USNG invests only in Futures Contracts and Other Natural Gas Related Investments that are traded in sufficient volume to permit, in the opinion of the General Partner, ease of taking and liquidating positions in these financial interests.

While natural gas Futures Contracts traded on the NYMEX can be physically settled, USNG does not intend to take or make physical delivery. However, USNG may from time to time trade in Other Natural Gas Related Investments, including contracts based on the spot price of natural gas.

While USNG’s historical ratio of margin to total assets has generally ranged from 5% to 10%, the General Partner endeavors to have the value of USNG’s Treasuries, cash and/or cash equivalents, whether held by USNG or posted as margin or collateral at all times, approximate the aggregate face value of USNG's obligations under its Futures Contracts and Other Natural Gas Related Investments.

Borrowings are not used by USNG, unless USNG is required to borrow money in the event of physical delivery, USNG trades in cash commodities, or for short-term needs created by unexpected redemptions. USNG maintains the value of its Treasuries, cash and/or cash equivalents whether held by USNG or posted as margin or collateral to at all times approximate the aggregate face value of its obligations under USNG's Futures Contracts and Other Natural Gas Related Investments. USNG has not established and does not plan to establish credit lines.

USNG has not and will not employ the technique, commonly known as pyramiding, in which the speculator uses unrealized profits on existing positions as variation margin for the purchase or sale of additional positions in the same or another commodity interest.

BBH&Co. is the registrar and transfer agent for the units. BBH&Co. is also the Custodian for USNG. In this capacity, BBH&Co. holds USNG’s Treasuries, cash and/or cash equivalents pursuant to a custodial agreement. In addition, BBH&Co. performs certain administrative and accounting services for USNG and prepares certain Securities and Exchange Commission ("SEC") and CFTC reports on behalf of USNG. The General Partner pays BBH&Co. a fee for these services.

USNG also employs a Marketing Agent. The General Partner pays the Marketing Agent a marketing fee of $425,000 per annum plus an incentive fee as follows: 0.00% on USNG’s assets from $0-500 million; 0.04% on USNG’s assets from $500 million-$4 billion; and 0.03% on USNG’s assets in excess of $4 billion; provided, however, that in no event may the aggregate compensation paid to the Marketing Agent and any affiliate of the General Partner for distribution-related services in connection with the offering of units exceed ten percent (10%) of the gross proceeds of the offering.

UBS Securities LLC (“UBS Securities”) is USNG’s futures commission merchant. USNG and UBS Securities have entered into an Institutional Futures Client Account Agreement. This Agreement requires UBS Securities to provide services to USNG in connection with the purchase and sale of Natural Gas Interests that may be purchased or sold by or through UBS Securities for USNG’s account. USNG pays the fees of UBS Securities.

UBS Securities’ principal business address is 677 Washington Blvd, Stamford, CT 06901. UBS Securities is a futures clearing broker for USNG. UBS Securities is registered in the U.S. with the Financial Industry Regulatory Authority ("FINRA") as a broker-dealer and with the CFTC as a futures commission merchant. UBS Securities is a member of various U.S. futures and securities exchanges.

UBS Securities was involved in the 2003 Global Research Analyst Settlement. This settlement was part of the global settlement that UBS Securities and nine other firms reached with the SEC, FINRA, New York Stock Exchange (the "NYSE") and various state regulators. As part of the settlement, UBS Securities agreed to pay $80,000,000 divided among retrospective relief, for procurement of independent research and for investor education. UBS Securities has also undertaken to adopt enhanced policies and procedures reasonably designed to address potential conflicts of interest arising from research practices.

UBS Securities acts only as clearing broker for USNG and, as such, is paid commissions for executing and clearing trades on behalf of USNG. UBS Securities neither acts in any supervisory capacity with respect to the General Partner nor participates in the management of the General Partner or USNG.

Currently, the General Partner does not employ commodity trading advisors. If, in the future, the General Partner does employ commodity trading advisors, it will choose each advisor based on arms-length negotiations and will consider the advisor’s experience, fees and reputation.

Form of Units

Registered Form. Units are issued in registered form in accordance with the LP Agreement. The Administrator has been appointed registrar and transfer agent for the purpose of transferring units in certificated form. The Administrator keeps a record of all holders of the units in the registry (the “Register”). The General Partner recognizes transfers of units in certificated form only if done in accordance with the LP Agreement. The beneficial interests in such units are held in book-entry form through participants and/or accountholders in the Depository Trust Company ("DTC").

Book Entry. Individual certificates are not issued for the units. Instead, units are represented by one or more global certificates, which are deposited by the Administrator with DTC and registered in the name of Cede & Co., as nominee for DTC. The global certificates evidence all of the units outstanding at any time. Unitholders are limited to (1) participants in DTC such as banks, brokers, dealers and trust companies ("DTC Participants"), (2) those who maintain, either directly or indirectly, a custodial relationship with a DTC Participant ("Indirect Participants"), and (3) those banks, brokers, dealers, trust companies and others who hold interests in the units through DTC Participants or Indirect Participants, in each case who satisfy the requirements for transfers of units. DTC Participants acting on behalf of investors holding units through such participants’ accounts in DTC follow the delivery practice applicable to securities eligible for DTC’s Same-Day Funds Settlement System. Units are credited to DTC Participants’ securities accounts following confirmation of receipt of payment.

DTC. DTC is a limited purpose trust company organized under the laws of the State of New York and is a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). DTC holds securities for DTC Participants and facilitates the clearance and settlement of transactions between DTC Participants through electronic book-entry changes in accounts of DTC Participants.

Transfer of Units

Transfers of Units Only Through DTC. The units are only transferable through the book-entry system of DTC. Limited partners who are not DTC Participants may transfer their units through DTC by instructing the DTC Participant holding their units (or by instructing the Indirect Participant or other entity through which their units are held) to transfer the units. Transfers are made in accordance with standard securities industry practice.

Transfers of interests in units with DTC are made in accordance with the usual rules and operating procedures of DTC and the nature of the transfer. DTC has established procedures to facilitate transfers among the participants and/or accountholders of DTC. Because DTC can only act on behalf of DTC Participants, who in turn act on behalf of Indirect Participants, the ability of a person or entity having an interest in a global certificate to pledge such interest to persons or entities that do not participate in DTC, or otherwise take actions in respect of such interest, may be affected by the lack of a definitive security in respect of such interest.

DTC has advised us that it takes any action permitted to be taken by a unitholder (including, without limitation, the presentation of a global certificate for exchange) only at the direction of one or more DTC Participants in whose account with DTC interests in global certificates are credited and only in respect of such portion of the aggregate principal amount of the global certificate as to which such DTC Participant or Participants has or have given such direction.

Transfer/Application Requirements. All purchasers of USNG’s units, and potentially any purchasers of units in the future, who wish to become limited partners or other record holders and receive cash distributions, if any, or have certain other rights, must deliver an executed transfer application in which the purchaser or transferee must certify that, among other things, he, she or it agrees to be bound by USNG’s LP Agreement and is eligible to purchase USNG’s securities. Each purchaser of units must execute a transfer application and certification. The obligation to provide the form of transfer application is imposed on the seller of units or, if a purchase of units is made through an exchange, the form may be obtained directly through USNG. Further, the General Partner may request each record holder to furnish certain information, including that holder’s nationality, citizenship or other related status. A record holder is a unitholder that is, or has applied to be, a limited partner. An investor who is not a U.S. resident may not be eligible to become a record holder or one of the USNG’s limited partners if that investor’s ownership would subject USNG to the risk of cancellation or forfeiture of any of USNG’s assets under any federal, state or local law or regulation. If the record holder fails to furnish the information or if the General Partner determines, on the basis of the information furnished by the holder in response to the request, that such holder is not qualified to become one of USNG’s limited partners, the General Partner may be substituted as a holder for the record holder, who will then be treated as a non-citizen assignee, and USNG will have the right to redeem those securities held by the record holder.

