UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22435

Kayne Anderson Energy Development Company

(Exact name of registrant as specified in charter)

| | |

| 811 Main Street, 14th Floor, Houston, Texas | | 77002 |

| (Address of principal executive offices) | | (Zip code) |

David Shladovsky, Esq.

KA Fund Advisors, LLC, 811 Main Street, 14th Floor, Houston, Texas 77002

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 493-2020

Date of fiscal year end: November 30, 2013

Date of reporting period: November 30, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The report of Kayne Anderson Energy Development Company (the “Registrant”) to stockholders for the fiscal year ended November 30, 2013 is attached below.

Energy Development Company

KED Annual Report

November 30, 2013

CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This report of Kayne Anderson Energy Development Company (the “Company”) contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Company’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; master limited partnership (“MLP”) industry risk; leverage risk; valuation risk; interest rate risk; tax risk; and other risks discussed in the Company’s filings with the Securities and Exchange Commission (“SEC”). You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Company undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Company’s investment objectives will be attained.

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

January 24, 2014

Dear Fellow Stockholders:

We are pleased to report that the year ended November 30, 2013 was an extremely successful year for the Company. We generated very strong total returns for our stockholders, substantially increased our distribution and reached some important milestones with our portfolio during the year. Further, the Company is well positioned to make new investments and continue to generate attractive returns for its investors.

Fueled by a strengthening domestic economy, calendar 2013 will be remembered for the outstanding performance of the broader equity markets. The S&P 500 Index set many new all-time highs during 2013 and generated a total return of over 32% — its strongest gain since 1995. While the MLP market, as measured by the Alerian MLP index, did not quite keep pace, it generated a total return of 28% during calendar 2013, which is outstanding when considering the fact that this performance was accomplished in a rising interest rate environment. Most importantly, we believe the outlook for MLPs remains solid and the sector is poised to generate low double digit returns for several years to come. As of November 30, 2013, over 90% of the Company’s portfolio was invested in public MLPs.

Our portfolio underwent a major transition during fiscal 2013. At the start of fiscal 2013, our private investments consisted of holdings in Direct Fuels Partners, L.P. (“Direct Fuels”), Plains All American GP LLC (“PAA GP”), VantaCore Partners LP (“VantaCore”) and ProPetro Services, Inc. At the time, these private investments represented approximately 30% of our long-term investments. In May, we successfully completed the merger of Direct Fuels into Emerge Energy Services LP (“Emerge”) and the concurrent initial public offering of Emerge. As of December 31, 2013, Emerge’s unit price had increased by 161% over its IPO price, making it the best performing MLP initial public offering in calendar 2013. In October, our investment in PAA GP became publicly traded through the initial public offering of Plains GP Holdings, L.P. (our ownership of PAA GP is exchangeable into shares of Plains GP Holdings). Based on current trading levels for Plains GP Holdings ($25.19 per share as of January 24, 2014), our investment in PAA GP has increased four-fold since our initial investment in December 2010.

As these two investments have become “public MLPs,” we continue to look to put additional capital to work in private MLPs. In today’s energy market, however, we are finding it more challenging to invest in private MLPs that provide appropriate rates of return. Competition from private equity firms, a receptive market for MLP initial public offerings, as well as the willingness of public MLPs to purchase smaller private midstream businesses are trends that have impacted our ability to form new private MLPs. Market conditions will undoubtedly change over time, and we will continue to search for suitable private investments that meet our return expectations. In the interim, we will continue to deploy capital in public MLPs that offer attractive returns. In making these investments, selectivity will be the key to achieving high rates of return for KED. As a result, we are likely to take more concentrated positions in public MLPs.

As we have discussed in previous annual letters, the “Shale Revolution” (the development of domestic unconventional resources) continues to be the biggest story in the energy industry. As we predicted two years ago, it has become increasingly clear that the Shale Revolution will have an extremely meaningful impact on the broader domestic economy. Judging by the large number of news articles published in 2013 on the shale plays, hydraulic fracturing and the impact of surging domestic energy production, it is safe to say that most people are aware of the impact unconventional resources are having on all of our day-to-day lives. Job growth related to the energy industry, as well as from increased domestic manufacturing activity, continues to be a boon for the U.S. economy. This impact will continue for many years to come. Plentiful domestic energy supplies and low relative energy prices have led to a resurgence in U.S. manufacturing and positioned the U.S. to become one of the largest exporters of energy products in the world.

1

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

The Shale Revolution creates both challenges and opportunities for energy companies. As a result of production increases, significant amounts of new midstream assets must be built to facilitate transportation of this new production to end-users. We believe this creates a tremendous opportunity for MLPs. Conversely, increased production can put pressure on absolute commodity prices — as witnessed by low natural gas and natural gas liquids prices in 2012 and 2013. It can also create very large pricing differences between geographic areas, which can result in producers receiving substantial discounts to “market” prices for their production. Further, production in new areas of the country is altering historical transportation routes and, as a result, materially impacting operating results (both positively and negatively) for certain midstream assets. Whether by pipeline or by rail, the transportation of energy products always involves risks, and it is important to understand which management teams are capable of managing these risks. We believe that our team of experienced investment professionals is well positioned to continue to navigate the ever-changing market conditions, as well as identify and capitalize on opportunities as they develop.

2013 Performance

We are very proud of the Company’s performance during fiscal 2013. One of the measures we employ to evaluate our performance is Net Asset Value Return, which is equal to the change in net asset value per share plus the cash distributions paid during the period, assuming reinvestment through our dividend reinvestment program. For fiscal 2013, the Company delivered a Net Asset Value Return of 35.1%, which was best among all closed-end fund peers. During the same period, the total return of the Alerian MLP index was 21.6%, a return which KED outperformed by a remarkable 13.5%. Given our structure as a taxable entity, we are very pleased to have outperformed the Alerian MLP index by such a wide margin. As a reminder, the Alerian MLP index is a non-investable index that does not factor in expenses or corporate taxes.

In addition to the Company’s strong adjusted NAV returns, it increased its quarterly distribution by 16.3% during the year, and has increased its distribution by 20 cents per share over the last three years (a 67% increase). We are very proud of this distribution growth and believe the Company’s portfolio is well positioned to provide additional distribution growth to our shareholders.

Another metric by which we measure the Company’s performance is Market Return, which is equal to the change in share price plus the cash distributions paid during the period, assuming reinvestment through our dividend reinvestment program. Our Market Return was 18.1% for fiscal 2013. This measure was below our Net Asset Value Return, as our share price was trading at a 9.6% premium to NAV at the start of fiscal 2013, but ended the year at a 4.2% discount to NAV.

MLP Market Overview

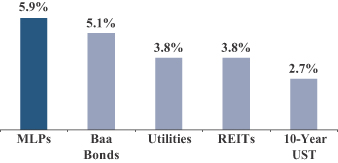

As a result of the transition of our portfolio, public MLPs have become increasingly important and now represent over 90% of our long-term investments as of November 30, 2013. MLPs performed very well during the fiscal year, generating a 21.6% total return. Notably, MLPs delivered this strong performance despite the headwind of rising interest rates. At the beginning of fiscal 2013, the yield on 10-year U.S. Treasury Bonds was 1.61%. By November 30, 2013, the yield on these bonds was 2.74%, an increase of 113 basis points. This rise in rates resulted primarily from the anticipated reduction in the Federal Reserve’s quantitative easing, which was a topic of constant speculation throughout much of the year. Over this same time period, the average MLP yield declined from 6.34% to 5.90%, resulting in the MLP “spread to Treasuries” contracting from 473 basis point to 316 basis points. The spread to Treasuries was abnormally wide at the start of 2013, and we believe market participants were building in a cushion based on the expectation of rising interest rates. In spite of the tightening of the spread to Treasuries, we continue to believe MLP yields are attractive, particularly relative to other income-oriented investments. As illustrated in Figure 1 below, MLP yields are significantly higher than yields for investment grade (Baa) bonds, utilities and REITs.

