QuickLinks -- Click here to rapidly navigate through this document

DOUGLAS EMMETT PORTFOLIO

PORTFOLIO AND MARKET EVALUATION

Prepared by:

![]()

September 1, 2006

DOUGLAS EMMETT PORTFOLIO

PORTFOLIO AND MARKET EVALUATION

| | | | ||

|---|---|---|---|---|

| TABLE OF CONTENTS | ||||

| • | EXECUTIVE SUMMARY | |||

| • | CALIFORNIA OVERVIEW | |||

| • | LOS ANGELES OVERVIEW | |||

| • | LOS ANGELES OFFICE MARKET OVERVIEW | |||

| • | LOS ANGELES OFFICE SUBMARKETS/ DOUGLAS EMMETT PORTFOLIO OVERVIEW | |||

| • | HAWAII OVERVIEW | |||

| • | HONOLULU OFFICE MARKET OVERVIEW | |||

| • | HONOLULU OFFICE SUBMARKETS/ DOUGLAS EMMETT PORTFOLIO OVERVIEW | |||

| • | MULTI-FAMILY HOLDINGS | |||

| • | LOS ANGELES MULTI-FAMILY MARKET OVERVIEW | |||

| • | OAHU MULTI-FAMILY MARKET OVERVIEW | |||

![]()

100 Wilshire Boulevard, Suite 1600, Santa Monica, CA 90401 -- (310) 526-2450 -- (310) 587-2578 fax

101 California Street, Suite 2950, San Francisco, CA 94111 -- (415) 228-2900 -- (415) 228-3023 fax

| | | | ||

|---|---|---|---|---|

| Roy H. March CEO | Jeffrey N. Weber Senior Managing Director | Shannon W. Ching Senior Vice President |

| | | |

|---|---|---|

| Greg M. Goldstein Associate | Ian T. McCullough Analyst |

EXECUTIVE SUMMARY

Eastdil Secured has been asked by Douglas Emmett Realty Advisors ("Douglas Emmett" or "the Company") to assist in the evaluation of its 11,554,297 square foot office and 2,868-unit multi-family portfolio (the "Portfolio"). In the following paragraphs and sections, Eastdil Secured has provided an evaluation of (1) the fundamental economic drivers within Los Angeles and Hawaii, (2) the office and multi-family markets within Los Angeles and Hawaii and (3) the Douglas Emmett individual assets relative to the markets in which they are located. The evaluation is based on research and information provided by third parties as well as Eastdil Secured's extensive real estate transaction experience and expertise within the office and multi-family capital markets.

PORTFOLIO SUMMARY: Douglas Emmett has acquired a portfolio of office and multi-family properties primarily located in major Los Angeles markets with a focus on the following prominent characteristics: 1) Markets that are most proximate to high-end, executive housing and key amenities; 2) Markets with significant barriers to entry; 3) Acquiring a critical mass in its markets in order to provide competitive advantages through operating and leasing leverage; 4) Broadly multi- tenanted buildings where tenants are less rent sensitive and where no single tenant commands excess leverage; and 5) Markets close to its own senior management to provide further competitive advantages. In all nine Los Angeles County markets in which Douglas Emmett has a presence, it has between 12% and 76% of the top tier office square footage. In four of these nine markets, Douglas Emmett's presence is greater than 50% of the top tier office footage. In aggregate, the Douglas Emmett portfolio enjoys a rental premium of 11.8% compared to the various Los Angeles markets in which they are located.

PORTFOLIO OPERATING SYNERGY: As the largest owner of Westside real estate, Douglas Emmett benefits from operating synergies, in leasing, operating costs, and in the ability of management to focus and react quickly to emerging market opportunities. Upon acquisition, Douglas Emmett has consistently been able to reduce operating costs. While it is unrealistic to assume monopoly control of a market pushes rents to above economic levels, Douglas Emmett's position in its core markets provides the company with advantages in information, relationships and leverage in tenant negotiations as well as a greater degree of flexibility in accommodating changing tenant needs. As a result, Douglas Emmett's assets run at premiums in both rent and occupancy to the broader class A markets in which they compete. Our calculations show that Douglas Emmett owns approximately 40% of the first tier assets in their core markets. We do not believe any other public company has attained such a market share in a gateway city. This is an important distinction when comparing Douglas Emmett to other office REITs.

LOS ANGELES: Los Angeles is one of the most important financial, trade and cultural centers in the United States, and benefits from one of the strongest and most diverse economies in the world. If the five-county Los Angeles area were a sovereign nation, it would rank as the world's 15th largest economy with $755 billion in gross domestic product in 2005. For comparison, the countries of Australia, the Netherlands, and Taiwan have gross products of $708, $625 and $346 billion, respectively.

WEST LOS ANGELES OFFICE MARKET: The "premier" Los Angeles office locations are found in a series of "edge cities" in the West Los Angeles area as opposed to the central business district. These West Los Angeles markets include Santa Monica, Westwood, Beverly Hills, Century City, the Olympic Corridor and Brentwood, which are distinguished by virtue of high-end, executive housing, superior amenities and coastal proximity. Collectively, these markets comprise 43.2 million square feet of Class A and B office space, and carry an average asking market rent of $36.00 per square foot per year, as compared to the Los Angeles County market's average asking rents of $29.17 per square foot per month.

1

SAN FERNANDO VALLEY OFFICE MARKET: The San Fernando Valley office market is located in the northwestern region of the Los Angeles metropolitan area and contains approximately 22.3 million square feet of Class A and B office space (average asking market rent of $26.76 per square foot per month). Benefiting from its close proximity to the West Los Angeles office market, the San Fernando Valley office market has historically been an affordable cost alternative location. However, in recent years the region has become more of a self-contained, sub-metropolis with the office market evolving into a major business center. Due to strict zoning regulations, the primary business districts are contained mainly within Woodland Hills, Sherman Oaks and Encino (most of the office inventory located outside of these areas is comprised of smaller mid- and low-rise buildings of less than 50,000 square feet). Additionally, the recent development of upscale, master-planned residential communities such as Santa Clarita, Valencia and Newhall, have attracted affluent, well-educated home buyers in search of more cost effective housing. As such, this migration of a high quality labor force has attracted a substantial number of businesses to the area, which have in turn increased demand for quality office space.

BARRIERS TO ENTRY: Unlike most other gateway cities, the most desired Los Angeles office markets are typically edge city markets—more specifically the markets containing the Douglas Emmett portfolio, which service high-margin businesses willing to pay premium rents for quality office space—are governed by strict development ordinances prohibiting future office development. Based on current zoning ordinances and city specific plans, which specify building height limits as well as FAR restrictions, many of the Douglas Emmett properties are irreplaceable. Even if these city ordinances were changed and permitted the physical duplication, the current high cost of land and construction make office development highly unlikely. These barriers enhance rent growth prospects and limit cyclical operating risk. We are not aware of any portfolio of comparison, public or private, that offers anything close to this level of market penetration within a tier one market with such a supply constrained setting. Additionally, since much of the best inventory is in what we believe to be long-term investors' hands, it is difficult to acquire single assets—let alone market positions of any consequence. We believe this scarcity value enhances the value of the Portfolio.

REPLACEMENT COST: While a majority of the Douglas Emmett assets are considered irreplaceable due to 1) a lack of developable land in the marketplace and 2) restrictive zoning ordinances/city specific plans, the high cost of development within Los Angeles and Hawaii further make these buildings cost prohibitive to replicate. Within Los Angeles, hard and soft construction costs range from $375 to $425 per square foot for buildings with structured/subterranean parking. Ascribing a West Los Angeles land value of $150 to $175 per FAR square foot (while developable land of size is rare in Los Angeles, currently there is a parcel of land entitled for 900,000 square feet of office space located in Playa Vista—West Los Angeles adjacent and considered an inferior location compared to Douglas Emmett assets—under contract for $125 per FAR square foot), replacement costs range from $525 to $600 per square foot, substantially higher than values ascribed to the Douglas Emmett portfolio. It is noteworthy to mention that development costs in Hawaii would be considerably higher due to additional transportation and labor costs as well as higher sales taxes.

OFFICE VS. RESIDENTIAL DEVELOPMENT: In addition to the limited developable land and prohibitive zoning regulations within the Douglas Emmett markets, the high cost of land and construction does not currently justify office development. New residential developments continue to generate significantly higher returns as compared to office developments. Condo buyers within the Westside are paying as much as $1,200 per square foot for luxury condos. In Century City, the Related Companies, a New York based condo converter, purchased the St. Regis Hotel in January 2005 for approximately $250 a FAR foot with projected condo sale prices of approximately $1,000 to $1,250 per square foot. In addition, in 2004 Westfield purchased Gateway West, a 14-story 280,500 square foot office building located adjacent to the Westfield Century City Shopping Center, to make way for a $500 million 42-story tower mixed-use development with six floors of retail/office and 260 luxury

2

condominiums. It is noteworthy to mention that Century City is less favored as a residential area as compared to Santa Monica, Brentwood and Westwood (where Douglas Emmett owns a majority of their assets). As such, existing office buildings on the Westside are insulated from future supply and are positioned to benefit from a captive market where rental rates are well short of a level required to justify new construction.

RELATIVE ASSET QUALITY—LOCALLY: The relative quality of Douglas Emmett's assets within each market is critical to portfolio valuation. For example, in Santa Monica, Douglas Emmett owns 11% of the class A and B market square footage, however it owns six of the 10 top tier office buildings in the market, and its market share in the downtown Santa Monica market is over 45%. Similarly, while Douglas Emmett owns 45% of the West San Fernando Valley class A and B market, its share of the top tier square footage in the Warner Center/Woodland Hills market, which is the largest and most prestigious concentration of Class A space in the West Valley, is over 75%. The next two largest Westside landlords, EOP and JP Morgan, each have Westside portfolios that are roughly 60% smaller than the Douglas Emmett portfolio. Furthermore, none of the Los Angeles based public REITs, (Kilroy, Maguire) have more than 3.2 million square feet of class A space in the Douglas Emmett markets.

EMBEDDED RENT GROWTH: The portfolio has significant embedded rent growth when comparing existing contractual rents to current market rents within both the residential and office portfolios. The estimated embedded rent growth in the office portfolio represents a potential increase of approximately 14.5% in rents, and embedded rent growth within the apartments represents a potential increase of 32.4% in rents.

