As filed with the Securities and Exchange Commission on August 11, 2006

Registration No. 333-133895

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 4

To

FORM S-4

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

AFFINION GROUP, INC.

and the Guarantors identified in footnote (1) below

(Exact name of registrant as specified in its charter)

| | | | |

| Delaware | | 7389 | | 06-1637809 |

(State or other jurisdiction

of incorporation or organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer

Identification Number) |

100 Connecticut Avenue

Norwalk, CT 06850

(203) 956-1000

(Address, including zip code, and telephone number, including area code, of registrants’ principal executive offices)

Todd H. Siegel, Esq.

Executive Vice President and General Counsel

Affinion Group, Inc.

100 Connecticut Avenue

Norwalk, CT 06850

(203) 956-1000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Rosa A. Testani, Esq.

Akin Gump Strauss Hauer & Feld LLP

590 Madison Avenue

New York, New York 10022

(212) 872-1000

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

ADDITIONAL SUBSIDIARY GUARANTOR REGISTRANTS:

| (1) | Each of the following is a guarantor of the obligations of Affinion Group, Inc. under the 10 1/8% Senior Notes due 2013 and the 11½% Senior Subordinated Notes due 2015, each is a Co-Registrant, and each is incorporated in the jurisdiction and has the I.R.S. Employer Identification Number indicated: Affinion Benefits Group, Inc., a Delaware corporation (06-1282786); Affinion Data Services, Inc., a Delaware corporation (22-3797237); Affinion Group, LLC, a Delaware limited liability company (06-1501906); Affinion Publishing, LLC, a Delaware limited liability company (06-1282776); Cardwell Agency, Inc. a Virginia corporation (54-1374514); CUC Asia Holdings, a Delaware general partnership (06-1487080); Long Term Preferred Care, Inc., a Tennessee corporation (62-1455251); Travelers Advantage Services, Inc., a Delaware corporation (20-2221128); Trilegiant Auto Services, Inc., a Wyoming corporation (06-1633722); Trilegiant Corporation, a Delaware corporation (20-0641090); Trilegiant Insurance Services, Inc., a Delaware corporation (06-1588614); Affinion Loyalty Group, Inc., a Delaware corporation (06-1623335); and Trilegiant Retail Services, Inc., a Delaware corporation (06-1625615). Pursuant to Rule 457(n), no additional registration fee is payable with respect to such guarantees. |

The registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not complete the exchange offer and issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell securities and it is not soliciting an offer to buy these securities in any state where the offer is not permitted.

Subject to completion, dated August 11, 2006

Affinion Group, Inc.

Offer to Exchange

$304,000,000 aggregate principal amount of 10 1/8% Senior Notes due 2013 which have been registered under the Securities Act of 1933 for $304,000,000 aggregate principal amount of outstanding 10 1/8% Senior Notes due 2013.

$355,500,000 aggregate principal amount of 11 1/2% Senior Subordinated Notes due 2015 which have been registered under the Securities Act of 1933 for $355,500,000 aggregate principal amount of outstanding 11 1/2% Senior Subordinated Notes due 2015.

We hereby offer, upon the terms and subject to the conditions set forth in this prospectus and the accompanying letter of transmittal (which together constitute the “exchange offer”), to exchange up to

| | • | | $304,000,000 aggregate principal amount of our registered 10 1/8% Senior Notes due 2013, which we refer to as the exchange senior notes, for a like principal amount of our outstanding 10 1/8% Senior Notes due 2013, which we refer to as the old senior notes, and |

| | • | | $355,500,000 aggregate principal amount of our registered 11 1/2% Senior Secured Subordinated Notes due 2015, which we refer to as our exchange senior subordinated notes, for a like principal amount of our outstanding 11 1/2% Senior Secured Subordinated Notes due 2015, which we refer to as our old senior subordinated notes. |

The terms of the exchange notes are identical to the terms of the old notes in all material respects, except for the elimination of some transfer restrictions, registration rights and additional interest provisions relating to the old notes.

Interest on the exchange notes, like the old notes, will be payable semiannually on April 15 and October 15. The exchange senior notes will mature on October 15, 2013, and the exchange senior subordinated notes will mature on October 15, 2015. We may redeem some or all of the exchange senior notes at any time on or after October 15, 2009 and the exchange senior subordinated notes at any time on or after October 15, 2010, at the redemption prices set forth in this prospectus. In addition, we may redeem up to 35% of the aggregate principal amount of the exchange senior notes and the exchange senior subordinated notes using net proceeds from certain equity offerings completed on or prior to October 15, 2008.

The exchange senior notes and guarantees thereof, like the old senior notes and guarantees thereof, will be our and the applicable guarantor’s senior unsecured obligations and will rank equally in right of payment to all of our and the applicable guarantor’s existing and future senior indebtedness ($1,124.0 million as of March 31, 2006 on a pro forma basis, including the senior notes), senior in right of payment to all of our and the applicable guarantor’s existing and future subordinated indebtedness ($355.5 million as of March 31, 2006 on a pro forma basis, all of which would have consisted of the senior subordinated notes and guarantees thereof), be effectively subordinated in right of payment to our and the applicable guarantor’s secured indebtedness to the extent of the value of the assets securing such indebtedness (approximately $820.8 million as of March 31, 2006 on a pro forma basis), and be effectively subordinated to all obligations, including trade payables, of each of our and the applicable guarantor’s existing and future subsidiaries that are not guarantors (approximately $90.1 million as of March 31, 2006 on a pro forma basis).

The exchange senior subordinated notes and guarantees thereof, like the old senior subordinated notes and guarantees thereof, will be our and the applicable guarantor’s senior subordinated unsecured obligations and will rank junior in right of payment to all of our and the applicable guarantor’s existing and future senior indebtedness ($1,124.0 million as of March 31, 2006 on a pro forma basis), rank equally in right of payment with all of our and the applicable guarantor’s future senior subordinated indebtedness, be effectively subordinated in right of payment to our and the applicable guarantor’s secured indebtedness to the extent of the value of the assets securing such indebtedness ($820.8 million as of March 31, 2006 on a pro forma basis), and be effectively subordinated to all obligations, including trade payables, of each of our and the applicable guarantor’s existing and future subsidiaries that are not guarantors (approximately $90.1 million as of March 31, 2006 on a pro forma basis) and rank senior in right of payment to all of our and the applicable guarantor’s future subordinated indebtedness.

We will exchange any and all old notes that are validly tendered and not validly withdrawn prior to 5:00 p.m., New York City time, on September 12, 2006, unless extended.

We have not applied, and do not intend to apply, for listing the notes on any national securities exchange or automated quotation system.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal states that by so acknowledging and delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for old notes where such old notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

You should carefully consider therisk factors beginning on page 21 of this prospectus before participating in this exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2006.

TABLE OF CONTENTS

You should rely only on the information contained in this document. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our exchange notes. In this prospectus, unless the context otherwise requires or indicates, (i) all references to “Affinion,” the “Company,” “we,” “our” and “us” refer to Affinion Group, Inc., a Delaware corporation, and its subsidiaries on a consolidated basis after giving effect to the consummation on October 17, 2005 of the acquisition (the “Acquisition”) by Affinion Group, Inc. of Affinion Group, LLC (known as Cendant Marketing Group, LLC prior to the consummation of the Acquisition) (“AGLLC”) and Affinion International Holdings Limited (known as Cendant International Holdings Limited prior to the consummation of the Acquisition) (“AIH”) and the other transactions described in this prospectus under “The Transactions,” but for periods prior to the Acquisition, refer to the historical operations of Cendant Marketing Services Division (a division of Cendant Corporation) (the “Predecessor”) that we acquired in the Acquisition, (ii) all references to “Holdings” refer to our parent company, Affinion Group Holdings, Inc., a Delaware corporation, (iii) all references to “pro forma” statement of operations data give effect to the Transactions, the Refinancing and the Additional Senior Notes Offering set forth under “Unaudited Pro Forma Condensed Consolidated Financial Information,” and all references to “pro forma” balance sheet data give effect to the Refinancing and the Additional Senior Notes Offering and (iv) all references to “fiscal year” are to the twelve months ended December 31 of the year referenced.