2

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

Figure 1. MLP Yields versus Other Income Alternatives (January 24, 2014)

Current yields are not the whole story, however. As we have highlighted over the years, we believe it is the combination of current yield and distribution growth that has contributed to the strong performance of MLPs and continues to make MLPs a compelling investment opportunity. During 2013, distributions grew 7.1% compared to 7.3% in 2012 and 6.3% in 2011, and we believe that prospects for distribution growth in 2014 are also very strong (we forecast growth in the 7% area). As a result, after taking distribution growth into consideration, MLPs look even more attractive relative to other income alternatives.

A major driver of distribution growth in the MLP sector has been the significant amounts of capital spent to build the midstream infrastructure required to handle growing oil and natural gas production from the development of unconventional reserves. In calendar 2013, we estimate that MLPs spent in excess of $25 billion on organic capital projects to construct and expand this critical energy infrastructure. We expect MLPs to spend in excess of $20 billion on organic growth projects during 2014. Distribution growth was also driven by acquisitions, and 2013 was one of the most active M&A markets we have ever seen. We estimate that MLPs announced over $65 billion in acquisitions during calendar 2013, including a record three MLP-to-MLP mergers, as well as several large joint ventures between MLPs. While it is difficult to predict merger and acquisition activity, we believe the strategic and competitive dynamics that led to the flurry of activity in 2013 could lead to further consolidation in 2014.

Since 2010, there have been 54 IPOs (including a record 21 in 2013), which is amazing considering there are only 114 MLPs currently trading. While the expansion of the sector has certainly been driven by the Shale Revolution, it is also important to note that quite a few of these new entrants are not “traditional” midstream businesses. In particular, the recent vintage of IPOs has seen refining, petrochemical, “frac” sand, wholesale fuel distribution and offshore drilling companies, among others, form MLPs. While we welcome the expansion of the MLP market into other businesses, we believe it is critical to understand the additional risks associated with these new businesses and will only invest in them if we are properly compensated for these additional risks.

We expect the MLP market to continue to expand across the entire energy sector, as more companies view the formation of an MLP to be a strategic imperative. Furthermore, we expect the increasing diversity and complexity of the sector to create wider disparities in valuation and performance among MLPs. As a result, the message that we have been delivering for several years now is truer today than ever — a strong understanding of each MLP’s assets, the domestic and international energy markets and the ability to select individual stocks is critical to outperforming the market. We are confident that our team of over 20 seasoned investment professionals is well suited to take advantage of the sector’s increasing complexity.

3

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

Energy Market Overview

We have been highlighting for several years that the development of unconventional reserves or shale plays is the biggest story in the energy market, and this year is no different. The development of these resources promises to be a multi-decade story. Over the past few years, the focus of activity has shifted from the gas-rich basins such as the Barnett Shale, the Fayetteville Shale and the Haynesville Shale, to more oil-rich and NGL-rich basins such as the Bakken Shale, Eagle Ford Shale, Marcellus Shale and Utica Shale.

As a result of continued development of shale plays, domestic production of crude oil, NGLs and natural gas grew in 2013 for the fifth consecutive year. Domestic crude oil production is expected to increase by over one million barrels per day in 2013 (a 16% increase), and for the second consecutive year, crude oil production has recorded the largest annual production increase in our country’s history. Since its trough in 2008, domestic crude oil production has increased by over 50%. The U.S. is currently the largest producer of natural gas in the world, and many experts are predicting that it will become the largest producer of crude oil in the next five to ten years. Further, as discussed below in more detail, the U.S. is set to become one of the largest exporters of energy products over the next decade.

This rapid increase in production across all commodities is rapidly displacing imports. According to the most recent EIA data, the U.S was supplying over one-half of its own crude needs for the first time in almost 20 years and was a net exporter of petroleum products at the highest recorded level since the EIA has been tracking the data. These exports are driven in large part by refined products (exports of crude oil are, with a few minor exceptions, prohibited by U.S. laws), but there has also been significant growth in the export of natural gas liquids, or NGLs. In particular, Enterprise Products Partners L.P. and Targa Resources Partners LP began operating two newly constructed propane export terminals during 2013. Partly as a result of these projects, propane prices have recovered significantly in 2013, rising 59% from their lows in January. Both of these projects are being expanded and several other MLPs are evaluating NGL export projects of their own. There has also been significant interest among MLPs and other energy companies in exporting natural gas as liquefied natural gas, or LNG. The LNG liquefaction projects are multi-billion dollar capital projects and are expected to be placed in service in the second half of this decade. Once in service, the U.S. will become a top exporter of LNG. These export opportunities will create large scale investment opportunities for MLPs and other energy companies, as well as ensure a closer relationship between domestic energy prices and international prices.

There was no shortage of developments in the crude oil markets. During the year, we saw crude oil “differentials” (which is the spread between crude oil prices at different locations) widen to record levels to due excess supply in certain regions. To combat these differentials, a record amount of crude oil production was transported by rail cars and marine transportation in lieu of pipelines during 2013.

Increased production from new producing areas (such as the Bakken Shale and the Marcellus Shale) continues to have a material impact on historical transportation patterns. While this creates opportunities for many, as new midstream assets need to be built to facilitate product movement, it also creates challenges, as changing transportation patterns can put pressure on certain existing midstream assets that are no longer needed. For instance, oil production from the Bakken Shale, which is located in North Dakota, has increased five-fold in the last five years. The vast majority of that production is not consumed in North Dakota and it must be shipped to refineries elsewhere in the U.S. This has overwhelmed the existing midstream infrastructure in the area and created tremendous opportunities for midstream companies to develop both short-term and long-term transportation solutions. In the Marcellus Shale, natural gas and NGL production has increased to levels well above what the Northeast uses for most of the year. This has put pressure on natural gas prices in the region, as insufficient infrastructure exists to move the natural gas to other markets. Additionally, the increased “local” production reduces the area’s need to source natural gas from its traditional supplier — the gulf coast of Texas and Louisiana — and many of the pipelines from those regions need to be reconfigured in order to maintain their

4

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

current cash flows. We continue to watch these trends very carefully and position the Company’s portfolio accordingly.

Portfolio and Private Investments

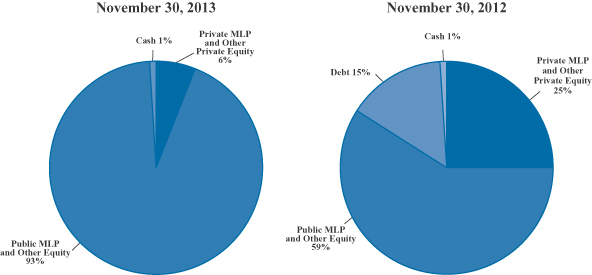

Our portfolio allocations changed materially during fiscal 2013. As of November 30, 2012, private investments, public equities and traded debt securities represented 30%, 59% and 11% of our long-term investments, respectively. As of November 30, 2013, we had 94% of our long-term investments in public equities (91% in public MLPs), 6% in private investments and did not hold any debt securities. Successful transactions at Direct Fuels and PAA GP were the primary drivers of this transition in our portfolio, as well as the sale of our equity interests and refinancing of our debt holdings at ProPetro Services, Inc.

At the start of fiscal 2013, Direct Fuels was our largest private investment (valued at $45 million). In May, Direct Fuels successfully completed a merger with two other private companies to form Emerge Energy Services and the concurrent IPO of Emerge, which trades under the ticker symbol “EMES.” Emerge has a large frac sand business in addition to operating the legacy transmix business of Direct Fuels. Since the IPO, Emerge’s common units have performed extremely well, trading up 168% from the IPO price of $17.00 per unit to $45.50 as of January 24th. We received $48 million in cash from the IPO and subsequent sales of a portion of our Emerge common units, and still retain Emerge common units worth $49 million as of January 24th.

Our investment in PAA GP also contributed to our strong performance this year. In October, Plains GP Holdings, L.P. completed its initial public offering. Plains GP Holdings is a holding company that owns interests in PAA GP, which controls the general partner of Plains All American Pipeline, L.P. Our investment in PAA GP is exchangeable for shares of Plains GP Holdings on a one-for-one basis at our option. The initial public offering of Plains GP Holdings priced at $22.00 per share, and the shares are now trading at $25.19 as of January 24th, an increase of 14.5%. As a result, the value of our investment increased by over two times during fiscal 2013 and is up four-fold since our initial investment in December 2010.

