 MM … compensate Distribution Supply & Gas International Non-energy Generation Spain Wind energy business … … in a difficult scenario of low prices & in a difficult scenario of low prices & moderate demand growth moderate demand growth |

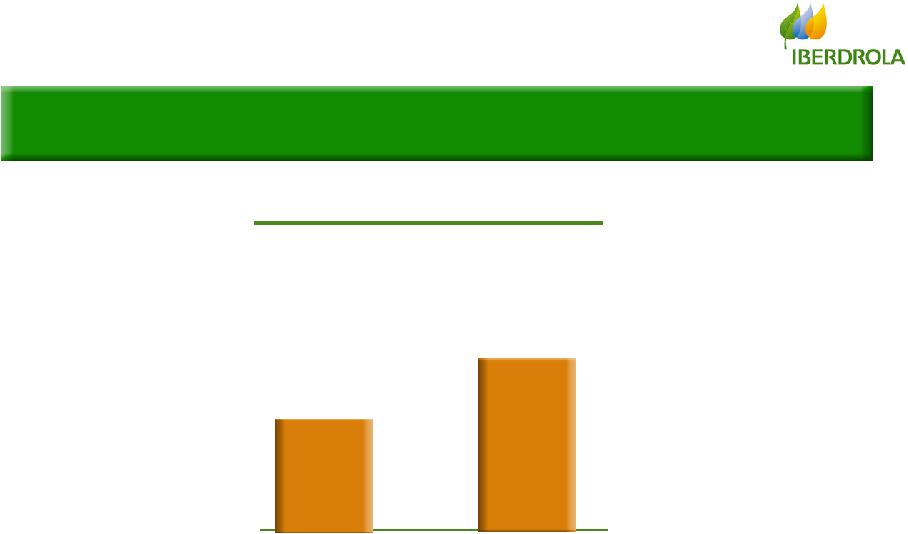

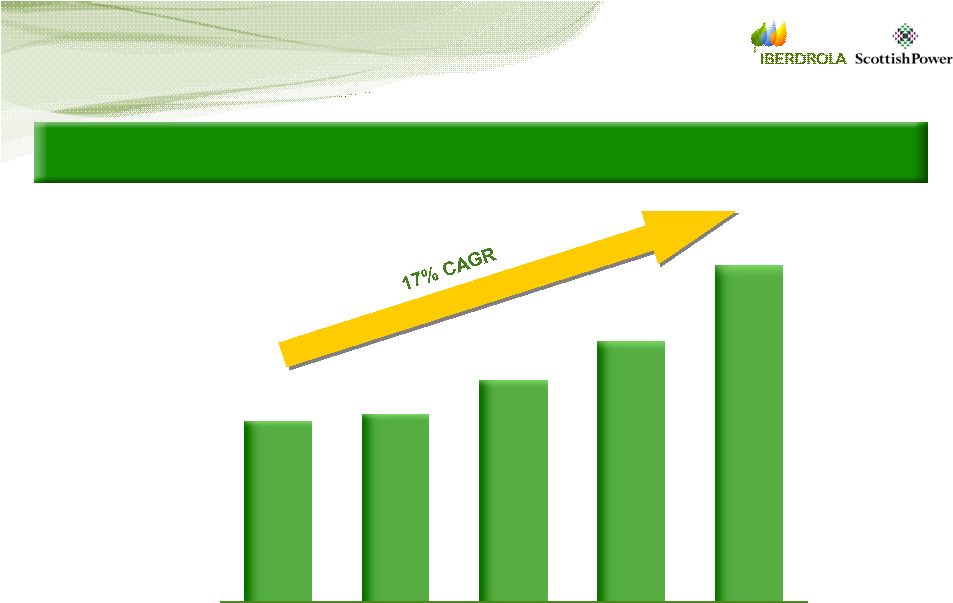

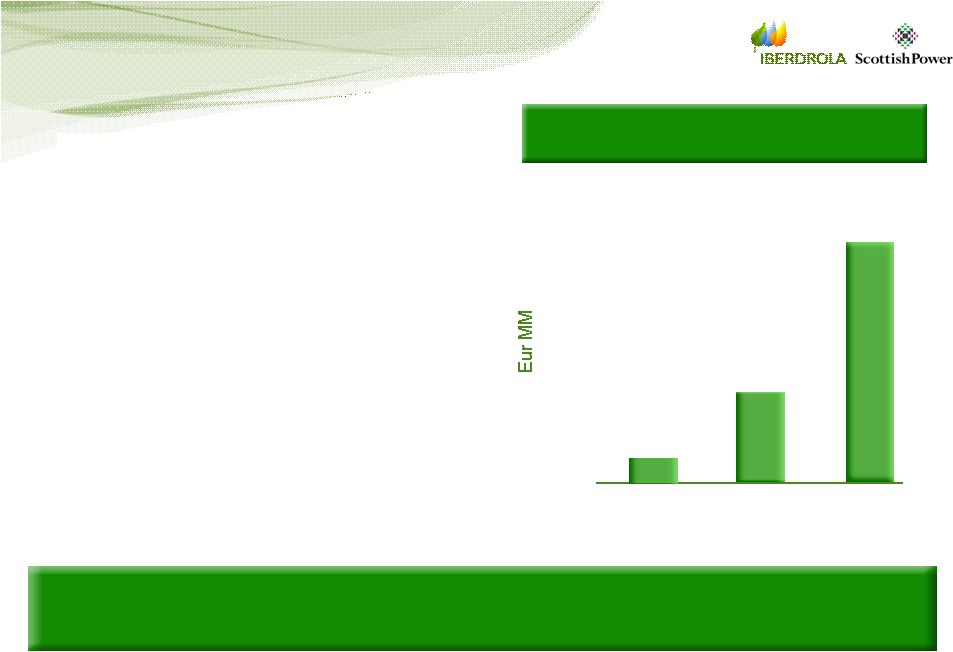

12 Net Profit +13.6% to Eur 458.2 MM … Net Profit 403.2 +13.6% +13.6% 458.2 Net Profit (Eur Net Profit (Eur MM) MM) Q1 2006 Q1 2007 … … in line with double digit growth in line with double digit growth expectations for 2007 expectations for 2007 |

13 Consolidating the international expansion through new wind energy transactions … Internationalization … … in US & Europe, in countries in US & Europe, in countries with high growth potential with high growth potential USA: acquisition of CPV • ~1,100 MW to become operational between 2008-2011 • Agreement with GE for the supply of turbines • USD 75 MM for 100% of equity Italy: 50% joint venture with API • 350 MW to become operational between 2008-2009 Greece: taking full control of Rokas • Increasing stake to 52.7% |

14 Agenda Highlights of the Period Highlights of the Period Analysis of Results Analysis of Results Conclusion Conclusion Consolidated Consolidated By Business By Business |

