Exhibit 99.1

Vedanta Limited

TAX TRANPARENCY REPORT

2020-21

Contents

1 | Chairman’s Value Statement | 3 | ||||

2 | Economic Responsibility | 7 | ||||

3 | Tax Governance and Strategy | 11 | ||||

• Substance, Transparency and Arm’s Length Principle | 11 | |||||

• Tax Risk Management | 11 | |||||

• Dynamic Tax Environment | 11 | |||||

• Relationship with Tax Authorities and Dispute Resolution | 11 | |||||

4 | Our Contribution to Exchequer in FY 20-21 | 14 | ||||

5 | Basis of Preparation | 21 | ||||

6 | Independent Reasonable Assurance Report | 23 | ||||

7 | Annexures | 25 | ||||

2

CHAIRMAN’S VALUE STATEMENT

“The year bygone has been unusual for all of us. There has been a paradigm shift in the way we live and conduct our business and Vedanta was no different. While we had our fair share of unprecedented challenges, we were quick to rise to the occasion and adapt to the new world and extend our humble support to the nation in its growth and recovery against Covid-19 by way of economic and social contribution.

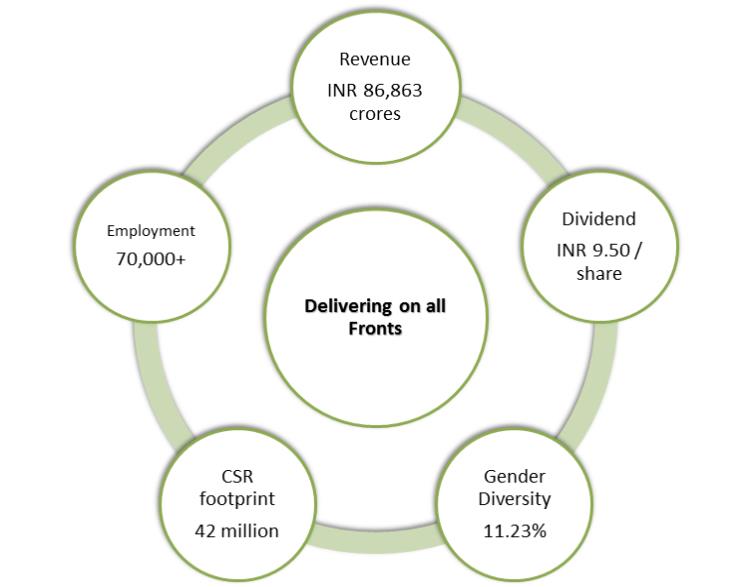

In continuity to our past performance, and commitment to building on transparency, we proudly present our sixth Tax transparency Report. During the FY 2020-21 our contribution to exchequer was INR 34,562 crores which accounts for 40% of our consolidated turnover.

At Vedanta, we are cognizant of the immense growth potential and will invest in opportunities that create value for all stakeholders. As we power ahead, we stand in solidarity with India, it’s ambition of being Aatmanirbhar and creating a 5 trillion-dollar economy.

Anil Agarwal,

Chairman, Vedanta Limited

3

ABOUT THE REPORT

Vedanta Limited is one of the world’s foremost natural resources conglomerates with primary interests in zinc-lead-silver, iron ore, steel, copper, power, oil and gas. With world-class, low-cost, long-life strategic assets based in India and Africa, we are rightly positioned to create long-term value with superior cash flows. We cater to diverse consumer markets for their primary material needs and are leaders in the segment we operate. Through our activities that generate economic, human and social value, we responsibly support India in its journey towards self- reliance.

We have a long standing commitment to transparency and are proud of the value we generate and how this contributes to building trust with the communities in which we operate. Vedanta has been working incessantly towards excellence in conjunction with the various stakeholders and with a vision to deliver value, while operating sustainably. The same is demonstrated in our vision, objectives, actions and achievements.

Operating responsibly and ethically is an integral part of Vedanta’s core values. We are fully committed to working with integrity and have upheld ‘uncompromising business ethics’. Our core values define our behavior and operations.

This Tax transparency Report is a voluntary initiative to ensure proactive transparency in tax reporting and greater accountability towards stakeholders which helps in getting detailed information about the overall economic contribution of Vedanta to the Government of countries where we operate.

At Vedanta, we undertake our business with a strict adherence to ethical management and responsible operations, and constantly strive to go beyond compliance to create positive impact.