MARKET RENTAL RATE GROWTH: According to Torto Wheaton Research's Winter 2006 Office Outlook Report, Greater Los Angeles rental rates are projected to increase 5.5% by year-end 2006 with both the West Los Angeles and San Fernando Valley markets projected to outperform the rental rate growth of the overall Los Angeles market. Torto Wheaton forecasts a strong future for the Los Angeles Office market with a 5 year, 2006 through 2010, average annual rental growth rate projection of 5.2%.

HAWAII STORY: Douglas Emmett has recently developed a presence in the Hawaii office and residential markets. Similar to the opportunities that Douglas Emmett has realized in West Los Angeles, the strategy appears to be to acquire the leverage of critical mass in a supply constrained market with excellent growth prospects. Douglas Emmett has acquired two major office buildings in Downtown Honolulu and two major apartment communities. Douglas Emmett has pursued this strategy with a local partner as a continuation of their emphasis on placing senior level management in close proximity to their assets and markets.

MULTI-FAMILY PORTFOLIO: As of June 30, 2006, 15.3% of Douglas Emmet's annualized rent comes from its multifamily portfolio of 2,868 units, which consists of four of the top ten apartment communities (containing over 50 units) on the Westside and two of the largest apartment assets in suburban Honolulu containing a combined 1,098 units. Douglas Emmett's presence in each market positions them as one of the largest apartment owners in the market. Additionally, based on current zoning and land use restrictions, three of their four major Westside assets cannot be duplicated. As a result of Los Angeles and Santa Monica's respective rent control ordinances (both of which allow for market rents upon tenant move-out), embedded rent growth is over 30%, indicating a significant opportunity for future rent growth.

PROXIMITY TO EXECUTIVE HOUSING: Many business executives choose to reside within the West Los Angeles coastal communities. To attract such executives, many businesses are located in office markets within close proximity of prime coastal residential neighborhoods. Thus, the most desired office locations are in the West Los Angeles area (the areas in which Douglas Emmett has focused

3

their acquisitions). By contrast, in cities such as New York and San Francisco, the CBD commands higher rents and is considered a prime location for businesses.

CALIFORNIA OVERVIEW

Background: Since entering the Union in 1850, California has achieved a reputation as a destination for opportunity, quality of life and advancement. As the source of major economic expansions, California continually proves its dominance as the center for diversity, innovation and trade within the United States. As the most populous state in the nation with over 36.5 million residents, California continues to experience growth levels above the national average, providing the human resources necessary to pioneer new industries and diversify its culture. According to Claritas, California's population is expected to grow by 2.3 million residents, or 6.3%, over the next five years, versus 4.8% expected for the United States over the same period.

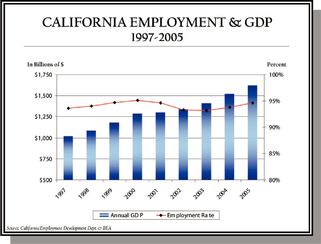

Gross Domestic Product ("GDP") and Employment: California's economic strength has been proven through its stable growth during volatile macroeconomic shifts. While the technology downturn in 2000 and the slowing of the economy over the last few years have largely impacted the rest of the nation, California continues to demonstrate steady growth. Since 1997, California has experienced consistent GDP growth, averaging approximately 6.0% per annum. Strong construction, agriculture and service-related industries have helped mitigate the economic slow down. According to the LAEDC, in 2005 California's GDP totaled over $1.6 trillion, a 6.9% increase from 2004. As illustrated in the table below, if California were a sovereign country, it would rank 8th in terms of GDP in the world, slightly behind Italy. In addition to this large and growing GDP, California has maintained a high employment rate. According to the California Employment Development Department, employment averaged 94% over the past five years within California. Moreover, during the same period, the population of California grew by 2.3 million people or approximately 6.6%, thus proving the economy's ability to absorb a significant immigration of new residents.

4

2005 Gross Product Comparisons

(2005 figures in billions of U.S. Dollars based on average exchange rates)

| Rank | Country/Economy | GDP | |||

|---|---|---|---|---|---|

| 1 | United States | $ | 12,486 | ||

| 2 | Japan | $ | 4,571 | ||

| 3 | Germany | $ | 2,797 | ||

| 4 | China (excluding Hong Kong) | $ | 2,225 | ||

| 5 | United Kingdom | $ | 2,202 | ||

| 6 | France | $ | 2,106 | ||

| 7 | Italy | $ | 1,766 | ||

| 8 | California | $ | 1,631 | ||

Source: LAEDC

*Theoretical ranking as if the area were a sovereign nation

Total Population & Growth

California vs United States

| Year | California Total | Rate* | United States, Total | Rate* | |||||

|---|---|---|---|---|---|---|---|---|---|

| 2000 | 33,871,648 | — | 281,421,906 | — | |||||

| 2006 | 36,579,455 | 298,021,266 | |||||||

| 2010 | 38,656,963 | 14.1 | % | 309,574,407 | 10.0 | % |

Source: Claritas 2006

*Rate over the previous 10-year period

Economic Landscape: California's broad economic base is anchored by Los Angeles in the South, San Francisco in the North and the agricultural stronghold of Central California. The following paragraphs outline the aforementioned economies and their individual strengths:

- •

- Home to over 18 million residents, the five-county Los Angeles area is the most populous metropolitan area in the nation. Recognized as a world-leading center of commerce, if the five-county Los Angeles area were a sovereign nation, it would rank as the world's 15th largest economy with $755 billion in GDP. The largest industry sectors, based on employment statistics, are business, financial, and professional management services, tourism, motion picture/television production, technology, bio-medical and international trade. The two major seaports of the Port of Los Angeles and the Port of Long Beach combined are considered to be the largest in North America, ranking first in tonnage and dollar volume. These two ports are also the primary entry points for trade with the Pacific Rim and therefore are the largest transfer points for products being shipped to and from China and Japan. Additionally, Los Angeles is considered to be the entertainment capital of the world, and is home to Hollywood as well as the movie and television studios of Warner Brothers, Universal, Fox and Disney.

- •

- The San Francisco Bay Area (the "Bay Area") is recognized as one of the nation's most important financial centers. The Bay Area serves as the national and regional headquarters for many of the world's leading financial institutions and corporations. In addition, the Bay Area is home to the Federal Reserve Bank of San Francisco and many private equity and venture capital firms that are key to fueling the region's economy. Surrounded on three sides by water, San Francisco houses approximately 750,000 residents in just 46.7 square miles.

- •

- California's core agricultural area lies in the Central Valley, where principal agricultural production includes raising cattle, avocados, broccoli, tomatoes, nuts, and raisins. The Central

5

Valley extends north to south nearly 450 miles from the Klamath Mountains to the Tehachapi Mountains between the Coastal and Sierra Nevada mountain ranges. This vast plain contains 75% of California's total irrigated agricultural area, and is the largest area of irrigated farmland west of the Rocky Mountains.

Affluent Population: California attracts a large portion of skilled labor, which invariably supports significantly higher wages than the United States average. For example, according to Claritas projections, 9.3% of households in California will earn over $150,000 in 2006 compared to the expected national average of 6.4%. In addition, California's mean household income is $74,900, a 14% premium above the United States mean household income of $65,800.

Percent of Household Income Levels

California vs U.S.

| Household Income | California | U.S. | |||

|---|---|---|---|---|---|

| Over $150,000 | 9.3 | % | 6.4 | % | |

| Over $250,000 | 2.8 | % | 2.0 | % | |

| Over $500,000 | 0.9 | % | 0.6 | % |

Source: Claritas 2006

SUMMARY

As the leader in international trade and advanced technology, California serves as a bellwether for the economic status of the United States. California's ability to maintain high employment levels, absorbing the continual influx of new residents, while fostering growth and prosperity prove its resilience to specific industry-based economic shifts.

LOS ANGELES OVERVIEW

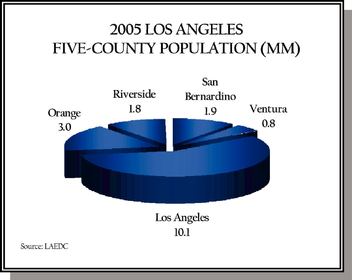

Widely recognized as a major financial, trade and cultural center, Los Angeles benefits from one of the strongest and most diverse economies in the world. As of December 31, 2005, the Los Angeles region had the largest metropolitan economy in California, the second largest metropolitan economy in the nation and accounted for more jobs than any U.S. region other than the New York metropolitan area. The largest industry sectors, based on employment statistics, are business, financial, and professional management services, tourism, motion picture/television production, technology, bio-medical and international trade. The Los Angeles area is comprised of five major counties totaling over 35,000 square miles. These counties include Los Angeles County (4,752 square miles), Orange County (948 square miles), Riverside County (7,304 square miles), San Bernardino County (20,106 miles) and Ventura County (2,208 miles).

If the five-county Los Angeles area were a sovereign nation, it would rank as the world's 15th largest economy with $755 billion in gross domestic product. Los Angeles County alone would rank 17th among the nations of the world with a GDP of $424 billion. The remaining framework of the five-county area includes Orange County ($162 billion), Riverside-San Bernadino Area ($129 billion), and Ventura County ($36 billion). For comparison, the countries of Australia, the Netherlands, and Taiwan have gross products of $708, $625 and $346 billion, respectively.

