UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____ to

Commission file number: 000-52192

ALPHAMETRIX MANAGED FUTURES LLC (ASPECT SERIES)

(Exact name of registrant as specified in its charter)

| Delaware | 03-0607985 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

c/o ALPHAMETRIX, LLC

181 West Madison

Suite 3825

Chicago, Illinois 60602

(Address of principal executive offices)

(312)267-8400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Units of Limited Liability Company Interest

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark if the disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer o | (Do not check if a smaller reporting company) | Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes o No ý

The units of limited liability company interest of the registrant are not publicly traded. Accordingly, there is no aggregate market value for the registrant’s outstanding equity that is readily determinable.

As of December 31, 2008, units of limited liability company interest of the registrant with an aggregate net asset value of $71,216,262 were outstanding and held by non-affiliates; units of limited liability company interest of the registrant with an aggregate net asset value of $10,911 were outstanding and held by AlphaMetrix, LLC, the sponsor of the registrant.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant’s Financial Statements and Report of Independent Registered Public Accounting Firm for the period ended December 31, 2008 are incorporated by reference into Part II, Item 8, and Part IV hereof and filed as Exhibit 13.01 herewith.

ii

ALPHAMETRIX FUTURES LLC (ASPECT SERIES)

ANNUAL REPORT FOR 2008 ON FORM 10-K

Table of Contents

| Page | ||

| PART I | ||

| Item 1. | BUSINESS | 1 |

| Item 1A. | RISK FACTORS | |

| Item 1B. | UNRESOLVED STAFF COMMENTS | |

| Item 2. | PROPERTIES | |

| Item 3. | LEGAL PROCEEDINGS | |

| Item 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | |

| PART II | ||

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | |

| Item 6. | SELECTED FINANCIAL DATA | |

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | |

| Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | |

| Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | |

| Item 9A(T). | CONTROLS AND PROCEDURES | |

| Item 9B. | OTHER INFORMATION | |

| PART III | ||

| Item 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | |

| Item 11. | EXECUTIVE COMPENSATION | |

| Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | |

| Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | |

| Item 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | |

| PART IV | ||

| Item 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | |

| SIGNATURES | S-1 | |

iii

PART I

Item 1: Business

(a) General Development of Business

The registrant AlphaMetrix Managed Futures LLC (Aspect Series) (the “Aspect Series”) is a “segregated series” of AlphaMetrix Managed Futures LLC (the “Platform”). AlphaMetrix, LLC (the “Sponsor”) acts as the sponsor for both the Aspect Series and the Platform. The Platform was formed on July 25, 2006 as a Delaware series limited liability company pursuant to the Delaware Limited Liability Company Act. The Aspect Series invests all or substantially all of its assets in AlphaMetrix Managed Futures (Aspect) LLC (the “Trading Fund”), which invests all or substantially all of its assets in AlphaMetrix Aspect Fund-MT0001 (the “Master Fund”). The Trading Fund and the Master Fund are advised by Aspect Capital Limited (the “Trading Advisor”). The Aspect Series, the Trading Fund and the Master Fund are collectively referred to herein as the “Series.” The Series engages in the speculative trading of bonds, currencies, interest rates, equities, equity indices, debt securities and selected physical commodities and derivatives. UBS Securities LLC is the Series’ futures clearing broker (the “Clearing Broker”) and UBS AG is currently the foreign exchange clearing broker of the Series, although the Series may execute foreign exchange trades through another foreign exchange clearing broker at any time. The Sponsor, over time, intends to offer investors a selection of different trading advisors, each managing a different segregated series of the Platform. There can be no assurance, however, that any series other than the Series will be offered or that the Series will continue to be offered. The Series was organized on October 26, 2006 and commenced trading on March 16, 2007. The Series filed a Form 10, under the Securities Exchange Act of 1934, as amended, with the Securities and Exchange Commission to register the units of limited liability company interest (“Units”), which registration became effective October 17, 2006.

On November 1, 2008, UBS Managed Fund Services Inc.’s (“UBS MFS” or the “former sponsor”), UBS Securities LLC and the Sponsor executed a General Assignment and Assumption Agreement that provided for the assignment of all UBS MFS’s managerial interest in the Aspect Series, the Platform and the Trading Fund to the Sponsor, subject to the consent of investors in the Aspect Series, and the Sponsor assumed control of all rights and duties as sponsor of the Aspect Series. In connection with this Assignment, the Platform and the Aspect Series changed their names as follows: the Aspect Series from UBS Managed Futures LLC (Aspect Series) to AlphaMetrix Managed Futures LLC (Aspect Series), the Platform from UBS Managed Futures LLC to Aspect Managed Futures LLC and the Trading Fund from UBS Managed Futures (Aspect) LLC to AlphaMetrix Managed Futures (Aspect) LLC. In connection with this assignment, UBS MFS redeemed its units on October 31, 2008 and on November 1, 2008, the Series issued 8.120 Units to the Sponsor for $10,000.

The Series may terminate upon the determination of the Sponsor to do so for any reason (for the avoidance of doubt, the Sponsor shall be entitled, without any violation of any contractual or fiduciary obligation to any investor in the Series (a “Member”), to dissolve the Series at any time).

(b) Financial Information about Segments

The Series’ business constitutes only one segment for financial reporting purposes, i.e. a speculative “commodity pool.” The Series does not engage in sales of goods or services. Financial information regarding the Series’ business is set forth in Item 6 “Selected Financial Data” and in the Series’ Financial Statements filed as Exhibit 13.01 herewith.

(c) Narrative Description of Business

General

The Trading Advisor manages the assets of the Series pursuant to its Aspect Diversified Program (the “Program”). The Program is a broadly diversified global trading system that deploys multiple trading strategies that seek to identify and exploit directional moves in market behavior of a broad range of global financial instruments including

1

but not limited to bonds, currencies, interest rates, equities, equity indices, debt securities and selected physical commodities and derivatives. By maintaining comparatively small exposure to any individual market, the aim is to achieve real diversification. The Program seeks to maintain positions in a variety of markets. Market concentration varies according to the strength of signals, volatility and liquidity, amongst other factors.

The Program employs a fully automated system to collect, process and analyze market data (including current and historical price data) and identify and exploit directional moves, or “trends”, in market behavior, trading across a variety of frequencies to exploit trends over a range of timescales. Positions are taken according to the aggregate signal and are adjusted to control risk.

The investment objective of the Program is to generate significant medium term capital growth independent of overall movements in traditional stock and bond markets within a rigorous risk management framework. This investment objective is intended to be achieved via the investment policy for the Program, which is to trade relevant asset classes applying the Program.

The core objectives of the Program are:

(i) to produce strong medium-term capital appreciation; (“medium-term” generally referring to a three- to five-year time period);

(ii) to seek and exploit profit opportunities in both rising and falling markets using a disciplined quantitative investment process;

(iii) to seek non-correlation with the broad bond and stock markets and thereby play a valuable role in enhancing the risk/return profile of traditional investment portfolios; and

(iv) to minimize risk by operating in a diverse range of markets and sectors using a consistent investment process that adheres to pre-defined and monitored risk limits and determines market exposure in accordance with factors including (but not limited to) market correlation, volatility, liquidity and the cost of market access.

