OTC: DAKP A NNUAL S TOCKHOLDER P RESENTATION 18 J UNE 2013 WWW . DAKOTAPLAINS . COM

Forward Looking Statements Statements made by representatives of Dakota Plains Holdings, Inc . (“Dakota Plains” or the “Company”) during the course of this presentation that are not historical facts, are forward - looking statements . These statements are based on certain assumptions and expectations made by the Company which reflect management’s experience, estimates and perception of historical trends, current conditions, anticipated future developments and other factors believed to be appropriate . Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond the control of the Company, which may cause actual results to differ materially from those implied or anticipated in the forward - looking statements . These include risks relating to global economics or politics, our ability to obtain additional capital needed to implement our business plan, minimal oper ating history, loss of key personnel, lack of business diversification, reliance on strategic, third - party relationships, financial performance and results, prices and demand for oil, our ability to make acquisitions on economically acceptable terms, and other factors described from time to time in the Company’s reports filed with the SEC, including the annual report on Form 10 - K, filed March 14 , 2013 , that could cause actual results to differ materially from those anticipated or implied in the forward - looking statements . Dakota Plains undertakes no obligation to publicly update any forward - looking statements, whether as a result of new information or future events . 2

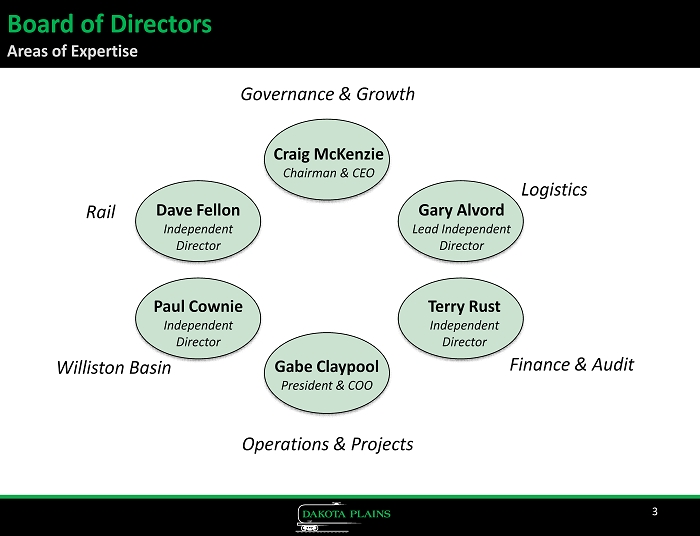

3 Craig McKenzie Chairman & CEO Gary Alvord Lead Independent Director Terry Rust Independent Director Gabe Claypool President & COO Paul Cownie Independent Director Dave Fellon Independent Director Rail Williston Basin Operations & Projects Finance & Audit Logistics Governance & Growth Board of Directors Areas of Expertise