Our only remaining private investment, VantaCore, is an aggregates mining and asphalt company operating in Tennessee, Kentucky, Louisiana and Pennsylvania. VantaCore entered the Pennsylvania market in June of 2012 with the acquisition of Laurel Aggregates, a limestone quarry south of Pittsburgh that primarily supplies aggregates to oil and gas companies drilling in the Marcellus Shale. This acquisition more than doubled the partnership’s EBITDA and further diversified VantaCore from a geographic and market perspective. In VantaCore’s legacy markets, demand for aggregates is closely tied to construction activity in the commercial, residential and infrastructure sectors. Laurel Aggregates, on the other hand, is very focused on energy customers that build infrastructure, including roads and drilling pads, necessary for the development of the Marcellus Shale.

VantaCore performed well in 2013, with Laurel Aggregates delivering better than expected results in its first full year of operations and VantaCore’s legacy operations also performing above budget. Since the financial crisis, and the resulting impact on construction activity, VantaCore’s ability to pay cash distributions has been constrained by limitations in its credit facility. As a result, only a portion of VantaCore’s distributions have been paid in cash, with the remainder paid in additional preferred units. Over the past three years, the cash portion of VantaCore’s distribution has increased from $0.47 per unit in fiscal 2011 to $0.95 in fiscal 2012 and $1.23 in fiscal 2013. As the economy recovers and VantaCore executes on its growth initiatives, we expect the cash portion of the distribution to continue to increase.

2014 Outlook

Our outlook for 2014 is positive. We expect that distribution growth of approximately 7% will lead to another year of low double-digit total returns for the MLP sector. Continued development of unconventional reserves will create plentiful growth opportunities for the sector. While we expect that rising interest rates could

5

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

LETTER TO STOCKHOLDERS

lead to higher yields for MLPs (which would reduce total returns), we believe this will be a temporary headwind. Ultimately, the sector’s attractive yields and prospects for many years of distribution growth will lead to a continuation of strong returns.

Though we have seen fewer opportunities for private MLPs over the last two years, we will continue to look for new private investments during 2014. As always, we intend to be very patient and selective in making these investments to ensure we find opportunities that meet our investment criteria. In the meantime, we will utilize our flexibility to invest in public MLPs and will take concentrated positions when we identify public MLPs with potential for attractive risk-adjusted returns.

We look forward to continuing to execute our business plan of achieving high after-tax total returns by investing in public MLPs, private companies and energy company debt. We invite you to visit our website at kaynefunds.com for the latest updates.

Sincerely,

Kevin S. McCarthy

Chairman of the Board of Directors,

President and Chief Executive Officer

6

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

PORTFOLIO SUMMARY

(UNAUDITED)

Portfolio Investments by Category

Top 10 Holdings by Issuer

| | | | | | | | | | | | | | | | | | | | | | |

| | | Public/ Private | | Equity/

Debt | | Sector | | Percent of Total

Investments(1) as of

November 30, |

| Holding | | | | | 2013 | | 2012 |

1. Emerge Energy Services LP(2) | | Public | | | | Equity | | | Frac Sand | | | | 14.0 | % | | | | 13.3 | % |

2. VantaCore Partners LP | | Private | | | | Equity | | | Aggregates | | | | 6.2 | | | | | 7.5 | |

3. Enterprise Products Partners L.P. | | Public | | | | Equity | | | Midstream | | | | 5.1 | | | | | 5.2 | |

4. Energy Transfer Partners, L.P. | | Public | | | | Equity | | | Midstream | | | | 4.9 | | | | | 1.3 | |

5. Williams Partners L.P. | | Public | | | | Equity | | | Midstream | | | | 4.7 | | | | | 1.1 | |

6. Crestwood Midstream Partners LP | | Public | | | | Equity | | | Midstream | | | | 4.3 | | | | | 1.5 | |

7. Plains GP Holdings, L.P.(3) | | Public | | | | Equity | | | Midstream | | | | 4.2 | | | | | 2.4 | |

8. MarkWest Energy Partners, L.P. | | Public | | | | Equity | | | Midstream | | | | 3.9 | | | | | 2.0 | |

9. Buckeye Partners, L.P. | | Public | | | | Equity | | | Midstream | | | | 3.7 | | | | | 3.0 | |

10. DCP Midstream Partners, LP | | Public | | | | Equity | | | Midstream | | | | 3.6 | | | | | 3.0 | |

| (1) | Includes cash and repurchase agreement (if any). |

| (2) | As of November 30, 2012, our private investment in Direct Fuels Partners, L.P. (“Direct Fuels”) represented 13.3% of total investments. Direct Fuels combined with two other private companies to form Emerge Energy Services LP on May 14, 2013. |

| (3) | We hold an interest in Plains All American GP LLC (“PAA GP”), which controls the general partner of Plains All American, L.P. Our ownership of PAA GP is exchangeable into shares of Plains GP Holdings, L.P. (which trades on the NYSE under the ticker “PAGP”) on a one-for-one basis at our option. See Note 3 — Fair Value. |

7

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

MANAGEMENT DISCUSSION

(UNAUDITED)

Company Overview

Kayne Anderson Energy Development Company is a non-diversified, closed-end management investment company organized under the laws of the State of Maryland. We are a taxable corporation, paying federal and applicable state taxes on our taxable income. Our operations are externally managed and advised by our investment adviser, KA Fund Advisors, LLC (“KAFA” or the “Adviser”), pursuant to an investment management agreement. Our investment objective is to generate both current income and capital appreciation primarily through equity and debt investments. We seek to achieve this objective by investing at least 80% of our total assets in securities of Energy Companies. A key focus area for our investments is equity and debt investments in private and public entities structured as limited partnerships (“MLPs”). We also own equity and debt investments in Upstream, Midstream and Other Energy Companies (as such terms are defined in Note 1 — Organization).

As of November 30, 2013, we had total assets of $477 million, net assets of $313 million (net asset value of $29.96 per share), and 10.5 million shares of common stock outstanding. As of November 30, 2013, we held $471 million in equity investments and no debt investments.

Recent Events

On January 28, 2014, we renewed our Credit Facility with a syndicate of lenders. The new Credit Facility has a three-year commitment, maturing on January 28, 2017, and a total commitment amount of $120 million, which is an increase of $25 million from the prior Credit Facility. The interest rate on the facility is LIBOR plus 1.60% (prior to the renewal, the interest rate was LIBOR plus 2.00%). If borrowings exceed the borrowing base attributable to “quoted” securities, the interest rate will increase to LIBOR plus 3.00%. We pay a fee of 0.30% per annum on any unused amounts of the Credit Facility (the fee was 0.50% per annum prior to the renewal).

Results of Operations — For the Three Months Ended November 30, 2013

Investment Income. Investment income totaled $2.9 million for the quarter and consisted primarily of net dividends and distributions. We received $8.7 million of dividends and distributions during the quarter, of which $5.9 million was treated as a return of capital. Interest and other income was $0.1 million. We received $0.2 million of paid-in-kind dividends during the quarter, which are not included in investment income but are reflected as an unrealized gain.

Operating Expenses. Operating expenses totaled $2.7 million, including $1.8 million of net investment management fees, $0.6 million of interest expense and $0.3 million of other operating expenses. Interest expense included $0.1 million of amortization of debt offering costs. As discussed in Note 5 — Agreements and Affiliations to the Financial Statements, KAFA agreed to waive 0.25% of its 1.75% management fee for a one-year period effective October 3, 2013.

Net Investment Income. Our net investment income totaled $0.1 million and included a current income tax expense of $0.5 million and a deferred income tax benefit of $0.5 million.

Net Realized Gains. We had net realized gains from investments of $1.6 million after taking into account a current income tax benefit of $1.1 million and a deferred income tax expense of $2.1 million.

Net Change in Unrealized Gains. We had a net increase in unrealized gains of $25.2 million. The net increase consisted of $40.1 million of unrealized gains from investments and a deferred income tax expense of $14.9 million.

Net Increase in Net Assets Resulting from Operations. We had an increase in net assets resulting from operations of $26.9 million. This increase was comprised of net investment income of $0.1 million, net realized gains of $1.6 million and net unrealized gains of $25.2 million, as noted above.

