Filed by Safran S.A.

Pursuant to Rule 425 under the Securities Act of 1933, as amended

Subject Company: Zodiac Aerospace S.A.

Commission File No. 333-154066

Date: January 20, 2017

Creating a global leader in aerospace : Safran TO Acquire Zodiac Aerospace January, 19th 2017 Safran name of the activity / Confidential / Date / Department (menu "Insert / Header and footer") 1

IMPORTANT ADDITIONAL INFORMATION This communication is not intended to and does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy or an invitation to purchase or subscribe for any securities or the solicitation of any vote or approval in any jurisdiction in connection with the transaction or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law. The tender offer and the merger are subject to consultation of the work’s council committees, execution of definitive documentation and obtaining of required regulatory and other customary authorisations. The tender offer and the merger would only be filed after such and other conditions have been fulfilled. These materials must not be published, released or distributed, directly or indirectly, in any jurisdiction where the distribution of such information is restricted by law.It is intended that Safran and Zodiac Aerospace will file with the French Market Authority (“AMF”) a prospectus and other relevant documents with respect to the tender offer to be made in France, and with respect to the merger of Zodiac Aerospace into Safran. Pursuant to French regulations, the documentation with respect to the tender offer and the merger which, if filed, will state the terms and conditions of the tender offer and the merger will be subject to the review by the French Market Authority (AMF). Investors and shareholders in France are strongly advised to read, if and when they become available, the prospectus and related offer and merger materials regarding the tender offer and the merger referenced in this communication, as well as any amendments and supplements to those documents as they will contain important information regarding Safran, Zodiac Aerospace, the contemplated transactions and related mattersADDITIONAL U.S. INFORMATIONAny securities to be issued under the transaction may be required to be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”). The transaction will be submitted to the shareholders of Zodiac Aerospace for their consideration. If registration with the U.S. Securities and Exchange Commission (the “SEC”) is required in connection with the transaction, Safran will prepare a prospectus for Zodiac Aerospace’s shareholders to be filed with the SEC, will mail the prospectus to Zodiac Aerospace’s shareholders and file other documents regarding the proposed transaction with the SEC. Investors and shareholders are urged to read the prospectus and the registration statement of which it forms a part when and if it becomes available, as well as other documents that may be filed with the SEC, because they will contain important information. If registration with the SEC is required in connection with the transaction, shareholders of Zodiac Aerospace will be able to obtain free copies of the prospectus and other documents filed by Safran with the SEC at the SEC’s web site, http://www.sec.gov. Those documents, if filed, may also be obtained free of charge by contacting Safran Investor Relations at 2, Boulevard du Général Martial Valin 75724 Paris Cedex 15 – France or by calling (33) 1 40 60 80 80. Alternatively, if the requirements of Rule 802 under the Securities Act are satisfied, offers and sales made by Safran in the proposed business combination will be exempt from the provisions of Section 5 of the Securities Act and no registration statement will be filed with the SEC by Safran. FORWARD-LOOKING STATEMENTS This communication contains forward-looking statements relating to Safran, Zodiac Aerospace and their combined businesses, which do not refer to historical facts but refer to expectations based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those included in such statements. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to Safran, Zodiac Aerospace and their combined businesses, based on current beliefs of management as well as assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “possible,” “potential,” “predict,” “project” or other similar words, phrases or expressions. Many of these risks and uncertainties relate to factors that are beyond Safran’s or Zodiac Aerospace’s control. Therefore, investors and shareholders should not place undue reliance on such statements. Factors that could cause actual results to differ materially from those in the forward-looking statements include, but are not limited to: the ability obtain the approval of the transaction by shareholders; failure to satisfy other closing conditions with respect to the transaction on the proposed terms and timeframe; the possibility that the transaction does not close when expected or at all; the risks that the new businesses will not be integrated successfully or that the combined company will not realize estimated cost savings and synergies; Safran’s or Zodiac Aerospace’s ability to successfully implement and complete its plans and strategies and to meet its targets; and the benefits from Safran’s or Zodiac Aerospace’s (and their combined businesses) plans and strategies being less than anticipated. The foregoing list of factors is not exhaustive. Forward-looking statements speak only as of the date they are made. Safran and Zodiac Aerospace do not assume any obligation to update any public information or forward-looking statement in this communication to reflect events or circumstances after the date of this communication, except as may be required by applicable laws. Disclaimer Month/day/year 2

