Exhibit 99.1

Proposed Transaction for Shareholder

Approval

November 2007

Safe Harbor Statement

This presentation has been filed with the SEC on November 7, 2007 as part of a Current Report on Form 8-K of the Company. The Company is

holding presentations for its security holders, as well as certain other persons, regarding the proposed vessel acquisition. A copy of the complete

presentation is available at the Securities and Exchange Commission's ("SEC") website (http://www.sec.gov).

Except for the historical information contained herein, this presentation contains among other things, certain forward looking statements, within the

meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Such statements may include, without limitation,

statements with respect to the Company's plans, objectives, expectations and intentions and other statements identified by words such as

“may,” “could,” “would,” “should,” “believes,” “expects,” “anticipates,” “estimates,” “intends,” “plans” or similar expressions. These statements are

based upon the current beliefs and expectations of the Company's management and are subject to significant risks and uncertainties, including those

detailed in the Company's filings with the Securities and Exchange Commission ("SEC"). Actual results, including, without limitation, operating or

financial results, if any, may differ from those set forth in the forward-looking statements. These forward-looking statements involve certain risks and

uncertainties that are subject to change based on various factors (many of which are beyond the Company's control).

Forward-looking statements include statements regarding:

The delivery to and operation of assets by the Company;

The Company's future operating or financial results;

Future, pending or recent acquisitions and business strategy;

Areas of possible expansion, and expected capital spending or operating expenses; and

Dry bulk market trends, including charter rates and factors affecting vessel supply and demand.

The financial information and data contained in this presentation is unaudited and does not conform to the SEC's Regulation S-X. Accordingly, such

information and data may not be included, or may be presented differently, in the Company's proxy statement to solicit shareholder approval for its

proposed business combination. This presentation includes certain estimated financial information and forecasts (EBIT, EBITDA, and Time Charter

Equivalent Revenue) that are not derived in accordance with generally accepted accounting principles ("GAAP"), and which may be deemed to be non-

GAAP financial measures within the meaning of Regulation G promulgated by the SEC.

2

Safe Harbor Statement

The Company believes that the presentation of these non-GAAP measures provides information that is useful to the Company’s shareholders as they

indicate the ability of the Company to meet capital expenditures, working capital requirements and other obligations, and make distributions to

its shareholders. However, EBIT, EBITDA and Time Charter Equivalent Revenue should be considered in addition to, and not as substitutes for, or

superior to, operating income, cash flows, revenue or other measures of financial performance prepared in accordance with GAAP. EBIT, EBITDA and

Time Charter Equivalent Revenue may not be comparable to similarly titled measures reported by other companies.

The Company undertakes no obligation to publicly update or revise any forward-looking statements or other information or data contained in this

presentation, whether to reflect any change in our expectations with respect to such statement or any change in events, conditions or circumstances

on which any statement is based, or otherwise.

The Company and its directors and executive officers may be deemed to be participants in the solicitation of proxies for the special meeting of the

Company’s shareholders to be held to approve the proposed vessel acquisition and other matters. Each of the Company’s officers and directors are

also shareholders of the Company and have waived their rights to any liquidation distribution the Company makes with respect to shares they acquired

before the IPO. Therefore, their securities will be worthless if the Company does not acquire a target business within two years of the IPO date, as

required by its Articles of Incorporation and as more fully described in its prospectus relating to the initial public offering of its securities.

Shareholders of the Company and other interested persons are advised to read the Company’s preliminary proxy statement and definitive proxy

statement, when available, in connection with the Company’s solicitation of proxies for the special meeting because these documents will contain

important information. The definitive proxy statement will be mailed to shareholders as of a record date to be established for voting on the proposed

vessel acquisition and other matters. Shareholders will also be able to obtain a copy of the definitive proxy statement, without charge, by directing a

request to:

Oceanaut, Inc.

17th Km National Road Athens-Lamia & Finikos Street

145 64 Nea Kifisia

Athens, Greece

The preliminary proxy statement and definitive proxy statement, once available, can also be obtained, without charge, at the Securities and Exchange

Commission’s website at http://www.sec.gov.