8

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

MANAGEMENT DISCUSSION

(UNAUDITED)

Results of Operations — For the Fiscal Year Ended November 30, 2013

Investment Income. Investment income totaled $8.0 million and consisted primarily of net dividends and distributions and interest income on our debt investments. We received $27.2 million of dividends and distributions, of which $21.6 million was treated as a return of capital during the year. During the third quarter of 2013, we received 2012 tax reporting information that was used to increase our prior year return of capital estimate by a total of $0.3 million. During the year, we received $2.4 million of interest income, of which $0.4 million was paid-in-kind interest. We also received $0.9 million of paid-in-kind dividends, which are not included in investment income, but are reflected as an unrealized gain.

Operating Expenses. Operating expenses totaled $10.5 million, including $6.8 million of net investment management fees, $2.3 million of interest expense and $1.4 million of other operating expenses. Interest expense included $0.4 million of amortization of debt offering costs.

Net Investment Loss. Our net investment loss totaled $1.5 million and included a current income tax expense of $0.4 million and a deferred income tax benefit of $1.4 million.

Net Realized Gains. We had net realized gains from investments of $3.9 million, after taking into account a current income tax benefit of $0.9 million and a deferred income tax expense of $3.2 million.

Net Change in Unrealized Gains. We had a net increase in unrealized gains of $80.9 million. The net increase consisted of $128.3 million of unrealized gains from investments and a deferred income tax expense of $47.4 million.

Net Increase in Net Assets Resulting from Operations. We had an increase in net assets resulting from operations of $83.3 million. This increase is composed of a net investment loss of $1.5 million, net realized gains of $3.9 million and net unrealized gains of $80.9 million, as noted above.

Distributions to Common Stockholders

We pay quarterly distributions to our common stockholders, funded generally by net distributable income (“NDI”) generated from our portfolio investments. NDI is the amount of income received by us from our portfolio investments less operating expenses, subject to certain adjustments as described below. NDI is not a financial measure under the accounting principles generally accepted in the United States of America (“GAAP”). Refer to the “Reconciliation of NDI to GAAP” section below for a reconciliation of this measure to our results reported under GAAP.

Income from portfolio investments includes (a) cash dividends and distributions, (b) paid-in-kind dividends or non-cash distributions received, and (c) interest income from debt securities and commitment fees from private investments in public equity (“PIPE investments”).

Operating expenses include (a) investment management fees paid to KAFA, (b) other expenses (mostly comprised of fees paid to other service providers) and (c) interest expense.

9

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

MANAGEMENT DISCUSSION

(UNAUDITED)

Net Distributable Income (NDI)

(amounts in millions, except for per share amounts)

| | | | | | | | |

| | | Three Months

Ended

November 30,

2013 | | | Fiscal Year

Ended

November 30,

2013 | |

Distributions and Other Income from Investments | | | | | | | | |

Dividends and Distributions(1) | | $ | 8.7 | | | $ | 27.2 | |

Paid-In-Kind Dividends and Distributions(1) | | | 0.2 | | | | 0.9 | |

Interest and Other Income | | | 0.1 | | | | 2.4 | |

| | | | | | | | |

Total Distributions and Other Income from Investments | | | 9.0 | | | | 30.5 | |

Expenses | | | | | | | | |

Investment Management Fee | | | (1.8 | ) | | | (6.8 | ) |

Other Expenses | | | (0.3 | ) | | | (1.4 | ) |

Interest Expense | | | (0.5 | ) | | | (1.9 | ) |

| | | | | | | | |

Net Distributable Income (NDI) | | $ | 6.4 | | | $ | 20.4 | |

| | | | | | | | |

Weighted Average Shares Outstanding | | | 10.45 | | | | 10.43 | |

NDI per Weighted Average Share Outstanding | | $ | 0.613 | | | $ | 1.956 | |

| | | | | | | | |

Adjusted NDI per Weighted Average Share Outstanding(2) | | $ | 0.547 | | | $ | 1.878 | |

| | | | | | | | |

Distributions paid per Common Share(3) | | $ | 0.500 | | | $ | 1.830 | |

| (1) | See Note 2 — Significant Accounting Policies to the Financial Statements for additional information regarding paid-in-kind and non-cash dividends and distributions. |

| (2) | Adjusted NDI excludes $0.2 million and $1.7 million of non-cash distributions from Common and Preferred A units of VantaCore Partners LP for the three months and fiscal year ended November 30, 2013, respectively. Adjusted NDI also excludes a special distribution from PAA GP of $0.5 million for both periods. |

| (3) | The distribution of $0.50 per share for the fourth quarter of fiscal 2013 will be paid on January 31, 2014 to common stockholders of record on January 27, 2014. Distributions for fiscal 2013 include the distributions paid in April 2013, July 2013, October 2013 and January 2014. |

Payment of future distributions is subject to Board of Directors approval, as well as meeting the covenants of our credit facility. In determining our quarterly distribution to common stockholders, our Board of Directors considers a number of factors which include, but are not limited to:

| | • | | NDI and Adjusted NDI generated in the current quarter; |

| | • | | Expected NDI and Adjusted NDI over the next twelve months; |

| | • | | The extent to which NDI and Adjusted NDI is comprised of non-cash interest and distributions; |

| | • | | The impact of potential liquidity events at our portfolio companies; and |

| | • | | Realized and unrealized gains generated by the portfolio. |

On January 16, 2014, we declared a quarterly distribution of $0.50 per share for the fourth quarter of fiscal 2013 (a total distribution of $5.2 million). The distribution represents an increase of 9.9% from the prior quarter’s distribution and an increase of 16.3% from the distribution for the quarter ended November 30, 2012. The distribution will be paid on January 31, 2014 to common stockholders of record on January 27, 2014.

10

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

MANAGEMENT DISCUSSION

(UNAUDITED)

Reconciliation of NDI to GAAP

The difference between distributions and other income from investments in the NDI calculation and total investment income as reported in our Statement of Operations is reconciled as follows:

| | • | | GAAP recognizes that a significant portion of the cash distributions received from MLPs is characterized as a return of capital and therefore excluded from investment income, whereas the NDI calculation includes the return of capital portion of such distributions. |

| | • | | NDI includes the value of paid-in-kind dividends and distributions, whereas such amounts are not included as investment income for GAAP purposes during the period received, but rather are recorded as unrealized gains upon receipt. |

| | • | | NDI includes commitment fees from PIPE investments, whereas such amounts are generally not included in investment income for GAAP purposes, but rather are recorded as a reduction to the cost of the investment. |

| | • | | Certain of our investments in debt securities were purchased at a discount or premium to the par value of such security. When making such investments, we consider the security’s yield to maturity, which factors in the impact of such discount (or premium). Interest income reported under GAAP includes the non-cash accretion of the discount (or amortization of the premium) based on the effective interest method. When we calculate interest income for purposes of determining NDI, in order to better reflect the yield to maturity, the accretion of the discount (or amortization of the premium) is calculated on a straight-line basis to the earlier of the expected call date or the maturity date of the debt security. |

The treatment of expenses included in NDI also differs from what is reported in the Statement of Operations as follows:

| | • | | The non-cash amortization or write-offs of capitalized debt issuance costs related to our debt financings is included in interest expense for GAAP purposes, but is excluded from our calculation of NDI. |

Liquidity and Capital Resources

As of November 30, 2013, our amended and restated senior secured revolving credit facility (the “Credit Facility”) had a total commitment amount of $95 million. On January 28, 2014, we renewed our Credit Facility, which was scheduled to mature on March 30, 2014, with a syndicate of lenders. The new Credit Facility has a three-year commitment, maturing on January 28, 2017, and a total commitment amount of $120 million. Under the new Credit Facility, the interest rate is LIBOR plus 1.60% based on current borrowings and current borrowing base (prior to the renewal, the interest rate was LIBOR plus 2.00%). If borrowings exceed the borrowing base attributable to “quoted” securities (generally defined as equity investments in public MLPs and midstream companies and investments in bank debt and high yield bonds that are traded), the interest rate will increase to LIBOR plus 3.00%. We pay a commitment fee of 0.30% per annum on any unused amounts of the new Credit Facility (the fee was 0.50% per annum prior to the renewal).