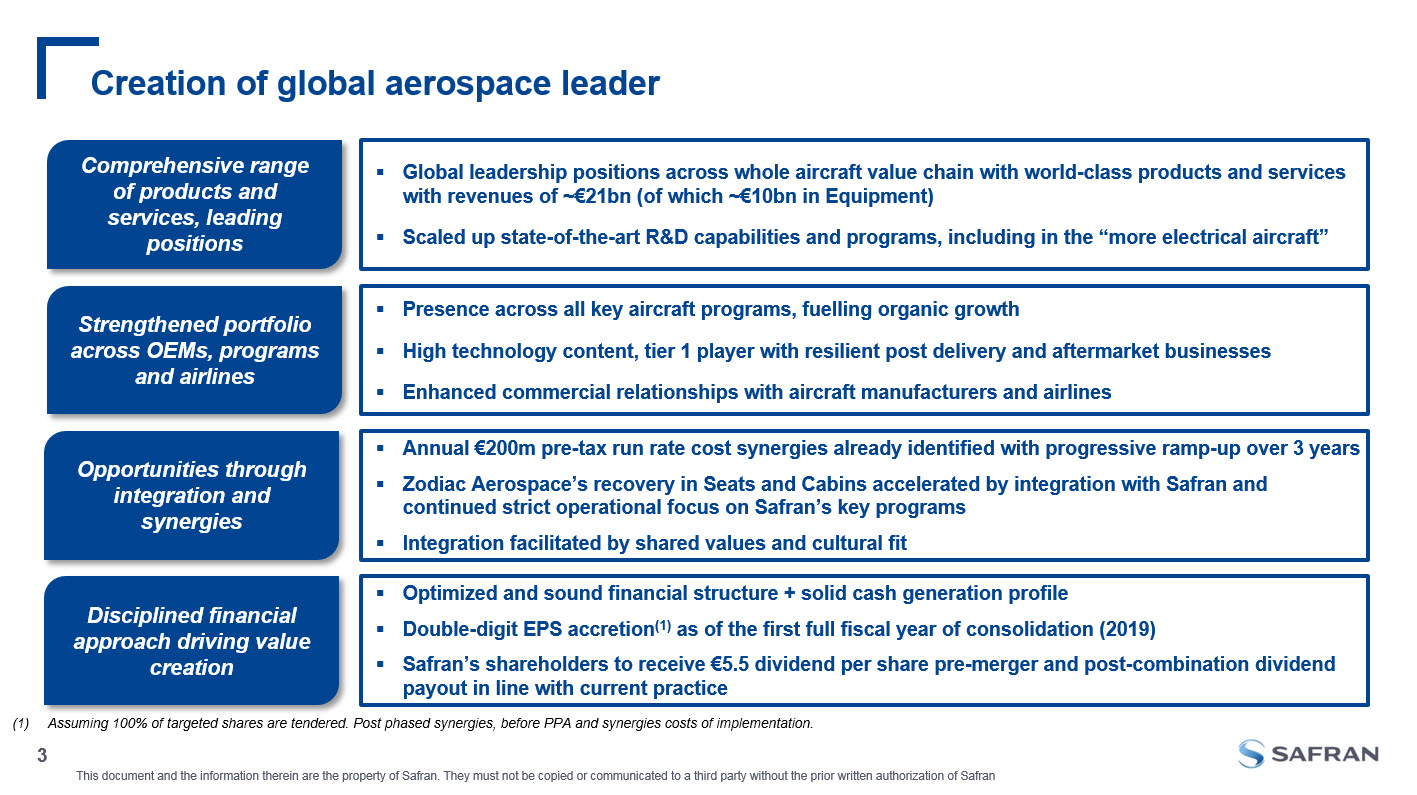

Creation of global aerospace leader Month/day/year 3 Opportunities through integration and synergies Strengthened portfolio across OEMs, programs and airlines Comprehensive range of products and services, leading positions Disciplined financial approach driving value creation Global leadership positions across whole aircraft value chain with world-class products and services with revenues of ~€21bn (of which ~€10bn in Equipment)Scaled up state-of-the-art R&D capabilities and programs, including in the “more electrical aircraft” Presence across all key aircraft programs, fuelling organic growthHigh technology content, tier 1 player with resilient post delivery and aftermarket businesses Enhanced commercial relationships with aircraft manufacturers and airlines Annual €200m pre-tax run rate cost synergies already identified with progressive ramp-up over 3 yearsZodiac Aerospace’s recovery in Seats and Cabins accelerated by integration with Safran and continued strict operational focus on Safran’s key programsIntegration facilitated by shared values and cultural fit Optimized and sound financial structure + solid cash generation profileDouble-digit EPS accretion(1) as of the first full fiscal year of consolidation (2019)Safran’s shareholders to receive €5.5 dividend per share pre-merger and post-combination dividend payout in line with current practice Assuming 100% of targeted shares are tendered. Post phased synergies, before PPA and synergies costs of implementation.

Transaction highlights Safran to launch a public tender offer on Zodiac Aerospace(1) at a price of €29.47 per share in cashThe offer price represents a premium of 26.4% over Zodiac Aerospace’s closing price as of 18/01/17 and 36.1 % over 3-month VWAP Following the offer, Zodiac Aerospace will be merged with SafranExchange ratio set at 97 Safran shares (ex-special dividend) for 200 Zodiac Aerospace shares (0.485 for 1)Prior to the merger and subject to completion of the transaction, existing Safran shareholders will receive an special dividend of €5.5 per shareTransaction Value of €9.7bn(2)Transaction Value / LTM Current Operating Income of ~13x based on Zodiac Aerospace’s profitability guidance(3) Month/day/year 4 Key transaction terms Targeting all outstanding shares except those shares subject to an undertaking not to tender. (2) €29.47 per Zodiac Aerospace fully diluted, excluding treasury, shares and including Zodiac Aerospace debt and debt-like items as at 31/08/2016. (3) Mid-double digit operating margin is expected at horizon FY2019/2020 as communicated by Zodiac Aerospace during FY15/16 results on 22/11/16. Family shareholders and 2 institutional investors (FFP and Fonds Stratégique de Participations) of Zodiac Aerospace undertake to contribute their shares to the mergerAnd together with the French State will own ~22% of Safran post-merger with a 2-year lock-up provision Reference shareholders support the transaction Approvals and timing The proposed transaction has received the support of both Zodiac Aerospace’s Supervisory Board and Safran’s Board of DirectorsCompletion of the proposed transaction will be subject to Safran’s and Zodiac Aerospace’s respective works council processes and shareholders approvals as well as regulatory approvals and other customary conditionsEstimated close by early 2018

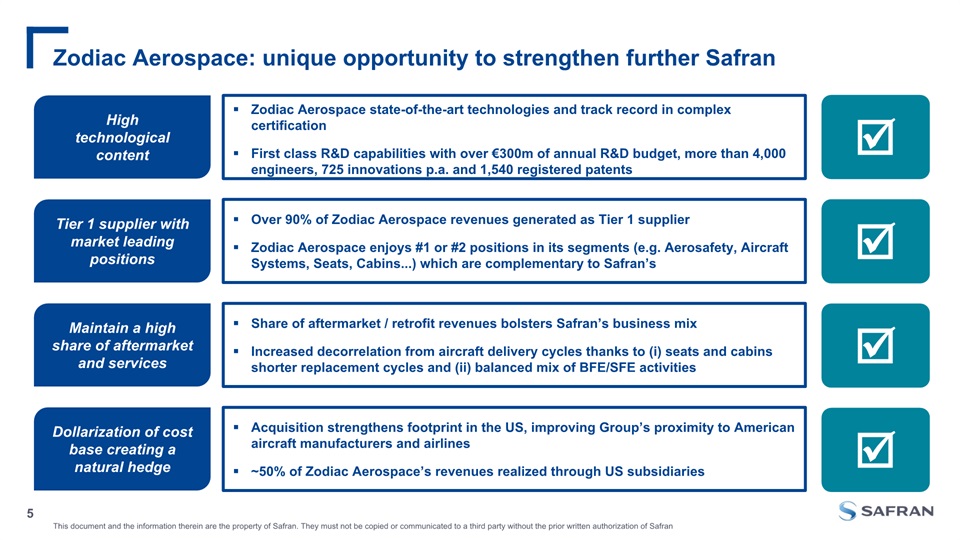

Zodiac Aerospace state-of-the-art technologies and track record in complex certificationFirst class R&D capabilities with over €300m of annual R&D budget, more than 4,000 engineers, 725 innovations p.a. and 1,540 registered patents Zodiac Aerospace: unique opportunity to strengthen further Safran Month/day/year 5 Tier 1 supplier with market leading positions Maintain a high share of aftermarket and services Hightechnologicalcontent Dollarization of cost base creating a natural hedge Acquisition strengthens footprint in the US, improving Group’s proximity to American aircraft manufacturers and airlines ~50% of Zodiac Aerospace’s revenues realized through US subsidiaries Over 90% of Zodiac Aerospace revenues generated as Tier 1 supplierZodiac Aerospace enjoys #1 or #2 positions in its segments (e.g. Aerosafety, Aircraft Systems, Seats, Cabins...) which are complementary to Safran’s Share of aftermarket / retrofit revenues bolsters Safran’s business mixIncreased decorrelation from aircraft delivery cycles thanks to (i) seats and cabins shorter replacement cycles and (ii) balanced mix of BFE/SFE activities