3

Oceanaut Overview

Oceanaut is a SPAC trading on the AMEX (ticker: OKN)

Formed to pursue a business combination in the shipping industry

Raised $150 million in proceeds via an Initial Public Offering in March 2007

$8.00 Unit – 1 common share and 1 warrant

Current unit price $10.71 up 33.9% since IPO

Oceanaut entered into a definitive agreement to acquire 9 dry bulk carriers

from companies controlled by the Restis family in October 2007

Vessel purchase price of $700 million

4 vessels currently on the water

2 vessels scheduled for delivery in 2008

3 vessels scheduled for delivery in 2009

Note: Unit price as of market close 11/6/2007.

4

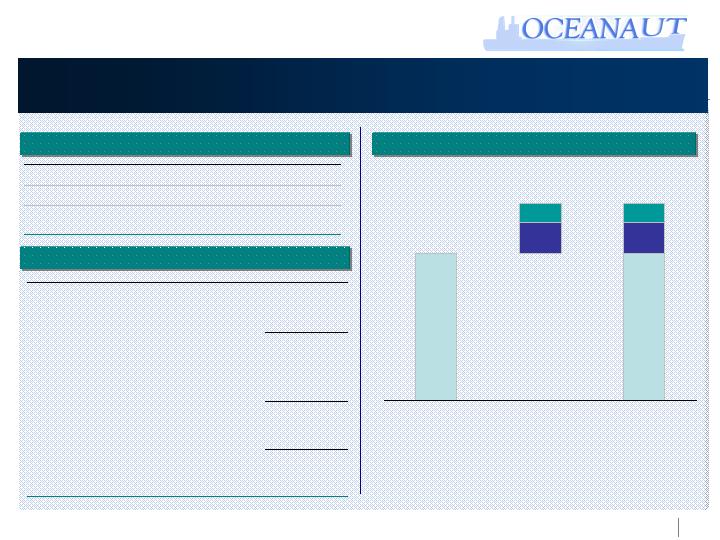

Transaction Structure

Transaction Sources

Transaction Uses

Post Closing Ownership (2)

Note: Sources and Uses exclude fees relating to proxy and debt financing.

(1) Expected to be provided by a credit facility, proceeds from the exercise of warrants and / or other sources. Payment to shipyard for newbuilds.

(2) Does not include shares underlying warrants.

$709.5

Total

260.8

Additional Funding Post Closing(1)

221.8

Funded Debt at Closing

82.5

Proceeds from Private Placement

$144.4

Cash in Trust

Sources

5.0

Working Capital

65.2

Initial Payment for Newbuilds

$709.5

Total

260.8

Additional Payment for Newbuilds

4.5

Deferred Underwriters’ Fee

$374.0

Purchased Vessels at Closing

Uses

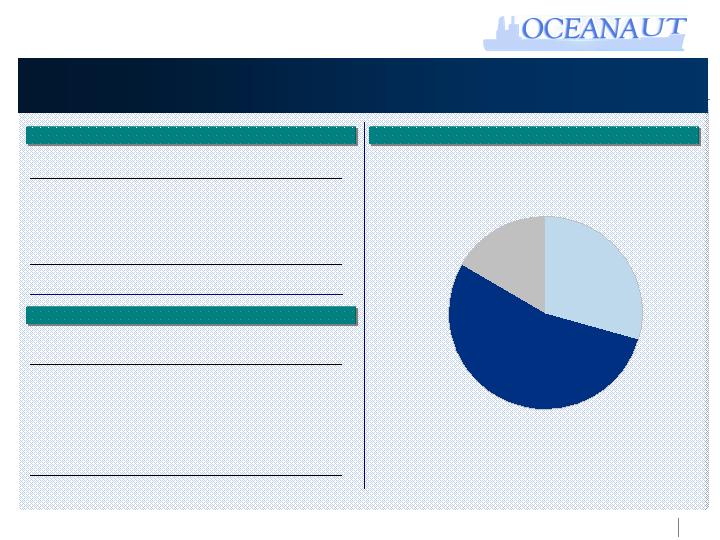

Public

53.8%

Restis Family

29.6%

Excel Maritime /

Insiders

16.7%

$ in millions

5

$50.6

Value of Warrants

$299.1

Pro Forma Market Capitalization

$2.31

Oceanaut Warrant Price as of 11/6/07

21.9

Warrants Outstanding(2)

