Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on April 17, 2007

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Stallion Oilfield Services, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1389 | 72-1618455 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

410 Roberts Street

Houston, Texas 77003

(713) 528-5544

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Craig M. Johnson

Chief Executive Officer

410 Roberts Street

Houston, Texas 77003

(713) 528-5544

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Vinson & Elkins L.L.P. First City Tower, Suite 2300 1001 Fannin Street Houston, Texas 77002 (713) 758-2222 Attn: T. Mark Kelly Attn: Christopher S. Collins | Baker Botts L.L.P. One Shell Plaza 910 Louisiana Street Houston, Texas 77002 (713) 229-1234 Attn: R. Joel Swanson Attn: Felix P. Phillips |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Proposed Maximum Price(1)(2) | Amount of Registration Fee(3) | ||

Common Stock, par value $0.01 | $400,000,000 | $12,280 |

| (1) | Includes common stock issuable upon the exercise of the underwriters’ option to purchase additional shares. |

| (2) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act 1933. |

| (3) | The registrant previously paid registration fees of $30,763 in connection with the Registration Statement on Form S-1 (Registration No. 333-135589) filed on July 3, 2006, with respect to common shares having a proposed maximum aggregate offering price of $287,500,000. The Registration Statement on Form S-1 (Registration No. 333-135589) was withdrawn on November 2, 2006. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated April 17, 2007

PROSPECTUS

Shares

Common Stock

This is the initial public offering of Stallion Oilfield Services, Inc. common stock. We are offering shares of our common stock and the selling stockholders, including members of our senior management, are offering shares of our common stock in this initial public offering. No public market currently exists for our common stock. We will not receive any of the proceeds from the shares of our common stock sold by the selling stockholders.

We have applied for listing of our common stock on The NASDAQ Stock Market LLC under the symbol “SOFS.” We currently estimate that the initial public offering price will be between $ and $ per share.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 10.

| Per Share | Total | |||

Public offering price | $ | $ | ||

Underwriting discounts and commissions | $ | $ | ||

Proceeds to the Company (before expenses) | $ | $ | ||

Proceeds to the selling stockholders (before expenses) | $ | $ | ||

We have granted the underwriters a 30-day option to purchase up to an aggregate of additional shares of common stock on the same terms and conditions set forth above if the underwriters sell more than shares of common stock in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Lehman Brothers, on behalf of the underwriters, expects to deliver the shares on or about , 2007

| LEHMAN BROTHERS | CREDIT SUISSE | UBS INVESTMENT BANK |

, 2007

Table of Contents

Index to Financial Statements

Table of Contents

Index to Financial Statements

| Page | ||

| 1 | ||

| 10 | ||

| 23 | ||

| 23 | ||

| 24 | ||

| 25 | ||

| 27 | ||

| 29 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 31 | |

| 57 |

| Page | ||

| 72 | ||

| 87 | ||

| 90 | ||

| 91 | ||

| 94 | ||

Certain United States Federal Tax Considerations for Non-United States Holders | 96 | |

| 99 | ||

| 105 | ||

| 105 | ||

| 105 |

Dealer Prospectus Delivery Obligation

Until , 2007, 25 days after the date of this prospectus, all dealers that effect transactions in our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ABOUT THIS PROSPECTUS

You should rely only on the information contained in this prospectus. We and the selling stockholders have not authorized any other person to provide you with information different from that contained in this prospectus. We and the selling stockholders are only offering to sell, and only seeking offers to buy, the common stock in jurisdictions where offers and sales are permitted.

The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus includes market share and industry data and forecasts that we obtained from internal company surveys, market research, consultant surveys, publicly available information and industry publications and surveys. We believe the information included in this prospectus from market research, consultant surveys and industry publications and surveys is reliable.

Non-GAAP Financial Measures

The body of accounting principles generally accepted in the United States of America is commonly referred to as “GAAP.” A non-GAAP financial measure is generally defined by the Securities and Exchange Commission, or SEC, as one that purports to measure historical or future financial performance, financial position or cash flow, but excludes or includes amounts that would not be so adjusted in the most comparable GAAP measures. In this prospectus, we disclose EBITDA, a non-GAAP financial measure. EBITDA is calculated as net income before interest expense, taxes, depreciation and amortization. EBITDA is not a substitute for GAAP measures of earnings and cash flow. EBITDA is included in this prospectus because our management considers it an important supplemental measure of our performance and believes that it is frequently used by security analysts, investors and other interested parties in the evaluation of companies in our industry, some of which present EBITDA when reporting their results.

Table of Contents

Index to Financial Statements

This summary highlights selected information in this prospectus, but it does not contain all of the information that you should consider before deciding to invest in our common stock. You should read this entire prospectus carefully, including the “Risk Factors” section and our historical financial statements and pro forma financial data, which are included elsewhere in this prospectus.

Unless otherwise indicated or the context otherwise requires, (i) the information contained in this prospectus assumes that the underwriters’ option to purchase additional shares is not exercised, (ii) the information contained in this prospectus relating to us assumes the completion of the Restructuring as described under the caption “The Restructuring” below, and (iii) references in this prospectus to “Stallion,” “we,” “us” and “our” are references to Stallion Oilfield Services, Inc. together with all of its subsidiaries subsequent to the Restructuring and refer to our predecessor entities and their respective subsidiaries prior to the Restructuring.