6

2005 GROSS PRODUCT COMPARISONS

(2005 figures in billions of U.S. Dollars based on average exchange rates)

| Rank | Country/Economy | GDP | |||

|---|---|---|---|---|---|

| 1 | United States | $ | 12,486 | ||

| 2 | Japan | $ | 4,571 | ||

| 3 | Germany | $ | 2,797 | ||

| 4 | China (excluding Hong Kong) | $ | 2,225 | ||

| 5 | United Kingdom | $ | 2,202 | ||

| 6 | France | $ | 2,106 | ||

| 7 | Italy | $ | 1,766 | ||

| 8 | Canada | $ | 1,130 | ||

| 9 | Spain | $ | 1,127 | ||

| 10 | South Korea | $ | 793 | ||

| 11 | Brazil | $ | 793 | ||

| 12 | India | $ | 775 | ||

| 13 | Mexico | $ | 768 | ||

| 14 | Russia | $ | 766 | ||

| 15* | Los Angeles 5-County Area | $ | 755 | ||

| 17* | Los Angeles County | $ | 424 | ||

Source: LAEDC

*Theoretical ranking as if the area were a sovereign nation

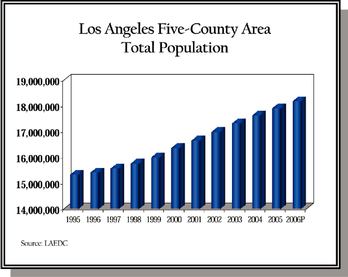

Population Growth: According to Claritas, if the Los Angeles five-county area were a separate state, it would have the fourth largest population in the United States with approximately 17.7 million residents. Only the states of California (36.2 million), Texas (22.7 million) and New York (19.3 million) would be more populous. Between 1995 and 2005, the five-county Los Angeles region experienced a gain of approximately 2.6 million residents, or a 16.8% total increase. This compares favorably to the nation as a whole, with the Los Angeles region outpacing the national average between 1995 and 2005 by 5.4%. In 2006, the LAEDC forecasts the Los Angeles five-county area's population to increase 1.5% to 18.2 million residents.

|  |

Affluent Population: Los Angeles' position along the California coast combined with its diverse economy and temperate weather make it home to many of the nation's upscale communities. From 1995 to 2005, household income growth in Los Angeles County averaged 3.9% annually. The average

7

estimated 2006 household income in the City of Los Angeles is $64,000. In 2006, an estimated 7.5% of households have income over $150,000, 2.9% of households have income over $250,000 and 1.1% of households have income over $500,000.

Percent of Household Income Levels of Other Leading Cities

| Household Income | DE Markets | Los Angeles | New York | Washington, DC | San Francisco | U.S. | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Over $150,000 | 17.8 | % | 7.5 | % | 7.7 | % | 11.0 | % | 16.1 | % | 6.4 | % | |

| Over $250,000 | 8.4 | % | 2.9 | % | 2.9 | % | 4.3 | % | 5.6 | % | 2.0 | % | |

| Over $500,000 | 3.9 | % | 1.1 | % | 1.1 | 1.6 | % | 2.1 | % | 0.6 | % |

Source: Claritas SiteReports 2006

As highlighted in the table below, income and education statistics for the Douglas Emmett markets reveal an educated, affluent, resident profile, well above the Los Angeles, California, and national averages.

Demographics

| Douglas Emmett Markets | 2006 E Mean HH Income | 2006E Median HH Income | 2005 Mean Home Price | Bachelor's Degree or higher | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Douglas Emmett Markets | |||||||||||||

| Beverly Hills | $ | 142,026 | $ | 81,567 | $ | 1,647,000 | 54.5 | % | |||||

| Brentwood1 | $ | 152,921 | $ | 98,193 | $ | 1,900,000 | 69.4 | % | |||||

| Westwood1 | $ | 100,394 | $ | 52,040 | $ | 1,598,000 | 66.4 | % | |||||

| Santa Monica | $ | 92,687 | $ | 58,715 | $ | 1,427,000 | 54.4 | % | |||||

| Sherman Oaks/Encino1 | $ | 83,450 | $ | 51,704 | $ | 885,000 | 38.1 | % | |||||

| Century City1 | $ | 124,692 | $ | 69,278 | $ | 795,000 | 48.7 | % | |||||

| Olympic Corridor1 | $ | 105,197 | $ | 67,675 | $ | 996,000 | 49.9 | % | |||||

| Woodland Hills | $ | 104,019 | $ | 74,188 | $ | 800,000 | 47.3 | % | |||||

| Burbank | $ | 71,115 | $ | 54,237 | $ | 662,000 | 29.0 | % | |||||

| Los Angeles—Long Beach—Santa Ana | $ | 68,908 | $ | 47,454 | $ | 529,000 | 2 | 24.5 | % | ||||

| San Francisco—Oakland—Freemont | $ | 94,558 | $ | 66,662 | $ | 716,000 | 2 | 44.6 | % | ||||

| New York—N. New Jersey—Long Island | $ | 65,505 | $ | 43,515 | $ | 445,000 | 2 | 27.2 | % | ||||

| Washington—Arlington—Alexandria | $ | 76,464 | $ | 48,347 | $ | 426,00 | 2 | 40.0 | % | ||||

| United States | $ | 65,849 | $ | 48,775 | $ | 219,000 | 2 | 24.6 | % | ||||

- 1.

- Unincorporated area, estimates based upon local Zip Codes

- 2.

- National Association of Realtors—median housing value

Source: Claritas Sitereports 2006 & Public Records

8

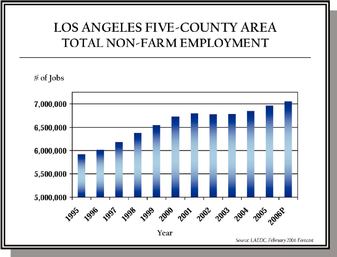

Job Growth: In addition to being one of the 15 largest economies in the world, the five-county Los Angeles area provides over 6.9 million jobs and is considered to have one of the most diverse employment bases. In fact, the Los Angeles-Long Beach-Santa Ana MSA accounts for more jobs than any other Metropolitan Statistical Area after the New York-Northern New Jersey-Long Island MSA. During the period from 1995 to 2005, total employment in the five-county Los Angeles region posted a net gain of over 1.0 million jobs, or a 17.7% total increase and is projected to increase by 1.3% to 7.1 million jobs in 2006. This statistic compares favorably to the nation as a whole, with the Los Angeles region outpacing the national average between 1995 and 2005 by 3.1%. Further more, according to the Los Angeles Economic Development Council, employment in the five-county area is estimated to have increased by 163,000 jobs from 2000 to 2004. For comparison, over the same period New York and San Francisco had net job losses of -181,000 and -94,700, respectively. We believe the economic future of Los Angeles is healthy with projected job growth of 1% over the 2006 through 2010 period, according to Torto Wheaton Research.

Los Angeles houses the international headquarters for many large companies including: Walt Disney, Occidental Petroleum, Northrop Grumman, Health-Net, Mattel, KB Home, Amgen Inc., and Hilton Hotels. Los Angeles is also home to numerous Fortune 500 companies and is recognized as the worldwide center of the entertainment industry.

Large and Diversified Economy: Los Angeles hosts an array of industries that include traditional and nontraditional sectors. Steel and iron co-exist with fiber optics and biogenetics. Los Angeles' ports and freeway system give the region a logistical advantage, which attracts firms whose footprints include the regional, national and international marketplaces. Firms have capitalized on this strength and have helped to grow the area into a hub of trade and logistics. The region is the nation's largest metro area for manufacturing. Los Angeles' largest manufacturing sectors are apparel and textiles, machinery and equipment, minerals and metals, and transportation equipment. Services which includes hospitality and leisure, healthcare, administrative and financial, legal and other professional service providers continue to be a main driver in Los Angeles, leading the way in total jobs. Other leading industries that drive the economy include trade, tourism and motion picture production. In addition, recent increases in federal defense spending have contributed to a sizable rebound by the aerospace industry. The economic base of the Los Angeles five-county area is summarized in the following table:

9

The Economic Base of the Los Angeles Five-County Area

2005 Annual Average of Non-Farm Employment (in 000s)

| Industry | LA County | Orange County | Riverside/ San Bernardino County | Ventura County | Five County Total | % | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total Nonfarm Employment | 4,020.1 | 1,483.1 | 1,173.2 | 287.2 | 6,963.6 | 100.0 | % | ||||||

| Mining | 4.1 | 0.6 | 1.2 | 0.7 | 6.6 | 0.1 | % | ||||||

| Construction | 145.9 | 95.5 | 118.9 | 18.4 | 378.7 | 5.4 | % | ||||||

| All Manufacturing* | 475.9 | 184.4 | 120.8 | 38.0 | 819.1 | 11.8 | % | ||||||

| Wholesale Trade | 212.6 | 82.8 | 45.4 | 11.8 | 352.6 | 5.1 | % | ||||||

| Retail Trade | 407.8 | 156.5 | 154.3 | 35.6 | 754.2 | 10.8 | % | ||||||

| Transport/Communications/Public Util. | 164.1 | 29.1 | 56.5 | 5.6 | 255.3 | 3.7 | % | ||||||

| Information | 213.2 | 32.7 | 13.6 | 6.8 | 266.3 | 3.8 | % | ||||||

| Finance Insurance/Real Estate | 245.5 | 132.6 | 46.4 | 23.5 | 448.0 | 6.4 | % | ||||||

| Services | 1,570.6 | 614.8 | 401.2 | 104.8 | 2,691.4 | 38.7 | % | ||||||

| Government | 580.4 | 154.1 | 214.9 | 42.0 | 991.4 | 14.2 | % |

Source: LAEDC

*Aerospace & Hi-Tech are included as part of Manufacturing.

Transportation and Foreign Trade: Los Angeles is the transportation and distribution hub for the southwest United States. The area is served by four major airports, two major seaports, 15 railroad companies, an extensive freeway network and an expanding Metro Rail mass transit system.

- •

- Air Transportation: The area's airports include: Los Angeles International Airport ("LAX"), Bob Hope Airport (Burbank/Glendale/Pasadena), Ontario International Airport, and Long Beach Airport. LAX is the 5th busiest airport in the world (behind Hartsfield-Jackson Atlanta International, Chicago O'Hare, London Heathrow, and Tokyo International) and has the 3rd largest passenger terminal in the United States, servicing over 75 major airlines and over 61 million passengers annually. Due to Los Angeles' strong presence as a place for international business and a tourist destination, over 17 million passengers traveled internationally through LAX in 2005.

| Airport | Location | 2005 Total Passengers | ||

|---|---|---|---|---|

| Hartsfield-Jackson Atlanta International | Atlanta | 85,907,423 | ||

| O'Hare International Airport | Chicago | 76,510,003 | ||

| London Heathrow Airport | London | 67,915,389 | ||

| Tokyo International (Haneda) Airport | Tokyo | 63,282,219 | ||

| Los Angeles International Airport | Los Angeles | 61,485,269 | ||

| Dallas-Fort Worth International Airport | Dallas | 59,064,360 | ||

| Charles De Gaulle International Airport | Paris | 53,756,200 | ||

| Frankfurt International Airport | Frankfurt | 52,219,412 | ||

| Las Vegas McCarran International Airport | Las Vegas | 44,280,190 | ||

| Schiphol Airport | Amsterdam | 44,163,098 |

Source: Airports Council International

- •

- Shipping: The area has two major seaports: the Port of Los Angeles and the Port of Long Beach. Combined, these ports are the largest in North America, ranking first in tonnage and dollar

10

volume. In fact, the Port of Los Angeles alone is the 8th busiest container port in the world. These two ports are also the primary entry points for trade with the Pacific Rim and therefore are the largest transfer points for products being shipped to and from Japan. The LAEDC forecasts that the total value of two-way international trade passing through the Los Angeles customs district will increase by 12.2% in 2006 over 2005 to $330.9 billion, with significant portions of this amount attributable to trade with Japan and China. Currently underway are two major redevelopment projects, totaling $1.1 and $1.3 billion, to enlarge both the Los Angeles and Long Beach Ports, respectively.

| Port | Tonnage CY 2005 | Annual Container Volume (in TEUs) CY 2005 | ||

|---|---|---|---|---|

| Los Angeles | 169.0 MMRTs | 7.5 Million TEUs | ||

| Long Beach | 80.7 MMTs | 6.7 Million TEUs |

- •

- Rail Transportation: The 15 railroads that link Southern California with the rest of the United States and Canada carry approximately eight billion tons of manufactured goods to and from the Los Angeles five-county area annually.

