UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

NOTICE OF EXEMPT SOLICITATION

1. Name of the Registrant

The Charles Schwab Corporation

2. Name of person relying on exemption

Norges Bank

3. Address of person relying on exemption

Bankplassen 2

P.O. Box 1179 Sentrum

Oslo Q8 0107

4. Written Materials. Attach written material required to be submitted pursuant to Rule 14a-6(g)(1).

1

Proxy Access Proposals

Investor Presentation

March/April 2012

Runa Urheim, Vegard Torsnes

2

Outline

§ Government Pension Fund Global

§ Ownership activities

§ Proxy Access

§ Structure of NBIM’s proposals

§ Selected companies

3

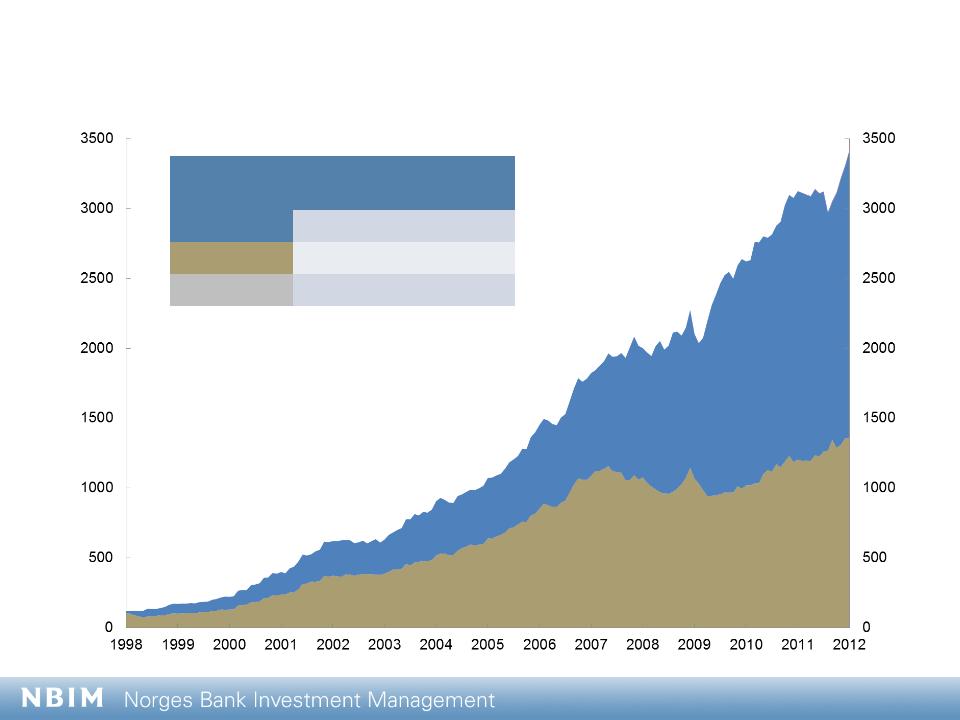

Government Pension Fund Global

4

Source: NBIM

2000 bn. 13 Oct 2008

3000 bn. 19 Oct 2010

1000 bn. Dec 2004

Asset class | Value | Percentage fund |

Equities | 1 945 | 58.7% |

Fixed Income | 1 356 | 41.0% |

Real Estate | 11 | 0.3% |

The fund’s market value

Billions of kroner, as of 31 December 2011

Billions of kroner, as of 31 December 2011

5

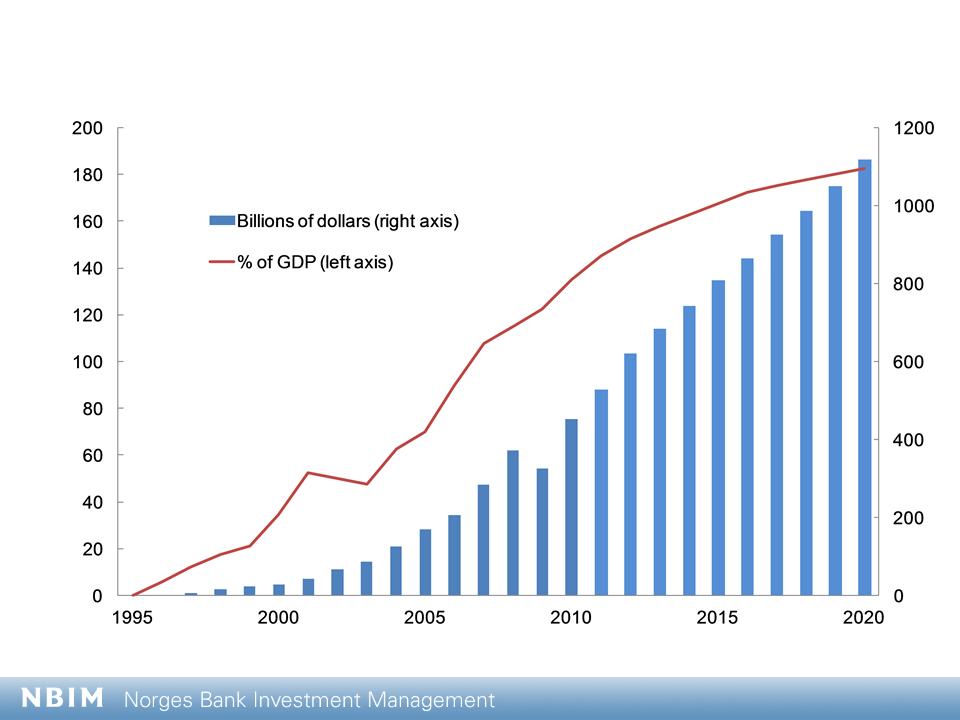

Sources: Ministry of Finance, National Budget 2012 and Norges Bank

Projected fund size

6

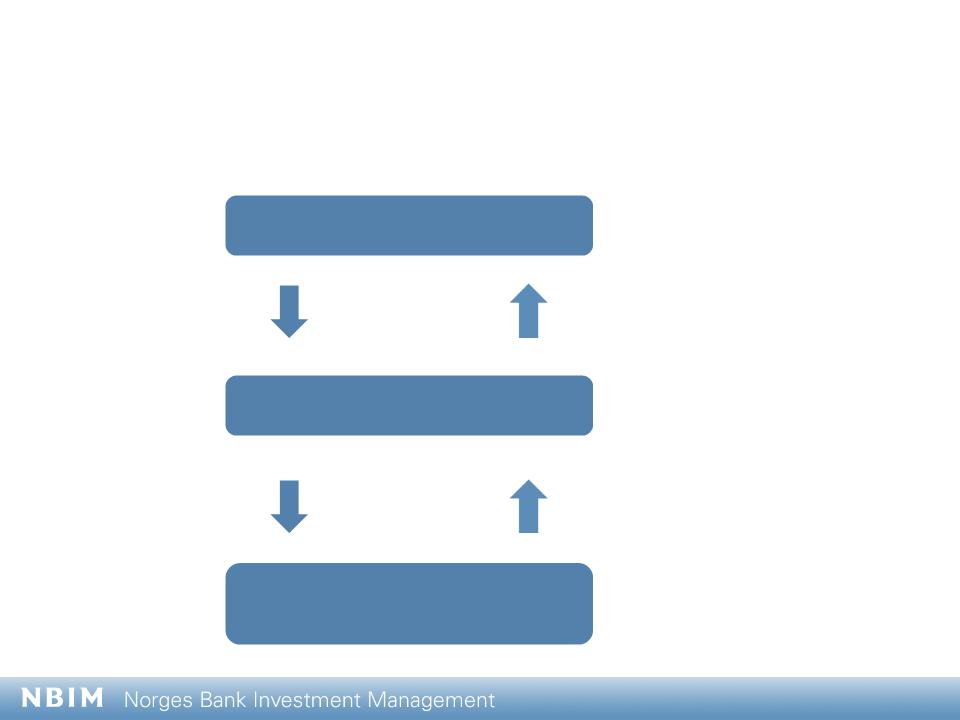

Governance structure

Stortinget (Norwegian Parliament)