The maximum amount that we can borrow under our new Credit Facility is limited to the lesser of our commitment amount of $120 million and our borrowing base. Our borrowing base, subject to certain limitations, is generally calculated by multiplying the fair value of each of our investments by an advance rate. The total contribution to our borrowing base from private MLPs is limited to no more than 25% of the total borrowing base, and there is a $12 million limit on the borrowing base contribution from any single issuer.

11

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

MANAGEMENT DISCUSSION

(UNAUDITED)

As of November 30, 2013, we had $85 million of borrowings under our Credit Facility (at an interest rate of 2.17%), which represented 47.0% of our borrowing base of $181.0 million (47.1% of our borrowing base of $180.5 million attributable to quoted securities). At November 30, 2013, our asset coverage ratio under the Investment Company Act of 1940, as amended (the “1940 Act”), was 469%.

As of January 28, 2014, we had $84.0 million borrowed under our Credit Facility (at an interest rate of 1.77%), and we had $2.0 million of cash. Our borrowings represented 40.9% of our borrowing base of $205.5 million (41.0% of our borrowing base of $204.9 million attributable to quoted securities).

12

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2013

(amounts in 000’s)

| | | | | | | | | | | | |

Description | | | | | | No. of

Shares/Units | | | Value | |

Long-Term Investments — 150.2% | | | | | | | | | | | | |

Equity Investments(1) — 150.2% | | | | | | | | | | | | |

Public MLP and Other Equity — 140.8% | | | | | | | | | | | | |

Access Midstream Partners, L.P. | | | 232 | | | $ | 13,028 | |

Alliance Holdings GP, L.P. | | | 66 | | | | 3,651 | |

Arc Logistics Partners LP(2) | | | 237 | | | | 4,778 | |

Atlas Pipeline Partners, L.P. | | | 44 | | | | 1,521 | |

BreitBurn Energy Partners L.P. | | | 11 | | | | 204 | |

Buckeye Partners, L.P. | | | 258 | | | | 17,600 | |

Capital Product Partners L.P. | | | 352 | | | | 3,155 | |

Capital Product Partners L.P. — Class B Units(3)(4) | | | 606 | | | | 5,776 | |

Crestwood Equity Partners LP | | | 195 | | | | 2,993 | |

Crestwood Midstream Partners LP | | | 902 | | | | 20,425 | |

Crosstex Energy, L.P. | | | 287 | | | | 7,642 | |

DCP Midstream Partners, LP | | | 357 | | | | 17,194 | |

Dynagas LNG Partners LP(2) | | | 108 | | | | 2,029 | |

El Paso Pipeline Partners, L.P. | | | 115 | | | | 4,785 | |

Emerge Energy Services LP(5) | | | 1,649 | | | | 65,868 | |

Enbridge Energy Management, L.L.C.(6) | | | 25 | | | | 717 | |

Enbridge Energy Partners, L.P. | | | 325 | | | | 9,783 | |

Enduro Royalty Trust | | | 188 | | | | 2,484 | |

Energy Transfer Partners, L.P.(7) | | | 425 | | | | 23,002 | |

Enterprise Products Partners L.P.(7) | | | 385 | | | | 24,256 | |

EV Energy Partners, L.P. | | | 337 | | | | 11,017 | |

Exterran Partners, L.P. | | | 228 | | | | 6,351 | |

Global Partners LP | | | 205 | | | | 7,346 | |

Kinder Morgan, Inc. | | | 48 | | | | 1,706 | |

Kinder Morgan Energy Partners, L.P | | | 54 | | | | 4,429 | |

Kinder Morgan Management, LLC(6) | | | 157 | | | | 12,030 | |

Legacy Reserves LP | | | 88 | | | | 2,375 | |

Lehigh Gas Partners LP | | | 2 | | | | 57 | |

LRR Energy, L.P. | | | 19 | | | | 312 | |

Magellan Midstream Partners, L.P. | | | 12 | | | | 721 | |

MarkWest Energy Partners, L.P.(5) | | | 264 | | | | 18,234 | |

Mid-Con Energy Partners, LP | | | 108 | | | | 2,457 | |

Midcoast Energy Partners, L.P.(2) | | | 18 | | | | 324 | |

NuStar Energy L.P. | | | 170 | | | | 9,085 | |

ONEOK, Inc. | | | 52 | | | | 3,037 | |

ONEOK Partners, L.P. | | | 279 | | | | 14,966 | |

Plains All American Pipeline, L.P.(5) | | | 206 | | | | 10,599 | |

Plains GP Holdings, L.P. — Unregistered(3)(5)(8) | | | 918 | | | | 19,657 | |

PVR Partners, L.P. | | | 356 | | | | 8,795 | |

QEP Midstream Partners, LP | | | 58 | | | | 1,302 | |

Regency Energy Partners LP | | | 581 | | | | 14,173 | |

SandRidge Mississippian Trust II | | | 31 | | | | 295 | |

SandRidge Permian Trust | | | 115 | | | | 1,501 | |

Sprague Resources LP(2) | | | 84 | | | | 1,447 | |

Summit Midstream Partners, LP | | | 187 | | | | 6,263 | |

SunCoke Energy Partners, L.P. | | | 146 | | | | 3,945 | |

See accompanying notes to financial statements.

13

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2013

(amounts in 000’s)

| | | | | | | | | | | | |

Description | | | | | | No. of

Shares/Units | | | Value | |

Public MLP and Other Equity (continued) | | | | | | | | | | | | |

| | |

Sunoco Logistics Partners L.P. | | | 4 | | | $ | 304 | |

Tallgrass Energy Partners, LP | | | 47 | | | | 1,164 | |

Targa Resources Corp. | | | 18 | | | | 1,419 | |

Targa Resources Partners LP | | | 116 | | | | 5,945 | |

USA Compression Partners, LP | | | 135 | | | | 3,316 | |

The Williams Companies, Inc. | | | 81 | | | | 2,867 | |

Western Gas Partners, LP | | | 168 | | | | 10,673 | |

Williams Partners L.P. | | | 432 | | | | 22,200 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 441,203 | |

| | | | | | | | | | | | |

Private MLP(3)(5) — 9.4% | | | | | | | | |

VantaCore Partners LP — Common Units(6) | | | 2,187 | | | | 20,775 | |

VantaCore Partners LP — Class A Preferred Units(6)(9) | | | 359 | | | | 5,927 | |

VantaCore Partners LP — Class B Preferred Units(10) | | | 162 | | | | 2,676 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 29,378 | |

| | | | | | | | | | | | |

Total Long-Term Equity Investments — 150.2% (Cost — $312,410) | | | | 470,581 | |

| | | | | | | | | | | | |

Credit Facility | | | | (85,000 | ) |

Other Liabilities in Excess of Other Assets | | | | (72,177 | ) |

| | | | | | | | | | | | |

Net Assets | | | $ | 313,404 | |

| | | | | | | | | | | | |

| (1) | Unless otherwise noted, equity investments are common units/common shares. |

| (2) | Security is not currently paying cash distributions, but is expected to pay cash distributions within the next 12 months. |

| (3) | Fair valued security, restricted from public sale. See Notes 2, 3 and 9 in Notes to Financial Statements. |

| (4) | Class B Units are convertible on a one-for-one basis into common units of Capital Product Partners L.P. (“CPLP”) and are senior to the common units in terms of liquidation preference and priority of distributions. The Class B Units pay quarterly cash distributions of $0.21375 per unit and are convertible at any time at the option of the holder. If CPLP increases the quarterly cash distribution per common unit, the distribution per Class B Unit will increase by an equal amount. If CPLP does not redeem the Class B Units by May 2022, then the distribution increases by 25% per quarter to a maximum of $0.33345 per unit. CPLP may require that the Class B Units convert into common units after May 2015 if the common unit price exceeds $11.70 per unit, and the Class B Units are callable after May 2017 at a price of $9.27 per unit and after May 2019 at $9.00 per unit. |

| (5) | The Company believes that it is an affiliate of Emerge Energy Services LP, MarkWest Energy Partners, L.P., Plains GP Holdings, L.P. (“Plains GP”), Plains All American Pipeline, L.P. and VantaCore Partners LP (“VantaCore”). See Note 5 — Agreements and Affiliations. |

| (6) | All or a portion of dividends or distributions are paid-in-kind. |

| (7) | In lieu of cash distributions, the Company has elected to receive distributions in additional units through the partnership’s dividend reinvestment program. |

| (8) | The Company holds an interest in Plains All American GP LLC (“PAA GP”), which controls the general partner of Plains All American, L.P. The Company’s ownership of PAA GP is exchangeable into shares of Plains GP (which trades on the NYSE under the ticker “PAGP”) on a one-for-one basis at the Company’s option. See Note 3 — Fair Value. |

See accompanying notes to financial statements.

