![]()

CONTENTS

| CEO’s Letter to Shareholders | 2 |

| Interview with the President & COO | 4 |

| Property Overview | 6 |

| Reserve & Resource Tables | 12 |

| MD&A | 18 |

| Financial Statements | 32 |

| OWNERSHIP | 100% |

| RESERVES | 976 Mt Mill @ 0.50% CuEq (0.20% Cu, 0.24 g/t Au, 1.73 g/t Ag) 82 Mt Heap @ 0.37 g/t Au, 2.55 g/t Ag |

| PROCESS | Conventional flotation and gold heap leach |

| MINE TYPE | Open pit |

| MINE LIFE | 23 years |

| LOCATION | 380 km (240 mi) northwest of Whitehorse, Yukon 560 km (350 mi) from year-round port at Skagway, Alaska |

| STATUS | Pre-feasibility study completed/Permitting Preparation/Exploration |

WESTERN COPPER IS A CANADIAN MINING EXPLORATION AND DEVELOPMENT COMPANY WITH A FULL PIPELINE OF PROJECTS, A STRONG CASH POSITION, NO DEBT AND AN EXPERIENCED MANAGEMENT TEAM.

| CEO’S LETTER TO THE SHAREHOLDERS |

Dear Shareholders,

2010 turned out to be a very good year for Western Copper Corporation. Our market capitalization, which was around $70 million mid-year, increased to $245 million by year-end and currently stands at $350 million.

After 2 years of intensive work at Casino, our flagship property, we more than doubled the size of the deposit to 2.8 billion tonnes. The numbers speak for themselves: measured, indicated and inferred resources consisting of 18 million ounces of gold, 10 billion pounds of copper, 1.3 billion pounds of molybdenum and 140 million ounces of silver. These numbers, most notably the 18 million ounces of gold, are impressive to say the least.

Throughout much of 2010, our engineering team worked on overhauling the existing pre-feasibility study for Casino. We released a significantly updated pre-feasibility study in early April 2011, which demonstrated the excellent economics of the project. At long term metal prices the project has an internal rate of return of 16.2 %, and 26.8 % at current metal prices. The project will cost $2.1 billion and will re-pay its capital in 3.3 years at long term metal prices and 2.1 years at current metal prices.

Casino is truly one of the world’s largest undeveloped copper, gold and molybdenum deposits. I am very proud of the great work that our technical team, including consultants, have done in bringing this project to its current level. The same team will now focus on the next step of completing a full feasibility and getting the project ready for permitting.

We are also continuing to advance our Carmacks copper project. Studies are underway that will address the concerns of the Water Board and it is our intent to re-submit our application later this year or early next year.

At Island Copper we are planning a comprehensive evaluation which will include a new resource estimate, a new geophysical survey and additional diamond drilling to better define the deposit; this information will be used to prepare a Preliminary Economic Assessment.

At Redstone, the geologic department of the University of British Columbia will be back in the field for their third year of assessing the potential of this exciting deposit.

Last year I noted that metal demand and prices were back to where they were prior to the 2009 financial crisis. This year it is safe to say that demand for all metalsand commodities in general has been remarkable.

| 02 | OVERVIEW |

| 2010 ANNUAL REPORT |

The major copper producers and producing nations are predicting that copper supplies will fall short of demand by 500,000 tonnes in 2011 and 2012 with little hope that supply and demand will be in balance in the foreseeable future. This is due to an unprecedented demand from China and other developing countries. Copper inventories currently stand at just under 600,000 tonnes; in China alone, total consumption is expected to reach over 7 million tonnes this year.

At the current projected world growth rate of 4%, it will require that 8 projects the size of Casino be built every year to meet demand. In other words, we expect that copper prices will continue to rise and that the current copper price will eventually prove to be conservative.

Western Copper has truly broken out in 2010, reaching new heights and entering anew league of development companies

As we work together to increase the company’s value even more so, the team is as focused and committed as ever to moving our projects forward to the benefit of our shareholders.

On behalf of the Board of Directors,

Dale CormanChairman and CEO

April 22, 2011

"AT THE CURRENT

PROJECTED WORLD

GROWTH RATE OF 4%,

IT WILL REQUIRE THAT

8 PROJECTS THE SIZE

OF CASINO BE BUILT

EVERY YEAR TO MEET

DEMAND"

| OVERVIEW | 03 | |

| 2010 ANNUAL REPORT |

| INTERVIEW WITH THEPRESIDENT& COO |  |

Q:What were the biggest high-lights of 2010, in your mind?

A:The key highlights from 2010 centered around our Casino project.

The new resource we issued in November was the result of an extensive program of drilling, re-logging, and re-modeling the deposit. The current resource figures raise the Casino project into a select group of very large world class copper-gold projects. The release of the new resource was followed by the pre-feasibility study update we released in early 2011, which cemented the robustness of the economics of Casino.

The other big highlight of 2010 was metal prices, with both copper and gold having a very strong year in 2010. Casino with 4.4 billion pounds of copper and 8.4 million ounces of gold in reserve is certainly an asset we are glad to have in this metal price environment.

Q:What was the biggest challenge of 2010?

A:Our biggest challenge during 2010 was keeping the company focused on Casino as our key project.

Having four excellent projects in our portfolio is certainly one of our strengths, but work on these projects needs to be managed carefully to ensure that our energies are directed on what will realize the most value to shareholders.

Q:What do you foresee as your biggest challenge for 2011?

A:For 2011, I see the key challenge as bringing the Island Copper project into active exploration while keeping the Casino project moving forward.

We think that the Island Copper project looks as strong as the Casino project; it’s just a couple of years behind.

We’ve got a great team in place already and we’re excited about bringing a second copper-gold project forward.

| 04 | OVERVIEW |

| 2010 ANNUAL REPORT |

Q:You ended the year by raising capital – how far will that take you and do you foresee another financing this year?

A:We may do a small flow-through financing this year to support the Island Copper project exploration program, but I don’t expect to do another large financing.

The $23 million we raised last year should easily support what we have planned for 2011 and bring us well into 2012.

Q:What distinguishes Western Copper from other companies in the junior copper space?

A:There are several things that distinguish Western Copper from other companies in the junior space.

First, is our rich portfolio of projects.

Not many junior mining companies can boast of having four excellent projects—particularly in the copper space.

Second is our team.

We have a strong internal team of engineers and geologists that can pick the right projects and move them forward quickly.

Last, is our track history.

Going back to the predecessor company, Western Silver, we’ve shown that we can build great shareholder value by taking projects from drill holes to feasibility and beyond, and we’re going to just keep working in that direction.

"NOT MANY JUNIOR

MINING COMPANIES CAN

BOAST OF HAVING FOUR

EXCELLENT PROJECTS

— PARTICULARLY IN THE

COPPER SPACE"

| OVERVIEW | 05 | |

| 2010 ANNUAL REPORT |

WORLD CLASS PROJECT IN THE YUKON

Casino

OVERVIEW

The Casino project is located 380 km northwest of Whitehorse, Yukon, within Selkirk First Nation traditional territory. Based on an updated pre-feasibility study completed in April 2011, the deposit will be developed as an open pit mine and a mill processing 120,000 tpd and producing an average of 435,000 ounces of gold, 234 million pounds of copper, 13 million pounds of molybdenum and 1.6 million ounces of silver per year over the first four years of production.

The pre-feasibility study recommends development of the Casino deposit as a conventional, electrified truck-shovel open pit mine. The initial development will focus on the deposit’s oxide cap as a heap leach operation to recover gold and silver in doré form. The main sulphide deposit will be processed using a conventional concentrator to produce copper-gold and molybdenum concentrates. Additionally, a pyrite rich stream from the concentrator will be leached in a CIL circuit for recovery of gold and silver. Copper-gold and molybdenum concentrates will be transported to the port of Skagway, Alaska for shipping to smelters.

