UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________

Commission file number: 01-31937

YANGLIN SOYBEAN, INC.

(Exact name of registrant as specified in its charter)

Nevada (State or other jurisdiction of incorporation or organization) | | 20-4136884 (I.R.S. Employer Identification No.) |

NO. 99 FANRONG STREET, JIXIAN COUNTY

SHUANG YA SHAN CITY

HEILONGJIANG PROVINCE

CHINA, 155900

(Address of Principal Executive Offices)

86-469-469300

(Registrant’s Telephone Number, Including Area Code)

VICTORY DIVIDE MINING COMPANY

(Former Name, Former Address And Former Fiscal Year, If Changed Since Last Report)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class: | | Name of Each Exchange on Which Registered |

| Common Stock, par value $0.001 | | None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes o No þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filed. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ |

| | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act):

Yes o No þ

The total revenue for the most recent fiscal year is US $155,206,867.

There was no active public trading market as of the last business day of the Company’s second fiscal quarter.

As of March 31, 2008, there are 20,000,003 shares of common stock outstanding.

YANGLIN SOYBEAN, INC.

(A Nevada Corporation)

TABLE OF CONTENTS

| | | | Page |

| | PART I | | |

| Item 1 | Business | | 3 |

| Item 1A | Risk Factors | | 16 |

| Item 1B | Unresolved Staff Comments | | 25 |

| Item 2 | Properties | | 26 |

| Item 3 | Legal Proceedings | | 27 |

| Item 4 | Submission of Matters to a Vote of Security Holders | | 27 |

| | | | |

PART II |

| Item 5 | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 27 |

| Item 6 | Selected Financial Data | | 27 |

| Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operation | | 29 |

| Item 7A | Quantitative and Qualitative Disclosures About Market Risk | | 29 |

| Item 8 | Financial Statements and Supplementary Data | | 44 |

| Item 9 | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | | 45 |

| Item 9A | Controls and Procedures | | 45 |

| Item 9B | Other Information | | 47 |

| | | | |

PART III |

| Item 10 | Directors, Executive Officers and Corporate Governance | | 47 |

| Item 11 | Executive Compensation | | 49 |

| Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 51 |

| Item 13 | Certain Relationships and Related Transactions, and Director Independence | | 54 |

| Item 14 | Principal Accounting Fees and Services | | 55 |

| | | | |

PART IV |

| Item 15 | Exhibits and Financial Statement Schedules | | 56 |

PART I

Item 1. Business

Organizational History

Yanglin Soybean Inc. (formerly known as Victory Divide Mining Company, the “Company”) was incorporated in the state of Nevada on May 26, 1921. Prior to October 3, 2007 the company has only nominal operations and assets.

On October 3, 2007, the Company executed a reverse-merger with Faith Winner Investments Limited (“Faith Winner (BVI)”) by an exchange of shares whereby the Company issued 18,500,000 common shares at $0.001 par value in exchange for all Faith Winner (BVI) shares.

Faith Winner (BVI) formed Faith Winner (Jixian) Agriculture Development Company (“Faith Winner (Jixian)” or “WFOE”), which entered into a series of agreements with Heilongjiang Yanglin Soybean Group Co., Ltd. (“Yanglin”) including but not limited to management, loan, purchase option, consignment, trademark licensing, non-competition, etc. As a result of entering the abovementioned agreements, WFOE is deemed to control Yanglin as a Variable Interest Entity as required by FASB Interpretation No. 46 (revised December 2003) Consolidated of Variable Interest Entities, an Interpretation of ARB No. 51

The reverse-merger also included an equity financing of $21,500,000 by the issuance of 10,000,000 Series A Convertible Preferred Stock at $2.15 per share to 10 accredited investors.

The Company, through its subsidiaries and Yanglin (hereinafter, collectively referred to as “the Group”), is now in the business of manufacturing, distribution, and selling of non-genetically modified soybean oil, salad oil, and soybean meal throughout the Province of Heilongjiang, China.

On January 17, 2008, the Company changed its name from “Victory Divide Mining Company” to Yanglin Soybean, Inc.”

Our Industry

We are a leading non-genetically modified (non-GM) soybean processor in the PRC. We currently manufacture soybean oil in bulk package and soybean meal which are sold throughout China our customers directly or through distributors. Most of our customer (approximately 80%) are located in Northern China.

Our manufacturing process includes sifting, crushing, heating and pressing soybeans, extracting and separating oil from crushed soybeans, and cleansing, hydrating and packaging oil as well as drying and packaging soybean meal. Currently, our main products include soybean oil, salad oil and soybean meal. We plan to broaden our product line to include high end products such as squeezed oil, powdered oil and protein concentrates, textured protein, and defatted soybean powder, while greatly enlarging the production capacity of salad oil. We have installed the equipment for manufacturing squeezed oil and expanded the production line for salad oil and have started production of these products by the end of 2007. The production facilities for powdered oil have been built and are now in trial production phase. We have also begun to build facilities for manufacturing soybean protein concentrates, textured protein and defatted soy powder, and these production lines will be put into operations in the middle of 2008.

The Soybean Processing Industry

Soybean processing is a traditional industry. Typically, soybeans are ground and refined into soybean oil and protein meal, which in turn are processed into refined oils, animal feed, proteins and more value-added products such as foods, pharmaceuticals and cosmetics.

(i) Soybean Oil and Soybean Salad Oil

Soybean oil is obtained by the extraction of oil from soybean seeds. Soybean oil contains various vitamins, minerals and unsaturated fatty acids which are essential to the well-being of the human body. It is an important ingredient in products such as salad dressings, margarine, paint and medicines. The price, adaptability and performance of soybean oil make it appropriate for a broad range of food, chemical and medical manufacturing applications. Soybean oil refers to Grade IV oil, as compared to the more refined salad oil. Both oils are for human consumption.

(ii) Soybean Meal

Soybean meal is manufactured by grinding soybean flakes which remain after removal of most of the oil from soybeans by a solvent or mechanical extraction process. Soybean meal is an important raw material used in the animal feed and farming industry due to its high protein content, low fat composition and edible characteristics. Given the PRC’s closer proximity to customers in the Asian region, there is a growing demand for PRC produced soybean meal from countries such as Korea and Japan. This in turn has led to an increase in demand for our soybean meal products.

Growth in the Soybean Industry

Apart from being a food commodity, soybean oil is also used in the cosmetics, pharmaceutical and medical industries. As soybean oil consumption in the PRC has been rapidly increasing, the PRC has imported soybean oil from other countries, such as Argentina, Brazil and the USA. In 2004/2005, the PRC imported 1.7 million tons of soybean oil. It is further projected that the demand for soybean oil in the PRC will increase to 14.4 million tons by 2015. (Source: http://www.chinawinner.net/nongchanpin00016.htm). We believe that such a development will have a positive impact on our business operations.

