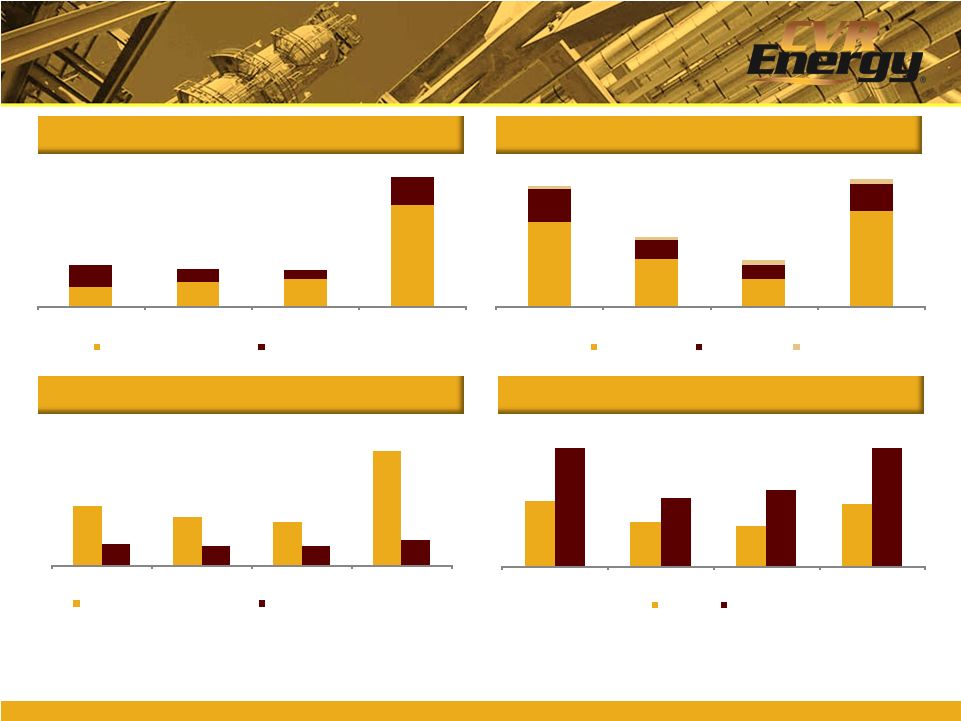

28 28 28 28 28 Non-GAAP Financial Measures (cont’d) EBITDA represents net income before the effect of interest expense, interest income, income tax expense (benefit) and depreciation and amortization. EBITDA is not a calculation based upon GAAP; however, the amounts included in EBITDA are derived from amounts included in the consolidated statement of operations of the Company. Adjusted EBITDA by operating segment results from operating income by segment adjusted for items that the company believes are needed in order to evaluate results in a more comparative analysis from period to period. Additional adjustments to EBITDA include major scheduled turnaround expense, the impact of the Company’s use of accounting for its inventory under first-in, first-out (FIFO), net unrealized gains/losses on derivative activities, share-based compensation expense, loss on extinguishment of debt, and other income (expense). Adjusted EBITDA is not a recognized term under GAAP and should not be substituted for operating income or net income as a measure of performance but should be utilized as a supplemental measure of financial performance in evaluating our business. EBITDA: The Company’s basis for determining inventory value on a GAAP basis. Changes in crude oil prices can cause fluctuations in the inventory valuation of our crude oil, work in process and finished goods, thereby resulting in favorable FIFO impacts when crude oil prices increase and unfavorable FIFO impacts when crude oil prices decrease. The FIFO impact is calculated based upon inventory values at the beginning of the accounting period and at the end of the accounting period. First-in, first-out (FIFO): |