A transferee’s broker, agent or nominee may complete, execute and deliver a transfer application and certification. USNG may, at its discretion, treat the nominee holder of a unit as the absolute owner. In that case, the beneficial holder’s rights are limited solely to those that it has against the nominee holder as a result of any agreement between the beneficial owner and the nominee holder.

A person purchasing USNG’s existing units, who does not execute a transfer application and certify that the purchaser is eligible to purchase those securities acquires no rights in those securities other than the right to resell those securities. Whether or not a transfer application is received or the consent of the General Partner obtained, USNG's units are securities and are transferable according to the laws governing transfers of securities.

Any transfer of units will not be recorded by the transfer agent or recognized by the General Partner unless a completed transfer application is delivered to the General Partner or the Administrator. When acquiring units, the transferee of such units that completes a transfer application will:

· be an assignee until admitted as a substituted limited partner upon the consent and sole discretion of the General Partner and the recording of the assignment on the books and records of the partnership;

· automatically request admission as a substituted limited partner;

· agree to be bound by the terms and conditions of, and execute, the LP Agreement;

· represent that such transferee has the capacity and authority to enter into the LP Agreement;

· grant powers of attorney to the General Partner and any liquidator of USNG; and

· make the consents and waivers contained in the LP Agreement.

An assignee will become a limited partner in respect of the transferred units upon the consent of the General Partner and the recordation of the name of the assignee on our books and records. Such consent may be withheld in the sole discretion of the General Partner.

If consent of the General Partner is withheld, such transferee shall be an assignee. An assignee shall have an interest in the partnership equivalent to that of a limited partner with respect to allocations and distributions, including, without limitation, liquidating distributions, of the partnership. With respect to voting rights attributable to units that are held by assignees, the General Partner shall be deemed to be the limited partner with respect thereto and shall, in exercising the voting rights in respect of such units on any matter, vote such units at the written direction of the assignee who is the recordholder of such units. If no such written direction is received, such units will not be voted. An assignee shall have no other rights of a limited partner.

Until a unit has been transferred on USNG's books, we and the transfer agent may treat the record holder of the unit as the absolute owner for all purposes, except as otherwise required by law or stock exchange regulations.

Withdrawal of Limited Partners

As discussed in the LP Agreement, if the General Partner gives at least fifteen (15) days’ written notice to a limited partner, then the General Partner may for any reason, in its sole discretion, require any such limited partner to withdraw entirely from the partnership or to withdraw a portion of its partner capital account. If the General Partner does not give at least fifteen (15) days’ written notice to a limited partner, then it may only require withdrawal of all or any portion of the capital account of any limited partner in the following circumstances: (i) the unitholder made a misrepresentation to the General Partner in connection with its purchase of units; or (ii) the limited partner’s ownership of units would result in the violation of any law or regulations applicable to the partnership or a partner. In these circumstances, the General Partner without notice may require the withdrawal at any time, or retroactively. The limited partner thus designated shall withdraw from the partnership or withdraw that portion of its partner capital account specified, as the case may be, as of the close of business on such date as determined by the General Partner. The limited partner thus designated shall be deemed to have withdrawn from the partnership or to have made a partial withdrawal from its partner capital account, as the case may be, without further action on the part of the limited partner and the provisions of the LP Agreement shall apply. Calculating NAV

USNG’s NAV is calculated by:

| | · | Taking the current market value of its total assets |

| | · | Subtracting any liabilities |

The Administrator calculates the NAV of USNG once each trading day. The NAV for a particular trading day is released after 4:15 p.m. New York time. It calculates the NAV as of the earlier of the close of the NYSE or 4:00 p.m. New York time. Trading on the AMEX typically closes at 4:15 p.m. New York time. USNG uses the NYMEX closing price (determined at the earlier of the close of the NYMEX or 2:30 p.m. New York time) for the contracts held on the NYMEX, but calculates or determines the value of all other USNG investments as of the earlier of the close of the NYSE or 4:00 p.m. New York time.

In addition, in order to provide updated information relating to USNG for use by investors and market professionals, the AMEX calculates and disseminates throughout the trading day an updated indicative fund value. The indicative fund value is calculated by using the prior day’s closing NAV per unit of USNG as a base and updating that value throughout the trading day to reflect changes in the most recently reported trade price for the Benchmark Futures Contracts on the NYMEX. The prices reported for the active Benchmark Futures Contract month are adjusted based on the prior day’s spread differential between settlement values for that contract and the spot month contract. In the event that the spot month contract is also the active contract, the last sale price for the active contract is not adjusted. The indicative fund value unit basis disseminated during AMEX trading hours should not be viewed as an actual real time update of the NAV, because the NAV is calculated only once at the end of each trading day.

The indicative fund value is disseminated on a per unit basis every 15 seconds during regular AMEX trading hours of 9:30 a.m. New York time to 4:15 p.m. New York time. The normal trading hours of the NYMEX are 10:00 a.m. New York time to 2:30 p.m. New York time. This means that there is a gap in time at the beginning and the end of each day during which USNG’s units are traded on the AMEX, but real-time NYMEX trading prices for futures contracts traded on the NYMEX are not available. As a result, during those gaps there is no update to the indicative fund value.

The AMEX disseminates the indicative fund value through the facilities of CTA/CQ High Speed Lines. In addition, the indicative fund value is published on the AMEX's website and is available through on-line information services such as Bloomberg and Reuters.

Dissemination of the indicative fund value provides additional information that is not otherwise available to the public and is useful to investors and market professionals in connection with the trading of USNG units on the AMEX. Investors and market professionals are able throughout the trading day to compare the market price of USNG and the indicative fund value. If the market price of USNG units diverges significantly from the indicative fund value, market professionals have an incentive to execute arbitrage trades. For example, if USNG appears to be trading at a discount compared to the indicative fund value, a market professional could buy USNG units on the AMEX and sell short futures contracts. Such arbitrage trades can tighten the tracking between the market price of USNG and the indicative fund value and thus can be beneficial to all market participants.

In addition, other Futures Contracts, Other Natural Gas Related Investments and Treasuries held by USNG are valued by the Administrator, using rates and points received from client approved third party vendors (such as Reuters and WM Company) and advisor quotes. These investments are not included in the indicative value. The indicative fund value is based on the prior day’s NAV and moves up and down solely according to changes in the average of the prices of the Benchmark Futures Contracts for natural gas traded on the NYMEX.