Our Company

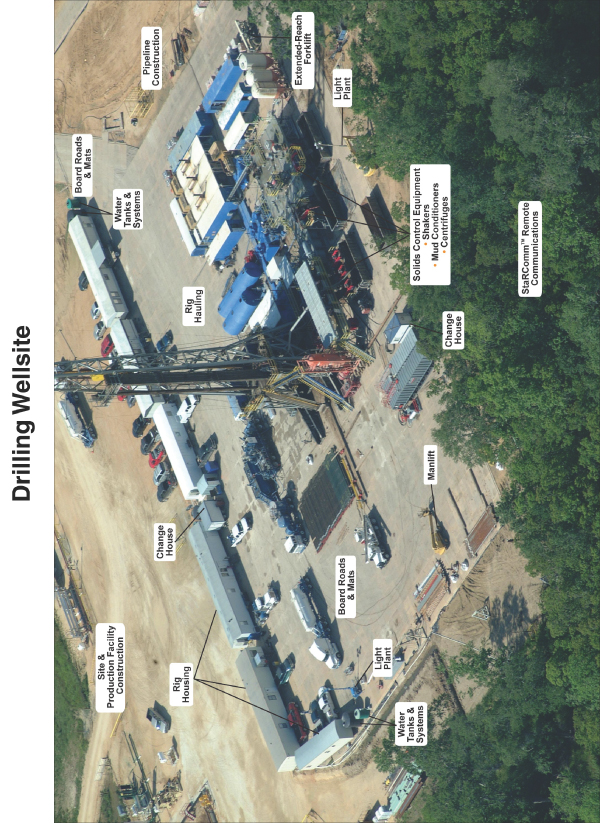

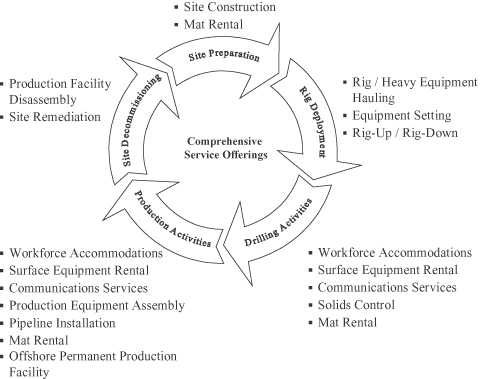

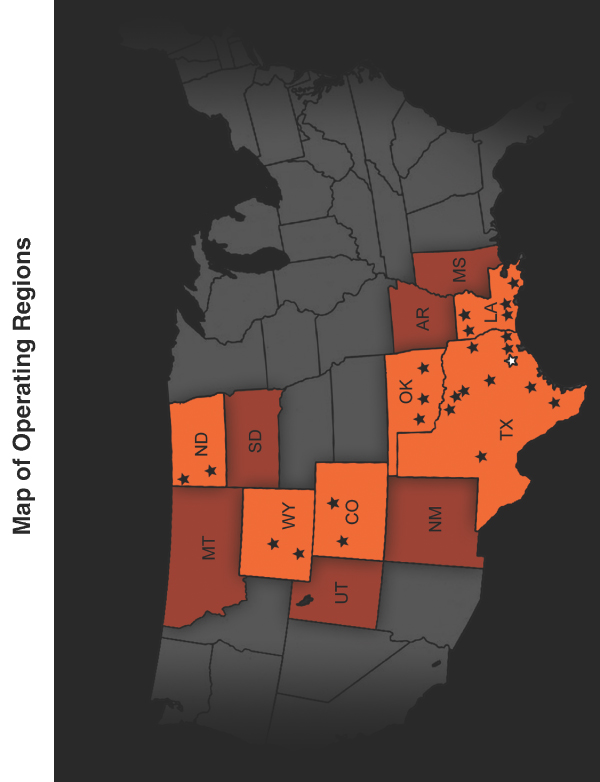

We are a growth-oriented oilfield service company that provides comprehensive wellsite support services and construction and logistics services to exploration and production companies and drilling contractors throughout the United States. Our company slogan,Everything but the RigSM, reflects our business strategy of providing a broad and comprehensive range of critical services to support wellsite operations, including onshore and offshore workforce accommodations, surface equipment rental, solids control, site construction, rig relocation and heavy equipment hauling. Our service offerings are designed to improve living and working conditions at the wellsite, wellsite safety and our customers’ productivity. We currently focus on oil and natural gas regions within North America that we believe have stable oil and gas drilling activity and which provide attractive long-term potential for growth, including South Texas, the Gulf Coast, ArkLaTex, North Texas, the Permian Basin, the Mid-Continent and Rocky Mountain regions. We also supply offshore workforce accommodations and related equipment for use in the Gulf of Mexico and, to a lesser extent, other international offshore regions. We provide services to a diverse group of over 2,000 customers. The Glossary of Terms included as Appendix A to this prospectus contains a description of some of these regions and a map of these regions appears at the end of the appendix.

Our services span the entire life-cycle of the land-based wellsite—wellsite preparation, rig deployment, drilling activities, production activities and decommissioning. We are typically the first service provider on the wellsite, as we assist in the initial preparation of the wellsite and often haul the rig and related heavy equipment onto the site using our fleet of tractors, trailers, trucks and cranes. Throughout the drilling and completion phases of the land-based well, we provide rental equipment and required support services to the wellsite. We also, in some cases, provide continuing support services during the production phase of the well, including construction of production facilities and well connections to existing pipeline infrastructure. We frequently are the last service provider to leave the wellsite as we perform production facility disassembly and site restoration, which are the last phases of the wellsite decommissioning process. In addition, our offshore workforce accommodations business serves our offshore customers during many phases of the offshore drilling and production life-cycle.

Our business is comprised of two segments:

Wellsite Support Services. Through our wellsite support services segment, we offer integral services used by oil and natural gas companies, drilling contractors and other wellsite service providers to support wellsite operations. This segment includes the following primary service lines:

| • | Workforce accommodations. We provide onshore workforce accommodations in the United States with, as of December 31, 2006, over 2,000 transportable units in our inventory. Our fleet of land-based units |

1

Table of Contents

Index to Financial Statements

is designed to accommodate various personnel on wellsite locations before, during and after drilling operations. In addition, we design, manufacture, lease and repair offshore workforce accommodation structures, which include units certified by the U.S. Coast Guard and/or the International Convention for the Safety of Life at Sea, 1974, the paramount international treaty concerning the safety of merchant ships (“SOLAS”). Our workforce accommodation units are specifically configured to provide transportable, comfortable living quarters and functional workspaces. |

| • | Surface equipment rental. We provide a variety of surface rental equipment used in and critical to wellsite activities including forklifts, manlifts, power generators, compressors, loaders and water systems. |

• | Communications services. We provide integrated communications services through ourStaRCommTM/SM satellite system that provides wireless communications via intercoms and telephone, fax and internet/data services throughout the wellsite location. |

| • | Solids control. We provide customized solids control services, closed-loop mud systems and fluid recovery services to help maximize our customers’ operating efficiency at the wellsite. We provide high-quality shakers, mud conditioners, centrifuges and peripheral backside equipment, as well as solids removal and waste handling coordination services. |

Construction and Logistics Services. Through our construction and logistics services segment, we offer services that are critical to establish, maintain and decommission the wellsite and position key equipment prior to, during and after drilling operations. This segment includes the following primary service lines:

| • | Site construction. We provide construction equipment and services to build and reclaim infrastructure at wellsites before, during and after drilling operations. Our services include site clearing, road construction, mat placement, production facility assembly and construction, pipeline installation, pit remediation, production decommissioning and site restoration. We provide services for wellsites in both land and inland marine environments. |

| • | Rig relocation and heavy equipment hauling. We provide a fleet of cranes, tractors, trailers, trucks and loaders used for the hauling and relocation of drilling rigs and related heavy equipment. We maintain a focus on providing reliable, efficient and safe transportation services. |

Wellsite support services and construction and logistics services are critical to establish and operate the land-based wellsite; however, these onshore services have historically been provided primarily by small, regional service providers and have not been the focus of larger oilfield service companies. We believe we have a distinct advantage over these smaller competitors due to our scale, access to capital and our ability to provide a single supply source for many of our customers’ needs. In addition, we provide offshore workforce accommodations to exploration and production companies in the Gulf of Mexico and, to a lesser extent, other international offshore regions. These services have been historically provided by relatively few service providers. We believe we have a competitive advantage over our competitors in this market due to our knowledge of the industry, relationships with customers and the quality of our products.

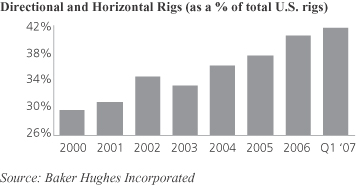

Recent Industry Trends

In recent years, our industry has experienced higher demand for oil and natural gas and a constrained oil and natural gas supply, resulting in higher commodity prices and increased drilling activity. We believe this trend of increased natural gas prices and drilling activity, as well as other industry trends reflected below, will benefit us and facilitate implementation of our business strategy:

| • | Labor shortages and increasing safety concerns. Due to the increase in the demand for labor in the oilfield and offshore, our customers continue to attempt to improve living and working conditions at the |