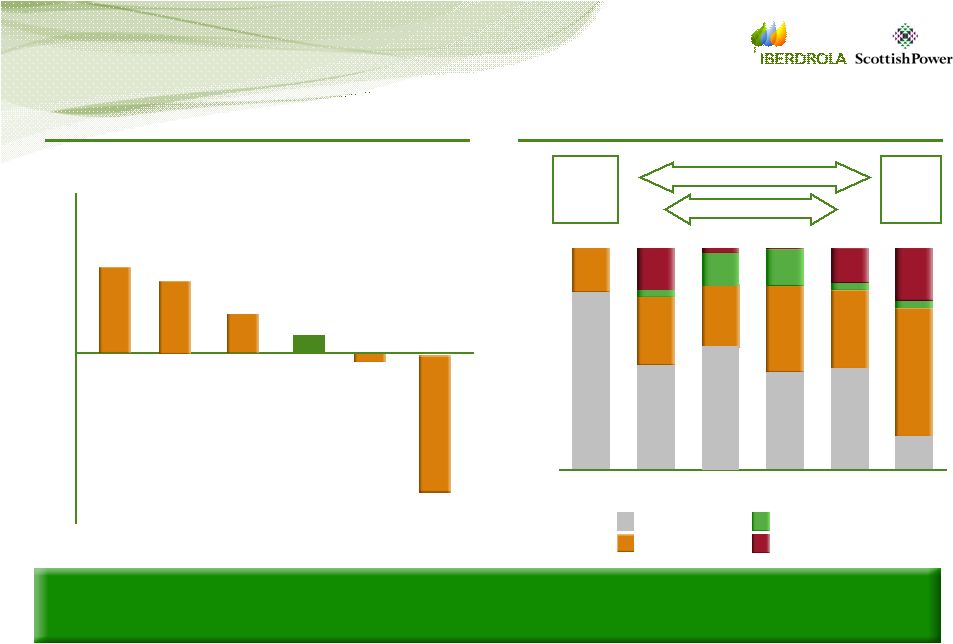

15 Gross Margin Change % Q1 2007 Net Op. Expenses Eur MM Q1 2006 Income Statement - Group EBITDA Operating Profit (EBIT) Net Profit Non-recurrent assets +Equity Income +2.9 1,087.1 1,056.6 +0.8 794.8 788.4 N/M 29.3 5.7 +13.6 458.2 403.2 +5.3 1,572.4 1,493.9 Financial Result +0.1 -163.5 -163.4 -439.3 +12.3 -391.2 Positive results in a difficult scenario Iberdrola Iberdrola estimates Eur estimates Eur 26.5 MM of tariff insufficiency 26.5 MM of tariff insufficiency |

16 Net Sales Net Sales fall by 8.8% to Eur 2,716.6 MM driven by Domestic Energy … … … due to lower prices in Generation & Wind due to lower prices in Generation & Wind Net Sales Net Sales Q1 2006 Q1 2007 -261.8 MM -261.8 MM 2,978.4 2,716.6 +36.2% +4.6% -20.2% 470.1 470.1 611.4 611.4 1,635.1 1,635.1 Eur MM Non-energy International International Domestic Domestic Energy Energy |

17 Procurement Costs Procurements decrease 17.5% to Eur 1,136.1 MM … Eur MM Procurements Procurements Q1 2006 Q1 2007 -241.0 MM -241.0 MM 1,377.1 1,136.1 Non-energy Non-energy -energy energy +47.8% International International -11.3% Domestic Domestic Energy Energy -36.3% 284.5 284.5 344.9 344.9 506.7 506.7 … … due to the different production mix in Generation due to the different production mix in Generation Spain & lower procurements in International Spain & lower procurements in International |

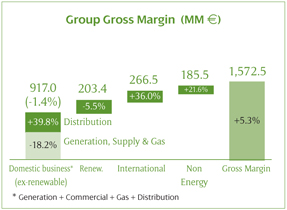

18 Gross Margin - Group Eur MM Domestic Energy * (ex-Wind) 917.0 (-1.4%) -18.2% -18.2% Non Energy Gross Margin 1,572.4 +5.3% +5.3% 185.5 266.5 Internat. 203.4 Wind Gross Margin +5.3% to Eur 1,572.4 MM, driven by Distribution, Supply & Gas, International and Non-energy +21.6% +21.6% -5.5% -5.5% +36.0% +36.0% Generation Spain & Wind affected by lower prices Generation Spain & Wind affected by lower prices * Generation + Supply + Gas + Distribution +39.8% +39.8% Generation, Supply & Gas Distribution |

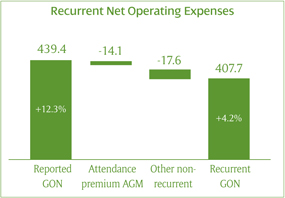

19 Recurrent Net Op. Expenses +4.2%, less than Gross Margin, vs. a 12.3% growth of Reported Net Op. Exp. … Net Operating Expenses - Group Net Op. Exp. by item Net Op. Exp. by item % vs. Q1 2006 Q1 ‘07 … … due to non-recurrent expenses & due to non-recurrent expenses & the 2007 AGM attendance premium the 2007 AGM attendance premium Reported Net Op. Exp. 439.3 +12.3% +12.3% Recurrent Net Op. Exp. 407.6 +4.2% +4.2% -17.6 Other non-recurrent -14.1 AGM attendance premium Recurrent Net Op. Exp. Recurrent Net Op. Exp. Eur MM Net Personnel Total 439.3 +12.3% 202.9 -4.0% Rec. N. Ext. Services 204.7 +13.8% Rep. Net Ext. Servs. 236.4 +31.5% Other non-recurrent 17.6 AGM attendance premium 14.1 |

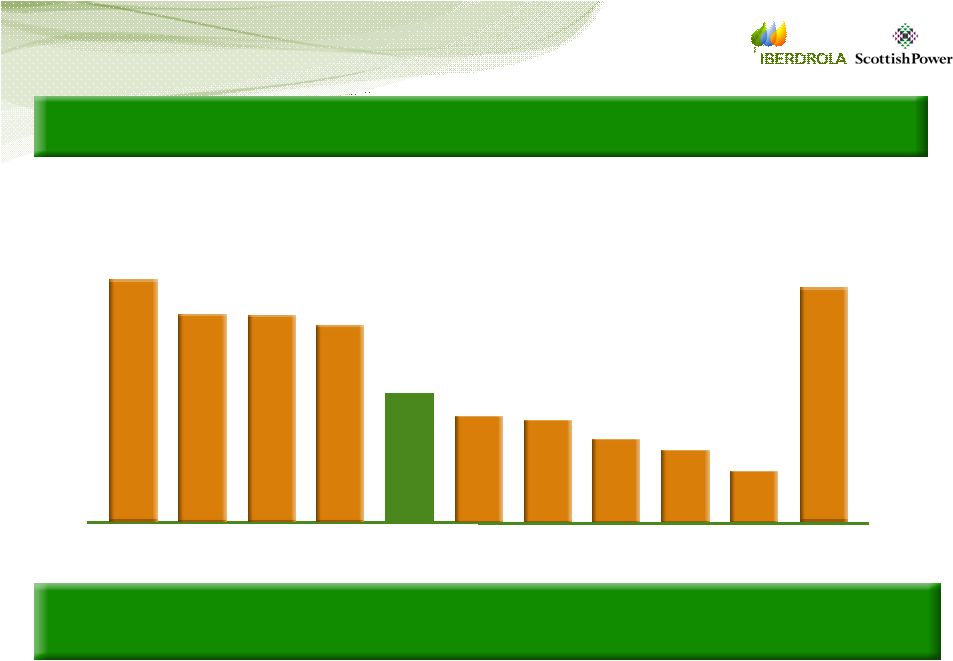

20 EBITDA - Group EBITDA +2.9% to Eur 1,087.1 MM Eur MM Domestic Energy * (ex-Wind) 604.1 (-6.2%) -25.5% -25.5% Non Energy EBITDA 1,087.1 +2.9% +2.9% 122.5 200.5 Internat. 160.0 Wind +40.0% +40.0% -12.4% -12.4% +41.0% +41.0% +95.0% +95.0% Generation, Supply & Gas Distribution * Generation + Supply + Gas + Distribution |