- •

- Metrolink and Metropolitan Transit Authority ("MTA"): Over $18 billion has been spent developing an approximate 530-mile, commuter rail system within the metropolitan area. Combined, the Metrolink and MTA rail system serves over 300,000 passengers daily.

- •

- Freeway Infrastructure: Los Angeles is recognized as having the largest and most utilized freeway system in the world. Over 900 miles of interstate and state freeways serve the metropolitan area, providing exceptional access for commerce and commuters.

SUMMARY

A world-leading center of commerce, Los Angeles is a vibrant metropolis attracting many people and businesses as a result of its economy, transportation systems, climate and cultural and recreational amenities. The area's unique role as a national trendsetter combined with its continuing population and economic growth indicates a long-term positive outlook for properties in the region.

11

LOS ANGELES OFFICE MARKET OVERVIEW

LOS ANGELES OFFICE MARKET

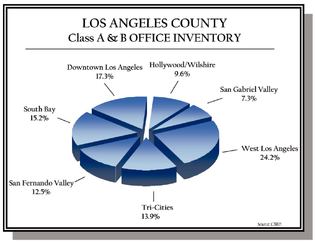

Los Angeles County contains approximately 368 million square feet of office space, the largest concentration of office space on the West Coast and the second largest in the nation. It is comprised of seven distinct regional markets: West Los Angeles, Downtown Los Angeles, South Bay, San Fernando Valley, Tri-Cities, the Hollywood/Wilshire Corridors, and the San Gabriel Valley.

According to CB Richard Ellis, the combined class A and B office inventory is comprised of approximately 178.5 million square feet. As noted in the adjacent chart, the West Los Angeles market contains the greatest concentration of class A and B office space in Los Angeles County.

The table below summarizes the Los Angeles County office markets and highlights the performance of the Douglas Emmett markets versus the rest of Los Angeles County. As of second quarter 2006, the Douglas Emmett markets posted an average asking monthly rental rate of $32.14 per square foot and a vacancy rate of 6.8%, versus $26.14 and 12.2% for the markets where Douglas Emmett does not have a presence. According to Torto Wheaton Research's Winter 2006 Office Market Report, Greater Los Angeles rental rates are projected to increase 5.5% by year-end 2006, and the Douglas Emmett markets are projected to outperform the broader Los Angeles market. Furthering this trend, Torto Wheaton projects rental growth rates of 5.9%, 5.3%, 4.9%, and 4.2% in 2007, 2008, 2009, and 2010, respectively.

The table below highlights Class A and B statistics for the Douglas Emmett markets and the rest of Los Angeles County.

Los Angeles County Office Market—Class A & B

as of Second Quarter 2006

| Markets | Total Sq Ft. | % of Total | Asking Rental Rate/sf/mo | Occupancy | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| West Los Angeles | 43,183,281 | 24.2 | % | 36.00 | 93.1 | % | ||||

| San Fernando Valley | 22,291,618 | 12.5 | % | 26.76 | 92.8 | % | ||||

| Tri-Cities | 24,768,349 | 13.9 | % | 30.24 | 93.6 | % | ||||

| TOTAL | 90,243,248 | 50.6 | % | $ | 32.14 | 93.2 | % | |||

Downtown Los Angeles | 30,960,102 | 17.3 | % | 30.12 | 86.3 | % | ||||

| South Bay | 27,108,214 | 15.2 | % | 22.44 | 84.1 | % | ||||

| Hollywood/Wilshire | 17,194,280 | 9.6 | % | 25.68 | 90.7 | % | ||||

| San Gabriel Valley | 12,981,596 | 7.3 | % | 24.96 | 95.2 | % | ||||

| TOTAL | 88,244,192 | 49.4 | % | $ | 26.14 | 87.8 | % | |||

Total/Avg.(1) | 178,487,440 | 100.0 | % | $ | 29.17 | 90.5 | % | |||

Source: CB Richard Ellis

- (1)

- Weighted average based on total square feet of competitive office space.

12

It should also be noted that due to the climate and amenity base, most business executives choose to reside within the West Los Angeles coastal communities. As such, to avoid long commutes to work, many businesses are located in office markets within close proximity of prime coastal residential neighborhoods. Thus, many desired office locations are in the West Los Angeles area (Santa Monica, Beverly Hills, Century City, Brentwood and Westwood, the cities in which Douglas Emmett has focused their acquisitions), commanding the highest rent in the Greater Los Angeles area. This is highly irregular when compared to other cities like New York and San Francisco where the CBD commands higher rents and is considered a prime location for businesses.

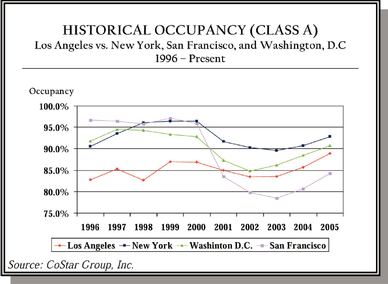

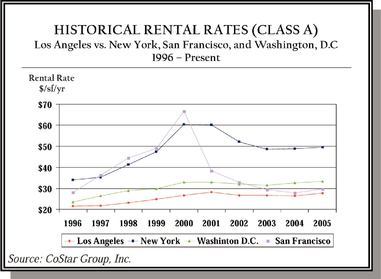

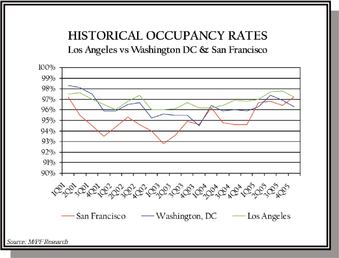

Nationally, major gateway cities such as Los Angeles, San Francisco, New York and Washington DC have historically experienced less volatile office rental rate and occupancy fluctuation; of course San Francisco's heavy dependence on technology caused it to experience record spikes in vacancy forcing dramatic decreases in rental rates. As highlighted in the graphs below from 4th quarter 2000 to 4th quarter 2003, San Francisco Class A office buildings experienced a rental rate decrease from approximately $66.74 per square foot per year to $29.49 per square foot per year, a 56% decrease, while vacancy increased significantly from 4.1% to 21.5%. After 9/11, Manhattan New York experienced a downturn in rental rates and occupancy; however, its resilient economy quickly recovered and stabilized in 2003. Washington DC has experienced similar stable rental rate trends to Los Angeles; however, its occupancy has substantially fluctuated in recent years. Overall Los Angeles has demonstrated the least volatility in rental rate and occupancy compared to the other major gateway cities—San Francisco, New York and Washington DC. This is directly attributed to Los Angeles' diverse economic base which is not overly exposed or dependent on any one specific industry.

|  |

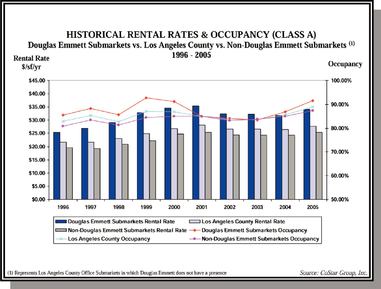

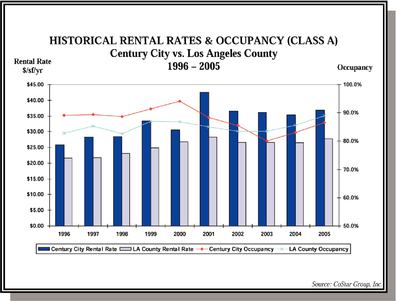

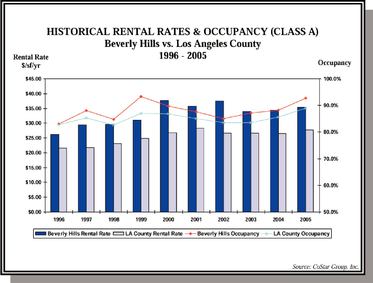

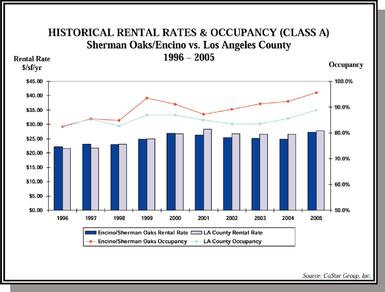

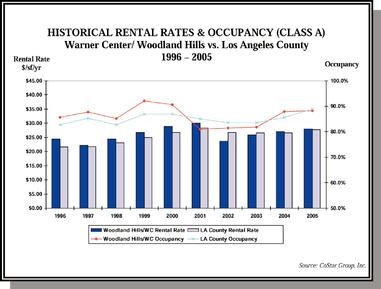

In addition to its seven major markets, the Los Angeles County office market is further defined by 59 distinct office submarkets located within the seven major markets according to CB Richard Ellis. These submarkets differ widely in terms of their desirability, tenant base, rental and occupancy rates and barriers to new construction and supply. Within Douglas Emmett's three Los Angeles County office markets (West Los Angeles, San Fernando Valley and Tri-Cities), Douglas Emmett has focused on what we believe are nine of the premier office submarkets in these markets and in Los Angeles County as a whole. Six of these submarkets, Santa Monica, Brentwood, Olympic Corridor, Westwood, Century City and Beverly Hills, are located in the West Los Angeles market. Two of these submarkets, Sherman Oaks/Encino and Warner Center/Woodland Hills, are located in the San Fernando Valley market, and one, the Burbank Media District, is located in the Tri-Cities market. These submarkets are distinguished by their high level of lifestyle amenities and proximity to high-end executive housing, features that have contributed to these submarkets historically achieving premium rents and higher occupancy levels than the other Los Angeles County office submarkets, as well as the Los Angeles County office market as a whole. The table below illustrates a comparison of the historical rental rates

13

and occupancy levels of Class-A office space in Douglas Emmett submarkets, the other Los Angeles County submarkets and the Los Angeles County office market as a whole.