NEXT STEPS

ADVANCE PROJECT FORWARD

- Initiate steps towards full feasibilitystudy

- Begin application for environmentalassessment

SECURE FINANCING

- Evaluate funding options

| 06 | OVERVIEW |

| 2010 ANNUAL REPORT |

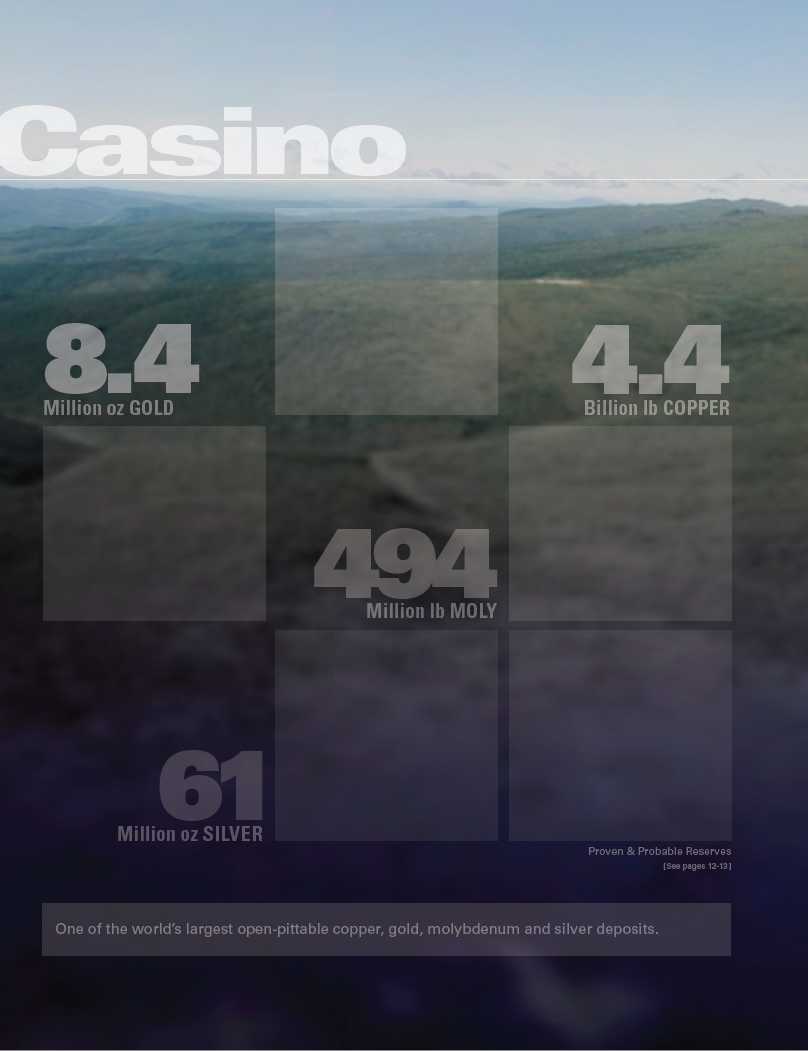

PROVEN + PROBABLE RESERVE

| GOLD | COPPER | MOLY | SILVER |

| 8.4 | 4.4 | 494 | 61 |

| Million oz | Billion lb | Million lb | Million oz |

[See pages 12-13]

SNAPSHOT

| OWNERSHIP | 100% |

| DEPOSIT TYPE | Porphyry |

| PROCESS | Conventional flotation mill + gold heap leach |

| MINE TYPE | Open pit |

| MINE LIFE | 23 years |

| EMPLOYEES | 608 (peak) and 1,600 during construction |

| LOCATION | 380 km (240 mi) northwest of Whitehorse, Yukon 560 km (350 mi) from year-round port at Skagway, Alaska |

| STATUS | Permitting preparation / Exploration / Pre-feasibility update / Planning towards full feasibility |

KEY DATA

| SPOT | LONG | |

| Mar 2011(1) | TERM(2) | |

| Total Capex (C$ M) | 2,130 | |

| Pre-Tax NPV @ 5% (C$ M) | 5,860 | 2,570 |

| Pre-Tax NPV @ 8% (C$ M) | 3,927 | 1,570 |

| Pre-Tax IRR (100% equity) (%) | 32.2% | 19.6% |

| After-Tax NPV @ 5% (C$ M) | 4,004 | 1,700 |

| After-Tax NPV @ 8% (C$ M) | 2,621 | 963 |

| After-Tax IRR (100% equity) (%) | 26.8% | 16.2% |

| Cash Flow (Y1-Y4) (C$ M/y) | 830 | 567 |

| Cash Flow (LOM) (C$ M/y) | 430 | 250 |

| Payback (y) | 2.1 | 3.3 |

| Cu Cash Cost (net of credits) (US$ /lb) | (0.49) | 0.06 |

Based on Pre-Feasibility Study - April 2011

Notes:

| 1. | Metal price: US$ 4.30/lb Copper, US$1,439/oz Gold, US$17.29/lb Moly, US$37.87/oz Silver Foreign Exchange: C$1.00 = US$1.00 |

| 2. | Metal price: US$ 2.78/lb Copper, US$1,222.22/oz Gold, US$15.56/lb Moly, US$18.89/oz Silver Foreign Exchange C$1.00 = US$1.00 |

| OVERVIEW | 07 | |

| 2010 ANNUAL REPORT |

READY FOR CONSTRUCTION

Carmacks

OVERVIEW

The project will be an open pit mine producing copper cathode on site by crushing, stacking, and heap leaching the ore and treating the leach solution through a solvent extraction/electrowinning (SX-EW) plant. Construction will require 2 years, followed by more than 6 years of production. Power for the project will be taken from the yukon power grid via an 11 km spur line. Acid will be produced on site by a 140 tpd acid plant.

NEXT STEPS

OBTAIN WATER USE LICENSE

- Anticipate water license issued in 2012

GET PROJECT READY FOR PRODUCTION

- Examine development options

| 08 | OVERVIEW |

| 2010 ANNUAL REPORT |

| PRODUCTION | CASH COST |

| 32 | 0.84 |

| Million lb Cu/yr | US$/lb Cu |

SNAPSHOT

| OWNERSHIP | 100% |

| RESERVE | 10.6 million tonnes (Proven + Probable) |

| PRIMARY METALS | Copper |

| PROCESS | Heap leach, solvent extraction/electrowinning |

| END PRODUCT | Copper cathode |

| MINE TYPE | Open pit |

| MINE LIFE | 6+ years |

| EMPLOYEES | 180 (peak production), 250 (peak construction) |

| LOCATION | 220 km north of Whitehorse, Yukon - 400 km from year-round port at Skagway, AK |

| INFRASTRUCTURE | Good road access, upgrade of a 13 km access road |

| POWER | 12 km from Yukon power grid |

| STATUS | Engineering / Permitting (Obtained license allowing construction) |

KEY DATA

| SPOT | LONG | |

| Apr 2011(1) | TERM(2) | |

| Total Capex (C$ M) | 151 | |

| Copper (C$ M) | 4.30 | 2.50 |

| Foreign Exchange (%) | 1.00 | 0.90 |

| Pre-Tax NPV @ 8% (C$ M) | 313 | 92 |

| Pre-Tax IRR (100% equity) (%) | 50.3 | 22.1 |

| After Tax NPV @ 8% (C$ M) | 193 | 49 |

| After Tax IRR (100% equity) (%) | 37.5 | 16.4 |

| Cash Flow (C$ M/y) | 94 | 49 |

| Payback (y) | 1.6 | 3.8 |

Based on Pre-Feasibility Study - May 2007

Notes:

| 1. | Metal price: US$ 4.30/lb Copper - Foreign Exchange C$1.00 = US$1.00 |

| 2. | Metal price: US$ 2.50/lb Copper - Foreign Exchange C$.90 = US$1.00 |

| OVERVIEW | 09 | |

| 2010 ANNUAL REPORT |

PRIME LOCATION

Island Copper

OVERVIEW

The project is located on Vancouver Island 29 km from the reclaimed BHP Island Copper Mine. Excellent infrastructure including parts of the BHP marine load-out and hydro power infrastructure remain in place.

The Island Copper porphyry copper-molybdenum-gold property consists of 216 mineral claims (approximately 42,669 hectares) and is comprised of the Hushamu, Red Dog and NW Expo deposits. After internal review of the project an exploration plan for 2011 has been put in place.

SNAPSHOT

| OWNERSHIP | 100% |

| DEPOSIT TYPE | Porphyry |

| PRIMARY METALS | Copper, gold, molybdenum and rhenium |

| MINE TYPE | Open pit |

| LOCATION | Vancouver Island (25 km west of Port Hardy, BC) |

| INFRASTRUCTURE | 29 km (18 mi) from infrastructure of Island Copper Mine tide water port and high voltage power |

| STATUS | Commencing exploration options |

| RESOURCE | 231 M tonnes @ 0.47 CuEq (0.28% Cu, 0.31 g/t Au) |

Based on Technical Report: April 2005

| MEASURED + INDICATED RESOURCE | |

| COPPER | GOLD |

| 1.4 | 2.3 |

| Million lb | Million oz |

[See page 15]

NEXT STEPS

CONTINUE EXPLORATION

- Induced polarization (IP) study

- 5,000 – 10,000 m of drilling

| 10 | OVERVIEW |

| 2010 ANNUAL REPORT |

ENORMOUS POTENTIAL

Redstone

OVERVIEW

The Redstone project is located 290 km south of Norman Wells, Northwest Territories and comprises discontinuous claims and leases stretching over approximately 100 km in a northwest-southeast orientation. The Redstone copper belt is essentially an unmetamorphasized succession that is locally well exposed in an arcuate belt less than 15 km wide and about 300 km long. The inferred resource is located on the Coates Lake leases, which represents a small proportion of the total area of mineral rights. Western Copper is currently in the midst of a three year project with the University of British Columbia’s (UBC) mineral deposit research unit to analyze the regional geology in order to develop our future exploration plans.