The Series’ account traded pursuant to the Program may experience returns that differ from other Trading Advisor accounts traded pursuant to the same Program due to, among other factors: (a) regulatory constraints on the ability of the Series to have exposure to certain contracts; (b) the Series’ selection of the Clearing Broker, which affects access to markets; (c) the effect of intra-month adjustments to the trading level of the account; (d) the manner in which the account’s cash reserves are invested; (e) the size of the Series’ account; (f) the Series’ functional currency, the U.S. dollar; and (g) the particular futures contracts traded by the Series’ account. Additionally, certain markets may not be liquid enough to be traded for the Series’ account.

The investment approach that underpins the Program is proprietary. The Trading Advisor’s investment philosophy has remained consistent and involves a scientific approach to investment driven by the Trading Advisor’s belief that market behavior is not random but rather contains statistically measurable and predictable price movements and anomalies which, through sophisticated quantitative research and a disciplined approach, can be successfully identified and exploited for profit.

Allocation Methodology

Allocations to the strategy, markets and asset classes traded by the Program are reviewed on a regular basis using a robust and stable quantitative methodology which takes into account a range of factors that may include liquidity, risk and expected returns. The Program, subject to applicable investment policies, does not have any inherent preference for, or bias towards, any market, asset class or instrument but rather aims to maximize returns within liquidity constraints, such as speculative position limits or market disruptions.

Market Access and Trading Costs

The Trading Advisor appreciates the importance of executing trades in a cost efficient manner and the significance of market impact and trading costs on the Series’ performance. The Trading Advisor takes into account the liquidity of the markets in which it executes trades so as to endeavor to provide optimal market execution results (including executing electronically wherever beneficial).

2

Risk Management

A fundamental principle of the Trading Advisor’s investment approach is the importance of a robust risk management framework. The Trading Advisor employs a value-at-risk methodology and other risk management procedures to monitor the risk of the Program within pre-defined guidelines. Additionally, the Trading Advisor has developed mechanisms to control risk at both an individual market and portfolio level. In order to monitor and respond to changes in the trading conditions in a market at all times, the Trading Advisor believes a high level of transparency is required. This transparency is achieved by generally investing in liquid instruments with real time pricing, although this may not be possible in all markets or all instruments.

Research Commitment and Program Development

The Trading Advisor retains the right to develop and make changes to the Program at its sole discretion, including (without limitation) the incorporation of new markets, instruments, strategies and asset classes into the Program. The Series will be notified of such changes only if they amount to material changes to the investment objective or investment policy of the Program.

The Program is proprietary and highly confidential to the Trading Advisor. Accordingly, the description of the Program as contained herein is general only and is not intended to be exhaustive or absolute.

Custody of Assets

A substantial amount of the Series’ assets are held in customer accounts at the Clearing Broker, an indirect, wholly-owned subsidiary of an affiliate of the former sponsor, although they may be held at other affiliates of the Clearing Broker or other third-party clearing brokers selected by the Sponsor.

Only assets held to margin Commodity Futures Trading Commission (“CFTC”)-regulated futures contracts may be held in CFTC-regulated “segregated funds” accounts. “Segregated funds” accounts are insulated from liability for any claims against a broker other than those of other customers. As of December 31, 2008, 78.6% of the net assets of the Series was held in segregated funds. The bulk of the Series’ capital is not held in segregation, but rather in custody or other client accounts maintained by affiliates of the Clearing Broker. Subject to any applicable regulatory restrictions, these affiliates may make use of such capital, which is treated as a liability or deposit owed by such affiliates to the Series. However, if such an affiliate were to incur financial difficulties, the Series’ assets could be lost (the Series becoming only a general creditor of such affiliate) and, even if not lost, could be unavailable to the Series for an extended period.

The Sponsor considers the Clearing Broker’s policies regarding the safekeeping of the Series’ assets to be fully consistent with industry practices. However, the Series’ capital may be subject to the risk of its custodians’ insolvency. The Administrator (defined below) also accesses a custody account established between the Platform, the Series and Mellon Bank N.A. to hold small amounts of funds in order to pay expenses of the Series and Platform.

Approximately 70% to 95% of the Series’ capital is held in cash or cash equivalents at any given time.

Interest

The Series generally earns interest, as described below, on the cash actually held by the Series, plus unrealized gain and loss marked to market daily on open positions (the “Cash Assets”). The Series does not earn interest income on the Series’ gains or losses on their open forward, commodity option and certain non-U.S. futures positions because such gains and losses are not collected or paid until such positions are closed out. Interest is earned only on funds actually held in the Series’ account.

3

The Series’ Cash Assets may be greater than, less than or equal to such Series’ Net Asset Value (as described in Item 6 “Selected Financial Data,” “net asset value for all other purposes”) primarily because Net Asset Value reflects all gains and losses on open positions as well as accrued but unpaid expenses.

The Clearing Broker pays interest as of the end of each month at a rate corresponding to an annual rate equal to the prevailing Federal Funds Rate less 0.50% (meaning, if the prevailing Federal Funds Rate is 1.00% per annum, the Clearing Broker would pay the Series 0.50% per annum) on the Series’ average daily Cash Assets. The Clearing Broker will retain any returns on the Series’ Cash Assets in excess of the Federal Funds Rate less 0.50%. The Clearing Broker retains the additional economic benefit (which may be significant) derived from possession of the Series’ Cash Assets and Dekla Financial, LLC (the “Introducing Broker”), an affiliate of the Sponsor, may receive a portion of these revenues.

The Clearing Broker, in the course of acting as commodity broker for the Series, lends certain currencies to, and holds certain non-U.S. currency balances on behalf of, the Series. If, for example, the Series needed to make a margin deposit in Swiss Francs, the Clearing Broker would lend the Series the Swiss Francs, charging a local short-term rate plus a spread of up to 1.0% per annum (at current rates). Should the Series hold Swiss Franc balances in its account, the Clearing Broker will credit the Series with interest at the same local short-term rate less a spread of up to 2.0% per annum (at current rates).

The Clearing Broker follows its standard procedures for crediting and charging interest to the Series. The Clearing Broker is able to generate significant economic benefit from doing so, especially as the Clearing Broker is able to meet the margin requirements imposed on its customers as a group, whereas each customer must margin its account on a stand-alone basis. Consequently, the Clearing Broker may record a loan of Swiss Francs (in the above example) to the Series’ account which the Clearing Broker charges interest even though the Clearing Broker itself does not have to deposit any Swiss Francs at the applicable clearinghouse.

Description of Current Expenses

The Trading Advisor receives a 2% per annum management fee of the Series’ net asset value for all other purposes. Such fee is calculated and paid on a monthly basis. The Trading Advisor has agreed to share 0.50% of such management fee with UBS Financial Services Inc., a selling agent for the Series (“UBS FS”). The Trading Advisor also will receive a performance fee equal to 20% of the new net trading profits of the Series for each quarter. New net trading profits during each quarter refers to the excess, if any, of the cumulative level of net trading profits attributable to the Series at the end of such quarter over the highest level of cumulative net trading profits as of the end of any preceding quarter (the “High Water Mark”). Performance fees do not, while losses do, reduce cumulative net trading profits. New net trading profits do not include interest income. To the extent that any redemptions are made from the Series, the High Water Mark is proportionately reduced and a proportionate performance fee paid (if accrued).

The Sponsor receives a monthly sponsor fee of 0.02083 of 1% (a 0.25% annual rate) of the Series’ month-end net asset value for all other purposes, including interest income, of a Member’s investment in the Series for such month.