4

|

Aligned to our Group objective of “Zero Harm, Zero Waste and Zero Discharge” | |

| Committed to be the lowest cost producer in a sustainable manner. Sustained operations with zero import of coal in 2021 through coal substitution scheme of Gol | |

| Delivered industry leading operational margins of 39% and exceptional quarters for key businesses | |

| Pledged INR 150 crores to support India in its fight against the second wave of Covid 19 | |

| INR 2,74,000 crores contribution to the national exchequer in the past 10 years | |

| AA- Credit ratings Crisil and India

| |

5

6

ECONOMIC RESPONSIBILITY

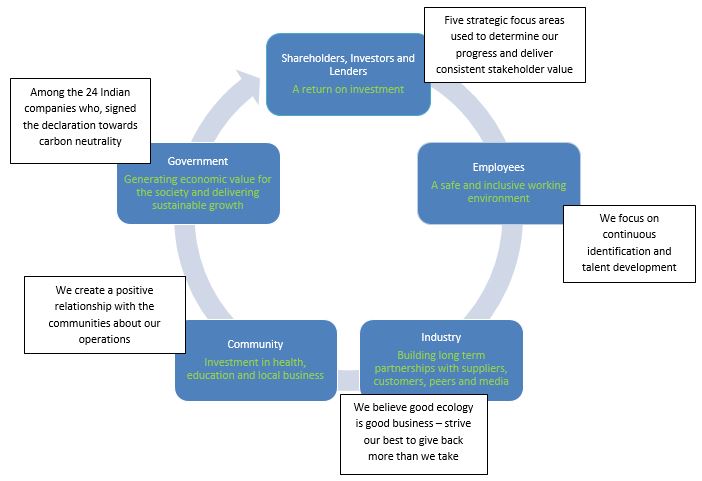

As one of the world’s leading diversified natural resource companies with business operations in multiple geographies spanning continents, we are mindful of our commitments to society, our people and the environment.

At Vedanta, our sustainability-focused and integrated business model continues to propel our value-creation process. Operating responsibly and ethically is an integral part of Vedanta’s core values which help us to deliver on our commitments to all internal and external stakeholders. Our long-term focus is reflected in our key strategic pillars that ingrains ESG as a core facet of business viability. We believe that large-scale environment conservation and community empowerment make our business intrinsically strong and future ready.

We have also extended our support to the nation’s fight against the Covid -1 9 pandemic through contributions to the PM CARES fund and undertaking initiatives that positively impact the lives of more than 15 lakh people.

Giving back is in the DNA of Vedanta, which is focused on enhancing the lives of local communities. Retaining the social license to operate is central to our ability to do business as Vedanta is the primary economic driver in most of the geographies where we operate in. The Chairman has signed the Giving Pledge, a movement of global philanthropists who commit to giving the majority of their wealth to philanthropy or charitable causes.

In line with the past trends, we are proud to declare that we have contributed INR 34,562 crores to the public exchequer of the various countries where we operate. The total contribution to exchequer is the result of value addition by various business segments across their respective value chain and multiple hierarchies of business cycle.

At Vedanta, our sustainability-focused and integrated business model continues to propel our value-creation process, helping deliver better returns for all stakeholders along its value chain.

7

8

Awards and Recognition

| 1. | Dow Jones Sustainability Index - Ranked 2nd in Asia-Pacific region and 12th Globally in Metal and Mining sector |

| 2. | Featured in The Sustainability Yearbook 2020 by S & P Global and RobecoSAM as Sustainability Leaders |

| 3. | FTSE4Good Emerging Index- Member of FTSE4Good Emerging Index across - Environment, Social and Governance |

| 4. | CSR Health Impact Award - Women & Child Health Initiative - Conferred with the title of ‘Game Changer’ for its Khushi Anganwadi Program |

| 5. | Great Place to Work-CertifiedTM by Great Place to Work Institute |

COVID 19 initiatives

Vedanta has contributed over Rs 400 crores to help in the Nation’s fight against

Covid 19 in the form of set up of health infrastructure and oxygen supply. The

company has undertaken one of the largest vaccination drives to ensure 100

per cent coverage of our employees, families and business partners.