Until , 2006 (90 days after the date of this prospectus), all dealers effecting transactions in the exchange notes, whether or not participating in the exchange offer, may be required to deliver a prospectus.

i

WHERE YOU CAN FIND MORE INFORMATION

We will be required to file annual and quarterly reports and other information with the SEC after the registration statement described below is declared effective by the SEC. You may read and copy any reports, statements and other information that we file with the SEC at the SEC’s public reference room located at 100 F Street, N.E. Room 1580, Washington, D.C. 20549. You may request copies of the documents, upon payment of a duplicating fee, by writing the Public Reference Section of the SEC. Please call 1-800-SEC-0330 for further information on the public reference rooms. Our filings will also be available to the public from commercial document retrieval services and at the web site maintained by the SEC at http://www.sec.gov.

We have filed a registration statement on Form S-4 to register with the SEC the exchange notes to be issued in exchange for the old notes and guarantees thereof. This prospectus is part of that registration statement. As allowed by the SEC’s rules, this prospectus does not contain all of the information you can find in the registration statement or the exhibits to the registration statement. You should note that where we summarize in the prospectus the material terms of any contract, agreement or other document filed as an exhibit to the registration statement, the summary information provided in the prospectus is less complete than the actual contract, agreement or document. You should refer to the exhibits filed to the registration statement for copies of the actual contract, agreement or document.

We have not authorized anyone to give you any information or to make any representations about us or the transactions we discuss in this prospectus other than those contained in this prospectus. If you are given any information or representations about these matters that is not discussed in this prospectus, you must not rely on that information. This prospectus is not an offer to sell or a solicitation of an offer to buy securities anywhere or to anyone where or to whom we are not permitted to offer or sell securities under applicable law.

INDUSTRY AND MARKET DATA

Industry and market data used throughout this prospectus were obtained from the Direct Marketing Association’s Statistical Fact Book 2005, Topic Overview: US Online Retail by Forrester Research, Inc. (December 2005), and others. While we believe that our own research and estimates are reliable and appropriate, we have not independently verified such data nor have we made any representation as to the accuracy of such information. Unless otherwise indicated, all references to market share data appearing in this prospectus are as of December 31, 2005.

TRADEMARKS

We have proprietary rights to a number of trademarks used in this prospectus which are important to our business, including Affinion Group, Trilegiant, Progeny Marketing Innovations, Cims, Trilegiant Loyalty Solutions, PrivacyGuard, Hot-Line, Travelers Advantage, Shoppers Advantage, AutoVantage, CompleteHome, Buyers Advantage, HealthSaver, NHPA, Enhanced Checking, Small Business Solutions and Wellness Extras. We have omitted the “®” and “™” trademark designations for such trademarks in this prospectus. Nevertheless, all rights to such trademarks named in this prospectus are reserved.

ii

SUMMARY

The following summary contains basic information about this offering contained elsewhere in this prospectus. It is not complete and may not contain all of the information that is important to you. You should read this entire prospectus carefully, including “Risk Factors,” the consolidated and combined financial statements and the related notes thereto, before making an investment decision.

We refer to the old senior notes and the old senior subordinated notes collectively as the old notes. We refer to the exchange senior notes and the exchange senior subordinated notes collectively as the exchange notes. We refer to the old notes and the exchange notes collectively as the notes. We refer to the old senior notes and the exchange senior notes collectively as the senior notes and the old senior subordinated notes and the exchange senior subordinated notes collectively as the senior subordinated notes.

Our Company

We are a leading affinity direct marketer to consumers of value-added membership programs and services in which program members receive various benefits, discount opportunities and incentives, and of insurance and package enhancement programs and services to our affinity partners who in turn offer them to their consumers. We have over 30 years of experience in the affinity direct marketing industry. Affinity direct marketing is a subset of the larger direct marketing industry which involves direct marketing to the customers of affinity partners, such as financial institutions and retailers. We offer our programs and services worldwide through approximately 4,500 affinity partners as of March 31, 2006. Affinity partners are third parties with whom we have a contractual relationship and through whom we offer our products and services to their clients. Our diversified base of affinity partners includes leading companies in a wide variety of industries, including financial services, retail, travel, telecommunications, utilities and Internet. We market to consumers using direct mail, online marketing, in-branch marketing, telemarketing and other marketing methods. We generate predictable revenues and cash flows because of our large base of existing customers, which accounts for the majority of our near-term cash flow, and the fact that customer retention and renewals generally follow well-established patterns. We also have a growing loyalty solutions operation which administers points-based loyalty programs in which members receive points that can be redeemed for discounts, cash and merchandise as a reward for continued loyalty to a particular program or partner. As of December 31, 2005, we had worldwide approximately 70 million members and end-customers, and approximately 3,000 employees in the U.S. and 11 countries, primarily in Europe. We refer to members as those consumers to whom we provide services directly and have a contractual relationship. We refer to end-customers as those consumers that we service on behalf of a third party, such as one of our affinity partners, with whom we have a contractual relationship. We calculate the number of our members by taking a weighted average for the period based on the number of customers who are active in our programs. We calculate the number of end-customers based on the number of customers whom we are required to service under our agreements. For the year ended December 31, 2005, we had pro forma net revenues of $1.2 billion, pro forma Adjusted EBITDA (as defined on page 19) of $257.2 million and a pro forma net loss of $433.8 million. For the year ended December 31, 2005 and the three months ended March 31, 2006, we derived approximately 59% and 58%, respectively, of our net revenues from members and end-customers under marketing and servicing arrangements with 10 of our affinity partners. For the three months ended March 31, 2006, we had pro forma net revenues of $245.9 million, and a pro forma net loss of $127.2 million.

1

We operate our business through the following operating segments:

| | • | | Membership Operations(54.0% of 2005 pro forma net revenues)—Our membership operations in the U.S. are operated through Trilegiant, which designs, implements, and markets membership programs to customers of our affinity partners. We believe we are the leader in the U.S. affinity membership marketing industry with approximately 13.6 million members as of December 31, 2005. For an annual or monthly membership fee, we provide members with access to a variety of discounts and shop-at-home conveniences in such areas as retail merchandise, travel, automotive and home improvement; as well as personal protection benefits and value-added services including credit monitoring and identity-theft resolution services. Our affinity partners, such as financial institutions, retailers and other consumer-oriented companies, offer individual membership programs to their customers as an enhancement to, or in connection with, their use of credit and/or debit cards, checking accounts, mortgage loans or other financial payment vehicles. |

| | • | | Insurance and Package Operations (26.5% of 2005 pro forma net revenues)—Our insurance and package enhancement operations in the U.S. are operated through Affinion Benefits Group, Inc. (formerly known as Progeny Marketing Innovations, Inc.) (“Progeny”). We believe we are a leading direct marketer of accidental death and dismemberment insurance (“AD&D”) in the U.S. with over 31 million end-customers. We serve as an agent and third-party administrator for the marketing of AD&D and other insurance programs, and market private-label insurance programs to the customers of our affinity partners, typically financial institutions, primarily through direct mail. |

| | • | | International Operations (14.8% of 2005 pro forma net revenues)—Our international membership and package enhancement operations are operated primarily in Europe through Cims. We believe we are the largest marketer of membership programs and package enhancement programs in Europe, with approximately 2.2 million members and 16.7 million end-customers as of December 31, 2005. |

| | • | | Loyalty Operations (4.7% of 2005 pro forma net revenues)—Our growing loyalty operations are operated through Affinion Loyalty Group, Inc. (“ALG”) (formerly known as Trilegiant Loyalty Solutions) (“TLS”). We believe we are a leader in online points redemption and administrative services and currently manage approximately 125 billion points for our customers with an estimated redemption value of over $1.5 billion as of December 31, 2005. We typically charge clients a per-member and/or a per-activity administrative fee for our services and do not retain any points-related liabilities. |

Our Competitive Strengths

Global Leader in a Growing Industry.We are a leading affinity direct marketer of value-added membership, insurance and package enhancement programs and services with approximately 70 million members and end-customers worldwide and a network of approximately 4,500 affinity partners as of March 31, 2006.