DPM Mellon, LLC (the “Administrator”) receives a monthly fee as to be determined by the Sponsor and the Administrator up to 0.0167 of 1% of the Series’ net asset value for all other purposes as of the beginning of each month (a 0.25% annual rate), subject to a monthly minimum of $10,000. Effective December 31, 2008, the administration agreement between the Administrator and the Platform, Series and Trading Fund was terminated, however, the Administrator will provide services necessary to allow the Sponsor to prepare reports for the Series for the period ending December 31, 2008. The Sponsor has entered into an agreement with Spectrum Global Fund Administration, LLC to act as the administrator for the Platform and the Series effective January 1, 2009.

The Series brokerage commissions are paid upon completion or liquidation of one-half of a trade and are referred to as “per side” commissions, which cover either the initial purchase (or sale) or the subsequent offsetting sale (or purchase) of a single commodity futures contract. The principal operating costs of the Series are the per side brokerage commissions paid to the Clearing Broker and the Introducing Broker (a portion of which is paid to the Series’ executing brokers, which may or may not include the Clearing Broker, as commissions for their execution services) and the currency forward contract (“F/X”) dealer spreads paid to UBS AG and others. The “per side”

4

commissions for U.S. markets paid by the Series are approximately $4 per side plus fees (except in the case of certain non-U.S. contracts on which the rates may be as high as $50 per side plus fees due, in part, to the large size of the contracts traded).

Many of the Series’ currency trades are executed in the spot and forward non-U.S. exchange markets (the “F/X Markets”) in which there are no direct execution costs. Instead, the banks and dealers in the F/X Markets, including UBS AG, take a “spread” between the prices at which they are prepared to buy and sell a particular currency, and such spreads are built into the pricing of the spot or forward contracts with the Series. A significant portion of the Series’ non-U.S. currency trades may be executed through UBS AG, an affiliate of the former sponsor. In general, the Sponsor estimates that aggregate brokerage commission charges (including F/X spreads) will not exceed 3.5%, and should range between approximately 0.5% and 3% per annum of the Series’ average month-end assets (meaning the average month-end net asset value for all other purposes for the then-current fiscal year).

The former sponsor advanced expenses incurred in connection with the organization of the Platform and the organization and initial offering of the Units of the Series. The Series reimbursed the former sponsor for these costs. For financial reporting purposes in conformity with U.S. generally accepted accounting principles, the Series expensed the total organizational costs of $208,820 when incurred and deducted the initial offering costs of $119,732 from Members’ capital as of March 16, 2007, the date of commencement of operations of the Series (“net asset value for financial reporting” or the “net asset value per Unit for financial reporting” – see Item 6 “Selected Financial Data”. For all other purposes, the Series amortizes organizational and initial offering costs over a 60 month period (“net asset value for all other purposes” or the “net asset value per Unit for all other purposes”). The amortization of such costs reduce the net asset value for all other purposes of the Units for purposes of determining subscriptions, redemptions and any fees based on the Units’ net asset value for all other purposes and for reporting performance for all purposes other than as related to financial reporting. However, the amount of such costs attributable to the Platform’s organization that are not already amortized may be allocated to and amortized by other Series for net asset value for all other purposes when and if such other Series are added to the Platform or in a manner as the Sponsor may otherwise determine.

Each Member or Member-related account is subject to an upfront, waivable placement fee of 0% to 2% of the subscription price of the Units, which will be paid once by the relevant Member, not by the Platform, the Series or the Sponsor, on such Member’s initial subscription to the Series during any twelve month period. No placement fee will be charged in connection with an exchange. The placement fee payable on such initial subscription is deducted from the subscription amount. The placement fee to which Members are subject will vary among Members. Each Member also will pay an ongoing sales commission equal to 2% per annum of the month-end net asset value for all other purposes, including interest income, of a Member’s investment in the Series. UBS FS, in consultation with the Sponsor, may waive or reduce such sales commission for certain Members without entitling any other Member to any such waiver or reduction.

The Series will pay its own operating costs, including, without limitation: ongoing offering expenses; execution and clearing brokerage commissions; forward and other over the counter trading spreads; administrative, transfer, exchange and redemption processing, legal, regulatory, reporting, filing, tax, audit, escrow, accounting and printing fees and expenses, as well as extraordinary expenses. Such operating costs are allocated pro rata among the Units based on their respective net asset values for all other purposes. These expenses are paid in addition to the other expenses described below.

The Sponsor has retained outside service providers to supply certain services, including, without limitation, tax reporting, accounting and escrow services. Operating costs include the Series’ allocable share of the fees and expenses of such outside service providers.

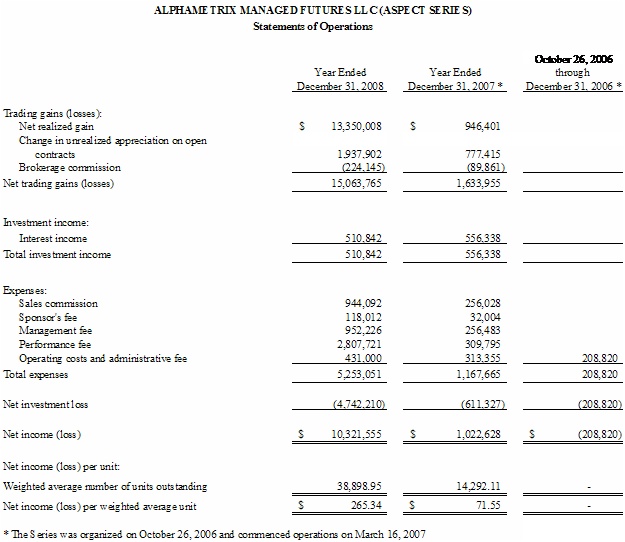

The following table summarizes the expenses incurred by the Series for the year ended December 31, 2008:

| 2008 | 2007 | |||||||||||||||

| Expenses | Dollar Amount | % of Average Month-End Net Asset Value for Financial Reporting | Dollar Amount | % of Average Month-End Net Asset Value for Financial Reporting | ||||||||||||

| Performance fees | $ | 2,807,721 | 6.04 | % | 309,795 | 2.09 | % | |||||||||

| Management fees | 952,226 | 2.05 | % | 256,483 | 1.73 | % | ||||||||||

| Sales Commissions | 944,092 | 2.03 | % | 256,028 | 1.72 | % | ||||||||||

| Brokerage Commission | 224,145 | 0.48 | % | 89,861 | 0.61 | % | ||||||||||

| Sponsor’s fees | 118,012 | 0.26 | % | 32,004 | 0.22 | % | ||||||||||

| Other expenses | 431,000 | 0.93 | % | 313,355 | 2.11 | % | ||||||||||

| Total | $ | 5,477,196 | 11.79 | % | 1,257,526 | 8.48 | % | |||||||||

5

The foregoing table does not reflect the bid-ask spreads paid by the Series on its forward trading, or the benefits which may be derived by UBS from the deposit of certain of the Series’ assets maintained at the Clearing Broker.

The Series’ average month-end net asset value for financial reporting during 2008 equaled $46,465,647.

During 2008 the Series earned $510,842 in interest income or approximately 1.09% of the Series’ average month-end net asset value for financial reporting.