2

Table of Contents

Index to Financial Statements

wellsite to help retain employees. Our customers also continue to enhance their safety procedures to help reduce injuries and to help ensure compliance with more stringent regulatory requirements. |

| • | Increasingly complex technologies. The increasing complexity of technology used in the oil and natural gas development process requires a greater number of technicians on location during drilling and, therefore, additional workforce accommodations. |

| • | Geographically dispersed drilling operations. With the shift toward consolidation in the land drilling industry, land crews based in one region may accompany a rig to work on wellsites in geographically dispersed oil and natural gas regions a significant distance away from the home office. This development has resulted in the need for full-time accommodations for multiple shifts of the rig crew. |

| • | Increase in drilling and developing unconventional resources. The decline of conventional North American oil and natural gas reservoirs is leading to a shift toward the drilling and development of onshore unconventional oil and natural gas resources. We believe the increased drilling requirements of these unconventional resources will lead to continued drilling activity. Recently, there has been an increase in the construction of new drilling rigs to meet this demand. |

| • | Environmental sensitivity. In response to increasing regulation and environmental sensitivity, onshore wellsite operators are utilizing closed-loop solids control systems to help reduce onsite discharge of drilling fluids and cuttings in environmentally sensitive areas and when working with oil-based and synthetic drilling fluids. These systems require customized solids control configurations to maximize drilling fluid efficiency. |

| • | Outsourcing ancillary services. Some of the services we provide have been historically handled by drilling contractors themselves. In many instances, these services are only ancillary to the primary activity of drilling and completing wells and represent only a minor portion of the total well drilling cost. Many drilling contractors are increasingly electing to outsource these services to suppliers who can provide high-quality and reliable services. |

| • | Increased deepwater development activity. Deepwater exploration and production activities are typically complex with long durations and require personnel involved in drilling, production and construction. Growth in these deepwater activities has resulted in the need for more workforce accommodations on offshore platforms. |

While we believe that these trends will benefit us, our business may be adversely affected by circumstances that are beyond our control. Any prolonged substantial reduction in oil and natural gas prices would likely affect oil and natural gas drilling and production levels and demand for the services we provide. For more information on this and other risks to our business and our industry, please read “Risk Factors—Risks Related to Our Business and Our Industry.”

Our Business Strategy

We believe we are well positioned to become a leading provider of wellsite support and construction and logistics services. Our business strategy consists of the following core elements:

Broaden the suite of services we provide. We have established strong working relationships with our customers which provide us a stable base of operations. We work closely with our customers to define new service offerings that meet specific customer needs in the onshore markets where we operate and also intend to expand our offshore service offerings. We intend to continue to invest in developing or acquiring new high-quality assets and services which add to the breadth and quality of our service portfolio.

3

Table of Contents

Index to Financial Statements

Establish and maintain a leadership position in our principal operating areas.We intend to continue to build leading market positions in the areas in which we operate by offering a comprehensive and integrated package of services which allows us to provide our customers with wellsite support services required across their drilling locations. We view the incremental steps in achieving this to include:

| • | Deploying our suite of services across existing land-based operating areas. We believe we have developed expertise in specific service lines which can be effectively marketed across the majority of our land-based operating areas. We intend to continue to roll-out our existing services across our current operating areas in an effort to deliver a comprehensive portfolio of services in each region. We believe our established customer base and strong regional relationships will continue to provide a strategic distribution network for our service deployment efforts. |

| • | Continue to develop our offshore service offerings. We believe we are a leading provider of offshore workforce accommodations to exploration and production companies. We intend to expand our manufacturing capabilities and offshore service offerings to meet the growing needs of our customers. |

Extend our operations into new geographic areas.We intend to apply our expertise in wellsite support services and land-based construction and logistics services in markets where we currently do not operate and which provide an attractive platform for future growth. We intend to continue to improve the ease with which our clients can use our services from one wellsite location to the next. We expect to support our customers’ entry into other active drilling regions by introducing our service offerings in those regions.

Expand our services internationally. Our offshore workforce accommodation business predominantly operates in the Gulf of Mexico. We intend to pursue strategic opportunities to expand our service offerings into other international offshore markets by leveraging our custom product design and existing customer base.

Focus on service quality, business performance and safety. Our management team is responsible for assessing our service quality, performance and safety compliance and coordinates with our field offices to help ensure that our quality and performance metrics and safety standards are met at every level of our organization. In addition to our internal safety policies, we adhere to certain external safety regulations, such as certifying certain of our offshore workforce accommodation units with the U.S. Coast Guard and/or SOLAS prior to deployment. We intend to continue to invest in and promote designs, systems and methodologies which improve the reliability, responsiveness, accountability and safety of our operations.

Continue to pursue strategic expansion opportunities.We believe that the markets in which we operate remain fragmented and that there are numerous consolidation opportunities within these markets. We completed 17 acquisitions in 2005 and 2006 and intend to continue pursuing strategic acquisitions which add to the scope and quality of our service portfolio. In evaluating such acquisitions we consider a number of factors, including synergies with existing operations, financial performance and acquisition costs.

Capitalize on regional experience. One component of our acquisition and growth strategy is to acquire assets located in strategic operating areas that include personnel with strong local leadership and regional experience. We believe that by having the administrative functions previously performed at the regional level centralized in and handled by our corporate office, we have enhanced our controls environment and enabled our local management to focus on our customers, our employees and the effective management and deployment of our assets.

The execution of our business strategy depends on our ability to manage the growth that we have experienced and successfully operate on an integrated basis. The failure to manage growth and successfully operate on an integrated basis could result in diminished financial performance, our inability to report financial results or require a disproportionate amount of management’s attention. For more information on this and other risks to our business and our industry, please read “Risk Factors—Risks Related to Our Business and Our Industry.”

4

Table of Contents

Index to Financial Statements

For further information on our business strategy, please read “Business—Our Business Strategy.”

Our Competitive Strengths

We believe our operations benefit from a number of competitive strengths, including the following:

| • | Extensive breadth of service throughout the wellsite life-cycle. We provide a broad array of wellsite services throughout each phase of the land-based drilling and production process. This breadth of service strengthens our relationships with our customers and allows us to identify and cross-sell additional services. By providing comprehensive wellsite services to our customers, we believe we have an advantage over our competitors, who generally offer fewer services. |

| • | Extensive geographic footprint with a strong regional and local presence. Our regional operations are located in some of the most active onshore oil and natural gas drilling regions of the United States, including South Texas, the onshore Gulf Coast, ArkLaTex, North Texas, the Permian Basin, the Mid-Continent and Rocky Mountain regions. Within these regions there were approximately 1,525 active land drilling rigs as of December 31, 2006. In addition, our products are utilized in certain offshore markets, including the Gulf of Mexico, and, to a lesser extent, other international offshore regions. Within the offshore Gulf of Mexico market, there were approximately 81 active offshore drilling rigs as of December 31, 2006. Our regional managers have developed strong relationships with our customers throughout their regions and are largely responsible for the sales, marketing and delivery of our services. |

| • | Large scale of operations. We believe we are one of the largest providers of comprehensive land-based wellsite services in our operating areas. Our scale enables us to deliver a comprehensive range of reliable and high-quality wellsite services to our customers. |

| • | Experienced management team with proven acquisition track record and control environment. Our senior management team has extensive experience in the oil and natural gas industry, with an average of 22 years of experience. We believe this background provides our management team with an in-depth understanding of our customers’ needs and enhances our ability to deliver customer driven solutions. Our management also has substantial experience in identifying, completing and integrating acquisitions and since our inception through March 31, 2007, we have acquired 24 businesses. We have also implemented a standardized control environment that includes accounting, safety, environmental and maintenance processes and controls. |

| • | Leveraged to drilling activity. We believe that favorable supply and demand fundamentals will maintain the current level of drilling for oil and natural gas. Efforts to maintain current levels of production will necessitate continued drilling for the foreseeable future, which will sustain demand for our services. As our package of services typically comprises less than 15% of total drilling expenditures, our business has not historically experienced the pricing volatility experienced by drilling contractors, who represent a much larger portion of total drilling expenditures. |

| • | Leadership position in the offshore workforce accommodation business. We are one of a few providers of U.S. Coast Guard and SOLAS certified offshore workforce accommodation units worldwide. We believe our history, our custom design and the quality of our products and services provide a competitive advantage over our existing competitors and new entrants into this market. |

Recent Developments

9.75% Senior Notes. In a private placement on January 19, 2007, Stallion Oilfield Services Ltd. issued $300 million of 9.75% Senior Notes due February 1, 2015 (the “Senior Notes”). Proceeds from the sale of the

5

Table of Contents

Index to Financial Statements

Senior Notes were used to retire the outstanding balance on Stallion Oilfield Services Ltd.’s $210.0 million Term B Loan and to pay down approximately $44.5 million under our revolving credit facility. For further information on our Senior Notes, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—9.75% Senior Notes.”