Ministry of Finance

Norges Bank Executive Board

NBIM

• Government Pension Fund Act

• National Budget

• Annual white paper

• National Accounts

• Mandate

• Quarterly and annual

reports

• Investment strategy

advice

7

Mission and Strategy

To safeguard and build financial

wealth for Norway’s future generations

§ A respected, transparent and responsible manager

8

Source: NBIM

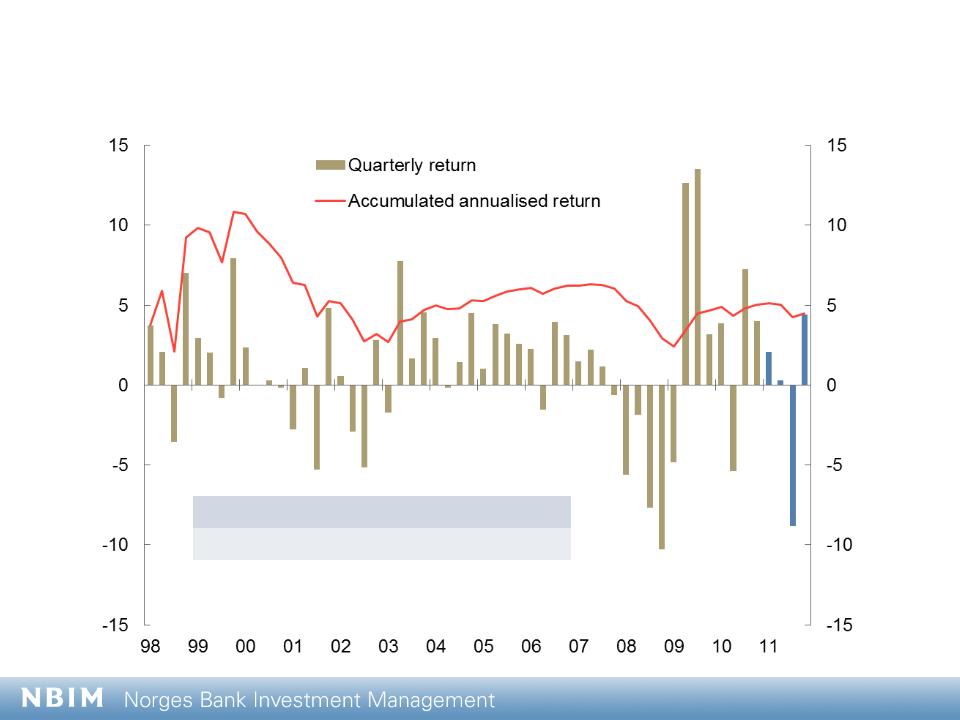

Return 2011 | - 2.5% |

Annualised since 1998 | 4.5% |

Quarterly and annualised absolute returns

Percent, measured in international currency

Percent, measured in international currency

9

Quarterly and annualised excess return*

Percentage points, measured in international currency

Percentage points, measured in international currency

Source: NBIM

Excess return 2011 | - 0.13% |

Annualised since 1998 | 0.28% |

*) Excluding real estate

10

Ownership activities

11

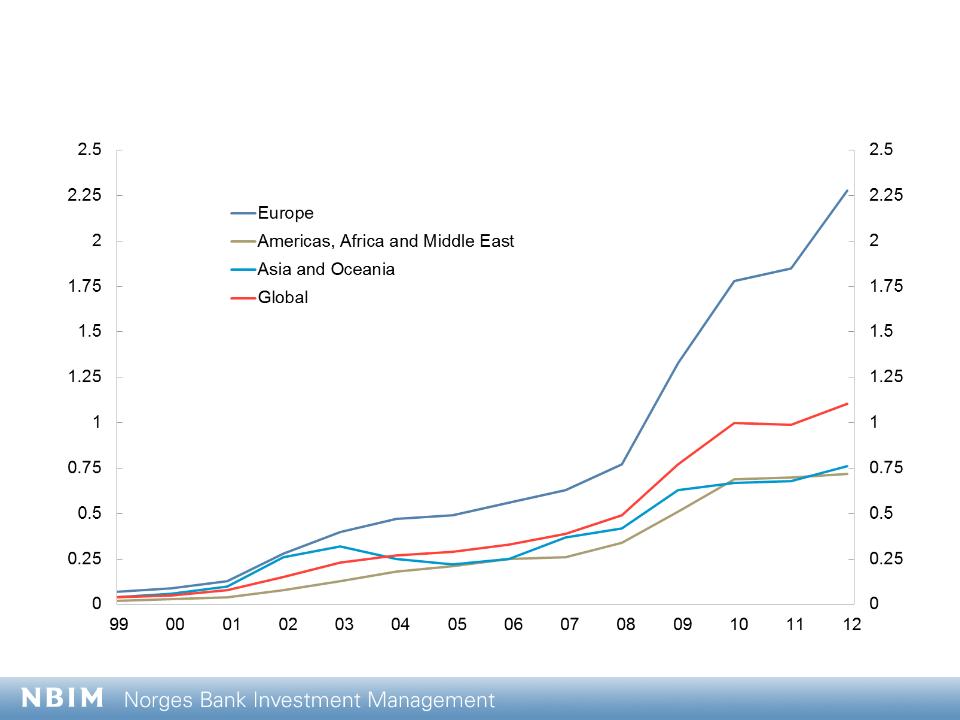

Ownership interest in equity markets

Percent of FTSE All Cap Index’s market capitalisation

Percent of FTSE All Cap Index’s market capitalisation

Source: FTSE, NBIM

12

Ownership focus areas

1. Equal treatment of shareholders

2. Shareholder influence and board

accountability

accountability

3. Well-functioning, legitimate and efficient

financial markets

financial markets

4. Climate change management

5. Water management

6. Children’s rights

13

1. Expectation documents

2. Dialogue with companies

3. Voting

4. Shareholder proposals

5. Contact with regulatory authorities

6. Public views

7. Legal action

Ownership tools

14

§ Annual and quarterly reports

§ Holding lists annually

§ Voting records annually

§ Real-time updated market

value on website

value on website

§ www.nbim.no

Transparency

15

Proxy Access

16

Shareholder nomination rights are fundamental

§ Fundamental principle of corporate governance

§ Will increase board accountability

§ The right to nominate is normally delegated to the board

§ It is crucial that shareholder can nominate candidates in special

circumstances

circumstances

§ A successful board should not fear Proxy Access

§ A nominee, regardless of proposer, must always be elected by

the general meeting

the general meeting

§ The general meeting will elect the nominee best suited to serve

the interests of all shareholders

the interests of all shareholders

17

NBIM’s motivations

§ NBIM has 108 bn USD (18%) of its assets in US equities

§ Proxy Access will lower our US investment risk

§ Long term returns depend on good corporate governance

§ Need for better board accountability in companies where

poor performance show an urgency of board changes

poor performance show an urgency of board changes