The decline in occupancies in Douglas Emmett's submarkets from 2000 to 2003 was the result of a combination of factors. A large amount of previously entitled office space was delivered to the market in 2000 and 2001, and such space, especially in Santa Monica and Century City, was largely occupied by firms created during the technology boom of the late 1990s. The combined impact of this new construction with the slowing of the technology sector and the general economic downturn that affected Los Angeles County as a whole in 2000 led to a decrease in office space absorption as well as increasing vacancies in Douglas Emmett submarkets from 2000 through 2003. Occupancy levels in these submarkets began to recover in 2004 and on average have significantly outperformed the Los Angeles County office market as a whole since then, with occupancy increasing from 83.4% in 2003 to 91.5% in 2005, or 8.1 percentage points, compared to the Los Angeles County market which increased from 83.6% to 88.9%, or 5.3 percentage points, and compared to the submarkets in which Douglas Emmett does not have a presence, which increased from only 83.7% to 87.4%, or 3.7 percentage points. Rental rates in Douglas Emmett submarkets began to recover in 2005, with annual rental rates increasing from $31.76 per square foot in 2004 to $34.04 per square foot in 2005, or an increase of 7.2%, compared to Los Angeles County, which increased from $26.53 per square foot to $27.71 per square foot, or an increase of 4.4%, and compared to the submarkets in which Douglas Emmett does not have a presence, which increased from $24.23 per square foot to $25.36 per square foot, or an increase of 4.7%. We project average Class-A office rental rate growth of approximately 10.0% per year for 2006 and 2007 across Douglas Emmett's nine Los Angeles County submarkets with a projected five year growth rate average of 6.9% from 2006 to 2010.

14

As outlined below, the highest sales per square foot transactions occur in the West Los Angeles markets. It is noteworthy to mention Trizec's purchase of 14 Southern California office assets from Arden Realty Trust in December 2005 for $1.6 billion, or $375 per square foot, and subsequent sale to Blackstone and Brookefield for $4.8 billion in June 2006. The majority of these assets are not located in Douglas Emmett markets and are generally in less desirable locations. Based on the average price per square foot, 2004-2006 office building transactions located within Santa Monica benefited from an approximate $107 per square foot premium, approximately 37% more, over downtown office buildings. As further evidence of Douglas Emmett's market strength, based on the data below, markets where Douglas Emmett has a presence enjoy a $391 per square foot average sale price versus $301 per square foot for markets where Douglas Emmett does not have a presence. Details of noteworthy Los Angeles office transactions are outlined in the following table.

2003-2006 Noteworthy Office Sales Activity

Los Angeles

| Date | Property | Sq. Ft. | Market | Buyer | Est. Price | $/SF | Comments | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pending | Luckman Plaza | 308,698 | Beverly Hills* | Confidential | $ | 156,000,000 | $ | 505 | *Located in W. Hollywood, but included due to proximity to the entrance to Beverly Hills. | |||||||

| Pending | Maple Drive Collection | 600,000 | Beverly Hills | Confidential | $ | 325,000,000 | $ | 542 | ||||||||

| Jun-06 | Wilshire Rodeo Plaza | 246,916 | Beverly Hills | TIAA | $ | 194,950,000 | $ | 790 | Includes approx. 60k sf of high end urban retail. Office PSF approx $614, cap rate approx 5.2%. | |||||||

| Apr-06 | 9701 Wilshire | 109,757 | Beverly Hills | Kennedy Wilson | $ | 51,000,000 | $ | 465 | ||||||||

| Dec-05 | 9665 Wilshire | 169,000 | Beverly Hills | Trizec | 63,400,000 | $ | 375 | Part of 14 asset portfolio purchased from Arden | ||||||||

| Sep-05 | 407 N Maple Dr | 160,000 | Beverly Hills | Tishman Speyer | $ | 71,000,000 | $ | 444 | 100% vacant. | |||||||

| Sep-05 | 9465 Wilshire Blvd | 220,000 | Beverly Hills | Morgan Stanley | $ | 136,000,000 | $ | 618 | 90% occupancy. 40,000 sf of street retail. | |||||||

| Aug-05 | Maple Plaza | 285,000 | Beverly Hills | Tishman Speyer | $ | 106,000,000 | $ | 372 | 75% leased building. In-place cap rate below 5%, stabilized cap over 7%. | |||||||

| Jun-05 | Bank of America Building | 87,596 | Beverly Hills | Real Estate Capital Partners | $ | 31,200,000 | $ | 356 | 94% occupancy. | |||||||

| May-05 | Beverly Mercedes Pl. | 130,054 | Beverly Hills | Tishman Speyer | $ | 38,200,000 | $ | 294 | 63% leased. | |||||||

| Mar-05 | 450 N Roxbury Dr | 103,000 | Beverly Hills | Starpoint Properties | $ | 43,450,000 | $ | 422 | Owner to occupy remaining vacant space on top floor. 5.9% cap rate. | |||||||

| Aug-04 | Beverly Hills Medical Center | 100,413 | Beverly Hills | Douglas Emmett & Company | $ | 32,000,000 | $ | 319 | 100% leased building. | |||||||

| Apr-04 | 331 N Maple Dr | 82,193 | Beverly Hills | Bendheim/Kim | $ | 28,500,000 | $ | 347 | Dreamworks bought out of lease leaving building 33% occupied. | |||||||

| Subtotal: | 2,602,627 | $ | 1,276,700,000 | $ | 491 | |||||||||||

| Pending | Cornerstone Plaza | 163,909 | Santa Monica* | Confidential | $ | 65,600,000 | $ | 400 | *Located in West LA, included due to proximity to Santa Monica | |||||||

| Sep-05 | Courtyard on Wilshire | 86,000 | Santa Monica | Xemit Corp. | $ | 35,550,000 | $ | 413 | 96% occupancy. | |||||||

| Mar-05 | Tribecca Plaza | 151,000 | Santa Monica | Broadreach Capital Partners | $ | 30,500,000 | $ | 202 | Buyer planning $4 million renovation. 48% leased. | |||||||

| Dec-04 | Lantana Center | 331,739 | Santa Monica | Maguire Partners | $ | 120,800,000 | $ | 364 | Total sale $136.8mil included $16mil for 184,105sf addl entitlements. 7% cap rate. | |||||||

| Jul-04 | Colorado Center | 1,100,000 | Santa Monica | TIAA / EOP | $ | 460,000,000 | $ | 418 | Sale price is approx. a 7% stabilized cap rate. | |||||||

| Jun-04 | Arboretum Gateway | 201,000 | Santa Monica | ING Clarion Partners | $ | 98,000,000 | $ | 488 | Property is fully leased through 2016 to Universal Music. 7.5% cap rate. | |||||||

| Subtotal: | 2,033,648 | $ | 810,450,000 | $ | 399 | |||||||||||

*Real Capital Analytics, Pending Deals represent estimates by Eastdil Secured

15

2003-2006 Noteworthy Office Sales Activity

Los Angeles

| Date | Property | Sq. Ft. | Market | Buyer | Est. Price | $/SF | Comments | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pending | Burbank Office Portfolio | 1,380,000 | Burbank | Confidential | $ | 565,740,000 | $ | 410 | M. David Paul Portfolio, Includes Pinnacle II, Central Park, and Media Studios North. | |||||||

| Dec-05 | Legacy Media Tower | 147,889 | Burbank | Legacy Partners | $ | 43,000,000 | $ | 291 | 36% occupancy. | |||||||

| Jul-05 | Buena Vista Plaza | 115,130 | Burbank | Behringer Harvard | $ | 36,000,000 | $ | 313 | 100% occupancy. | |||||||

| Jun-05 | Burbank Empire Center I-II | 230,000 | Burbank | CBRE Investors (State of Alaska) | $ | 70,250,000 | $ | 305 | Allianz (40%) credit for 12+ years, solid remainder of rent roll. 5.75% cap rate. | |||||||

| Aug-04 | 4 Media Center | 131,000 | Burbank | Palisades Associates | $ | 39,450,000 | $ | 293 | Net-leased to Liberty Media through 2016. 8% cap rate. | |||||||

| Jul-03 | The Tower Burbank | 493,803 | Burbank | Blackrock Real Estate | $ | 167,000,000 | $ | 338 | Disney lease for 95% of building expires in 2008. 6.1% cap rate. | |||||||

| Jul-03 | The Pinnacle | 393,776 | Burbank | DB Real Estate (RREEF) | $ | 145,000,000 | $ | 368 | Excellent project, location, term, and credit tenancy. 90% occupied, 7% cap rate. | |||||||

| Subtotal: | 2,891,598 | $ | 1,066,440,000 | $ | 331 | |||||||||||

| Dec-05 | 1940 Century Park | 46,856 | Century City | 1940 Century City LLC | $ | 22,500,000 | $ | 480 | 98% occupancy. | |||||||

| Aug-04 | Alcoa Building | 280,500 | Century City | Westfield of America Inc. | $ | 80,000,000 | $ | 285 | Class B building adjacent to Buyer's retail center. 88% leased. | |||||||

| Subtotal: | 327,356 | $ | 102,500,000 | $ | 313 | |||||||||||

| Pending | LNR Warner Center I-III | 808,000 | Woodland Hills | Confidential | $ | 310,000,000 | $ | 384 | Class-A suburban office building. | |||||||

| Jan-05 | The Trillium | 578,500 | Woodland Hills | Douglas Emmett & Company | $ | 153,500,000 | $ | 265 | Class A, 88% leased, suburban office building | |||||||