| 2300+ Nand Ghars created for social | Disposed 100% of fly | |

| welfare | ash generated, utilized 92% of lime grit |

Anil Agarwal Foundation

Under the aegis of Anil Agarwal Foundation, Vedanta has pledged Rs 5,000

crores over the next five years on social impact programmes focused on nutrition,

women and child development, healthcare, animal welfare and grassroot level.The company has

also announced a `Swasth Gaon Abhiyaan’ which will

strengthen end-to-end healthcare services across 1,000 villages in 12 states,

impacting more than 20 lakh people

9

| Amounts in ₹ Crores | ||||

Direct Economic Value Generated | 94,090 | |||

Economic Value Distributed (70,296): |

| |||

Operating Costs (Payments made to our suppliers for the purchase of utilities, goods and services) | 54,625 | |||

Payment to Government (CIT and Profit Petroleum) | 3,612 | |||

Employee Wages and Benefits (Employee expenses for salary, wages and incentives) | 2,861 | |||

Payments to Providers of Funds (● Dividend payments ● Interest payments) | 8,867 | |||

Community Investments Voluntary donations | 331 | |||

Direct Economic Value Retained | 23,794 | |||

10

TAX GOVERNANCE AND STRATEGY

Substance, Transparency and Arm’s length Principle

Transparency is our core value as we firmly believe in long term sustainable value creation for our multiple-stakeholders including the government and society at large. We remain at the forefront of tax reporting by managing our tax affairs in a succinct and straightforward manner.

We understand ‘substance’ as economically owning an asset and actively taking and executing decisions that entail management of risks associated to any taxable result. All transactions have a commercial and business reason and we adhere to the arm’s length principle.

Tax Risk Management

In line with our tax governance model of being tax transparent, we maintain internal controls in the form of compliance calendars, internal audit process by MAS (Management Assurance Services) teams, authorization matrix under maker-checker concept. These systems, processes and controls enable the Group to fulfill its tax compliance obligations and mitigate associated risks.

The Group strives to ensure that commercial transactions are structured in tax-efficient ways where credible technical analysis and interpretation is available. In particular, we ensure that such transactions should be in full compliance with the law. We claim tax incentives and exemptions as legitimately available in the countries where we operate.

Material tax risks or disputes are reported to the Audit Committee for its consideration. This review includes assessment of probabilities of different outcomes, cash flow and reputational impact. The Audit Committee then updates the Board.

Dynamic Tax Environment

We strive to strengthen our systems, processes, group structures, transactions etc. to comply with changing tax laws across the globe. Classic example of this was the advent of Goods & Services Tax (‘GST’) in India where majority of business operations of the group are located. In a bid to increase transparency in tax matters ‘faceless assessment’ got introduced in India. Vedanta team has systems and standard protocols inherently imbibed and was able to handle this transition without any disruptions.

Relationship with Tax Authorities and dispute resolution

We maintain an open, honest, transparent and constructive relationship in all our dealings with the tax authorities in the jurisdictions in which we operate. Our dealings are based on mutual trust in line with Vedanta’s Code of Business Conduct and Ethics.

We actively participate in the tax authority’s formal consultation processes on matters having material impact on the Group. We work with Industry chambers wherever possible to contribute in development of tax laws and attendant policies.

All dispute resolution mechanisms including arbitration, conciliation and mechanisms available under various Double Taxation Avoidance Agreements are appropriately evaluated including resolution by engaging with the Government through industry groups or forums.

For strategic and critical transactions, the Group proactively evaluates dispute avoidance mechanisms and has applied for advance pricing agreements wherever feasible

11

Our Code of Business Conduct and Ethics, which applies to all employees, sets out our zero tolerance on corruption and bribery. Vedanta requires its employees, tax advisors and suppliers of tax services to act with integrity and maintain high ethical standards in all tax activities.

Vedanta has also formed an internal ‘Tax Council’ which acts as an overarching governing body to the tax function as a whole. The Tax Council operates with a mix of experienced professionals internally drawn from Tax and Finance, and externally drawing on senior lawyers, retired Bureaucrats and independent tax practitioners. The Council addresses issues relating to both direct and indirect tax. The body plays a vital role in ensuring that all the businesses across the group duly comply with the risk governance framework and tax strategy of the group. It conducts periodical reviews, provides guidance and advises with respect to tax compliance, tax litigation and other related matters which ensures adequate transparency and consistency.

The tax strategy is owned and approved by the company’s Board. It is subject to annual review by the Board whereas an annual compliance report is submitted to the Board & Audit Committee. The Group Chief Financial Officer holds the responsibility for tax at the Board level and communicates with and advises the Board on the tax affairs and risks of the Group with support from the Group’s Corporate tax team. Responsibility for tax governance rests with the tax function, in consultation with the Chief Financial Officer/Financial Controller.