2

Proven Business Model Generates Predictable Financial Results with Significant Future Revenue Streams.Our business model includes planning new marketing initiatives based on predicted response and attrition rates, as well as other variables (such as product and servicing costs) drawn from in-depth analysis of our prior marketing campaigns.

Flexible Operating Model Focused on Free Cash Flow Generation. We believe that our operating model will generate significant free cash flow, which we define as cash provided by operating activities less capital expenditures and required debt service payments, as a result of our low capital expenditure requirements and variable cost structure. Our operating model is also highly scalable, allowing us to expand our business without significant additional fixed costs.

Strong, Long-Term Relationships with Diverse Affinity Partners.We have cultivated strong long-term relationships with our affinity partners who are in a wide variety of industries, including financial services, retail, travel, telecommunications, utilities, Internet and other media.

Disciplined Marketing Approach Driven by Models and Proprietary Databases.We have over 30 years of experience in creating, executing and refining marketing programs with our affinity partners. Our marketing approach employs models and proprietary databases containing preferences and response rates for our products, as well as detailed performance and profitability data.

Leading Loyalty Solutions Platform.We currently manage approximately 125 billion points with an estimated redemption value of over $1.5 billion as of December 31, 2005. We believe we are well positioned in this business due to our scale, leading technical capabilities and experience in assisting companies to manage their points liabilities, which are vital to companies seeking to differentiate their programs and enhance their efficiency and profitability.

Committed and Experienced Management Team. Our senior management team has extensive experience in the direct marketing industry, with a proven operational track record and strong relationships with key decision-makers at our affinity partners.

Risk Factors

Despite our competitive strengths summarized above and discussed elsewhere in this prospectus, participating in this exchange offer involves substantial risk. In addition, our ability to execute our business strategy is subject to certain risks. Before you participate in this exchange offer, you should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors” beginning on page 21. For example, the following key risks may cause us not to realize the full benefits of our competitive strengths or may cause us to be unable to successfully execute all or part of our business strategy or may materially adversely affect our business, financial condition, results of operations or ability to pay the notes.

| | • | | Substantial Indebtedness.We are a highly leveraged company. As of March 31, 2006, we would have had, after giving pro forma effect to the Refinancing (as defined on page 6) and the Additional Senior Notes Offering (as defined on page 6), $1.5 billion principal amount of outstanding indebtedness. Our substantial indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from making debt service payments on the notes. We may not be able to generate sufficient cash to service all of our indebtedness, including the notes, and may be forced to take other actions to satisfy our obligations under our indebtedness that may not be successful. Despite our substantial indebtedness, we may still be able to incur significantly more debt. In addition, your right to receive payments on the notes is effectively junior to those lenders who have a security interest in our assets and to all liabilities of our non-guarantor subsidiaries. |

3

| | • | | Limited Operating History. We have a limited history as a stand-alone company and may not be successful as an independent company. The financial information in this prospectus may not be reflective of our operating results and financial condition as a separate, stand-alone entity. |

| | • | | Concentration Risk.We derive a substantial amount of our revenue from the members and end-customers we obtained through only a few of our affinity partners. If we were to lose one or more of our agreements with our affinity partners, we would lose access to prospective members and end-customers and could lose sources of revenue. |

| | • | | Competition Risk. Our business is highly competitive. We may be unable to compete effectively with other companies in our industry that have financial or other advantages and increased competition could lead to reduced market share, a decrease in margins and a decrease in revenue. |

| | • | | Regulatory Risk. Our business is increasingly subject to U.S. and foreign governmental regulation, which could impede our ability to market our programs and services and reduce our profitability. In addition, we are subject to numerous legal actions that could have a negative impact on our financial condition, results of operations, cash flows or reputation. |

| | • | | Control by Apollo. Approximately 97% of the common stock of Holdings is held by investment funds affiliated with Apollo. As a result, Apollo controls us and has the power to elect a majority of the members of our board of directors, appoint new management and approve any action requiring the approval of the holders of Holdings’ stock, including approving acquisitions or sales of all or substantially all of our assets. Apollo’s interests may differ from your interests as a holder of the notes. |

Our Business Strategy

Our strategy is to maintain and enhance our position as a leading global affinity direct marketer by providing valuable, high quality and affordable programs and services that reinforce the relationship between the customer and our affinity partners and to focus on attractive opportunities which would increase our growth and cash flows. The principal elements of this strategy are summarized below.

| | • | | Focus on Increasing Profitability. The integration of our operations will enable us to further optimize the allocation of our marketing spend across all of our operations and geographic regions in order to maximize the returns on each marketing campaign and, therefore, our overall long-term profitability. In addition, we expect that an expansion of our range of hybrid or bundled programs, the ongoing shift of members from annual to monthly billing programs, minimizing operating costs and capitalizing on the benefits of outsourcing and a more variable cost structure will increase our profitability. |

| | • | | Continue to Execute Our Online Strategy for Customer Acquisition and Fulfillment. Since late 2003, we have pursued a strategy of leveraging the Internet for customer acquisition and fulfillment in order to capitalize on the increasing penetration and usage rates of the Internet, and we will continue to do so. |

| | • | | Expand Our Range of Affinity Partners. We believe there are substantial opportunities to increase our presence in the travel, cable, telecom and utilities industries, in both the U.S. and Europe. |

| | • | | Grow Our International Retail Operations. We believe that we are well positioned to provide our affinity partners and clients with comprehensive offerings on a global basis, particularly with our membership programs. We intend to grow our international retail membership operations by leveraging our significant U.S. experience to offer membership programs comparable to existing U.S. membership programs to European customers. |

| | • | | Continue to Focus on New Program Development. We continually develop and test new programs to identify consumer trends that can be converted into revenue-enhancing opportunities. |

4

| | • | | Leveraging Best Practices and Cross-Selling Opportunities. Since completing the integration of our operations, which we began in 2004, we have begun implementing best practices across our operations. We also intend to capitalize on the significant opportunities to cross-sell products across business lines and geographical regions that have been created by our business integration. |

The Transactions

On July 26, 2005, we, along with our parent company, Holdings, entered into a purchase agreement with Cendant. Pursuant to the purchase agreement, on October 17, 2005, we purchased from Cendant all of the equity interests of AGLLC, and all of the share capital of AIH. The aggregate purchase price paid to Cendant was approximately $1.8 billion (consisting of cash and newly issued preferred stock of Holdings and after giving effect to certain fixed adjustments), subject to further adjustments as provided in the purchase agreement. These purchase price adjustments primarily relate to management retention and supplemental bonus payments which are earned over a one year period from the closing date of the Acquisition. If payments are not made to members of management because they resign or are terminated for cause, applicable cash amounts will be paid to Cendant. Any purchase price adjustment related to these management bonus refunds will be recorded in the fourth quarter of 2006. In addition, Cendant received a warrant to purchase up to 7.5% of the common stock of Holdings, subject to customary anti-dilution adjustments.

As a result of the Acquisition, Holdings owns 100% of our total capital stock. As of December 31, 2005, (i) approximately 97% of Holdings’ outstanding common stock is owned by Affinion Group Holdings, LLC, a Delaware limited liability company (“Parent LLC”) and an affiliate of Apollo Management V, L.P. (“Apollo”), with the remaining 3% owned by the management stockholders and (ii) 100% of Holdings’ outstanding preferred stock is owned by Cendant.

