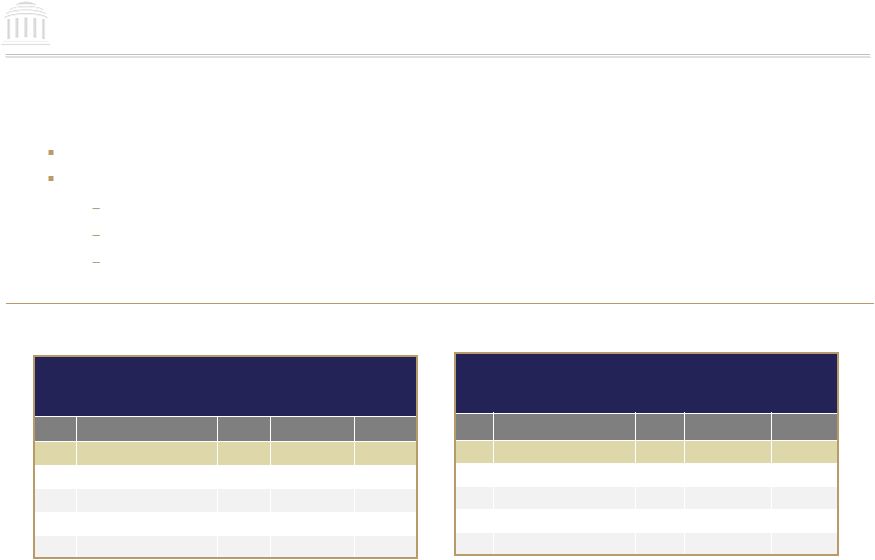

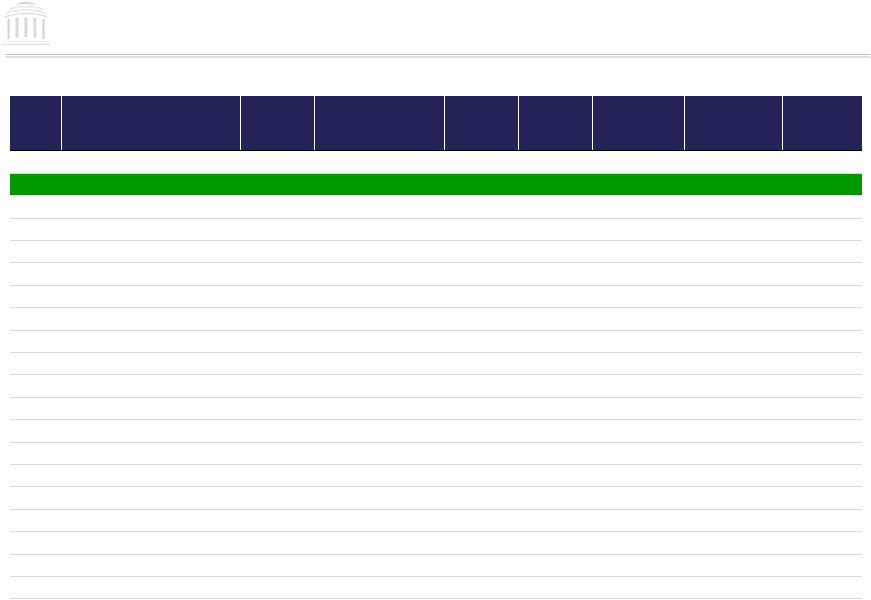

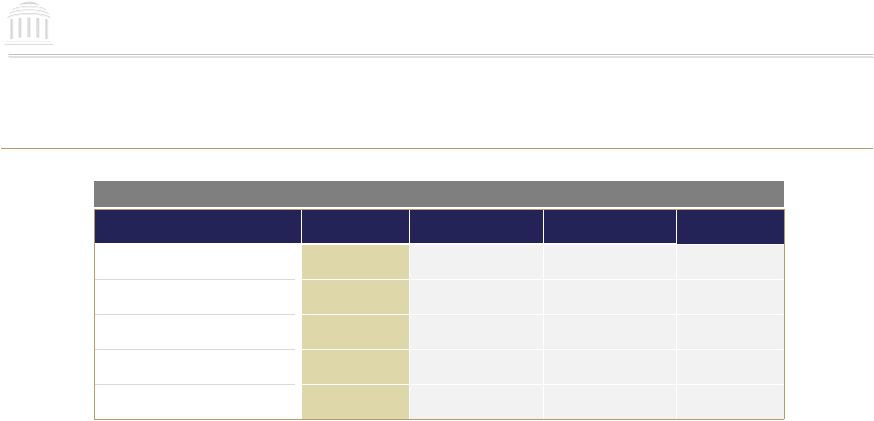

19 Source: SNL Financial. Sectors include: Banking, Insurance, Securities & Investments, Specialty Finance, Financial Technology, Real Estate, Energy and Media & Communications. 1. Overall Ranking based on percentage of outstanding shares repurchased. 2. DIRECTV market cap as of 6/30/15 due to AT&T acquisition. Overall Rank 1 Company Ticker Industry Market Cap. 7/28/15 ($ MM) Shares Out, 12/31/09 Shares Repurchased (1Q10 - 2Q15) Shares Out, 3/31/15 + Repurchases % of Shares Repurchased 1 Atlanticus Holdings Corporation ATLC Specialty Lender $55 47,717,723 34,693,349 48,680,291 71.3% 2 FBR & Co. FBRC Broker-Dealer 179 16,016,196 10,571,970 18,152,581 58.2% 3 MCG Capital Corporation MCGC Investment Company 162 76,394,000 40,764,725 77,838,842 52.4% 4 World Acceptance Corporation WRLD Specialty Lender 473 16,211,659 9,610,956 18,580,904 51.7% 5 WebMD Health Corp. WBMD New Media 1,662 50,946,766 39,042,397 76,808,359 50.8% 6 Outerwall Inc. OUTR Media & Entertainment 1,515 31,076,784 17,014,955 35,513,933 47.9% 7 Montpelier Re Holdings Ltd. MRH Insurance Underwriter 1,789 79,998,795 39,255,113 83,054,366 47.3% 8 DIRECTV 2 DTV Communications 467,642 933,187,782 449,992,796 953,973,973 47.2% 9 Anthem, Inc. ANTM Insurance Underwriter 40,848 449,789,672 225,687,546 490,593,144 46.0% 10 Validus Holdings, Ltd. VR Insurance Underwriter 3,732 128,459,478 70,287,964 153,922,879 45.7% | 20 Magellan Health, Inc. MGLN Financial Technology 1,644 34,535,000 17,699,729 45,026,104 39.3% | 50 Arch Capital Group ACGL Insurance Underwriter 8,903 164,285,034 59,048,246 183,809,087 32.1% | 100 W.R. Berkley Corporation WRB Insurance Underwriter 6,961 156,552,355 41,752,938 166,686,213 25.0% | 500 Cogent Communications Holdings, Inc. CCOI Communications 1,469 44,853,974 2,270,205 48,464,831 4.7% | 1,000 Tiptree Financial Inc. TIPT Investment Company 188 20,158,894 75,743 32,068,213 0.2% FBR RANKS #2 IN SHARE REPURCHASES AMONG MORE THAN 5,000 DOMESTIC PUBLIC COMPANIES SINCE 2010 |