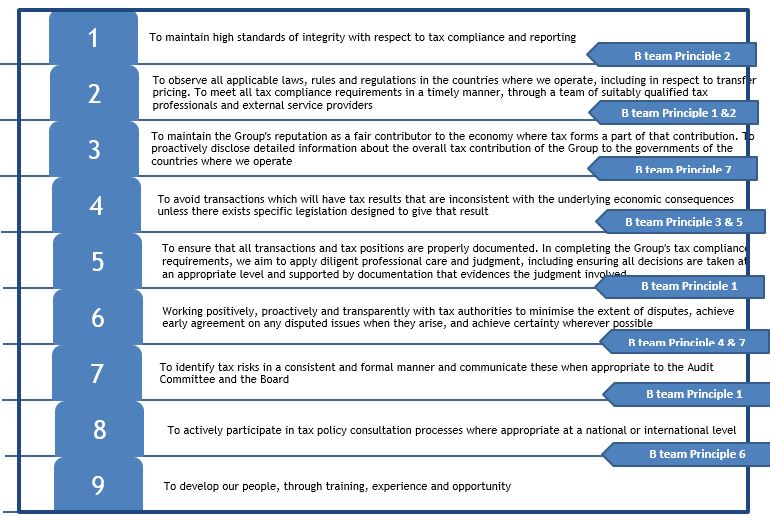

Further to providing guidance to our approach to tax, we have documented a group tax strategy statement which also complies with the requirements of the UK tax strategy legislation. Our tax principles have inherently endorsed the concepts of accountability, compliance, transparency, business jurisprudence, etc. It reflects in essence the new bar of (seven) tax principles detailed by B Team1 aimed at setting best practices.

| 1 | A movement initiated by business and civil society leaders for concerted positive action to ensure business becomes a driving force for social, environmental and economic benefit |

12

GUIDING TAX PRINCIPLES:

13

OUR CONTRIBUTION TO EXCHEQUER IN FY 2020-21

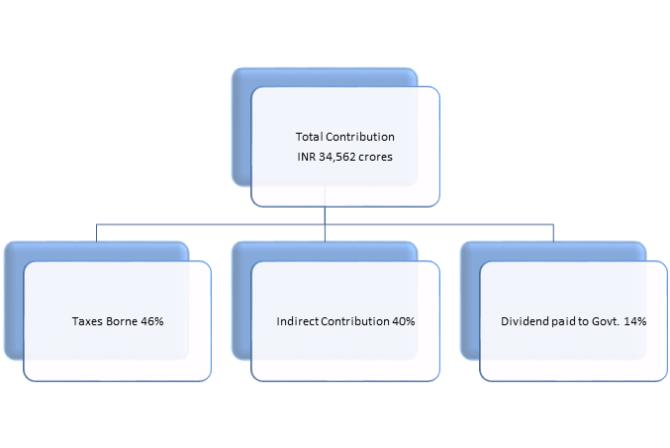

Vedanta contributed INR 34,562 crores, around 40% of its turnover to the exchequer through a wide range of contributions in the nature of Corporate Income taxes, royalties, profit-oil, through significant indirect revenue contributions by way of withholding taxes and Indirect taxes. With this edition, the Company is publishing its sixth Tax transparency Report.

The total contribution to the exchequer comprises of the following –

14

15

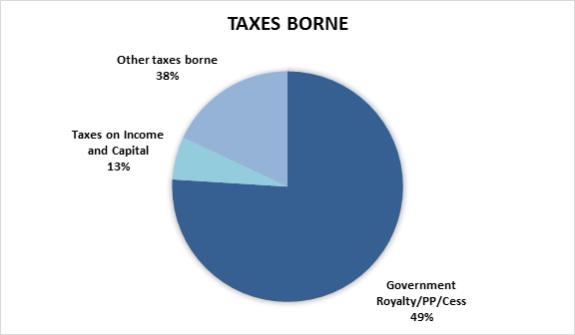

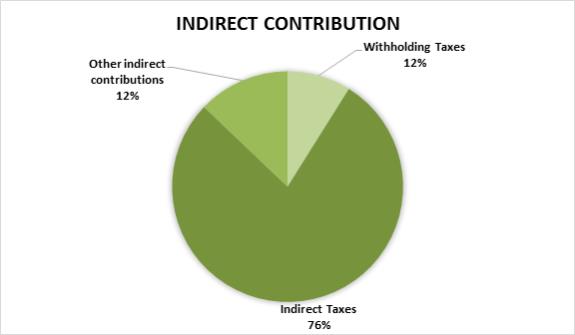

For the purpose of preparation of this table, we have shown the tax contributions under two broad categories of taxes i.e. Taxes borne and Indirect Contributions.