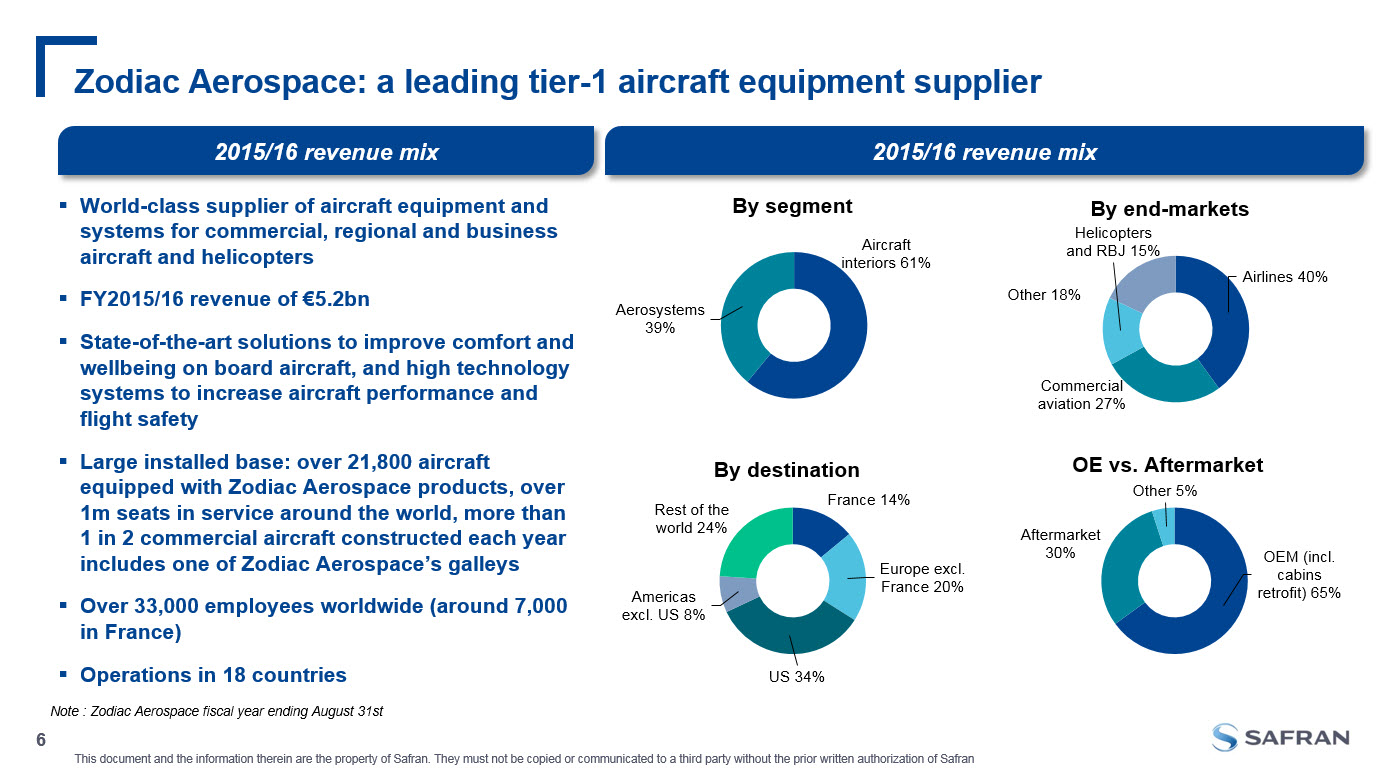

Zodiac Aerospace: a leading tier-1 aircraft equipment supplier Month/day/year 6 World-class supplier of aircraft equipment and systems for commercial, regional and business aircraft and helicoptersFY2015/16 revenue of €5.2bnState-of-the-art solutions to improve comfort and wellbeing on board aircraft, and high technology systems to increase aircraft performance and flight safetyLarge installed base: over 21,800 aircraft equipped with Zodiac Aerospace products, over 1m seats in service around the world, more than 1 in 2 commercial aircraft constructed each year includes one of Zodiac Aerospace’s galleysOver 33,000 employees worldwide (around 7,000 in France)Operations in 18 countries 2015/16 revenue mix 2015/16 revenue mix Note : Zodiac Aerospace fiscal year ending August 31st

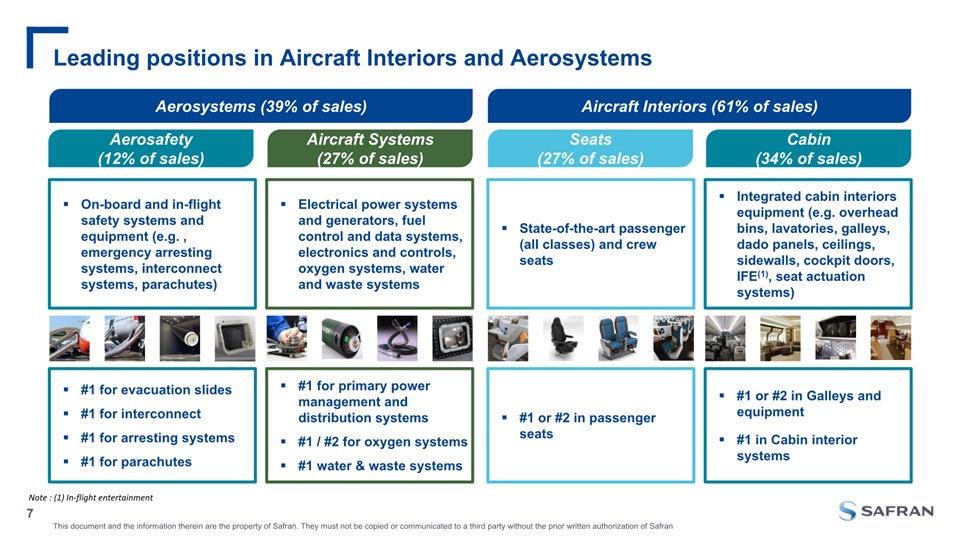

Leading positions in Aircraft Interiors and Aerosystems Month/day/year 7 Aircraft Interiors (61% of sales) Aerosystems (39% of sales) Aerosafety(12% of sales) On-board and in-flight safety systems and equipment (e.g. , emergency arresting systems, interconnect systems, parachutes) Electrical power systems and generators, fuel control and data systems, electronics and controls, oxygen systems, water and waste systems State-of-the-art passenger (all classes) and crew seats Integrated cabin interiors equipment (e.g. overhead bins, lavatories, galleys, dado panels, ceilings, sidewalls, cockpit doors, IFE(1), seat actuation systems) Aircraft Systems(27% of sales) Seats (27% of sales) Cabin(34% of sales) Note : (1) In-flight entertainment #1 for evacuation slides#1 for interconnect#1 for arresting systems#1 for parachutes #1 for primary power management and distribution systems#1 / #2 for oxygen systems#1 water & waste systems #1 or #2 in passenger seats #1 or #2 in Galleys and equipment#1 in Cabin interior systems