SNAPSHOT

| OWNERSHIP | 100% |

| DEPOSIT TYPE | Sediment-hosted straitiform copper deposit |

| RESOURCE | 34 Million t @ 4.0 CuEq (3.92% Cu, 9.0 g/t Ag) |

| METALS | Copper and silver |

| MINE TYPE | Underground |

| LOCATION | Nahanni Mining District, Northwest Territories claims and leases over approximately 160 km |

| STATUS | UBC project to study regional geology and identify area with good exploration potential |

Based on Technical Report: August 2005

| INFERRED RESOURCE | |

| COPPER | COPPER |

| 2.9 | 3.92 |

| Billion lb | % Grade |

[See page 15]

NEXT STEPS

CONTINUE EXPLORATION PROGRAM

- UBC to continue ongoing study ofregional geology

- Exploration program to be developedbased on UBC’s results

| OVERVIEW | 11 | |

| 2010 ANNUAL REPORT |

RESERVE & RESOURCE TABLES

CASINO

NI 43-101 Compliant Resource Estimate*

LEACHED CAP / OXIDE GOLD ZONE AT 0.25 g/t Au Cut-off

| Resource Grade | Contained Metal | |||||||||

| Category | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| Measured | 31 | 0.05 | 0.52 | 0.025 | 2.94 | 0.55 | 0.0 | 0.5 | 17 | 2.9 |

| Indicated | 53 | 0.03 | 0.33 | 0.017 | 2.36 | 0.36 | 0.0 | 0.6 | 20 | 4.0 |

| Measured + Indicated | 84 | 0.04 | 0.40 | 0.020 | 2.57 | 0.43 | 0.1 | 1.1 | 37 | 6.9 |

| Inferred | 17 | 0.01 | 0.31 | 0.008 | 1.93 | 0.27 | 0.0 | 0.2 | 3 | 1.1 |

SUPERGENE OXIDE ZONE AT 0.25% Cu EQ Cut-off

| Resource Grade | Contained Metal | |||||||||

| Category | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| Measured | 25 | 0.28 | 0.52 | 0.026 | 2.38 | 0.78 | 0.2 | 0.4 | 14 | 1.9 |

| Indicated | 36 | 0.23 | 0.21 | 0.019 | 1.44 | 0.48 | 0.2 | 0.2 | 15 | 1.7 |

| Measured + Indicated | 61 | 0.25 | 0.34 | 0.022 | 1.82 | 0.60 | 0.3 | 0.7 | 30 | 3.6 |

| Inferred | 26 | 0.26 | 0.17 | 0.010 | 1.43 | 0.44 | 0.1 | 0.1 | 6 | 1.2 |

SUPERGENE SULPHIDE ZONE AT 0.25% Cu EQ Cut-off

| Resource Grade | Contained Metal | |||||||||

| Category | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| Measured | 36 | 0.39 | 0.41 | 0.029 | 2.34 | 0.83 | 0.3 | 0.5 | 23 | 2.7 |

| Indicated | 216 | 0.24 | 0.22 | 0.019 | 1.72 | 0.50 | 1.1 | 1.5 | 90 | 11.9 |

| Measured + Indicated | 252 | 0.26 | 0.25 | 0.020 | 1.81 | 0.55 | 1.5 | 2.0 | 114 | 14.7 |

| Inferred | 102 | 0.20 | 0.19 | 0.010 | 1.49 | 0.39 | 0.5 | 0.6 | 23 | 4.9 |

HYPOGENE ZONE AT 0.25% Cu EQ Cut-off

| Resource Grade | Contained Metal | |||||||||

| Category | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| Measured | 32 | 0.32 | 0.38 | 0.026 | 1.94 | 0.72 | 0.2 | 0.4 | 19 | 2.0 |

| Indicated | 711 | 0.17 | 0.21 | 0.023 | 1.65 | 0.45 | 2.7 | 4.8 | 360 | 37.7 |

| Measured + Indicated | 743 | 0.18 | 0.22 | 0.023 | 1.66 | 0.46 | 2.9 | 5.2 | 379 | 39.7 |

| Inferred | 1568 | 0.14 | 0.16 | 0.020 | 1.36 | 0.37 | 4.8 | 8.1 | 691 | 68.6 |

| 12 | OVERVIEW |

| 2010 ANNUAL REPORT |

NI 43-101 Compliant Reserve Estimate**

| Reserve Grade | Contained Metal | |||||||||

| Class | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| MILL ORE Proven | 91 | 0.34 | 0.44 | 0.028 | 2.23 | 0.79 | 0.7 | 1.3 | 55 | 6.5 |

| MILL ORE Probable | 885 | 0.19 | 0.22 | 0.023 | 1.68 | 0.47 | 3.7 | 6.2 | 439 | 47.8 |

| MILL ORE TOTAL | 976 | 0.20 | 0.24 | 0.023 | 1.73 | 0.50 | 4.4 | 7.5 | 494 | 54.3 |

| Proven + Probable | ||||||||||

| HEAP LEACH Proven | 30 | 0.052 | 0.494 | - | 2.88 | n/a | 0.03 | 0.5 | - | 2.7 |

| HEAP LEACH Probable | 52 | 0.035 | 0.299 | - | 2.37 | n/a | 0.04 | 0.5 | - | 4.0 |

| HEAP LEACH TOTAL | 82 | 0.04 | 0.37 | - | 2.55 | n/a | 0.1 | 1.0 | - | 6.7 |

| Proven + Probable | ||||||||||

NOTES

| * | Supergene Oxide, Supergene Sulfide & Hypogene Zone cut-off 0.25% Cu Eq Leach Cap / Oxide Gold Zone cut-off 0.25 g/t Au |

Technical Report December 2010 - NI 43-101 Independent Qualified Person: Gary H. Giroux, P.Eng - Cu Eq Metal Prices: US$2.00/lb copper, US$875/oz gold, US$11.25/lb molybdenum | |

| ** | Technical Report May 2011 - NI 43-101 Independent Qualified Person: M. Hester FAusIMM - Cu Eq Metal prices: US$2.00/lb copper, US$875.00/oz gold and US$11.25/lb molybdenum |

| OVERVIEW | 13 | |

| 2010 ANNUAL REPORT |

CARMACKS

NI 43-101 Compliant Resource Estimate*

OXIDE

| Reserve Grade | Contained Metal | |||||||||

| Category | Tonnes M | Total Copper % | Oxide Copper % | Gold g/t | Silver g/t | CuEq % | Copper M lb | Gold k oz | Silver k oz | |

| Measured | 4.0 | 1.10 | 0.90 | 0.59 | 5.7 | 1.52 | 98 | 76 | 739 | |

| Indicated | 7.9 | 1.04 | 0.83 | 0.39 | 4.0 | 1.32 | 182 | 100 | 1,022 | |

| Measured + Indicated | 12.0 | 1.06 | 0.85 | 0.46 | 4.57 | 1.39 | 280 | 176 | 1,761 | |

| Inferred | 0.1 | 0.73 | 0.53 | 0.13 | 1.8 | 0.83 | 1 | 0 | 5 | |

SULPHIDE

| Reserve Grade | Contained Metal | |||||||||

| Category | Tonnes M | Total Copper % | Oxide Copper % | Gold g/t | Silver g/t | CuEq % | Copper M lb | Gold k oz | Silver k oz | |

| Measured | 0.7 | 0.80 | 0.02 | 0.26 | 2.5 | 0.99 | 12 | 6 | 56 | |

| Indicated | 3.6 | 0.74 | 0.03 | 0.21 | 2.3 | 0.89 | 59 | 25 | 270 | |

| Measured + Indicated | 4.3 | 0.75 | 0.03 | 0.22 | 2.33 | 0.91 | 72 | 30 | 325 | |

| Inferred | 4.0 | 0.71 | 0.01 | 0.18 | 1.9 | 0.84 | 63 | 23 | 246 | |

NI 43-101 Compliant Reserve Estimate**

| Reserve Grade | Contained Metal | |||||||||

| Class | Tonnes M | Total Copper % | Oxide Copper % | Gold g/t | Silver g/t | CuEq % | Copper M lb | Gold k oz | Silver k oz | |

| Proven | 3.2 | 1.23 | 1.028 | 0.659 | 6.20 | 1.70 | 86 | 68 | 636 | |

| Probable | 7.4 | 0.97 | 0.822 | 0.408 | 3.94 | 1.26 | 158 | 97 | 940 | |

| Proven & Probable | 10.6 | 1.04 | 0.88 | 0.48 | 4.62 | 1.39 | 222 | 165 | 1,576 | |

NOTES

| * | Technical Report: Wardrop, December 2007 - Qualified Person: G. Arsenau Ph.D., P.Geo & Scott Casselman P.Geo. - Total copper Cut-off: 0.25% - Cu Eq Metal prices: US$2.00/lb copper, US$875.00/oz gold, US$11.25/oz silver - Oxide resource estimate for Zones 1, 4 and 7. Sulphide resource estimate for Zone 1 - No discount for metallurgical recovery in contained metal figures |

| ** | Technical Report: May 2007 - Qualified Person: M. Hester FAusIMM - Cu Eq Metal prices: US$2.00/lb copper, US$875.00/oz gold, US$11.25/oz silver - Includes mining dilution |

| 014 | OVERVIEW |

| 2010 ANNUAL REPORT |

ISLAND COPPER

NI 43-101 Compliant Resource Estimate

| Resource Grade | Contained Metal | |||||

| Class | Tonnes M | Copper % | Gold g/t | CuEq % | Copper B lb | Gold M oz |

| Measured | 39 | 0.29 | 0.31 | 0.49 | 0.3 | 0.4 |

| Indicated | 192 | 0.27 | 0.31 | 0.47 | 1.1 | 1.9 |

| Measured + Indicated | 231 | 0.27 | 0.31 | 0.47 | 1.4 | 2.3 |

| Inferred | 53 | 0.28 | 0.38 | 0.52 | 0.3 | 0.6 |

NOTES

Technical Report: April 2005 - Qualified Persons: G. Giroux P. Eng. & D. Pawliuk P.Geo. - Total copper Cut-off: 0.20% - Cu Eq Metal prices: US$0.80/lb copper, US$350/oz gold - No discount for metallurgical recovery in contained metal figures