| • | Taxes borne primarily comprise Corporate income tax, royalty related tax payments, production entitlements i.e. profit oil and other material payments made to the Government such as production based Oil Cess, Stamp Duty Payments, Levies on Import/Export, Local Municipal taxes, etc. |

| • | Indirect Contributions primarily comprise of taxes collected and paid on behalf of our employees and vendors i.e. withholding taxes, payroll taxes (professional taxes), payments of value added taxes on sales and other Social Security Contributions to fund the Social Security program of the governments for the employees etc. |

Government Royalty, Profit Petroleum & Oil Cess - 49% - ₹ 7,880 crores

Government Royalties and oil cess – ₹ 5,044 Crores

We pay royalties to the state governments of Chhattisgarh, Rajasthan, Andhra Pradesh, Goa and Karnataka in India based on extraction of bauxite, lead-zinc, silver, iron ore, Crude oil and natural gas. The most significant of these is the royalty that HZL is required to pay to the state government of Rajasthan, where all of HZL’s mines are located.

We also pay cess to the GoI (Government of India) . Generally in respect of oil and gas operations, royalty and cess payments are made by the joint operation partners in proportion to their participating interest.

Profit Petroleum- ₹ 2,836 Crores

The GoI is the owner of the hydrocarbons wherein it has assigned the responsibility to the joint operation (Contractor) to explore, develop and produce the hydrocarbons. Contractor is entitled to recover out of Petroleum produced, all the costs incurred according to the Production Sharing Contracts in exploring, developing and producing the hydrocarbons, which is known as “Cost Petroleum”. Excess of revenue (value of hydrocarbons produced) over and above the cost incurred as above, is called “Profit Petroleum”, which is shared between the GoI and Contractor Parties as per procedure laid down in Production Sharing Contracts.

Taxes on Income and capital – 13% -₹ 2,097 crores

Profits of companies in India are subject to either regular income tax or Minimum Alternate Tax (“MAT”), whichever is greater. Regular Income tax on Indian companies is charged at a statutory rate of 30.0% plus a surcharge of 12.0% on the tax and has an additional health and education cess of 4.0% on the tax including surcharge, which results in an effective statutory tax rate of 34.944%.

The effective MAT rate during the year for Indian companies was 17.47% . The excess of amounts paid as MAT over the regular income tax amount during the year may be carried forward and applied towards regular income taxes payable in any of the succeeding fifteen years subject to certain conditions.

16

Other taxes borne - 38% - ₹ 6,040 crores

Indirect Taxes -76% -₹ 10,500 crores

GST is a supply driven concept and would therefore apply on supply of goods and services.

Taxes under GST apply as follows:

| • | Central goods and service tax and state goods and services tax are simultaneously levied on intra-state supply of goods and services. |

| • | Integrated goods and service tax are levied on imports and inter-state supply of goods and services. |

| • | In addition, GST compensation cess also applies on certain specified goods and services. The general rate of GST on our output supplies is 18.0%. However, supply of iron ore attracts GST at the rate of 5.0%, whereas silver attracts GST at 3.0%. |

Withholding taxes – 12% ₹ 1,622 crores

This comprises of the following –

| • | Payroll & Employer Taxes payable as a result of a company’s capacity as an employer. |

| • | payroll and employee taxes withheld from employee remuneration and are paid to governments on behalf of employees. |