| | |

World Vegetable Oil Consumption 2006 | |

| | |

| |

| | | | | | |

| | | Million Short Tons | | Million Metric Tons | |

| Palm | | | 42.0 | | | 38.1 | |

| Soybeans | | | 39.3 | | | 35.7 | |

| Rapeseed | | | 19.7 | | | 17.8 | |

| Sunflower seed | | | 11.3 | | | 10.2 | |

| Peanut | | | 5.4 | | | 4.9 | |

| Cottonseed | | | 5.2 | | | 4.8 | |

| Palm Kernel | | | 4.8 | | | 4.3 | |

| Coconut | | | 3.6 | | | 3.3 | |

| Olive | | | 3.2 | | | 2.9 | |

| Total | | | 134.5 | | | 122.0 | |

Source: USDA

| | |

World Protein Meal Consumption 2006 | |

| | |

| |

| | | Million Short Tons | | Million Metric Tons | |

| Soybeans | | | 166.7 | | | 151.3 | |

| Rapeseed | | | 30.2 | | | 27.4 | |

| Cottonseed | | | 16.4 | | | 14.9 | |

| Sunflower seed | | | 12.7 | | | 11.5 | |

| Peanut | | | 6.3 | | | 5.7 | |

| Fish | | | 6.0 | | | 5.5 | |

| Palm Kernel | | | 6.1 | | | 5.5 | |

| Copra | | | 1.9 | | | 1.7 | |

| Total | | | 246.3 | | | 223.4 | |

Source: USDA

In the past few years, the soybean industry has seen a period of sustained growth. We believe that the soybean industry in the PRC has significant potential for further growth and we, through Yanglin, are well positioned to take advantage of such growth. Soybeans are grown for their oil and protein and are used to manufacture various products including soybean oil and soybean meal. According to the Food and Agriculture Organization of the United Nations, global consumption of oils and fats has been steadily increasing, rising at an average rate of approximately 3-4%. The growth is driven by the sustained income growth in the emerging market countries such as the PRC and India and we believe it is the increased consumption of soybean and palm oil in these countries that is to account for the bulk of such growth.

Specifically, the PRC is a major importer of soybeans. In recent years, there has been a marked increase in the volume of soybeans imported by the PRC from countries such as the USA, Argentina and Brazil. The latest statistics of China’s Customs showed that the PRC imported 30.8 million tons of soybeans in 2007, at a growth of about 9% over the previous year (source: China’s 2007 Import Volume of Soybean Reached Record-high 30.82 Million Tons, http://content.caixun.com/NE/00/nm/NE00nmcu.shtml). China’s National Grains and Oils Information Center estimated that the total consumption of soybeans from 2005 to 2006 (October 2005 to September 2006) was 42.32 million tons. (Source: ,http://sg.biz.yahoo.com/060223/15/3ywco.html, February 23, 2006-12-20, Source: http://www.tdctrade.com/report/indprof/indprof_070703.htm dated July 9, 2007)

We believe that such growth in consumption of soybeans in the PRC market is beneficial to our business operations and presents great potential for our further development.

Source: http://sjzl.agri.gov.cn/rpt/reportControl/reports.aspx?Target=_self&ReportID=21

Non-Genetically Modified Soybean Products

Genetically modified soybean plants are widespread in the world’s leading soybean producing countries (such as Brazil, Argentina and the United States) and genetically modified soybeans comprise a very large proportion of the world’s soybean production. Conversely, most of the soybean food products exported from the PRC is primarily made from non-genetically modified soybeans that are cultivated and grown in the PRC.

We believe that a growing number of consumers prefer their soybean products to be made from non-genetically modified soybeans. Owing to potential health issues associated with genetically modified soybean products, such non-genetically modified soybean products are perceived to be “green” and hence more desirable to certain classes of consumers than genetically modified soybean products, especially with respect to soy protein and other value-added soybean products. Furthermore, we believe that as a result of the increasing affluence and sophistication of the consumers in the PRC, European Union, Korea and Japan, they have also become more aware of potential health issues arising from the consumption of genetically modified soybean products and are willing to pay a premium for non-genetically modified soybean products.

As a producer of non-genetically modified soybean products, we believe we are well positioned to take advantage of such growth.

Government Support for the Soybean Industry

In addition, there has been strong government support for the development of our industry. In recent years, the PRC government has sought to differentiate soybean exports from the PRC from those from other international exporters of soybeans such as the United States and Argentina. Specifically, the PRC government has take measures to promote industries and enterprises, such as our business operations, that produce non-genetically modified soybean food products. In 2003, the PRC Ministry of Agriculture announced a plan to develop the PRC’s northeastern region (including the Heilongjiang province where we are located) into the world’s largest non-genetically modified soybean production centre for export within five years.

In addition, the Heilongjiang provincial government has introduced a number of measures to develop its organic farming industry such as improving its local agriculture infrastructure and promoting the development of large industrial groups that produce green and organic food products. Over the past five years, Heilongjiang's green food industry has grown significantly and has become an important growth sector in Heilongjiang’s burgeoning economy. Further, we believe that the proportion of “deep-processed” soybean food products produced by the PRC will increase and is expected to grow significantly, particularly with the completion of the PRC’s largest non-genetically modified soybean deep-processing base in by 2010.

We believe that these various government initiatives at national and local level will have a positive impact on the further development of our business operations.

Our Competitive Advantages

We believe that we have several competitive advantages:

1. Our products have favorable brand recognition because of the superior quality of our products;

2. Our workers have great skills and experience in the soybean industry. Many of them worked in the industry for more than 20 years;

3. Our business is better managed and is more flexible than many larger state-owned soybean processors. As a privately owned business, we are more efficient and in better financial conditions.

4. Our costs are lower than those of our major competitors because our management is lean and efficient.

5. We have vast sales networks covering the most areas of China and better arrangements of the distributors which save cost and promote higher efficiency.

6. We believe that we are one of the largest players in the non-genetically modified soybean industry. Given that large international agricultural conglomerates such as Archer Daniels Midlands and Cargill produce predominantly genetically modified soybean food products, we do not face direct competition from these players in our niche market.

Our Strategy

Increase Our Sources of Supply

Due to the increasing market demand, we expect our business to grow significantly in the next few years. Our need for soybean supply will only increase. In order to increase our raw material supplies, we intend to expand the soybean cultivation area supplying us through the development of further supply arrangements with other private and state-owned farms within the Heilongjiang province. Currently, we have access to soybeans produced in approximately 164,745 acres of farmland and we plan to increase our access to approximately 823,723 acres of farmland in the next few years in other locations by signing up more soybean farmers and through other arrangements.

Expand Capacity by Building New Plants or through Acquisitions

To meet the demand for soybean products, we plan to increase our capacity. We intend to expand our production facilities by acquiring of 3 or 4 additional factories. We expect that these acquisitions will allow us to increase our current annual soybean processing capacity to approximately 1.5 million tons of soybeans over the next 3 years.

Expansion of our Sales Network

We currently sell more in the northern China than other parts of China and currently do not have many sales offices in the South. We plan to expand our sales and marketing network by establishing more sales offices within the PRC. In addition, we are talking to potential agents in Southeast Asia and Russia. We intend to use Chinese export agents to manage currency risk. Our plan is to expand internationally into countries such as Singapore, Malaysia, Canada and the United States.

Expansion of our Product Line

We believe that value added soybean products will yield higher profits margins for our operations. We intend to expand our product lines to include the following high end soybean products:

(i) Powdered Soybean Oil

Powdered soybean oil is manufactured by processing soybean oil and soybean salad oil together with corn syrup and other raw materials. Powdered soybean oil not only retains the nutritional value of liquid soybean oil , but also has a long shelf life and can be easily packaged and transported. In addition, powdered soybean oil can be used as a cheap substitute for milk or powdered milk because it can be easily dissolved or mixed with other ingredients in water to produce a mixture that has a strong fragrance similar to that of milk, as well as containing beneficial proteins and minerals.

(ii) Textured Protein

Textured protein products are manufactured from soy protein. Textured protein products are hydrated in the production process and accordingly have a symmetrical, consistent and smooth texture and specific structure. Textured protein can be added to food products to impart a taste that is similar to that of meat. Therefore, textured protein can be used as a food substitute for beef and pork. In addition, textured protein contains anti-oxygenation ingredients that could prolong the shelf-life of certain food products.

