2779 Highway 24 Lawler, Iowa 52154 Telephone (563) 238-5555 Fax (563) 238-5557 www.homelandenergysolutions.com |

December 2, 2011

United States Securities and Exchange Commission

Division of Corporation Finance

Washington, D.C. 20549-7010

Mail Stop 7010

Attn: Rufus Decker

Accounting Branch Chief

Re: Homeland Energy Solutions, LLC

Form 10-K for the Year Ended December 31, 2010

Filed February 18, 2011

Form 10-Q for the Period Ended June 30, 2011

Filed August 12, 2011

File No. 0-53202

Dear Mr. Decker:

Homeland Energy Solutions, LLC (the "Company") is in receipt of your letter dated November 8, 2011, providing comments to the filings referenced above. We reviewed your comments and the purpose of this letter is to provide the Company's responses to your comments. In order to facilitate your review of the responses, set forth below are each of your comments immediately followed by the responses. It is our understanding that actual amendments of the previously-filed reports mentioned in your letter are not required.

Form 10-K for the Year Ended December 31, 2010

Financial Statements

Report of Independent Registered Public Accounting Firm, Page 28

Report of Independent Registered Public Accounting Firm, Page 29

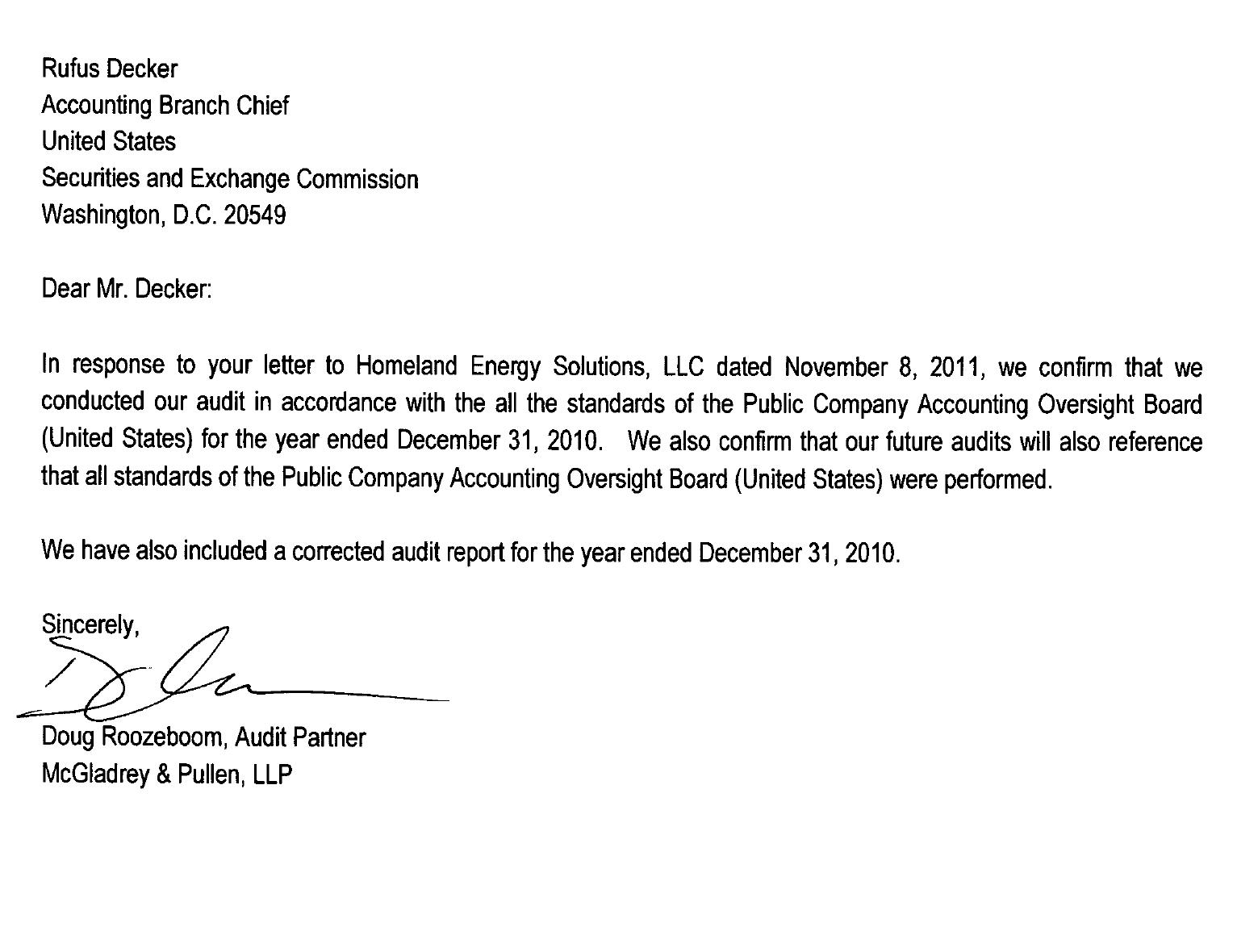

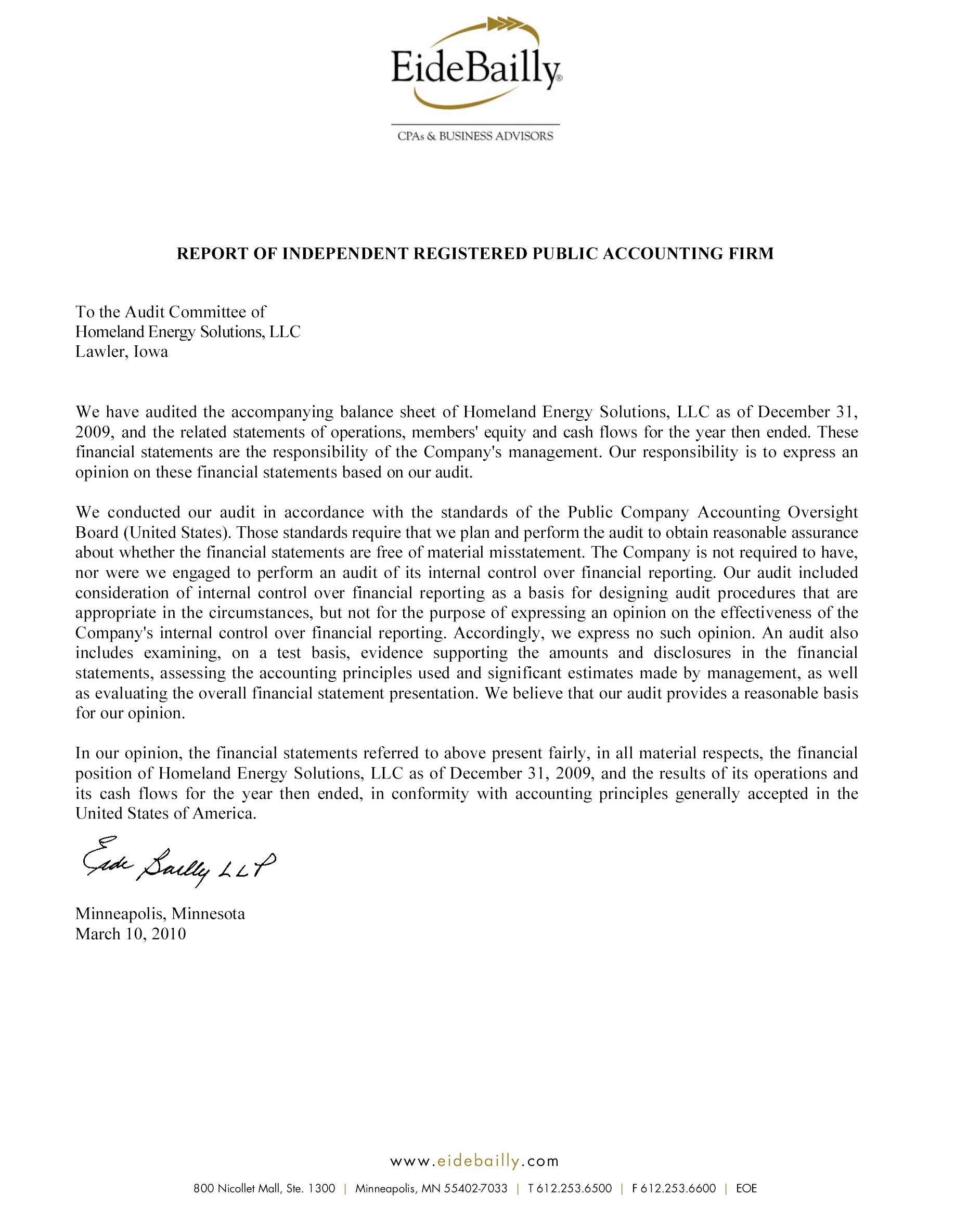

| 1. | The standards of the Public Company Accounting Oversight Board (United States) encompass more than just auditing standards. Please make arrangements with each of your auditors to provide us with a written signed letter confirming that their audits were conducted in accordance with all of the standards of the PCAOB instead of just the auditing standards. Each letter should confirm that future audit reports will reference to the standards of the PCAOB rather than solely the auditing standards and also include a corrected and signed audit report. Please include the letters from each of your auditors as an attachment to your supplemental response. See SEC Release 33-8422 and PCAOB Auditing Standard No. 1. |

RESPONSE: Please see the attached letters and revised audit reports for the year ended December 31, 2010 from McGladrey & Pullen, LLP and Eide Bailly, LLP as requested.