17

| • | Other taxes collected/deducted |

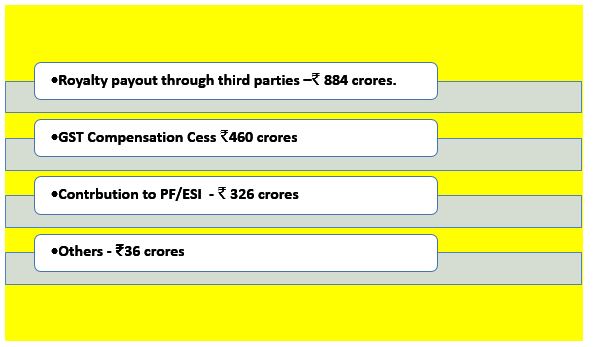

Other indirect contributions – 12% ₹ 1,706 crores

This comprises of the following taxes –

18

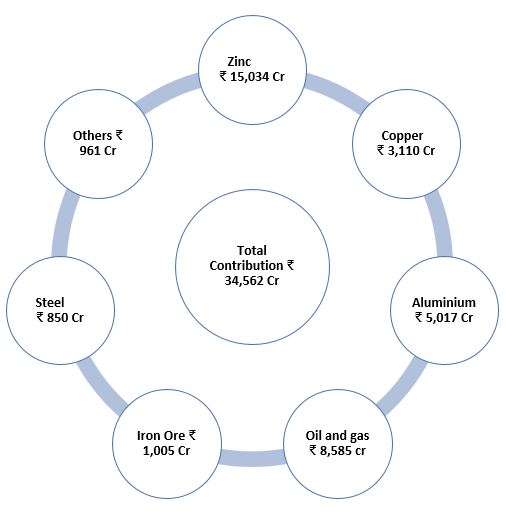

BUSINESS SPREAD OF CONTRIBUTION TO EXCHEQUER. (Highest contribution – Zinc 43%)

19

The below Table-1 details the country wise amounts of revenue, Profit before tax (PBT) Global Tax and Other Contributions by the Company to exchequer in FY 2020-2021

All amounts are in ₹ Crore

Country | Revenue (External) | Profit Before Tax (PBT) | Taxes Borne | Indirect Revenue Contributions | Dividend paid to Govt. | Contribution to exchequer | ||||||||||||||||||||||||||||||||||||||||||

| Taxes on Income and Capital | Government Royalties & Profit Oil | Others | Total Payments Borne | Withholding Taxes | Indirect Taxes | Others | Total | |||||||||||||||||||||||||||||||||||||||||

| A | B | C | I=A+B+C | D | E | F | II=D+E+F | III | I+II+III | |||||||||||||||||||||||||||||||||||||||

India | 77,993 | 27,529 | 2,058 | 7,871 | 6,025 | 15,954 | 1,534 | 10,500 | 1,673 | 13,707 | 4,717 | 34,378 | ||||||||||||||||||||||||||||||||||||

South Africa | 2,699 | 729 | 37 | 8 | 2 | 47 | 68 | — | 10 | 78 | — | 125 | ||||||||||||||||||||||||||||||||||||

Namibia | 30 | (45 | ) | 0 | 1 | 0 | 1 | 15 | — | 1 | 16 | — | 17 | |||||||||||||||||||||||||||||||||||

Others* | 6,141 | (11,000 | ) | 2 | 0 | 13 | 15 | 5 | 0 | 22 | 27 | — | 42 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Total | 86,863 | 17,213 | 2,097 | 7,880 | 6,040 | 16,017 | 1,622 | 10,500 | 1,706 | 13,828 | 4,717 | 34,562 | ||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

| * | This includes contribution for Australia, Japan, South Korea, UAE, Ireland, Mauritius, Netherlands, Taiwan and Liberia. |

20

BASIS OF PREPARATION

Note 1

Amounts reported in the above table have been subject to external assurance. Assurance Report forms a part of this report. The financial information it contains is consistent with that used to prepare our FY 2020-21 consolidated financial statements and financial statements of the Group’s listed/non-listed operating subsidiary companies. In case of joint venture operations, contributions are shown at gross level as made by the Unincorporated Joint Venture (UJV) of which the Company’s subsidiary is the operator irrespective of our percentage interest in the UJV.

Note 2

All data is prepared for the year from 1 April 2020 to 31 March 2021. The above contributions have been reported on a cash basis. The social expenditures have not been considered in the contribution to exchequer shown in the above table.

Note 3

Vedanta has disclosed in taxes borne in table above, the taxes charged by suppliers/ service providers in their invoices and paid by the Group to the extent not creditable. Indirect contributions shown in the table above inter-alia include royalty and cess paid through third parties, and these collectively represent gross output liabilities discharged by the Group.

