Exhibit 99.1

| Raymond James 29th Annual Institutional Investor Conference March 2008 |

| 1 Notice on Forward Looking Statements This presentation as well as oral statements made by officers or directors of Allegiant Travel Company, its advisors and affiliates (collectively or separately, the "Company") will contain forward-looking statements that are only predictions and involve risks and uncertainties. Forward-looking statements may include, among others, references to future performance and any comments about our strategic plans. There are many risk factors that could prevent us from achieving our goals and cause the underlying assumptions of these forwardlooking statements, and our actual results, to differ materially from those expressed in, or implied by, our forward-looking statements. These risk factors and others are more fully discussed in our filings with the Securities and Exchange Commission. Any forward-looking statements are based on information available to us today and we undertake no obligation to update publicly any forward-looking statements, whether as a result of future events, new information or otherwise. The Company cautions users of this presentation not to place undue reliance on forward looking statements, which may be based on assumptions and anticipated events that do not materialize. |

| Andrew Levy CFO & MD Planning |

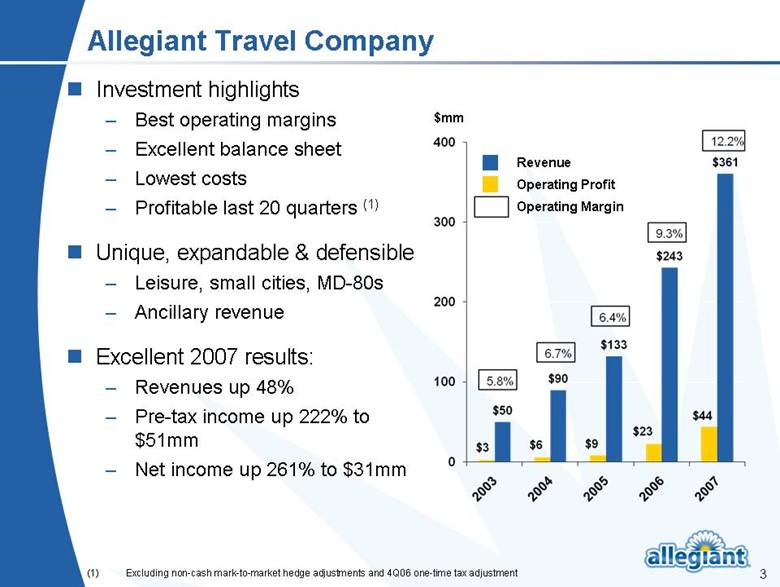

| 3 Allegiant Travel Company $mm Investment highlights – Best operating margins – Excellent balance sheet – Lowest costs – Profitable last 20 quarters (1) Unique, expandable & defensible – Leisure, small cities, MD-80s – Ancillary revenue Excellent 2007 results: – Revenues up 48% – Pre-tax income up 222% to $51mm – Net income up 261% to $31mm Revenue Operating Profit Operating Margin (1) Excluding non-cash mark-to-market hedge adjustments and 4Q06 one-time tax adjustment $mm 400 300 200 100 0 2003 2004 2005 2006 2007 $3 $50 $6 $90 $9 $133 $23 $243 $44 $361 5.8% 6.7% 6.4% 9.3% 12.2% |