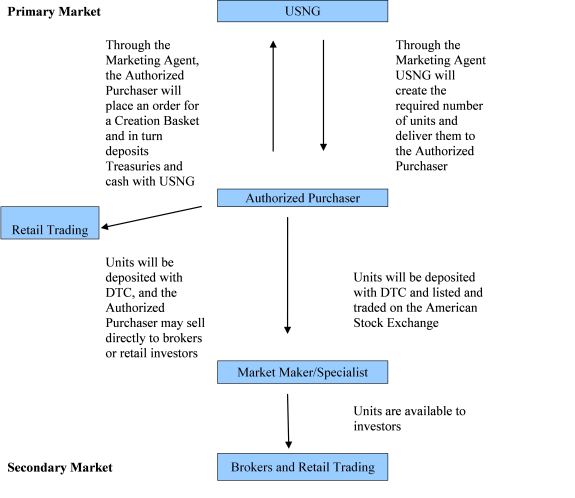

Creation and Redemption of Units

USNG creates and redeems units from time to time, but only in one or more Creation Baskets or Redemption Baskets. The creation and redemption of baskets are only made in exchange for delivery to USNG or the distribution by USNG of the amount of Treasuries and any cash represented by the baskets being created or redeemed, the amount of which is based on the combined NAV of the number of units included in the baskets being created or redeemed determined as of 4:00 p.m. New York time on the day the order to create or redeem baskets is properly received.

Authorized Purchasers are the only persons that may place orders to create and redeem baskets. Authorized Purchasers must be (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, that are not required to register as broker-dealers to engage in securities transactions as described below, and (2) DTC Participants. To become an Authorized Purchaser, a person must enter into an Authorized Purchaser Agreement with the General Partner. The Authorized Purchaser Agreement provides the procedures for the creation and redemption of baskets and for the delivery of the Treasuries and any cash required for such creations and redemptions. The Authorized Purchaser Agreement and the related procedures attached thereto may be amended by USNG, without the consent of any limited partner or unitholder or Authorized Purchaser. Authorized Purchasers pay a transaction fee of $1,000 to USNG for each order they place to create or redeem one or more baskets. Authorized Purchasers who make deposits with USNG in exchange for baskets receive no fees, commissions or other form of compensation or inducement of any kind from either USNG or the General Partner, and no such person has any obligation or responsibility to the General Partner or USNG to effect any sale or resale of units. As of December 31, 2007, 4 Authorized Purchasers had entered into agreements with USNG to purchase Creation Baskets.

Certain Authorized Purchasers are expected to have the facility to participate directly in the physical natural gas market and the natural gas futures market. In some cases, an Authorized Purchaser or its affiliates may from time to time acquire natural gas or sell natural gas and may profit in these instances. The General Partner believes that the size and operation of the natural gas market make it unlikely that an Authorized Purchaser’s direct activities in the natural gas or securities markets will impact the price of natural gas, Futures Contracts, or the price of the units.

Each Authorized Purchaser is required to be registered as a broker-dealer under the Exchange Act and is a member in good standing with FINRA, or exempt from being or otherwise not required to be licensed as a broker-dealer or a member of FINRA, and qualified to act as a broker or dealer in the states or other jurisdictions where the nature of its business so requires. Certain Authorized Purchasers may also be regulated under federal and state banking laws and regulations. Each Authorized Purchaser has its own set of rules and procedures, internal controls and information barriers as it determines is appropriate in light of its own regulatory regime.

Under the Authorized Purchaser Agreement, the General Partner has agreed to indemnify the Authorized Purchasers against certain liabilities, including liabilities under the Securities Act of 1933, as amended, and to contribute to the payments the Authorized Purchasers may be required to make in respect of those liabilities.

The following description of the procedures for the creation and redemption of baskets is only a summary and an investor should refer to the relevant provisions of the LP Agreement and the form of Authorized Purchaser Agreement for more detail, each of which is attached as an exhibit to this annual report on Form 10-K.

Creation Procedures

On any business day, an Authorized Purchaser may place an order with the Marketing Agent to create one or more baskets. For purposes of processing purchase and redemption orders, a “business day” means any day other than a day when any of the AMEX, the NYMEX or the NYSE is closed for regular trading. Purchase orders must be placed by 12:00 p.m. New York time or the close of regular trading on the NYSE, whichever is earlier; except in the case of the initial Authorized Purchaser’s or any other Authorized Purchaser’s initial order to purchase one or more Creation Baskets on the first day the baskets are to be offered and sold, when such orders shall be placed by 9:00 a.m. New York time on the day agreed to by the General Partner and the initial Authorized Purchaser. The day on which the Marketing Agent receives a valid purchase order is the purchase order date.

By placing a purchase order, an Authorized Purchaser agrees to deposit Treasuries, cash or a combination of Treasuries and cash with USNG, as described below. Prior to the delivery of baskets for a purchase order, the Authorized Purchaser must also have wired to the Custodian the non-refundable transaction fee due for the purchase order. Authorized Purchasers may not withdraw a creation request.

Determination of Required Deposits

The total deposit required to create each basket (“Creation Basket Deposit”) is the amount of Treasuries and/or cash that is in the same proportion to the total assets of USNG (net of estimated accrued but unpaid fees, expenses and other liabilities) on the date the order to purchase is accepted as the number of units to be created under the purchase order is in proportion to the total number of units outstanding on the date the order is received. The General Partner determines, directly in its sole discretion or in consultation with the Administrator, the requirements for Treasuries and the amount of cash, including the maximum permitted remaining maturity of a Treasury and proportions of Treasury and cash that may be included in deposits to create baskets. The Marketing Agent publishes such requirements at the beginning of each business day. The amount of cash deposit required is the difference between the aggregate market value of the Treasuries required to be included in a Creation Basket Deposit as of 4:00 p.m. New York time on the date the order to purchase is properly received and the total required deposit.

Delivery of Required Deposits

An Authorized Purchaser who places a purchase order is responsible for transferring to USNG’s account with the Custodian the required amount of Treasuries and cash by the end of the third business day following the purchase order date. Upon receipt of the deposit amount, the Administrator directs DTC to credit the number of baskets ordered to the Authorized Purchaser’s DTC account on the third business day following the purchase order date. The expense and risk of delivery and ownership of Treasuries until such Treasuries have been received by the Custodian on behalf of USNG is borne solely by the Authorized Purchaser.

Because orders to purchase baskets must be placed by 12:00 p.m., New York time, but the total payment required to create a basket during the continuous offering period will not be determined until 4:00 p.m., New York time, on the date the purchase order is received, Authorized Purchasers will not know the total amount of the payment required to create a basket at the time they submit an irrevocable purchase order for the basket. USNG’s NAV and the total amount of the payment required to create a basket could rise or fall substantially between the time an irrevocable purchase order is submitted and the time the amount of the purchase price in respect thereof is determined.

Rejection of Purchase Orders

The General Partner acting by itself or through the Marketing Agent may reject a purchase order or a Creation Basket Deposit if:

| · | it determines that the investment alternative available to USNG at that time will not enable it to meet its investment objective; |

| · | it determines that the purchase order or the Creation Basket Deposit is not in proper form; |

| · | it believes that the purchase order or the Creation Basket Deposit would have adverse tax consequences to USNG or its unitholders; |

| · | the acceptance or receipt of the Creation Basket Deposit would, in the opinion of counsel to the General Partner, be unlawful; or |

| · | circumstances outside the control of the General Partner, Marketing Agent or Custodian make it, for all practical purposes, not feasible to process creations of baskets. |

None of the General Partner, Marketing Agent or Custodian will be liable for the rejection of any purchase order or Creation Basket Deposit.