Credit Facility. Concurrent with the placement of the Senior Notes, we amended our existing senior secured credit facility to increase our revolving credit line from $70 million to $125 million and reduced the applicable interest rate to LIBOR plus 2.00%. Additionally the revolving credit covenant package was adjusted to provide greater operating flexibility. For further information on our credit facility, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—2006 Credit Facility.”

Risk Factors

You should carefully consider the matters described under “Risk Factors.” These risks could materially and adversely impact our business, financial condition, operating results and cash flows, which could cause the trading price of our common stock to decline and could result in a partial or total loss of your investment.

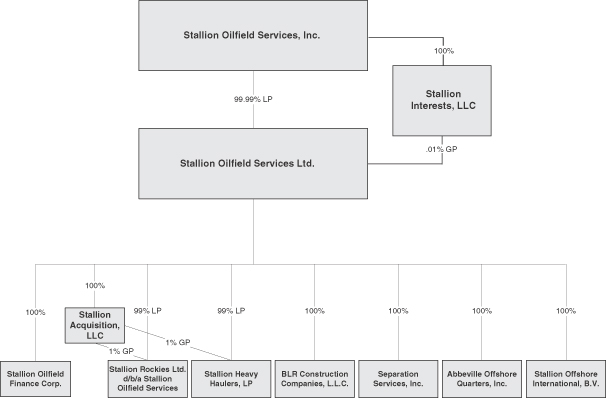

The Restructuring

We were formed as a Delaware corporation in June 2006. In connection with this offering, we will succeed to the business and operations of Stallion Oilfield Holdings, Ltd. (“Stallion Ltd.”), which are described in this prospectus. Prior to the completion of this offering, Stallion Ltd. will merge with and into Stallion Oilfield Services, Inc., with Stallion Oilfield Services, Inc. being the surviving corporate parent and owning all of the operating subsidiaries of Stallion Ltd. (the “Restructuring”). The majority owners of Stallion Ltd. are C/R Stallion Investment Partnership, L.P. and C/R Energy Coinvestment II, L.P. (together, “Carlyle/Riverstone”) and an affiliate of Craig Johnson, our President, Chief Executive Officer and Chairman of the Board. Since the entities are under common ownership and control, the Restructuring will be accounted for at historical cost. In the Restructuring, assuming an initial public offering price of $ , which is the midpoint of the public offering price range set forth on the cover of this prospectus, the partners of Stallion Ltd. will receive an aggregate of shares of our common stock in exchange for all of the Stallion Ltd. partnership interests held by them. Immediately following completion of the Restructuring and prior to this offering, we will have shares of common stock outstanding, % of which will be owned by Carlyle/Riverstone and % of which will be owned by an affiliate of Craig Johnson.

For additional information about the Restructuring, please read “Certain Relationships and Related Party Transactions—The Restructuring.” Please see “Business—Corporate Structure” for a chart depicting our corporate structure following the Restructuring.

Our Executive Offices

Our principal executive offices are located at 410 Roberts Street, Houston, Texas 77003, and our telephone number is (713) 528-5544. Information contained on or accessible from our website,www.stallionoilfield.com, is not part of this prospectus.

6

Table of Contents

Index to Financial Statements

The Offering

Common stock offered by us | shares or shares if the underwriters exercise in full their option to purchase additional shares of common stock |

Common stock offered by the selling stockholders | shares |

Common stock outstanding after this offering | shares or shares if the underwriters exercise in full their option to purchase additional shares of common stock |

Use of proceeds | We estimate that our net proceeds from this offering, after deducting underwriting discounts and commissions and estimated offering expenses, will be approximately $ million, assuming an initial public offering price of $ , which is the midpoint of the range set forth on the cover page of this prospectus. |

We intend to use the net proceeds we receive from this offering:

| • | to repay $ million of indebtedness under our credit facility; and |

| • | for general corporate purposes, including potential acquisitions and capital expenditures in connection with our anticipated growth. See “Use of Proceeds.” |

Some of the underwriters are lenders under our credit facility and will receive proceeds of the offering in connection with the repayment.

We will not receive any of the proceeds from the sale of shares of our common stock by the selling stockholders. The selling stockholders include members of our senior management. See “Principal and Selling Stockholders.” |

We will use any net proceeds from the exercise of the underwriters’ option to purchase additional shares of common stock for general corporate purposes.

The NASDAQ Stock Market LLC symbol | “SOFS” |

Risk Factors | See “Risk Factors” beginning on page 10 of this prospectus for a discussion of factors that you should carefully consider before deciding to invest in shares of our common stock. |

The number of shares of common stock that will be outstanding after the offering includes as of March 31, 2007, an aggregate of shares of restricted common stock issued to officers and key employees under our 2007 Stock Incentive Plan that are subject to vesting and excludes, as of March 31, 2007, an aggregate of shares of common stock reserved and available for future issuance under our 2007 Stock Incentive Plan.

7

Table of Contents

Index to Financial Statements

Summary Historical Financial Information

The following table sets forth our summary historical consolidated financial and operating data as of the dates and for the periods shown. Our operations are currently conducted by Stallion Oilfield Holdings, Ltd., a limited partnership, and its operating subsidiaries. Immediately prior to the closing of this offering, this limited partnership will merge with and into Stallion Oilfield Services, Inc., and we will operate under a corporate parent structure. Stallion Oilfield Services, Inc., the surviving entity of the Restructuring, will serve as the parent holding company under this new structure. The amounts for each historical annual period presented below were derived from our audited consolidated financial statements. The following information should be read in conjunction with “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our consolidated financial statements and related notes and the unaudited pro forma consolidated financial data included elsewhere in this prospectus. Stallion Oilfield Holdings, Ltd. was formed in 2002 and commenced operations in 2003. As a result, financial results for 2002 are not presented.