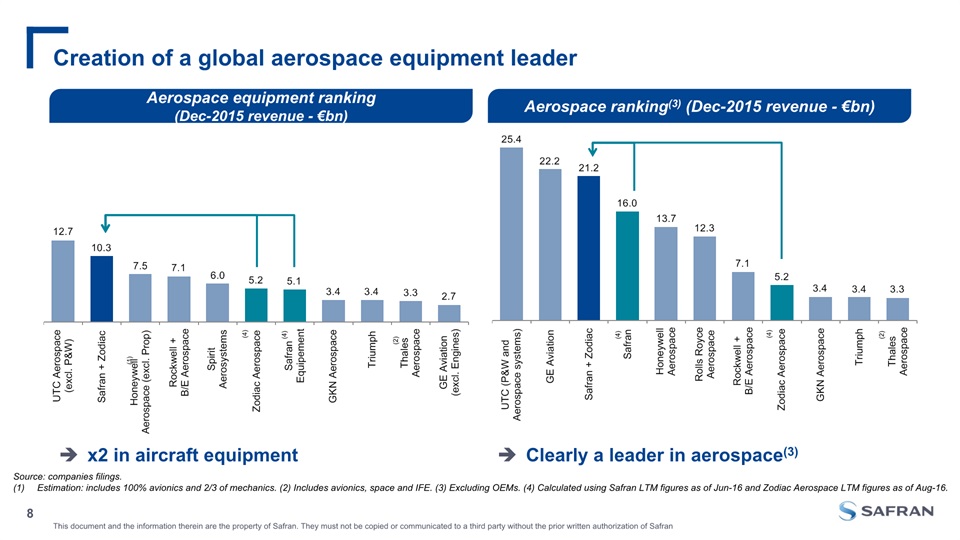

Creation of a global aerospace equipment leader Month/day/year 8 Aerospace ranking(3) (Dec-2015 revenue - €bn) Aerospace equipment ranking (Dec-2015 revenue - €bn) (2) (1) (2) x2 in aircraft equipment Source: companies filings.Estimation: includes 100% avionics and 2/3 of mechanics. (2) Includes avionics, space and IFE. (3) Excluding OEMs. (4) Calculated using Safran LTM figures as of Jun-16 and Zodiac Aerospace LTM figures as of Aug-16. Clearly a leader in aerospace(3) (4) (4) (4) (4)

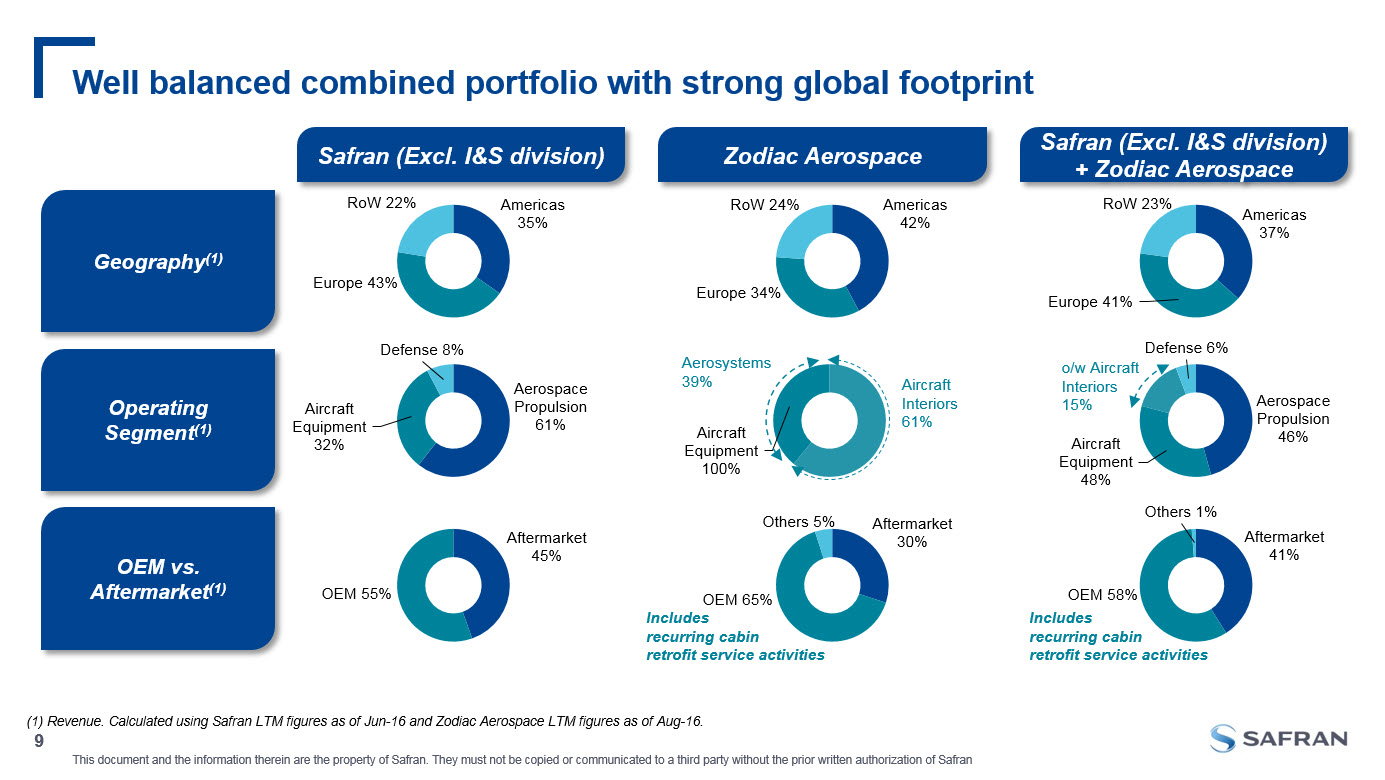

Well balanced combined portfolio with strong global footprint 9 (1) Revenue. Calculated using Safran LTM figures as of Jun-16 and Zodiac Aerospace LTM figures as of Aug-16. Safran (Excl. I&S division) + Zodiac Aerospace Safran (Excl. I&S division) Geography(1) OEM vs. Aftermarket(1) Operating Segment(1) Zodiac Aerospace Includesrecurring cabinretrofit service activities Aircraft Interiors61% o/w Aircraft Interiors15% Includesrecurring cabinretrofit service activities Aerosystems 39%