9.5x - 10.5x

Public Comps

7.8x

Implied FV / Est. Full Fleet EBITDA(1)

$815.5

Implied Firm Value

465.8

Net Debt (3)

$349.7

Diluted Pro Forma Market Capitalization

34.9

Total Common Shares

10.3

Private Placement Shares

24.6

Existing Common Shares

$8.57

Oceanaut Share Price as of 11/6/07

6.7x

Transaction Value / Est. Full Fleet EBITDA(1)

105

Estimated Full Fleet EBITDA(1)

$700

Acquisition Price

Value Creation

Significant Upside Remains

Potential Multiple Expansion

Pro Forma Valuation

Note: Vessels under charters which expire prior to achieving full run rate are assumed to operate under current forward market estimates.

(1) Represents full year of EBITDA in which all 9 vessels are on the water and generating revenue.

(2) Excludes founder’s warrants.

(3) Assumes debt is used to fund additional payment for newbuilds. $482.6 of total debt, $5.0 million of cash held for working capital and $11.8 mm of cash on balance sheet. Assumes warrants are

not yet exercised.

7.8x

7.8x

1.7x

9.5x

10.5x

2.7x

Pro Forma Firm

Value

Value Creation

Fully Distributed

$ in millions

6

Approximate

LQA

Firm Value /

# of

Average

(a)

Payout

FV/

Dividend

2008E

Vessels

Fleet Age

DWT

Ratio

(b)

TAV

Yield

EBITDA

21

5.4

2.4

100%

131.9%

5.4%

11.8x

49

2.0

2.7

100

102.3

6.0

14.0

9

11.7

0.7

85

137.8

7.6

6.8

11

6.5

0.7

75

110.6

7.6

6.8

32

7.0

2.7

55

127.8

3.9

9.5

37

5.2

4.1

50

89.9

4.6

9.9

54

4.8

5.4

20

112.9

1.6

8.1

Mean

30

6.1

2.7

69%

116.2%

5.2%

9.6x

Median

32

5.4

2.7

75

112.9

5.4

9.5

9

6.1

0.8

114.7%

7.7x

(d)

(e)

(c)

High Payout Dry Bulk Peer Comparison

Note: Share prices as of November 6, 2007. Fleet information includes announced transactions and ordered newbuilds.

(a) In years.

(b) Dividend as percent of Distributable Cash Flow (DCF); DCF is defined as 2007E EBITDA - Interest Expense - Drydock.

(c) Total Asset Value does not include the value of the recently announced acquisition of 2 Panamax vessels.

(d) 21 of 26 newbuilds have charters of 10 or more years.

(e) Represents full year of EBITDA in which all 9 vessels are on the water and generating revenue.

7

Investment Highlights

Quality of Vessels and Diversity of Fleet

Weighted average age of ~6 years(1)

2 Capesize, 4 Panamax and 3 Supramax

Strong Industry Fundamentals

Demand for raw materials in developing countries has been driving growth in industry and

increases in rates

Extended delivery times for newbuildings in dry bulk

Predictable Revenues

Charter Parties with South African Marine provide predetermined charter rates

Sponsors’ Value Adding Experience

Significant knowledge and experience in the shipping industry in general and dry bulk in particular

Valuation Upside

(1) Weighted average based on dwt.

8

Company Overview

Oceanaut, Inc.