| Ponder Harrison MD Sales and Marketing |

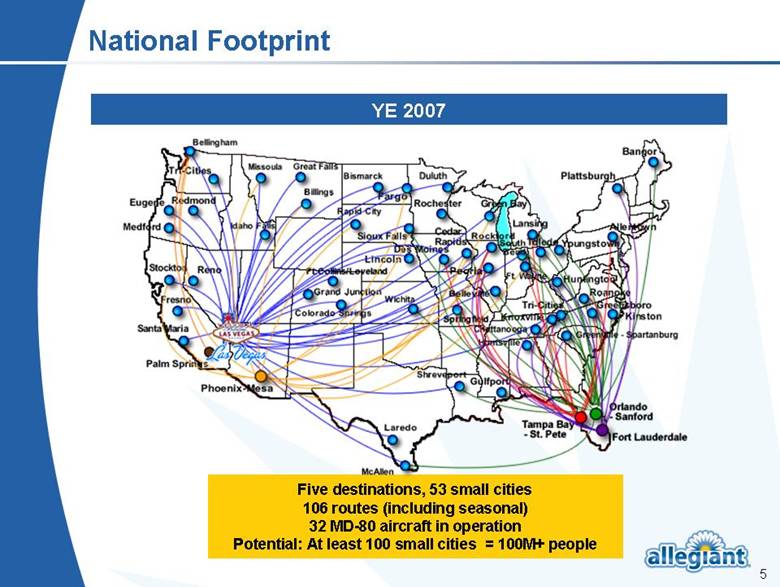

| 5 National Footprint YE 2007 Five destinations, 53 small cities 106 routes (including seasonal) 32 MD-80 aircraft in operation Potential: At least 100 small cities = 100M+ people |

| 6 Minimal Direct Competition Delta: – Knoxville – Greenville/ Spartanburg – Greensboro – Huntsville US Airways: – Colorado Springs – Medford – Eugene US Airways/United: – Fresno Head-to-Head Competition on Only Eight of 106 Routes • Competition pre-existed on all eight routes • To date, it is rare for other carriers to react to our entry • Competitors appear to view us as an irritant, not a threat |

| 7 Industry-Leading Ancillary Revenue/Passenger Since 2002, Ancillary/Passenger has Grown at over 80% CAGR $25 $20 $15 $10 $5 $0 2002 2003 2004 2005 2006 4Q06 2007 4Q07 $1.06 $3.40 $5.87 $11.55 $16.11 $18.84 $21.53 $24.30 |

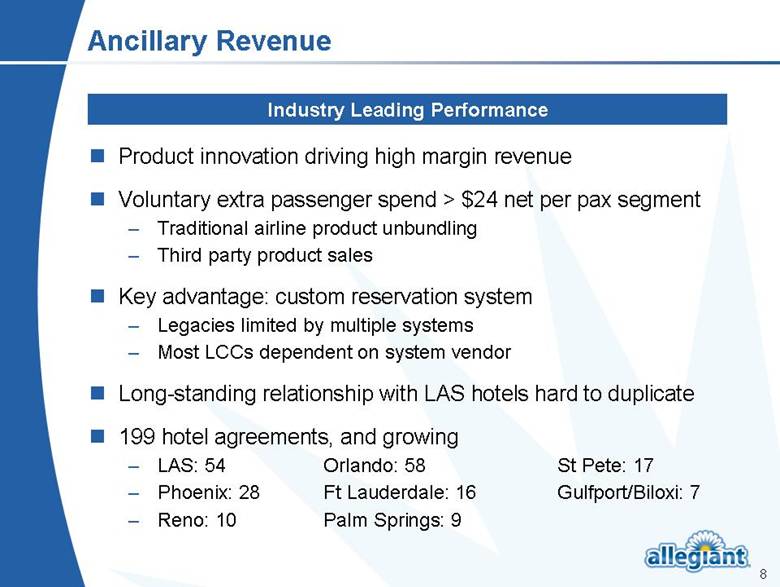

| 8 Ancillary Revenue Product innovation driving high margin revenue Voluntary extra passenger spend > $24 net per pax segment – Traditional airline product unbundling – Third party product sales Key advantage: custom reservation system – Legacies limited by multiple systems – Most LCCs dependent on system vendor Long-standing relationship with LAS hotels hard to duplicate 199 hotel agreements, and growing – LAS: 54 Orlando: 58 St Pete: 17 – Phoenix: 28 Ft Lauderdale: 16 Gulfport/Biloxi: 7 – Reno: 10 Palm Springs: 9 Industry Leading Performance |