(iii) Defatted Soybean Powder

Defatted soybean powder is manufactured from specially-extracted soy meal and has a high protein content (higher than 50 per cent.). Defatted soybean powder can be added to fish, noodles, meat, dairy products and candy to improve the quality and taste of food. Further, defatted soybean powder can prolong shelf life [and reduce cost.

(iv) Squeezed Oil

Squeezed oil is made by extracting crude soybean oil from selected soybeans through traditional methods of refining and hydration in order to remove the acids in the oil. Squeezed oil is readily absorbed by the human body and contains no cholesterol. It possesses vitamins such as A, D, and E, as well as other nutrients which have been shown to help growth, improve immunity and prevent hypertension and arteriosclerosis.

(v) Concentrated Soy Protein

Concentrated soy protein has a high protein content of up to 98% and contains no cholesterol. Concentrated soy protein can be used as an ingredient in food products to improve their texture and nutritional value. Concentrated soy protein is used as an ingredient in a wide range of food products, including nutritional supplements, seafood, processed meats, frozen food, nutritional beverages, cream soups, sauces and snacks.

Our Current Products

Our current products include the following:

Product | Use | Major Customers | 2007 Volume (tons) |

| Soybean Oil | Cooking | Yingkou Bohai Grease Industrial Co. Ltd., Yi Liping | 49,566 |

| Salad Oil | Cooking | Yingkou Bohai Grease Industrial Co. Ltd., Yu Guanghai | 15,207 |

| Soybean Meal | Animal Feed | Yingkou Bohai Grease Industrial Co. Ltd., Tongliao Hongzhan Animal Feed Factory, Li Yuqiu, Gu Changchun, Wang Chunyu | 319,706 |

We sell our products under the “Yanglin” brand name to various geographic regions of the PRC through our various distribution channels (see “Sales and Marketing” below) directly to our customers primarily within the PRC market. In the fiscal year ending 2007, we processed approximately 385,000 tons of soybeans and generated total revenues amounting to approximately $155.2 million with net income amounting to $10.3 million. Within the 2007 production volume of our main products, namely soybean meal, soybean oil and salad oil, soybean meal occupied a major share of about 83%, while soybean oil and salad oil made up 17% together.

Our Suppliers of Soybeans

Maintaining a stable supply of raw materials (soybeans) is one of the key components for our success. We purchase all our soybean supplies from various farms in the Heilongjiang province. We have established and maintained good relationships with these farms.

The following is a list of our top ten major suppliers of soybeans for the financial year ended December 31, 2007:

| Supplier | | Amount Purchased (in US$) | | % of Total Purchases (%) | |

| Baoqing North Granary | | | 10,905,894.11 | | | 7.46 | |

| Cui Bingyan | | | 6,138,677.51 | | | 4.20 | |

| Duan Xufeng | | | 5,437,402.67 | | | 3.72 | |

| Chi Cuie | | | 5,211,779.68 | | | 3.56 | |

| Wang Li | | | 5,176,965.99 | | | 3.54 | |

| Tang Lijun | | | 4,890,610.42 | | | 3.35 | |

| Jiang Minghui | | | 4,279,171.14 | | | 2.93 | |

| Bai Wenlong | | | 4,261,078.14 | | | 2.91 | |

| Chen Fuzhen | | | 3,622,287.92 | | | 2.48 | |

| Chen Libin | | | 3,534,869.87 | | | 2.42 | |

Note: the amounts are converted from RMB value using the yearly average rate of 2007, 1USD = 7.6172RMB.

Our top ten suppliers together made up an aggregate of 36.6% of our total supply of soybeans, but our biggest supplier only supplied less than 7.5% of our total supply, while none of the other top suppliers occupied a share of over 5%. We believe this diversification of supply is beneficial to us as it increases our bargaining power and prevents us from being over-reliant on any single supplier.

We have been using a unique type of arrangements with soybean suppliers. Through our affiliate company, Heilongjiang Yanglin Group Seed Co. Ltd., we supply these farmers with “Yanglin” soybean seeds which provide higher oil yield. Pursuant to annual supply contracts, the farmers sell the harvested soybeans back to us. We extend favorable commercial terms to these farmers, such as low price and credit payment terms, for them to purchase “Yanglin” soybean seeds, and offer favorable price, which is higher than average market price, and cash-upon-delivery payment terms to the farmers for our purchases of the harvested soybeans grown from “Yanglin” soybean seeds. These arrangements ensure that we maintain good relations with our suppliers, enjoy a stable supply of soybeans that meet our high quality standards at competitive rates, and allow us to maintain a low rate of expenditure on raw materials.

To further ensure a consistent and supply of soybeans and to increase its volume, we intend to enter into similar supply agreements with other soybean farmers in the PRC.

The Supplier of “Yanglin” Soybean Seeds

Heilongjiang Yanglin Group Seed Co, Ltd. is owned and managed by Mr. Shulin Liu, our chief executive officer.

Heilongjiang Yanglin Group Seed Co., Ltd has developed several strains of non-genetically modified soybean seeds (collectively, “Yanglin” seeds”). The Yanglin “East Nong 42” and the “Black Nong 44” boast high protein and fat content. It has also developed the high oil content “Yang 02-01”, “Yang 03-02” and “Yang 03-03” soybean seeds, the high protein content “Yang 03-656” soybean seeds and the high protein and high yielding “Yang 03-149” soybean seeds.

A brief summary of the characteristics of each strain of soybean seed is set forth below:

Soybean | Oil Content | Protein Content | Status of Development |

| “East Nong 42” | 19.33% | 45% - 46.4% | Completed |

| “Black Nong 44” | 21.56% - 22.61% | 38.56% - 46.69% | Completed |

| “Yang 02-01” (high oil) | 22.3%-22.6% | 37.8%-40.2% | Received governmental approval |

| “Yang 03-02” (high oil) | 21.9%-22.7% | 37.2%-41.5% | In trial phase |

| “Yang 03-03” (high protein) | 21.7%-22.1% | 38.4%-45.9% | In trial phase |

| “Yang 03-656” (high protein) | 19.8%-20.6% | 39.7%-45.3% | In trial phase |

| “Yang 03-149” (high protein) | 20.3%-21.9% | 41.5%-44.7% | In trail phase |

Major Customers

Our customers are primarily distributors of soybean oil and soybean meal, with some of them being soybean food processors and animal feed manufacturers. The following is a list of our top ten major customers for fiscal year 2007. All of our major customers are located in the PRC.

Customers | Type of Product | Fiscal 2007 Sales (USD) | % of Total Sales (%) |

| Yingkou Bohai Grease Industrial Co. Ltd. | Soybean Oil | 15,705,039.65 | 10.1% |

| Wang Chunyu | Soybean Meal | 5,290,261.11 | 3.4% |

| Huang Zujian | Soybean Meal | 5,184,750.61 | 3.3% |

| Tongliao Hongzhan Animal Feed Factory | Soybean Meal | 4,553,189.66 | 2.9% |

| Wang Linli | Soybean Meal | 4,233,973.89 | 2.7% |

| Gu Changchun | Soybean Meal | 3,764,879.43 | 2.4% |

| Wang Xihe | Soybean Meal | 3,669,944.96 | 2.4% |

| Li Yuqiu | Soybean Meal | 3,666,983.30 | 2.4% |

| Li Zhengqian | Soybean Meal | 3,407,444.15 | 2.2% |

| Yu Guanghai | Soybean Meal | 3,379,734.87 | 2.2% |

Note: the amounts are converted from RMB value using the yearly average rate of 2007, 1USD = 7.6172RMB.