Redemption Procedures

The procedures by which an Authorized Purchaser can redeem one or more baskets mirror the procedures for the creation of baskets. On any business day, an Authorized Purchaser may place an order with the Marketing Agent to redeem one or more baskets. Redemption orders must be placed by 12:00 p.m. New York time or the close of regular trading on the NYSE, whichever is earlier. A redemption order so received will be effective on the date it is received in satisfactory form by the Marketing Agent. The redemption procedures allow Authorized Purchasers to redeem baskets and do not entitle an individual unitholder to redeem any units in an amount less than a Redemption Basket, or to redeem baskets other than through an Authorized Purchaser. By placing a redemption order, an Authorized Purchaser agrees to deliver the baskets to be redeemed through DTC’s book-entry system to USOF not later than 3:00 p.m. New York time on the third business day following the effective date of the redemption order. Prior to the delivery of the redemption distribution for a redemption order, the Authorized Purchaser must also have wired to USOF’s account at the Custodian the non-refundable transaction fee due for the redemption order. Authorized Purchasers may not withdraw a redemption request.

Determination of Redemption Distribution

The redemption distribution from USNG consists of a transfer to the redeeming Authorized Purchaser of an amount of Treasuries and/or cash that is in the same proportion to the total assets of USNG (net of estimated accrued but unpaid fees, expenses and other liabilities) on the date the order to redeem is properly received as the number of units to be redeemed under the redemption order is in proportion to the total number of units outstanding on the date the order is received. The General Partner, directly or in consultation with the Administrator, determines the requirements for Treasuries and the amounts of cash, including the maximum permitted remaining maturity of a Treasury, and the proportions of Treasuries and cash that may be included in distributions to redeem baskets. The Marketing Agent publishes such requirements as of 4:00 p.m. New York time on the redemption order date.

Delivery of Redemption Distribution

The redemption distribution due from USNG will be delivered to the Authorized Purchaser by 3:00 p.m. New York time on the third business day following the redemption order date if, by 3:00 p.m. New York time on such third business day, USNG’s DTC account has been credited with the baskets to be redeemed. If USNG’s DTC account has not been credited with all of the baskets to be redeemed by such time, the redemption distribution will be delivered to the extent of whole baskets received. Any remainder of the redemption distribution will be delivered on the next business day to the extent of remaining whole baskets received if USNG receives the fee applicable to the extension of the redemption distribution date which the General Partner may, from time to time, determine and the remaining baskets to be redeemed are credited to USNG’s DTC account by 3:00 p.m. New York time on such next business day. Any further outstanding amount of the redemption order shall be cancelled. Pursuant to information from the General Partner, the Custodian will also be authorized to deliver the redemption distribution notwithstanding that the baskets to be redeemed are not credited to USNG’s DTC account by 3:00 p.m. New York time on the third business day following the redemption order date if the Authorized Purchaser has collateralized its obligation to deliver the baskets through DTC’s book entry-system on such terms as the General Partner may from time to time determine.

Suspension or Rejection of Redemption Orders

The General Partner may, in its discretion, suspend the right of redemption, or postpone the redemption settlement date, (1) for any period during which the AMEX or the NYMEX is closed other than customary weekend or holiday closings, or trading on the AMEX or the NYMEX is suspended or restricted, (2) for any period during which an emergency exists as a result of which delivery, disposal or evaluation of Treasuries is not reasonably practicable, or (3) for such other period as the General Partner determines to be necessary for the protection of the limited partners. None of the General Partner, the Marketing Agent, the Administrator, or the Custodian will be liable to any person or in any way for any loss or damages that may result from any such suspension or postponement.

The General Partner will reject a redemption order if the order is not in proper form as described in the Authorized Purchaser Agreement or if the fulfillment of the order, in the opinion of its counsel, might be unlawful.

Creation and Redemption Transaction Fee

To compensate USNG for its expenses in connection with the creation and redemption of baskets, an Authorized Purchaser is required to pay a transaction fee to USNG of $1,000 per order to create or redeem baskets. An order may include multiple baskets. The transaction fee may be reduced, increased or otherwise changed by the General Partner. The General Partner shall notify DTC of any change in the transaction fee and will not implement any increase in the fee for the redemption of baskets until 30 days after the date of the notice.

Tax Responsibility

Authorized Purchasers are responsible for any transfer tax, sales or use tax, stamp tax, recording tax, value added tax or similar tax or governmental charge applicable to the creation or redemption of baskets, regardless of whether or not such tax or charge is imposed directly on the Authorized Purchaser, and agree to indemnify the General Partner and USNG if they are required by law to pay any such tax, together with any applicable penalties, additions to tax or interest thereon.

Secondary Market Transactions

As discussed above, Authorized Purchasers are the only persons that may place orders to create and redeem baskets. Authorized Purchasers must be registered broker-dealers or other securities market participants, such as banks and other financial institutions that are not required to register as broker-dealers to engage in securities transactions. An Authorized Purchaser is under no obligation to create or redeem baskets, and an Authorized Purchaser is under no obligation to offer to the public units of any baskets it does create. Authorized Purchasers that do offer to the public units from the baskets they create do so at per-unit offering prices that are expected to reflect, among other factors, the trading price of the units on the AMEX, the NAV of USNG at the time the Authorized Purchaser purchased the Creation Baskets and the NAV at the time of the offer of the units to the public, the supply of and demand for units at the time of sale, and the liquidity of the Futures Contract market and the market for Other Natural Gas Related Investments. The prices of units offered by Authorized Purchasers are expected to fall between USNG’s NAV and the trading price of the units on the AMEX at the time of sale. Units initially comprising the same basket but offered by Authorized Purchasers to the public at different times may have different offering prices. An order for one or more baskets may be placed by an Authorized Purchaser on behalf of multiple clients. Authorized Purchasers who make deposits with USNG in exchange for baskets receive no fees, commissions or other form of compensation or inducement of any kind from either USNG or the General Partner, and no such person has any obligation or responsibility to the General Partner or USNG to effect any sale or resale of units. Units are expected to trade in the secondary market on the AMEX. Units may trade in the secondary market at prices that are lower or higher relative to their NAV per unit. The amount of the discount or premium in the trading price relative to the NAV per unit may be influenced by various factors, including the number of investors who seek to purchase or sell units in the secondary market and the liquidity of the Futures Contracts market and the market for Other Natural Gas Related Investments. While the units trade on the AMEX until 4:15 p.m. New York time, liquidity in the market for Futures Contracts and Other Natural Gas Related Investments may be reduced after the close of the NYMEX at 2:30 p.m. New York time. As a result, during this time, trading spreads, and the resulting premium or discount, on the units may widen.

Prior Performance of USNG and Affiliates

USNG’s offering began on April 18, 2007 and is a continuous offering. As of December 31, 2007, the total amount of money raised by USNG from Authorized Purchasers was $1,458,787,976; the total number of Authorized Purchasers was 4, the number of baskets purchased by Authorized Purchasers was 379; and the aggregate amount of units purchased was 37.9 million. For more information on the performance of USNG, see the Performance Tables below.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

Experience in Raising and Investing in Funds through December 31, 2007

| Dollar Amount Offered: | $ | 3,664,500,000 |

| | | |

| Dollar Amount Raised: | $ | 1,458,787,976 |

| | | |

| Offering Expenses*: | | |

| SEC registration fee**: | $ | 104,010 |

| FINRA registration fee**: | | 151,000 |

| AMEX Listing fee**: | $ | 5,000 |

| Auditor's fees and expenses**: | $ | 29,000 |

| Legal fees and expenses**: | $ | 526,746 |

| Printing expenses: | $ | 40,323 |

| | | |

| Length of Offering: | | Continuous |

——————

* Amounts are for organizational and offering expenses incurred in connection with offerings from April 18, 2007 through December 31, 2007.