§ Shareholder proposals necessary in the absense of a

universal rule

universal rule

§ NBIM will continue to pursue a universal rule

18

Structure of NBIM’s proposals

19

Terms

§ Binding by-law changes

§ Enables shareholders to nominate candidates subject to

reasonable limitations

reasonable limitations

§ 1% ownership requirement

§ 1 year holding requirement

§ Max 25% of the board nominated by each nominator

§ Shareholders nominees can constitute max 25% of the board

20

A hypothetical board election

§ Company board has 12 seats

§ Any shareholder may nominate directors up to 25% of the board

seats. With 12 seats, this is a maximum of 3 nominees per

shareholder or shareholder group.

seats. With 12 seats, this is a maximum of 3 nominees per

shareholder or shareholder group.

§ The board nominates 12 candidates

§ Two shareholders or groups nominate 3 candidates each

§ The ballot will include 18 nominees, consisting of the 12

company nominees and the 6 shareholder nominees

company nominees and the 6 shareholder nominees

§ Each shareholder may vote FOR a maximum of 12 candidates

and against as many candidates he wants

and against as many candidates he wants

21

Example Vote Outcomes

§ If one shareholder nominee

receives more votes than the company nominee receiving the fewest votes, then

that shareholder nominee would be elected to the board along with the other 11

company nominees.

that shareholder nominee would be elected to the board along with the other 11

company nominees.

§ If 2 or 3 shareholder nominees

receive more votes than the company nominees receiving the fewest votes, then

those 2 or 3 shareholder nominees would be elected to the board along with the

10 or 9, respectively, company nominees who received greater shareholder

support.

those 2 or 3 shareholder nominees would be elected to the board along with the

10 or 9, respectively, company nominees who received greater shareholder

support.

§ HOWEVER, if 4 or more shareholder nominees

receive more votes than certain of the candidates nominated by the company, the

25% cap is triggered and ONLY the 3 shareholder nominees receiving the

greatest number of votes would be elected to the board. The resulting board,

therefore, would consist of the 3 shareholder nominated candidates who received

the greatest number of votes and the 9 company nominated candidates who

received the greatest number of votes.

25% cap is triggered and ONLY the 3 shareholder nominees receiving the

greatest number of votes would be elected to the board. The resulting board,

therefore, would consist of the 3 shareholder nominated candidates who received

the greatest number of votes and the 9 company nominated candidates who

received the greatest number of votes.