Note 4

TAXES BORNE

| A) | Taxes on Income and Capital |

This comprises Corporate Income Tax but does not include Deferred Tax, Interest and Penalty, if any. These taxes are provided at amounts paid during the year FY 2020-21 with respect to corporate income tax liability of the same year and of previous years at respective corporate tax rates applicable for those years. Typically, these taxes would be reflected in corporate income tax returns made to governments, and tend to become payable, and are paid ((either directly by way of advance tax or self-assessment tax or through credit of withholding tax), either in the year the profits were made or up to one year later, depending on the tax laws of the respective countries as to the timing of payments.

| B) | Government Royalties and Profit Oil |

This comprises contributions made to exchequer in the form of royalties, license fees and resource rents; for example, contribution for the extraction of minerals, metals, crude oil or gas whether paid directly to the Government or through the third parties. These form part of operating costs. Profit oil represents share of profit paid to the government on account of production of crude oil and natural gas from the fields awarded by the government as per the terms of Production Sharing Contract (PSC). Typically, this is reflected in various forms/ returns prescribed by the government for this purpose. The government’s share of profit oil is accounted for when the obligation (legal or constructive) in respect to the same arises. Profit oil is netted off from revenue generated from such operations.

21

| C) | Other taxes borne |

This comprises cess paid on production of crude oil In India, stamp duty that arises on the transfer of assets or capital, levies on import/export of goods (considered on gross basis), municipal taxes, electricity duty, service tax, excise duty, GST, entry tax/octroi and other taxes borne. These form part of operating costs, except where creditable.

INDIRECT REVENUE CONTRIBUTIONS

| D) | Withholding Taxes |

This comprises payroll and employee taxes (including professional tax) withheld from employee remuneration, and paid to governments, i.e., tax collected and remitted to governments on behalf of employees. Typically, these taxes would be reflected in payroll tax returns made to exchequer and tend to be payable, and are paid, on a regular basis (often monthly) throughout the year, shortly after the submission of the returns. It also comprises taxes withheld or collected from various payments made to contractors and paid to governments, i.e., taxes collected/deducted and remitted to governments on behalf of the service providers/vendors/group companies.

| E) | Indirect Taxes |

This comprises taxes paid to the governments on procurement or production or sale of goods such as Value Added Tax (VAT)/sales tax, excise duty, central sales tax, Goods and Services Tax, etc. (considered gross basis) These taxes would not be collected if the Group had not produced and made sales to the customers.

| F) | Other |

This includes contribution of employers and employees for funding the social security programme of the government such as Provident Fund (PF) and Employee State Insurance Fund (ESI). Such contributions are reflected in the monthly and annual returns made to the respective organisations.

DIVIDENDS TO GOVERNMENT

This includes dividends paid to government wherever the government holds shares in any of the Group companies and that company has paid dividend during the year.

Please refer to Annexure 1 on types of taxes paid by Vedanta in various countries.

22

Independent Reasonable Assurance Report

To Vedanta Limited on Global Tax & Other Contribution

We were engaged by the management of Vedanta Limited [hereinafter referred to as ‘VEDL’ or ‘the Company’] to report on ‘Global Tax & Other Contributions’ – Table 1 contained in VEDL’s Tax transparency Report for the financial year 2020-21 [the said Table 1 hereinafter referred to as ‘Global Tax & Other Contributions’], in the form of an independent reasonable assurance conclusion about whether VEDL’s statement that the Global Tax & Other Contributions is properly prepared, in all material respects, based on ‘Basis of Preparation’ attached to the Tax transparency Report is fairly stated.

VEDL’s Responsibilities

The management of VEDL are responsible for preparing the Global Tax & Other Contributions that is free from material misstatement in accordance with Basis of Preparation and for the information contained therein. The management of VEDL are also responsible for preparing the Basis of Preparation.

This responsibility includes designing, implementing and maintaining internal control relevant to the preparation and presentation of Global Tax & Other Contributions that is free from material misstatement, whether due to fraud or error. It also includes developing the Basis of Preparation. The Company is also responsible for preventing and detecting fraud and for identifying and ensuring that it complies with laws and regulations applicable to its activities.

Our Responsibilities

Our responsibility is to examine the Global Tax & Other Contributions prepared by the Company and to report thereon in the form of an independent reasonable assurance conclusion based on the evidence obtained. We conducted our engagement in accordance with International Standard on Assurance Engagements (ISAE) 3000: Assurance Engagements Other Than Audits or Reviews of Historical Financial Information issued by the International Auditing and Assurance Standards Board. That standard requires that we plan and perform our procedures to obtain reasonable assurance about whether the Global Tax & Other Contributions is properly prepared, in all material respects.