In connection with the Acquisition, (i) we and Holdings entered into a $960.0 million senior secured credit facility, consisting of a $100.0 million revolving credit facility and an $860.0 million term loan B facility, with Credit Suisse First Boston LLC (“Credit Suisse”) and Deutsche Bank Securities Inc. (“DBSI”) as joint bookrunners and joint lead arrangers, Credit Suisse, Cayman Islands Branch, as administrative agent, DBSI as syndication agent, Bank of America, N.A. and BNP Paribas Securities Corp. (“BNPPSC”) as co-documentation agents, and other lenders, (ii) we and Holdings entered into a $383.6 million unsecured senior subordinated bridge loan facility with Credit Suisse, Cayman Islands Branch, as administrative agent, DBSI as syndication agent, Banc of America Bridge LLC and BNPPSC as co-documentation agents, and Credit Suisse and DBSI as joint lead arrangers and joint bookrunners, and other lenders and (iii) we entered into an indenture with Wells Fargo Bank, National Association, as trustee, and issued $270 million of our 10 1/8% senior notes due 2013 (the “initial senior notes”) in a private placement offering.

Additionally, in connection with the Acquisition, affiliates of Apollo made a cash equity investment of approximately $275.0 million. In this prospectus, we refer to the borrowings under our credit facility and our senior subordinated bridge loan facility, our issuance of the initial senior notes and the equity investment, along with the application of the proceeds therefrom, collectively, the “Acquisition Financing.”

As used in this prospectus, the term “Transactions” means, collectively, the Acquisition and the Acquisition Financing.

The Acquisition was financed by:

| | • | | the $266.4 million of gross proceeds from the issuance of $270 million principal amount of our initial senior notes; |

| | • | | borrowings of $860.0 million under the term loan B portion of our credit facility (our $100.0 million revolving credit facility was undrawn on October 17, 2005); |

5

| | • | | borrowings of $383.6 million under our senior subordinated bridge loan facility (which amount has been fully refinanced, as described below under “—The Refinancing” and “—The Additional Senior Notes Offering”); |

| | • | | a cash equity investment of $275.0 million by affiliates of Apollo; and |

| | • | | the issuance to Cendant of preferred shares of Holdings having a $125.0 million liquidation preference (valued on a preliminary basis at $80.4 million in our consolidated financial statements) and a warrant (valued on a preliminary basis at $16.7 million in our consolidated financial statements). |

The warrant will be exercisable on or after the October 17, 2009 (or earlier, if Apollo achieves certain returns on its investment). The warrant is not currently exercisable and is not expected to become exercisable within 60 days. On March 20, 2006, the exercise price of the warrant was $10.50, which reflects a $10 per share purchase price paid by Parent LLC for shares of Holdings’ common stock in connection with the Transactions, and a 5% quarterly increase. The exercise price will be increased by 5% on every three month anniversary of the closing date of the Transactions, subject to certain adjustments, and will be multiplied by 2.18 if certain dividends or distributions are made on Holdings’ common stock.

The preferred stock entitles its holder to receive dividends of 8.5% per annum (payable, at Holdings’ option, either in cash or in kind) and ranks senior to shares of all other classes or series of stock with respect to rights upon a liquidation or sale of Holdings at a price of the then-current face amount, plus any accrued and unpaid dividends. The preferred stock is redeemable at Holdings’ option at any time, subject to the applicable terms of our debt instruments and applicable laws. See “Security Ownership of Certain Beneficial Owners and Management” for additional information about the terms of the preferred stock.

The Refinancing

As used in this prospectus, the term “Refinancing” means the April 26, 2006 offer and issuance of the $355.5 million principal amount of our old senior subordinated notes and the application of the gross proceeds from the old senior subordinated notes, together with cash on hand to repay $349.5 million of outstanding borrowings under our senior subordinated bridge loan facility, plus accrued interest, and to pay fees and expenses associated with such offering.

The Additional Senior Notes Offering

As used in this prospectus, the term “Additional Senior Notes Offering” means the May 3, 2006 offer and issuance of an additional $34.0 million principal amount of our 10 1/8% senior notes due 2013 (the “additional senior notes”) and the application of the gross proceeds from the additional senior notes, together with cash on hand, to repay the remaining $34.1 million of outstanding borrowings under our senior subordinated bridge loan facility, plus accrued interest, and to pay fees and expenses associated with such offering.

6

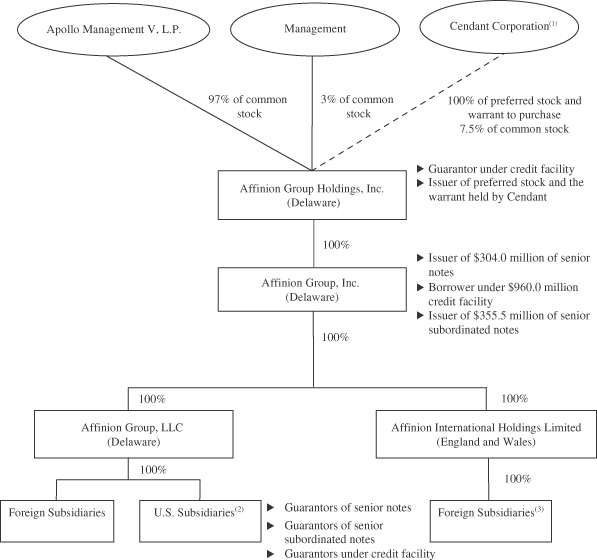

Corporate Structure

The chart below summarizes our simplified ownership and capital structure at March 31, 2006 on a pro forma basis after giving effect to the Refinancing and the Additional Senior Notes Offering:

| (1) | The warrant held by Cendant will be exercisable on or after October 17, 2009 (or earlier, if Apollo achieves certain returns on its investment). The warrant is not currently exercisable and is not expected to become exercisable within 60 days. See “Security Ownership of Certain Beneficial Owners and Management.” |

| (2) | Certain U.S. subsidiaries are not guarantors of the senior notes, the senior subordinated notes or our credit facility. See “Description of the Senior Notes—Guarantees” and “Description of the Senior Subordinated Notes—Guarantees.” |

| (3) | Certain foreign subsidiaries are not wholly-owned. See Note 11 to our 2005 audited consolidated and combined financial statements included elsewhere herein. |

7

The Sponsor

Apollo, our principal equity sponsor, is an affiliate of Apollo Management, L.P. Apollo Management, L.P. was founded in 1990 and is among the most active and successful private investment firms in the United States in terms of both number of investment transactions completed and aggregate dollars invested. Since its inception, Apollo Management, L.P. and affiliates have managed in excess of $13 billion in equity capital, in a wide variety of industries, both domestically and internationally, and are currently managing their latest fund, Apollo Investment Fund VI, L.P., with total committed capital of over $10 billion. Companies owned or controlled by Apollo Management, L.P. and affiliates or in which Apollo Management L.P. and affiliates have a significant equity investment include, among others, AMC Entertainment, Inc., Educate, Inc., General Nutrition Centers, Inc., Hexion Specialty Chemicals, Inc., Metals USA, Inc., Nalco Company and UAP Holding Corp.

Corporate Information

We are a Delaware corporation formed in July 2005 and are a holding company whose assets consist of the capital stock of our direct subsidiaries. Our headquarters and principal executive offices are located at 100 Connecticut Avenue, Norwalk, Connecticut 06850 and our telephone number is (203) 956-1000.