REDSTONE

NI 43-101 Compliant Resource Estimate

| Resource Grade | Contained Metal | |||||

| Class | Tonnes M | Copper % | Silver g/t | CuEq % | Copper M lb | Silver M oz |

| Inferred | 34 | 3.92 | 9.0 | 4.0 | 2,938 | 9.8 |

NOTES

Technical Report: August 2005 - Qualified Persons: A.W. Gourlay P.Geo. - 3.0% copper minimum assay intercept - Cu Eq Metal prices: US$2.00/lb copper, US$11.25/oz silver - No discount for metallurgical recovery in contained metal figures

| OVERVIEW | 15 | |

| 2010 ANNUAL REPORT |

MANAGEMENT

DISCUSSION & ANALYSIS

MANAGEMENT

DISCUSSION & ANALYSIS

MANAGEMENT DISCUSSION & ANALYSIS

The following management discussion and analysis of Western Copper Corporation (“Western Copper” or the “Company”) is dated March 24, 2011, and provides an analysis of the Company’s results of operations for the year ended December 31, 2010.

This discussion is intended to provide investors with a reasonable basis for assessing the financial performance of the Company as well as certain forward looking statements relating to its potential future performance. The information should be read in conjunction with the Western Copper Corporation December 31, 2010 audited annual consolidated financial statements and the related notes for the year then ended which have been prepared in accordance with Canadian generally accepted accounting principles. Western Copper’s accounting policies are described in note 2 of the December 31, 2010 audited annual consolidated financial statements. All of the financial information presented herein is expressed in Canadian dollars, unless otherwise indicated.

Western Copper is listed on the Toronto Stock Exchange (“TSX”) and the NYSE Amex under the symbol ‘WRN’. At March 24, 2011, the Company had 91,677,070 common shares outstanding.

Additional information on the Company can be found in the Company’s Annual Information Form (“AIF”), filed with Canadian regulators on SEDAR at www.sedar.com and with the United States Securities and Exchange Commission (the “SEC”) at www.sec.gov on Form 40-F.

The operations of the Company are highly speculative due to the high-risk nature of the mining industry. Western Copper faces risks that are generally applicable to its industry and others that are specific to its operations. Certain key risks affecting the Company’s current and future operations are discussed in its AIF and Form 40-F. This list is not exhaustive. Additional risks not currently known to the Company, or that the Company currently deems immaterial, may also impair the Company’s operations. If any of the risks actually occur, actual results could differ materially from those described in the forward looking statements contained in this management discussion and analysis. Reference is made to the discussion of forward-looking statements on page 27.

1. DESCRIPTION OF BUSINESS

Western Copper Corporation is a Canadian-based publicly-traded mineral exploration company with a primary focus of advancing its mineral properties towards production.

All of Western Copper’s properties are located in Canada. The Company’s two most advanced projects are located in the Yu-kon. The Casino project is one of the largest undeveloped porphyry deposits in Canada. Western Copper is currently working on updating the pre-feasibility study that it completed on the project in June 2008. The Carmacks Copper Project is in the last phase of permitting.

2. QUARTERLY SUMMARY OF ACTIVITIES

Significant increase to the Casino Project’s Mineral Resource Estimate

On November 1, 2010, Western Copper announced an updated resource estimate for the Casino Project. The new resource estimate is the first estimate to include the 26,000 metres of drilling performed by Western Copper over the past three years and represents a significant update to the resource estimated in 2008. In addition to the inclusion of the new drilling, the new estimate includes a re-interpretation of the geology of the deposit, which includes the re-logging of 90,000 metres of core.

| 18 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

Financing

On December 22, 2010, Western Copper issued 9,395,500 units at a price of $2.45 for gross proceeds of approximately $23 million. Each unit comprised one common share of the Company and half of one warrant. Each whole warrant is exercisable for one common share of the Company at a price of $3.45 and expires on December 22, 2012.

NYSE Amex Listing

Western Copper began trading on the New York Stock Exchange (“NYSE”) Amex on February 9, 2011 under the symbol ‘WRN’, the same symbol that the Company trades under on the TSX.

Carmacks Copper Project Water Use License Appeal Decision

On February 24, 2011, Western Copper received notification of the Yukon Supreme Court’s ruling regarding the Company’s appeal of the Yukon Water Board’s decision not to grant the Carmacks Copper Project a Water Use License. Western Copper had appealed the Yukon Water Board’s decision in order to clarify the rules it would have to follow for re-application of a Water Use License.

3. PROPERTY OVERVIEW

Casino (Yukon, Canada)

The Casino porphyry copper-gold-molybdenum deposit is located 300 kilometres northwest of Whitehorse, Yukon. It has been the subject of considerable exploration going back to 1967.

Should Western Copper make a production decision on the property, it is required to make a cash payment of $1 million. Production on the claims is also subject to a 5% net profits interest.

In June 2008, Western Copper announced that an independent pre-feasibility study on the Casino property supports the development of the project.

On November 1, 2010, Western Copper announced an updated resource estimate for the Casino Project. The new resource estimate is the first estimate to include the 26,000 metres of drilling performed by Western Copper over the past three years and represents a significant update to the resource estimated in 2008. In addition to the inclusion of the new drilling, the new estimate includes a re-interpretation of the geology of the deposit, which includes the re-logging of 90,000 metres of core under the direction of Jack McClintock, Consulting Geologist for Western Copper. The NI 43-101 technical report was filed on December 1, 2010.

The goal of the drilling campaign, to increase the near-surface supergene sulfide zone, was achieved. The size of this zone has increased from 133 million tonnes to 252 million tonnes at the measured and indicated level – an increase of 90% (Table 1).

The largest increase to the resource comes at the inferred level of categorization. The combined supergene oxide, super-gene sulphide, and hypogene inferred resource, at a 0.25% Copper Equivalent (“CuEq”) cutoff grade has been increased over 6 times to 1.70 billion tonnes (Table 2). The most recent results have added 7.4 million ounces of gold, 4.4 billion pounds of copper, and 615 million pounds of molybdenum to the resource at the inferred level.

The increase in supergene mineralization should result in higher grades at the beginning of the mine life and a lower strip ratio. Both of these factors are expected to improve the project’s economics. Western Copper plans to release the results of an updated pre-feasibility near the end of March 2011.

Other than the new resource estimate, the updated pre-feasibility is expected to include an increased throughput of 120,000 tonnes per day, the use of natural gas for power generation, and a new road route, among other items.

| MANAGEMENT DISCUSSION &ANALYSIS | 19 | |

| 2010 ANNUAL REPORT |

Following the release of the updated pre-feasibility study results, the Company will refine the engineering on metallurgy, geo-technical, and infrastructure and other aspects of the project with a view of progressing the Casino Project to the feasibility study stage by the end of 2012.

The Company will also continue its environmental programs in 2011 with a view of submitting the application to the Yukon Environmental and Socio-Economic Board (“YESAB”) by the end of 2012.

Table 1: Supergene Sulphide Zone Measured & Indicated Resource

Supergene Sulfide Zone (2010 Estimate)

| Class | Cutoff CuEq (%) | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % |

| Measured | 0.25% | 36 | 0.39 | 0.41 | 0.029 | 2.34 | 0.84 |

| Indicated | 0.25% | 216 | 0.24 | 0.22 | 0.019 | 1.72 | 0.50 |

| Total Measured + Indicated | 252 | 0.26 | 0.25 | 0.021 | 1.81 | 0.55 |

Supergene Sulfide Zone (2008 Estimate)

| Class | Cutoff CuEq (%) | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % |

| Measured | 0.25% | 33 | 0.39 | 0.47 | 0.030 | – | 0.87 |

| Indicated | 0.25% | 100 | 0.29 | 0.25 | 0.020 | – | 0.56 |

| Total Measured + Indicated | 133 | 0.31 | 0.31 | 0.020 | – | 0.63 |

Table 2: Inferred Resource of combined Supergene Oxide, Supergene Sulphide, and Hypogene Zones at 0.25% CuEq Cut-off

| Estimate | Tonnes M | Copper % | Gold g/t | Moly % | Silver g/t | CuEq % | Copper B lb | Gold M oz | Moly M lb | Silver M oz |

| New (2010) | 1,696 | 0.14 | 0.16 | 0.019 | 1.37 | 0.37 | 5.2 | 8.7 | 711 | 74.7 |

| Old (2008) | 232 | 0.16 | 0.18 | 0.019 | – | 0.38 | 0.8 | 1.3 | 95 | – |

| • | Gary Giroux, P.Geo. is the independent qualified person responsible for the preparation of the updated Mineral Resource estimate and the 2008 Mineral Resource estimate. | |

| ||

| • | The Copper Equivalent grade has been calculated using the following commodity prices: US$2.00/lb copper, US$875/oz gold, US$11.25/lb molybdenum, US$11.25/oz silver, and assuming 100% metallurgical recoveries. | |

| ||

| • | The 2008 Mineral Resource estimate Copper Equivalent grade has been calculated using the following commodity prices: US$0.80/lb copper, US$350/oz gold, US$4.50/lb molybdenum, and assuming 100% metallurgical recoveries. | |

| • | There has been no discount for metallurgical recovery in contained metal figures. |

Carmacks Copper Project (Yukon, Canada)

The Carmacks Copper Project is located 220 kilometres north of Whitehorse, Yukon.