21 EBIT - Group Operating Profit (EBIT) up 0.8% to Eur 794.8 MM … D & A % vs. Q1 2006 Total Q1 2007 292.3 +9.0% 283.8 +13.8% Provisions 8.5 -54.5% EBIT EBIT Q1 2006 Q1 2007 +6.4 MM +6.4 MM 788.4 794.8 Eur MM … … driven by 13.8% rise in D&A driven by 13.8% rise in D&A due to new plants in operation due to new plants in operation |

22 Flat evolution of the Financial Result: +0.1% … Financial Result -163.4 -163.4 -163.5 -163.5 Q1 2006 Q1 2006 Q1 2007 Q1 2007 +0.1 MM +0.1 MM … … due to the control of the average cost of debt due to the control of the average cost of debt Financial Result (Eur Financial Result (Eur MM) MM) Average Cost of Debt Average Cost of Debt Q1 2006 Q1 2006 Q1 2007 Q1 2007 4.65% 4.65% 4.6% 4.6% |

23 Leverage falls to 54.1% vs. 54.7% in Q1 2006 Leverage Q1 2006 Q1 2007 Leverage Leverage 54.1% Ex-tariff insufficiency impact Net Debt & Equity (Eur Net Debt & Equity (Eur MM) MM) Q1 2006 Tariff insufficiency Tariff insufficiency Adjusted Net Debt Adjusted Net Debt ex-insufficiency ex-insufficiency Equity Equity 1,583 1,583 11,448 11,448 9,486 9,486 Q1 2007 606 606 12,454 12,454 10,564 10,564 Adjusted Net Debt Adjusted Net Debt 13,031 13,031 13,061 13,061 54.7% |

24 Profit Before Taxes up 4.7% to Eur 660.6 MM PBT, Net profit & FFO 403.2 458.2 Q1 2006 Q1 2007 Profit Before Taxes Profit Before Taxes Q1 2006 Q1 2007 630.7 +4.7% +4.7% 660.6 Eur MM Sustainable lower tax rate drives higher increase in Net Profit (+13.6%) FFO* up 8.3% to Eur 721.2 MM Net Profit Net Profit +13.6% +13.6% Eur MM Funds from Operations Funds from Operations Q1 2006 Q1 2007 665.7 +8.3% +8.3% 721.2 Eur MM * Net Profit + Depreciation & Amortization – Equity Income – Non Recurrent Results |

25 Agenda Highlights of the Period Highlights of the Period Analysis of Results Analysis of Results Conclusion Conclusion Consolidated Consolidated By Business By Business |

26 Gross Margin -23.1% as lower procurement costs partially compensate pool prices Financial highlights (Eur Financial highlights (Eur MM) MM) Operating highlights Operating highlights Results by Business Generation Business Gross Margin EBITDA -23.1% 524.0 -33.1% 349.0 Q1 2007 Net Op. Exp. +17.3% -139.0 % vs. Q1 2006 EBITDA affected by Eur EBITDA affected by Eur 17.6 MM of Non-recurrent Expenses 17.6 MM of Non-recurrent Expenses Similar production: -0.6% Energy prices -40.9% Lower CO 2 average cost: Eur 2.95/Tn Lower procurements cost: -43.1%* * Excluding CO2 cost ** Iberdrola’s estimates Lower capacity payments: Eur 27.8 MM** Compensated by Fuel Cost (Eur/MWh) Fuel Cost (Eur/MWh) Q1 ‘07 38.4 38.4 Avg. Fuel Cost * Q1 ‘06 38.5 38.5 % -0.1% -0.1% 0.1% |

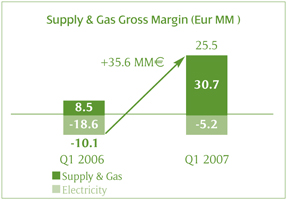

27 Supply + Gas Gross Margin rises 35.6 MM to Eur 25.5 MM driven by optimization of gas strategy Results by Business Supply & Gas Supply + Gas Supply + Gas Gross Margin (Eur Gross Margin (Eur MM) MM) Q1 ‘06 Elect. Supply Gas Q1 ‘07 8.5 8.5 30.7 30.7 -5.2 -5.2 -18.6 -18.6 -10.1 25.5 +35.6 MM +35.6 MM EBITDA Gross Margin Q1 2007 25.5 21.7 -10.1 -27.2 Q1 2006 Net Op. Exp. -12.4 -13.6 Taxes 8.6 -3.6 Financial highlights Financial highlights EBITDA improves Eur EBITDA improves Eur 48.9 MM vs. Q1 2006 48.9 MM vs. Q1 2006 Eur MM |

28 Results by Business – Wind + Mh Q1 2006 4,552 4,552 Q1 2007 + 638 MW + 638 MW Capacity (MW) Capacity (MW) Wind Spain Mini-hydro 3,751 459 Q1 2006 2,253 2,253 2,725 2,725 Q1 2007 +21.0% +21.0% Production (GWh) Production (GWh) Capacity: +16.3% to 4,552 MW Production: +21.0% to 2,725 GWh International Wind: 10.1% of installed capacity & production International Wind: 10.1% of installed capacity & production 342 Wind Intl. 3,914 3,914 3,330 268 316 Wind Spain Mini-hydro 2,304 274 147 Wind Intl. 1,942 151 160 |

29 5.5% decrease in Gross Margin due to lower prices (-21.8%) to 74.7 Eur/MWh Results by Business – Wind + Mh Financial highlights Financial highlights -5.5% 203.4 EBITDA -12.4% 160.0 Gross Margin Q1 2007 Eur MM Net Op. Exp. +34.3% -41.1 34.3% increase in Net Op. Expenses 34.3% increase in Net Op. Expenses due to international expansion due to international expansion EBITDA (EUR MM) EBITDA (EUR MM) % vs. Q1 2006 +405.2% -8.0 - International 148.0 12.0 Domestic International -14.5% +26.3% 160.0 -12.4% Total |