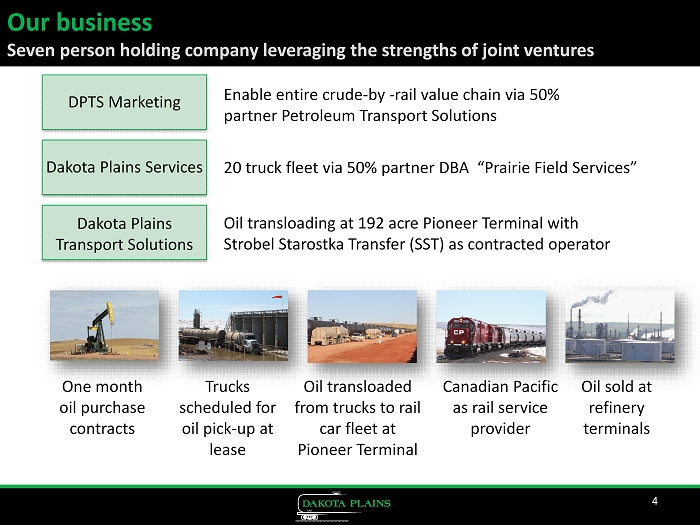

4 DPTS Marketing Enable entire crude - by - rail value chain via 50% partner Petroleum Transport Solutions One month oil purchase contracts Dakota Plains Services 20 truck fleet via 50% partner DBA “Prairie Field Services” Trucks scheduled for oil pick - up at lease Oil transloaded from trucks to rail car fleet at Pioneer Terminal Canadian Pacific as rail service provider Oil sold at refinery terminals Dakota Plains Transport Solutions Oil transloading at 192 acre Pioneer Terminal with Strobel Starostka Transfer (SST) as contracted operator 7 Our business Seven person holding company leveraging the strengths of joint ventures

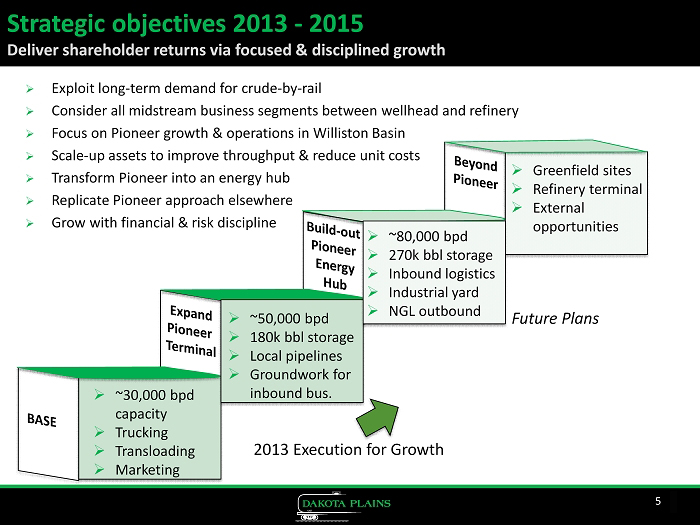

Strategic objectives 2013 - 2015 Deliver shareholder returns via focused & disciplined growth » Exploit long - term demand for crude - by - rail » Consider all midstream business segments between wellhead and refinery » Focus on Pioneer growth & operations in Williston Basin » Scale - up assets to improve throughput & reduce unit costs » Transform Pioneer into an energy hub » Replicate Pioneer approach elsewhere » Grow with financial & risk discipline 5 » ~30,000 bpd capacity » Trucking » Transloading » Marketing » ~50,000 bpd » 180k bbl storage » Local pipelines » Groundwork for inbound bus. » Greenfield sites » Refinery terminal » External opportunities » ~80,000 bpd » 270k bbl storage » Inbound logistics » Industrial yard » NGL outbound 2013 Execution for Growth Future Plans