Regulation

The Sponsor and the Trading Advisor are registered with the CFTC as commodity pool operators and commodity trading advisors (“CTAs”) and are members of the National Futures Association (“NFA”) in such capacities. The CFTC may suspend a commodity pool operator’s or trading advisor’s registration if it finds that its trading practices tend to disrupt orderly market conditions or in certain other situations. In the event that the registration of the Sponsor or of the Trading Advisor as a commodity pool operator or a commodity trading advisor were terminated or suspended, the Sponsor or Trading Advisor, as applicable, would be unable to continue to manage the business of the Series. Should the Sponsor’s or Trading Advisor’s registration be suspended, termination of the Series might result. In addition to such registration requirements, the CFTC and certain commodity exchanges have established limits on the maximum net long or net short positions that any person may hold or control in particular commodities. Most exchanges also limit the changes in futures contract prices that may occur during a single trading day. Currency forward contracts are not subject to regulation by any U.S. government agency.

Other than in respect of the registration requirements pertaining to the Series’ securities under Section 12(g) of the Securities Exchange Act of 1934, as amended, the Platform and the Series are generally not subject to regulation by the Securities and Exchange Commission. The Trading Advisor is also regulated by the Financial Service Authority of the United Kingdom.

(i) through (xii) – not applicable.

(xiii) the Series has no employees.

(d) Financial Information About Geographic Areas

The Series does not engage in material operations in foreign countries, nor is a material portion of the Series’ revenue derived from customers in foreign countries. The Series will trade on a number of U.S. and non-U.S. commodities exchanges. The Series will not engage in the sales of goods or services.

| Item 1A: | Risk Factors |

Not applicable

Not applicable

6

| Item 1B: | Unresolved Staff Comments |

Not applicable

| Item 2: | Properties |

The Series does not own or use any physical properties in the conduct of its business.

The Series’ administrative office is the administrative office of the Sponsor (181 West Madison, Suite 3825, Chicago, IL 60602). The Sponsor performs administrative services for the Series from the Sponsor’s offices.

| Item 3: | Legal Proceedings |

The Sponsor is not aware of any pending legal proceedings to which either the Series is a party or to which any of its assets are subject. In addition there are no pending material legal proceedings involving the Sponsor

| Item 4: | Submission of Matters to a Vote of Security Holders |

None.

PART II

| Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

(a) Market Information

There is no trading market for the Units, and none is likely to develop. Units may be redeemed at the net asset value per Unit for all other purposes as of the end of any calendar month. Redemption requests must be submitted on or prior to the 15th day of the calendar month (or the following business day) in which such Units are to be redeemed.

(b) Holders

As of December 31, 2008, there were 392 holders of Units, including the Sponsor.

(c) Dividends

No distributions or dividends have been made on the Units, and the Sponsor has no present intentions to make any.

(d) Securities Authorized for Issuance Under Equity Compensation Plans

None.

(e) Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

The Series did not sell any unregistered securities since it commenced operations on March 16, 2007 that have not previously been included in the Series’ Quarterly Reports on Form 10-Q or in a Current Report on Form 8-K.

(f) Issuer Purchases of Equity Securities

Pursuant to the Platform’s Amended and Restated Limited Liability Company Agreement and the Series’ Amended and Restated Separate Series Agreement, Members may redeem their Units at the end of each calendar month at the then current month-end net asset value per Unit for all other purposes, i.e. reflecting the amortization of organizational and initial offering costs. The redemption of Units has no impact on the value of Units that remain

7

outstanding, and Units are not reissued once redeemed. The following table summarizes the redemptions by Members during the fourth quarter of 2008:

| Month | Units Redeemed | Redemption Date Net Asset Value per Unit for All Other Purposes |

| October 31, 2008 | 1,176.726 | $ 1,231.50 |

| November 30, 2008 | 653.420 | $ 1,294.37 |

| December 31, 2008 | 1,116.484 | $ 1,343.64 |

| Total | 2,946.630 |

8

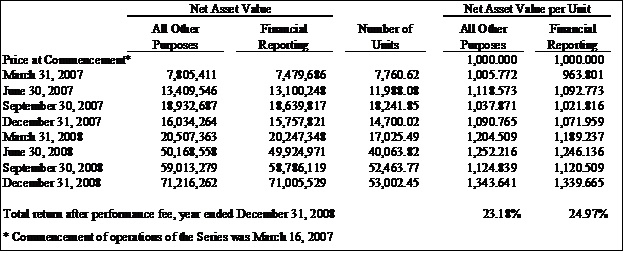

The following selected data has been derived from the audited Financial Statements of the Series.

9

ALPHAMETRIX MANAGED FUTURES LLC (ASPECT SERIES)

Statements of Financial Condition

| December 31, 2008 | December 31, 2007 | |||||||

| Assets | ||||||||

| Equity in commodity trading account at clearing broker: | ||||||||

| Cash | $ | 71,677,315 | $ | 20,995,051 | ||||

| Net unrealized appreciation on open contracts | 2,715,317 | 777,415 | ||||||

| Net payable related to unexpired contracts | (9,090 | ) | (14,822 | ) | ||||

| 74,383,542 | 21,757,644 | |||||||

| Cash | 314,724 | 92,369 | ||||||

| Net interest receivable | 1,933 | 63,269 | ||||||

| Total assets | $ | 74,700,199 | $ | 21,913,282 | ||||

| Liabilities and Members’ Capital | ||||||||

| Liabilities | ||||||||

| Accrued brokerage commissions | $ | 5,627 | $ | 4,631 | ||||

| Accrued sales commission | 121,422 | 36,009 | ||||||

| Accrued sponsor’s fee | 15,178 | 4,501 | ||||||

| Accrued management fee | 124,314 | 35,963 | ||||||

| Accrued performance fee | 1,613,251 | - | ||||||

| Accrued operating costs and administrative fee | 183,724 | 99,345 | ||||||

| Subscriptions received in advance | 131,000 | 444,250 | ||||||

| Redemptions payable | 1,500,154 | 5,530,762 | ||||||

| Total liabilities | 3,694,670 | 6,155,461 | ||||||

| Members’ Capital | ||||||||

| Members (52,994.33 and 14,690.08 units outstanding at December 31, 2008 and 2007, respectively, unlimited units authorized) | 70,994,651 | 15,747,164 | ||||||

| Sponsor (8.12 and 9.94 units outstanding at December 31, 2008 and 2007, respectively, unlimited units authorized) | 10,878 | 10,657 | ||||||

| Total members’ capital | 71,005,529 | 15,757,821 | ||||||

| Total liabilities and members’ capital | $ | 74,700,199 | $ | 21,913,282 | ||||

The Sponsor paid all expenses incurred in connection with the organizational and initial offering of the Units. As described in the Series’ current Confidential Disclosure Document, the Series reimbursed the Sponsor for these costs in 2008. For financial reporting purposes in conformity with U.S. generally accepted accounting principles, the

10

Series expensed the total organizational costs of $208,820.00 when incurred and deducted the initial offering costs of $119,732 from Members’ capital as of March 16, 2007 (the date of commencement of operations of the Series) (“net asset value for financial reporting” or the “net asset value per Unit for financial reporting”). For all other purposes, including determining the net asset value per Unit for subscription and redemption purposes, the Series amortizes organizational and initial offering costs over a 60 month period (“net asset value for all other purposes” or the “net asset value per Unit for all other purposes”).The net asset value and net asset value per Unit are as follows:

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

All figures and performance returns noted in this Item 7 are based on the net asset value and/or the net asset value per Unit for all other purposes, which complies with U.S. generally accepted accounting principles, except with respect to organizational and initial offering costs (which are being amortized over 60 months) as described in Item 6 “Selected Financial Data.” All figures and performance returns communicated to Members are based on the net asset value and/or the net asset value per Unit for all other purposes.