22

Selected companies

23

Wells Fargo

§ The Board has circumvented a shareholder proposal

§ The Board implemented a 25% capital requirement to call an EGM, in contradiction

to a 2011 shareholder proposal with a 10% threshold

to a 2011 shareholder proposal with a 10% threshold

§ The Board may amend bylaws without shareholder approval

§ A shareholder proposed amendment needs support of 50% of outstanding shares

§ The Board has authority to issue new preferred stock

§ Can potentially be used as a takeover defense

§ Combined roles of CEO and Chairman

§ Wells Fargo has failed to explain the re-nomination of directors

receiving relatively low shareholder support over several years

receiving relatively low shareholder support over several years

§ Directors should be assessed on how they have served shareholders across all

boards where they have been entrusted with a board seat

boards where they have been entrusted with a board seat

§ Low shareholder support expresses shareholder concerns on board accountability,

independence and transparency

independence and transparency

24

Staples

§ Board has circumvented shareholder proposals

§ Implemented a 25% capital requirement to call an EGM, in contradiction to a 2008

proposal with a 10% threshold receiving support of 67% of votes cast

proposal with a 10% threshold receiving support of 67% of votes cast

§ Despite majority support on written consent shareholder proposals in 2010 & 2011,

the Board has not implemented such right

the Board has not implemented such right

§ The Board may amend bylaws without shareholder

approval

approval

§ A shareholder proposed amendment needs support of 50% of outstanding shares

§ The Board has authority to issue new preferred stock

§ Can potentially be used as a takeover defense

§ Combined roles of CEO and Chairman

§ Staples currently is seeking to exclude NBIM’s proposal

25

Staples

§ Total share return inferior to peer group

§ As defined by Staples for executive compensation

Source: Factset

26

Western Union

§ Classified Board

§ Western Union has recently proposed declassification

§ Shareholders cannot convene an EGM

§ Shareholders cannot act by written consent

§ The Board may amend bylaws without shareholder

approval

approval

§ A shareholder proposed amendment needs support of 50% of outstanding

shares

shares

§ The Board has authority to issue new preferred stock

§ Can potentially be used as a takeover defense

§ In January 2012, the Company stated that the Board would

submit its own proxy access proposal for consideration by

shareholders, but has since changed its mind.

submit its own proxy access proposal for consideration by

shareholders, but has since changed its mind.