30 Results by Business - Distribution Gross Margin up 39.8% to Eur 371.2 MM Eur MM EBITDA Gross Margin Q1 2007 371.2 226.5 +39.8% +95.0% % vs. Q1 2006 Higher regulated revenues and Higher regulated revenues and lower Net Operating Expenses lower Net Operating Expenses Net Op. Exp. -114.0 -8.7% Operating Highlights Operating Highlights No impact from RDL 3/2006 Higher regulated revenues in 2007 tariff Financial Highlights Financial Highlights |

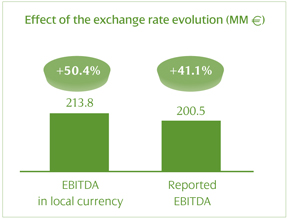

31 Results by Business – International …and 50.4% in local currency …and 50.4% in local currency International EBITDA grows 41.0% to Eur 200.5 MM … Financial Highlights Financial Highlights EBITDA Gross Margin Q1 2007 Eur MM Net Op. Exp. +36.0% 266.5 +23.0% -63.7 +41.0% 200.5 213.8 200.5 EBITDA in local currency Reported EBITDA +50.4% +41.1% Effect of currency evolution Effect of currency evolution % vs. Q1 2006 |

32 Results by Business - International Operating Highlights Operating Highlights International accounts for 18.4% of total EBITDA Brazil Mexico-Guatemala Contribution to financial statements 119.1 EBITDA (Eur MM) 81.4 EBITDA (Eur MM) As a % of Debt As a % of Equity As a % of Debt As a % of Equity +6.5% demand Higher tariffs +24.2% more production (Altamira V; 1,121 MW) High availability and efficiency Business Evolution 4.6% 9.8% 7.9% 8.1% -4.4% exchange rate -8.6% exchange rate |

33 EBITDA up 40.0% to Eur 122.5 MM, driven by strong growth in Real Estate Results by Business Non energy + Engineering Financial Highlights (Eur Financial Highlights (Eur MM) MM) +21.6% 185.5 Q1 2007 EBITDA Gross Margin Net Op. Exp. -4.0% -61.0 +40.0% 122.5 % vs. Q1 2006 Over Eur Over Eur 6.0 Bn* estimated market value of stakes in listed & 6.0 Bn* estimated market value of stakes in listed & non-energy companies and of Real Estate; Eur non-energy companies and of Real Estate; Eur 3.5 Bn 3.5 Bn of capital gains** of capital gains** Breakdown of Gross Margin Breakdown of Gross Margin Engineering & Construction Iberdrola Inmobiliaria IBV Other Services * Does not include Engineering & Construction ** Pre-tax 37% 10% 25% 28% |

34 Iberdrola Inmobiliaria Gross Margin triples to Eur 68.2 MM Financial Highlights Financial Highlights +199.9% 68.2 +301.7% 61.1 Q1 2007 EBITDA Gross Margin Eur MM +506.6% 35.9 Net Profit Property Portfolio Property Portfolio (buildable (buildable sq. mt.) sq. mt.) Dec-2006 Q1-2007 +4.4% +4.4% 3.57 MM 3.57 MM 3.42 MM 3.42 MM Commercial Commercial Residential Residential Rentals Rentals 28% 28% 28% 60% 60% 60% 12% 12% 12% 20% 20% 20% 68% 68% 68% 12% 12% 12% % vs. Q1 ‘06 Q1 2006 affected by seasonality Q1 2006 affected by seasonality |

35 Engineering & Construction Sales to third parties up 57.4% to Eur 177.5 MM Increasing backlog to Eur Increasing backlog to Eur 2.6 Bn 2.6 Bn Q1 2006 112.8 112.8 177.5 177.5 Q1 2007 +57.4% +57.4% Sales to third parties (Eur Sales to third parties (Eur MM) MM) Backlog (Eur Backlog (Eur Bn) Bn) 1.0 2.6 Q1 2006 Q1 2007 +2.6x +2.6x |

36 Agenda Highlights of the Period Highlights of the Period Analysis of Results Analysis of Results Conclusion Conclusion Consolidated Consolidated By Business By Business |

37 Conclusion Positive results in a difficult scenario… Different trend in prices expected for 2007 vs. 2006 Impact of RDL 3/2006 in 2006 Tariff improvements in Distribution Personnel non-recurrent expenses Q4 ‘06 Higher hydro production & reserves Double-digit growth in 2007 Flexibility of gas contracts … … that will lead for an improvement throughout 2007 that will lead for an improvement throughout 2007 |

38 First Quarter 2007 First Quarter 2007 Results Results |

Exhibit 99.4

LEGAL NOTICE:

DISCLAIMER

This document has been prepared by Iberdrola, S.A. (the “Company”) solely for use during the presentation corresponding to the First Quarter 2007 Results.

The information and any forward looking statements contained in this document have not been independently verified and no representation or warranty express of implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein.

None of the Company, or any of its advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document.

This document does not constitute an offer or invitation to purchase or subscribe for any securities in accordance with the Spanish Securities Market Law (Law 24/1988, as amended), Royal Decree-Law 5/2005 and/or Royal Decree 1310/2005 and the rules and regulations made there under.

Furthermore, this document does not constitute an offer to purchase, sell or exchange or the solicitation of an offer to purchase, sell or exchange any securities or the solicitation of any vote or approval in any other jurisdiction.

Neither this document nor any part of it shall form the basis of or be relied in connection with any contract or commitment whatsoever.

IMPORTANT INFORMATION

This communication does not constitute an offer to purchase, sell or exchange or the solicitation of an offer to purchase, sell or exchange any securities. The shares of Iberdrola, S.A. may not be offered or sold in the United States except pursuant to an effective registration statement under the Securities Act or pursuant to a valid exemption from registration.

FORWARD-LOOKING STATEMENTS

This communication and other documents relating to the Offer contain forward-looking information and statements about ScottishPower and Iberdrola, S.A. and their combined businesses after completion of the proposed Offer and otherwise. Forward-looking statements are statements that are not historical facts. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, capital expenditures, synergies, products and services, and statements regarding future performance. Forward-looking statements are generally identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates” and similar expressions. Although the managements of ScottishPower and Iberdrola, S.A. believe that the expectations reflected in such forward-looking statements are reasonable, investors and holders of ScottishPower and Iberdrola, S.A. shares are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and generally beyond the control of ScottishPower and Iberdrola, S.A., that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the public documents sent by ScottishPower and Iberdrola, S.A. to the Comisión Nacional del Mercado de Valores and under “Risk Factors” in the annual report on Form 20-F for the year ended March 31, 2006 filed by ScottishPower with the SEC on June 30, 2006.