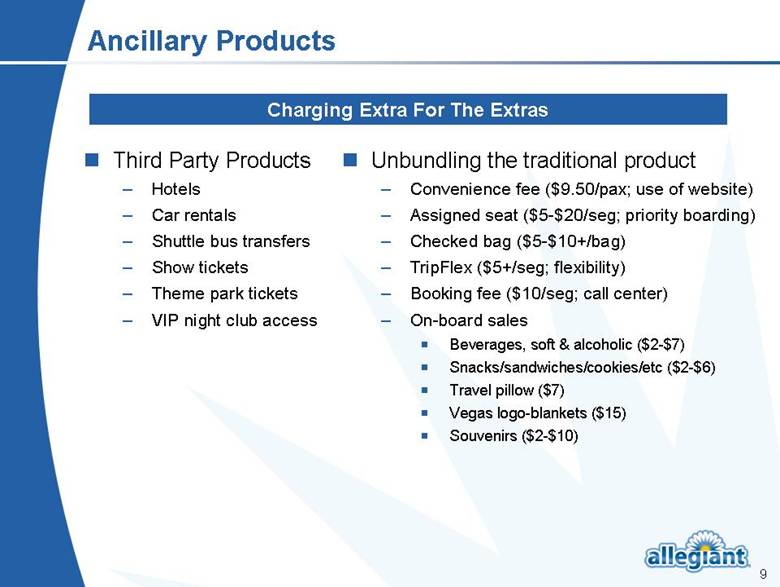

| 9 Ancillary Products Third Party Products – Hotels – Car rentals – Shuttle bus transfers – Show tickets – Theme park tickets – VIP night club access Unbundling the traditional product – Convenience fee ($9.50/pax; use of website) – Assigned seat ($5-$20/seg; priority boarding) – Checked bag ($5-$10+/bag) – TripFlex ($5+/seg; flexibility) – Booking fee ($10/seg; call center) – On-board sales Beverages, soft & alcoholic ($2-$7) Snacks/sandwiches/cookies/etc ($2-$6) Travel pillow ($7) Vegas logo-blankets ($15) Souvenirs ($2-$10) Charging Extra For The Extras |

| 10 Control the Customer www.allegiantair.com – Leverage direct relationship with customers – Maximize e-commerce opportunities – 4Q07 unique visitors 2.6mm, up 62% year-over-year – Instantly relevant to leisure customers in our small cities – Accounts for almost 90% of sales – Generates email lists for future low-cost communication – Significant untapped potential to sell non-Allegiant travel products Advertising – Nonstop service to LAS/FL/AZA a big deal – free media – Small city media markets inexpensive – Email advertising (see above) even cheaper – Word-of-mouth – significant & lowest-cost form of advertising Big Fish in Small, Underserved Ponds |