Our sales are widely diversified among our customers. Our largest customer accounts for only 10.1 % of our total sales in fiscal 2007 while our top ten customers accounted for about 34 % of our net sales in fiscal 2007. As such, we are not dependent on any single customer and have accordingly maintained our bargaining position in relation to our customers. Holding such a diversified customer base, we have mitigated the commercial risk and associated impact of the loss of sales from any single customer. As we begin to expand our product offering to include “high end” soybean products, our customer base will accordingly change to include more industrial users and some retail consumers.

Sales of Products by Type and Locations

The following table shows the breakdown of sales volume by customer type.

Type | Salad Oil | Soy Oil | Soy Meal |

Volume (Tonnes) | Number of customers | % | Volume (Tonnes) | Number of customers | % | Volume (Tonnes) | Number of customers | % |

| Distributor | 14,898 | 71 | 98 | 48,080 | 85 | 97 | 287,740 | 85 | 90 |

| Food Manufacturer | | | | | | | 2,877 | 8 | 0.9 |

| Animal Feed Manufacturer | | | | | | | 25,576 | 14 | 8 |

| Others | 309 | 5 | 2 | 1,486 | 8 | 3 | 3,513 | 4 | 1.1 |

| Total | 15,207 | 76 | 100 | 49,566 | 93 | 100 | 319,706 | 111 | 100 |

All our sales are primarily made to customers within the PRC, though some of our products may be exported by some of the distributors to countries such as Japan, Korea, Russia and India. The geographical distribution of our sales in the PRC for fiscal 2007 is shown below.

Province | Sales Revenue (Salad Oil) | Sales Revenue (Soybean Oil) | Sales Revenue (Soybean Meal) |

Volume (Tonnes) | Value (USD) | Volume (Tonnes) | Value (USD) | Volume (Tonnes) | Value (USD) |

| Heilongjiang | 13,686 | 14,014,298.24 | 29,752 | 28,254,752.43 | 35,970 | 10,414,262.27 |

| Jilin | 1,521 | 1,557,485.58 | 17,355 | 16,481,622.36 | 36,936 | 10,693,944.71 |

| Liaoning | | | 2,459 | 2,335,265.89 | 64,841 | 18,773,177.10 |

| Inner Mongolia | | | | | 8,999 | 2,605,447.49 |

| Beijing | | | | | 9,994 | 2,893,526.19 |

| Tianjin | | | | | 9,598 | 2,778,873.76 |

| Shandong | | | | | 15,987 | 4,628,657.52 |

| Shanxi | | | | | 15,789 | 4,571,331.31 |

| Henan | | | | | 14,798 | 4,284,410.71 |

| Sha’anxi | | | | | 9,591 | 2,776,847.08 |

| Gansu | | | | | 10,285 | 2,977,778.36 |

| Guangxi | | | | | 17,987 | 5,207,710.19 |

| Sichuan | | | | | 18,976 | 5,494,051.74 |

| Hebei | | | | | 49,955 | 14,463,424.53 |

Note: the amounts are converted from RMB value using the yearly average rate of 2007, 1USD = 7.6172RMB.

Our Competitors

Our competitors are the non-genetically modified soybean processors operating in the PRC. Our main competitor is Heilongjiang 93 Oil and Fat Co., Ltd., an integrated state-owned enterprise which is located in Heilongjiang, Dalian and Tianjin. The rest of our competitors are smaller state-owned enterprises.

Position | Company | Estimated Annual Non-GM Production Capacity (in Tonnes) | Estimated Market Share |

| 1 | Heilongjiang Jiushan 93 Group (SOE) | 600,000 | 6.7% |

2 | Yanglin Soybean Group, Ltd | 520,000 | 5.0% |

| 3 | Shandong Gaotang Lanshan Group (SOE) | 200,000 | 2.2% |

| 4 | Henan Xuchang Vegetable Oil Company (SOE) | 100,000 | 1.1% |

| 5 | Qitaihe City Nature Oil Company | 100,000 | 1.1% |

| 6 | Shandong Guanxian Vegetable Oil Company | 100,000 | 1.1% |

| 7 | Jiamusi Zhenda Company | 90,000 | 1.0% |

Source: Information from respective companies' websites and Yanglin estimates

We do not compete with companies that produce genetically modified soybean products, whether in the PRC or internationally.

Sales and Marketing

Apart from our high product quality, our marketing efforts have also contributed to our success in PRC markets. Presently, our main method of selling our products is direct marketing, supplemented with indirect marketing. Given that we are located in the Heilongjiang province, we are in close proximity to our suppliers and customers, so it’s easier for us to deal with them directly (as opposed to going through the Dalian Commodities Exchange).

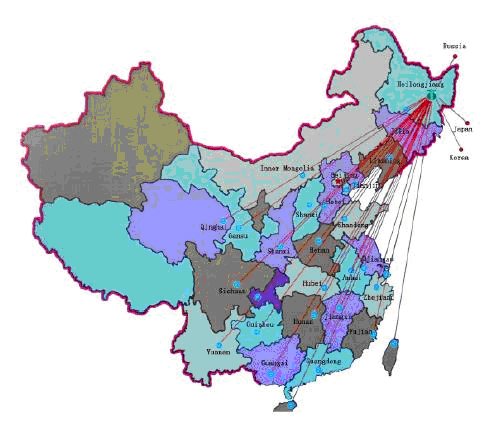

We have sales offices in more than 5 cities in the PRC with approximately 40 independent distributors spread over approximately 27 provinces. These provinces include locations in the northeastern, northwestern and southern regions of the PRC. Furthermore, we have a dedicated in-house sales team with approximately 10 salespersons. Their duties include monitoring the soybean industry, collecting market and price information, developing and managing distributors, providing recommendations for our marketing and sales strategy and pricing policies, filling sales orders and after-sale services.

The following map illustrates the geographical coverage of our sales and distribution network within the PRC:

In addition to our direct marketing efforts in the PRC, and as part of our international expansion plans, we plan to appoint sales agents in North America, Europe, Russia, Japan, Korea and other countries in southeast Asia in the near future.

Advertising

We advertise our products through various forms of media, including billboards alongside highways. We are now building our own business website (www.yanglin.com.cn).

In addition, our marketing team develops and maintains a unified and distinctive image throughout all our corporate publicity materials, including our corporate billboard advertisements, media publicity and corporate branding.

Publicity

We hold an annual conference with the distributors and potential customers to promote our products. We regularly attend exhibitions in different regions to market our products, and plan to attend the Guangzhou Commodity Fair to promote our high end products when we begin to produce them. We plan to maintain and strengthen our existing customer relations through symposiums, guided tours of the company and direct correspondences that provide further information of our product offering. We will also strengthen communications with the relevant government departments in order to keep abreast of new policies and guidelines. This will enable us to adapt quickly to any changes, better seize business opportunities and develop new markets.

Delivery of Products

Approximately 70 % of our products are transported to our customers by railways, thanks to our easy access to the PRC railroad network (see “Our Competitive Advantages”). The costs of transportation are borne by our customers and are pre-paid in advance ahead of delivery of the products. The remainder of our products is collected from our facilities by our customers.

Pricing and Terms

Prices of our products are determined based on the daily spot market price, which is determined by the average of ex-works prices of local producers and the quotation on commodities exchanges. We distinguish between long-term customers and short-term customers and provide rebate policies accordingly. Our short-term customers (typically customers we have been dealing with for less than a year) are required to pay us the full retail price in cash in advance of delivery of their ordered products. For our long-term customers, we may offer credit terms as well as certain preferential terms to them depending on the size of their orders. Since we are paid with cash in advance most of the time, there are almost no accounts receivables.