| Dec-04 | 21st Century Plaza | 517,638 | Woodland Hills | JP Morgan Fleming | $ | 130,000,000 | $ | 251 | Leasehold int. Ground lease has 70 yrs remaining. 7.25% cap rate. | |||||||

| Oct-04 | Warner Corporate Center | 253,698 | Woodland Hills | Arden Realty | $ | 64,500,000 | $ | 254 | Class-A multi-tenant office building. 7.2% cap rate. | |||||||

| Subtotal: | 2,157,836 | $ | 658,000,000 | $ | 305 | |||||||||||

| Feb-05 | Water's Edge | 250,000 | Marina Del Rey | Maguire Partners | $ | 85,500,000 | $ | 389 | Electronic Arts occupies entire bldg. Partial interest (88%) sale. | |||||||

| Mar-04 | Univision Building | 161,700 | Marina Del Rey | Univision Television Group | $ | 52,500,000 | $ | 325 | User purchase. | |||||||

| Subtotal: | 411,700 | $ | 138,000,000 | $ | 335 | |||||||||||

*Real Capital Analytics, Pending Deals represent estimates by Eastdil Secured

16

2003-2006 Noteworthy Office Sales Activity

Los Angeles

| Date | Property | Sq. Ft. | Market | Buyer | Est. Price | $/SF | Comments | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Jan-06 | One California Plaza | 974,000 | Downtown LA | Macquarie Office Trust | $ | 325,000,000 | $ | 334 | 96% occupancy. Part of six building portfolio. | |||||||

| Sep-05 | AON Center | 1,028,852 | Downtown LA | Broadway Partners (Confidential) | $ | 192,500,000 | $ | 187 | Class B+ office tower. Small floorplates with excellent views. 72% leased. | |||||||

| Oct-05 | Mellon Bank Center | 663,000 | Downtown LA | Tishman Speyer | $ | 245,600,000 | $ | 370 | 93% occupancy. | |||||||

| Jul-05 | Figueroa at Wilshire | 1,038,000 | Downtown LA | Trizec | $ | 356,700,000 | $ | 344 | Part of 14 asset portfolio purchased from Arden | |||||||

| Jul-05 | Figueroa at Wilshire | 1,040,000 | Downtown LA | Trizec Properties | $ | 365,000,000 | $ | 351 | Arguably the highest quality building in downtown. Occupancy to drop to 55% first year. Sub 8% IRR. | |||||||

| Dec-05 | Union Bank Plaza | 626,000 | Downtown LA | Hines | $ | 144,000,000 | $ | 230 | Union Bank occupies over half of building. 7.2% cap rate on 92% occupancy. | |||||||

| Jan-05 | 777 Tower | 1,004,522 | Downtown LA | Maguire Properties | $ | 345,000,000 | $ | 343 | Estimated price. Purchased as part of 10 bldg portfolio. 90% occupied. | |||||||

| Feb-05 | SBC Center | 885,768 | Downtown LA | Layton-Belling & Associates | $ | 129,000,000 | $ | 146 | 2-building complex. Recent SBC 10 yr lease for 225k sf. 90% leased. | |||||||

| Jul-05 | Bank of America Tower | 1,421,711 | Downtown LA | Trizec Properties | $ | 435,000,000 | $ | 306 | Class-A office tower with high quality rent roll. 6% cap rate, 92% occupied. | |||||||

| Subtotal: | 8,681,853 | $ | 2,537,800,000 | $ | 292 | |||||||||||

| Pending | Glendale Plaza | 532,815 | Glendale | Confidential | $ | 215,000,000 | $ | 404 | 98% occupied. | |||||||

| Aug-06 | Glendale Corp. Center | 114,450 | Glendale | Broadreach Capital | $ | 22,890,000 | $ | 200 | Part of 10 building portfolio | |||||||

| Mar-06 | 500 N Brand Blvd | 415,000 | Glendale | ING Clarion Partners | $ | 145,000,000 | $ | 349 | 80% occupancy. Includes 23,000 sf of retail. | |||||||

| Aug-05 | 505 N Brand Blvd | 311,787 | Glendale | LaSalle Investment Management | $ | 108,750,000 | $ | 349 | 85% occupancy. Yahoo! and United Healthcare are major tenants. | |||||||

| Jun-05 | Glendale City Center | 395,619 | Glendale | Principal Global Investors | $ | 104,300,000 | $ | 264 | Sold with 56% vacancy. | |||||||

| Mar-05 | 801 N Brand Blvd | 282,433 | Glendale | Maguire Properties | $ | 80,173,000 | $ | 284 | Estimated price. High quality suburban office building. Part of 10 building portfolio. 6.5% cap rate. | |||||||

| Subtotal: | 2,052,104 | $ | 676,113,000 | $ | 329 | |||||||||||

*Real Capital Analytics, Pending Deals represent estimates by Eastdil Secured

17

LOS ANGELES OFFICE SUBMARKETS/

DOUGLAS EMMETT PORTFOLIO OVERVIEW

LOS ANGELES OFFICE MARKETS

The Los Angeles office market is unique among gateway cities where the premier office locations are found in a series of "edge cities" in the West Los Angeles area and San Fernando Valley as opposed to the CBD (such as in New York, San Francisco, Washington, D.C., etc.). These markets include Santa Monica, Westwood, Beverly Hills, Century City, the Olympic Corridor, and Brentwood in West Los Angeles and Sherman Oaks, Encino and Warner Center/Woodland Hills in the West and Central San Fernando Valley; each is distinguished by virtue of their proximity to executive housing and superior amenities. These attributes are pillars of Douglas Emmett's strategy and consequently, their portfolio holdings are clustered in the premier West Los Angeles and San Fernando office markets and communities. Collectively, these nine submarkets comprise over 50 million square feet of Class A and B office space. As of June 30, 2006, the weighted average asking rental rates for Douglas Emmett's Los Angeles office portfolio was $35.28 per square foot, representing a premium of 11.8% over Douglas Emmett's nine submarkets' average asking rental rate of $31.56 per square foot. Excluding the Warner Center/Woodland Hills submarket, where properties with significant vacancies were acquired, Douglas Emmett's occupancy rate (as of June 30, 2006) was 96.1%, which reflects a 2.5 percentage point premium to Douglas Emmett's submarkets (including the Warner Center/Woodland Hills submarket, the occupancy rate reflects a 0.4 percentage point premium). Furthermore, each of these markets are highly supply-constrained as a result of a lack of competitive development sites, economic constraints, stringent legislative barriers, community-organized opposition to development and severe down-zoning (Proposition U and Specific Plans). Approximately 90% of the Douglas Emmett assets are considered to be irreplaceable under current zoning regulations. Approved in 1986, Proposition U decreased the development capacity of the city by roughly 50% and applies to the Brentwood, Olympic Corridor, Westwood and Sherman Oaks/Encino office submarkets. Additionally, Specific Plans governing development within Warner Center/Woodland Hills, Century City, Santa Monica and the Burbank Media District severely hinder or completely preclude future office development while development within the city of Beverly Hills is met with severe resident and public office anti-development opposition.

Overall, Douglas Emmett owns over 10.4 million square feet of Class A office space in the premier West Los Angeles and San Fernando Valley markets, over 20% of the total Class A and B inventory within submarkets where Douglas Emmett has a presence, and their position within the top ten buildings of each office submarket is even greater. We are not aware of any publicly owned portfolio of comparison that has attained such a high concentration of class A office space within a gateway city. The following table highlights the total square footage, average asking market rent and current occupancy for Douglas Emmett's aggregate holdings in each of their respective office markets.

Los Angeles Markets (Class A&B)/Portfolio Overview

Douglas Emmett Holdings by Office market(1)

| | | | Avg. Asking Rate ($/sf/yr) | | | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | Occupancy %(2) | |||||||||||||

| Market | | | ||||||||||||||

| Sq. Ft. D.E. | Market | D.E. | Market | D.E. | Market | |||||||||||

| West Los Angeles | ||||||||||||||||

| Santa Monica | 860,159 | 7,619,589 | $ | 59.11 | $ | 41.76 | 99.2 | % | 94.8 | % | ||||||

| Brentwood | 1,390,625 | 3,331,731 | $ | 36.03 | $ | 33.72 | 95.7 | % | 92.8 | % | ||||||

| Olympic Corridor | 922,405 | 2,327,630 | $ | 29.81 | $ | 28.92 | 90.0 | % | 90.8 | % | ||||||

| Westwood | 396,728 | 3,365,978 | $ | 34.80 | $ | 41.28 | 95.2 | % | 92.7 | % | ||||||

| Century City | 866,039 | 9,574,342 | $ | 35.30 | $ | 35.16 | 93.0 | % | 89.3 | % | ||||||

| Beverly Hills | 571,869 | 6,503,630 | $ | 47.75 | $ | 37.20 | 97.8 | % | 94.8 | % | ||||||

| Total/ Weighted Average DE Submarkets(2) | 5,007,825 | 32,722,900 | $ | 39.96 | $ | 35.46 | 95.0 | % | 92.4 | % | ||||||

18

| | | | Avg. Asking Rate ($/sf/yr) | | | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | Occupancy %(2) | |||||||||||||

| Market | | | ||||||||||||||

| Sq. Ft. D.E. | Market | D.E. | Market | D.E. | Market | |||||||||||

| Fox Hills/Culver City | 3,492,048 | $ | 31.56 | 94.0 | % | |||||||||||

| Marina Del Rey | 1,615,660 | $ | 25.08 | 92.9 | % | |||||||||||

| West Hollywood | 2,419,222 | $ | 34.92 | 96.8 | % | |||||||||||

| West LA | 2,933,451 | $ | 30.72 | 95.2 | % | |||||||||||

| Total/Weighted Average Non DE Submarkets | 10,460,381 | $ | 31.10 | 94.8 | % | |||||||||||

San Fernando Valley | ||||||||||||||||

| Sherman Oaks/Encino | 2,878,769 | 5,721,621 | $ | 33.11 | $ | 27.79 | 97.4 | % | 95.3 | % | ||||||

| Warner Center/Woodland Hills | 2,567,814 | 6,392,299 | $ | 28.28 | $ | 27.96 | 84.1 | % | 90.4 | % | ||||||

| Total/ Weighted Average DE Submarkets(2) | 5,446,583 | 12,113,920 | $ | 30.83 | $ | 27.87 | 91.1 | % | 93.0 | % | ||||||