Operational Overview

This performance summary describes the manner in which the Series has performed in the past and is not an indication of future performance. While certain market movements are attributable to various market factors, such factors may or may not have caused such movements but they may have simply occurred at or about the same time.

The Series is unlikely to be profitable in markets in which trends do not occur. Static or erratic prices are likely to result in losses. Similarly, sharp trend reversals, which can be caused by many unexpected events, can lead to major short-term losses, as well as gains.

While there is no assurance the Series will profit in any market condition, markets having substantial and sustainable price movements offer the best profit potential for the Series.

Liquidity

Virtually all of the Series’ capital is held in cash or cash equivalents at the Clearing Broker and is used to margin the Series’ futures and forward currency positions and is withdrawn, as necessary, to pay redemptions and expenses.

11

The Series does not maintain any sources of financing other than that made available by the Clearing Broker to fund foreign currency settlements for those instruments transacted and settled in foreign currencies. The Series pays prevailing market rates for such borrowings. A portion of the assets maintained at the Clearing Broker are restricted cash required to meet maintenance margin requirements. Included in cash deposits with the Clearing Broker as of December 31, 2008 was restricted cash for margin requirements of $5,111,823. This cash becomes unrestricted if the underlying positions it supports are liquidated.

Other than potential market-imposed limitations on liquidity, due, for example, to limited open interest in certain futures markets or to daily price fluctuation limits, which are inherent in the Series’ futures and forward trading, the Series’ assets are highly liquid and are expected to remain so. Because the Series’ assets are held in cash, it expects to be able to liquidate all of its open positions or holdings quickly and at prevailing market prices, except in unusual circumstances. This permits the Trading Advisor to enter and exit markets, leverage and deleverage in accordance with its strategy. From its commencement of operations on March 16, 2007 through December 31, 2008, the Series experienced no meaningful periods of illiquidity in any of the markets in which it traded. The Series processes redemptions on a monthly basis. The Series incurred redemptions of $4,915,292 (3,914.03 Units) for the year ended December 31, 2008, and accrued $1,500,154 in redemptions payable to Members at December 31, 2008.

Capital Resources

The Series’ Units may be offered for sale as of the beginning, and may be redeemed as of the end, of each month.

The amount of capital raised for the Series is not expected to have a significant impact on its operations, as the Series has no significant capital expenditure or working capital requirements other than for monies to pay trading losses, brokerage commissions and charges. Within broad ranges of capitalization, the Series’ trading positions should increase or decrease in approximate proportion to the size of the Series.

The Series raises additional capital only through the sale of Units and capital is increased through trading profits (if any). The Series does not maintain any sources of financing other than that made available by the Clearing Broker to fund foreign currency settlements for those instruments transacted and settled in foreign currencies.

The Series may trade a variety of futures-related instruments, including (but not limited to) instuments related to bonds, currencies, interest rates, equities, equity indices, debt securities and selected physical commodities and derivatives. Risk arises from changes in the value of these contracts (market risk) and the potential inability of counterparties or brokers to perform under the terms of their contracts (credit risk). Market risk is generally to be measured by the face amount of the futures positions acquired and the volatility of the markets traded. The credit risk from counterparty non-performance associated with these instruments is the net unrealized gain, if any, on these positions plus the value of the margin or collateral held by the counterparty. The risks associated with exchange-traded contracts are generally perceived to be less than those associated with over-the-counter transactions, because exchanges typically (but not universally) provide clearinghouse arrangements in which the collective credit (in some cases limited in amount, in some cases not) of the members of the exchange is pledged to support the financial integrity of the exchange. In over-the-counter transactions, on the other hand, traders must rely solely on the credit of their respective individual counterparties. Margins that may be subject to loss in the event of a default are generally required in exchange trading, and counterparties may require margin or collateral in the over-the-counter markets.

The Trading Advisor attempts to control risk in all aspects of the investment process, although there can be no assurance that it will, in fact, succeed in doing so. The Series is designed to take market risk on a systematic basis across a broad portfolio of liquid markets and to monitor and minimize exposure to all other risks, such as credit and liquidity risks. The trading systems used include various proprietary systems that are designed to control the risk taken at the individual position level as well as at the overall portfolio level. The Trading Advisor monitors and controls market risk within limits at both sector and portfolio levels.

The financial instruments traded by the Series contain varying degrees of risk whereby changes in the market values of the futures and forward contracts or the Series’ satisfaction of the obligations may exceed the amount recognized in the Statements of Financial Condition of the Series.

12

Due to the nature of the Series’ business, substantially all its assets are represented by cash and U.S. government obligations, while the Series maintains its market exposure through open futures and forward contract positions.

The Series’ futures contracts are settled by offset and are generally cleared by the exchange clearinghouse function. Open futures positions are marked to market each trading day and the Series’ trading accounts are debited or credited accordingly. The Series’ spot and forward currency transactions conducted in the interbank market are settled by netting offsetting positions or payment obligations and by cash payments.

The value of the Series’ cash and financial instruments is not materially affected by inflation. Changes in interest rates, which are often associated with inflation, could cause the value of certain of the Series’ debt securities to decline, but only to a limited extent. More importantly, changes in interest rates could cause periods of strong up or down market price trends, during which the Series’ profit potential generally increases. However, inflation can also give rise to markets which have numerous short price trends followed by rapid reversals, in which the Series is likely to suffer losses.

Results of Operations

General

The Trading Advisor manages the assets of the Series pursuant to the Program (see Item 1(c) “Narrative Description of Business”). The Trading Advisor was established in 1997 by Anthony Todd, Dr. Eugene Lambert, Martin Lueck and Michael Adam, all of whom were involved in the development of AHL (Adam, Harding and Lueck), now part of Man Group plc, where they advanced the application of systematic quantitative techniques in managed futures investment. The Trading Advisor has grown to a team of over 100 employees and manages approximately $4.3 billion as of December 31, 2008. The Trading Advisor is a limited liability company registered in England and Wales, which is regulated in the United Kingdom by the Financial Services Authority. Since October 1999, the Trading Advisor has been a member of NFA and has been registered with the CFTC as a commodity trading advisor and commodity pool operator. The Trading advisor has also been registered with NFA as a principal of its commodity trading advisor subsidiary Aspect Capital Inc. since August 2004. The Trading Advisor has also been registered with the Securities and Exchange Commission as an investment adviser since October 2003.

The Series commenced trading activities March 16, 2007 with an initial capitalization of $7,760,620, of which $5,000,000 was contributed by the Trading Advisor as seed capital. On December 31, 2007 the Trading Advisor redeemed the full value of its seed capital. As of December 31, 2008, the Series had a capitalization of $71,005,529 based on the net asset value for all other purposes.

Performance Summary

This performance description is a brief summary of how the Series performed in the past, not necessarily an indication of how it will perform in the future. In addition, the general causes to which certain price movements are attributed may or may not in fact have caused such movements, but simply occurred at or about the same time. The Series’ past performance is not necessarily indicative of how it will perform in the future.

December 31, 2008

The Series posted an overall gain for the period from January 1, 2008 to December 31, 2008 of 23.18%, based on the net asset value for all other purposes (refer to Item 6 “Selected Financial Data”).