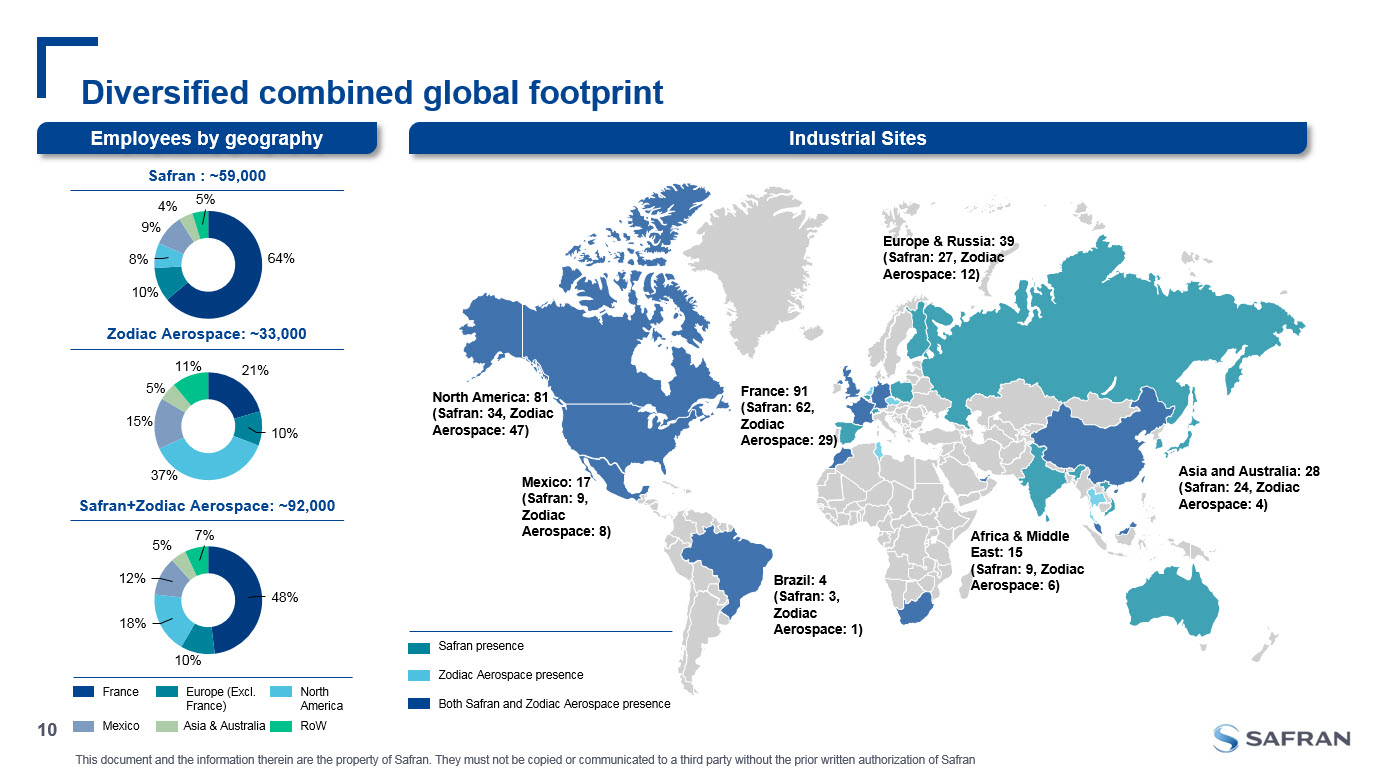

Diversified combined global footprint Employees by geography Mexico: 17(Safran: 9, Zodiac Aerospace: 8) Month/day/year 10 North America: 81(Safran: 34, Zodiac Aerospace: 47) Brazil: 4(Safran: 3, Zodiac Aerospace: 1) Africa & Middle East: 15(Safran: 9, Zodiac Aerospace: 6) Europe & Russia: 39(Safran: 27, Zodiac Aerospace: 12) Asia and Australia: 28(Safran: 24, Zodiac Aerospace: 4) France: 91(Safran: 62, Zodiac Aerospace: 29) Safran presence Zodiac Aerospace presence Both Safran and Zodiac Aerospace presence Industrial Sites Safran : ~59,000 Zodiac Aerospace: ~33,000 Safran+Zodiac Aerospace: ~92,000 France Europe (Excl. France) North America Mexico Asia & Australia RoW

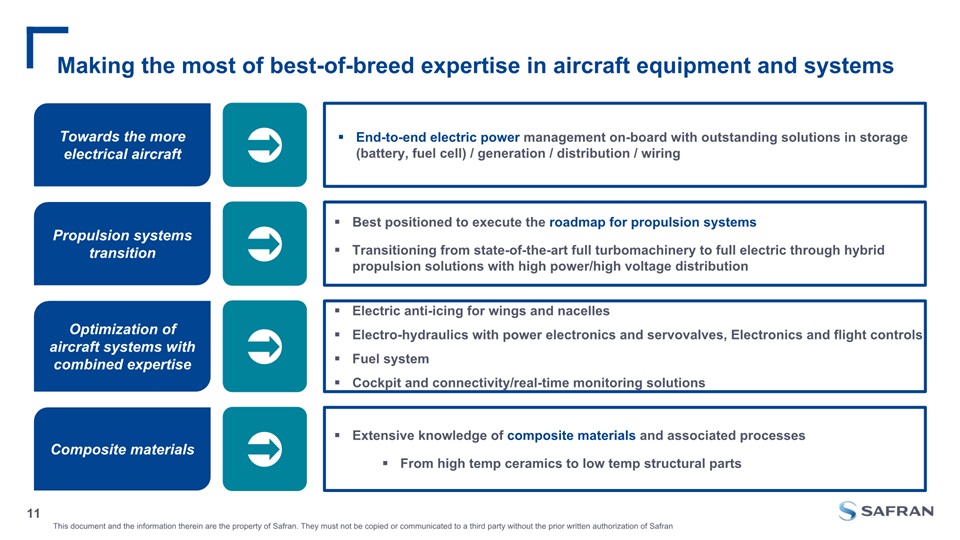

Making the most of best-of-breed expertise in aircraft equipment and systems Month/day/year 11 Propulsion systems transition Optimization of aircraft systems with combined expertise Towards the more electrical aircraft Composite materials Extensive knowledge of composite materials and associated processes From high temp ceramics to low temp structural parts Best positioned to execute the roadmap for propulsion systemsTransitioning from state-of-the-art full turbomachinery to full electric through hybrid propulsion solutions with high power/high voltage distribution Electric anti-icing for wings and nacellesElectro-hydraulics with power electronics and servovalves, Electronics and flight controlsFuel systemCockpit and connectivity/real-time monitoring solutions End-to-end electric power management on-board with outstanding solutions in storage (battery, fuel cell) / generation / distribution / wiring