** Paid for by the General Partner in connection with the initial public offering.

Performance Capsule

| Name of Commodity Pool: | | USNG | |

| Type of Commodity Pool: | | Exchange traded security | |

| Inception of Trading: | | April 18, 2007 | |

| Aggregate Gross Capital Subscriptions (from inception through December 31, 2007): | | $ | 1,458,787,977 | |

| Total Net Assets as of December 31, 2007: | | $ | 593,394,981 | * |

| Initial NAV Per Unit as of Inception: | | $ | 50.00 | |

| NAV per Unit as of December 31, 2007: | | $ | 36.18 | |

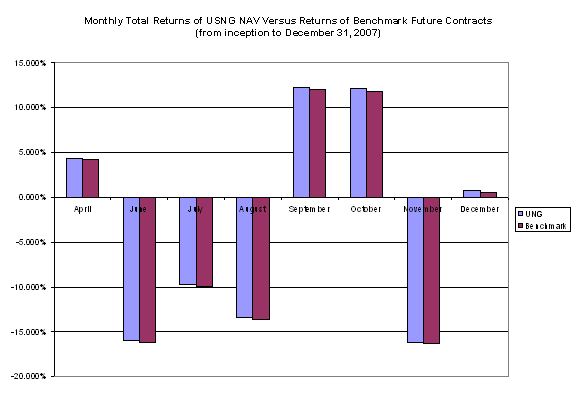

| Worst Monthly Percentage Draw-down: | | | November 2007 (-16.16 | %) |

| Worst Peak-to-Valley Draw-down: | | | April 2007- August 2007 (-34.74 | %) |

| Total Rate of Return Since Inception: | | | (27.64 | %) |

——————

* Inclusive of transactions recorded on a trade date + 1 basis.

| Month | | Rates of Return For the Year 2007 | |

| April | | | 4.30 | % |

| May | | | (0.84 | %) |

| June | | | (15.90 | %) |

| July | | | (9.68 | %) |

| August | | | (13.37 | %) |

| September | | | 12.28 | % |

| October | | | 12.09 | % |

| November | | | (16.16 | %) |

| December | | | 0.75 | % |

The General Partner is also currently the general partner of USOF, US12OF and USG. Each of the General Partner, USOF, US12OF and USG is located in California.

USOF is a publicly traded limited partnership which seeks to have the changes in percentage terms of its units' NAV track the changes in percentage terms of the spot price of light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the changes in the price of the futures contract on light, sweet crude oil as traded on the NYMEX that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case the futures contract will be the next month contract to expire, less USOF's expenses. USOF invests in a mixture of listed crude oil futures contracts, other non-listed oil related investments, Treasuries, cash and cash equivalents. USOF began trading on the AMEX on April 10, 2006 and is a continuous offering. As of December 31, 2007, the total amount of money raised by USOF from Authorized Purchasers was $6,142,802,106; the total number of Authorized Purchasers was 12; the number of baskets purchased by Authorized Purchasers was 1,074; and the aggregate amount of units purchased was 107.4 million.

US12OF is a publicly traded limited partnership which seeks to have the changes in percentage terms of its units’ NAV track the changes in percentage terms of the price of light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the changes in the average of the prices of 12 futures contracts on crude oil traded on the NYMEX, consisting of the near month contract to expire and the contracts for the following 11 months for a total of 12 consecutive months’ contracts, except when the near month contract is within two weeks of expiration, in which case it will be measured by the futures contracts that are the next month contract to expire and the contracts for the following 11 consecutive months, less US12OF’s expenses. US12OF invests in a mixture of listed crude oil futures contracts, other non-listed oil related investments, Treasuries, cash and cash equivalents. US12OF began trading on the AMEX on December 6, 2007 and is a continuous offering. As of December 31, 2007, the total amount of money raised by US12OF from Authorized Purchasers was $20,127,316; the total number of Authorized Purchasers was 2; the number of baskets purchased by Authorized Purchasers was 4; and the aggregate amount of units purchased was 400,000.

USG is a publicly traded limited partnership which seeks to have the changes in percentage terms of its units’ NAV track the changes in percentage terms of the price of unleaded gasoline delivered to the New York harbor, as measured by the changes in the price of the futures contract on gasoline traded on the NYMEX, less USG’s expenses. USG invests in a mixture of listed gasoline futures contracts, other gasoline related investments, Treasuries, cash and cash equivalents. USG began trading on the AMEX on February 26, 2008 and is a continuous offering. During the year ended December 31, 2007, USG had not yet commenced investment activities nor issued units.

Since the offering of USOF units to the public on April 10, 2006 to December 31, 2007, the simple average daily change in the price of a specified oil futures contract (the “Benchmark Oil Futures Contract”) was -0.031%, while the simple average daily change in the NAV of USOF over the same time period was 0.042%. The average daily difference was 0.011% (or 1.1 basis point, where 1 basis point equals 1/100 of 1%). As a percentage of the daily movement of the Benchmark Oil Futures Contract, the average error in daily tracking by the NAV was 2.98%, meaning that over this time period USOF’s tracking error was within the plus or minus 10% range established as its benchmark tracking goal.

Since the offering of US12OF units to the public on December 6, 2007 to December 31, 2007, the simple average daily change in the average of the prices of 12 futures contracts on crude oil traded on the NYMEX (the “Benchmark 12 Month Oil Futures Contracts”) was 0.480%, while the simple average daily change in the NAV of US12OF over the same time period was 0.489%. The average daily difference was 0.009% (or 0.9 basis point, where 1 basis point equals 1/100 of 1%). As a percentage of the daily movement of the Benchmark 12 Month Oil Futures Contracts, the average error in daily tracking by the NAV was 2.651%, meaning that over this time period US12OF’s tracking error was within the plus or minus 10% range established as its benchmark tracking goal.

There are significant differences between investing in USOF and US12OF and investing directly in the futures market. The General Partner’s results with USOF and US12OF may not be representative of results that may be experienced with a fund directly investing in futures contracts or other managed funds investing in futures contracts. For more information on the performance of USOF and US12OF, see the Performance Tables below. Since USG did not commence investment activities nor issue units during the year ended December 31, 2007, performance information has not been included for USG.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

Experience in Raising and Investing in Funds through December 31, 2007

| Dollar Amount Offered in USOF Offering*: | | $ | 7,094,860,000 | |

| Dollar Amount Raised in USOF Offering: | | $ | 6,142,801,102 | |

| Organizational Expenses in USOF Offering: | | | | |

| SEC registration fee**: | | $ | 800,474 | |

| FINRA registration fee**: | | $ | 377,500 | |

| AMEX listing fee**: | | $ | 5,000 | |

| Auditor’s fees and expenses**: | | $ | 59,000 | |

| Legal fees and expenses**: | | $ | 1,249,109 | |

| Printing expenses**: | | $ | 241,977 | |

| Length of USOF offering: | | Continuous | |

| * | Reflects the offering price per unit set forth on the cover page of the registration statement registering such units filed with the SEC. |

| ** | Through December 31, 2006, these expenses were paid for by an affiliate of the General Partner in connection with the initial public offering. Following December 31, 2006, USOF has recorded these expenses. |

| Dollar Amount Offered in US12OF Offering*: | | $ | 550,000,000 | |

| Dollar Amount Raised in US12OF Offering: | | $ | 20,127,316 | |

| Organizational Expenses in US12OF Offering: | | | | |

| SEC registration fee**: | | $ | 16,885 | |

| FINRA registration fee**: | | $ | 75,500 | |

| AMEX listing fee**: | | $ | 5,000 | |

| Auditor’s fees and expenses**: | | $ | 10,700 | |

| Legal fees and expenses**: | | $ | 233,799 | |

| Printing expenses**: | | $ | 23,755 | |

| Length of US12OF offering: | | Continuous | |

| * | Reflects the offering price per unit set forth on the cover page of the registration statement registering such units filed with the SEC. |

| ** | These expenses were paid for by the General Partner. |

Compensation to the General Partner and Other Compensation

USOF:

Expenses Paid by USOF through December 31, 2007 in dollar terms (unaudited):

| Expense | | Amount in Dollar Terms | |

| Amount Paid to General Partner in USOF Offering: | | $ | 3,622,613 | |

| Amount Paid in Portfolio Brokerage Commissions in USOF offering: | | $ | 1,184,956 | |

| Other Amounts Paid in USOF Offering: | | $ | 1,530,281 | |

| Total Expenses Paid in USOF Offering: | | $ | 6,337,850 | |

Expenses Paid by USOF through December 31, 2007 as a Percentage of Average Daily Net Assets (unaudited):

| Expenses in USOF Offering: | Amount As a Percentage ofAverage Daily Net Assets | |

| General Partner: | 0.50% annualized | |

| Portfolio Brokerage Commissions: | 0.16% annualized | |

| Other Amounts Paid in USOF Offering | 0.21% annualized | |

| Total Expense Ratio: | 0.87% annualized | |

| | USOF Performance: | |

| | Name of Commodity Pool: | USOF |

| | Type of Commodity Pool: | Exchange traded security |

| | Inception of Trading: | April 10, 2006 |

| | Aggregate Subscriptions (from inception through December 31, 2007): | $6,142,801,105 |

| | Total Net Assets as of December 31, 2007: | $485,222,737 |

| | Initial NAV Per Unit as of Inception: | $67.39 |

| | NAV per Unit as of December 31, 2007: | $75.82 |

| | Worst Monthly Percentage Draw-down: | September 2006 (11.71%) |

| | Worst Peak-to-Valley Draw-down: | June 2006 - January 2007 (30.60%) |

US12OF:

Expenses Paid by US12OF through December 31, 2007 in dollar terms (unaudited):

| Expense | | Amount in Dollar Terms | |

| Amount Paid to General Partner in US12OF Offering: | | $ | 8,790 | |

| Amount Paid in Portfolio Brokerage Commissions in US12OF offering: | | $ | 892 | |

| Other Amounts Paid in US12OF Offering: | | $ | 3,479 | |

| Total Expenses Paid in US12OF Offering: | | $ | 13,161 | |

Expenses Paid by US12OF through December31, 2007 as a Percentage of Average Daily Net Assets (unaudited):

| Expenses in US12OF Offering: | Amount As a Percentage ofAverage Daily Net Assets |

| General Partner: | 0.60% annualized |

| Portfolio Brokerage Commissions: | 0.06% annualized |

| Other Amounts Paid in US12OF Offering | 0.24% annualized |

| Total Expense Ratio: | 0.90% annualized |

| US12OF Performance: | |

| Name of Commodity Pool: | US12OF |

| Type of Commodity Pool: | Exchange traded security |

| Inception of Trading: | December 6, 2007 |

| Aggregate Subscriptions (from inception through December 31, 2007): | $20,126,316 |

| Total Net Assets as of December 31, 2007: | $21,691,479 |

| Initial NAV Per Unit as of Inception: | $50.00 |

| NAV per Unit as of December 31, 2007: | $54.23 |

| Worst Monthly Percentage Draw-down: | N/A |

| Worst Peak-to-Valley Draw-down: | N/A |

COMPOSITE PERFORMANCE DATA FOR USOF

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

| Month | | Rates of Return For the Year 2006 | |

| April* | | | 3.47 | % |

| May | | | (2.91 | %) |

| June | | | 3.16 | % |

| July | | | (0.50 | %) |

| August | | | (6.97 | %) |

| September | | | (11.71 | %) |

| October | | | (8.46 | %) |

| November | | | 4.73 | % |

| December | | | (5.21 | %) |

| Annual Rate of Return (since inception through December 31, 2006) | | | (23.03 | %) |

* Partial from April 10, 2006.

| Month | | Rates of Return For the Year 2007 | |

| January | | | (6.55 | %) |

| February | | | 5.63 | % |

| March | | | 4.61 | % |

| April | | | (4.26 | %) |

| May | | | (4.91 | %) |

| June | | | 9.06 | % |

| July | | | 10.57 | % |

| August | | | (4.95 | %) |

| September | | | 12.11 | % |

| October | | | 16.98 | % |

| November | | | (4.82 | %) |

| December | | | 8.67 | % |

| Annual Rate of Return (through December 31, 2007) | | | 46.17 | % |

COMPOSITE PERFORMANCE DATA FOR US12OF

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

| Month | | Rates of Return For the Year 2007 | |

| December* | | | 8.46 | % |

| Annual Rate of Return (through December 31, 2007) | | | 8.46 | % |

* Partial from December 6, 2007.

Draw-down: Losses experienced over a specified period. Draw-down is measured on the basis of monthly returns only and does not reflect intra-month figures.

Worst Monthly Percentage Draw-down: The largest single month loss sustained since inception of trading.

Worst Peak-to-Valley Draw-down: The largest percentage decline in the NAV per unit over the history of the fund. This need not be a continuous decline, but can be a series of positive and negative returns where the negative returns are larger than the positive returns. Worst Peak-to-Valley Draw-down represents the greatest percentage decline from any month-end NAV per unit that occurs without such month-end NAV per unit being equaled or exceeded as of a subsequent month-end. For example, if the NAV per unit declined by $1 in each of January and February, increased by $1 in March and declined again by $2 in April, a “peak-to-trough drawdown” analysis conducted as of the end of April would consider that “drawdown” to be still continuing and to be $3 in amount, whereas if the NAV per unit had increased by $2 in March, the January-February drawdown would have ended as of the end of February at the $2 level.

Nicholas Gerber, the president and CEO of the General Partner, ran the Marc Stevens Futures Index Fund over 10 years ago. This fund combined commodity futures with equity stock index futures. It was a very small private offering, which had under $1 million in assets. The Marc Stevens Futures Index Fund was a commodity pool and Mr. Gerber was the CPO. Ameristock Corporation is an affiliate of the General Partner and it is a California-based registered investment advisor registered under the Investment Advisers Act of 1940, as amended (the "Advisers Act") that has been sponsoring and providing portfolio management services to mutual funds since 1995. Ameristock Corporation is the investment adviser to the Ameristock Mutual Fund, Inc., a mutual fund registered under the Investment Company Act of 1940, as amended (the "1940 Act") that focuses on large cap U.S. equities that has approximately $425 million in assets as of December 31, 2007. Ameristock Corporation is also the investment advisor to the Ameristock ETF Trust, an open-end management investment company registered under the 1940 Act that seeks investment results that correspond to the performance of U.S. Treasury indices owned and compiled by Ryan Holdings LLC and Ryan ALM, Inc.

Investments

The General Partner applies substantially all of USNG’s assets toward trading in Futures Contracts and Other Natural Gas Related Investments, Treasuries, cash and/or cash equivalents. The General Partner has sole authority to determine the percentage of assets that are:

| | · | held on deposit with the futures commission merchant or other custodian, |

| | · | used for other investments, and |

| | · | held in bank accounts to pay current obligations and as reserves. |

The General Partner deposits substantially all of USNG’s net assets with the Custodian or other custodian. When USNG purchases a Futures Contract and certain exchange traded Other Natural Gas Related Investments, USNG is also required to deposit with the futures commission merchant on behalf of the exchange a portion of the value of the contract or other interest as security to ensure payment for the obligation under natural gas at maturity. This deposit is known as “margin.” USNG invests the remainder of its assets equal to the difference between the margin deposited and the face value of the Futures Contract in Treasuries, cash and/or cash equivalents.