8

Summary of the Terms of the Exchange Offer

In connection with the Acquisition Financing, we and the guarantors of the initial senior notes entered into a registration rights agreement with the initial purchasers of the initial senior notes. Under that agreement, we agreed to use commercially reasonable efforts to file a registration statement related to the exchange of initial senior notes for exchange senior notes with the SEC on or before April 15, 2006 and to cause the registration statement to become effective under the Securities Act on or prior to the 300th day after the issue date of the initial senior notes. Because we did not file the registration statement with the SEC on or before April 15, 2006, we have incurred additional interest expense pursuant to the registration rights agreement in the aggregate amount of approximately $46,500. We intend to pay the additional interest on October 15, 2006, the next scheduled interest payment date.

In connection with the Refinancing, we and the guarantors of the old senior subordinated notes entered into a registration rights agreement with the initial purchasers of the old senior subordinated notes. Under that agreement, we agreed to use commercially reasonable efforts to file a registration statement related to the exchange of old senior subordinated notes for exchange senior subordinated notes with the SEC on or prior to the 180th day after the issue date of the old senior subordinated notes and to cause the registration statement to become effective under the Securities Act on or prior to the 300th day after the issue date of such old senior subordinated notes.

In connection with the Additional Senior Notes Offering, we and the guarantors of the additional senior notes entered into a registration rights agreement with the initial purchasers of the additional senior notes. Under that agreement, we agreed to use commercially reasonable efforts to file a registration statement related to the exchange of additional senior notes for exchange senior notes with the SEC on or prior to the 180th day after the issue date of the additional senior notes and to cause the registration statement to become effective under the Securities Act on or prior to the 300th day after the issue date of such additional senior notes.

The registration statement of which this prospectus forms a part was filed in compliance with the obligations under these registration rights agreements.

You are entitled to exchange in this exchange offer your old notes for exchange notes which are identical in all material respects to the old notes except that:

| | • | | the exchange notes have been registered under the Securities Act and will be freely tradable by persons who are not affiliated with us; |

| | • | | the exchange notes are not entitled to registration rights which are applicable to the old notes under the registration rights agreements; and |

| | • | | our obligation to pay additional interest on the old notes as described in the registration rights agreements does not apply to the exchange notes. |

For purposes of this and other sections in this prospectus, we refer to the old notes and the exchange notes together as the “notes.”

9

The Exchange Offer

Senior Notes | We are offering to exchange up to $304,000,000 aggregate principal amount of our 10 1/8% Senior Notes due 2013 which have been registered under the Securities Act for up to $270,000,000 aggregate principal amount of our old senior notes which were issued on October 17, 2005 and up to $34,000,000 aggregate principal amount of our old senior notes which were issued on May 3, 2006. Old senior notes may be exchanged only in integral amounts of $1,000. |

Senior Subordinated Notes | We are offering to exchange up to $355,500,000 aggregate principal amount of our 11 1/2% Senior Subordinated Notes due 2015 which have been registered under the Securities Act for up to $355,500,000 aggregate principal amount of our old senior subordinated notes which were issued on April 26, 2006. Old senior subordinated notes may be exchanged only in integral amounts of $1,000. |

Resales | Based on interpretations by the staff of the Securities and Exchange Commission (the “SEC”) set forth in no-action letters issued to third parties, we believe that the exchange notes issued pursuant to this exchange offer in exchange for old notes may be offered for resale, resold and otherwise transferred by you (unless you are our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration provisions of the Securities Act, provided that you |

| | • | | are acquiring the exchange notes in the ordinary course of business, and |

| | • | | have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. |

Each participating broker-dealer that receives exchange notes for its own account pursuant to this exchange offer in exchange for the old notes that were acquired as a result of market-making or other trading activity must acknowledge that it will deliver a prospectus in connection with any resale of the exchange notes. See “Plan of Distribution.”

Any holder of notes who

| | • | | does not acquire the exchange notes in the ordinary course of business, or |

| | • | | tenders in this exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes |

cannot rely on the position of the staff of the SEC expressed in Exxon Capital Holdings Corporation, Morgan Stanley & Co. Incorporated or

10

| | similar no-action letters and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the exchange notes. |

Expiration; Withdrawal of Tenders | This exchange offer will expire at 5:00 p.m., New York City time, September 12, 2006, or such later date and time to which we extend it. We do not currently intend to extend the expiration date. A tender of old notes pursuant to this exchange offer may be withdrawn at any time prior to the expiration date. Any old notes not accepted for exchange for any reason will be returned without expense to the tendering holder promptly after the expiration or termination of this exchange offer. |

Delivery of the Exchange Notes | The exchange notes issued pursuant to this exchange offer will be delivered to the holders who tender old notes promptly following the expiration date. |

Conditions to this Exchange Offer | This exchange offer is subject to customary conditions, some of which we may waive. See “The Exchange Offer—Certain Conditions to this Exchange Offer.” |

Procedures for Tendering Old Notes | If you wish to accept this exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a copy of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, or the copy, together with the old notes and any other required documents, to the exchange agent at the address set forth on the cover of the letter of transmittal. If you hold old notes through The Depository Trust Company (“DTC”) and wish to participate in this exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. |

By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things:

| | • | | any exchange notes that you will receive will be acquired in the ordinary course of your business; |

| | • | | you have no arrangement or understanding with any person or entity to participate in the distribution of the exchange notes; |

| | • | | if you are a broker-dealer that will receive exchange notes for your own account in exchange for old notes that were acquired as a result of market-making activities, that you will deliver a prospectus, as required by law, in connection with any resale of such exchange notes; and |

| | • | | you are not our “affiliate” as defined in Rule 405 under the Securities Act. |

11

Guaranteed Delivery Procedures | If you wish to tender your old notes and your old notes are not immediately available or you cannot deliver your old notes, the letter of transmittal or any other documents required by the letter of transmittal or if you cannot comply with the applicable procedures under DTC’s Automated Tender Offer Program prior to the expiration date, you must tender your old notes according to the guaranteed delivery procedures set forth in this prospectus under “The Exchange Offer—Guaranteed Delivery Procedures.” |

Effect on Holders of Old Notes | As a result of the making of, and upon acceptance for exchange of all validly tendered old notes pursuant to the terms of, this exchange offer, we will have fulfilled a covenant contained in the registration rights agreements and, accordingly, additional interest on the old notes, if any, shall no longer accrue and we will no longer be obligated to pay additional interest as described in the registration rights agreements. If you are a holder of old notes and do not tender your old notes in this exchange offer, you will continue to hold such old notes and you will be entitled to all the rights and limitations applicable to the old notes in the indenture, except for any rights under the registration rights agreement that by their terms terminate upon the consummation of this exchange offer. |

Consequences of Failure to Exchange | All untendered old notes will continue to be subject to the restrictions on transfer provided for in the old notes and in the indentures governing the old notes. In general, the old notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with this exchange offer, or as otherwise required under certain limited circumstances pursuant to the terms of the registration rights agreements, we do not currently anticipate that we will register the old notes under the Securities Act. |

Certain U.S. Federal Income Tax Considerations | The exchange of old notes for exchange notes in this exchange offer should not be a taxable event for U.S. federal income tax purposes. See “Certain U.S. Federal Income Tax Considerations.” |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the exchange notes in this exchange offer. |

Exchange Agent | Wells Fargo Bank, National Association is the exchange agent for this exchange offer. The address and telephone number of the exchange agent are set forth in the section captioned “The Exchange Offer—Exchange Agent.” |

12

Summary of the Terms of the Exchange Notes

Issuer | Affinion Group, Inc. |

Exchange Notes Offered:

Senior Notes | $304,000,000 aggregate principal amount of 10 1/8% Senior Notes due 2013. |

Senior Subordinated Notes | $355,500,000 aggregate principal amount of 11 1/2% Senior Subordinated Notes due 2015. |

Maturity Date:

Senior Notes | The senior notes mature on October 15, 2013. |

Senior Subordinated Notes | The senior subordinated notes mature on October 15, 2015. |

Interest:

Senior Notes | 10 1/8% per annum, payable semi-annually on April 15 and October 15 of each year. |