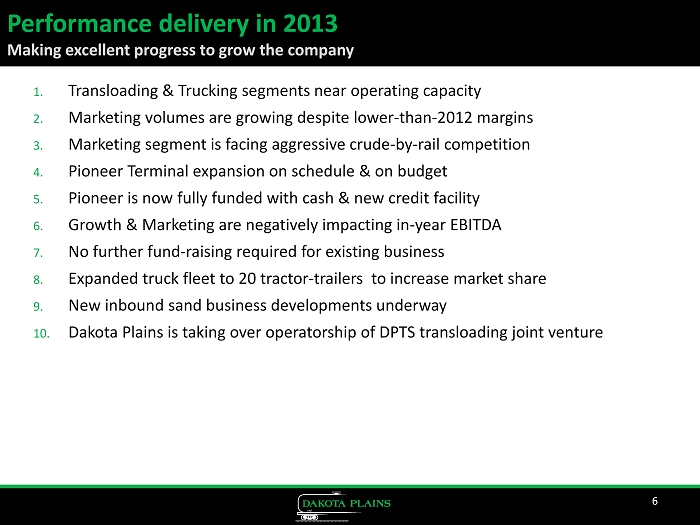

1. Transloading & Trucking segments near operating capacity 2. Marketing volumes are growing despite lower - than - 2012 margins 3. Marketing segment is facing aggressive crude - by - rail competition 4. Pioneer Terminal expansion on schedule & on budget 5. Pioneer is now fully funded with cash & new credit facility 6. Growth & Marketing are negatively impacting in - year EBITDA 7. No further fund - raising required for existing business 8. Expanded truck fleet to 20 tractor - trailers to increase market share 9. New inbound sand business developments underway 10. Dakota Plains is taking over operatorship of DPTS transloading joint venture 6 Performance delivery in 2013 Making excellent progress to grow the company

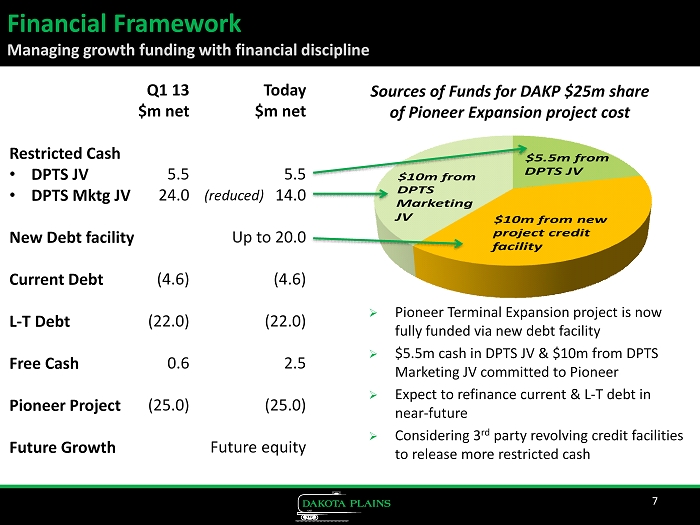

7 Financial Framework Managing growth funding with financial discipline Restricted Cash • DPTS JV • DPTS Mktg JV New Debt facility Current Debt L - T Debt Free Cash Pioneer Project Future Growth Q1 13 $m net 5.5 24.0 (4.6) (22.0) 0.6 (25.0) Today $m net 5.5 14.0 Up to 20.0 (4.6) (22.0) 2.5 (25.0) Future equity Sources of Funds for DAKP $25m share of Pioneer Expansion project cost (reduced) » Pioneer Terminal Expansion project is now fully funded via new debt facility » $5.5m cash in DPTS JV & $10m from DPTS Marketing JV committed to Pioneer » Expect to refinance current & L - T debt in near - future » Considering 3 rd party revolving credit facilities to release more restricted cash

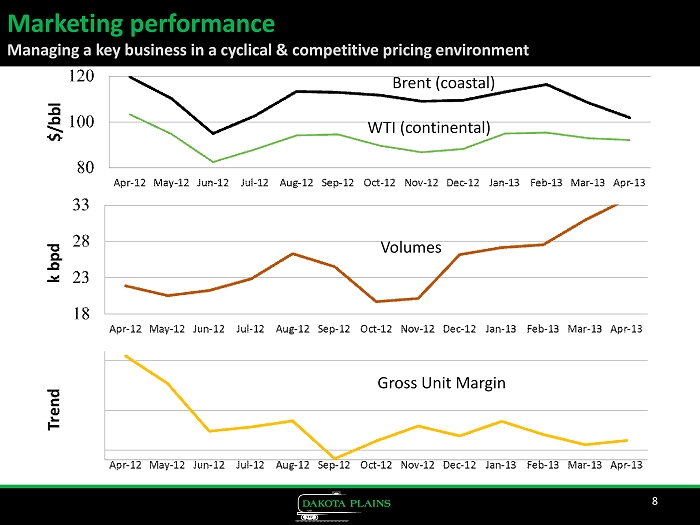

8 Marketing performance Managing a key business in a cyclical & competitive pricing environment Brent (coastal) WTI (continental) Volumes Gross Unit Margin