27

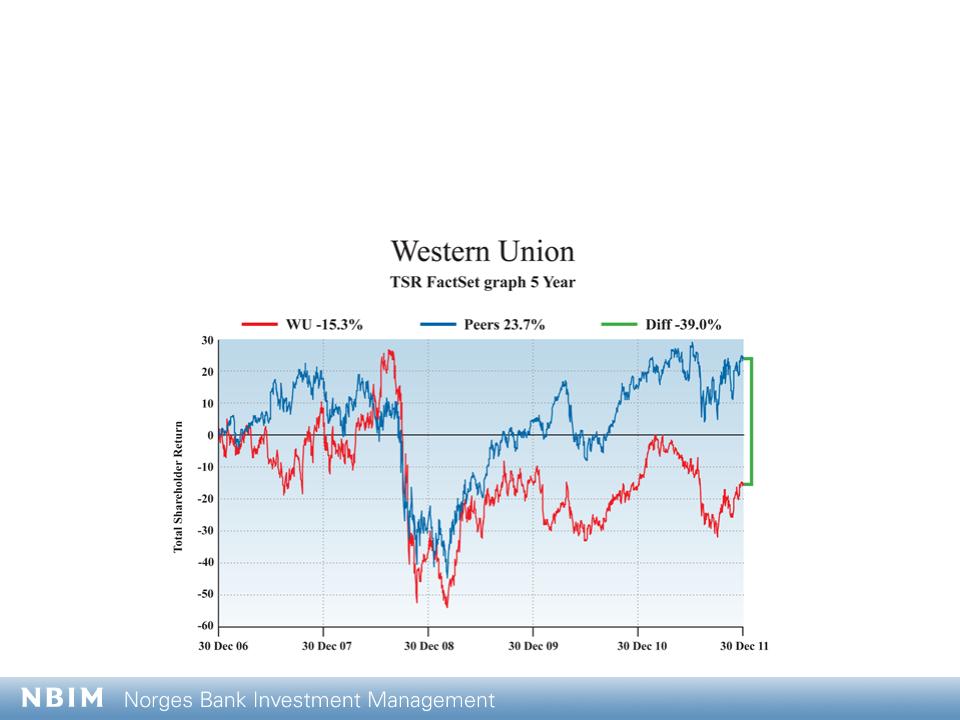

Western Union

§ Total share return inferior to peer group

§ As defined by Western Union for executive compensation

Source: Factset

28

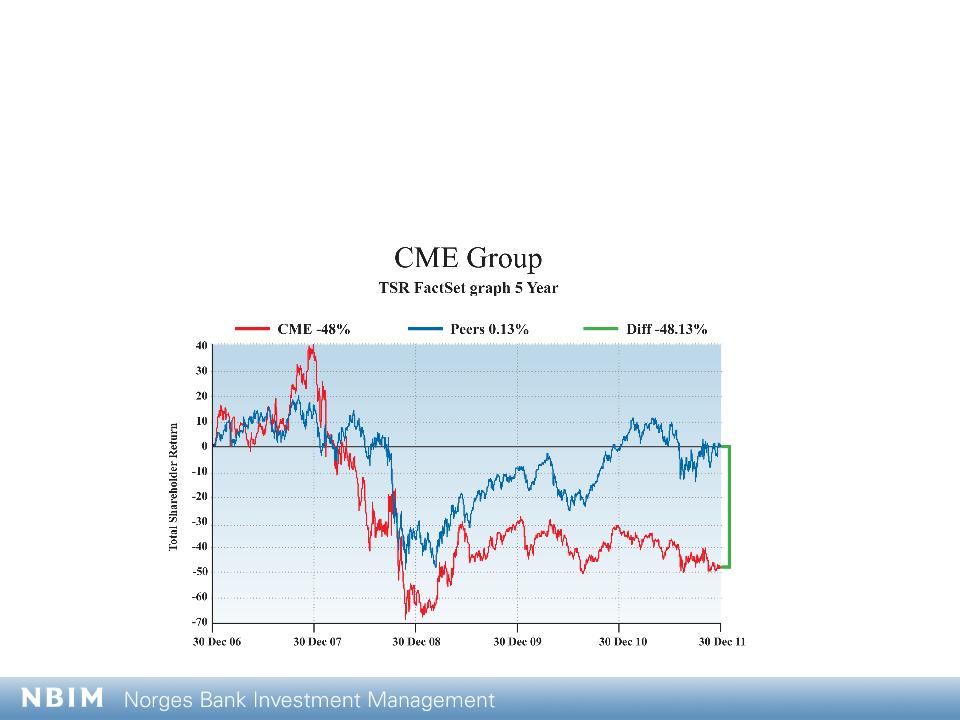

CME Group

§ Plurality voting standard for board elections

§ Classified Board

§ CME Group has recently proposed declassification

§ Large board with 32 directors

§ Several directors guaranteed re-nomination

§ Multiple share classes

§ Some with special board election rights

§ The Board has authority to issue new preferred stock

§ Can potentially be used as a takeover defense

§ Shareholders cannot convene an EGM

§ Shareholders cannot act by written consent

§ The Board may amend bylaws without shareholder approval

§ A shareholder proposed amendment needs support of 2/3 of outstanding shares

29

CME Group

§ Total share return inferior to peer group

§ As defined by CME Group for executive compensation

Source: Factset

30

Charles Schwab

§ Shareholders cannot convene an EGM

§ Shareholders cannot act by written consent

§ Classified Board

§ A 2011 shareholder proposal to declassify received 69 % support

§ Charles Schwab has recently proposed declassification

§ The Board may amend bylaws without shareholder

approval

approval

§ A shareholder proposed amendment needs support of 80% of outstanding shares

§ The Board has authority to issue new preferred stock

§ Can potentially be used as a takeover defense

31

Please do not send your proxy card to NBIM but return it to

the proxy-voting agent in the envelope that was or will be

provided to you by the respective company. NBIM is not able

to vote your proxies, nor does this communication

contemplate such an event. This communication is meant to

inform you about NBIM's proposals and to give you valuable

decision-making information when you review your

shareholder proxy for each of the 2012 annual meetings for

Wells Fargo & Company, Charles Schwab Corporation,

Western Union Company, CME Group, Inc., and Staples, Inc.

the proxy-voting agent in the envelope that was or will be

provided to you by the respective company. NBIM is not able

to vote your proxies, nor does this communication

contemplate such an event. This communication is meant to

inform you about NBIM's proposals and to give you valuable

decision-making information when you review your

shareholder proxy for each of the 2012 annual meetings for

Wells Fargo & Company, Charles Schwab Corporation,

Western Union Company, CME Group, Inc., and Staples, Inc.

Disclaimer

32