In 2007, Western Copper reported the key findings of its feasibility study on the project and announced that the study supports the development of the mine. Based on the proven and probable reserve estimate of 10.6 million tonnes, the mine has an estimated six year ore production life. The feasibility study indicated initial capital development costs of $144 million, including a contingency of $14.1 million. An additional sum of $7.3 million is attributable to owner’s costs, which include the Company’s project team salaries, spare parts, and bond costs. The life-of-mine operating costs were estimated to be $0.98/ lb. of copper (US$0.84/lb. of copper at 0.85 US$/$). Using a copper price of US$2.32 per pound and an exchange rate of 0.85 US$/$, the feasibility study indicated a pre-tax IRR of 21.1% for the project.

| 20 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

In April 2009, Western Copper received the Quartz Mining License (“QML”) for the Carmacks Copper Project. This license permits the Company to begin construction of the Carmacks Copper Mine and establishes many of the terms and conditions under which the mine will operate.

The Water Use License (“WUL”) is the next and final permit required to build and operate the Carmacks Copper Project.

On May 10, 2010, Western Copper was notified by the Yukon Water Board (“Water Board”) that the Carmacks Copper Project would not receive the WUL under the current application. The Company subsequently filed a Petition with the Yukon Supreme Court appealing certain aspects the Water Board decision in order to clarify the rules it would have to follow to reapply for a Water Use License. The appeal hearing concluded on December 9, 2010.

On February 24, 2011, the Yukon Supreme Court ruled that the Water Board is not required to accept the findings of the YESAB which concluded that the project can be built and operated without significant environmental effect. Western Copper is considering the decision and will review its options before submitting a new WUL application.

Any production from the Carmacks Copper Project is subject to either a 15% net profits interest or a 3% net smelter royalty, at Western Copper’s election. If Western Copper elects the net smelter royalty, it has the right to purchase the royalty for $2.5 million, less any advance royalty payments made to that date. The Company is required to make an advance royalty payment of $100,000 for any year in which the average daily copper price reported by the London Metal Exchange is US$1.10 per pound or greater. As at the date of this report, Western Copper has made $800,000 in advance royalty payments.

Island Copper (British Columbia, Canada)

The Island Copper property consists of three blocks of mineral claims in a prospective copper-gold porphyry belt located on northern Vancouver Island, approximately 25 kilometres west of Port Hardy and 360 kilometres northwest of Vancouver, Brit-ish Columbia. The mineral claim blocks are referred to as the Hushamu claims, the Apple Bay claims, and the Rupert Block.

In 2008, Western Copper exercised its option on the Apple Bay claims and now owns 100% interest in all three mineral claim blocks that comprise the Island Copper property. An unrelated third party maintains the right to explore the Apple Bay claims for non-metallic minerals.

From August 2008 to July 2010, the Island Copper property was under option, most recently with Kobex Minerals Inc. (“Ko-bex”). On July 15, 2010, Kobex terminated its rights to earn-in to the property.

In 2011, Western Copper intends to restart exploration activities at the Island Copper property. The program will likely include geophysical surveying and drilling.

Should a production decision be made on the Hushamu claims, Western Copper is required to make a cash payment of $1 million to an unrelated third party within 60 days of the production decision. These mineral claims are also subject to a 10% net profits interest.

Should a production decision be made on the Apple Bay claims, Western Copper is required to pay $800,000 in cash or in Western Copper stock to an unrelated third party. The payment method is at the election of Western Copper.

Redstone (Northwest Territories, Canada)

The Redstone property comprises five mining leases and 15 mineral claims in six distinct areas in the Nahanni Mining District southwest of Norman Wells in the Northwest Territories.

In 2007, the Company signed an agreement with the Mineral Deposits Research Unit at the University of British Columbia (“MDRU”) to fund a research program that will aim to provide a better understanding of the regional geology and to identify the areas covered by the Company’s existing claims and leases that offer the most exploration potential.

MDRU spent the summers of 2009 and 2010 collecting data at and around the property. MDRU will continue its research in 2011. The field portion of the research program is expected to conclude in 2011.

| MANAGEMENT DISCUSSION &ANALYSIS | 21 | |

| 2010 ANNUAL REPORT |

The only area that presently has a NI 43-101 compliant resource estimate is the Coates Lake area. This area consists of the five mining leases noted above. Should production be initiated at Coates Lake, the five mining leases are subject to a net smelter royalty of between 3-4% depending on the monthly average of the final daily spot price of copper reported on the New York Commodities Exchange relating to each production month, as follows:

| • | 3% if the price is less than, or equal to US$0.75 per pound; | |

| • | 3.5% if the price is greater than US$0.75 per pound, but less than, or equal to US$1.00 per pound; and | |

| • | 4% if the price is greater than US$1.00 per pound. |

4. SELECTED QUARTERLY FINANCIAL INFORMATION

The following quarterly information has been extracted from the Company’s unaudited interim consolidated financial statements.

| As at and for the quarter ended | 31-Dec-10 | 30-Sep-10 | 30-Jun-10 | 31-Mar-10 | ||||||||

| Expressed in Canadian dollars | $ | $ | $ | $ | ||||||||

| Loss and comprehensive loss | 665,986 | 573,719 | 775,448 | 761,826 | ||||||||

| Loss per share – basic and diluted | 0.01 | 0.01 | 0.01 | 0.01 | ||||||||

| Mineral properties | 85,330,161 | 84,307,328 | 80,893,851 | 75,376,844 | ||||||||

| Cash, cash equivalents, and short-term investments | 23,636,895 | 3,728,713 | 8,232,576 | 10,798,525 | ||||||||

| Total assets | 109,377,291 | 88,500,931 | 89,688,423 | 87,003,474 |

| As at and for the quarter ended | 31-Dec-09 | 30-Sep-09 | 30-Jun-09 | 31-Mar-09 | ||||||||

| Expressed in Canadian dollars | $ | $ | $ | $ | ||||||||

| Loss and comprehensive loss | 233,672 | 509,122 | 594,590 | 522,773 | ||||||||

| Loss per share – basic and diluted | – | 0.01 | 0.01 | 0.01 | ||||||||

| Mineral properties | 72,790,644 | 70,960,998 | 67,117,675 | 65,970,008 | ||||||||

| Cash, cash equivalents, and short-term investments | 13,667,179 | 11,786,066 | 10,931,098 | 12,177,922 | ||||||||

| Total assets | 86,876,176 | 83,316,052 | 78,478,161 | 78,503,650 |

The quarterly fluctuations are due to the following:

Loss and Comprehensive Loss

The loss for the three months ended December 31, 2010 is in-line with the loss figures from September 30, 2010 and from March 31, 2009 to September 30, 2009. This is the approximate loss figure expected on a quarterly basis.

Loss and comprehensive loss is higher for the quarter ended June 30, 2010 than the previous quarters due to payments relating to changes in management.

Loss and comprehensive loss is higher during the period ended March 31, 2010 than the previous quarters because Western Copper issued and donated common shares in February 2010. The fair value of the common shares totaled $117,900 and was recorded as an office and administration expense.

Loss and comprehensive loss for the quarter ended December 31, 2009 is lower than the other quarters due to a future income tax recovery of $396,000 recorded during the quarter.

| 22 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

Mineral Properties

The Company continues to incur expenditures that add value to its mineral properties. As a result, the carrying value of the mineral properties has increased in every quarter presented above.

Cash, Cash Equivalents, and Short-term Investments

Cash is being spent to fund ongoing operations and to increase the value of the Company’s mineral properties. This has led to a decrease in cash, cash equivalents and short-term investments in the quarters presented above with the exception of the three months ended September 30, 2009, December 31, 2009, and December 31, 2010. Cash, cash equivalents and short-term investments increased in those quarters because the Company raised funds through private placements and public financings. The Company raised gross proceeds of $9.4 million and $23 million in 2009 and in 2010, respectively.

Total Assets

Because most dollars spent are capitalized to mineral properties, there has been no significant impact on total assets unless there is a financing. Total assets increased significantly in quarters when a financing occurred. Otherwise, the figure has remained relatively constant in all quarters presented.