The current prices for our products, as of December 31, 2007 are: (including VAT)

Products | | Price (USD/metric ton) | |

| Soybean oil (Grade IV) | | $ | 1,451 | |

| Salad oil | | $ | 1,533 | |

| Soybean meal | | $ | 472 | |

Based on the basis exchange rate of 1US$ = 7.3046 RMB as published on the website of People’s Bank of China on December 28, 2007.

For the past three years, the price of soybean meal has been in the range of $246 per metric ton to $493 per metric ton (converted at the above mentioned foreign exchange rate published on the website of People’s Bank of China on December 28, 2007; the same rate is used hereinafter). By comparison the price range of soybean oil has been in the range of $659 per metric ton to $1,451 per metric ton, while the price range of salad oil was from $746 per metric ton to $1,533 per metric ton. The prices of our products are determined by taking into account the costs of labour as well as the seasonality of demand in the soybean market. Traditionally, our prices of our raw materials are lowest during the soybean harvest period between October and December. Our prices then peak from January to February because of the New Year and Spring Festival.

Intellectual Property

We have registered the following trademarks in the PRC, which are currently used for all our products:

Trademark | Country of Registration | Class | Registration Number | Date of Registration | Validity Period |

| “Yanglin”logo | PRC | [29] | 1587278 | June 14, 2001 | From June 14, 2001 to June 13, 2011 |

| “Yanglin”logo | PRC | [31] | 1586742 | June 14, 2001 | From June 14, 2001 to June 13, 2011 |

Class 29 is for meat, fish, poultry and game; meat extracts, preserved, dried and cooked fruits and vegetables; jellies, jams, fruit sauces; eggs, milk and milk products; edible oils and fats. Class 31 is for agricultural, horticultural and forestry products and grains not included in other classes; live animals, fresh fruits and vegetables; seeds, natural plants and flowers; foodstuffs for animals, malt.

Employees

Currently we have 466 employees, most of whom are involved in production and operations.

The functional breakdown of our full-time employees as at December 31, 2005, 2006 and 2007 was:

| | | FY2005 | | FY2006 | | FY2007 | |

| Production and operations | | | 212 | | | 291 | | | 291 | |

| Sales | | | 6 | | | 10 | | | 10 | |

| Management | | | 30 | | | 163 | | | 165 | |

| Total number of employees | | | 248 | | | 464 | | | 466 | |

Along with staff incentive policies, we provide social security to every employee who signs a long term contract with us, and we have paid all social security fees as required by laws and regulations.

We have a system of periodic performance reviews that are conducted annually.

Insurance

We have the following insurance policies:

Description of Policy | Term | Coverage ($) | Premium ($) | Insured |

| China Pacific Insurance Co., AAAH0300003307 | From Jan. 29, 2007 to Jan. 28, 2008 | 30,327.72 | 174.73 | The boiler of Factory No. 1 |

| China Dadi Insurance Co., PQZA200723010600000008 | From Jul. 10, 2007 to Jul. 9, 2008 | 1,782,920.71 | 2,396.77 | Workshop and Office Building of Factory No. 3 |

| China Dadi Insurance Co., PQZA200723010600000007 | From Jul. 10, 2007 to Jul. 10, 2008 | 2,221,703.38 | 2,986.62 | Machinery of Factory No. 3 |

| China Dadi Insurance Co., PQZA200723010600000008 | From Jul. 12, 2007 to Jul. 11, 2008 | 260,319.11 | 1,849.71 | The boiler of Factory No. 3 |

| China Pingan Insurance Co., 21900004601010700013 | From Sep. 29, 2007 to Sep. 29, 2008 | 2,886,315.47 | 4,157.20 | Machinery of Factory No. 1 |

| China Life Insurance Co. | From Jun. 30, 2007 to May. 29, 2008 | - | 2,441.84 | The employees of the three factories |

Note: the amounts in the column Coverage are converted from RMB value using the year end rate of 2007, 1USD = 7.3141RMB, and those in the column Premium are converted from RMB value using the yearly average rate of 2007, 1USD = 7.6172RMB.

Government Regulations

We are subject to various government regulations, such as Food Sanitation Law, Environment Protection Law and Fire Prevention Law, and to national standards for food issued by the national Food and Drug Administration. We have obtained the Sanitation Admission certificate from the local Sanitation Bureau as well as the industrial production permit, and our facilities are regularly inspected by local authorities.

In addition, we have been issued an ISO 9001-2000 Certificate by the Beijing Zhongjing Kehuan Quality Authorization Co. Ltd and a Certificate of Class A Green Food by the China Center of Development of Green Food.

Environmental Compliance

We are subject to the PRC environmental laws, rules and regulations governing our type of manufacturing facility. We have complied with the prescribed standard of environmental protection as evidenced by a certificate issued by the Jixian Environment Protection Bureau dated February, 2007.

The treatment of our waste water is subject to the PRC Environment Protection Law. Our process of treating waste water meets the strict requirement of this law.

Item 1A. Risk Factors

Cautionary Statement Regarding Future Results, Forward-Looking Information And Certain Important Factors

In this report we make, and from time to time we otherwise make, written and oral statements regarding our business and prospects, such as projections of future performance, statements of management’s plans and objectives, forecasts of market trends, and other matters that are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements containing the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimates,” “projects,” “believes,” “expects,” “anticipates,” “intends,” “target,” “goal,” “plans,” “objective,” “should” or similar expressions identify forward-looking statements, which may appear in documents, reports, filings with the Securities and Exchange Commission, news releases, written or oral presentations made by officers or other representatives made by us to analysts, stockholders, investors, news organizations and others, and discussions with management and other of our representatives. For such statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Our future results, including results related to forward-looking statements, involve a number of risks and uncertainties. No assurance can be given that the results reflected in any forward-looking statements will be achieved. Any forward-looking statement speaks only as of the date on which such statement is made. Our forward-looking statements are based upon assumptions that are sometimes based upon estimates, data, communications and other information from suppliers, government agencies and other sources that may be subject to revision. Except as required by law, we do not undertake any obligation to update or keep current either (i) any forward-looking statement to reflect events or circumstances arising after the date of such statement, or (ii) the important factors that could cause our future results to differ materially from historical results or trends, results anticipated or planned by us, or which are reflected from time to time in any forward-looking statement.

In addition to other matters identified or described by us from time to time in filings with the SEC, there are several important factors that could cause our future results to differ materially from historical results or trends, results anticipated or planned by us, or results that are reflected from time to time in any forward-looking statement. Some of these important factors, but not necessarily all important factors, include the following:

Risks Related To Our Business

Our raw material supply is vulnerable to natural disasters, which could severely disrupt the normal operation of our business and therefore adversely affect our business.

As soybeans are our main raw materials and most of our soybeans are grown in and obtained from farmers in the Heilongjiang province, natural disasters such as drought, earthquakes, floods, and heavy rains in Heilongjiang may lead to a shortage in our supply of soybeans and result in soybean price increases, and consequently adversely affect our operations.

Our efforts to manufacture value added products may not be successful.

In order to grow our business and achieve higher profit margins, we have begun to construct new plants and add new equipment to manufacture value added products such as high-grade oil, protein concentrate, textured protein, powdered oil, etc. If the consumers do not accept our new products, the market for such products has not fully developed, or we do not have experienced sales personnel to market such products, we may not achieve the result as we expect and our business operation and financial conditions may be adversely affected.

Soybean prices fluctuate greatly. This may adversely affect our operations.