Senior Subordinated Notes | 11 1/2 % per annum, payable semi-annually on April 15 and October 15 of each year. . |

Guarantees | The exchange notes, like the old notes, will be guaranteed by all of our existing and future domestic subsidiaries that guarantee our indebtedness under our credit facility and our old notes. Each of our existing domestic subsidiaries, other than Safecard Services Insurance Co., is a guarantor of the exchange notes. Our existing domestic subsidiaries who are guarantors consist of Affinion Benefits Group, Inc., Affinion Data Services, Inc., Affinion Group, LLC, Affinion Publishing, LLC, Cardwell Agency, Inc., CUC Asia Holdings, Long Term Preferred Care, Inc., Travelers Advantage Services, Inc., Trilegiant Auto Services, Inc., Trilegiant Corporation, Trilegiant Insurance Services, Inc., Affinion Loyalty Group, Inc., and Trilegiant Retail Services, Inc. The guarantees are full and unconditional and joint and several obligations of each of the guarantors. The obligations of each guarantor under its guarantee are limited as necessary to prevent that guarantee from constituting a fraudulent conveyance under applicable law. |

Ranking:

Senior Notes | The exchange senior notes, like the old senior notes, will be our senior unsecured obligations and will: |

| | • | | rank equally in right of payment to all of our existing and future senior indebtedness; |

| | • | | rank senior in right of payment to all of our existing and future subordinated indebtedness, including our senior subordinated notes; and |

| | • | | be effectively subordinated in right of payment to our secured indebtedness, including obligations under our credit facility, to the extent of the value of the assets securing such indebtedness, |

13

| | and be effectively subordinated to all obligations, including trade payables, of each of our existing and future subsidiaries that are not guarantors. |

| | Similarly, the guarantees of the exchange senior notes, like the guarantees of the old senior notes, will be senior unsecured obligations of the guarantors and will: |

| | • | | rank equally in right of payment to all of the applicable guarantor’s existing and future senior indebtedness; |

| | • | | rank senior in right of payment to all of the applicable guarantor’s existing and future subordinated indebtedness, including the guarantor’s guarantees under our senior subordinated notes; and |

| | • | | be effectively subordinated in right of payment to all of the applicable guarantor’s existing and future secured indebtedness, including the applicable guarantor’s guarantee under our credit facility, to the extent of the value of the assets securing such indebtedness, and be effectively subordinated to all obligations, including trade payables, of any subsidiary of a guarantor if that subsidiary is not also a guarantor. |

| | As of March 31, 2006, after giving pro forma effect to the Refinancing and the Additional Senior Notes Offering, the senior notes and the guarantees thereof would have ranked: |

| | • | | effectively subordinated to approximately $820.8 million of secured indebtedness, $820.0 million of which would have consisted of term loan borrowings under our credit facility; |

| | • | | effectively subordinated to approximately $90.1 million of liabilities, including trade payables, of our non-guarantor subsidiaries; and |

| | • | | senior in right of payment to approximately $355.5 million principal amount of subordinated indebtedness, all of which would have consisted of the senior subordinated notes. |

| | After giving pro forma effect to the Refinancing and the Additional Senior Notes Offering, our subsidiaries that are not guarantors of the senior notes would have accounted for approximately $33.2 million, or 13.5%, of our net revenues for the three months ended March 31, 2006 and would have held approximately $187.8 million, or 8.9%, of our total assets as of March 31, 2006. |

Senior Subordinated Notes | The exchange senior subordinated notes, like the old senior subordinated notes, will be our senior unsecured obligations and will: |

| | • | | rank junior in right of payment to all of our existing and future senior indebtedness, including our senior notes and obligations under our credit facility; |

| | • | | rank equally in right of payment with all of our future senior subordinated indebtedness; |

| | • | | be effectively subordinated in right of payment to our secured indebtedness, including obligations under our credit facility, to the extent of the value of the assets securing such indebtedness, |

14

| | and be effectively subordinated to all obligations, including trade payables, of each of our existing and future subsidiaries that are not guarantors; and |

| | • | | rank senior in right of payment to all of our future subordinated indebtedness. |

| | Similarly, the guarantees of the exchange senior subordinated notes, like the guarantees of the old senior subordinated notes, will be senior unsecured obligations of the guarantors and will: |

| | • | | rank junior in right of payment to all of the applicable guarantor’s existing and future senior indebtedness, including the guarantor’s guarantees under our senior notes; |

| | • | | rank equally in right of payment to all of the applicable guarantor’s existing and future senior subordinated indebtedness; |

| | • | | be effectively subordinated in right of payment to all of the applicable guarantor’s existing and future secured indebtedness, including the applicable guarantor’s guarantee under our credit facility, to the extent of the value of the assets securing such indebtedness, and be effectively subordinated to all obligations, including trade payables, of any subsidiary of a guarantor if that subsidiary is not also a guarantor; and |

| | • | | rank senior in right of payment to all of the applicable guarantor’s existing and future subordinated indebtedness. |

| | As of March 31, 2006, after giving pro forma effect to the Refinancing and the Additional Senior Notes Offering, the senior subordinated notes and the guarantees thereof would have ranked: |

| | • | | junior to approximately $1,124.0 million principal amount of senior indebtedness, $304.0 million principal amount of which would have consisted of the senior notes; |

| | • | | effectively subordinated to approximately $820.8 million of secured indebtedness, $820.0 million of which would have consisted of term loan borrowings under our credit facility; and |

| | • | | effectively subordinated to approximately $90.1 million of liabilities, including trade payables, of our non-guarantor subsidiaries. |

| | After giving pro forma effect to the Refinancing and Additional Senior Notes Offering, our subsidiaries that are not guarantors of the senior subordinated notes would have accounted for approximately $33.2 million, or 13.5%, of our net revenues for the three months ended March 31, 2006 and would have held approximately $187.8 million, or 8.9%, of our total assets as of March 31, 2006. |

Optional Redemption:

Senior Notes | We may redeem some or all of the senior notes at any time on or after October 15, 2009, at the redemption prices described in this prospectus. In addition, on or before October 15, 2008, we may redeem up to 35% of the aggregate principal amount of the senior |

15

| | notes with the net proceeds of certain equity offerings, provided that at least 65% of the aggregate principal amount of the senior notes initially issued remain outstanding immediately after such redemption. See “Risk Factors.” |

Senior Subordinated Notes | We may redeem some or all of the senior subordinated notes at any time on or after October 15, 2010 at the redemption prices described in this prospectus. In addition, on or before October 15, 2008, we may redeem up to 35% of the aggregate principal amount of the senior subordinated notes with the net proceeds of certain equity offerings, provided that at least 65% of the aggregate principal amount of the senior subordinated notes initially issued remain outstanding immediately after such redemption. See “Risk Factors.” |

Change of Control | If we experience a change of control (as defined in the indentures governing the notes) and fail to meet certain conditions, we will be required to make an offer to repurchase the notes at a price equal to 101% of the principal amount thereof, plus accrued and unpaid interest, if any, to the date of purchase. We will comply, to the extent applicable, with the requirements of Section 14(e) of the Exchange Act and any other securities laws or regulations in connection with the repurchase of notes in the event of a change of control. See “Risk Factors.” |

Restrictive Covenants | The indentures governing the exchange notes contain certain covenants that, among other things, limit our ability and the ability of our restricted subsidiaries to: |

| | • | | borrow money or sell preferred stock; |

| | • | | pay dividends on or redeem or repurchase stock; |

| | • | | make certain types of investments; |

| | • | | sell stock in our restricted subsidiaries; |

| | • | | restrict dividends or other payments from subsidiaries; |

| | • | | enter into transactions with affiliates; |

| | • | | issue guarantees of debt; and |

| | • | | sell assets or merge with other companies. |

| | These limitations are subject to a number of exceptions and qualifications. |

16

SUMMARY HISTORICALAND PRO FORMA CONDENSED CONSOLIDATED AND COMBINED FINANCIAL AND OTHER DATA

The following table presents our summary historical condensed consolidated and combined financial data and summary pro forma condensed consolidated financial data. This information is only a summary and should be read in conjunction with, and is qualified by reference to, the sections entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Unaudited Pro Forma Condensed Consolidated Financial Information” and the audited consolidated and combined financial statements and the notes thereto included elsewhere herein.