Forward-looking statements are not guarantees of future performance. They have not been reviewed by the auditors of Iberdrola, S.A. or of ScottishPower. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date they were made. All subsequent oral or written forward-looking statements attributable to Iberdrola, S.A. or ScottishPower or any of their respective members, directors, officers, employees or any persons acting on their behalf are expressly qualified in their entirety by the cautionary statement above. All forward-looking statements included in documents relating to the Offer are based on information available to Iberdrola, S.A. on the date thereof. Except as required by applicable law, Iberdrola, S.A. does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

| II | First Quarter 2007 financial results |

IBERDROLA-SCOTTISH POWER: A WORLDWIDE LEADER EMERGES

Net profit up 13.6% to 458 million euros

More production (+6.9%) with a generation mix of lower variable costs and emissions (-24.2%)

| • | Flexibility of generation capacity: Production grew 2.5% in Spain (sector: -0.5%). |

| • | Production without emissions: Clean power generation in Spain grew by 25%. |

• | CO2 emissions: Down 37.1% in Spain, which is 2.8 times lower than the rest of the sector. |

| • | Market environment: Energy prices fell by 41% to 46.4 Eur/Mwh, price of emissions rights set at 2.95 Eur/ton and demand increases by 1.8%. |

In an challenging environment of low energy prices and moderate increase of demand, Gross Operating Profit (EBITDA) rose 2.9% to 1,087.1 MM€

Growing in the international business

| • | USA: Acquisition of CPV Wind Ventures LLC for 55 million euros, with pipeline of 3,500 MW |

| • | Italy: Strategic alliance with italian energy group API Holding for the construction and operation of 350 MW of wind. |

| • | Greece: Increasing the stake at the Rokas Group to 52.7%, taking full control of the Company. |

Iberdrola - ScottishPower Integration

| • | On 29 and 30 March of this year, a broad majority of the shareholders in both companies approved the merger (99.4% at Iberdrola and 97.6% at ScottishPower). |

| • | The operation is effective from 23 April, after its approval by the Sessions Court in Edinburgh. |

| • | This has been carried out under the framework of what is known as Scheme of Arrangement in British law, pursuant to Section 425 of the Companies Act in Great Britain. |

| First Quarter 2007 financial results | 1 |

Basic figures for the businesses

Operating Data | Q1 2007 | Q1 2006 | % | |||||

Net production | GWh | 24,752 | 23,154 | 6.9 | ||||

Gas combined cycle | GWh | 8,880 | 9,093 | -2.3 | ||||

Wind and Mini-Hydroelectric | GWh | 2,725 | 2,253 | 21.0 | ||||

Hydroelectric | GWh | 4,861 | 2,386 | 103.7 | ||||

Nuclear | GWh | 6,509 | 6,662 | -2.3 | ||||

Fuel oil | GWh | 15 | 566 | -97.3 | ||||

Coal | GWh | 1,212 | 1,697 | -28.6 | ||||

Cogeneration | GWh | 550 | 497 | 10.7 | ||||

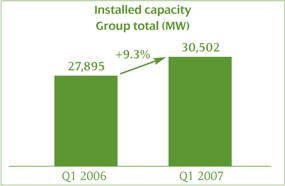

Installed capacity | MW | 30,502 | 27,895 | 9.3 | ||||

Gas combined Cycle | MW | 8,818 | 6,897 | 27.9 | ||||

Wind and Mini-hydroelectric | MW | 4,552 | 3,914 | 16.3 | ||||

Hydroelectric | MW | 9,149 | 9,118 | 0.3 | ||||

Nuclear | MW | 3,344 | 3,344 | — | ||||

Fuel oil | MW | 2,889 | 2,889 | — | ||||

Coal | MW | 1,253 | 1,253 | — | ||||

Cogeneration | MW | 497 | 480 | 3.5 | ||||

Energy Distributed | GWh | 34,010 | 33,054 | 2.9 | ||||

Consumers (supply points under management) | No (mil.) | 18.5 | 17.9 | 3.3 | ||||

Employees | No | 16,347 | 17,514 | -6.6 |

| 2 | First Quarter 2007 financial results |

Operating Data | Q1 2007 | Q1 2006 | % | |||||

Spain | ||||||||

Net Production | GWh | 18,208 | 17,767 | 2.5 | ||||

Gas Combined Cycle | GWh | 2,719 | 4,058 | -33.0 | ||||

Wind and Mini-Hydroelectric (1) | GWh | 2,725 | 2,253 | 21.0 | ||||

Hydroelectric | GWh | 4,598 | 2,156 | 113.3 | ||||

Nuclear | GWh | 6,509 | 6,662 | -2.3 | ||||

Fuel oil | GWh | 15 | 566 | -97.3 | ||||

Coal | GWh | 1,212 | 1,697 | -28.6 | ||||

Cogeneration | GWh | 430 | 375 | 14.7 | ||||

Installed capacity | MW | 26,084 | 24,606 | 6.0 | ||||

Gas combined cycle | MW | 4,800 | 4,000 | 20.0 | ||||

Wind and Mini-Hydroelectric (1) | MW | 4,552 | 3,914 | 16.3 | ||||

Hydroelectric | MW | 8,842 | 8,819 | 0.3 | ||||

Nuclear | MW | 3,344 | 3,344 | — | ||||

Fuel oil | MW | 2,889 | 2,889 | — | ||||

Coal | MW | 1,253 | 1,253 | — | ||||

Cogeneration | MW | 404 | 387 | 4.4 | ||||

Energy Distributed | GWh | 26,756 | 26,224 | 2.0 | ||||

Regulated market | GWh | 22,125 | 19,790 | 11.8 | ||||

Commercial | GWh | 4,631 | 6,434 | -28.0 | ||||

Gas Supplies | GWh | 9,904 | 15,466 | -36.0 | ||||

Customers | GWh | 4,124 | 6,008 | -31.3 | ||||

Gas combined cycle | GWh | 5,780 | 9,458 | -38.9 | ||||

Customers (supply points under management) | No (mil.) | 10.0 | 9.7 | 3.0 | ||||

Latin America | ||||||||

Production | GWh | 6,544 | 5,387 | 21.5 | ||||

Gas combined cycle | GWh | 6,161 | 5,035 | 22.4 | ||||

Hydroelectric | GWh | 263 | 230 | 14.3 | ||||

Cogeneration | GWh | 120 | 122 | -1.6 | ||||

Installed capacity | MW | 4,418 | 3,289 | 34.3 | ||||

Gas combined cycle | MW | 4,018 | 2,897 | 38.7 | ||||

Hydroelectric | MW | 307 | 299 | 2.7 | ||||

Cogeneration | MW | 93 | 93 | — | ||||

Energy distributed (under management) | GWh | 7,254 | 6,830 | 6.2 | ||||

Customers (supply points under management) | No (mil.) | 8.5 | 8.2 | 3.6 |

Note: Installed capacity, production, and number of employees according to consolidation criterion.

| (1) | Includes for 2007 460 MW of international capacity with production of 274 GWh. For 2006: 316 MWwith production of 151 GWh. |

| First Quarter 2007 financial results | 3 |

Market Data | Q1 2007 | Q1 2006 | ||||

Market capitalisation (3/31) | Million € | 31,906 | 24,017 | |||

Earnings per share (quarter) | € | 0.51 | 0.45 | |||

Net operating cash flow per share (quarter) | € | 0.80 | 0.74 | |||

PER | Times | 19.2 | 16.7 | |||

Price/Book Value (Capitalisation to NBV at end of period) | Times | 3.02 | 2.53 | |||