5. RESULTS OF OPERATIONS

| For the quarter ended December 31, | 2010 | 2009 | 2008 | ||||||

| Expressed in Canadian dollars | $ | $ | $ | ||||||

| ADMINISTRATIVE EXPENSES | |||||||||

| Accounting and legal | 173,422 | 196,078 | 400,035 | ||||||

| Filing and regulatory fees | 80,882 | 72,728 | 78,101 | ||||||

| Office and administration | 2,116,235 | 1,800,325 | 1,921,138 | ||||||

| Shareholder communication | 462,391 | 414,303 | 354,521 | ||||||

| LOSS BEFORE TAXES AND OTHER ITEMS | 2,832,930 | 2,483,434 | 2,753,795 | ||||||

| OTHER ITEMS | |||||||||

| Foreign exchange | 1,735 | 10,786 | 51,731 | ||||||

| Interest income | (57,686 | ) | (238,166 | ) | (599,575 | ) | |||

| Write-off of mineral properties | – | – | 405,001 | ||||||

| LOSS BEFORE TAXES | 2,776,979 | 2,256,054 | 2,610,952 | ||||||

| Future income tax recovery | – | (395,897 | ) | (451,703 | ) | ||||

| LOSS AND COMPREHENSIVE LOSS | 2,776,979 | 1,860,157 | 2,159,249 |

| MANAGEMENT DISCUSSION &ANALYSIS | 23 | |

| 2010 ANNUAL REPORT |

Western Copper had a loss of $2.78 million ($0.03 per common share) for the year ended December 31, 2010 compared to a loss of $1.86 million ($0.02 per common share) in for the year ended December 31, 2009. Although the scale and nature of the Company’s administrative activity have remained consistent throughout 2009 and 2010, there are a number of items that have led to differences in the loss and comprehensive loss figures.

Western Copper recorded a future income tax recovery of $396,000 in 2009 as a result of changes in future tax rates. There was no such recovery in 2010.

Decreasing cash and short-term investment balances and lower interest rates led to a decline in interest income of $180,000 in 2010 as compared to 2009. Western Copper earns interest on its short-term investments, but as the Company uses its working capital to fund operations and mineral property development, its interest bearing balances decrease, leading to lower interest income until the Company’s next financing. Western Copper raised approximately $23 million in gross proceeds in December 2010. As a result, interest income is expected to increase slightly in 2011.

In February 2010, Western Copper made a donation of 90,000 common shares to the University of British Columbia’s Earth Systems Science Building. The fair value of the common shares totaled $117,900 and was recorded as an office and administration expense. There was no such expense in 2009.

| For the quarter ended December 31, | 2010 | 2009 | ||||

| Expressed in Canadian dollars | $ | $ | ||||

| ADMINISTRATIVE EXPENSES | ||||||

| Accounting and legal | 34,644 | 36,949 | ||||

| Filing and regulatory fees | 4,552 | 6,655 | ||||

| Office and administration | 541,119 | 482,521 | ||||

| Shareholder communication | 99,662 | 143,528 | ||||

| LOSS BEFORE TAXES AND OTHER ITEMS | 679,977 | 669,653 | ||||

| OTHER ITEMS | ||||||

| Foreign exchange | 430 | 243 | ||||

| Interest income | (14,421 | ) | (40,327 | ) | ||

| LOSS BEFORE TAXES | 665,986 | 629,569 | ||||

| Future income tax recovery | – | (395,897 | ) | |||

| LOSS AND COMPREHENSIVE LOSS | 665,986 | 233,672 |

Western Copper had a loss of $666,000 ($0.01 per common share) for the three months ended December 31, 2010. For the same period in 2009, the Company had a loss of $234,000 (less than $0.01 per common share).

The most significant reason for the difference is the future income tax recovery recorded in 2009 as a result of a change in future tax rates. There is no such expense in 2010.

| 24 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

6. LIQUIDITY AND CAPITAL RESOURCES

| For the year ended December 31, | 2010 | 2009 | 2008 | ||||||

| Expressed in Canadian dollars | $ | $ | $ | ||||||

| CASH PROVIDED BY (USED IN) | |||||||||

| Operating activities | (2,339,148 | ) | (1,793,475 | ) | (1,735,717 | ) | |||

| Financing activities | 24,784,204 | 8,956,411 | 500 | ||||||

| Investing activities | (24,250,489 | ) | (8,764,009 | ) | (16,954,526 | ) | |||

| INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | (1,805,433 | ) | (1,601,073 | ) | (18,689,743 | ) | |||

| Cash and cash equivalents – beginning of the year | 3,436,131 | 5,037,204 | 23,726,947 | ||||||

| CASH AND CASH EQUIVALENTS – ENDING | 1,630,698 | 3,436,131 | 5,037,204 |

In addition to its cash and cash equivalents, the Company had $22 million in short-term investments at year-end. As at December 31, 2010, cash, cash equivalents, and short-term investments total $23.6 million. As at December 31, 2009, cash, cash equivalents, and short-term investments total $13.7 million. The figure increased $10 million in 2010 because of the Company raised net proceeds of $21.6 million on December 22, 2010 and received $2.5 million as a result of warrants exercised in 2010 while spending approximately $15 million on exploration and development costs and administrative expenses. Net proceeds from financing activities only totaled $9.0 million in 2009.

Cash and cash equivalents comprise cash deposits held at banks. Short-term investments consist of Guaranteed Investment Certificates (“GIC”) from Canadian chartered banks that are cashable at the Company’s discretion without penalty.

Western Copper is an exploration stage enterprise. As at December 31, 2010, the Company has not earned any production revenue. It depends heavily on its working capital balance and its ability to raise funds through capital markets to finance its operations.

Based on its current estimates, management expects that Western Copper will have sufficient working capital to fund its administrative expenses and its mineral property costs in 2011. The Company will have to raise significant additional capital in order to build any of its projects.

The financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company’s ability to continue as a going concern is substantially dependent on its ability to raise funds necessary to acquire assets, perform exploration and development activities, and conduct its corporate affairs primarily through the issuance of its common shares. There is a risk that in the future the Company may not be able to raise the capital required to fund operations. .

Operating Activities

The significant components of operating activities are discussed in the Results of Operations section above.

Financing Activities

On December 22, 2010, Western Copper raised gross proceeds of $23 million dollars by issuing 9,395,500 units at a price of $2.45. Each unit comprised one common share of the Company and half of one warrant.

| MANAGEMENT DISCUSSION &ANALYSIS | 25 | |

| 2010 ANNUAL REPORT |

On July 10, 2009, the Company issued 4 million units at a price of $1.00 per unit. Each unit comprised one flow-through common share and half of one warrant. On December 4, 2009, the Company issued 2.15 million units at a price of $2.50 per unit. Each unit comprised one flow-through common share and a whole warrant.

In May 2010, the expiration date of the investor warrants issued as part of the July 2009 private placement was accelerated from July 2012 to June 2010. As a result, Western Copper received $2.46 million from the exercise of 1,964,000 warrants during the year ended December 31, 2010. During the year ended December 31, 2009, the Company received $251,000 from the exercise of broker warrants relating to the July 2009 financing.

The Company received $695,000 from the exercise of stock options during the year ended December 31, 2010. During the year ended December 31, 2009, Western Copper received $107,000 from the exercise of stock options. The amount of stock options exercised increased in 2010 when compared to the previous year due to the timing of stock option expiry dates and an increase in Western Copper’s share price during the second half of 2010.

Investing Activities

Investing activities include both mineral property expenditures and purchases of short-term investments. In December, the Company transferred approximately $20 million received from the financing into short-term investments from cash and cash equivalents. Until the December transfer, the Company had divested $8 million in short-term investments in 2010 to pay for the exploration and on-going permitting activities at the Casino Project. In 2009, the Company purchased $2.23 million in short-term investments

The Company expended $12.5 million on mineral property expenditures during 2010. This compares with $6.5 million during 2009. The majority of these costs were spent on the exploration and permitting programs at the Casino Project. The scope of both of these programs was twice as much in 2010 compared to 2009.

A summary of activities relating to each project is available under the Property Overview section at the beginning of this document.

7. CONTRACTUAL OBLIGATIONS

The Company leases office space in Vancouver, British Columbia and Whitehorse, Yukon. The future minimum lease payments by calendar year are approximately as follows:

| Expressed in Canadian Dollars | Vancouver | Whitehorse | ||||

| $ | $ | |||||

| 2011 | 210,288 | 28,635 | ||||

| 2012 | 212,313 | - | ||||

| 2013 | 215,149 | - | ||||

| 2014 | 90,489 | - | ||||

| Thereafter | - | - | ||||

| TOTAL | 728,239 | 28,635 |

Western Copper has no debt and does not pay dividends.

The Company has no material off-balance sheet arrangements, no material capital lease agreements and no material long term obligations other than those described above or in the description of mineral properties contained in the consolidated financial statements.