Company Overview

Oceanaut will operate 9 dry bulk carriers

2 Capesize

4 Panamax

3 Supramax

Carrying capacity of 809,000 deadweight tons

Vessels will be commercially managed by Safbulk, an affiliate of the Restis Family

Vessels will be technically managed by Maryville Maritime, a subsidiary of Excel

Maritime Carriers

7 of the 9 vessels will be on time charters to South African Marine Corporation, an

affiliate of the Restis Family

10

Distinguishing Factors and Business Strategy

Established Customer Relationships

Experienced Sponsors

Highly Efficient Operations

Staggered Charter Maturities

Modern and Diversified Fleet

Fleet Growth Potential

Intend to Pay Quarterly Dividends

11

Fleet Profile

$700.0

~6.1(3)

809,000

Total

36

33.0

64.0

Apr-09

55,000

Supramax

TBN

36

36.0

69.5

Oct-08

55,000

Supramax

TBN

36

42.0

69.5

Jun-08

55,000

Supramax

TBN

18

38.0

61.0

Jun-93

73,500

Panamax

Miden Max

24

55.0

63.5

Jun-94

73,500

Panamax

Hamburg Max

24

55.0

60.5

Jun-93

73,500

Panamax

Bremen Max

12

28.5

50.0

Jun-94

73,500

Panamax

Bergen Max

60

45.0

131.0

Dec-09

175,000

Capesize

TBN

60

$45.0

$131.0

Oct-09

175,000

Capesize

TBN

Charter

Period(2)

Gross

Charter

Rate

Price (mm)

Year Built

Dwt(1)

Type

Name

(1) All Dwt numbers are approximate.

(2) Charter Period in Months from vessel delivery date.

(3) Calculated as of delivery of final newbuild; weighted average based on dwt.

12

Overview of Excel Maritime

Excel Maritime Carriers Ltd. (NYSE: EXM) was incorporated in 1998

Has been a publicly traded company since 1998

Headquartered in Athens, Greece

Excel has an on the water fleet of 16 vessels with 2 additional vessels expected to be delivered in 4Q2007

10 Panamax

6 Handymax

2 Supramax to be delivered in December 2007

Maryville Maritime Inc. provides technical management to Excel

Established in 1983

First ship management company in Greece to voluntarily receive simultaneous ISM and ISO Safety and Quality Systems Certification in February 1996; currently ISO 9001:2000 and ISO 14001:2004 compliant

Wholly owned subsidiary of Excel Maritime since 2001

Excel’s Market Capitalization was $1.2 bn as of 11/6/07

Share price of $61.74

Firm value of $1.3 bn

FV / 2008E EBITDA of 6.8x

LQA dividend yield of 1.3%

13

Overview of the Restis Family

The Restis family has been engaged in international shipping for over 40 years

Companies associated with the Family manage, own or operate 62 vessels with an additional 30 vessels on order

Combined carrying capacity in excess of 7,700,000 dwt

Family members have strategic minority holdings in companies controlling an additional 92 vessels

Expertise in various sectors of the shipping industry, including: dry bulk carriers, product tankers, crude oil carriers,

refrigerated cargo ships and cruise ships

Companies associated with the Restis family include:

South African Marine Corp.

Safbulk Pty. Ltd.

Enterprises Shipping and Trading S.A.

First Financial Corp.

Golden Energy Management S.A.

Active in other sectors including: banking, energy production and distribution, media,

food services, ship repair and conversion, leisure, financial and advisory services,

trading, real estate investment and development and aviation

Golden Energy Marine Corp.

SwissMarine Corp.

Freeseas Inc.

Paramount Tankers Corp.

Bulk Energy Transportation (Holdings) Limited

14

Overview of South African Marine

South African Marine was established in 1946

From 1946-1999, South African Marine grew into the largest shipping group on the

African continent

In 1999, the Restis family acquired the non-liner business of South African Marine

from a subsidiary of Old Mutual

Included a fleet of 13 dry bulk vessels, as well as the South African Marine and

Safbulk shipping brand names

Under the Restis family, Safbulk has expanded its operations

significantly

Commercially manages over 50 dry bulk vessels

Transports more than 35 mm tons or cargo annually

Expected to generate over $500 mm in revenues in 2007

South African Marine today is held by South African Marine S.A.