Stallion Oilfield Holdings, Ltd. Historical Consolidated | Stallion Oilfield Services, Inc. Pro Forma Consolidated | |||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | Year Ended December 31, 2006 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||

Revenue: | ||||||||||||||||||||

Wellsite support services | $ | 6,769 | $ | 15,452 | $ | 73,126 | $ | 162,661 | $ | 179,743 | ||||||||||

Construction and logistics services | — | — | — | 77,749 | 87,432 | |||||||||||||||

Total revenue | 6,769 | 15,452 | 73,126 | 240,410 | 267,175 | |||||||||||||||

Expenses: | ||||||||||||||||||||

Wellsite support services | 3,108 | 8,695 | 42,281 | 74,200 | 80,992 | |||||||||||||||

Construction and logistics services | — | — | — | 42,319 | 47,792 | |||||||||||||||

Selling, general and administrative | 2,145 | 3,745 | 9,883 | 43,359 | 48,232 | |||||||||||||||

Depreciation and amortization | 836 | 1,924 | 7,798 | 30,068 | 35,695 | |||||||||||||||

Loss on disposal of assets | 86 | 92 | 499 | 920 | 787 | |||||||||||||||

Total expenses | 6,175 | 14,456 | 60,461 | 190,866 | 213,498 | |||||||||||||||

Operating income | 594 | 996 | 12,665 | 49,544 | 53,677 | |||||||||||||||

Interest expense, net | (489 | ) | (917 | ) | (4,565 | ) | (18,919 | ) | (22,187 | ) | ||||||||||

Other income (expense) | — | — | (66 | ) | 71 | 180 | ||||||||||||||

Income before taxes | 105 | 79 | 8,034 | 30,696 | 31,670 | |||||||||||||||

Income tax(1) | — | — | (598 | ) | (4,927 | ) | (12,035 | ) | ||||||||||||

Net income | $ | 105 | $ | 79 | $ | 7,436 | $ | 25,769 | $ | 19,635 | ||||||||||

Pro forma income tax (unaudited)(1) | $ | 40 | $ | 30 | $ | 3,053 | $ | 11,664 | ||||||||||||

Pro forma net income (unaudited) | $ | 65 | $ | 49 | $ | 4,981 | $ | 19,032 | ||||||||||||

Earnings per share: | ||||||||||||||||||||

Basic | ||||||||||||||||||||

Diluted | ||||||||||||||||||||

Weighted average shares: | ||||||||||||||||||||

Basic | ||||||||||||||||||||

Diluted | ||||||||||||||||||||

Other Financial Data: | ||||||||||||||||||||

EBITDA(2) | $ | 1,430 | $ | 2,920 | $ | 20,397 | $ | 79,683 | ||||||||||||

Cash flow provided by operating activities | 144 | 1,734 | 7,087 | 41,124 | ||||||||||||||||

Cash flow used in investing activities | (7,536 | ) | (7,142 | ) | (83,462 | ) | (280,164 | ) | ||||||||||||

Cash flow provided by financing activities | 7,804 | 5,046 | 77,307 | 242,158 | ||||||||||||||||

Capital expenditures: | ||||||||||||||||||||

Acquisitions, net of cash acquired(3) | 5,505 | 1,158 | 47,191 | 178,045 | ||||||||||||||||

Property and equipment | 2,046 | 5,961 | 35,951 | 92,029 | ||||||||||||||||

8

Table of Contents

Index to Financial Statements

Stallion Oilfield Holdings, Ltd. Historical Consolidated | ||||||||||||

| Year Ended December 31, | ||||||||||||

| 2003 | 2004 | 2005 | 2006 | |||||||||

| (in thousands) | ||||||||||||

Balance Sheet Data | ||||||||||||

Cash and cash equivalents | $ | 412 | $ | 50 | $ | 982 | $ | 4,100 | ||||

Net property and equipment | 7,131 | 13,899 | 74,583 | 220,777 | ||||||||

Total assets | 16,252 | 24,713 | 123,136 | 446,907 | ||||||||

Total debt | 11,705 | 18,552 | 67,795 | 257,539 | ||||||||

Total partners’ capital | 3,533 | 3,611 | 43,597 | 153,534 | ||||||||

| (1) | Historically, we were not subject to taxes on a consolidated basis due to our partnership structure; however, certain of our subsidiary companies are taxable corporations and are subject to income tax. Pro forma net income for the year ended December 31, 2006 includes a provision for taxes on our consolidated income before tax. Pro forma income tax expense has been computed at a blended state and federal tax rate of 38% to reflect the pro forma income tax effect on net income for the periods presented assuming that the Restructuring happened on January 1, 2003. |

| (2) | EBITDA consists of net income before interest expense, taxes, depreciation and amortization. EBITDA is used as a supplemental financial measure by our management and by external users of our financial statements, such as investors and commercial banks, to assess: |

| • | the financial performance of our assets without regard to financing methods, capital structure, or historical cost basis; |

| • | the ability of our assets to generate cash sufficient to pay interest on our indebtedness; |

| • | our operating performance and return on invested capital as compared to those of other companies in the oilfield service industry, without regard to financing methods and capital structure; and |

| • | our compliance with certain financial covenants included in our credit facility. |

| EBITDA has limitations as an analytical tool and should not be considered an alternative to net income, operating income, cash flow from operating activities or any other measure of financial performance or liquidity presented in accordance with accounting principles generally accepted in the United States of America (“GAAP”). EBITDA excludes some, but not all, items that affect net income and operating income and these measures may vary among other companies. Limitations to using EBITDA as an analytical tool include: |

| • | EBITDA does not reflect our cash expenditures or future requirements for capital expenditures or capital commitments; |

| • | EBITDA does not reflect changes in, or cash requirements necessary to service interest or principal payments on, our debt; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and |

| • | other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure. |

| The following table presents a reconciliation of the non-GAAP financial measure of EBITDA to the most directly comparable GAAP financial measure on a historical basis for each of the indicated periods. |

| Year Ended December 31, | ||||||||||||

| 2003 | 2004 | 2005 | 2006 | |||||||||

| (in thousands) | ||||||||||||

Reconciliation of EBITDA to Net income: | ||||||||||||

Net income | $ | 105 | $ | 79 | $ | 7,436 | $ | 25,769 | ||||

Income taxes | — | — | 598 | 4,927 | ||||||||

Interest expense | 489 | 917 | 4,565 | 18,919 | ||||||||

Depreciation and amortization | 836 | 1,924 | 7,798 | 30,068 | ||||||||

EBITDA | $ | 1,430 | $ | 2,920 | $ | 20,397 | $ | 79,683 | ||||

| (3) | Acquisitions, net of cash acquired, consists only of the cash component of acquisitions. It does not include equity and/or notes issued for acquisitions. |

9

Table of Contents

Index to Financial Statements

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors, together with the other information contained in this prospectus, before deciding to invest in our common stock. Some of the following risks relate principally to the industry in which we operate and to our business. Other risks relate principally to the securities markets and ownership of our common shares. If any of the following risks develop into actual events, our business, financial condition or results of operations could be materially adversely affected, the trading price of your shares could decline, and you may lose all or part of your investment.

Risks Related to Our Business and Our Industry

Our business depends on domestic drilling activity and spending by the oil and natural gas industry in the United States. Our business may be adversely affected by industry conditions that are beyond our control.

We depend on our customers’ willingness to make expenditures to explore for and to develop and produce oil and natural gas in the United States. Our customers’ willingness to undertake these activities depends largely upon prevailing industry conditions that are influenced by numerous factors over which management has no control, such as:

| • | the supply of and demand for oil and natural gas; |

| • | long lead times associated with acquiring equipment and shortages of qualified personnel; |

| • | the level of prices, and expectations about future prices, of oil and natural gas; |

| • | the cost of exploring for, developing, producing and delivering oil and natural gas; |

| • | the expected rates of declining current production; |

| • | the discovery rates of new oil and natural gas reserves; |

| • | available pipeline, storage and other transportation capacity; |

| • | weather conditions, including hurricanes that can affect oil and natural gas operations over a wide area; |

| • | domestic and worldwide economic conditions; |

| • | political instability in oil and natural gas producing countries; |

| • | technical advances affecting energy consumption; |

| • | the price and availability of alternative fuels; |

| • | the ability of oil and natural gas producers to raise equity capital and debt financing; and |

| • | merger and divestiture activity among oil and natural gas producers. |

The level of oil and natural gas exploration and production activity in the United States is volatile. Expected trends in oil and natural gas production activities may not continue and demand for our services may not reflect the level of activity then existing in the industry. Any prolonged substantial reduction in oil and natural gas prices would likely affect oil and natural gas production levels and, therefore, affect demand for the services we provide. A material decline in oil and natural gas prices or drilling activity levels could have a material adverse effect on our business, financial condition, results of operations and cash flow. In addition, a decrease in the development rate of oil and natural gas reserves in our market areas may also have an adverse impact on our business, even in an environment of stronger oil and natural gas prices.