Neither the Company nor any of its subsidiaries has any externally imposed capital requirements.

| 26 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

8. SIGNIFICANT ACCOUNTING ESTIMATES

Use of Estimates

The preparation of the consolidated financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the financial statements and the related notes. Significant areas where management’s judgment is applied include the assessment of impairment to the carrying value of mineral properties, the determination of the likelihood that future income tax benefits can be realized, the assumptions used to calculate the fair value of warrants and stock options, amounts and likelihood of contingent liabilities, and the cost allocation methodologies used to determine results of operations, the value of financing components, and the value of purchased assets. Actual results could differ from the estimates by a material amount.

Mineral Properties

Direct costs related to the acquisition, exploration, and development of mineral properties owned or controlled by the Company are deferred on an individual property basis until the viability of a property is determined or until the property is sold, abandoned, placed into production or determined to be impaired. Administration costs and general exploration costs are expensed as incurred. If a property is placed into commercial production, deferred costs will be amortized using the unit-of production method based on proven and probable reserves. The carrying amount for mineral properties represents costs net of write-downs to date and does not necessarily reflect present or future values. Recovery of capitalized costs is dependent on successful development of economic mining operations or the disposition of the related mineral properties.

The Company reviews the carrying value of mineral properties when there are events or changes in circumstances that may indicate impairment. Where estimates of future cash flows are available, an impairment charge is recorded if the undiscounted future net cash flows expected to be earned from the property are less than the carrying amount. Reductions in the carrying value of properties are recorded to the extent the net book value of the property exceeds management’s estimate of fair values.

Fair value is determined with reference to discounted estimated future cash flow analysis or on recent transactions involving dispositions of similar properties.

The estimated cash flows used to assess recoverability of certain of the Company’s mineral property carrying values are developed using management’s projections for long-term average copper, gold and molybdenum prices, recoverable reserves, operating costs, capital expenditures, reclamation costs, and applicable foreign currency exchange rates. Management makes estimates relating to current and future market conditions. There are inherent uncertainties related to these factors and management’s judgment when using them to assess mineral property recoverability.

The Company believes that the estimates applied in the impairment assessment are reasonable; however such estimates are subject to significant uncertainties and judgments. Although management has made its best estimate of these factors based on current conditions, it is possible that the underlying assumptions can change significantly and impairment charges may be required in future periods. Such charges could be material.

Asset Retirement Obligation

The fair value of a liability for an asset retirement obligation (“ARO”), such as site closure and reclamation costs, is recognized in the period in which it is incurred if a reasonable estimate of fair value can be made. The Company is required to record the estimated present value of future cash flows associated with site closure and reclamation as a long-term liability and increase the carrying value of the related assets for that amount. Subsequently, these asset retirement costs will be amortized to expense over the life of the related assets. At the end of each period, the liability is revised to reflect the passage of time and changes in the estimated future cash flows underlying any initial fair value measurements.

Minimum standards for site reclamation have been established by various governmental agencies that affect certain operations of the Company. The determination of reclamation costs requires assumptions with respect to future expected costs and legislation in effect at that time. Changes in these assumptions could have a material effect on the amount required to be recognized as an ARO.

| MANAGEMENT DISCUSSION &ANALYSIS | 27 | |

| 2010 ANNUAL REPORT |

Income Taxes

Income taxes are calculated using the liability method of accounting. Temporary differences arising from the difference between the tax basis of an asset or liability and its carrying amount on the balance sheet are used to calculate future income tax liabilities or assets. Future income tax assets and liabilities are measured using enacted or substantively enacted tax rates and laws that are expected to apply when the temporary differences are likely to reverse. When the future realization of income tax assets does not meet the test of being more likely than not to be realized, a valuation allowance in the amount of the potential future benefit is recorded and no net asset is recognized. Changes to income tax rules, interpretations, or rates could have a material impact on amounts recorded in the financial statements.

Stock-based Compensation and Warrant Valuation

The fair value of stock-based compensation awards and warrant issuances is calculated using the Black-Scholes option pricing model. Option pricing models require the input of highly subjective assumptions including the expected price volatility. Changes in the subjective input assumptions can materially affect the fair value estimate, and therefore the existing models do not necessarily provide a reliable single measure of the fair value of stock options granted and warrants issued by the Company.

9. CHANGE IN ACCOUNTING POLICIES

The Company has elected to adopt the following standards effective January 1, 2010 so that its accounting policies are more closely aligned with International Financial Reporting Standards during the year ending December 31, 2010.

Business Combinations

Section 1582, Business Combinations, replaces Section 1581, Business Combinations and establishes standards for the accounting for business combinations. It provides the Canadian equivalent to International Financial Reporting Standard IFRS 3, Business Combinations. The section applies prospectively to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period after adoption.

Consolidated Financial Statements and Non-Controlling Interests

Section 1601, Consolidated Financial Statements, and Section 1602, Non-Controlling Interests, replace Section 1600, Consolidated Financial Statements. Section 1601 establishes standards for the preparation of consolidated financial statements. Section 1602 establishes standards for accounting for a non-controlling interest in a subsidiary in consolidated financial statements subsequent to a business combination. It is equivalent to the corresponding provisions of International Financial Reporting Standard IAS 27, Consolidated and Separate Financial Statements. The adoption of this standard had no effect on the Company’s financial statements.

10. INTERNATIONAL FINANCIAL REPORTING STANDARDS (“IFRS”)

Western Copper expects to adopt IFRS effective January 1, 2011. In 2011, the Company will have to report 2010 comparative figures restated using IFRS for each comparative period after the transition date.

Western Copper has compared its current accounting policies under Canadian Generally Accepted Accounting Principles (“GAAP”) to IFRS and identified differences between the two standards. Based on its review of historical transactions and current business activities, the Company has identified the treatment of exploration and evaluation (“E&E”) costs, income taxes, and asset impairment as areas with the greatest potential to create significant differences in the Company’s financial statements as a result of adopting IFRS.

| 28 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

Western Copper performed a comprehensive analysis of the areas noted above to determine the potential impact that adopting IFRS will have on the Company’s financial statements.

IFRS 6 allows companies to choose a policy that capitalizes E&E costs. The Company expects to continue capitalizing its E&E costs in a manner consistent with its current accounting policy.

The method of accounting for income taxes under IFRS is similar to Canadian GAAP, but one of the differences under IFRS is expected to have a significant impact on the Company’s financial reporting. Current IFRS guidelines prohibit the recognition of future income tax (“FIT”) assets or liabilities that arise from the initial recognition of assets or liabilities that do not impact profit or loss and that occur other than in a business combination. The majority of the Company’s FIT liability balance is due to the difference between the carrying value and the tax value of the properties that Western Copper acquired through its purchase of Lumina Resources Corp. in 2006. Western Copper accounted for the transaction as an acquisition of assets, not as a business combination. As a result of the rule noted above, the FIT liability balance recognized under Canadian GAAP would be eliminated. This would also decrease the carrying value of mineral properties by a similar amount because when the FIT liability was recognized, the carrying values of the related mineral properties were grossed up by the same amount.

Under Canadian GAAP, mineral property impairment testing is performed using a two-step test. The first step is to determine if there is an impairment loss by using an undiscounted cash flow analysis. If that analysis identifies an impairment loss, the loss is measured as the amount by which carrying value exceeds fair value. The fair value is often based on discounted cash flows. Under IFRS, assets are tested for impairment using a one-step process based on discounted cash flows. IFRS also allow the reversal of impairment charges from previous years if the fair value exceeds the carrying value of long-lived assets. Western Copper does not anticipate that the adoption of the IFRS in regards to mineral property impairment will have a material impact on the carrying value of its mineral properties.

Other IFRS that apply to the Company’s operations, but that are not expected to have a significant effect on 2010 financial results based on the Company’s activities are functional currency, business combinations, share based payments, and decommissioning and retirement obligations.

The Company has performed its review of IFRS based on standards applicable as of the date of this report. The International Accounting Standards Board is still developing IFRS and may propose changes to the standards between the date of this report and the date the Company adopts IFRS. Changes to IFRS could have material effects on Western Copper’s analysis discussed above.

The SEC has announced that it will not require a financial statements prepared in accordance with IFRS to be reconciled to accounting principles generally accepted in the United States (“US GAAP”). As a result, the Company’s annual consolidated financial statements for the year ended December 31, 2011 are not expected to include a US GAAP reconciliation note.

Western Copper does not expect the adoption of IFRS to have a significant impact on its information technology and data systems, internal control over financial reporting, or disclosure controls and procedures. Employees who have accounting responsibilities have received IFRS specific training. The Company’s directors have been provided with an overview of IFRS.

11. DISCLOSURE CONTROLS AND PROCEDURES

Management is responsible for designing, establishing, and maintaining a system of disclosure controls and procedures. Disclosure controls and procedures are designed to provide reasonable assurance that material information relating to the Company is made known to management, particularly during the period in which the annual filings are being prepared and that information required to be disclosed by the Company in its annual filings, interim filings or other reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time periods specified in securities legislation.

As a result of the material weakness identified during the assessment of internal control over financial reporting, as described below, management has also concluded that its disclosure controls and procedures were not effective as at December 31, 2010.

| MANAGEMENT DISCUSSION &ANALYSIS | 29 | |

| 2010 ANNUAL REPORT |

12. MANAGEMENT’S REPORT ON INTERNAL CONTROLS OVER FINANCIAL REPORTING AND DISCLOSURE CONTROLS

Management is responsible for designing, establishing, and maintaining a system of internal control over financial reporting to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with the Company’s generally accepted accounting principles.