The General Partner believes that all entities that hold or trade USNG’s assets are based in the United States and are subject to United States regulations.

Approximately 5% to 10% of USNG’s assets have normally been committed as margin for Futures Contracts. However, from time to time, the percentage of assets committed as margin may be substantially more, or less, than such range. The General Partner invests the balance of USNG’s assets not invested in natural gas interests or held in margin as reserves to be available for changes in margin. All interest income is used for USNG’s benefit.

The futures commission merchant, a government agency or a commodity exchange could increase margins applicable to USNG to hold trading positions at any time. Moreover, margin is merely a security deposit and has no bearing on the profit or loss potential for any positions taken.

USNG’s assets are held in segregation pursuant to the CEA and CFTC regulations.

The Commodity Interest Markets

General

The CEA governs the regulation of commodity interest transactions, markets and intermediaries. In December 2000, the CEA was amended by the Commodity Futures Modernization Act of 2000 (the "CFMA"), which substantially revised the regulatory framework governing certain commodity interest transactions and the markets on which they trade. The CEA, as amended by the CFMA, now provides for varying degrees of regulation of commodity interest transactions depending upon the variables of the transaction. In general, these variables include (1) the type of instrument being traded (e.g., contracts for future delivery, options, swaps or spot contracts), (2) the type of commodity underlying the instrument (distinctions are made between instruments based on agricultural commodities, energy and metals commodities and financial commodities), (3) the nature of the parties to the transaction (retail, eligible contract participant, or eligible commercial entity), (4) whether the transaction is entered into on a principal-to-principal or intermediated basis, (5) the type of market on which the transaction occurs, and (6) whether the transaction is subject to clearing through a clearing organization. Information regarding commodity interest transactions, markets and intermediaries, and their associated regulatory environment, is provided below.

Futures Contracts

A futures contract such as a Futures Contract is a standardized contract traded on, or subject to the rules of, an exchange that calls for the future delivery of a specified quantity and type of a commodity at a specified time and place. Futures contracts are traded on a wide variety of commodities, including agricultural products, bonds, stock indices, interest rates, currencies, energy and metals. The size and terms of futures contracts on a particular commodity are identical and are not subject to any negotiation, other than with respect to price and the number of contracts traded between the buyer and seller.

The contractual obligations of a buyer or seller may generally be satisfied by taking or making physical delivery of the underlying commodity or by making an offsetting sale or purchase of an identical futures contract on the same or linked exchange before the designated date of delivery. The difference between the price at which the futures contract is purchased or sold and the price paid for the offsetting sale or purchase, after allowance for brokerage commissions, constitutes the profit or loss to the trader. Some futures contracts, such as stock index contracts, settle in cash (reflecting the difference between the contract purchase/sale price and the contract settlement price) rather than by delivery of the underlying commodity.

In market terminology, a trader who purchases a futures contract is long in the market and a trader who sells a futures contract is short in the market. Before a trader closes out his long or short position by an offsetting sale or purchase, his outstanding contracts are known as open trades or open positions. The aggregate amount of open positions held by traders in a particular contract is referred to as the open interest in such contract.

Forward Contracts

A forward contract is a contractual obligation to purchase or sell a specified quantity of a commodity at or before a specified date in the future at a specified price and, therefore, is economically similar to a futures contract. Unlike futures contracts, however, forward contracts are typically traded in the over-the-counter markets and are not standardized contracts. Forward contracts for a given commodity are generally available for various amounts and maturities and are subject to individual negotiation between the parties involved. Moreover, generally there is no direct means of offsetting or closing out a forward contract by taking an offsetting position as one would a futures contract on a U.S. exchange. If a trader desires to close out a forward contract position, he generally will establish an opposite position in the contract but will settle and recognize the profit or loss on both positions simultaneously on the delivery date. Thus, unlike in the futures contract market where a trader who has offset positions will recognize profit or loss immediately, in the forward market a trader with a position that has been offset at a profit will generally not receive such profit until the delivery date, and likewise a trader with a position that has been offset at a loss will generally not have to pay money until the delivery date. In recent years, however, the terms of forward contracts have become more standardized, and in some instances such contracts now provide a right of offset or cash settlement as an alternative to making or taking delivery of the underlying commodity.

The forward markets provide what has typically been a highly liquid market for foreign exchange trading, and in certain cases the prices quoted for foreign exchange forward contracts may be more favorable than the prices for foreign exchange futures contracts traded on U.S. exchanges. The forward markets are largely unregulated. Forward contracts are, in general, not cleared or guaranteed by a third party. Commercial banks participating in trading foreign exchange forward contracts often do not require margin deposits, but rely upon internal credit limitations and their judgments regarding the creditworthiness of their counterparties. In recent years, however, many over-the-counter market participants in foreign exchange trading have begun to require that their counterparties post margin.

Further, as the result of the CFMA, over-the-counter derivative instruments such as forward contracts and swap agreements (and options on forwards and physical commodities) may begin to be traded on lightly-regulated exchanges or electronic trading platforms that may, but are not required to, provide for clearing facilities. Exchanges and electronic trading platforms on which over-the-counter instruments may be traded and the regulation and criteria for that trading are more fully described below under “Futures Exchanges and Clearing Organizations.” Nonetheless, absent a clearing facility, USNG’s trading in foreign exchange and other forward contracts is exposed to the creditworthiness of the counterparties on the other side of the trade.

Options on Futures Contracts

Options on futures contracts are standardized contracts traded on an exchange. An option on a futures contract gives the buyer of the option the right, but not the obligation, to take a position at a specified price (the striking, strike, or exercise price) in the underlying futures contract or underlying interest. The buyer of a call option acquires the right, but not the obligation, to purchase or take a long position in the underlying interest, and the buyer of a put option acquires the right, but not the obligation, to sell or take a short position in the underlying interest.

The seller, or writer, of an option is obligated to take a position in the underlying interest at a specified price opposite to the option buyer if the option is exercised. Thus, the seller of a call option must stand ready to take a short position in the underlying interest at the strike price if the buyer should exercise the option. The seller of a put option, on the other hand, must stand ready to take a long position in the underlying interest at the strike price.

A call option is said to be in-the-money if the strike price is below current market levels and out-of-the-money if the strike price is above current market levels. Conversely, a put option is said to be in-the-money if the strike price is above the current market levels and out-of-the-money if the strike price is below current market levels.

Options have limited life spans, usually tied to the delivery or settlement date of the underlying interest. Some options, however, expire significantly in advance of such date. The purchase price of an option is referred to as its premium, which consists of its intrinsic value (which is related to the underlying market value) plus its time value. As an option nears its expiration date, the time value shrinks and the market and intrinsic values move into parity. An option that is out-of-the-money and not offset by the time it expires becomes worthless. On certain exchanges, in-the-money options are automatically exercised on their expiration date, but on others unexercised options simply become worthless after their expiration date.