10

Table of Contents

Index to Financial Statements

A decline in or substantial volatility of oil and natural gas prices could adversely affect the demand for our services.

The demand for our services is primarily influenced by current and anticipated oil and natural gas prices and the related level of drilling activity and general production spending in the areas in which we have operations. Volatility or weakness in oil and natural gas prices (or the perception that oil and natural gas prices will decrease) affects the spending patterns of our customers and may result in the drilling of fewer new wells. This, in turn, could result in lower demand for our services. As a result, we may experience lower utilization of, and may be forced to lower our rates for, our services and equipment. A decline in oil and natural gas prices or a reduction in drilling and production activities could have a material adverse affect on the demand for our services and our results of operations.

Prices for oil and natural gas historically have been extremely volatile and are expected to continue to be volatile. For example, over the last three years, the WTI Cushing crude oil spot price has ranged from a low of $25.24 per bbl on April 29, 2003 to a high of $77.03 per bbl on July 14, 2006. As of March 31, 2007, the WTI Cushing crude oil spot price was $65.88 per bbl. The Henry Hub natural gas spot price has ranged from $3.99 per mcf on October 31, 2003 to $15.39 per mcf on December 13, 2005. As of March 31, 2007, the Henry Hub natural gas spot price was $7.50 per mcf. Producers generally react to declining oil and natural gas prices by reducing expenditures. This has in the past had, and may in the future have, an adverse effect on our business. Mild weather in January 2007 caused some declines in the price of oil and natural gas and we experienced some signs of softer demand for our services early in the first quarter of 2007, which appeared to stabilize in the latter part of the quarter. We are unable to predict future oil and natural gas prices or the level of oil and natural gas industry activity. A prolonged low level of activity in the oil and natural gas industry will adversely affect both the demand for our products and services and our financial condition and results of operations.

When land-based rig counts are low, our rig relocation customers may not have a need for our services.

Many of the major United States drilling services contractors have significant capabilities to move their own land-based drilling rigs and related oilfield equipment and to mobilize rigs. When regional rig counts are high, drilling contractors often exceed their own capabilities and contract for additional oilfield equipment hauling and onshore rig mobilization capacity. Our rig relocation business activity is correlated to the onshore rig count; however, the correlation varies over the rig count range. The Baker Hughes onshore rotary rig rate for the weeks ended December 29, 2006 and March 30, 2007 were 1,626 and 1,676, respectively. As rig count declines, some drilling contractors reach a point where all of their oilfield equipment hauling and rig mobilization needs can be met by their own fleets. If one or more of our rig relocation customers decide not to outsource their rig and equipment hauling needs, our revenue attributable to rig relocation may decline much faster than the corresponding rig count. This relationship between our rig relocation business activity and the rig count in the areas where we have rig relocation operations can significantly increase the volatility of our earnings with respect to rig relocation.

We may not be able to manage future growth successfully, to grow successfully through future acquisitions, or to integrate the businesses we do acquire effectively.

Our business strategy has included, and will continue to include, growth through the acquisition of other businesses. In 2006, we acquired 11 businesses for a total purchase consideration of approximately $207 million. We may not be able to continue to identify attractive acquisition opportunities or successfully acquire identified targets on terms favorable to us. Competition for acquisition opportunities is substantial and may escalate, increasing our cost of making future acquisitions or causing us to refrain from making acquisitions. We may be required to incur substantial indebtedness to finance future acquisitions. Such additional debt service requirements may impose a significant burden on our results of operations and financial condition. Our credit agreement and indenture require that we meet certain financial covenants in order to borrow money to fund future acquisitions. In addition, we may not be successful in integrating our current or future acquisitions into our existing operations, which may result in unforeseen operational difficulties, diminished financial performance or

11

Table of Contents

Index to Financial Statements

our inability to report financial results and may require a disproportionate amount of our management’s attention. For example, if we are unable to effectively apply systems and controls to acquired businesses, including internal controls, the availability or timeliness of financial reports could be materially reduced.

Some of the financial statements included in this prospectus were audited by an accounting firm that does not regularly participate in the public securities offering process or prepare financial statements of the type that would be included in a public offering prospectus.

Wright, Moore, DeHart, Dupuis & Hutchinson, L.L.C., the audit firm for the financial statements of BLR Construction Companies, L.L.C. and affiliate and of BLR Construction Co., Inc. and affiliates included in this prospectus, is not registered with PCAOB and does not generally participate in public offerings or prepare financial statements of the type that would be included in a public offering prospectus. There can be no assurances that these financial statements would not be subject to revision if re-audited by UHY or another accounting firm registered with PCAOB and adjustments could be required.

We are vulnerable to the potential difficulties associated with rapid growth and expansion.

We have grown rapidly over the last several years through organic growth and acquisitions of other companies. Since our inception through March 31, 2007, we have acquired 24 businesses. We believe that our future success depends on our ability to manage the rapid growth that we have experienced and the demands from increased responsibility on our management personnel. The following factors could present difficulties to us:

| • | lack of sufficient executive-level personnel; |

| • | increased administrative burden; |

| • | increased organizational challenges common to large, expansive operations; and |

| • | long lead times associated with acquiring equipment. |

Our operating results could be adversely affected if we do not successfully manage these potential difficulties.

Our operating history may not be sufficient for investors to evaluate our business and prospects.

The historical financial information incorporated herein is not necessarily indicative of the results that would have been achieved had we operated on a fully integrated basis or the results of that may be realized in the future. We have a short operating history. In addition, we have grown significantly over the last few years through acquisitions. This may make it more difficult for investors to evaluate our business and prospects and to forecast our future operating results. Our future results will depend on our ability to efficiently manage our integrated operations and execute our business strategy.

We may require additional capital in the future, which may not be available to us.

Our acquisition strategy requires significant capital. In addition, our business is capital intensive, requiring specialized equipment and trained personnel to provide our services. We may need to raise additional funds through public or private debt or equity financings. Adequate funds may not be available when needed or may not be available on favorable terms. If funding is insufficient at any time in the future, we may be unable to service our equipment, fund acquisitions, take advantage of business opportunities or respond to competitive pressures, any of which could harm our business. Our future capital requirements primarily depend on the frequency, timing, size and success of our acquisitions.

12

Table of Contents

Index to Financial Statements

We depend on significant customers.

We derive a significant amount of our revenue from exploration and production companies and drilling contractors who are active in our markets. For the year ended December 31, 2006, our top ten customers accounted for approximately 35.2% of our revenue. Our inability to continue to perform services for a number of our large existing customers could have a material adverse effect on our business and operations.

Our success depends on key members of our management, the loss of any of whom could disrupt our business operations.

We depend to a large extent on the services of some of our executive officers and directors. We may not be able to retain our executive officers and may not be able to enforce the non-compete provisions in their employment agreements. The loss of the services of our executive officers, directors, or other key personnel could disrupt and adversely affect our operations. Please see “Management—Employment Agreements.”