Economic/Financial Data | ||||||

Income Statement | Q1 2007 | Q1 2006 | ||||

Net Sales | Million € | 2,716.6 | 2,978.4 | |||

EBITDA | Million € | 1,087.1 | 1,056.6 | |||

EBIT | Million € | 794.8 | 788.4 | |||

Net Profit | Million € | 458.2 | 403.2 | |||

Net Operating expenses / gross Margin | % | 27.9 | 26.2 | |||

Balance sheet | Q1 2007 | Q1 2006 | ||||

Total assets | Million € | 34,002 | 33,061 | |||

Shareholders’ Equity | Million € | 10,564 | 10,567 | |||

Net adjusted financial debt (1) | Million € | 13,061 | 13,119 | |||

ROE | % | 16.2 | 16.6 | |||

Financial leverage (2) | % | 55.3 | 55.4 | |||

Debt/equity ratio | Times | 1.24 | 1.24 |

| (1) | Includes the amounts corresponding to the tariff insufficiency: 606 million euros from March of 2007 and 572 million euros from December 2006. |

| (2) | Net Debt/Net Debt+FL. Includes financing the tariff insufficiency. If the tariff insufficiency was not included, leverage as at March 2007 would be 54.1 % and 54.3% as at December 2006. |

| 4 | First Quarter 2007 financial results |

Operating highlights

• | In the first quarter of 2007, IBERDROLA reached a new Group production record, with production rising by 6.9% to 24,752 GWh. This was achieved with a mix of low cost and cleaner generation, which allowed CO2 emissions to fall by 24.2%. |

In Spain, IBERDROLA saw growth in production of 2.5%, while overall system production in Spain fell by 0.5%. Emissions in Spain were down 37.1%, to 133 gr/kWh, a third of the rest of the sector (378 gr/kWh). Other highlights include:

| • | 103.7% increase in hydroelectric production to 5,598 GWh and a 23.2% increase in wind production to 2,578 GWh (274 GWh international). |

| • | Market environment during the first quarter of 2007 was marked by low energy prices (-41%) and very mild winter temperatures which led to a moderate increase in domestic demand (+1.8%). |

| • | In this challenging scenario of low prices and moderate increase of demand, Operating Profit improved in both gross terms (EBITDA +2.9%) and net terms (EBIT +0.8%). |

| • | Domestic Energy Business EBITDA falls by -7.6%. Distribution business growth by 95%, what offsets the falls in Generation (-33.1%) and Renewables (-12.4%), reflecting the downward trend of pool prices. In the case of Generation, lower prices have been compensated with a fall in Procurements due to a cleaner generation mix (76% of non-pollutant technologies), and lower regulatory impacts. |

| • | International and Engineering and Non Energy business achive strong growths at EBITDA level, offsetting the falls in Generation and Renewables: |

| • | International: EBITDA up 41.1% to 200.5 million euros, thanks primarily to the good development of business in Mexico and Brazil. The generation business saw an increase in production of 21.5%. The distribution business recorded an increase of 6.2% in energy distributed. In addition, it should be mentioned that the change in the exchange rate between the Brazilian Real and the Dollar in the period resulted in an effect of about-13.3 million euros. |

| • | Engineering and Non-Energy Businesses increased their EBITDA by 40.0% to 122.5 million euros, basically boosted by the results of Iberdrola Inmobiliaria. |

| • | Net Profit totalled 458.2 million euros, an increase of 13.6%, in line with the expectations of double digit growth contemplated for the full 2007 fiscal year. |

| First Quarter 2007 financial results | 5 |

Profit before taxes is up by 4.7%, slightly improving the trend followed at the operating level. The effective tax rate in 2007 has been normalized in the 29.3%, according to current tax rules, compare to 35.1% for the same period of 2006.

| • | On 29 and 30 March of this year, a broad majority of the shareholders in both companies approved the merger (99.4% at Iberdrola and 97.6% at ScottishPower). The operation is effective from 23 April, after approval by the Sessions Court in Edinburgh, and has been carried out under the framework of what is known as Scheme of Arrangement in British law, pursuant to Section 425 of the Companies Act in Great Britain. |

| 6 | First Quarter 2007 financial results |

Development of the Strategic Plan

1. GENERATION

Total installed capacity

Over the first quarter of 2007, IBERDROLA brought into service 118 MW of additional power compare to December 2006, taking total installed capacity up to 30,502 MW. All of the additional installed capacity is derived from newly installed renewable capacity, both in Spain (98 MW) and abroad (20 MW). Year on year, the additional capacity represents an increase of 9.3%.

1.1 Traditional Generation

1.1.1. Combined Cycle Plants

Spain

Installed capacity

IBERDROLA’s Combined Cycle Plant (CCGTs) total capacity in Spain was 4,800 MW at the end of March 2007 (5,600 MW under management), corresponding to nine plants. It is planned to bring the Castellón 4 Plant, with an additional 800 MW, on line during 2007.

Project | Capacity (MW managed) | Start of operations | |||

Castellón | 800 | Operative 2002 | |||

Castejón | 400 | Operative 2003 | |||

BBE | 800 | Operative 2003 | |||

Tarragona | 400 | Operative 2003 | |||

Santurce | 400 | Operative 2004 | |||

Arcos Grupos I y II | 800 | Operative 2004 | |||

Aceca | 400 | Operative 2005 | |||

Arcos Grupo III | 800 | Operative 2005 | |||

Escombreras | 800 | Operative 2006 | |||

Total 2006 | 5,600 | ||||

Castellón 4 | 800 | Planned 2007 | |||

TOTAL 2002-2007 | 6,400 | (5,600 owned) | |||

Mexico

IBERDROLA is the leading private electricity producer in Mexico. The Company now has 3,815 MW of installed capacity in operation in Mexico.

Proyect | Capacity (MW) | Operational Status | ||

Enertek | 120 | 100% operative | ||

Monterrey III | 1,037 | 100% operative | ||

Altamira III y IV | 1,036 | 100% operative | ||

La Laguna II | 500 | 100% operative | ||

Altamira V | 1,121 | 100% operative | ||

Tamazunchale | 1,135 | Operative 2007 | ||

Total | 4,949 | |||

In February 2007, IBERDROLA started the testing period for the Tamazunchale electrical plant

| First Quarter 2007 financial results | 7 |

located in the Mexican state of San Luís Potosí. With installed capacity of 1,135 MW, it is the largest combined cycle plant in operation in the country.

Portugal

On 10 April of this year, IBERDROLA and the municipality of Figueira da Foz signed a contract for the acquisition of land on which, after having received the approval of the Direcção Geral de Energia in Portugal, the first combined-cycle plant to be built by the Company in Portugal will be located. The land for the new IBERDROLA gas plant, which will be built in Lavos (Figueira da Foz), between Lisbon and Porto, has a total area of about 208,000 square metres. This new electrical generation plant, which will have an installed capacity of 850 MW, could come on line at the end of 2009 if all necessary requirements are met.