13

The energy sector, and particularly crude oil, posted strong gains for the Series. The first half of 2008 was marked by a long upward trend in crude that saw prices go from $90 a barrel to record breaking highs at $147 a barrel, a gain of over 50%. After June, crude reversed and fell all the way to $40 a barrel, another long and consistent trend downwards. The financial crisis caused a slump in economic activity and demand destruction leading to this sharp reversal in oil prices. The Series was well positioned to take advantage of this downward trend, particularly during the months of September through December. Natural gas followed the price of crude oil closely and profited similarly. Although historically not correlated to crude oil, natural gas futures prices rose from $9 in January 2008 to $14 in June, and proceeded to then fall all the way back to below $5 by the end of the year. The Series was able to capture and profit from both trends.

The agricultural commodity sector, which includes grains, softs and meats, saw positive trends in the first two quarters of the year, and the Series benefitted by taking long positions. Sharp reversals around the month of July caused the Series to give back its initial gains. The models repositioned themselves to take reduced long position exposure towards the latter part of the year since the prices receded so far from their highs. Price movement for most grains, such as wheat, corn and soybeans, softs such as coffee and cotton, and meats such as cattle and hogs, were very similar and resembled the price movement in the energy sector. The first half of 2008 saw long upward trends that reversed dramatically in July and August. The Series experienced difficulty in the transition months of July and August and reduced exposures going into the fourth quarter. Although all these markets tend not to be too highly correlated historically, much larger fundamental forces, such as increased demand from China early in the year, and then the financial crisis beginning in late summer, caused very strong trends in both directions with turmoil in between during the trend reversal. The Series is designed to capture and profit from trending markets, but the volatility increased so dramatically that positions were reduced and losses were incurred in this sector for 2008.

Along with energy, interest rates and bonds posted strong gains for the Series in 2008. Profits came from both short-term interest rates as well as long term government bonds, particularly in the fourth quarter. The continued turmoil in the financial sector, increased risk aversion among investors and coordinated interest rate cuts by major central banks led to extremely strong upward trends in the interest rate sector in the latter part of the year. The Series was able to take advantage of the flight to quality in bonds and changes in short-term interest rate expectations, finishing the year strongly. The Series is designed to capture strong trends both long and short, and it performed accordingly by capturing these upward moves.

The currency sector posted losses for the Series during the period. The currency sector saw increased volatility and sharp swings due to uncertainty in government policies and a bleak global economic outlook. The initial part of the year saw the models short US Dollar until July in order to take advantage of the downward trend of the US Dollar against many currencies, particularly the Euro and Swiss Franc. Sharp reversals in late summer made it difficult for the system to reposition itself and react quickly leading to difficult trading and negative performance for this sector. The sharp reversals in the global markets were due to risk aversion trades, relative strengthening of US Dollar driven by a flight to safety, and changes in interest rate policy in Australia and Europe. The Series is not designed to digest all these fundamental factors but is instead designed to capture trends in price movement. The quick reversals and dramatic increases in price volatility caused the Series to reduce exposures and tread cautiously.

The metals sector was difficult to trade for most of the year. The Series initially posted marginal losses in both precious and industrial metals. Strong demand from China, particularly for industrial metals in their build-up to the

14

Beijing Olympics kept prices high. After the Olympics and correspondingly around mid-year, industrial metals reversed and traded down for most of the rest of the year as stock build-ups and recessionary concerns put downward pressure on industrial metals. The Series captured the downward trend to post gains by positioning itself on the short side of the trade, and so the fourth quarter was the most profitable for this sector. Precious metals, specifically gold and silver, experienced strong though quick trends up and down, and the speed of these trends made it difficult for the models to adjust quickly enough.

The stock indices sector was one of the most profitable sectors for the Series. The slowing global growth environment, recessionary concerns for the US economy and increased risk aversion among investors saw the global stock markets trend downward for most of the year. The Series took short positions early and held in order to take advantage of the bear market trend. The profits may have been better for this sector had it not been for the unprecedented volatility in most global equity indices. The systematic risk management responded to this increased volatility by reducing positions and navigating through the unchartered price movements delicately. Because of this, returns in the third and fourth quarters were modest even though equity indices sold off dramatically.

Variables Affecting Performance

The principal variables that determine the net performance of the Series are gross profitability from the Series’ trading activity and interest income.

The Series’ assets are maintained at the Clearing Broker. On assets held in U.S. dollars, the Clearing Broker credits the Series with interest at the prevailing Federal Funds Rate less 50 basis points per annum. In the case of non-U.S. dollar instruments, the Clearing Broker lends to the Series all required non-U.S. currencies at a local short-term interest rate plus a spread of up to 100 basis points per annum (at current rates). For deposits held in non-U.S. currencies, the Clearing Broker credits the local short-term interest rate less a spread of up to 200 basis points per annum (at current rates).

The Series’ management, Sponsor’s and administrative fees and the sales commissions are a constant percentage of the Series’ net asset value for all other purposes. Brokerage commissions, which are not based on a percentage of the Series’ net assets, are based on the volume of trades executed and cleared on behalf of the Series. Brokerage commissions are based on the actual number of contracts traded. The performance fees payable to the Trading Advisor are based on the new net trading profits, if any, generated by the Series, excluding interest income and after reduction for brokerage commissions and certain other fees and expenses.

For the Series, there is generally no meaningful distinction between realized and unrealized profits. Most of the instruments traded on behalf of the Series are highly liquid and can be closed out immediately.

Off-balance Sheet Arrangements

The Series has no applicable off-balance sheet arrangements of the type described in Items 3.03(a)(4) of Regulation S-K.

Contractual Obligations

The Series does not enter into any contractual obligations or commercial commitments to make future payments of a type that would be typical for an operating company or that would affect its liquidity or capital resources. The Series’ sole business is trading futures and forward currency contracts, both long (contracts to buy) and short (contracts to sell). All such contracts are settled by offset, not delivery. The Series’ Financial Statements filed as Exhibit 13.01 herewith present a Condensed Schedule of Investments setting forth net unrealized appreciation (depreciation) of the Series’ open future and forward currency contracts, both long and short, at December 31, 2008.

Item 7A: Quantitative and Qualitative Disclosures About Market Risk

Not applicable; the Series is a smaller reporting company

Item 8: Financial Statements and Supplementary Data

15

| Net Income by Quarter | ||||||||||||||||||||

| Four Quarters through December 31, 2008 | ||||||||||||||||||||

| First | Second | Third | Fourth | |||||||||||||||||

| Quarter | Quarter | Quarter | Quarter | |||||||||||||||||

| 2008 | 2008 | 2008 | 2008 | Total | ||||||||||||||||

| Total Income (Loss) | 2,572,891 | 4,066,882 | (5,452,453 | ) | 14,387,287 | 15,574,607 | ||||||||||||||

| Total Expenses | (782,405 | ) | (1,281,577 | ) | (709,630 | ) | (2,479,438 | ) | (5,253,051 | ) | ||||||||||

| Net Income (Loss) | 1,790,486 | 2,785,305 | (6,162,083 | ) | 11,907,849 | 10,321,556 | ||||||||||||||

| Net Income (Loss) per Unit (1) | 46.03 | 71.60 | (158.41 | ) | 306.12 | 265.34 | ||||||||||||||

(1) Based on average number of Units for the year

Financial Statements meeting the requirements of Regulation S-X appear in Exhibit 13.01 to this report. The supplementary financial information specified by Item 302 of Regulation S-K is included in this report under Item 6 “Selected Financial Data” above.