14

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2013

(amounts in 000’s)

| (9) | The Class A Preferred Units have a liquidation preference of $17.50 per unit and were issued by VantaCore to holders of the Common and Class A Preferred Units to the extent that such units did not receive full cash distributions. The Class A Preferred Units have a minimum quarterly distribution of $0.475 per unit and are senior to VantaCore’s Common Units in liquidation preference. See Note 9 — Restricted Securities. |

| (10) | The Class B Preferred Units have a liquidation preference of $17.50 per unit and a minimum quarterly distribution of $0.3825 per unit and are senior to all other equity classes of VantaCore in distributions and liquidation preference. See Note 9 — Restricted Securities. |

See accompanying notes to financial statements.

15

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

STATEMENT OF ASSETS AND LIABILITIES

NOVEMBER 30, 2013

(amounts in 000’s, except share and per share amounts)

| | | | |

ASSETS | | | | |

Investments, at fair value: | | | | |

Non-affiliated (Cost — $244,811) | | $ | 326,845 | |

Affiliated (Cost — $67,599) | | | 143,736 | |

| | | | |

Total investments (Cost — $312,410) | | | 470,581 | |

Cash | | | 1,468 | |

Receivable for securities sold | | | 1,933 | |

Interest, dividends and distributions receivable | | | 293 | |

Debt offering costs, prepaid expenses and other assets | | | 397 | |

Deferred income tax asset | | | 1,971 | |

Income tax receivable | | | 594 | |

| | | | |

Total Assets | | | 477,237 | |

| | | | |

| |

LIABILITIES | | | | |

Payable for securities purchased | | | 382 | |

Investment management fee payable | | | 1,790 | |

Accrued directors’ fees and expenses | | | 84 | |

Accrued expenses and other liabilities | | | 557 | |

Deferred income tax liability | | | 76,020 | |

Credit facility | | | 85,000 | |

| | | | |

Total Liabilities | | | 163,833 | |

| | | | |

NET ASSETS | | $ | 313,404 | |

| | | | |

NET ASSETS CONSIST OF | | | | |

Common stock, $0.001 par value (200,000,000 shares authorized; 10,459,911 shares issued and outstanding) | | $ | 10 | |

Paid-in capital | | | 202,316 | |

Accumulated net investment loss, net of income taxes, less dividends | | | (55,894 | ) |

Accumulated net realized gains on investments, net of income taxes | | | 67,462 | |

Net unrealized gains on investments, net of income taxes | | | 99,510 | |

| | | | |

NET ASSETS | | $ | 313,404 | |

| | | | |

NET ASSET VALUE PER SHARE | | $ | 29.96 | |

| | | | |

See accompanying notes to financial statements.

16

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

STATEMENT OF OPERATIONS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2013

(amounts in 000’s)

| | | | |

INVESTMENT INCOME | | | | |

Income | | | | |

Dividends and distributions: | | | | |

Non-affiliated investments | | $ | 16,627 | |

Affiliated investments | | | 10,588 | |

| | | | |

Total dividends and distributions | | | 27,215 | |

Return of capital | | | (21,583 | ) |

| | | | |

Net dividends and distributions | | | 5,632 | |

Interest and other income — non-affiliated investments | | | 1,966 | |

Interest — affiliated investments | | | 448 | |

| | | | |

Total Investment Income | | | 8,046 | |

| | | | |

Expenses | | | | |

Investment management fees, before investment management fee waiver | | | 6,963 | |

Professional fees | | | 512 | |

Directors’ fees and expenses | | | 326 | |

Administration fees | | | 88 | |

Insurance | | | 68 | |

Other expenses | | | 454 | |

| | | | |

Total Expenses — before waiver and interest expense | | | 8,411 | |

Investment management fee waiver | | | (183 | ) |

Interest expense and amortization of offering costs | | | 2,309 | |

| | | | |

Total Expenses | | | 10,537 | |

| | | | |

Net Investment Loss — Before Income Taxes | | | (2,491 | ) |

Current income tax expense | | | (380 | ) |

Deferred income tax benefit | | | 1,367 | |

| | | | |

Net Investment Loss | | | (1,504 | ) |

| | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) | | | | |

Net Realized Gains | | | | |

Investments — non-affiliated | | | 17,738 | |

Investments — affiliated | | | (11,568 | ) |

Current income tax benefit | | | 879 | |

Deferred income tax expense | | | (3,158 | ) |

| | | | |

Net Realized Gains | | | 3,891 | |

| | | | |

Net Change in Unrealized Gains | | | | |

Investments — non-affiliated | | | 48,252 | |

Investments — affiliated | | | 80,086 | |

Deferred income tax expense | | | (47,403 | ) |

| | | | |

Net Change in Unrealized Gains | | | 80,935 | |

| | | | |

Net Realized and Unrealized Gains | | | 84,826 | |

| | | | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 83,322 | |

| | | | |

See accompanying notes to financial statements.

17

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

STATEMENT OF CHANGES IN NET ASSETS

(amounts in 000’s, except share amounts)

| | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | |

| | | 2013 | | | 2012 | |

OPERATIONS | | | | | | | | |

Net investment income (loss), net of tax | | $ | (1,504 | ) | | $ | 808 | |

Net realized gains, net of tax | | | 3,891 | | | | 9,885 | |

Net change in unrealized gains, net of tax | | | 80,935 | | | | 13,630 | |

| | | | | | | | |

Net Increase in Net Assets Resulting from Operations | | | 83,322 | | | | 24,323 | |

| | | | | | | | |

DIVIDENDS AND DISTRIBUTIONS(1) | | | | | | | | |

Dividends | | | (18,348 | ) | | | (16,794 | ) |

Distributions — return of capital | | | — | | | | — | |

| | | | | | | | |

Dividends and Distributions | | | (18,348 | ) | | | (16,794 | ) |

| | | | | | | | |

CAPITAL STOCK TRANSACTIONS | | | | | | | | |

Issuance of 54,781 and 62,400 shares of common stock from reinvestment of dividends and distributions, respectively | | | 1,413 | | | | 1,458 | |

| | | | | | | | |

Total Increase in Net Assets | | | 66,387 | | | | 8,987 | |

| | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of year | | | 247,017 | | | | 238,030 | |

| | | | | | | | |

End of year | | $ | 313,404 | | | $ | 247,017 | |

| | | | | | | | |

| (1) | Distributions paid to common stockholders for the fiscal years ended November 30, 2013 and 2012 are characterized as dividends (eligible to be treated as qualified dividend income). This characterization is based on the Company’s earnings and profits. |

See accompanying notes to financial statements.