Dedicated chartering company with a fleet of 16 vessels including the Oceanaut

ships

15

Financial Overview

Oceanaut, Inc.

Estimated Annual Run Rate Performance

Run Rate Operating Performance

Total

Newbuilds

Ships on

Water Today

$45

(2)

(7)

$55

$60

(2)

(8)

$70

$105

EBITDA

(4)

General & Administrative Expense

(15)

Operating Expenses

$125

Net Charter Revenue

Note: Represents full year of EBITDA in which all 9 vessels are on the water and generating revenue.

Vessels under charters which expire prior to achieving full run rate are assumed to operate under current forward market estimates.

Numbers do not add due to rounding.

Assumptions:

Estimated Full Fleet EBITDA assumes all 9 vessels are on the water and generating revenue

Rates are based on chartering agreements

For charter contracts expiring prior to achieving full run rate, rates are based on forward industry

estimates

$55.0 thousand / day in 2009

$38.0 thousand / day in 2010

No taxes

$ in millions

17

Capital Structure and Dividend Policy

Oceanaut is in the process of finalizing a credit facility to help finance the fleet

acquisition

Over the long-term, Oceanaut will target a capital structure comparable to dividend oriented dry

bulk peers

Oceanaut plans to pay a quarterly dividend

Target payout is expected to be inline with industry peers

Oceanaut will update the market once a dividend policy has been set

18

Industry Highlights

Oceanaut, Inc.

Major Dry Bulk Seaborne Trade Routes

Source: Derived from industry sources.