None.

The Sponsor, with the participation of the Sponsor’s principal executive officer and principal financial officer, has evaluated the effectiveness of the design and operation of its disclosure controls and procedures with respect to the Series as of the end of the fiscal year for which this Annual Report on Form 10-K is being filed, and, based on their evaluation, have concluded that these disclosure controls and procedures are effective. There were no significant changes in the Sponsor’s internal controls with respect to the Series or in other factors applicable to the Series that could materially affect these controls subsequent to the date of their evaluation.

Changes in Internal Control over Financial Reporting

The Sponsor assumed responsibility for internal controls over financial reporting from the Series’ former sponsor on November 1, 2008. The Sponsor kept such internal controls largely intact by retaining the Administrator through year-end and hiring an employee who had worked for the former sponsor solely with respect to the Series. Accordingly, there have been no material changes in internal control over financial reporting of the Series.

Management’s Annual Report on Internal Control over Financial Reporting

The Sponsor is responsible for establishing and maintaining adequate internal control over the financial reporting of the Series. Internal control over financial reporting is defined in Rules 13a-15(f) and 15d-15(f) under the Securities Exchange Act of 1934, as amended, as a process designed by, or under the supervision of, a company’s principal executive and principal financial officers and effected by a company’s board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles. The Sponsor’s internal control over financial reporting includes those policies and procedures that:

• pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the Series;

16

• provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements of the Series in accordance with U.S. generally accepted accounting principles, and that receipts and expenditures of the Series are being made only in accordance with authorizations of management and directors of the Sponsor; and

• provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the Series’ assets that could have a material effect on its financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

The management of the Sponsor assessed the effectiveness of its internal control over financial reporting with respect to the Series as of December 31, 2008. In making this assessment, management used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) in Internal Control — Integrated Framework. Based on its assessment, management has concluded that, as of December 31, 2008, the Sponsor’s internal control over financial reporting with respect to the Series is effective based on those criteria.

This annual report does not include an attestation report of the Series’ registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by the Series’ registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit the company to provide only management’s report in this annual report.

None.

PART III

(a) and (b) Identification of Directors and Executive Officers

As a segregated series of a limited liability company, the Series itself has no officers or directors and is managed by the Sponsor.

The following are the principal officers and managers of the Sponsor.

Aleks Kins. Mr. Kins, age 38, has been President and Chief Executive Officer of AlphaMetrix, LLC (“AlphaMetrix”) since he founded AlphaMetrix in April 2005. Mr. Kins is also the founder and a principal of AlphaMetrix Alternative Investment Advisors, LLC, an independent research affiliate of AlphaMetrix. Mr. Kins is also an associated person and principal of Dekla Financial, LLC, an affiliate of AlphaMetrix. Dekla is a registered introducing broker that serves as the introducing broker for various commodity pools sponsored by AlphaMetrix and other futures trading accounts. Mr. Kins was the President and co-founder of Access Asset Management, a registered CPO and CTA, from November 2000 through the founding of AlphaMetrix in April 2005. Mr. Kins received a B.A. in Economics from Brown University in 1993.

Dennis R. Zarr. Mr. Zarr, age 61, joined AlphaMetrix in February 2008 and is its Chief Operations Officer. Mr. Zarr is also an associated person and principal of Dekla, an affiliate of AlphaMetrix. From March 1993 until joining AlphaMetrix, Mr. Zarr served as Senior Vice President and Director of Business Development for Rand Financial Services, Inc., a registered futures commission merchant. Mr. Zarr received his B.S. in Finance from DePaul University in 1970.

George Brown. Mr. Brown, age 53, joined AlphaMetrix in March 2008 and is its Chief Financial Officer. Mr. Brown served as a consultant for Nature’s Best, a sports nutrition and protein beverages producer, from

17

December 2007 to February 2008, as Chief Financial Officer of Ultraguard Corporation, a manufacturer of dual smoke/carbon monoxide detectors and wireless monitor systems, from September 2005 to August 2007 and as Chief Financial Officer for Old London Foods, Inc., a producer of branded crackers and co-packed private label bread crumbs, from July 1997 until August 2007. From September 2007 to December 2007, Mr. Brown was self-employed as a financial consultant. Mr. Brown received an M.B.A. in Finance from the University of Chicago in 1979 and a B.A. in Economics (Morehead Scholarship) from the University of North Carolina in 1977.

(c) Identification of Certain Significant Employees

None.

(d) Family Relationships

Mr. Kins and Mr. Brown are brothers-in-law.

(e) Business Experience

See Item 10(a) and (b) above.

(f) Involvement in Certain Legal Proceedings

None.

(g) Section 16(a) Beneficial Ownership Reporting Compliance

None

(h) Code of Ethics

The Series has no employees, officers or directors and is managed by the Sponsor. The Sponsor has adopted an Executive Code of Ethics that applies to its principal executive officers, principal financial officer and principal accounting officer. A copy of this Executive Code of Ethics may be obtained at no charge by written request to AlphaMetrix, LLC, 181 West Madison, Suite 3825, Chicago, Illinois 60602.

(i) Audit Committee Financial Expert

Because the Series has no employees, officers or directors, the Series has no audit committee. The Series is managed by the Sponsor. George Brown serves as the Sponsor’s “audit committee financial expert.” George Brown is not independent of the management of the Sponsor. The Sponsor is a privately owned limited liability company. It has no independent directors.

Item 11: Executive Compensation

The Series has no directors, officers or employees. None of the directors, officers or employees of the Sponsor receive compensation from the Series. The Sponsor receives a monthly sponsor fee of 0.02083 of 1% (equivalent to an annual rate of approximately 0.25%) of the Series’ month-end net asset value for all other purposes, including interest income, of a Member’s investment in the Series for such month. The officers of the Sponsor receive no “other compensation” from the Series. There are no compensation plans or arrangements relating to a change in control of any of the Series, the Platform or the Sponsor.

18

| Item 12: | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

(a) Security Ownership of Certain Beneficial Owners

Not applicable. All of the Platform’s manager interest is held by the Sponsor.

(b) Security Ownership of Management

As of December 31, 2008, the Trading Advisor and the executive officers and the principals of the Sponsor did not own directly or indirectly any Units. As of December 31, 2008, the Sponsor owned directly 8.120 Units, which constituted 0.02% of the total Units outstanding, and did not own any Units indirectly.

(c) Changes in Control

None.

(d) Securities Authorized for Issuance Under Equity Compensation Plans

None.

(a) Transactions With Related Persons

See Item 11 “Executive Compensation,” Item 12 “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters,” and “Item 1(c) “Narrative Description of Business.” As of December 31, 2008, the Series had paid the following: brokerage commissions of $224,145 to the Clearing Broker and UBS AG, the prime broker, of which Dekla Financial , LLC (“Dekla” or the “Introducing Broker”) received $35,480; Sponsor’s fees of $118,012 to the Sponsor; and selling commissions and placement fees of $944,092 and $681,006, respectively, to UBS FS.