18

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

STATEMENT OF CASH FLOWS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2013

(amounts in 000’s)

| | | | |

CASH FLOWS FROM OPERATING ACTIVITIES | | | | |

Net increase in net assets resulting from operations | | $ | 83,322 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: | | | | |

Return of capital distributions | | | 21,583 | |

Net realized gains on investments | | | (6,170 | ) |

Net unrealized gains on investments | | | (128,338 | ) |

Amortization of bond premium, net | | | 18 | |

Purchase of long-term investments | | | (174,950 | ) |

Proceeds from sale of long-term investments | | | 152,865 | |

Decrease in receivable for securities sold | | | 3,516 | |

Decrease in interest, dividends and distributions receivable | | | 339 | |

Increase in deferred income tax asset | | | (1,971 | ) |

Increase in income tax receivable | | | (594 | ) |

Decrease in other receivable | | | 2,900 | |

Amortization of deferred debt offering costs | | | 444 | |

Increase in prepaid expenses and other assets | | | (3 | ) |

Decrease in payable for securities purchased | | | (177 | ) |

Increase in investment management fee payable | | | 280 | |

Increase in accrued directors’ fees and expenses | | | 6 | |

Decrease in accrued expenses and other liabilities | | | (16 | ) |

Decrease in current income tax liability | | | (460 | ) |

Increase in deferred income tax liability | | | 51,161 | |

| | | | |

Net Cash Provided by Operating Activities | | | 3,755 | |

| | | | |

CASH FLOWS FROM FINANCING ACTIVITIES | | | | |

Increase in borrowings under credit facility | | | 13,000 | |

Cash distributions paid to stockholders | | | (16,935 | ) |

| | | | |

Net Cash Used in Financing Activities | | | (3,935 | ) |

| | | | |

NET DECREASE IN CASH | | | (180 | ) |

CASH — BEGINNING OF YEAR | | | 1,648 | |

| | | | |

CASH — END OF YEAR | | $ | 1,468 | |

| | | | |

Supplemental disclosure of cash flow information:

Non-cash financing activities not included herein consisted of reinvestment of distributions pursuant to the Company’s dividend reinvestment plan of $1,413.

During the fiscal year ended November 30, 2013, there were $651 of federal income taxes paid and $96 of state income tax refunds, net of payments. Interest paid was $1,859.

During the fiscal year ended November 30, 2013, the Company received $3,493 of paid-in-kind and non-cash dividends and distributions and $448 of paid-in-kind interest. See Note 2 — Significant Accounting Policies.

See accompanying notes to financial statements.

19

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | | | For the

Period

September 21,

2006

through

November 30,

2006 | |

| | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Per Share of Common Stock(1) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 23.74 | | | $ | 23.01 | | | $ | 20.56 | | | $ | 16.58 | | | $ | 16.10 | | | $ | 23.95 | | | $ | 24.03 | | | $ | 23.32 | |

Net investment income (loss) | | | (0.14 | ) | | | 0.08 | | | | 0.25 | | | | (0.18 | ) | | | 0.10 | | | | 0.09 | | | | 0.08 | | | | (0.07 | ) |

Net realized and unrealized gain (loss) on investments | | | 8.13 | | | | 2.27 | | | | 3.60 | | | | 5.39 | | | | 1.68 | | | | (5.89 | ) | | | 1.18 | | | | 0.78 | |

Net change in unrealized losses — conversion to taxable corporation | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.38 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total income (loss) from investment operations | | | 7.99 | | | | 2.35 | | | | 3.85 | | | | 5.21 | | | | 1.78 | | | | (6.18 | ) | | | 1.26 | | | | 0.71 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends(2) | | | (1.76 | ) | | | (1.62 | ) | | | (1.37 | ) | | | (0.51 | ) | | | — | | | | — | | | | (0.95 | ) | | | — | |

Distributions from net realized long-term capital gains(2)(3) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.15 | ) | | | — | |

Distributions — return of capital(2) | | | — | | | | — | | | | — | | | | (0.69 | ) | | | (1.30 | ) | | | (1.67 | ) | | | (0.24 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (1.76 | ) | | | (1.62 | ) | | | (1.37 | ) | | | (1.20 | ) | | | (1.30 | ) | | | (1.67 | ) | | | (1.34 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Effect of shares issued in reinvestment of distributions | | | (0.01 | ) | | | — | | | | (0.03 | ) | | | (0.03 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 29.96 | | | $ | 23.74 | | | $ | 23.01 | | | $ | 20.56 | | | $ | 16.58 | | | $ | 16.10 | | | $ | 23.95 | | | $ | 24.03 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Market value per share, end of period | | $ | 28.70 | | | $ | 26.01 | | | $ | 20.21 | | | $ | 18.21 | | | $ | 13.53 | | | $ | 9.63 | | | $ | 23.14 | | | $ | 22.32 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total investment return based on market value(4) | | | 18.1 | % | | | 37.8 | % | | | 19.3 | % | | | 45.8 | % | | | 56.0 | % | | | (54.8 | )% | | | 9.3 | % | | | (10.7 | )%(5) |

See accompanying notes to financial statements.

20

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | | | For the

Period

September 21,

2006

through

November 30,

2006 | |

| | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Supplemental Data and Ratios(6) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period | | $ | 313,404 | | | $ | 247,017 | | | $ | 238,030 | | | $ | 211,041 | | | $ | 168,539 | | | $ | 162,687 | | | $ | 240,758 | | | $ | 240,349 | |

Ratio of expenses to average net assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Management fees | | | 2.5 | % | | | 2.4 | % | | | 2.4 | % | | | 2.1 | % | | | 2.0 | % | | | 0.4 | % | | | 3.1 | % | | | 2.4 | % |

Other expenses | | | 0.5 | | | | 0.6 | | | | 0.7 | | | | 1.0 | | | | 1.3 | | | | 1.1 | | | | 0.9 | | | | 1.3 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Subtotal | | | 3.0 | | | | 3.0 | | | | 3.1 | | | | 3.1 | | | | 3.3 | | | | 1.5 | | | | 4.0 | | | | 3.7 | |

Interest expense | | | 0.8 | | | | 0.9 | | | | 0.8 | | | | 0.9 | | | | 0.8 | | | | 2.0 | | | | 1.0 | | | | — | |

Management fee waivers | | | (0.1 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.4 | ) | | | (0.5 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses (excluding tax expense) | | | 3.7 | | | | 3.9 | | | | 3.9 | | | | 4.0 | | | | 4.1 | | | | 3.5 | | | | 4.6 | | | | 3.2 | |

Tax expense | | | 17.1 | | | | 5.6 | | | | 10.0 | | | | 16.3 | | | | 6.9 | | | | — | (7) | | | 0.8 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total expenses(8) | | | 20.8 | % | | | 9.5 | % | | | 13.9 | % | | | 20.3 | % | | | 11.0 | % | | | 3.5 | % | | | 5.4 | % | | | 3.2 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income (loss) to average net assets | | | (0.5 | )% | | | 0.3 | % | | | 1.1 | % | | | (1.0 | )% | | | 0.7 | % | | | 0.4 | % | | | 0.3 | % | | | (0.3 | )% |

Net increase (decrease) in net assets resulting from operations to average net assets | | | 29.2 | % | | | 9.9 | % | | | 17.1 | % | | | 28.3 | % | | | 11.3 | % | | | (29.5 | )% | | | 5.1 | % | | | 3.0 | %(5) |

Portfolio turnover rate | | | 38.4 | % | | | 34.6 | % | | | 68.1 | % | | | 33.4 | % | | | 20.9 | % | | | 27.0 | % | | | 28.8 | % | | | 5.6 | %(5) |

Average net assets | | $ | 284,880 | | | $ | 246,183 | | | $ | 231,455 | | | $ | 188,307 | | | $ | 160,847 | | | $ | 211,531 | | | $ | 246,468 | | | $ | 234,537 | |

Average shares of common stock outstanding | | | 10,430,618 | | | | 10,372,215 | | | | 10,301,878 | | | | 10,212,289 | | | | 10,116,071 | | | | 10,073,398 | | | | 10,014,496 | | | | 10,000,060 | |

Average amount of borrowings outstanding under the credit facility | | $ | 77,786 | | | $ | 78,180 | | | $ | 62,559 | | | $ | 54,956 | | | $ | 53,422 | | | $ | 75,563 | | | $ | 32,584 | | | | — | |

Asset coverage of total debt(9) | | | 468.7 | % | | | 443.1 | % | | | 409.1 | % | | | 470.2 | % | | | n/a | | | | n/a | | | | n/a | | | | n/a | |

Average amount of borrowings per share of common stock during the period | | $ | 7.46 | | | $ | 7.54 | | | $ | 6.07 | | | $ | 5.38 | | | $ | 5.28 | | | $ | 7.50 | | | $ | 3.25 | | | | — | |

See accompanying notes to financial statements.