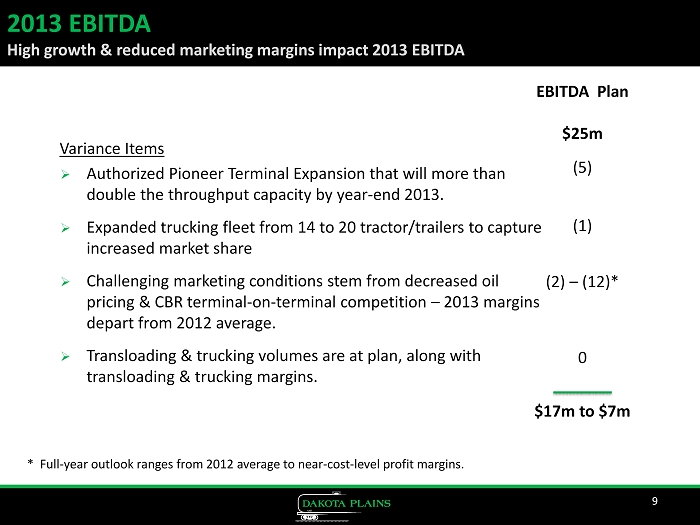

» Authorized Pioneer Terminal Expansion that will more than double the throughput capacity by year - end 2013. » Expanded trucking fleet from 14 to 20 tractor/trailers to capture increased market share » Challenging marketing conditions stem from decreased oil pricing & CBR terminal - on - terminal competition – 2013 margins depart from 2012 average. » Transloading & trucking volumes are at plan, along with transloading & trucking margins. 9 EBITDA Plan $25m (5) (1) (2) – (12)* 0 $17m to $7m 2013 EBITDA High growth & reduced marketing margins impact 2013 EBITDA * Full - year outlook ranges from 2012 average to near - cost - level profit margins. Variance Items

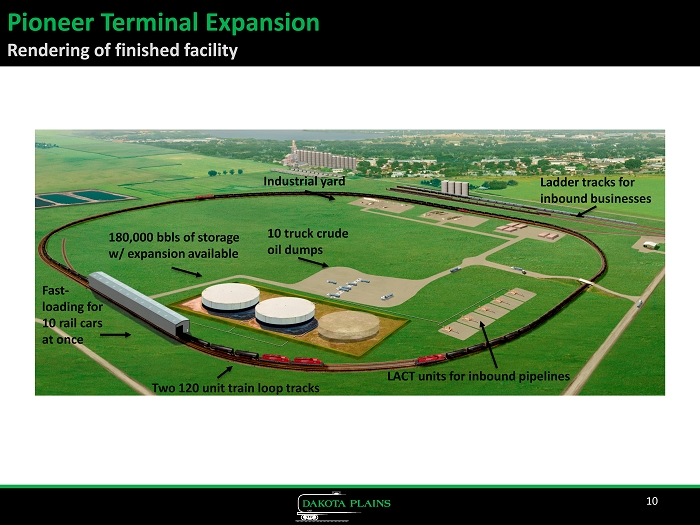

10 Pioneer Terminal Expansion Rendering of finished facility LACT units for inbound pipelines Industrial yard 180,000 bbls of storage w/ expansion available 10 truck crude oil dumps Fast - loading for 10 rail cars at once Two 120 unit train loop tracks Ladder tracks for inbound businesses