The firm applies International Standard on Quality Control 1 and accordingly maintains a comprehensive system of quality control including documented policies and procedures regarding compliance with ethical requirements, professional standards and applicable legal and regulatory requirements.

We have complied with the independence and other ethical requirements of the Code of Ethics for Professional Accountants issued by the International Ethics Standards Board for Accountants, which is founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality and professional behavior.

The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of Global Tax & Other Contributions whether due to fraud or error.

23

In making those risk assessments, we have considered internal control relevant to the preparation and presentation of Global Tax & Other Contributions in order to design assurance procedures that are appropriate in the circumstances, but not for the purposes of expressing a conclusion as to the effectiveness of the Company’s internal control over the preparation and presentation of Global Tax & Other Contributions. Our engagement also included assessing the appropriateness of Global Tax & Other Contributions, the suitability of the Basis of Preparation used by the Company in preparing the Global Tax & Other Contributions in the circumstances of the engagement, evaluating the appropriateness of the procedures used in the preparation of Global Tax & Other Contributions and the reasonableness of estimates made by the Company and evaluating the overall presentation of the Global Tax & Other Contributions. Reasonable assurance is less than absolute assurance.

The procedures performed by us have been included herein as Annexure 2.

CONCLUSION

Our conclusion has been formed on the basis of, and is subject to, the matters outlined in this report. We believe that the evidence we have obtained is sufficient and appropriate to provide a basis for our conclusion. In our opinion, the Global Tax & Other Contributions is properly prepared in all material respects, based on the Basis of Preparation.

Restriction of Use of Our Report

In accordance with the terms of our engagement, this independent reasonable assurance report on Global Tax & Other Contributions has been prepared for VEDL solely for inclusion in its Tax transparency Report for 2020-21 and for no other purpose or in any other context.

Our report should not be regarded as suitable to be used or relied on by any party wishing to acquire rights against us other than VEDL for any purpose or in any context. Any party other than VEDL who obtains access to our report or a copy thereof and chooses to rely on our report (or any part thereof) will do so at its own risk. To the fullest extent permitted by law, we accept or assume no responsibility and deny any liability to any party other than VEDL for our work, for this independent reasonable assurance report, or for the conclusions we have reached.

Our report is released to VEDL on the basis that it shall not be copied, referred to or disclosed, in whole (save for inclusion in VEDL’s Tax transparency Report) or in part, without our prior written consent.

For KPMG Assurance and Consulting Services LLP

Place: Mumbai, India

Date: 04 August, 2021

24

Annexure -1 Taxes Paid

Below mentioned are the types of taxes paid by Vedanta companies:

| (1) | Corporate Income Tax |

| (2) | Government Royalties |

| (3) | Profit Oil |

| (4) | Oil Cess / NCCD |

| (5) | Duties on Export and Import |

| (6) | Other Cesses and Surcharges |

| (7) | Stamp duty |

| (8) | Municipal Taxes |

| (9) | Withholding taxes |

| (10) | Excise Duties |

| (11) | Value Added Tax |

| (12) | Service Tax |

| (13) | Goods and Service tax |

| (14) | Octroi/ Entry Tax |

| (15) | Provident Fund and Employee State Insurance |

| (16) | Land Tax/Property Tax |

| (17) | License Fees |

| (18) | Signature, Discovery & Production Bonuses |

| (19) | Electricity Taxes/Duty |

| (20) | Export License Utilization |

| (21) | Taxes paid under Amnesty Scheme (Excise Duty, Service Tax) |

| (22) | Any other taxes inter-alia Niryat Kar, Panchayat Tax, Paryavaran Tax, Upkar Tax, Inhabitant Tax, SPV |

25

Annexure 2- ASSURNACE PROCEDURES – GLOBAL TAX & OTHER CONTRIBUTIONS

| • | Understand and examine the processes and controls at Vedanta Group level in managing, collating and reviewing the data for the Global Tax & Other Contributions |

| • | Discussion over call to review the methodology of information request sent by central team and thereafter reporting of data by each department/ entity |

| • | Review the entity/ department wise break-up of the various tax and other specified items reported in the Global Tax & Other Contributions |

| • | Detailed review of tax data reported from the respective source documents on a sample basis with coverage of locations, sectors and tax types |

| • | Any queries or variances verified with respective entity/ location |

26