Agoura Hills | 0 | 757,902 | NA | $ | 25.32 | NA | 83.7 | % | ||||||||

| Calabasas | 0 | 1,467,184 | NA | $ | 27.96 | NA | 97.0 | % | ||||||||

| Canoga Park | 0 | 157,704 | NA | $ | 19.80 | NA | 94.2 | % | ||||||||

| Chatsworth | 0 | 929,249 | NA | $ | 18.36 | NA | 85.3 | % | ||||||||

| Granada Hills | 0 | 101,000 | NA | $ | 27.00 | NA | 98.2 | % | ||||||||

| Mission Hills | 0 | 158,730 | NA | $ | 24.60 | NA | 97.7 | % | ||||||||

| Northridge | 0 | 521,419 | NA | $ | 24.60 | NA | 93.8 | % | ||||||||

| Palmdale | 0 | 41,500 | NA | $ | 14.40 | NA | 84.1 | % | ||||||||

| Panorama City | 0 | 175,642 | NA | $ | 18.60 | NA | 89.2 | % | ||||||||

| Tarzana | 0 | 579,000 | NA | $ | 22.56 | NA | 93.1 | % | ||||||||

| Valencia | 0 | 1,987,209 | NA | $ | 31.20 | NA | 90.6 | % | ||||||||

| Van Nuys | 0 | 1,025,752 | NA | $ | 24.24 | NA | 97.5 | % | ||||||||

| West Hills | 0 | 740,583 | NA | $ | 27.00 | NA | 93.6 | % | ||||||||

| Westlake Village (LAC) | 0 | 1,534,824 | NA | $ | 26.04 | NA | 97.2 | % | ||||||||

| Total/Weighted Average Non DE Submarkets | 0 | 10,177,698 | NA | $ | 25.90 | NA | 92.9 | % | ||||||||

Tri-Cities | ||||||||||||||||

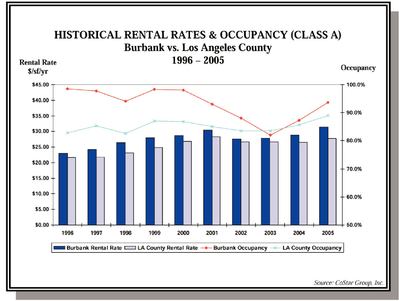

| Burbank | 420,949 | 5,744,318 | $ | 37.20 | $ | 32.76 | 100.0 | % | 95.2 | % | ||||||

| Total/ Weighted Average DE Submarkets(2) | 420,949 | 5,744,318 | $ | 37.20 | $ | 32.76 | 100.0 | % | 95.2 | % | ||||||

Arcadia/Monrovia | 0 | 1,324,734 | NA | $ | 24.48 | NA | 95.5 | % | ||||||||

| Glendale | 0 | 6,392,484 | NA | $ | 29.76 | NA | 86.9 | % | ||||||||

| North Hollywood | 0 | 946,460 | NA | $ | 23.28 | NA | 97.3 | % | ||||||||

| Pasadena | 0 | 8,638,578 | NA | $ | 30.24 | NA | 96.6 | % | ||||||||

| Studio City | 0 | 316,085 | NA | $ | 31.20 | NA | 99.5 | % | ||||||||

| Universal City | 0 | 1,405,690 | NA | $ | 32.88 | NA | 93.5 | % | ||||||||

| Total/Weighted Average Non DE Submarkets | 0 | 19,024,031 | NA | $ | 29.54 | NA | 93.1 | % | ||||||||

TOTAL/WEIGHTED AVERAGE DE SUBMARKETS | 10,875,357 | 50,581,138 | $ | 35.28 | $ | 31.56 | 93.2 | % | 92.8 | % | ||||||

TOTAL/WEIGHTED AVERAGE NON- DE SUBMARKETS | 0 | 39,662,110 | $ | 29.02 | 93.5 | % | ||||||||||

TOTAL/WEIGHTED AVERAGE LOS ANGELES COUNTY(3) | 10,875,357 | 90,243,248 | $ | 35.28 | $ | 29.56 | 93.2 | % | 93.4 | % | ||||||

Source: CB Richard Ellis (other than Douglas Emmett data)

19

- (1)

- For Douglas Emmett properties, represents leases commenced on or before June 30, 2006 and calculated as rentable square feet less available square feet divided by rentable square feet.

- (2)

- Weighted average for both Douglas Emmett properties and submarket based on Douglas Emmett rentable square feet.

- (3)

- Weighted average based upon Douglas Emmett properties' square footage for Douglas Emmett submarkets, otherwise based upon the overall submarket square footage.

As outlined in the table below, over the past five years, new supply growth in Douglas Emmett's nine Los Angeles County office submarkets has been limited with approximately 3.1 million square feet of new additions from 2001 to 2005. This represents an average increase of only 1.1% per year in Class-A inventory across these submarkets. Of the 3.1 million total square feet delivered over the five-year period, approximately 60% of the total was concentrated in the Burbank and Century City submarkets. Additionally, over this time period, there were no new significant office deliveries in the Westwood, Brentwood and Sherman Oaks/Encino submarkets. Within Douglas Emmett's Los Angeles County submarkets, the following developments are expected over the three-year span from 2006 to 2008: 194,000 square feet planned in the Santa Monica submarket; two buildings totaling approximately 500,000 square feet planned in the Warner Center/Woodland Hills submarket; and one new building in the Century City submarket totaling 780,000 square feet of which 300,000 square feet has been pre-leased. In addition, in the Burbank submarket, where Douglas Emmett owns one building that is currently 100% leased to a single tenant through 2019, 180,000 square feet of new office space was completed in 2006, while an additional 1.1 million square feet is planned and 370,000 square feet is proposed over the three-year span from 2006 to 2008. Assuming all current planned and proposed construction in the Douglas Emmet submarkets is completed by 2008, this pipeline represents an increase in Class-A inventory of 3,124,000 square feet over the period or approximately 1.9% per year across the Douglas Emmett submarkets. Excluding the Burbank submarket, this increase would be 1,474,000 square feet over the period or approximately 1.1% per year. No other significant office space in the Douglas Emmett submarkets is currently under construction, planned to begin construction or proposed during this period.

Historical Los Angeles New Supply

Douglas Emmett Office Submarkets

| | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | Totals | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Brentwood | — | — | — | — | — | — | — | — | — | — | — | |||||||||||

| Olympic Corridor | — | — | — | — | — | — | 151,019 | — | — | — | 151,019 | |||||||||||

| Century City | — | — | — | — | — | — | — | 775,037 | — | — | 775,037 | |||||||||||

| Santa Monica | 40,500 | — | — | 340,103 | 878,203 | — | — | — | 76,000 | — | 1,334,806 | |||||||||||

| Beverly Hills | — | — | — | — | 82,193 | 84,000 | — | 163,811 | — | — | 330,004 | |||||||||||

| Westwood | — | — | — | — | — | — | — | — | — | — | — | |||||||||||

| Sherman Oaks/Encino | — | — | — | — | — | — | — | — | — | — | — | |||||||||||

| Warner Center/Woodland Hills | — | — | — | — | 286,985 | 357,587 | 92,878 | 179,342 | — | 179,342 | 1,096,134 | |||||||||||

| Burbank | — | 95,400 | 215,000 | — | 95,700 | 155,000 | 621,597 | — | — | 269,231 | 1,451,928 | |||||||||||

| Total | 40,500 | 95,400 | 215,000 | 340,103 | 1,343,081 | 596,587 | 865,494 | 1,118,190 | 76,000 | 448,573 | 5,138,928 | |||||||||||

Source CoStar Group, Inc.

20

The following information is based on Eastdil Secured defined markets consisting of Class A office buildings considered to be most competitive to Douglas Emmett properties. In defining these markets, Eastdil Secured relied on its market expertise as well as analyzed raw market data from CoStar and CB Richard Ellis. Specific buildings have been excluded from the market due to quality or use in order to provide the most meaningful comparison.

Downtown Santa Monica: The CB Richard Ellis defined Santa Monica submarket consists of 7,619,589 square feet of Class A and B office space. Eastdil Secured separates Santa Monica into two distinct office submarkets: Downtown and East Santa Monica. The Eastdil Secured defined Downtown Santa Monica submarket consists of 1,894,305 square feet of Class A office space. Douglas Emmett owns 860,159 square feet of Class A office space in seven buildings within the Santa Monica submarket. All seven buildings are located in downtown Santa Monica, a market that commands the highest average asking rents of any office market in Los Angeles County. Downtown Santa Monica features numerous shopping, dining and entertainment attractions and is located near the executive housing areas of northern Santa Monica, Brentwood, Pacific Palisades, Malibu and is adjacent to the Pacific Ocean, public beaches and extensive restaurant and retail amenities. In addition, the City of Santa Monica adopted a plan in the mid-1980s that imposed stringent limits on development in the downtown area. Provisions include limiting new building heights to four stories and strict FAR restrictions. As a result, most of the new construction in Santa Monica has occurred in the eastern part of the city, a less desirable market compared to downtown. For example, new development entitlements that were granted in the late 1980s and that had a 10-year expiration allowed for the construction of 1.2 million square feet of new office space, Water Garden, that was completed between 1999 and 2000. This cluster of development lies just north of the 10 Freeway surrounding the Water Garden development at the intersection of Cloverfield and Colorado Boulevards. While Douglas Emmett's share of the overall CB Richard Ellis defined Santa Monica submarket is 11.3%, their share of the Eastdil Secured defined downtown submarket, where average asking rents are 17% higher than in eastern Santa Monica, is 45.4%.