Competition within the oilfield service industry may adversely affect our ability to market our services.

The oilfield service industry is competitive and fragmented and includes numerous small companies capable of competing in our markets on a local basis as well as several large companies that possess substantially greater financial and other resources than us. Our larger competitors’ greater resources could allow them to compete more effectively than us. We believe that the principal competitive factors in the market areas that we serve are quality of product and service, price, availability and technical proficiency. Our operations may be adversely affected if our current competitors or new market entrants introduce new products or services with better features, performance, prices or other characteristics than our products and services. Competitive pressures, excess capacity in our industry or other factors also may result in significant price competition that could have a material adverse effect on our results of operations and financial condition. Finally, competition among oilfield service and equipment providers is also affected by each provider’s reputation for safety and quality. If our safety record or the quality of our service declines, we may not be able to maintain our competitive position.

Our industry has experienced a high rate of employee turnover. Any difficulty we experience replacing or adding personnel could adversely affect our business.

We may not be able to find enough skilled labor to meet our needs, which could limit our growth. The oilfield service business has been cyclical in the past and is heavily influenced by oil and natural gas prices. Our services require skilled workers who can perform physically demanding work. As a result of our industry volatility and the demanding nature of the work, workers may choose to pursue employment in fields that offer a more desirable work environment at wage rates that are competitive with ours. We believe that our success is dependent upon our ability to continue to employ, train and retain skilled personnel. The demand for skilled workers is high, and the supply is limited, particularly in the Rocky Mountain region, which is one of our key regions. It is possible that we will have to raise wage rates to attract workers from other fields and to retain or expand our current work force. If we are not able to increase our service rates sufficiently to compensate for wage rate increases, our operating results may be adversely affected. Our inability to employ, train or retain skilled personnel generally could have a material adverse effect on our results of operations.

Our operations are subject to hazards inherent in the oil and natural gas industry.

Through our wellsite construction services, we operate cranes, forklifts, bulldozers and other heavy equipment. In addition, in connection with providing rig logistics services, we transport land-based drilling rigs and related equipment through the use of our heavy hauler trucks and trailers, cranes and other trucking and relocation assets. The operation of heavy equipment at the wellsite and the transportation of rigs and related assets may result in accidents, which can cause personal injury, loss of life, suspension of operations, damage to facilities and damage to or destruction of property. These and other operational risks inherent in our industry could expose us to substantial liability for personal injury, wrongful death, property damage, loss of oil and

13

Table of Contents

Index to Financial Statements

natural gas production, pollution and other environmental damages. The frequency and severity of such incidents will affect our operating costs, insurability and relationships with customers, employees and regulators. In particular, our customers may elect not to purchase our services if they view our safety record as unacceptable, which could cause us to lose customers and substantial revenue.

We do not have insurance against all foreseeable risks, either because insurance is not available or because of the high premium costs. The occurrence of an event not fully insured against, or the failure of an insurer to meet its insurance obligations, could result in substantial losses. In addition, we may not be able to maintain adequate insurance in the future at rates we consider reasonable, and there can be no assurance that insurance will be available to cover any or all of these risks, or, even if available, that it will be adequate or that insurance premiums or other costs will not rise significantly in the future, so as to make such insurance costs prohibitive. In addition, our insurance is subject to coverage limits and some policies exclude coverage for damages resulting from environmental contamination. See “Business—Operating Risks and Insurance.”

We are subject to federal, state and local regulation regarding issues of health, safety and protection of the environment. Under these regulations, we may become liable for penalties, damages or costs of remediation. Any changes in laws and government regulations could increase our costs of doing business.

Our operations are subject to federal, state and local laws and regulations relating to protection of natural resources and the environment, health and safety, waste management, and transportation of waste and other materials. Liability under these laws and regulations could result in cancellation of landbased wellsite or offshore operations, fines and penalties, expenditures for remediation and liability for property damages and personal injuries. Sanctions for noncompliance with applicable environmental laws and regulations also may include assessment of administrative, civil and criminal penalties, revocation of permits and issuance of corrective action orders. We maintain three tug boats and three barges that are required to be certified by the U.S. Coast Guard before the vessels may be deployed for use. In addition, some of our offshore workforce accommodation units must be certified by the U.S. Coast Guard before we can supply the units to our customers for use offshore. If we are unsuccessful or are delayed in certifying our vessels or certain of our accommodation units with the U.S. Coast Guard, our business, operating results and financial condition could be harmed.

Laws protecting the environment generally have become more stringent over time and are expected to continue to do so, which could lead to material increases in costs for future environmental compliance and remediation. The modification or interpretation of existing laws or regulations, or the adoption of new laws or regulations, could curtail exploratory or developmental drilling for oil and natural gas and could limit wellsite services opportunities. Some environmental laws and regulations may impose strict liability, which means that in some situations we could be exposed to liability as a result of our conduct that was lawful at the time it occurred as a result of conduct or conditions caused by, prior operators or other third parties. Clean-up costs and other damages arising as a result of environmental laws, and costs associated with changes in environmental laws and regulations could be substantial and could have a material adverse effect on our financial condition. We maintain insurance against some risks associated with underground contamination that may occur as a result of wellsite service activities. However, this insurance is limited to activities at the wellsite, and this insurance may not continue to be available or may not be available at premium levels that justify its purchase. The occurrence of a significant event not fully insured or indemnified against could have a materially adverse effect on our financial condition and operations. Please read “Business—Environmental Matters” for more information on the environmental laws and government regulations that are applicable to us.

We have operations located on lands that are regulated by the Bureau of Land Management of the United States Department of Interior and these operations may be subject to long periods of interruption or suspension.

The Bureau of Land Management (the “BLM”) enforces regulations that protect certain animals, such as deer, sage grouse and raptors that inhabit lands in the northern United States, where we have operations. We

14

Table of Contents

Index to Financial Statements

provide services in these locations and our revenue attributable to these services accounted for 22.3% of our total revenue for the year ended December 31, 2006. We are affected by this enforcement through the following ways. The BLM may deny or delay the granting of permits to us or our customers necessary to conduct operations in these lands. In addition, the BLM may restrict access to or seek our relocation from these lands for a period of time. As a result of this enforcement, our operations on these lands have been and may be interrupted or suspended for long periods of time. For example, from mid-November until mid-May, the period during which mule deer roam these lands, certain of our operations cease and go on stand-by. In addition, during April and May of each year, sage grouse nesting occurs and as a result, we are required to relocate our operations for a period of time. If these regulations become more stringent and, as a result, our operations are interrupted or suspended for longer periods of time, we could lose revenue. The loss of revenue that could occur could have a material impact on our financial condition and results of our operation.

Delays in obtaining permits by our customers for their operations could impair our business.

Our customers’ business operations require permits from various governmental agencies, including the BLM. The ease of obtaining the necessary permits depends on the type of operation and the state in which the operation will take place. As with all governmental permit processes, permits may not be issued in a timely fashion, or at all, or in a form consistent with our plan of operations. As a result, our operations may be interrupted or suspended for long periods of time, which could cause us to lose revenue and have a material adverse effect on our results of operation.

Our holding company structure makes us dependent on our subsidiaries to meet our financial obligations.

As a holding company, we have no significant assets other than the equity of our subsidiaries. In order to meet financial obligations, we rely exclusively on the cash flow from our subsidiaries. Our operating subsidiaries may be unable to generate sufficient cash flow for us to meet our financial obligations. Substantially all of our operating subsidiaries have guaranteed our senior notes and the debt under our credit facility.