The consolidated balance sheet data of Affinion as of December 31, 2005, the combined balance sheet data of the Predecessor as of December 31, 2004 and the related consolidated statements of operations data and cash flows data of Affinion for the period October 17, 2005 to December 31, 2005 and the related combined statements of operations data and cash flows data of the Predecessor for the period from January 1, 2005 to October 16, 2005 and for the years ended December 31, 2004 and 2003 are derived from the audited consolidated and combined financial statements and the notes thereto included elsewhere herein. The combined balance sheet data as of December 31, 2002 and 2001 have been derived from the unaudited combined balance sheets of the Predecessor, and the combined statements of operations data and cash flows data for the year ended December 31, 2002 have been derived from the 2002 audited combined financial statements of the Predecessor, none of which are included herein. The table below does not include summary combined statement of operations data for the year ended December 31, 2001. See “Selected Historical Consolidated and Combined Financial and Other Data.”

The consolidated balance sheet data of Affinion as of March 31, 2006, the related consolidated statements of operations data and cash flows data of Affinion for the three months ended March 31, 2006 and the related combined statements of operations data and cash flows data of the Predecessor for the three months ended March 31, 2005 are derived from the unaudited condensed consolidated and combined financial statements and notes thereto included elsewhere herein. These unaudited condensed consolidated and combined financial statements have been prepared on the same basis as the audited consolidated and combined financial statements and, in the opinion of our management, include all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of the information set forth herein. Interim financial results are not necessarily indicative of results that may be expected for the full fiscal year or any future reporting period.

The unaudited pro forma condensed consolidated statement of operations data for the year ended December 31, 2005 gives effect, in the manner described under “Unaudited Pro Forma Condensed Consolidated Financial Information” and the notes thereto, to the Transactions, the Refinancing and the Additional Senior Notes Offering as if these events occurred on January 1, 2005. The unaudited pro forma condensed consolidated statement of operations data for the three months ended March 31, 2006 gives effect, in the manner described under “Unaudited Pro Forma Condensed Consolidated Financial Information” and the notes thereto, to the Refinancing and the Additional Senior Notes Offering as if these events occurred on January 1, 2005. The unaudited pro forma condensed consolidated balance sheet data as of December 31, 2005 and as of March 31, 2006 give effect to the Refinancing and the Additional Senior Notes Offering in the manner described under “Unaudited Pro Forma Condensed Consolidated Financial Information” and the notes thereto, as if it had occurred as of December 31, 2005 and as of March 31, 2006, respectively.

For purposes of this prospectus, we have described our segment performance measure as “Segment EBITDA.” Segment EBITDA consists of income/(loss) from operations before depreciation and amortization.

The summary unaudited pro forma condensed consolidated financial data is for information purposes only and is not intended to represent or be indicative of the consolidated results of operations that we would have reported had the Transactions, the Refinancing and the Additional Senior Notes Offering been completed as of the dates and for the period presented, and should not be taken as representative of our consolidated results of operations or financial condition following the completion of the Transactions, the Refinancing and the Additional Senior Notes Offering.

17

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | The Predecessor | | | The Company | | | The Predecessor | | | The Company | |

| | | Years Ended December 31, | | | For the

Period

January 1,

2005

to October 16,

2005 | | | For the

Period

October 17,

2005

to December 31,

2005(1) | | | Pro Forma for the

Transactions,

the Refinancing and

the Additional Senior

Notes Offering for

the Year Ended

December 31,

2005(1) | | | For the

Three Months

Ended

March 31,

2005 | | | For the

Three Months

Ended

March, 31

2006 | | | Pro Forma for

the Refinancing

and Additional

Senior Notes

Offering for

the Three

Months Ended

March 31, 2006 | |

| | | 2001 | | | 2002 | | | 2003 | | | 2004 | | | | | | | |

| | | (in millions) | | | | | | | | | | |

Condensed Consolidated and Combined Statements of Operations Data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net revenues | | | | | | $ | 1,458.4 | | | $ | 1,443.7 | | | $ | 1,530.9 | | | $ | 1,063.8 | | | $ | 134.9 | | | $ | 1,198.7 | | | $ | 337.5 | | | $ | 245.9 | | | $ | 245.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Marketing and commissions(2) | | | | | | | 698.6 | | | | 683.7 | | | | 665.3 | | | | 515.0 | | | | 87.1 | | | | 588.3 | | | | 168.1 | | | | 134.1 | | | | 134.1 | |

Operating costs | | | | | | | 409.6 | | | | 379.5 | | | | 383.3 | | | | 315.0 | | | | 48.7 | | | | 363.7 | | | | 106.4 | | | | 75.3 | | | | 75.3 | |

General and administrative | | | | | | | 112.5 | | | | 115.7 | | | | 185.0 | | | | 134.5 | | | | 20.2 | | | | 129.6 | | | | 32.1 | | | | 29.0 | | | | 29.0 | |

Gain on sale of assets | | | | | | | — | | | | — | | | | (23.9 | ) | | | (4.7 | ) | | | — | | | | (4.7 | ) | | | (0.6 | ) | | | — | | | | — | |

Depreciation and amortization | | | | | | | 45.3 | | | | 44.5 | | | | 43.9 | | | | 32.3 | | | | 84.5 | | | | 407.4 | | | | 10.4 | | | | 101.7 | | | | 101.7 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total expenses | | | | | | | 1,266.0 | | | | 1,223.4 | | | | 1,253.6 | | | | 992.1 | | | | 240.5 | | | | 1,484.3 | | | | 316.4 | | | | 340.1 | | | | 340.1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income/(loss) from operations | | | | | | | 192.4 | | | | 220.3 | | | | 277.3 | | | | 71.7 | | | | (105.6 | ) | | | (285.6 | ) | | | 21.1 | | | | (94.2 | ) | | | (94.2 | ) |

Interest income | | | | | | | 3.2 | | | | 2.0 | | | | 1.7 | | | | 1.9 | | | | 1.3 | | | | 3.2 | | | | 0.5 | | | | 1.2 | | | | 1.2 | |

Interest expense | | | | | | | (15.5 | ) | | | (14.1 | ) | | | (7.3 | ) | | | (0.5 | ) | | | (31.9 | ) | | | (153.1 | ) | | | (0.3 | ) | | | (34.1 | ) | | | (35.0 | ) |

Other income/(expense), net | | | | | | | (14.0 | ) | | | 6.7 | | | | 0.1 | | | | 5.9 | | | | — | | | | 5.9 | | | | (0.1 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income/(loss) before income taxes and minority interests | | | | | | | 166.1 | | | | 214.9 | | | | 271.8 | | | | 79.0 | | | | (136.2 | ) | | | (429.6 | ) | | | 21.2 | | | | (127.1 | ) | | | (128.0 | ) |

Provision for (benefit from) income taxes | | | | | | | 116.6 | | | | 71.3 | | | | (104.5 | ) | | | 28.9 | | | | — | | | | 4.1 | | | | 8.0 | | | | (0.9 | ) | | | (0.9 | ) |

Minority interests, net of tax | | | | | | | — | | | | (0.7 | ) | | | (0.1 | ) | | | — | | | | 0.1 | | | | 0.1 | | | | 0.1 | | | | 0.1 | | | | 0.1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income/(loss) before cumulative effect of accounting change | | | | | | | 49.5 | | | | 144.3 | | | | 376.4 | | | | 50.1 | | | | (136.3 | ) | | | (433.8 | ) | | | — | | | | — | | | | — | |