The outlook for Santa Monica remains strong in terms of limited projected deliveries of new office space. Excluding the 194,000 square feet of new development (South and East phases of the Lantana office project), which represents 2.5% of the total Class A and B office inventory, there are no remaining specific plan office entitlements left in Santa Monica. As such, the combination of low vacancy rates and the absence of new supply will provide the opportunity for significant rental rate growth in the foreseeable future.

| | Market* | Douglas Emmett Holdings | % of Market/ Rental Rate Premium | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Square Feet | 1,894,305 | 860,159 | 45.4 | % | |||||

| Average Asking Rents | $ | 52.52/yr | $ | 59.11/sf/yr | 12.5 | % | |||

*Eastdil Secured defined

21

Downtown Santa Monica—Top Tier Buildings

| Building | sf | Asking Rent $/sf/yr) | Owner | ||||

|---|---|---|---|---|---|---|---|

| 100 Wilshire | 256,968 | $ | 75.00 | Douglas, Emmett & Company | |||

| Portofino Plaza | 47,639 | $ | 57.00 | Mani Brothers Real Estate Investment | |||

| SeaRise | 124,116 | $ | 56.10 | Equity Office | |||

| First Federal Square | 221,181 | $ | 54.00 | Douglas, Emmett & Company | |||

| Palisades Promenade | 98,606 | $ | 54.00 | Douglas, Emmett & Company | |||

| Santa Monica Square | 77,375 | $ | 54.00 | Douglas, Emmett & Company | |||

| Second Street Plaza | 80,835 | $ | 54.00 | Douglas, Emmett & Company | |||

| Wilshire Palisades | 193,840 | $ | 51.00 | Equity Office | |||

| 1733 Ocean Ave | 84,724 | $ | 49.80 | Maguire Properties | |||

| Lincoln/Wilshire | 76,758 | $ | 47.40 | Douglas, Emmett & Company | |||

*Source: CoStar Group, Inc.

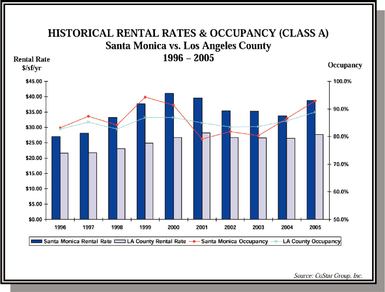

From 1996 to 2005, the 10-year average rental rate for Santa Monica was $35.01, a 38% premium over the Los Angeles County average of $25.39. Santa Monica's 10 year average occupancy is 86.2% versus 85.1% for Los Angeles County. As evidenced in the graph to the left, the Santa Monica market began a sustained recovery in occupancy rates beginning in 2004, followed by a significant recovery in rental rates beginning in 2005. Occupancy rates in this submarket increased from 80.3% in 2003 to approximately 93.0% in 2005 while rental rates increased from approximately $33.85 per square foot in 2004 to $38.80 per square foot in 2005, representing an increase of approximately 14.6%.

22

Santa Monica Demographics

| 2006 Population (estimated) | 89,191 | |||

| 1990 Population | 86,911 | |||

| Mean Household Income | $ | 92,687 | ||

| Median Household Income | $ | 58,715 | ||

| Mean Home Price | $ | 1,427,000 | ||

| Bachelor's Degree or higher | 54.4 | % |

Source: Claritas Site Reports 2006 & Public Records

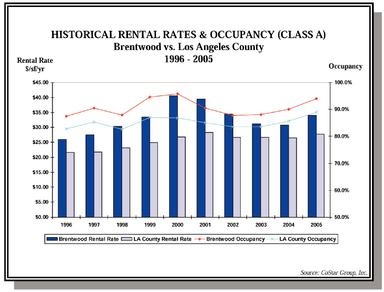

Brentwood: The CB Richard Ellis defined Brentwood submarket consists of 3,331,731 square feet of Class A and B office space, while the Eastdil Secured defined Brentwood submarket consists of 2,614,664 square feet of Class A office space. Douglas Emmett owns 1,390,625 square feet of Class A office space in 13 buildings within the Brentwood submarket.

The Brentwood submarket consists of two primary segments (1) the San Vicente Corridor, which is largely comprised of low and mid-rise buildings in one of the premier restaurant and retail districts in Los Angeles, and (2) the Wilshire Corridor, which is comprised of a variety of mid- and high-rise buildings located along Wilshire Boulevard, west of its intersection with San Vicente. The San Vicente market is characterized by numerous small tenancies, prominently featuring medical, legal, entertainment, and accounting professionals who reside in the upscale neighborhoods that immediately surround the San Vicente Corridor. As such, these tenants place significant value upon an office location that is proximate to their homes and clients, and are resistant to relocating their premises. The mid- and high-rise buildings along Wilshire Boulevard are occupied by somewhat larger and more prototypical office users, but feature relatively small floor plans and high-margin, front office tenancies are the norm. Like on the San Vicente Corridor, most decision makers place a high value on their office location.

Based on the CB Richard Ellis defined Brentwood market, Douglas Emmett owns over 40% of the Class A and B office space, however based on the Eastdil Secured defined Brentwood market, Douglas Emmett's office concentration is even higher—71.5% of the San Vicente Corridor and 45.3% of the Wilshire Corridor. Strict zoning restrictions including Proposition U, influential neighborhood groups and specific, stringent design standards create significant barriers to new development of all kinds, but especially competitive office development. The height limit along San Vicente Boulevard is three stories and on most of Wilshire Boulevard, the height limit is between three and six stories. It is noteworthy to mention that there have been no new Class A office building deliveries in Brentwood over the past 10 years and currently there are no new office deliveries projected in Brentwood from 2006 through 2008. While the combination of low vacancy rates and the absence of new supply will provide the opportunity to significantly increase rental rate growth in the foreseeable future, Brentwood may be temporarily impacted by the eventual disposition and development of the large amount of undeveloped land located in the vicinity of the Santa Monica (405) Freeway and Wilshire Boulevard that is currently owned by the Veterans Administration. It is noteworthy to mention that the approximately 400 acres of land was donated to the government in 1888 and over the last 100+ years, the Veterans Administration

23

has left the land largely untouched with no immediate or long term plans to sell/develop any portion of the land.

| | Market* | Douglas Emett Holdings | % of Market/ Rental Rate Premium | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Brentwood-San Vicente | ||||||||||

| Square Feet | 783,978 | 560,478 | 71.5 | % | ||||||

| Average Asking Rents | $ | 37.49/sf/yr | $ | 38.51/sf/yr | 2.7 | % | ||||

Brentwood-Wilshire | ||||||||||

| Square Feet | 1,830,686 | 830,147 | 45.3 | % | ||||||

| Average Asking Rents | $ | 36.38/sf/yr | $ | 34.35/sf/yr | -5.6 | % | ||||

Brentwood-Total | ||||||||||

| Square Feet | 2,614,664 | 1,390,625 | 53.2 | % | ||||||

| Average Asking Rents | $ | 36.71/sf/yr | $ | 36.03/sf/yr | -1.9 | % | ||||

*Eastdil Secured defined

Brentwood—Top Tier Buildings

| | sf | Asking Rent ($/sf/yr) | Owner | ||||

|---|---|---|---|---|---|---|---|

| Brentwood-San Vicente | |||||||

| Coral Plaza | 71,801 | $ | 37.20 | Douglas, Emmett & Company | |||

| 11777 San Vicente | 96,872 | $ | 37.20 | Douglas, Emmett & Company | |||

| Brentwood Executive Plaza | 89,660 | $ | 37.20 | Douglas, Emmett & Company | |||

| The Vintage Capital Bldg | 103,500 | $ | 37.20 | AIB Real Estate | |||

| Brentwood Square | 120,000 | $ | 33.00 | Brentwood Square L.P. | |||

Brentwood-Wilshire | |||||||

| World Savings Center | 482,974 | $ | 42.00 | Trizec Properties, Inc. | |||

| Wilshire Landmark I | 328,331 | $ | 36.95 | CA State Teachers Retirement System | |||

| Landmark II | 412,944 | $ | 35.40 | Douglas, Emmett & Company | |||

| 12400 Wilshire | 235,808 | $ | 33.60 | Douglas, Emmett & Company | |||

*Source: CoStar Group, Inc.

24

Brentwood Demographics

| 2006 Population (estimated) | 35,308 | |||

| 1990 Population | 33,521 | |||

| Mean Household Income | $ | 152,921 | ||

| Median Household Income | $ | 98,193 | ||

| Mean Home Price | $ | 1,900,000 | ||

| Bachelor's Degree or higher | 69.4 | % |

Source: Claritas Site Reports 2006 & Public Records

As shown in the above chart, over the last ten years, occupancy and rental rates in the Brentwood submarket have moved in line with and maintained their premium to the broader Los Angeles County market as a whole. From 1996 to 2005, the 10-year average rental rate for Brentwood was $32.74, a 29% premium over the Los Angeles County average of $25.39. Brentwood's 10-year average occupancy was 90.7% versus 85.1% for Los Angeles County. Due largely to the economic recovery that began in 2003, occupancy rates in this submarket have been growing steadily from 87.8% in 2002 to approximately 94.0% in 2005, representing an increase of 6.2%. Rental rates reached a five-year low in 2004 and began to recover significantly in 2005, increasing from $30.72 per square foot in 2004 to $34.03 per square foot in 2005, representing an increase of 10.8%.

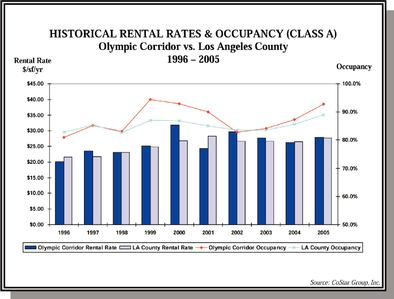

Olympic Corridor: While the CB Richard Ellis defined Olympic Corridor submarket consists of 2,327,630 square feet of Class A and B office space, the Eastdil Secured defined Olympic Corridor submarket consists of 2,216,347 square feet of Class A office space. Douglas Emmett owns 922,405 square feet of Class A office space (nearly 40% of the total CB Richard Ellis defined Class A and B inventory) in four buildings within the Olympic Corridor submarket.

Located in West Los Angeles just west of the 405 Freeway and north of Interstate 10 and clustered near the intersection of Olympic and Sepulveda Boulevard, the Olympic Corridor is an office hub that offers relative affordability and access (both freeway and surface streets) to office users who require a Westside location, but can forego the greater prestige of Santa Monica or Brentwood. Olympic Boulevard is a main east-west artery developed and named in connection with the 1932 Olympics in Los Angeles, running from Santa Monica to Downtown Los Angeles. Buildings in this market have attracted a diverse, high-quality tenant base, including top law firms, investment banks, and prominent

25

companies in the entertainment, technology and media sectors. Tenants with a significant presence in the market include Manatt, Phelps & Phillips, Monster.com, and AT&T. The market features a broad array of amenities, including high-end restaurants, neighborhood-serving retail establishments, and several fitness centers. Douglas Emmett has developed a significant presence in this market, amassing four of what we consider to be the top six buildings in the market.