Pioneer Terminal Expansion – June 6th photo 11

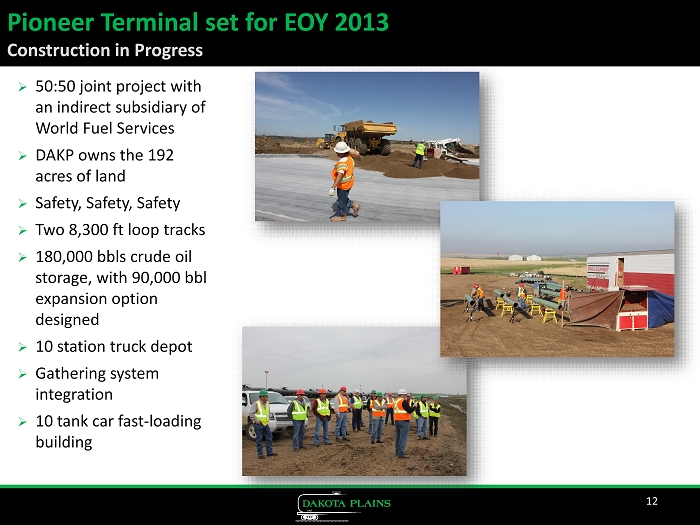

12 Pioneer Terminal set for EOY 2013 Construction in Progress » 50:50 joint project with an indirect subsidiary of World Fuel Services » DAKP owns the 192 acres of land » Safety, Safety, Safety » Two 8,300 ft loop tracks » 180,000 bbls crude oil storage, with 90,000 bbl expansion option designed » 10 station truck depot » Gathering system integration » 10 tank car fast - loading building

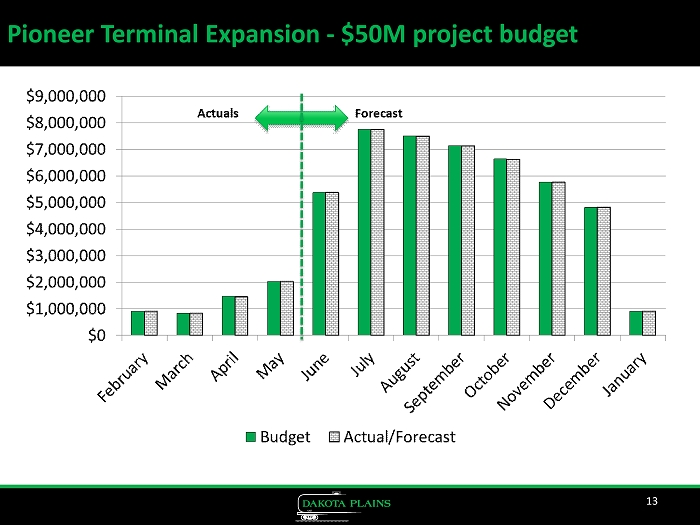

Pioneer Terminal Expansion - $50M project budget 13

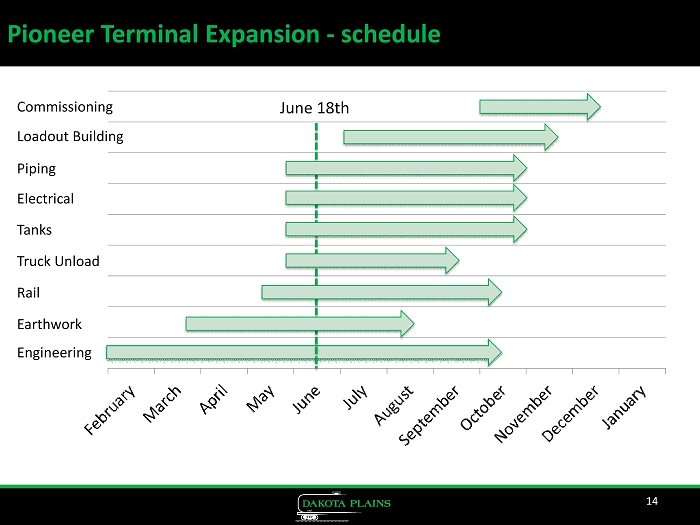

Pioneer Terminal Expansion - schedule 14 Commissioning Loadout Building Piping Truck Unload Tanks Engineering Earthwork Rail Electrical June 18th