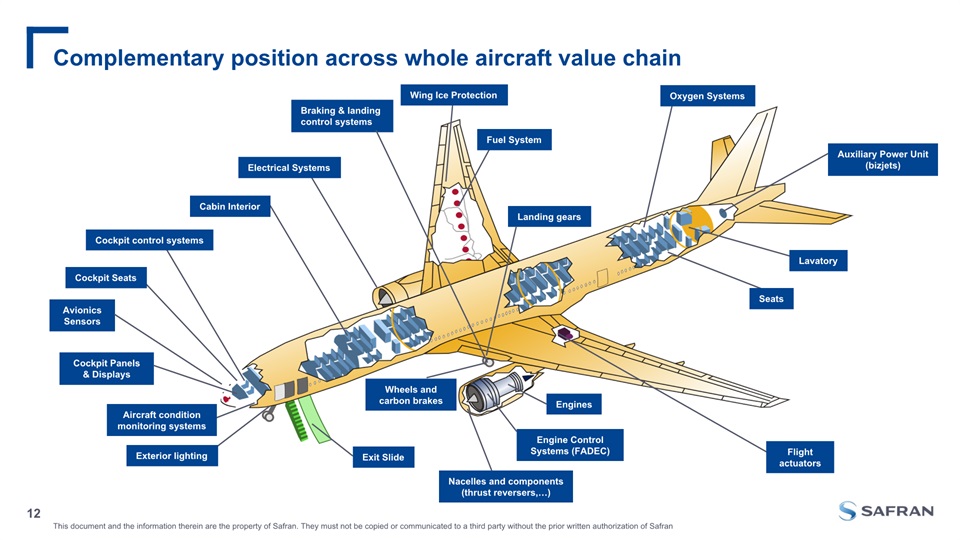

Complementary position across whole aircraft value chain Month/day/year 12 Avionics Sensors Cockpit Panels & Displays Exit Slide Auxiliary Power Unit (bizjets) Braking & landing control systems Wheels and carbon brakes Cockpit Seats Electrical Systems Lavatory Fuel System Nacelles and components(thrust reversers,…) Engine Control Systems (FADEC) Seats Exterior lighting Cockpit control systems Flight actuators Landing gears Aircraft condition monitoring systems Engines Oxygen Systems Cabin Interior Wing Ice Protection

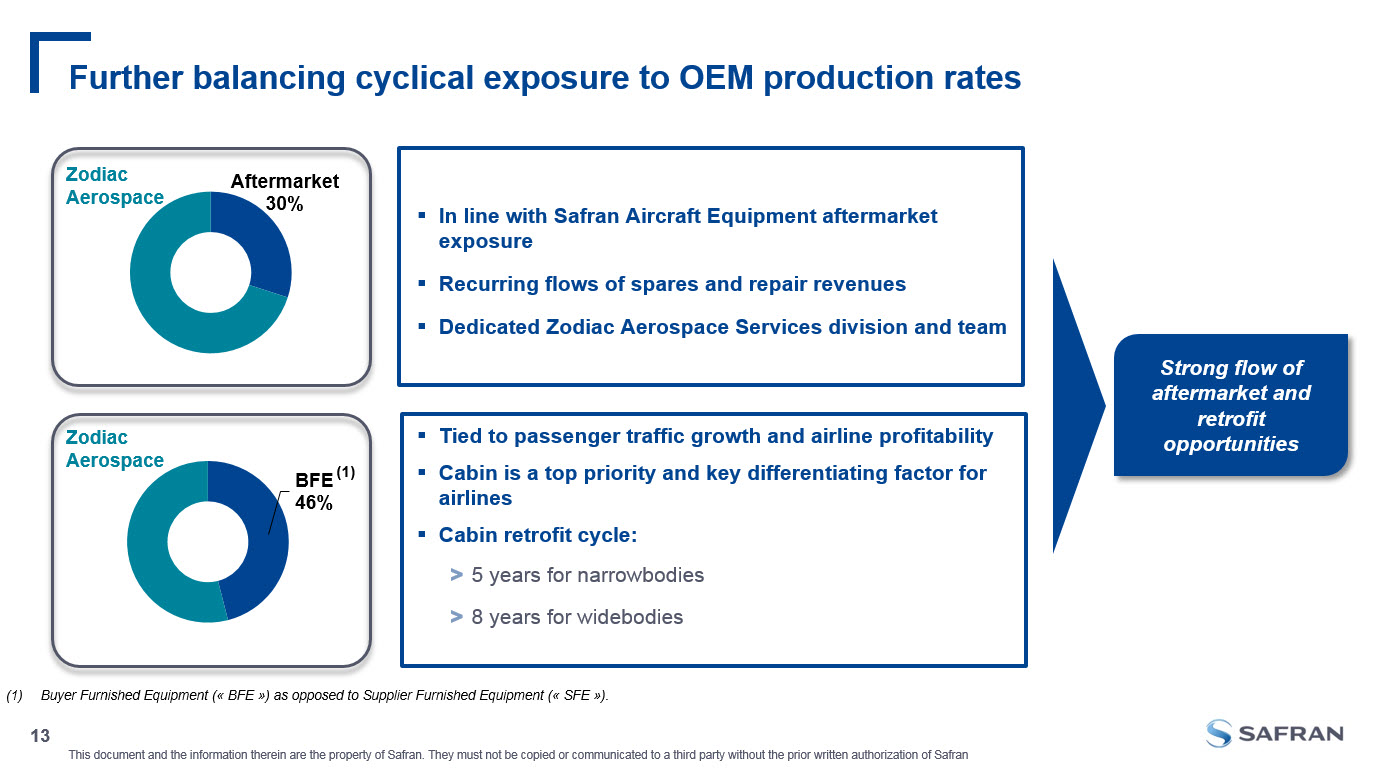

In line with Safran Aircraft Equipment aftermarket exposureRecurring flows of spares and repair revenuesDedicated Zodiac Aerospace Services division and team Further balancing cyclical exposure to OEM production rates Month/day/year 13 Buyer Furnished Equipment (« BFE ») as opposed to Supplier Furnished Equipment (« SFE »). Tied to passenger traffic growth and airline profitability Cabin is a top priority and key differentiating factor for airlinesCabin retrofit cycle:5 years for narrowbodies8 years for widebodies Strong flow of aftermarket and retrofit opportunities (1) Zodiac Aerospace Zodiac Aerospace