| Andrew Levy CFO & MD Planning |

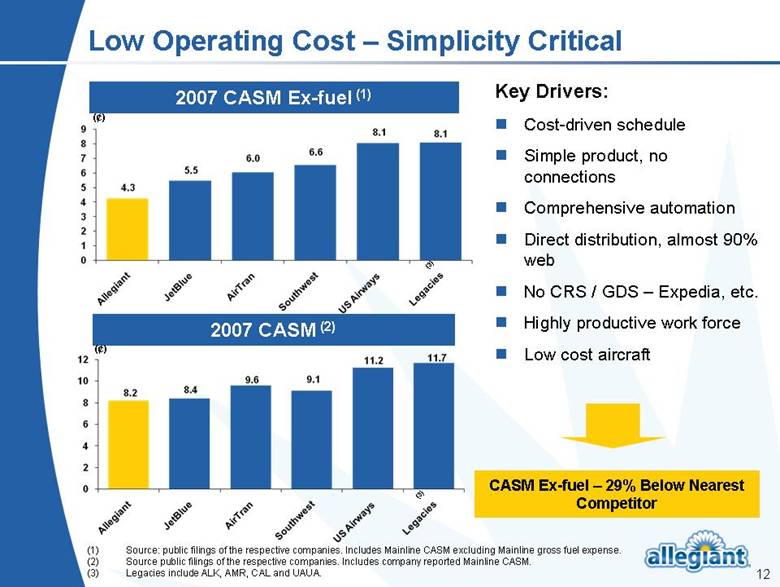

| 12 Low Operating Cost – Simplicity Critical Key Drivers: Cost-driven schedule Simple product, no connections Comprehensive automation Direct distribution, almost 90% web No CRS / GDS – Expedia, etc. Highly productive work force Low cost aircraft 2007 CASM Ex-fuel (1) 2007 CASM (2) Source: public filings of the respective companies. Includes Mainline CASM excluding Mainline gross fuel expense. (2) Source public f ilings of the respectiv e companies. Includes company reported Mainline CASM. (3) Legacies include ALK, AMR, CAL and UAUA. (¢) (¢) CASM Ex-fuel – 29% Below Nearest Competitor 9 8 7 6 5 4 3 2 1 0 4.3 5.5 6.0 6.6 8.1 8.1 Allegiant JetBlue AirTran Southwest US Airways Legacies 12 10 8 6 4 2 0 8.2 8.4 9.6 9.1 11.2 11.7 Allegiant JetBlue AirTran Southwest US Airways |

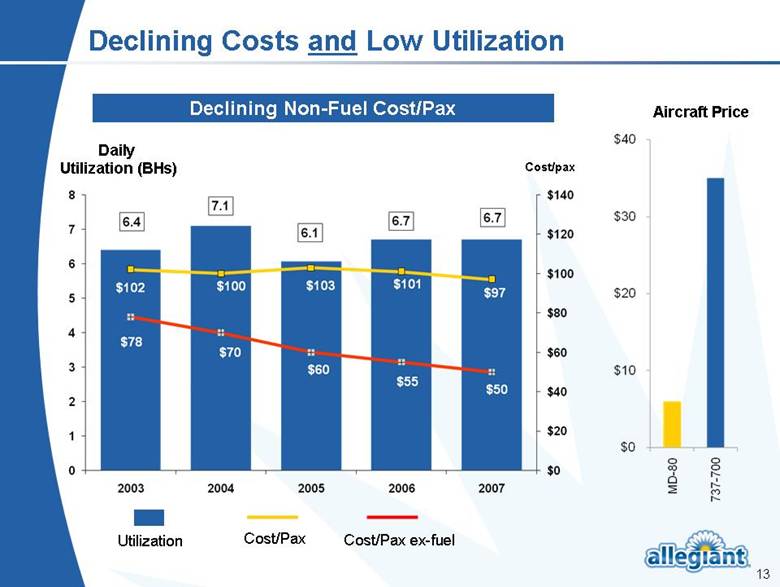

| 13 Declining Costs and Low Utilization Daily Utilization (BHs) Cost/pax Declining Non-Fuel Cost/Pax Aircraft Price Utilization Cost/Pax Cost/Pax ex-fuel 8 7 6 5 4 3 2 1 0 2003 2004 2005 2006 2007 6.4 7.1 6.1 6.7 6.7 $0 $20 $40 $60 $80 $100 $120 $140 $40 $30 $20 $10 $0 MD-80 737-700 Cost/pax |

| 14 Best Operating Margins 2007 Operating Margins 2007 Pre-Tax Margins Source: public filings of the respective companies. Southwest Hedge (7.4pp) Southwest Hedge (7.0pp) 16% 14% 12% 10% 8% 6% 4% 2% 0% (2%) (4%) Allegiant Southwest Alaska AirTran JetBlue US Airways Frontier 12.2% 8.0% 6.0% 6.0% 5.9% 4.6% -0.5% 16% 14% 12% 10% 8% 6% 4% 2% 0% (2%) (4%) Allegiant Southwest Alaska AirTran JetBlue US Airways Frontier 14.1% 10.7% 5.8% 3.8% 3.7% 1.4% -2.2% |