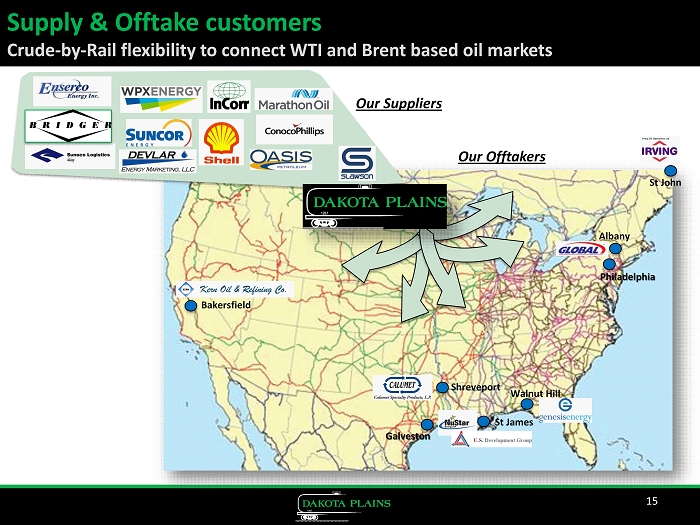

Supply & Offtake customers Crude - by - Rail flexibility to connect WTI and Brent based oil markets 15 Our Suppliers Bakersfield St James Walnut Hill Shreveport Albany St John Philadelphia Galveston Our Offtakers

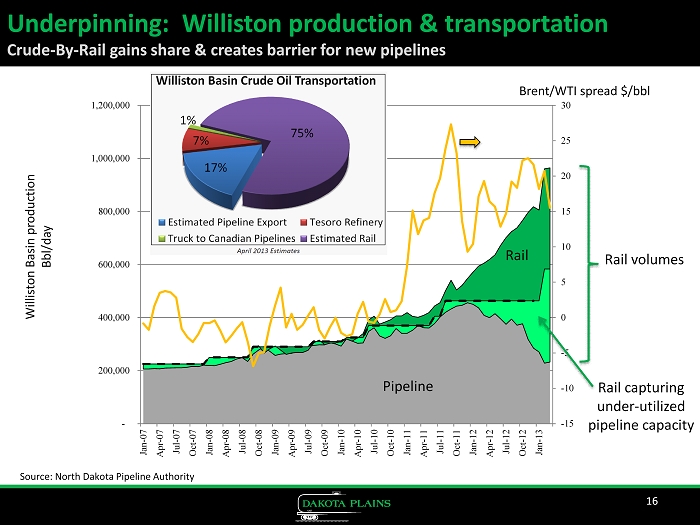

Underpinning: Williston production & transportation Crude - By - Rail gains share & creates barrier for new pipelines 16 Brent/WTI spread $/bbl Pipeline volumes Rail capturing under - utilized pipeline capacity Williston Basin production Bbl/day Source: North Dakota Pipeline Authority -15 -10 -5 0 5 10 15 20 25 30 - 200,000 400,000 600,000 800,000 1,000,000 1,200,000 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Rail volumes Pipeline Rail