1.1.2 Hydroelectric energy Spain

The Ministry of the Environment has authorised two hydroelectric plants, a new group in the plant at La Muela, in Valencia which will double its current capacity of 630 MW, and the expansion of the San Esteban plant in the Sil basin by 175 MW. The La Muela 2 pumping plant project is now underway, with the excavation of the access tunnel.

1.1.3 Cogeneration

Spain

Operating capacity

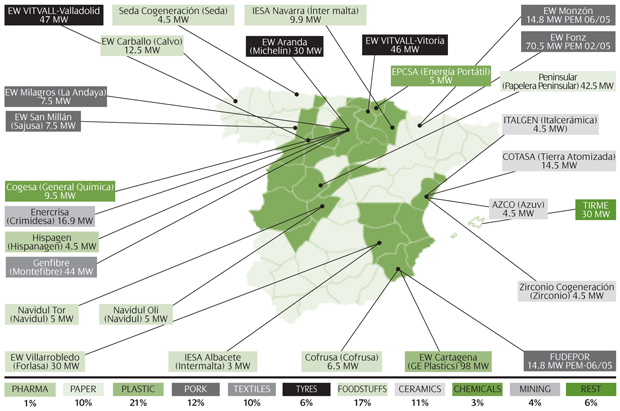

IBERDROLA has cogeneration operating installed capacity in Spain of an attributable 404 MW, equivalent to a total of 549 MW installed.

With the projects completed in 2006, IBERDROLA has consolidated its position as the largest cogeneration company in Spain, with a total of 549 MW installed. The Company also participates in more 29 cogeneration plants, supplying electricity and steam to clients such as Michelin, General Electric Plastics in Cartagena, Calvo Conservas in La Coruña, Holmen Paper in Madrid and Montefibre in Miranda de Ebro.

| 8 | First Quarter 2007 financial results |

Location of all IBERDROLA cogeneration plants

Capacity under construction

In April 2007, IBERDROLA presented a construction project for the Barcial del Barco (Zamora) bioethanol production plant. This plant, which will have the capacity to produce 149,000 cubic metres of bioethanol annually, will come on line in July 2008. The Project will be developed by the company Ecobarcial, in which Proencalsa has a 51% participation (property of our Company, Collosa and the Ente Regional de la Energía) and by Green Source (Sniace) (30%), Ecoteo (14%), ITACYL (4.9%) and various cooperatives (0.1%).

1.1.5 Wind and Mini-Hydroelectric Energy

At the close of the first quarter of 2007, IBERDROLA had an installed capacity of 4,552 MW (4,210 MW for wind farms and 342 MW for Mini-hydroelectric facilities), confirming IBERDROLA’s position as the world leader in this business. During the first quarter of the financial year, 118 MW of additional power were installed as compared with the capacity available at the close of 2006 (109 wind and 9 small-scale hydroelectric). Of the total power added, 98 MW corresponds to Spain and 20 MW is international.

| First Quarter 2007 financial results | 9 |

Year on year, the installed capacity at the close of the first quarter of 2007 is 16.3% greater than that at the close of the same period of 2006.

IBERDROLA has a portfolio of projects of almost 19,000 MW, the result of the development of our own projects and operations undertaken in the context of renewable energy outside of Spain.

Spain

The new capacity installed in Spain during the first quarter of 2007 totalled 98 MW, which breaks down as follows: Castilla y León 61 MW, Andalusia 15 MW, Region of Murcia 10 MW, Castilla - La Mancha 9 MW and La Rioja 3 MW.

United States

The United States have become one of the most important markets for developing IBERDROLA’s objectives in the area of renewable energy. The Company has 26 MW in operation, which consists of the wind farm at Locust Ridge coming from the acquisition of Community Energy, and a portfolio of projects that will be close to 8,500 MW in the first half of 2007, once they are included the MW coming from recent acquisitions. IBERDROLA already has a permanent office in the State of Pennsylvania.

To strengthen its portfolio of projects in the country, IBERDROLA has undertaken various operations. The highlights are as follows:

| • | Acquisition of the US wind company CPV Wind Ventures.IBERDROLA has reached an agreement to acquire, for 55 million euros, 100% of the US company CPV Wind Ventures LLC, headquartered in Silver Spring (Maryland), as part of the Company’s focus on international expansion and its interest in increasing its presence in the wind market in the United States. CPV Wind Ventures LLC has a portfolio of projects of 3,500 MW of wind power in 15 states in the US, with the construction of the first wind farms planned for next year. With this in mind, this company has already signed an agreement with General Electric to supply turbines beginning in 2008. |

| • | Agreement with Gamesa to purchase wind farms in the US.This agreement provides for the acquisition of wind installations with about 500 MW of power that Gamesa will bring on line before the end of 2009. Of these, 300 MW are firm commitments, while the remaining 200 MW will be subject to a right of purchase. The other 500 MW would correspond to the acquisition of developments under way. |

| • | Acquisition in the US of Community Energy (CEI),which has a portfolio of projects of 2,000 MW of wind power in various coastal zones of |

| 10 | First Quarter 2007 financial results |

the country in the initial study phase, an additional 200 MW are in an advanced stage of development. CEI has sales of more than 3,000 GWh of wind power, 100,000 residential customers and commercial agreements with about 20 municipal and private electricity companies. The US company has had two wind farms in operation since the end of 2005: Jersey-Atlantic (7.5 MW) and Bear Creek (24 MW). |

| • | Acquisition in the US of MREC Partners and its participation Midwest Renewable Energy Projects.The portfolio of projects of the two companies totals 1,600 MW of wind power located in various zones of the Midwest of the US. Of this total, 400 MW are in an advanced phase of development and 1,200 MW are in the initial study phase with a high probability of approval. |

Greece

The Alogorachis wind farm has been brought on line through its acquisition to Gamesa, and the Modi Ampliación wind farm through Rokas has been concluded, adding a total of 18 new MW. This gives IBERDROLA 210 MW in operation in the country. IBERDROLA is a strategic partner of the principal promoter and producer of wind energy in Greece, Rokas, in which it has a 52.7% interest.

Agreement with the Rokas family

During the first quarter of 2007, IBERDROLA, through its renewable energies subsidiary, has reached a new agreement with the Rokas family to promote the development of the Rokas Group, and gives another indication of the clear commitment the Company has to this market. Under the terms of the agreement:

| • | The Rokas family will transfer to IBERDROLA all of the preferred non-voting shares it holds, directly or indirectly, in the Rokas Group (about 45% of the existing shares) for about 32 million euros. |

| • | The agreement reached in December 2004 is replaced by this, subject to the approval by Greek competition authorities. After the acquisition in the market of an additional 2.8% of the capital share, for 12.5 million euros, IBERDROLA increases its participation in Rokas up to 52.7% |

In addition, the Rokas family, after reaching an agreement with various financial entities for sale of the majority of its common shares in the Rokas Group (9.82% of the capital), has proceeded to the sale of those shares. IBERDROLA has consented to this transaction, renouncing to its preferred acquisition right.

| First Quarter 2007 financial results | 11 |

The Rokas Group closed 2006 with installed wind capacity of 193.3 MW and production of 520 GWh. It currently has three wind farms under construction totalling about 60 MW, and is seeking authorisation to develop another 488 MW in Greece and 179 MW in Cyprus.