If we fail to develop or maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. As a result, our business and the trading price of our common stock could be affected as potential shareholders lose confidence in our financial reporting.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud and to operate successfully as a public company. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results could be harmed. We cannot be certain that our efforts to develop and maintain our internal controls will be successful or that we will be able to maintain adequate controls over our financial processes and reporting in the future, including compliance with the obligations under Section 404 of the Sarbanes-Oxley Act of 2002. Any failure to develop or maintain effective controls, or difficulties encountered in their implementation or other effective improvement of our internal controls could harm our operating results or cause us to fail to meet our reporting obligations. Ineffective internal controls could also cause investors to lose confidence in our reported financial information, which would likely have a negative effect on the trading price of our common stock.

Our indebtedness could restrict our operations and make us more vulnerable to adverse economic conditions.

We now have, and after this offering will continue to have, a significant amount of indebtedness. As of December 31, 2006, our total debt was $257.5 million, including $253.0 million in aggregate principal amount due under our term loan and credit facilities. Following this offering and giving effect to the use of proceeds therefrom and to our January 19, 2007 issuance of $300 million of 9.75% Senior Notes, on an as adjusted basis our total debt would have been $ million. Holding all other variables constant, if interest rates on our floating rate debt increased or decreased by 1%, interest expense for the year ended December 31, 2006 would have increased or decreased by approximately $0.3 million. We will also have the ability to incur substantially

15

Table of Contents

Index to Financial Statements

more debt. We have a total borrowing capacity of $125.0 million under our credit facility of which $124.1 million was available as of March 31, 2007.

Our current and future indebtedness could have important consequences to you. For example, it could:

| • | impair our ability to make investments and obtain additional financing for working capital, capital expenditures, acquisitions or other general corporate purposes; |

| • | limit our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to make principal and interest payments on our indebtedness; |

| • | limit our ability to borrow funds that may be necessary to operate or expand our business; |

| • | prevent us from paying dividends to our stockholders, entering into transactions with affiliates or entering into sale and leaseback transactions that may be beneficial to us; |

| • | limit our ability to purchase or acquire property or assets, merge or consolidate with other entities or sell all or substantially all of our assets; |

| • | put us at a competitive disadvantage to competitors that have less debt; |

| • | increase our vulnerability to interest rate increases; and |

| • | hinder our ability to adjust to rapidly changing economic and industry conditions. |

Our existing term credit facility requires us to maintain certain financial ratios and to satisfy certain financial conditions. In addition, our credit facility and indenture contain numerous covenants that limit our discretion with respect to business matters, including mergers or acquisitions, paying dividends, repurchasing our common stock, incurring additional debt or disposing of assets. A breach of any of these covenants could result in a default under the agreement. If an event of default were to occur, we and our subsidiary guarantors may not be able to pay our debts or borrow sufficient funds to refinance them. Even if new financing were available, it may not be on terms acceptable to us. As a result of this risk, we could be forced to take actions that we otherwise would not take, or not take actions that that we otherwise might take, in order to comply with the covenants in the credit agreement or the indenture. For example, these restrictions could also limit our ability to obtain future financings, make needed capital expenditures, withstand a downturn in our business or the economy in general, or otherwise conduct necessary corporate activities.

Please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—2006 Credit Facility” for a discussion of our credit facility.

A terrorist attack or armed conflict could harm our business.

Terrorist activities, anti-terrorist efforts and other armed conflicts involving the United States or other countries may adversely affect the United States and global economies and could prevent us from meeting our financial and other obligations. If any of these events occur, the resulting political instability and societal disruption could reduce overall demand for oil and natural gas, potentially putting downward pressure on demand for our services and causing a reduction in our revenue. Oil and natural gas related facilities could be direct targets of terrorist attacks, and our operations could be adversely impacted if infrastructure integral to our customers’ operations is destroyed or damaged. Costs for insurance and other security may increase as a result of these threats, and some insurance coverage may become more difficult to obtain, if available at all.

Our operations in the Gulf of Mexico and coastal regions of Louisiana and Texas are adversely impacted by the hurricane season, which generally occurs in the second and third calendar quarters of the year.

Hurricanes and the threat of hurricanes during this period will often result in the shut-down of oil and natural gas operations in the Gulf of Mexico, coastal regions and land operations within the hurricane path. Our

16

Table of Contents

Index to Financial Statements

operations are negatively affected by hurricanes in three ways. First, we may incur significant expenses when we transport our accommodation units and surface and other equipment away from and back to the affected wellsite. Second, during a shut-down period, we are unable to access wellsites and our services are suspended resulting in loss of revenue for this period of time. Third, if we are unsuccessful in transporting our accommodation units and surface equipment away from the storm threatened area, the units and equipment may suffer significant damage resulting in additional expenses incurred to repair or replace the damaged units or equipment. For example, a number of our accommodation units and mats were damaged, displaced or lost during Hurricane Katrina. A period of approximately 60 days passed before we were able to purchase and deploy new accommodation units and mats in this area, resulting in lost revenue during such time. In addition, a significant amount of our offshore workforce accommodation business is conducted in areas susceptible to hurricanes. The occurrence of a hurricane can therefore create unpredictability in activity and utilization rates and lead to the destruction of our property, which can have a material adverse impact on our business, financial condition, results of operations and cash flow.

We have operations in the Gulf of Mexico where we do not maintain business interruption insurance.

Our offshore workforce accommodation business operates in the Gulf of Mexico and, to a lesser extent, other international offshore regions. We are not insured against interruptions of our offshore operations or business activities. If our operations in these areas are disrupted by severe weather conditions such as hurricanes, or otherwise, we will be unable to recoup the lost revenue resulting from these disruptions. If these operations are disrupted frequently and/or for a significant period of time, we could lose substantial revenue.

Our customers may not maintain insurance against damage to or the loss of the offshore products that they lease from us.

In our offshore workforce accommodation business, our customers are contractually obligated to maintain insurance against property damage to or loss of our workforce accommodation units. However, if our customers do not comply with their insurance obligations and our products sustain damage or are lost, then we may be unable to recover the value of the damaged or lost products. For example, certain of our offshore workforce accommodation units were damaged in the hurricanes that occurred in 2004. Some of our customers failed to maintain insurance against the damage to these units. These damaged products were lost or unusable for a substantial period of time. As a result, we incurred additional costs to repair or replace these units and were not able to earn revenue from these units during this time.

Increasing trucking regulations may increase our costs and negatively impact our results of operations.

Through our rig relocation and heavy equipment hauling business, we operate trucks and loaders. As such, we operate as a motor carrier in providing certain of our services and therefore are subject to regulation by the United States Department of Transportation and by various state agencies. These regulatory authorities exercise broad powers governing activities such as the authorization to engage in motor carrier operations and regulatory safety. There are additional regulations specifically relating to the trucking industry, including testing and specifications of equipment and product handling requirements. The trucking industry is subject to possible regulatory and legislative changes that may affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. Some of these possible changes include increasingly stringent environmental regulations, changes in the hours of service regulations which govern the amount of time a driver may drive and/or work in any specific period, onboard black box recorder device requirements or limits on vehicle weight and size.

Interstate motor carrier operations are subject to safety requirements prescribed by the United States Department of Transportation. To a large degree, intrastate motor carrier operations are subject to state safety regulations that mirror federal regulations. Such matters as the weight and dimensions of equipment are also subject to federal and state regulations.

17

Table of Contents

Index to Financial Statements