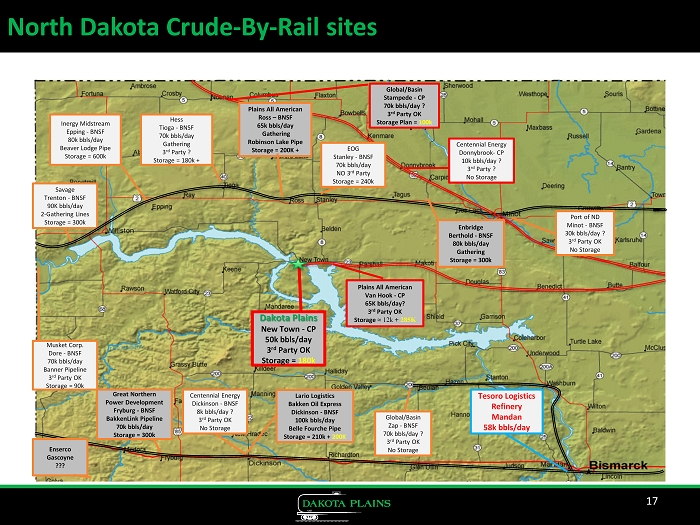

Dakota Plains New Town - CP 50k bbls/day 3rd Party OK Storage = 180k Lario Logistics Bakken Oil Express Dickinson - BNSF 100k bbls/day Belle Fourche Pipe Storage = 210k + 200K Global/Basin Zap - BNSF 70k bbls/day ? 3rd Party OK No Storage Savage Trenton - BNSF 90K bbls/day 2 - Gathering Lines Storage = 300k Inergy Midstream Epping - BNSF 80k bbls/day Beaver Lodge Pipe Storage = 600k Hess Tioga - BNSF 70k bbls/day Gathering 3rd Party ? Storage = 180k + Global/Basin Stampede - CP 70k bbls/day ? 3rd Party OK Storage Plan = 100k Centennial Energy Donnybrook - CP 10k bbls/day ? 3rd Party ? No Storage Musket Corp. Dore - BNSF 70k bbls/day Banner Pipeline 3rd Party OK Storage = 90k Centennial Energy Dickinson - BNSF 8k bbls/day ? 3rd Party OK No Storage Great Northern Power Development Fryburg - BNSF BakkenLink Pipeline 70k bbls/day Storage = 300k Plains All American Van Hook - CP 65K bbls/day? 3rd Party OK Storage ≈ 12k + 285K North Dakota Crude - By - Rail sites 17 Plains All American Ross – BNSF 65k bbls/day Gathering Robinson Lake Pipe Storage = 200K + EOG Stanley - BNSF 70k bbls/day NO 3rd Party Storage = 240k Enbridge Berthold - BNSF 80k bbls/day Gathering Storage = 300k Port of ND Minot - BNSF 30k bbls/day ? 3rd Party OK No Storage Tesoro Logistics Refinery Mandan 58k bbls/day Enserco Gascoyne ???

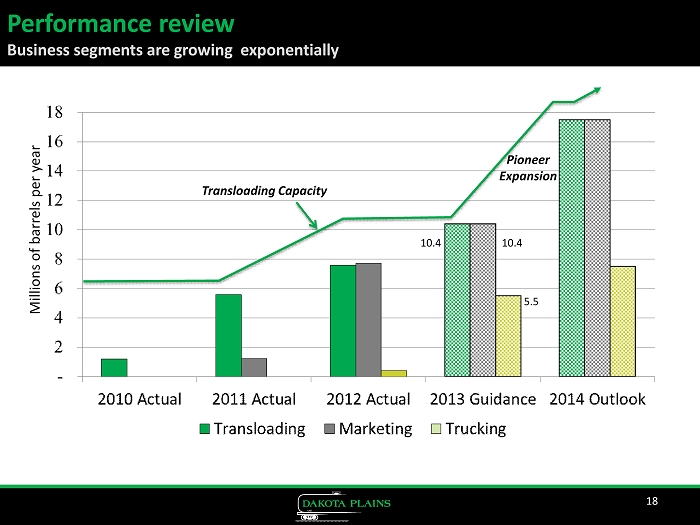

Performance review Business segments are growing exponentially 18 Millions of barrels per year Transloading Capacity Pioneer Expansion 10.4 10.4 5.5