Cumulative effect of accounting change, net of tax | | | | | | | (143.7 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income/(loss) | | | | | | $ | (94.2 | ) | | $ | 144.3 | | | $ | 376.4 | | | $ | 50.1 | | | $ | (136.3 | ) | | $ | (433.8 | ) | | $ | 13.1 | | | $ | (126.3 | ) | | $ | (127.2 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Consolidated and Combined Balance Sheet Data (at period end): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents (excludes restricted cash) | | $ | 97.4 | | | $ | 86.2 | | | $ | 63.2 | | | $ | 22.5 | | | | — | | | $ | 113.4 | | | $ | 97.4 | | | $ | 37.4 | | | $ | 84.7 | | | $ | 68.9 | |

Working capital deficit | | | (397.3 | ) | | | (450.3 | ) | | | (463.9 | ) | | | (322.4 | ) | | | — | | | | (92.7 | ) | | | (99.8 | ) | | | (283.8 | ) | | | (135.0 | ) | | | (142.1 | ) |

Total assets | | | 1,334.2 | | | | 1,335.0 | | | | 1,246.6 | | | | 1,158.5 | | | | — | | | | 2,200.0 | | | | 2,182.8 | | | | 1,167.5 | | | | 2,114,4 | | | | 2,100.7 | |

Total debt | | | 126.7 | | | | 140.4 | | | | 131.2 | | | | 31.6 | | | | — | | | | 1,491.0 | | | | 1,493.1 | | | | 11.4 | | | | 1,471.0 | | | | 1,473.1 | |

Stockholder’s/combined equity | | | 93.4 | | | | 123.7 | | | | 115.6 | | | | 293.6 | | | | — | | | | 233.9 | | | | 223.5 | | | | 349.3 | | | | 109.6 | | | | 102.5 | |

Consolidated and Combined Cash Flows Data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net cash provided by (used in): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating activities(3) | | | | | | $ | 32.6 | | | $ | 145.5 | | | $ | 261.1 | | | $ | 106.5 | | | $ | 31.1 | | | | — | | | $ | (20.9 | ) | | $ | (6.7 | ) | | | — | |

Investing activities(3) | | | | | | | (38.2 | ) | | | (5.6 | ) | | | (2.3 | ) | | | (39.5 | ) | | | (1,640.1 | ) | | | — | | | | (5.6 | ) | | | (2.3 | ) | | | — | |

Financing activities | | | | | | | (10.4 | ) | | | (165.6 | ) | | | (301.5 | ) | | | (23.4 | ) | | | 1,722.9 | | | | — | | | | 42.2 | | | | (20.1 | ) | | | — | |

Other Financial Data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Segment EBITDA(4) | | | | | | $ | 237.7 | | | $ | 264.8 | | | $ | 321.2 | | | | — | | | | — | | | $ | 121.8 | | | | — | | | | — | | | | — | |

Capital expenditures | | | | | | | 42.5 | | | | 20.8 | | | | 25.8 | | | $ | 24.0 | | | $ | 9.0 | | | | 33.0 | | | $ | 5.6 | | | $ | 4.4 | | | $ | 4.4 | |

Ratio of earnings to fixed charges(5) | | | | | | | 8.5x | | | | 11.4x | | | | 19.8x | | | | 15.9x | | | | — | | | | — | | | | | | | | — | | | | — | |

18

| (1) | The amounts shown reflect, among other things, the purchase accounting adjustments made in the Transactions. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Overview of 2005 Historical Operating Results.” |

| (2) | As discussed in Note 2 to the consolidated and combined financial statements included elsewhere herein, the Predecessor previously deferred costs which varied with and were directly related to acquiring new insurance business on its combined balance sheets as deferred acquisition costs to the extent such costs were deemed recoverable from future cash flows. These costs were amortized as marketing expense over a 12-year period using a declining balance method generally in proportion to the related insurance revenue, which amortization was based on attrition rates associated with the approximate rate that insurance revenues collected from customers decline over time. Amortization of deferred acquisition costs commenced upon recognition of the related insurance revenue. Immediately following the Transactions, we began expensing such costs as they are incurred. The acquisition costs incurred and capitalized by the Predecessor totaled approximately $57.2 million, $62.1 million and $58.9 million for the years ended December 31, 2002, 2003 and 2004, respectively, and $37.1 million for the period from January 1, 2005 to October 17, 2005. The Predecessor’s amortization expense of deferred acquisition costs was $31.0 million, $29.1 million and $43.7 million for the years ended December 31, 2002, 2003 and 2004, respectively, and $42.0 million for the period from January 1, 2005 to October 17, 2005. We incurred and expensed acquisition costs that totaled $12.6 million for the period from October 17, 2005 to December 31, 2005. |

| (3) | Certain restricted cash amounts have been reclassified from investing activities to operating activities. See Note 2 to our audited consolidated and combined financial statements and Note 1 to our unaudited condensed consolidated and combined financial statements included elsewhere herein. |

| (4) | Segment EBITDA consists of income from operations before depreciation and amortization. Segment EBITDA is the measure management uses to evaluate segment performance and we present Segment EBITDA to enhance your understanding of our operating performance. We use Segment EBITDA as one criterion for evaluating our performance relative to that of our peers. We believe that Segment EBITDA is an operating performance measure, and not a liquidity measure, that provides investors and analysts with a measure of operating results unaffected by differences in capital structures, capital investment cycles and ages of related assets among otherwise comparable companies. However, Segment EBITDA is not a measurement of financial performance under U.S. GAAP, and our Segment EBITDA may not be comparable to similarly titled measures of other companies. You should not consider our Segment EBITDA as an alternative to operating or net income determined in accordance with U.S. GAAP, as an indicator of our operating performance or as an alternative to cash flows from operating activities determined in accordance with U.S. GAAP, or as an indicator of cash flows, or as a measure of liquidity. For a reconciliation of net income/(loss) to Segment EBITDA, see the table included below. Adjusted EBITDA is defined as Segment EBITDA further adjusted to exclude non-cash and unusual items and other adjustments permitted in the indenture governing the notes to test the permissibility of certain types of transactions, including debt incurrence. We believe that the inclusion of the adjustments to Segment EBITDA applied in presenting Adjusted EBITDA are appropriate to provide additional information to investors about certain non-cash items and unusual items. However, Adjusted EBITDA is not a measurement of financial performance under U.S. GAAP, and our Adjusted EBITDA may not be comparable to similarly titled measures of other companies. You should not consider our Adjusted EBITDA as an alternative to operating or net income determined in accordance with U.S. GAAP, as an indicator of our operating performance or as an alternative to cash flows from operating activities determined in accordance with U.S. GAAP, or as an indicator of cash flows, or as a measure of liquidity. |

Set forth below is a reconciliation of net income/(loss) to Segment EBITDA and Adjusted EBITDA.

| | | | | | | | | | | | | | | | |

| | | The Predecessor | | | Pro

Forma(a) Year Ended

December 31, 2005 | |

| | | Years Ended

December 31, | | |

| | | 2002 | | | 2003 | | | 2004 | | |

| | | (in millions) | | | | |

Net income/(loss) | | $ | (94.2 | ) | | $ | 144.3 | | | $ | 376.4 | | | $ | (433.8 | ) |

Interest (income)/expense, net | | | 12.3 | | | | 12.1 | | | | 5.6 | | | | 149.9 | |

Provision for/(benefit from) income taxes | | | 116.6 | | | | 71.3 | | | | (104.5 | ) | | | 4.1 | |

Minority interests, net of tax | | | — | | | | (0.7 | ) | | | (0.1 | ) | | | 0.1 | |

Other (income)/expense, net | | | 14.0 | | | | (6.7 | ) | | | (0.1 | ) | | | (5.9 | ) |