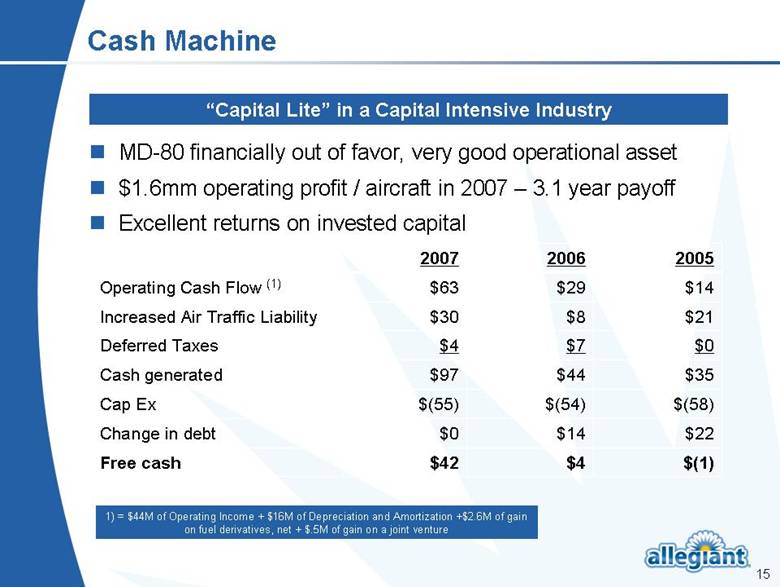

| 15 Cash Machine MD-80 financially out of favor, very good operational asset $1.6mm operating profit / aircraft in 2007 – 3.1 year payoff Excellent returns on invested capital “Capital Lite” in a Capital Intensive Industry 2007 2006 2005 Operating Cash Flow (1) $63 $29 $14 Increased Air Traffic Liability $30 $8 $21 Deferred Taxes $4 $7 $0 Cash generated $97 $44 $35 Cap Ex $(55) $(54) $(58) Change in debt $0 $14 $22 Free cash $42 $4 $(1) 1) = $44M of Operating Income + $16M of Depreciation and Amortization +$2.6M of gain on fuel derivatives, net + $.5M of gain on a joint venture |

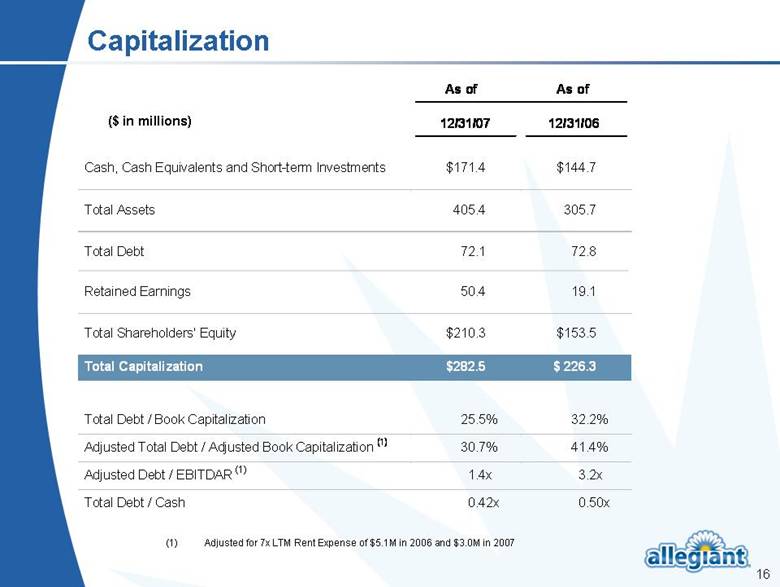

| 16 Capitalization (1) Adjusted for 7x LTM Rent Expense of $5.1M in 2006 and $3.0M in 2007 As of As of 12/31/07 12/31/06 Cash, Cash Equivalents and Short-term Investments $171.4 $144.7 Total Assets 405.4 305.7 Total Debt Retained Earnings 72.1 50.4 72.8 19.1 Total Shareholders’ Equity $210.3 $153.5 Total Capitalization $282.5 $ 226.3 Total Debt / Book Capitalization 25.5% 32.2% Adjusted Total Debt / Adjusted Book Capitalization (1) 30.7% 41.4% Adjusted Debt / EBITDAR (1) 1.4x 3.2x Total Debt / Cash 0.42x 0.50x ($ in millions) |