Positioned on all key programs: OEM / aftermarket, SFE/BFE Month/day/year 14 - 20 Seats 35 Seats 100 Seats 150 Seats 300 Seats + 500 Seats Nacelles Thrust Reverser Landing Gears Wheels and brakes Wiring Electrical Power Oxygen systems Fuel Systems Aerosafety Seats Cabin & Galleys BombardierGlobal Express BombardierChallenger 300 Dassault F7X Gulfstream V Embraer135 BombardierCRJ200 Embraer170/190/E2 SukkoïSuperjet 100 MRJ C-Series MS21 B737 A320 A330 B787 A350 B777 A340 B747 A380

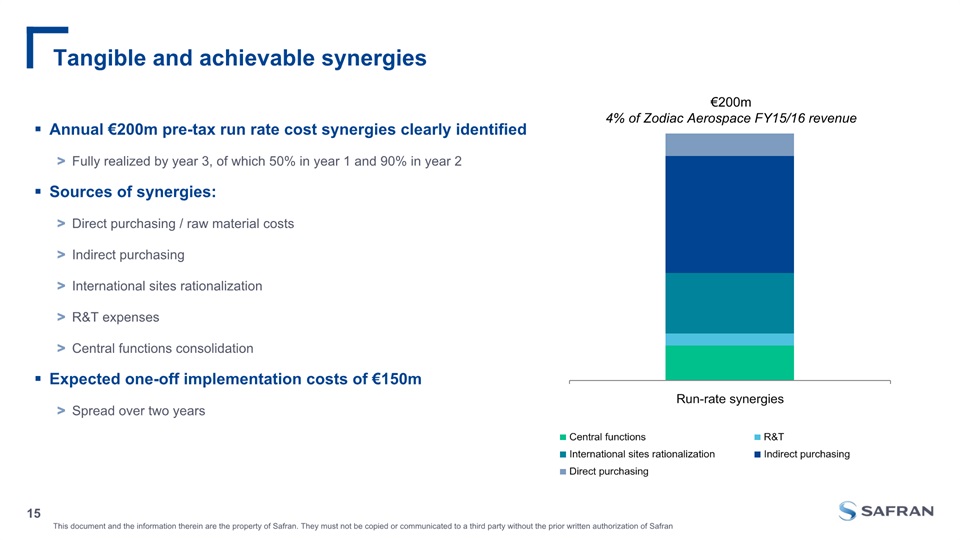

Annual €200m pre-tax run rate cost synergies clearly identifiedFully realized by year 3, of which 50% in year 1 and 90% in year 2Sources of synergies:Direct purchasing / raw material costsIndirect purchasingInternational sites rationalization R&T expenses Central functions consolidationExpected one-off implementation costs of €150mSpread over two years Tangible and achievable synergies 15 €200m4% of Zodiac Aerospace FY15/16 revenue

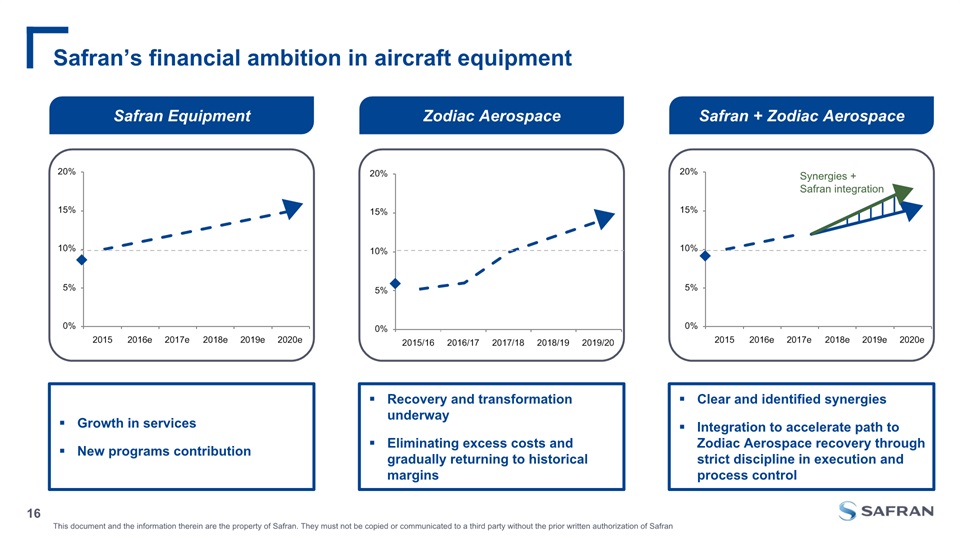

Safran’s financial ambition in aircraft equipment 16 Safran + Zodiac Aerospace Safran Equipment Zodiac Aerospace Growth in servicesNew programs contribution Recovery and transformation underwayEliminating excess costs and gradually returning to historical margins Clear and identified synergiesIntegration to accelerate path to Zodiac Aerospace recovery through strict discipline in execution and process control Synergies + Safran integration

ROCE post synergies above cost of capital within 3 years (2020) Safran’s financial acquisition criteria met 17 ROCE EPS Impact Balance Sheet Optimisation of balance-sheet structure while targeting an investment grade profileAdjusted net debt / adjusted EBITDA expected to be around 2.5x at closingRapid deleveraging expected (~0.5x / year) Double-digit EPS accretion(1) as of the first full fiscal year of consolidation (2019) Assuming 100% of targeted shares are tendered. Post phased synergies, before PPA and synergies costs of implementation.

