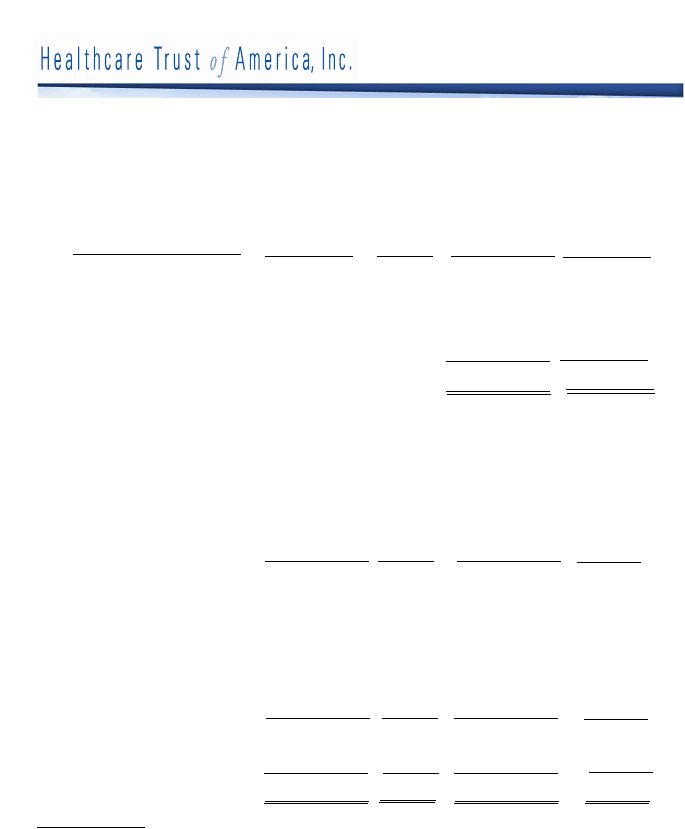

Acquisition-Related Expenses: Prior to 2009, acquisition-related expenses were capitalized and have historically been added back to FFO over time through depreciation; however, beginning in 2009, acquisition-related expenses related to business combinations are expensed. We believe by excluding expensed acquisition-related expenses, Normalized FFO provides useful supplemental information that is comparable for our real estate investments. Adjusted Earnings Before Interest Taxes, Depreciation and Amortization (Adjusted EBITDA): Is presented on an assumed annualized basis. We define Adjusted EBITDA for HTA as net (loss) income attributable to controlling interest computed in accordance with GAAP plus interest, depreciation, amortization, stock based compensation, change in fair value of derivatives, acquisition expenses, debt extinguishment costs, and listing expenses. We consider Adjusted EBITDA an important measure because it provides additional information to allow management, investors, and our current and potential creditors to evaluate and compare our core operating results and our ability to service debt. The following is a reconciliation of our net income (loss) attributable to controlling interest, the most directly comparable GAAP financial measure, to Adjusted EBITDA. Annualized Base Rent: Annualized base rent is calculated by multiplying contractual base rent for June 2012 by 12 (but excluding the impact of renewals, future step-ups in rent, abatements, concessions, and straight-line rent). Credit Ratings: Credit ratings of our tenants or their parent companies. Funds from Operations (FFO): We define FFO, a non-GAAP measure, as net income or loss computed in accordance with GAAP, excluding gains or losses from sales of property and impairment write downs of depreciable assets, plus depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. We present FFO because we consider it an important supplemental measure of our operating performance and believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of REITs, many of which present FFO when reporting their results. FFO is intended to exclude GAAP historical cost depreciation and amortization of real estate and related assets, which assumes that the value of real estate diminishes ratably over time. Historically, however, real estate values have risen or fallen with market conditions. Because FFO excludes depreciation and amortization unique to real estate, gains and losses from property dispositions and extraordinary items, it provides a performance measure that, when compared year over year, reflects the impact to operations from trends in occupancy rates, rental rates, operating costs, development activities and interest costs, providing perspective not immediately apparent from net income. We compute FFO in accordance with the current standards established by the Board of Governors of the National Association of Real Estate Investment Trusts, or NAREIT, which may differ from the methodology for calculating FFO utilized by other equity REITs and, accordingly, may not be comparable to such other REITs. The NAREIT reporting guidance directs companies, for the computation of NAREIT FFO, to exclude impairments of depreciable real estate and impairments to investments in affiliates when write-downs are driven by measurable decreases in the fair value of depreciable real estate held by the affiliate. FFO does not represent amounts available for management's discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments and uncertainties. FFO should not be considered as an alternative to net income (computed in accordance with GAAP) as an indicator of our financial performance or to cash flow from operating activities (computed in accordance with GAAP) as an indicator of our liquidity, nor is it indicative of funds available to fund our cash needs, including our ability to pay distributions. 17 Reporting Definitions Three Months Ended June 30, 2012 Adjusted EBITDA: Net (loss) income attributable to controlling interest (19,322) Add: Depreciation and amortization 30,964 Interest expense, net 15,869 EBITDA 27,511 Acquisition -related expenses 2,970 Debt extinguishment costs 1,886 Listing expenses 12,544 Stock based compensation 505 Adjusted EBITDA 45,416 Adjusted EBITDA Annualized 181,664 $ $ $ $ |