Item 9A. Controls and Procedures, page 45

Internal Control Over Financial Reporting, page 45

Management's Annual Report on Internal Control over Financial Reporting, page 45

| 2. | We note the following qualification in the last paragraph under this heading: |

This report shall not be deemed to be filed for purposes of Section 18 of the Securities Exchange Act of 1934, or otherwise subject to the likabilities of that section, and is not incorporated by reference into any filing of the Company, whether made before or after the date hereof, regardless of any general incorporation language in such filing.

Given that Item 308T of Regulation S-K, which permitted the above qualification, does not apply to reports for fiscal years ending after December 15, 2010, please supplementally acknowledge your understanding that your management's report on internal control over financial reporting in your 2010 Form 10-K is filed for purposes of Section 18 of the Exchange Act and is otherwise subject to the liability provisions of that section. Please also exclude the above qualification from your future filings.

RESPONSE: The Company acknowledges and understands that the management's report on internal control over financial reporting in its 2010 Form 10-K is filed for purposes of Section 18 of the Exchange Act and is otherwise subject to the liability provisions of that section. The above listed qualification will be excluded from the Company's future filings.

Item 15. Exhibits, Financial Statement Schedules, page 47

3. Please tell us what consideration you gave to filing or incorporating by reference the following as exhibits: (i) First and Second Amendments to the Master Loan Agreement dated November 30, 2007, and (ii) the agreement(s) pursuant to which you have procured corn from Comeback Farms Inc., an entity owned by Kyle Wendland, the son of your chief executive officer, Walter Wendland. Please refer to Item 601(b)(10) of Regulation S-K.

RESPONSE: With respect to the First and Second Amendments to the Master Loan Agreement dated November 30, 2007, both were ministerial amendments to the Master Loan Agreement and did not materially alter the terms of the Master Loan Agreement. The First Amendment to the Master Loan Agreement changed the wording of the definition of "Working Capital" but did not materially change the manner in which the Company's loan covenants were calculated. The First Amendment to the Master Loan Agreement also provided a different form that the Company was required to use to report compliance with its loan covenants. The Second Amendment to the Master Loan Agreement provided an acknowledgment from the Company's lender that the Company had received its grain dealer license and limited the amount of deferred pay contracts the Company could enter into for corn purchases. The Second Amendment to the Master Loan Agreement also provided a change to the reports the Company was required to provide to the lender to show compliance with the grain dealer restrictions. The Company believes that neither of these amendments materially changed the terms of the Company's credit agreements with its primary lender. As a result, the Company determined that these amendments were not material amendments and did not, therefore, file these amendments as exhibits to the Company's periodic reports.

With respect to any corn purchase contracts the Company has with Mr. Kyle Wendland's company, Comeback Farms Inc., corn purchases from Comeback Farms Inc. are made in the ordinary course of business and Comeback Farms Inc. is treated no differently from any of the Company's other corn suppliers. When the Company enters into a contract to purchase corn from Comeback Farms Inc., it is on the same standard contract used for all of the Company's corn suppliers and the prices are set based on standard corn prices available for all of the Company's corn suppliers. These corn prices are based on publicly available market corn prices and the Company believes that based on materiality thresholds in SEC Regulations, these contracts are immaterial based on the total amount of corn purchased from Comeback Farms Inc. Therefore, the Company believes that the corn purchase contracts that it periodically enters into with Comeback Farms Inc. are not material contracts that are required to be filed with the Company's periodic reports. Furthermore, the Company believes that the corn purchase transactions it has with Comeback Farms Inc. would fall under the disclosure exception in Number 7(a) to the Instructions to Regulation S-K Item 404(a). Nevertheless, the Company has previously chosen to disclose to its members the amount of corn it purchases from related parties, regardless of the disclosure exception referred to above.

In connection with the Company's response to the comments contained in the Commission's letter dated November 8, 2011, the Company's management hereby acknowledges that:

| • | The Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| • | Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | The Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

| Sincerely, | |

| Homeland Energy Solutions, LLC | |

| By: | /s/ Walter W. Wendland |

| Walter W. Wendland | |

| President and Chief Executive Officer | |