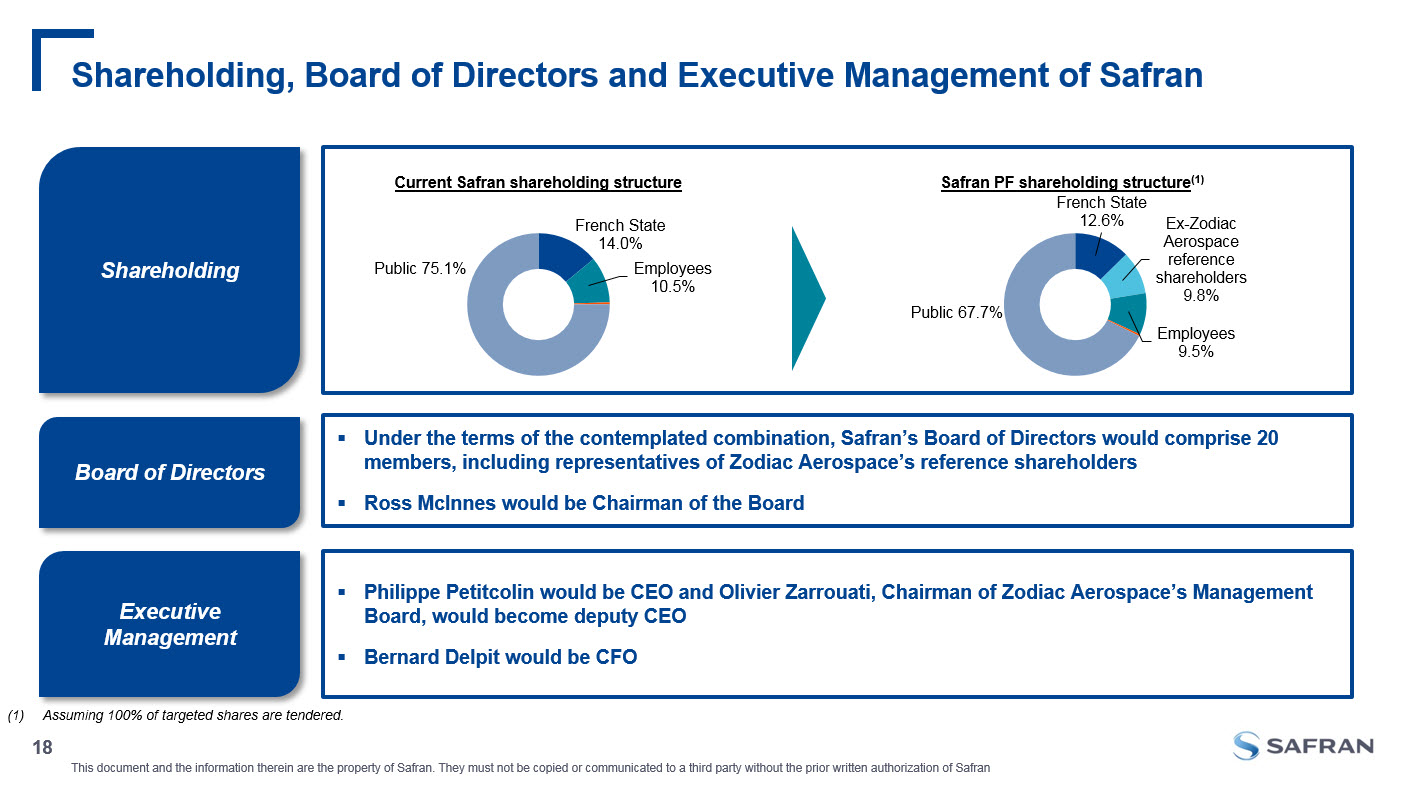

Under the terms of the contemplated combination, Safran’s Board of Directors would comprise 20 members, including representatives of Zodiac Aerospace’s reference shareholdersRoss McInnes would be Chairman of the Board Shareholding, Board of Directors and Executive Management of Safran 18 Board of Directors Executive Management Philippe Petitcolin would be CEO and Olivier Zarrouati, Chairman of Zodiac Aerospace’s Management Board, would become deputy CEOBernard Delpit would be CFO Shareholding Current Safran shareholding structure Safran PF shareholding structure(1) Assuming 100% of targeted shares are tendered.

LEAP transition:Focus on LEAP 1-A and LEAP 1-B EISRamp-up and production cost reductionContinued benefits from productivity improvement in Aircraft Equipment and Defense Key priorities Month/day/year 19 Maintain operational focus Post-transaction focus on strong organic growthBalance sheet disciplinePost-transaction Safran dividend practice unchanged Capital allocation Integration plan with Safran’s business units to be finalized in 2017Safran resources dedicated to Zodiac Aerospace integration identified Integration plan

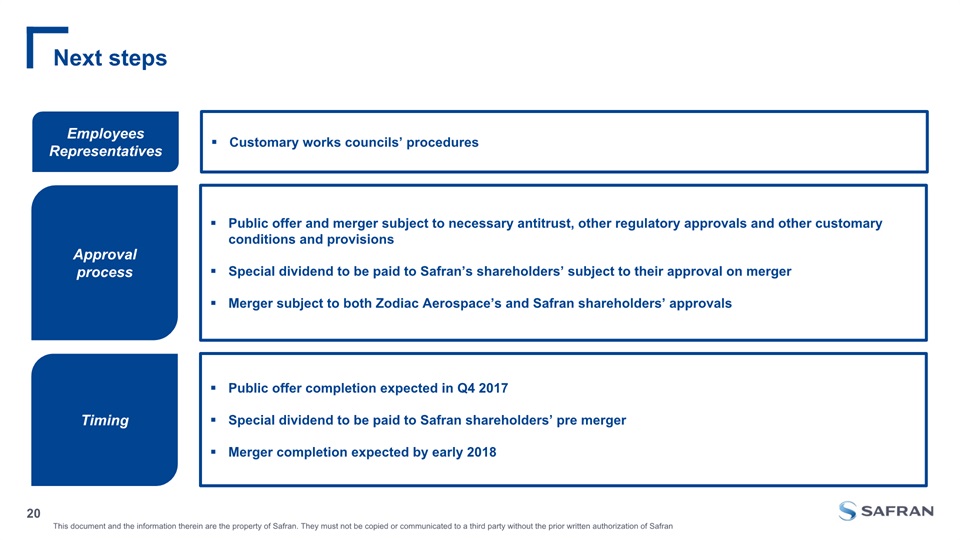

Public offer and merger subject to necessary antitrust, other regulatory approvals and other customary conditions and provisionsSpecial dividend to be paid to Safran’s shareholders’ subject to their approval on mergerMerger subject to both Zodiac Aerospace’s and Safran shareholders’ approvals Next steps Month/day/year 20 Approval process Public offer completion expected in Q4 2017Special dividend to be paid to Safran shareholders’ pre mergerMerger completion expected by early 2018 Timing Customary works councils’ procedures Employees Representatives

A global aerospace leader Month/day/year 21 Value creation through integration and synergies Balancing cyclical exposure to OEM production rates Comprehensive range of products : more value on aircraft Disciplined financial terms and execution

Month/day/year 22 Q&A