The Chief Executive Officer and the Chief Financial Officer evaluated the effectiveness of the Company’s disclosure controls and procedures and assessed the design and the operating effectiveness of the Company’s internal control over financial reporting as of December 31, 2010.

Based on that assessment, management concluded that, as at December 31, 2010, the Company’s internal control over financial reporting was not effective due to the existence of a material weakness. A material weakness existed in the design of internal control over financial reporting caused by a lack of adequate segregation of duties in the financial close process. The Chief Financial Officer is responsible for preparing, authorizing, and reviewing information that is key to the preparation of financial reports. He is also responsible for preparing and reviewing the resulting financial reports. This weakness has the potential to result in material misstatements in the Company’s financial statements, and should also be considered a material weakness in its disclosure controls and procedures.

Management has concluded, and the audit committee has agreed that taking into account the present stage of Western Copper’s development, the Company does not have sufficient size and scale to warrant the hiring of additional staff to correct the weakness at this time.

There has been no significant change in internal control over financial reporting or in disclosure controls and procedures from October 1 to December 31, 2010 that has materially affected, or is reasonably likely to affect, the Company’s its internal control over financial reporting or its disclosure controls and procedures.

13. FINANCIAL INSTRUMENT RISK

The Board of Directors has overall responsibility for the establishment and oversight of the Company’s risk management framework. The Company has exposure to credit, liquidity, currency, interest rate and market risks from the use of financial instruments. Financial instruments consist of cash and cash equivalents, short-term investments, other receivables, reclamation bonds, and accounts payable and accrued liabilities.

Market Risk

The Company does not generate cash from its operating activities. Its principal source of funds is the issuance of common shares. It uses the capital raised from the issuance of its common shares to explore and develop its mineral properties with the goal of increasing the price of the Company’s common shares. Western Copper’s common shares are publicly traded. As such, the price of its common shares is susceptible to factors beyond management’s control including, but not limited to, fluctuations in commodity prices and foreign exchange rates and changes in the general market outlook. Should Western Copper require funds during a time when the price of its common shares is depressed, the Company may be required to accept significant dilution to maintain enough liquidity to continue operations or may be unable to raise sufficient capital to meet its obligations. The Company’s contractual obligations are described in the Property Overview and the Contractual Obligations sections of this report

Liquidity Risk

Liquidity risk is the risk that the Company will be unable to meet its financial obligations as they come due. The Company uses cash forecasts to ensure as far as possible that there is sufficient cash on hand to meet short-term business requirements. Cash is invested in highly liquid investments which are available to discharge obligations when they come due. The Company does not maintain a line of credit.

| 30 | MANAGEMENTDISCUSSION & ANALYSIS | |

| 2010 ANNUAL REPORT |

Credit Risk

Financial instruments that potentially subject the Company to credit risk consist primarily of cash and cash equivalents and short-term investments. These financial instruments are at risk to the extent that the institutions issuing or holding them cannot redeem amounts when they are due or requested. To limit its credit risk, the Company uses a restrictive investment policy. It deposits cash and cash equivalents in Canadian chartered banks and purchases short-term investments that are guaranteed by Canadian governments or by Canadian chartered banks.

Currency Risk

Currency risk is the risk that the Company will lose significant purchasing power to operate its business as a result of changes in currency rates. The Company raises funds in Canadian dollars. The majority of the Company’s expenditures are incurred in Canadian dollars. To limit its exposure to currency risk, the Company maintains the majority of its cash and cash equivalents in Canadian dollars. The Company did not have a material amount of financial instruments denominated in foreign currencies as at December 31, 2010 or December 31, 2009.

Interest Rate Risk

The Company is exposed to interest rate risk on its cash and cash equivalents and its short-term investments to the extent that the institutions that hold or issue those instruments cannot pay the interest earned on them by Western Copper. Potential losses in interest income would not have a material impact on the Company’s results of operations.

CAUTIONARY NOTES

Forward-looking statements

This Management’s Discussion and Analysis contains certain forward-looking statements concerning anticipated developments in Western Copper’s operations in future periods. Statements that are not historical fact are forward-looking statements as that term is defined in the United States Private Securities Litigation Reform Act of 1995 and forward looking information as that term is defined in National Instrument 51-102 (“NI 51-102”) of the Canadian Securities Administrators. Certain forward looking information should also be considered future-oriented financial information (“FOFI”) as that term is defined in NI 51-102. The purpose of disclosing FOFI is to provide a general overview of management’s expectations regarding the anticipated results of planned 2011 operations and capital expenditures. Forward-looking statements and information (referred to herein together as “forward-looking statements”) are frequently, but not always, identified by words such as “expects”, “anticipates”, “believes”, “intends”, “estimates”, “potential”, “possible” and similar expressions, or statements that events, conditions or results “will”, “may”, “could” or “should” occur or be achieved. These forward-looking statements are set forth principally under the heading “Property Overview”, “Quarterly Summary of Activities” and elsewhere in Management’s Discussion and Analysis and may include statements regarding perceived merit of properties; mineral reserve and resource estimates; capital expenditures; feasibility study results, ability to obtain required permits for the construction and operation of the Carmacks Copper Project; exploration results at the Company’s properties; budgets; work programs; timelines; strategic plans; market price of precious and base metals; or other statements that are not statement of fact. The material factors or assumptions used to develop forward-looking statements include prevailing and projected market prices and foreign exchange rates, exploitation and exploration estimates and results, continued availability of capital and financing, and general economic, market or business conditions and as more specifically disclosed throughout this document. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of Western Copper and its subsidiaries may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors.

Western Copper’s forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made, and Western Copper does not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change except as required by law. For the reasons set forth above, investors should not place undue reliance on forward-looking statements. Important factors that could cause actual results to differ materially from Western Copper’s expectations include uncertainties involved in fluctuations in gold, copper and other commodity prices and currency exchange rates; uncertainties relating to interpretation of drill results and the geology, continuity and grade of mineral deposits; uncertainty of estimates of capital and operating costs, recovery rates, production estimates and estimated economic return; the need for cooperation of government agencies and First Nations in the exploration and development of properties and the issuance of required permits; the need to obtain additional financing to develop properties and uncertainty as to the availability and terms of future financing; the possibility of delay in exploration or development programs or in construction projects and uncertainty of meeting anticipated program milestones; uncertainty as to timely availability of permits and other governmental approvals; and other risks and uncertainties disclosed in Western Copper’s Annual Information Form, Western Copper’s annual report on Form 40-F, and other information released by Western Copper and filed with the applicable regulatory agencies.

Cautionary note to U.S. investors

The terms “measured mineral resource”, “indicated mineral resource”, and “inferred mineral resource” used in this management discussion and analysis are Canadian geological and mining terms as defined in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects (“NI 43-101”) under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the CIM) Standards on Mineral Resources and Mineral Reserves. We advise U.S. investors that while such terms are recognized and required under Canadian regulations, the SEC does not recognize them. “Inferred mineral resources” in particular have a great amount of uncertainty as to their existence, and great uncertainty as to their feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules estimates of inferred mineral resources may not generally form the basis of feasibility or other economic studies. U.S. investors are cautioned not to assume that any part of an inferred mineral resource exists, or is economically or legally mineable. Disclosure of contained metal expressed is in compliance with NI 43-101, but does not meet the requirements of Industry Guide 7 of the SEC, which will only accept the disclosure of tonnage and grade estimates for non-reserve mineralization.

| MANAGEMENT DISCUSSION &ANALYSIS | 31 | |

| 2010 ANNUAL REPORT |

FINANCIAL

STATEMENTS

FINANCIAL

STATEMENTS

MANAGEMENT'S RESPONSIBILITY

FOR FINANCIAL REPORTING

The accompanying consolidated financial statements of the Company have been prepared by management in accordance with accounting principles generally accepted in Canada and reconciled to accounting principles generally accepted in the United States as set out in note 15 and contain estimates based on management’s judgment.

Management maintains an appropriate system of internal control to provide reasonable assurance that assets are safeguarded, transactions are properly authorized and recorded, and proper records are maintained. Further information on the company’s internal control over financial reporting and its disclosure controls is available in management’s report on internal control, which follows.

The Audit Committee of the Board of Directors has met with the Company’s independent auditors to review the scope and results of the annual audit and to review the consolidated financial statements and related financial reporting matters prior to submitting the consolidated financial statements to the Board of Directors for approval.

The Company’s independent auditors, PricewaterhouseCoopers LLP, have audited the Company’s consolidated financial statements on behalf of the shareholders and their report follows.

| |

| Julien François | Dale Corman |

| Chief Financial Officer | Chief Executive Officer |

| March 24, 2011 | March 24, 2011 |

| 34 | CONSOLIDATEDFINANCIAL STATEMENTS | |

| 2010 ANNUAL REPORT |

MANAGEMENT'S REPORT ON INTERNAL

CONTROL OVER FINANCIAL REPORTING