To

Asia

From

Americas

Iron Ore

Coal

Grain

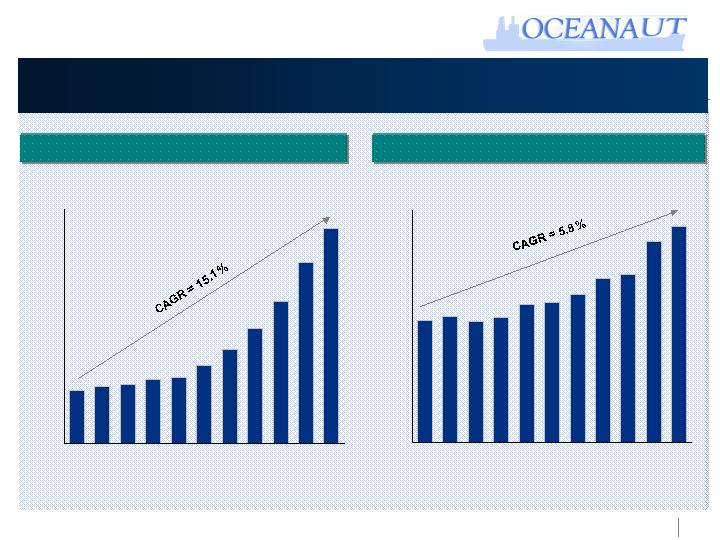

20

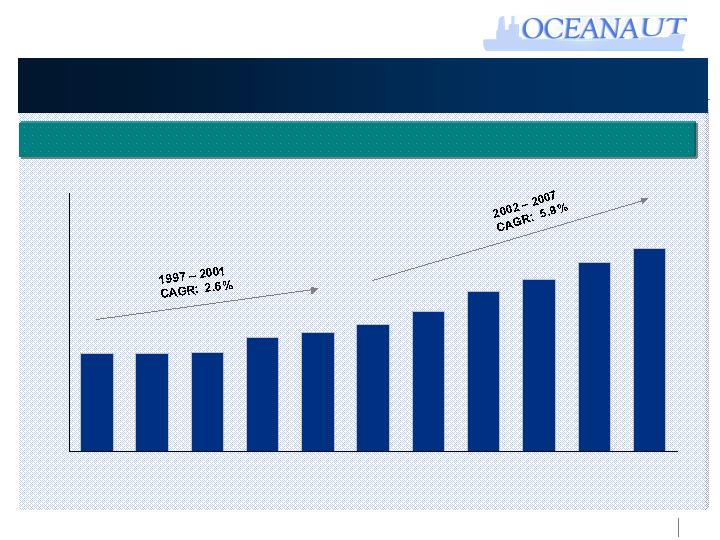

2,966

2,829

2,666

2,548

2,361

2,230

2,155

2,107

1,964

1,954

1,948

1,000

1,500

2,000

2,500

3,000

3,500

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007E

Dry Bulk Industry Performance

Source: Clarkson.

Seaborne Trade Growth

21

0.0

0.2

0.4

0.6

0.8

2000

2006

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

India

US

Europe

China

Japan

South

Korea

Increasing Steel Demand…

Rapid urbanization leads to increasing per capita consumption in China and India

Indian steel consumption expected to increase 400% to 200mm tons by 2020

India expanding investment in cities – 100mm people to move into urban areas in next 10 years

Tons per Urbanized Capita (2006)

China – Tons per Urbanized Capita

22

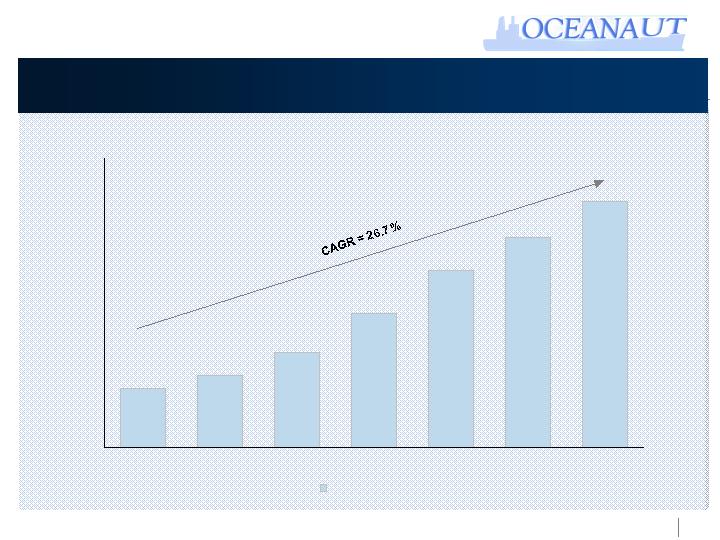

…Driving Steel Production and Dry Bulk Market

(Million Tons)

Indian Steel Production

Chinese Steel Production

(Million Tons)

0

50

100

150

200

250

300

350

400

450

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

0

5

10

15

20

25

30

35

40

45

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Source: Clarkson.

23

China’s Iron Ore Import Growth

Source: Clarkson.

(Million Tons)

0

50

100

150

200

250

300

350

400

450

2001

2002

2003

2004

2005

2006

2007E

Iron Ore Import (MT)