As a commodity, soybeans are subject to the price fluctuation of the commodity market in China and indirectly to the international commodity market. For example, the soybean price went up from RMB 1.23 per 500 grams at the beginning of the last year to RMB2.13 per 500 grams at the end of 2007, and in early March 2008 it has climbed to as high as RMB 2.75 per 500 grams, due to both the shortage in soybean supply caused by a severe drought in 2007 and farmers’ cutting growing areas of soybeans brought by the continuously low price level by the end of 2006. If the soybean price increases significantly, we may have a problem caused by increased demand on working capital to satisfy the raw materials needs of our operations.

Our full capacity may be reached soon. Our growth may be impacted if we could not expand our capacity in the near future.

The designed capacity of our facilities is 520,000 tons per year and the maximum utilization rate for our industry is approximately 90%. We processed 385,000 tons of soybean in 2007 and we expect to process about 420,000 tons in 2008. We will soon need additional capacity to grow our business. If we are not able to build or acquire new facilities in 2009, the growth of our business maybe adversely affected.

We do not have long-term soybean supply contracts, which could have a material adverse effect on us.

Currently, we source about 70% of our raw materials from farmers with whom we have a long term relationship and about 30% from intermediaries who purchase directly from other farmers. However, we do not have long term contracts with the farmers or the intermediaries. All current supply contracts with the soybean farmers are one-year contracts without fixed prices. Therefore, we may not be able to control supply risks. Any significant fluctuation in price of our raw materials could have a material adverse effect on the manufacturing cost of our products.

We have tried to mitigate the risks by paying attractive premium to those farmers who will purchase “Yanglin” soybean seeds, cultivate and plant them and then sell the soybeans to us in order to guarantee our soybean supplies. However, if our competitors also pay premium or even pay higher premium to attract the suppliers, we may lose our advantage in purchasing price and lose some of the soybean supplies.

The soybean price is largely beyond our control in addition to natural disaster or supply competition.

The soybean price may also be affected by other factors in addition to natural disaster or supply competition, such as global commodity price increase, government control or suppliers’ financial difficulties. We may have limited options in the short-term for alternative supply if our suppliers fail for any reason, including suppliers’ business failure or financial difficulties to continue the supply of raw materials. Moreover, identifying and accessing alternative sources may increase our costs. Although raw materials are generally available and we have not experienced any raw material shortage in the past, we cannot assure that the necessary materials will continue to be available to us at prices currently in effect or acceptable to us.

Some of our land may be reclaimed by the government and this may materially impact our operations.

Most land in China is state-owned and land use rights may be granted, transferred, leased or allocated. Allocated land use rights are generally provided by the government for an indefinite period (usually to state-owned entities) and cannot be pledged, mortgaged, leased, or transferred by the user. As the same time, allocated land can be reclaimed by the government at any time. The lands occupied by Factory No. 1 and No. 2 is allocated land and accordingly subject to the risk of being reclaimed. We are in the process of applying for the land use rights over Factory No. 2 to be changed to transferred. Although the risk being reclaimed is very small because the government is encouraging the growth of our industry and in general the market economy system and will continue to support our business, we cannot guarantee the land will not be reclaimed in the future.

We may lose our advantages if there is emergence of new production technologies for other competitors.

Our business is dependent on our ability to utilize current technologies to produce high quality products with low cost. Currently, we employ advanced technologies now available in our manufacturing process. However, newer and better manufacturing technologies may emerge. If we are unable to adapt the production processes to newer and more efficient manufacturing technologies that may be used by our competitors to manufacture products that are of higher quality or at a lower cost, we may lose market share and our financial performance may be adversely affected because we do not have the financial resources to build new facilities using such new technologies.

Our manufacturing process is highly dangerous, which could cause adverse effects on our operation.

In our manufacturing process, we use highly inflammable and explosive chemical solutions. Therefore, fires and explosions could occur, which could cause delay in our production, damages to our facilities and injuries to our workers.

We receive a significant portion of our revenues from a small number of customers. Our business will be harmed if our main customers reduce their orders from us.

Our customers mainly comprise approximately 40 distributors of soybean oil and other soybean products, as well as soybean food product and animal feed manufacturers. Although our sales are widely diversified among our customers and our largest customer accounts for only 10% of our total sales, our top ten customers accounted for about 34% of our net sales in fiscal 2007. Dependence on a few customers could make it difficult to negotiate attractive prices for our products and could expose us to the risk of substantial losses if a single dominant customer ceases purchasing. If we lose any customers and are unable to replace them with other customers that would purchase a similar amount of our products, our revenues and net income would decline considerably.

Our product delivery is dependent upon the efficiency of the rail system and any disruption in the services or increase in transportation costs will have a material adverse impact on our operations.

Approximately 70% of our products are transported to our customers by rail. We are largely dependent upon the efficiency of China’s rail system and network to deliver our products. Any disruption of their service will largely impact our ability to fulfill our orders on a timely basis and recognize revenue. Also any increase in transportation costs may deter our customers and lead them to source products from other nearby suppliers, thus negatively affecting our sales.

Potential environmental liability could have a material adverse effect on our operations and financial condition.

To the knowledge of management, we have complied with the prescribed standard of environment protection as evidenced by a certificate issued by the government. Although it has not been alleged by government officials that we have violated any current environmental regulations, we cannot assure that the government will not amend the current environmental protection laws and regulations. Our business and operating results may be materially and adversely affected if we were to be held liable for violating existing environmental regulations or if we were to increase expenditures to comply with environmental regulations affecting our operations.

Inadequate funding for our capital expenditure may affect our growth strategy and profitability.

Our continued growth depends upon our ability to raise capital from outside sources. To maintain our profitability, we should increase the efficiency and achieve economies of scale in production of those low-margin products, and at the same time to develop those high-margin profit products. Adequate funding is needed to expand the production scale or develop new products. However, adequate funding is dependent upon a number of factors, including but without limitation the nation’s or the world’s economy, our business condition, the financial environment as well as the relevant legal environment. If we are unable to obtain sufficient financing, our growth and profitability may be adversely limited.

The sales price fluctuation for our products is periodic, which could affect on our financial results.

The prices of our products vary seasonably, among others, by the change of soybean supply and demand. Usually, our prices are lowest during the soybean harvest time between October and December and on the peak from January to February because of the New Year and Spring Festival. However, the price also subject to other conditions. As a result, we believe that period-to-period comparisons of our historical results of businesses are not necessarily meaningful and that you should not rely on them as an indication for future performance. It is also possible that our quarterly results of operations may be below the expectations of public market analysts and investors.

Risks Related To Our Management and Internal Control

It will probably cost us a long time to establish adequate management and internal controls. As a result, there may be some operation risks with respect to our business management.

We are constantly striving to establish and improve our business management and internal accounting control to forecast, budget and allocate our funds. However, as a Chinese company that has just become a US public company, it is difficult for us to hire and retain a sufficient number of qualified employees of management and internal control in a short period. It will also probably take us a long time to educate our employees about the internal control. As a result, we may experience difficulty in collecting financial data and preparing financial statements, books of account and corporate records, and instituting business practices that meet international standards in a short period.

We depend on key personnel for our business operations, whose discontinuance could incur our high replacement cost.

Our future success depends substantially on the continued services of our executive officers, especially Mr. Shulin Liu, our chairman and chief executive officer, Mr. Zhongtai Guo, chief operating officer, and Mr. Shaocheng Xu, chief financial officer. If one or more of our key executive officers are unable or unwilling to continue in their present positions, we may not be able to replace them readily, if at all. Therefore, our business may be severely disrupted, and we may incur additional expenses and take additional time to recruit and retain new officers.

We may not be able to effectively protect our proprietary rights, which could harm our business and competitive position.