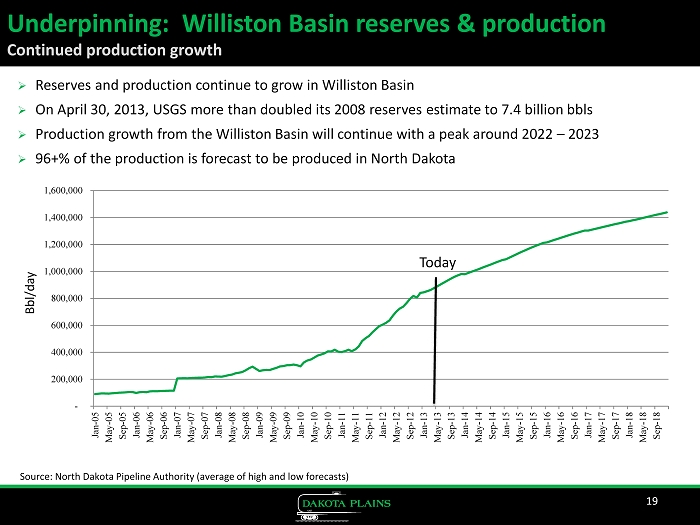

Underpinning: Williston Basin reserves & production Continued production growth 19 » Reserves and production continue to grow in Williston Basin » On April 30, 2013, USGS more than doubled its 2008 reserves estimate to 7.4 billion bbls » Production growth from the Williston Basin will continue with a peak around 2022 – 2023 » 96+% of the production is forecast to be produced in North Dakota - 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 Jan-05 May-05 Sep-05 Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Bbl/day Today Source: North Dakota Pipeline Authority (average of high and low forecasts)

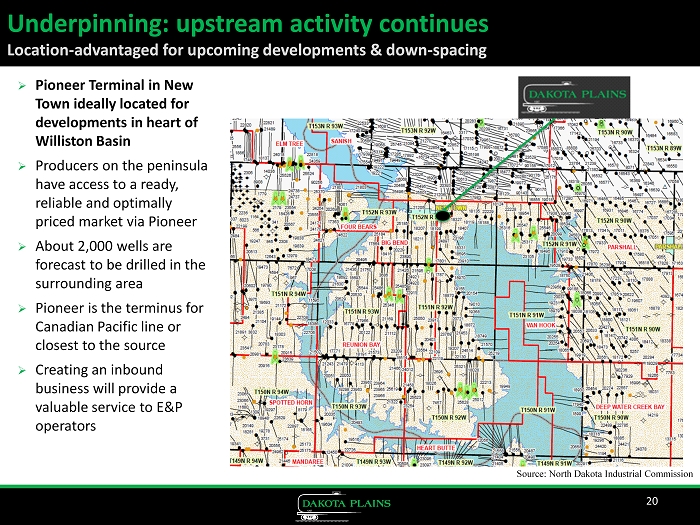

Source: North Dakota Industrial Commission 20 » Pioneer Terminal in New Town ideally located for developments in heart of Williston Basin » Producers on the peninsula have access to a ready, reliable and optimally priced market via Pioneer » About 2,000 wells are forecast to be drilled in the surrounding area » Pioneer is the terminus for Canadian Pacific line or closest to the source » Creating an inbound business will provide a valuable service to E&P operators Underpinning: upstream activity continues Location - advantaged for upcoming developments & down - spacing

Conclusions » Dakota Plains has created a safe, reliable and cost - advantaged crude - by - rail market for oil producers in the heart of the Williston Basin » Through the strength of its joint ventures and service agreements, Dakota Plains is poised to grow dramatically in the coming years » With Pioneer construction underway, the operations will grow from 30,000 barrels per day of capacity to up to 80,000 barrels per day by year - end 2013 » Our Pioneer terminal in New Town, ND, has a geographical and logistical advantage in the main fairway of the Bakken & Three Forks; » Business segments that include trucking, transloading, and marketing today will expand in 2014 to include storage and inbound commodity logistics services to local producers » Business and competitive dynamics underpin a consensus industry view that crude - by - rail is a long - term proposition 21