24

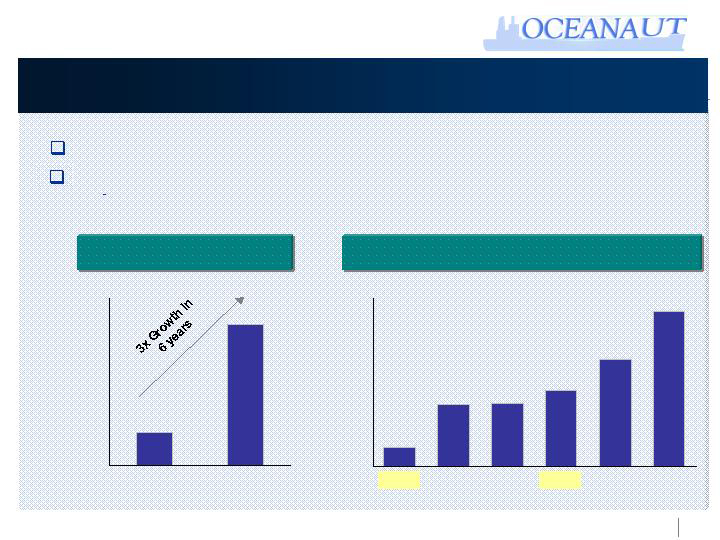

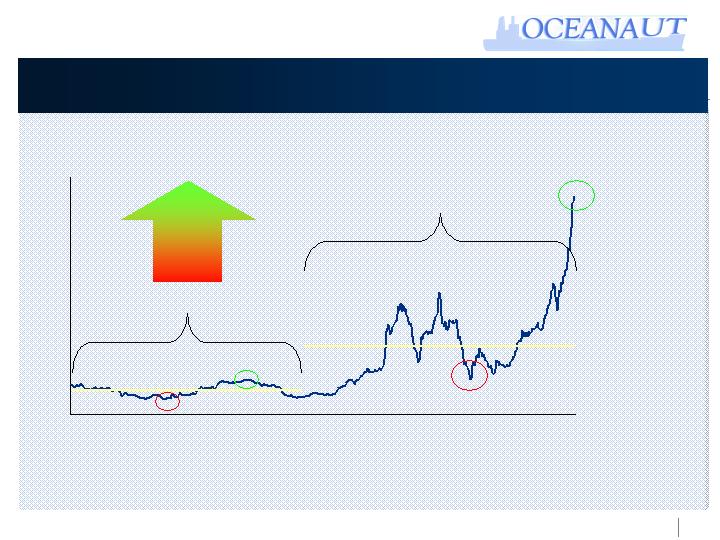

Baltic Dry Index Performance

Source: Bloomberg.

0

2,000

4,000

6,000

8,000

10,000

12,000

1/10/1997

3/5/1999

4/27/2001

6/20/2003

8/12/2005

10/5/2007

1997 – 2001 Average 1,235

2002 – 2007 Average 3,440

+ 178%

25

Dry Bulk Orderbook

Source: Clarkson and Drewry.

Existing Fleet (M DWT)

Deliveries Jan - Sep 07

Million DWT on Order

9/30/2007

Vessels

Million DWT

2007

2008

2009

2010

2011

2012

2013

Total

Capesize

128.10

42

7.86

2.39

11.32

20.03

40.44

17.32

3.77

0.36

103.49

Panamax

106.70

70

5.74

2.21

8.29

10.12

17.03

12.11

0.93

-

56.43

Handymax

75.20

76

3.96

1.53

8.38

13.79

12.52

5.35

1.00

-

46.52

Handysize

75.10

63

1.55

0.76

3.94

6.08

4.42

1.82

0.54

-

19.10

Total

385.10

251

19.11

6.88

31.92

50.02

74.41

36.60

6.24

0.36

225.54

% of Existing Fleet

-

-

5.0%

1.8%

8.3%

13.0%

19.3%

9.5%

1.6%

0.1%

58.6%

9/30/2007

9/30/2007

Existing Fleet (20+ years)

Existing DWT (vessels 20+ years)

Number of Vessels

% of Fleet

Total DWT (mm)

% of Orderbook

Capesize

140

18.6%

23.1

22.3%

Panamax

348

23.9%

23.3

41.3%

Handymax

389

24.8%

17.4

37.4%

Handysize

1,748

62.2%

47.1

246.6%

Total

2,625

39.8%

110.9

49.2%

26

Conclusion

Quality of Vessels and Diversity of Fleet

Weighted average age of ~6 years(1)

2 Capesize, 4 Panamax and 3 Supramax

Strong Industry Fundamentals

Demand for raw materials in developing countries has been driving growth in industry

and increases in rates

Extended delivery times for newbuildings in dry bulk

Predictable Revenues

Charter Parties with South African Marine provide predetermined charter rates

Sponsors’ Value Adding Experience

Significant knowledge and experience in the shipping industry in general and dry bulk

in particular

Valuation Upside

(1) Weighted average based on dwt.

27