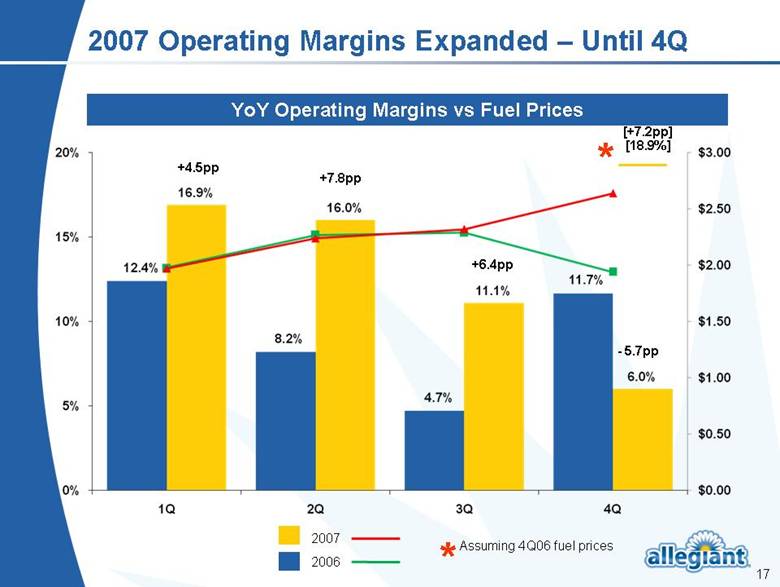

| 17 2007 Operating Margins Expanded – Until 4Q YoY Operating Margins vs Fuel Prices 2007 2006 +4.5pp +7.8pp +6.4pp - 5.7pp [18.9%] [+7.2pp] *Assuming 4Q06 fuel prices 20% 15% 10% 5% 0% 1Q 2Q 3Q 4Q 12.4% 16.9% 8.2% 16.0% 4.7% 11.1% 11.7% 6.0% $3.00 $2.50 $1.50 $1.00 $0.50 $0.00 |

| 18 Current Environment – Good News Traffic 1QTD very good – Jan: Pax up 59%, ASMs up 47%, Depts up 46%, LF 82.4%, +4.5 pts – Feb: Pax up 59%, ASMs up 45%, Depts up 47%, LF 86.4%, +5.5 pts 1Q & 2Q historically strongest quarters 1Q07 LAS adversely impacted by 2007 NBA All-Star Game LAS hotels facing slow down offering us lower prices and more rooms Recent customer survey - average income >$90K Good advance bookings |

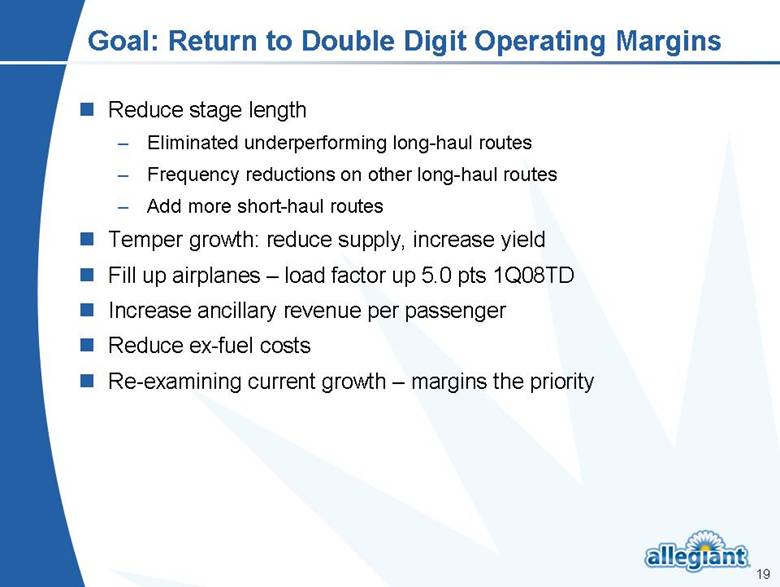

| 19 Goal: Return to Double Digit Operating Margins Reduce stage length – Eliminated underperforming long-haul routes – Frequency reductions on other long-haul routes – Add more short-haul routes Temper growth: reduce supply, increase yield Fill up airplanes – load factor up 5.0 pts 1Q08TD Increase ancillary revenue per passenger Reduce ex-fuel costs Re-examining current growth – margins the priority |