Portugal

The installation of the Alto Monçao wind farm has been completed, with an additional 18 MW included in the acquisition agreement with Gamesa in Portugal, which contemplates the construction of 32 MW. IBERDROLA also has another 18 MW in operation, corresponding to the wind farm at Catefica. In addition, IBERDROLA has 122 MW in advanced projects that will enter into operation in the next two years.

France

Fitou wind farm has been completed, with 1 additional MW. IBERDROLA’s installed wind capacity at the close of the first quarter of 2007 is 49 MW. More than 100 MW of power are planned for installation in 2007, as a result of the development of the most advanced projects of Perfect Wind and Gamesa. To reinforce its pipeline in the country, IBERDROLA acquired french company Perfect Wind, considered as one of the companies with larger development potential in our neighbour country, with a pipeline of 600 MW, 17 MW currently in operation and 78 MW corresponding to projects in an advanced stage of development.

Poland

The Kisielice wind farm (41 MW) is already in operation. This is IBERDROLA’s first installed capacity in Poland. This farm (27 1.5 MW General Electric 1.5 SL turbines) is the first Project in the portfolio acquired from Eternegy Polska in September of 2005 to be built and brought on line. When the Malbork farm (18 MW) is brought on line next, IBERDROLA will be one of the main wind generators in Poland. In addition, another 141 MW, now at an advanced stage of development, will be put into service between 2007 and 2008.

Germany

34 MW have been brought on line, as provided for in the agreement reached with Gamesa at the end of 2005. When put into service, Iberenova will be part of the German wind market, which is the most developed in the world, with more than 20,000 MW installed. The portfolio of projects totalls 47 MW.

United Kingdom

IBERDROLA is developing its own projects, with potential to reach 200 MW. In addition, the acquisition of two projects, Darracott y Clachan Flats (both in the final stage of development, totalling 21 MW) will permit IBERDROLA to have its first MWs in operation on the British market during 2007.

| 12 | First Quarter 2007 financial results |

Italy

During the period 2007 - 2009 IBERDROLA will acquire from Gamesa a total of 100 MW by means of an agreement signed for that purpose in the month of October of 2005.

Strategic alliance with the API Holding Group

During the first quarter of 2007, IBERDROLA signed a strategic alliance with the Italian energy group API Holding for the construction and development of approximately 350 MW of wind power in Italy. The projected investment is about 500 million euros. Once that alliance is realised, the Company will be a 50% stakeholder in the joint company that will be created with API Nova Energia, subsidiary of API Holding, called Società Energie Rinnovabili. The objective will be to develop seven wind projects located in the regions of Sicily and Puglia. These projects are currently at a very advanced stage of development. It is expected that the projects will be brought into service in 2008 and 2009.

Brazil

The Rio do Fogo wind farm has been completed and brought on line, an additional 43 MW to make a total of 49 MW. In Brazil, Neoenergia has the Afluente small-scale hydroelectric plant with 18 MW (8 MW attributable to IBERDROLA). Neoenergía (in which IBERDROLA has a 39% stake) has the concessions to build, maintain and operate the Baguari hydroelectric plant and the Nova Aurora and Goiandira small-scale hydroelectric plants, for a total of 188 MW.

Mexico

IBERDROLA is developing promotions in the State of Oaxaca that add up to 150 MW of capacity. In 2007, La Ventosa wind farm, 30 MW, will be brought on line.

Total project portfolio

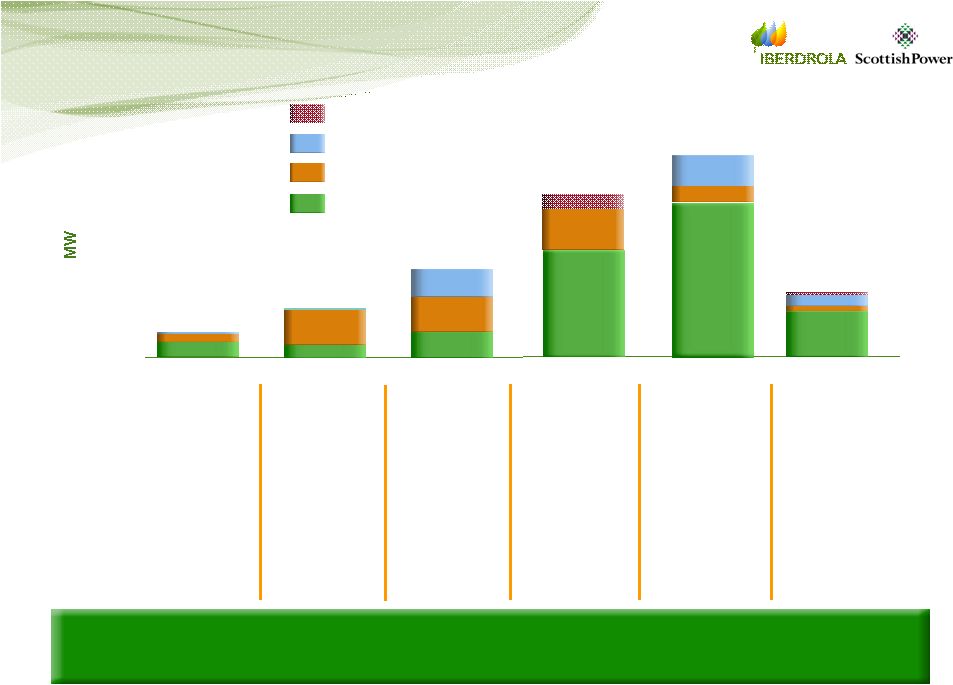

In total, IBERDROLA already has a portfolio of projects of about 19,000 MW in different stages of development, both in Spain and abroad. This pipeline is not including the MWs coming from recent acquisitions in the US, that will be included at closing of the first half of 2007.

MW | Under development | Validated resource | Connection rights & under construction | |||

Spain | 6,166 | 5,453 | 2,519 | |||

Wind | 5,279 | 4,973 | 2,066 | |||

Mini-hydroelectric | 176 | 176 | 76 | |||

Solar | 686 | 286 | 359 | |||

Biomass | 24 | 17 | 17 | |||

Wave energy | 1 | 1 | 0 | |||

International wind | 12,829 | 5,912 | 1,452 | |||

Total | 18,996 | 11,365 | 3,971 |

1.1.6 Other Sources of Renewable Energy (Non-Wind)

Thermo-solar energy

There are currently various solar thermo-electric energy projects using parabolic cylinder collector technology in development. Total power is 50 MW. Meteorological stations for measuring

| First Quarter 2007 financial results | 13 |

solar resources for the projects have been installed in Sevilla, Ciudad Real, Badajoz and Albacete. The portfolio of three projects totals 650 MW of power. They are being developed in Extremadura, Castilla y León, Andalucía, Castilla - La Mancha, Murcia, Madrid and Aragón. During the first quarter of 2007, work has begun on the first 50 MW plant in Puertollano.

Photovoltaic energy