21

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| (1) | Based on average shares of common stock outstanding. |

| (2) | The information presented for each period is a characterization of the total distributions paid to common stockholders as either a dividend (eligible to be treated as qualified dividend income) or a distribution (long-term capital gains or return of capital) and is based on the Company’s earnings and profits. |

| (3) | For the fiscal year ended November 30, 2007 and prior periods, the Company was treated as a regulated investment company under the U.S. Internal Revenue Code of 1986, as amended. Since December 1, 2007, the Company has been taxed as a corporation, and, as a result, the categorization of distributions from net realized long-term capital gains is no longer applicable. |

| (4) | Total investment return is calculated assuming a purchase of common stock at the market price on the first day and a sale at the current market price on the last day of the period reported. The calculation also assumes reinvestment of distributions, if any, at actual prices pursuant to the Company’s dividend reinvestment plan. |

| (6) | Unless otherwise noted, ratios are annualized. |

| (7) | For the fiscal year ended November 30, 2008, the Company accrued deferred income tax benefits of $33,264 (15.5% of average net assets) primarily related to unrealized losses on investments. Realization of the deferred tax benefit was dependent on whether there was sufficient taxable income of the appropriate character within the carryforward periods to realize a portion or all of the deferred tax benefit. Because it could not have been predicted whether the Company would incur a benefit in the future, a deferred income tax expense of 0% was assumed. |

| (8) | For the fiscal year ended November 30, 2008, total expenses exclude 0.4% relating to bad debt expense for the ratio of expenses to average net assets. |

| (9) | Calculated pursuant to section 18(a)(1)(A) of the 1940 Act. Represents the value of total assets less all liabilities not represented by senior securities representing indebtedness divided by senior securities representing indebtedness. Under the 1940 Act, the Company may not declare or make any distribution on its common stock nor can it incur additional indebtedness if at the time of such declaration or incurrence its asset coverage with respect to senior securities representing indebtedness would be less than 300%. For purposes of this test, the Credit Facility is considered a senior security representing indebtedness. Prior to July 7, 2010, the Company was a business development company under the 1940 Act and not subject to the requirements of section 18(a)(1)(A) for the asset coverage of total debt disclosure. |

See accompanying notes to financial statements.

22

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)

Kayne Anderson Energy Development Company (the “Company”) was organized as a Maryland corporation on May 24, 2006. The Company is an externally managed, non-diversified closed-end management investment company. The Company commenced investment operations on September 21, 2006. The Company’s shares of common stock are listed on the New York Stock Exchange (“NYSE”) under the symbol “KED.” Prior to November 30, 2007, the Company was treated as a regulated investment company (“RIC”) under the U.S. Internal Revenue Code of 1986, as amended. Since December 1, 2007, the Company has been taxed as a corporation. See Note 6 — Income Taxes.

The Company’s investment objective is to generate both current income and capital appreciation primarily through equity and debt investments. The Company seeks to achieve this objective by investing at least 80% of its total assets in securities of companies that derive the majority of their revenue from activities in the energy industry (“Energy Companies”), including: (a) Midstream Energy Companies, which are businesses that operate assets used to gather, transport, process, treat, terminal and store natural gas, natural gas liquids, propane, crude oil or refined petroleum products; (b) Upstream Energy Companies, which are businesses engaged in the exploration, extraction and production of natural resources, including natural gas, natural gas liquids and crude oil, from onshore and offshore geological reservoirs; and (c) Other Energy Companies, which are businesses engaged in owning, leasing, managing, producing, processing and selling of coal and coal reserves; the marine transportation of crude oil, refined petroleum products, liquefied natural gas, as well as other energy-related natural resources using tank vessels and bulk carriers; and refining, marketing and distributing refined energy products, such as motor gasoline and propane, to retail customers and industrial end-users. A majority of the Company’s investments are in entities structured as master limited partnerships (“MLPs”), including both publicly-traded MLPs and private MLPs, which are structured much like publicly-traded MLPs.

| 2. | Significant Accounting Policies |

A. Use of Estimates — The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ materially from those estimates.

B. Cash and Cash Equivalents — Cash and cash equivalents include short-term, liquid investments with an original maturity of three months or less and include money market fund accounts.

C. Calculation of Net Asset Value — The Company determines its net asset value no less frequently than as of the last day of each quarter based on the most recent close of regular session trading on the NYSE, and makes its net asset value available for publication quarterly. Net asset value is computed by dividing the value of the Company’s assets (including accrued interest and distributions and current and deferred income tax assets), less all of its liabilities (including accrued expenses, distributions payable, current and deferred accrued income taxes, and any borrowings) by the total number of common shares outstanding.

As of June 30, 2013, the Company began providing adjusted net asset value on a monthly basis for those months that do not constitute the end of a fiscal quarter. The Company’s adjusted net asset value is a non-GAAP measure and is intended to provide investors with a monthly update on the impact of price changes for the public securities in the Company’s portfolio. Adjusted net asset value is calculated based on the same methodology as net asset value and incorporates updated values for the publicly-traded equity securities (including PIPE investments) and quoted debt investments in the Company’s portfolio, including any related income tax impact. The Company’s adjusted net asset value calculation incorporates the Company’s month-end balance sheet but does not update the value of the non-traded securities in its portfolio.

23

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)

D. Investment Valuation — Readily marketable portfolio securities listed on any exchange other than the NASDAQ Stock Market, Inc. (“NASDAQ”) are valued, except as indicated below, at the last sale price on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the most recent bid and ask prices on such day. Securities admitted to trade on the NASDAQ are valued at the NASDAQ official closing price. Portfolio securities traded on more than one securities exchange are valued at the last sale price on the business day as of which such value is being determined at the close of the exchange representing the principal market for such securities.

Equity securities traded in the over-the-counter market, but excluding securities admitted to trading on the NASDAQ, are valued at the closing bid prices. Debt securities that are considered bonds are valued by using the mean of the bid and ask prices provided by an independent pricing service. For debt securities that are considered bank loans, the fair market value is determined by using the mean of the bid and ask prices provided by the agent or syndicate bank or principal market maker. When price quotes are not available, fair market value will be based on prices of comparable securities. In certain cases, the Company may not be able to purchase or sell debt securities at the quoted prices due to the lack of liquidity for these securities.

Exchange-traded options and futures contracts are valued at the last sale price at the close of trading in the market where such contracts are principally traded or, if there was no sale on the applicable exchange on such day, at the mean between the quoted bid and ask price as of the close of trading on such exchange.

The Company holds securities that are privately issued or otherwise restricted as to resale. For these securities, as well as any other portfolio security held by the Company for which reliable market quotations are not readily available, valuations are determined in a manner that most accurately reflects fair value of the security on the valuation date. Unless otherwise determined by the Board of Directors, the following valuation process is used for such securities:

| | • | | Investment Team Valuation. The applicable investments are valued by senior professionals of KA Fund Advisors, LLC (“KAFA” or the “Adviser”) who are responsible for the portfolio investments. |

| | • | | Investment Team Valuation Documentation. Preliminary valuation conclusions will be determined by senior management of KAFA. Such valuations are submitted to the Valuation Committee (a committee of the Company’s Board of Directors) and the Board of Directors on a quarterly basis. New private investments made during a quarter will be valued by senior management of KAFA. |

| | • | | Valuation Committee. The Valuation Committee meets to consider valuations presented by KAFA at the end of each quarter. The Valuation Committee’s valuation determinations are subject to ratification by the Board of Directors at its next regular meeting. |

| | • | | Valuation Firm. Quarterly, a third-party valuation firm engaged by the Board of Directors reviews the valuation methodologies and calculations employed for these securities. The independent valuation firm provides third-party valuation consulting services to the Board of Directors, which consist of certain limited procedures that the Company identified and requested them to perform. As of November 30, 2013, the independent valuation firm performed limited procedures on investments in three portfolio companies comprising approximately 11.5% of total assets. Upon completion of the limited procedures, the independent valuation firm concluded that the fair value of those investments subjected to the limited procedures appeared reasonable. |

| | • | | Board of Directors Determination. The Board of Directors meets quarterly to consider the valuations provided by KAFA and the Valuation Committee and ratify valuations for the applicable securities. The Board of Directors considers the report provided by the third-party valuation firm in reviewing and determining in good faith the fair value of the applicable portfolio securities. |

24

KAYNE ANDERSON ENERGY DEVELOPMENT COMPANY

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)