Our success depends, in part, on our ability to protect our proprietary rights. At present, we have registered the trademarks for “Yanglin” logo in China which are currently used for all our products. We cannot assure you that we will be able to effectively protect our trademarks in the future. Currently, implementation of PRC intellectual property-related laws has historically been lacking, primarily because of ambiguities in the PRC laws and difficulties in enforcement. Accordingly, intellectual property rights and confidentiality protections in the PRC may not be as effective as in the United States or other developed countries. Policing unauthorized use of proprietary technology is difficult and expensive, and we might need to resort to litigation to enforce our rights or defend us, or to determine the enforceability, scope and validity of our proprietary rights or those of others. Such litigation may require significant expenditure of cash and management efforts and could harm our business, financial condition and results of operations. An adverse determination in any such litigation will impair our intellectual property rights and may harm our business, competitive position, business prospects and reputation.

We may be exposed to intellectual property infringement and other claims by third parties, which, if successful, could cause us to pay significant damage awards and incur other costs.

While we believe that the technology we use is not protected by any patent or intellectual property rights, we face the risk of being the subject of intellectual property infringement claims. The validity and scope of claims relating to the manufacturing of soybean products may involve complex technical, legal and factual questions and analysis and, therefore, may be highly uncertain. The defense and prosecution of intellectual property suits, patent opposition proceedings and related legal and administrative proceedings can be both costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. An adverse determination in any such litigation or proceedings to which we may become a party could subject us to significant liability, including damage awards to third parties, require us to seek licenses from third parties, to pay ongoing royalties, or to redesign our products or subject us to injunctions preventing the manufacture and sale of our products. Protracted litigation could also result in our customers or potential customers deferring or limiting their purchase or use of our products until resolution of such litigation. Further, we do not have adequate product liability insurance coverage against defective products as our products are manufactured according to fairly basic formulas. Any disputes so far have been resolved through friendly negotiations. There is no guarantee that we will not be involved in any legal proceedings should such negotiations fail one day.

Risks Related to Our Expansion

We give no assurances that any plans for future expansion will be implemented or that they will be successful.

While we have expansion plans, which include manufacturing “deep-processed” and refined soybean products, expanding our production lines and expanding our sales, there is no guarantee that such plans will be implemented or that they will be successful. These plans are subject to, among other things, the feasibility to meet the challenges we face, our ability to arrange for sufficient funding for more manufacturing facilities and the increasing working capital and the ability to hire qualified and capable employees to carry out these expansion plans.

Our personnel may not effectively support our growth and therefore impeding the expansion plan.

We currently have sufficient experienced and skilled employees for our business operations. But if our business and markets grow and develop, it will be necessary for us to expand our operation in an orderly fashion, which will put added pressure on our management and operational infrastructure. We may not have the requisite experience to manage and operate a larger, more modern manufacturing plant and bigger production lines. In addition, we may face challenges in product offerings and in integrating acquired businesses. These events would increase demands on our existing management, workforce and facilities. Failure to satisfy these increased demands could interrupt or adversely affect our operations and cause production backlogs, longer product development time frames and administrative inefficiencies.

We may not able to increase our sources for soybean supply. As a result, we may not support our plan to increase production.

In order to increase our raw material supplies, we intend to expand our soybean supply area through development of additional farmland soybean agreements, which in turn will be accomplished through contract negotiations with private farmers and cooperation with state-owned farms. However, it is difficult to obtain access to farmlands from private farmers or state-owned farms. If we cannot expand the soybean supply area, we may not be able to increase the supplies of the soybean and our plan to increase soybean production.

We may have difficulty to expand our sales network in domestic market or to explore new overseas market.

We intend to intensify our marketing efforts in the PRC by expanding existing sales and marketing network coverage to reach more areas by establishing more sales offices within the PRC and maybe in other countries such as Singapore, Malaysia, Canada and the United States. However, overseas consumers may not accept the value of non-generically modified soybean products and would not like to pay the premium of it. It also may be difficult to expand the sales channels in China’s markets if we are unable to advertise our products through various forms of media. But the advertising in commercial magazines, popular newspapers or over the internet will enhance our sales costs.

Our acquisition plan may not succeed, which will adversely affect our overall expansion plan.

We plan to expand our production facilities through the acquisition of approximately 3 to 4 additional factories, which can increase our current annual soybean production capacity up to about 1.5 million tons of soybeans over the next 3 years. However, it will be difficult for us to negotiate the acquisition with those factories, who may bargain for higher acquiring prices. Additionally, the acquisition will be submitted to the government for approval. That process may increase the risk of the acquisition failure or increase our acquisition cost, which decreases the value of the acquisition. If our acquisition fails, it will block our overall expansion plan.

Risks Related To Our Industry

China’s commitments to the World Trade Organization may intensify competition.

In connection with its accession to the World Trade Organization, China made many commitments including opening its markets to foreign products, allowing foreign companies to conduct distribution business and reducing customs duties. Foreign manufacturers may begin to manufacture non-genetically modified soybean products and ship their products or establish manufacturing facilities in China. Competition from foreign companies may reduce profit margins and hence our business results would suffer.

If the substitute products for soybean oil increase, we may lose our market share of soybean oil market.

Substitute products for soybean oil, such as vegetable oil of peanut and palm oil could increase the intensity of competition faced by us. With the appearance of substitute products for soybean oil, consumers have more choices. Part of consumers may prefer vegetable oil. As a result, we may lose our market share of soybean oil market.

If we are not be able to maintain competitive in non-genetically modified soybean product business, we may not achieve sufficient product revenues.

At present, we are the largest and most integrated private non-genetically modified soybean producer in China. Our products compete with a multitude of products developed, manufactured and marketed by others and we expect competition from new market entrants in the future. Our current competitors are the other domestic non-genetically modified soybean companies and global manufacturers who may enter the non-genetically modified soybean business. Although currently we view ourselves in a favorable position, we may not remain competitive if existing or future competing products may provide better quality, greater utility, lower cost or other benefits from their intended uses than our products, or may offer comparable performance at lower cost. If our products fail to capture and maintain market share, we may not achieve sufficient product revenues, and our business would suffer.

The inability of the PRC government to keep the PRC a genetically modified-free soybean zone will remove our competitive edge and negatively impact our operations.

We distinguish ourselves from our competitors in that we manufacture and sell non-genetically modified soybean products. Because the PRC is a non-genetically modified soybean growing zone, our competitors are not the large, better capitalized producers of genetically modified soybean products. The PRC has one of the strictest bio-safety regulations in the world, requiring safety certificates and labeling of genetically modified products. However, with so much genetically modified soybeans being imported into the country, there is a question as to whether the PRC is able to keep it a genetically modified-free soybean zone. If the PRC is unsuccessful in keeping the PRC a genetically modified-free soybean zone and our soybeans are tainted through pollination, we will lose our competition edge and this would adversely affect our operations.

Our failure to comply with ongoing governmental regulations could hurt our operations and reduce our market share.

In China, the food industry is undergoing increasing regulations as environmental awareness increases in China. The trend is that the Chinese government toughens its regulations and penalties for violations of environmental regulations. New regulatory actions are constantly changing our industry. Although we believe we have complied with applicable government regulations, there is no assurance that we will be able to do so in the future.

Risks Related To Doing Business In China

We face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the PRC and the profitability of such business.

All of our business operations are conducted in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. The Chinese economy differs from the economies of most developed countries in many respects, including level of government involvement in economic activities, stage of national development, and control of foreign exchange.