The Introducing Broker is an affiliate of the Sponsor, is registered with the CFTC as an “introducing broker”, and began acting as the introducing broker for the Series’ futures and forward transactions effective November 1, 2008. The existing terms and amount of brokerage commissions charged related to the trading activities of the Series will not change, nor will the cost to the Series for utilizing the Introducing Broker.. For this service, the Introducing Broker receives a portion of the brokerage commissions paid to the Clearing Broker by the Series (depending on the contracts traded). The Introducing Broker will in no case hold the assets of the Series. The Sponsor negotiates the per-transaction rates at which such brokerage commissions are paid. The Introducing Broker does not currently, but may in the future, receive a portion of the forward currency trading bid-ask spreads and the exchange for physicals (“EFP”) spreads paid by the Series, and the Sponsor will negotiate such bid-ask spreads. The Sponsor negotiates the interest rates paid by the Clearing Broker on the Series’ assets, and the Introducing Broker may receive a substantial portion of the interest income generated by such assets. In addition, the Series pays UBS bid-ask spreads on forward currency trades. The Series also pays the Clearing Broker interest on short-term loans extended by the Clearing Broker to cover losses on non-US currency positions. The Clearing Broker and its affiliates have derived certain economic benefits from possession of a portion of the Series’ assets, as well as from foreign exchange and EFP trading, and some of the financial benefit of holding these assets, including the Introducing Broker.

The Sponsor controls the management of the Series and serves as its sponsor. Although the Sponsor will not sell any assets, directly or indirectly, to the Series, affiliates of the Sponsor will make substantial profits from the Series due to the foregoing arrangements. No loans have been, are or will be, outstanding between the Sponsor or any of its principals and the Series.

(b) Review, Approval or Ratification of Transactions with Related Persons

19

None of the fees paid by the Series to the Introducing Broker, an affiliate of the Sponsor, have been or will be negotiated, and they may be higher than would have been obtained in arm’s-length bargaining. Due to the fact that many of the parties involved in the operation of the Platform are affiliated with UBS MFS, the former sponsor, many of the business terms of the Platform and the Series were not negotiated at arm’s length.

(c) Director Independence

The Series does not have directors. None of the directors of the Sponsor are independent. See Item 10(a) and (b) “Identification of Directors and Executive Officers.”

(1) Audit Fees

Aggregate fees billed for professional services rendered by Ernst and Young LLP in connection with the audit of the Series’ financial statements and reviews of financial statements included in the Series’ Form 10-Q or for services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements as of and for the year ended December 31, 2008 were $147,000. Aggregate fees billed for these services for the year ended December 31, 2007 were $98,000 and for the period from October 26, 2006 (Date of Organization) to December 31, 2006 were $8,000.

(2) Audit-Related Fees

There were no fees for audit related services rendered by Ernst and Young LLP for the year ended December 31, 2008 related to the Series.

(3) Tax Fees

Aggregate fees billed for professional services rendered by Ernst & Young LLP in connection with tax compliance, tax advice and tax planning for the year ended December 31, 2008, were approximately $42,000.

(4) All Other Fees

No fees were incurred by Ernst and Young LLP, or any member firms of Ernst and Young LLP and their respective affiliates, during the period ended December 31, 2008 for any other professional services in relation to the Series.

(5) Pre-Approval Policies

The Sponsor’s executive officers review the estimated audit fees prior to engaging an auditor for the Series.

PART IV

(a)(1) Financial Statements

See Financial Statements filed herewith as Exhibit 13.01.

Affirmation of AlphaMetrix, LLC.

Report of Independent Registered Public Accounting Firm

Statements of Financial Condition

Statements of Operations

20

Statements of Changes in Members’ Capital

Condensed Schedules of Investments

Notes to Financial Statements

(a)(2) Financial Statement Schedules

Financial statement schedules not included in this Form 10-K have been omitted because they are not required or are not applicable or because equivalent information has been included in the Financial Statements filed herewith as Exhibit 13.01 or notes thereto.

(a)(3) Exhibits Required by Item 601 of Regulation S-K

The following exhibits are included herewith.

| Exhibit Number | Description of Document |

| **1.1 | Selling Agreement. |

| *3.1 | Certificate of Formation of AlphaMetrix Managed Futures LLC. |

| ****4.1 | Amended and Restated Limited Liability Company Operating Agreement |

| ****4.2 | Amended and Restated Separate Series Agreement for the Series. |

| ****10.1 | Advisory Agreement. |

| ****10.2 | Representation Letter. |

| **10.3 | Administration Agreement. |

| *10.4 | Form of Customer Agreement. |

| **10.5 | Form of Subscription Agreement. |

| ***10.6 | Assignment Agreement |

| ****10.7 | General Assignment and Assumption Agreement |

| ****10.8 | Administration Agreement Assignment |

| 13.01 | 2008 Financial Statements and Report of Independent Registered Public Accounting Firm. |

| 21.1 | List of Subsidiaries. |

| 31.1 | Certification of Principal Executive Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934. |

| 31.2 | Certification of Principal Financial Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934. |

| 32.1 | Certification of Principal Executive Officer pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

| 32.2 | Certification of Principal Financial Officer pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

* Incorporated by reference to the Series’ Form 10/A previously filed on November 2, 2006.

** Incorporated by reference to the Series’ Form 10/A previously filed on January 30, 2007.

*** Incorporated by reference to the Series’ Form 8-K previously filed on October 1, 2008.

**** Incorporated by reference to the Series’ Form 8-K previously filed on November 6, 2008.

21

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized on the 27th day of March, 2009.

Dated: March 27, 2009

ALPHAMETRIX MANAGED FUTURES LLC (ASPECT SERIES)

By: AlphaMetrix, LLC.

Sponsor

| By: /s/ Aleks Kins |

Name: Aleks Kins

Title: President and Chief Executive Officer

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the Sponsor of the registrant in the capacities and on the date indicated.

| Signature | Title with Managing Owner | Date | ||

| /s/ George Brown | Chief Financial Officer | March 27, 2009 | ||

| George Brown | ||||

| /s/ Dennis Zarr | Chief Operations Officers | March 27, 2009 | ||

| Dennis Zarr | ||||

AlphaMetrix, LLC

Sponsor of Registrant

March 27, 2009

S-1

Exhibit Index

| Exhibit Number | Description of Document |

| **1.1 | Selling Agreement. |

| *3.1 | Certificate of Formation of AlphaMetrix Managed Futures LLC. |

| ****4.1 | Amended and Restated Limited Liability Company Operating Agreement |

| ****4.2 | Amended and Restated Separate Series Agreement for the Series. |

| ****10.1 | Advisory Agreement. |

| ****10.2 | Representation Letter. |

| **10.3 | Administration Agreement. |

| *10.4 | Form of Customer Agreement. |

| **10.5 | Form of Subscription Agreement. |

| ***10.6 | Assignment Agreement |

| ****10.7 | General Assignment and Assumption Agreement |

| ****10.8 | Administration Agreement Assignment |

| 13.01 | 2008 Financial Statements and Report of Independent Registered Public Accounting Firm. |

| 21.1 | List of Subsidiaries. |

| 31.1 | Certification of Principal Executive Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934. |

| 31.2 | Certification of Principal Financial Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934. |

| 32.1 | Certification of Principal Executive Officer pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

| 32.2 | Certification of Principal Financial Officer pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

* Incorporated by reference to the Series’ Form 10/A previously filed on November 2, 2006.

** Incorporated by reference to the Series’ Form 10/A previously filed on January 30, 2007.

*** Incorporated by reference to the Series’ Form 8-K previously filed on October 1, 2008.

**** Incorporated by reference to the Series’ Form 8-K previously filed on November 6, 2008.

S-2