While the Chinese economy has grown significantly in the past 20 years, the growth has been uneven, both geographically and among various sectors of the economy. Policies of the PRC government can have significant effects on the economic conditions of the PRC. The PRC government has confirmed that economic development will follow the model of a market economy. Under this direction, we believe that the PRC will continue to strengthen its economic and trading relationships with foreign countries and business development in the PRC will follow market forces. While we believe that this trend will continue, we cannot assure you that this will be the case. A change in policies by the PRC government could adversely affect our interests by, among other factors: changes in laws, regulations or the interpretation of laws and regulations, confiscatory taxation, restrictions on currency conversion, imports or sources of supplies, or the expropriation or nationalization of private enterprises. Although the PRC government has been pursuing economic reform policies for more than two decades, we cannot assure you that the government will continue to pursue such policies or that such policies may not be significantly altered, especially in the event of a change in leadership, social or political disruption, or other circumstances affecting the PRC’s political, economic and social life.

Our business is largely subject to the uncertain legal environment in China and your legal protection could be limited.

The Chinese legal system is a civil law system based on written statutes. Unlike common law systems, it is a system in which precedents set in earlier legal cases are not generally used. The overall effect of legislation enacted over the past 20 years has been to enhance the protections afforded to foreign invested enterprises in China. However, these laws, regulations and legal requirements are relatively recent and are evolving rapidly, and their interpretation and enforcement involves uncertainties. These uncertainties could limit the legal protections available to foreign investors, such as the right of foreign invested enterprises to hold licenses and permits such as requisite business licenses. In addition, all of our executive officers and our directors are residents of China, and substantially all the assets of these persons are located outside the U.S. As a result, it could be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against us or any of these persons.

The Chinese government exerts substantial influence over the manner in which we must conduct our business activities.

China only recently has permitted provincial and local economic autonomy and private economic activities. Chinese government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, import and export tariffs, environmental regulations, land use rights, property and other matters. We believe that our operations in China are in material compliance with all applicable legal and regulatory requirements. However, the central or local governments of these jurisdictions may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations. Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy, or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof, and could require us to divest ourselves of any interest we hold in Chinese properties.

Inflation in China may inhibit our activity to conduct business in China.

In recent years, the Chinese economy has experienced periods of rapid expansion and high rates of inflation. During the past ten years, the rate of inflation in China has been as high as 20.7% and as low as -2.2%. These factors have led to the adoption by Chinese government, from time to time, of various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. While inflation has been more moderate since 1995, high inflation may in the future cause Chinese government to impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China, and thereby harm the market for our products.

Restrictions on currency exchange may limit our ability to receive and use our revenues effectively.

The majority of our revenues will be settled in Renminbi and U.S. Dollars, and any future restrictions on currency exchanges may limit our ability to use revenue generated in Renminbi to fund any future business activities outside China or to make dividend or other payments in U.S. dollars. Although the Chinese government introduced regulations in 1996 to allow greater convertibility of the Renminbi for current account transactions, significant restrictions still remain, including primarily the restriction that foreign-invested enterprises may only buy, sell or remit foreign currencies after providing valid commercial documents at those banks in China authorized to conduct foreign exchange business. In addition, conversion of Renminbi for capital account items, including direct investment and loans, is subject to governmental approval in China, and companies are required to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the Chinese regulatory authorities will not impose more stringent restrictions on the convertibility of the Renminbi.

The fluctuation of the Renminbi may materially and adversely affect your investment.

The value of our common stock will be affected by the foreign exchange rate between U.S. dollars and Renminbi, and between those currencies and other currencies in which our sales may be denominated. For example, to the extent that we need to convert U.S. dollars into Renminbi for our operational needs and should the Renminbi appreciate against the U.S. dollar at that time, our financial position, the business of the company, and the price of our common stock may be harmed. If we decide to convert our Renminbi into U.S. dollars for the purpose of declaring dividends on our common stock or for other business purposes and the U.S. dollar appreciates against the Renminbi, the U.S. dollar equivalent of our earnings from our subsidiaries in China would be reduced.

We may not be able to distribute our assets upon liquidation.

Our assets are predominately located inside China. Under the laws governing foreign investment enterprises in China, dividend distribution and liquidation are allowed but subject to special procedures under the relevant laws and rules. Any dividend payment will be subject to the decision of the board of directors and subject to foreign exchange rules governing such repatriation. Any liquidation is subject to both the relevant government agency’s approval and supervision as well the foreign exchange control. This may generate additional risk for our investors in case of liquidation.

We may be treated as a resident enterprise for PRC tax purposes after the Enterprise Income Tax Law becomes effective on January 1, 2008, which may subject us to PRC income tax for any dividends we receive from our subsidiaries and PRC income tax withholding for any dividends we pay to our non-PRC shareholders.

The Enterprise Income Tax Law provides that enterprises established outside of China whose “de facto management bodies” are located in China are considered “resident enterprises” and will generally be subject to the uniform 25.0% enterprise income tax rate as to their global income, including income we receive from our subsidiaries. The term “de facto management bodies” is not defined under the Enterprise Income Tax Law and it is currently unclear in which situations a non-PRC enterprise’s “de facto management body” is located in China. All of our management is currently based in China, and if a majority of the members of our management team continue to be located in China after the effective date of the Enterprise Income Tax Law, we may be considered a PRC resident enterprise and therefore subject to PRC enterprise income tax at the rate of 25% on our worldwide income, which will include any dividend income we receive from our subsidiaries. If we are required under the Enterprise Income Tax Law to pay income tax for any dividends we receive from our subsidiaries, our revenues could decrease significantly.

We have limited business insurance coverage in China, which could harm our business.

We are exposed to many risks, including equipment failures, natural disasters, industrial accidents, power outages, and other business interruptions. We do not carry business interruption insurance and as a result, we may be required to pay for financial and other losses, damages and liabilities, including those caused by natural disasters and other events beyond our control, out of our own funds, which could have a material adverse effect on our business, financial condition and results of operations.

Any future outbreak of severe acute respiratory syndrome or avian influenza in China, or similar adverse public health developments, may severely disrupt our business and operations.

A renewed outbreak of severe acute respiratory syndrome, the Avian Flu or another widespread public health problem in China, where all of our manufacturing facilities are located and where all of our revenues are derived from, could have a negative effect on our operations. In addition, there have been confirmed human cases of avian influenza in PRC, Vietnam, Iraq, Thailand, Indonesia, Turkey, Cambodia and other countries which have proven fatal in some instances. If such an outbreak or any other similar epidemic were to spread in China, where our operations are located, it may adversely affect our business and operating results. Such an outbreak could have an impact on our operations as a result of quarantines or closures of our manufacturing facilities or the retail outlets, which would severely disrupt our operations, the sickness or death of our key officers and employees, and a general slowdown in the Chinese economy.

Risks Related To The Market For Our Stock

Our Common Stocks subject to price volatility and may result in losses for investors.

The stock market has experienced significant price and volume fluctuations that have particularly affected the trading prices of equity securities of many companies that have business operations exclusively in China. These fluctuations have often been unrelated or disproportionate to the operating performance of many of these companies. Any negative change in the public’s perception of these companies could decrease our stock price regardless of our operating results. The market price of our common stock has been and may continue to be volatile. We expect our stock price to be subject to fluctuations as a result of a variety of factors, including factors beyond our control.

These factors include without limitation actual or anticipated variations in our quarterly operating results, announcements of technological innovations or new products or services by us or our competitors, announcements relating to strategic relationships or acquisitions, additions or terminations of coverage of our common stock by securities analysts, statements by securities analysts regarding us or our industry, conditions or trends in the our industry, and changes in the economic performance and/or market valuations of other soybean product companies.

The prices at which our common stock trades will affect our ability to raise capital, which may have an adverse affect on our ability to fund our operations.

Our common stock may be considered to be a “penny stock” and, as such, the market for our common stock may be further limited by certain SEC rules applicable to penny stocks.