Regardless of how much the market swings, the most an option buyer can lose is the option premium. The option buyer deposits his premium with his broker, and the money goes to the option seller. Option sellers, on the other hand, face risks similar to participants in the futures markets. For example, since the seller of a call option is assigned a short futures position if the option is exercised, his risk is the same as someone who initially sold a futures contract. Because no one can predict exactly how the market will move, the option seller posts margin to demonstrate his ability to meet any potential contractual obligations.

Options on Forward Contracts or Commodities

Options on forward contracts or commodities operate in a manner similar to options on futures contracts. An option on a forward contract or commodity gives the buyer of the option the right, but not the obligation, to take a position at a specified price in the underlying forward contract or commodity. However, similar to forward contracts, options on forward contracts or on commodities are individually negotiated contracts between counterparties and are typically traded in the over-the-counter market. Therefore, options on forward contracts and physical commodities possess many of the same characteristics of forward contracts with respect to offsetting positions and credit risk that are described above.

Swap Contracts

Swap transactions generally involve contracts between two parties to exchange a stream of payments computed by reference to a notional amount and the price of the asset that is the subject of the swap. Swap contracts are principally traded off-exchange, although recently, as a result of regulatory changes enacted as part of the CFMA, certain swap contracts are now being traded in electronic trading facilities and cleared through clearing organizations.

Swaps are usually entered into on a net basis, that is, the two payment streams are netted out in a cash settlement on the payment date or dates specified in the agreement, with the parties receiving or paying, as the case may be, only the net amount of the two payments. Swaps do not generally involve the delivery of underlying assets or principal. Accordingly, the risk of loss with respect to swaps is generally limited to the net amount of payments that the party is contractually obligated to make. In some swap transactions one or both parties may require collateral deposits from the counterparty to support that counterparty’s obligation under the swap agreement. If the counterparty to such a swap defaults, the risk of loss consists of the net amount of payments that the party is contractually entitled to receive less any collateral deposits it is holding.

Participants

The two broad classes of persons who trade commodities are hedgors and speculators. Hedgors include financial institutions that manage or deal in interest rate-sensitive instruments, foreign currencies or stock portfolios, and commercial market participants, such as farmers and manufacturers, that market or process commodities. Hedging is a protective procedure designed to lock in profits that could otherwise be lost due to an adverse movement in the underlying commodity, for example, the adverse price movement between the time a merchandiser or processor enters into a contract to buy or sell a raw or processed commodity at a certain price and the time he must perform the contract. In such a case, at the time the hedgor contracts to physically sell the commodity at a future date he will simultaneously buy a futures or forward contract for the necessary equivalent quantity of the commodity. At the time for performance of the contract, the hedgor may accept delivery under his futures contract and sell the commodity quantity as required by his physical contract or he may buy the actual commodity, sell if under the physical contract and close out his position by making an offsetting sale of a futures contract.

Unlike the hedgor, the speculator generally expects neither to make nor take delivery of the underlying commodity. Instead, the speculator risks his capital with the hope of making profits from price fluctuations in the commodities. The speculator is, in effect, the risk bearer who assumes the risks that the hedgor seeks to avoid. Speculators rarely make or take delivery of the underlying commodity; rather they attempt to close out their positions prior to the delivery date. Because the speculator may take either a long or short position in commodities, it is possible for him to make profits or incur losses regardless of whether prices go up or down.

Futures Exchanges and Clearing Organizations

Futures exchanges provide centralized market facilities in which multiple persons have the ability to execute or trade contracts by accepting bids and offers from multiple participants. Futures exchanges may provide for execution of trades at a physical location utilizing trading pits and/or may provide for trading to be done electronically through computerized matching of bids and offers pursuant to various algorithms. Members of a particular exchange and the trades executed on such exchange are subject to the rules of that exchange. Futures exchanges and clearing organizations are given reasonable latitude in promulgating rules and regulations to control and regulate their members. Examples of regulations by exchanges and clearing organizations include the establishment of initial margin levels, rules regarding trading practices, contract specifications, speculative position limits, daily price fluctuation limits, and execution and clearing fees.

U.S. Futures Exchanges

Futures exchanges in the United States are subject to varying degrees of regulation by the CFTC based on their designation as one of the following: a designated contract market, a derivatives transaction execution facility, an exempt board of trade or an electronic trading facility.

A designated contract market is the most highly regulated level of futures exchange. Designated contract markets may offer products to retail customers on an unrestricted basis. To be designated as a contract market, the exchange must demonstrate that it satisfies specified general criteria for designation, such as having the ability to prevent market manipulation, rules and procedures to ensure fair and equitable trading, position limits, dispute resolution procedures, minimization of conflicts of interest and protection of market participants. Among the principal designated contract markets in the United States are the Chicago Board of Trade, the Chicago Mercantile Exchange and the NYMEX. Each of the designated contract markets in the United States must provide for the clearance and settlement of transactions with a CFTC-registered derivatives clearing organization.

A derivatives transaction execution facility (a "DTEF"), is a new type of exchange that is subject to fewer regulatory requirements than a designated contract market but is subject to both commodity interest and participant limitations. DTEFs limit access to eligible traders that qualify as either eligible contract participants or eligible commercial entities for futures and option contracts on commodities that have a nearly inexhaustible deliverable supply, are highly unlikely to be susceptible to the threat of manipulation, or have no cash market, security futures products, and futures and option contracts on commodities that the CFTC may determine, on a case-by-case basis, are highly unlikely to be susceptible to the threat of manipulation. In addition, certain commodity interests excluded or exempt from the CEA, such as swaps, etc. may be traded on a DTEF. There is no requirement that a DTEF use a clearing organization, except with respect to trading in security futures contracts, in which case the clearing organization must be a securities clearing agency. However, if futures contracts and options on futures contracts on a DTEF are cleared, then it must be through a CFTC-registered derivatives clearing organization, except that some excluded or exempt commodities traded on a DTEF may be cleared through a clearing organization other than one registered with the CFTC.

An exempt board of trade is also a newly designated form of exchange. An exempt board of trade is substantially unregulated, subject only to CFTC anti-fraud and anti-manipulation authority. An exempt board of trade is permitted to trade futures contracts and options on futures contracts provided that the underlying commodity is not a security or securities index and has an inexhaustible deliverable supply or no cash market. All traders on an exempt board of trade must qualify as eligible contract participants. Contracts deemed eligible to be traded on an exempt board of trade include contracts on interest rates, exchange rates, currencies, credit risks or measures, debt instruments, measures of inflation, or other macroeconomic indices or measures. There is no requirement that an exempt board of trade use a clearing organization. However, if contracts on an exempt board of trade are cleared, then it must be through a CFTC-registered derivatives clearing organization. A board of trade electing to operate as an exempt board of trade must file a written notification with the CFTC.

An electronic trading facility is a new form of exchange that operates by means of an electronic or telecommunications network and maintains an automated audit trail of bids, offers, and the matching of orders or the execution of transactions on the electronic trading facility. The CEA does not apply to, and the CFTC has no jurisdiction over, transactions on an electronic trading facility in certain excluded commodities that are entered into between principals that qualify as eligible contract participants, subject only to CFTC anti-fraud and anti-manipulation authority. In general, excluded commodities include interest rates, currencies, securities, securities indices or other financial, economic or commercial indices or measures.

The General Partner intends to monitor the development of and opportunities and risks presented by the new less-regulated exchanges and exempt boards and may, in the future, allocate a percentage of USNG’s assets to trading in products on these exchanges. Provided USNG maintains assets exceeding $5 million, USNG would qualify as an eligible contract participant and thus would be able to trade on such exchanges.

Non-U.S. Futures Exchanges

Non-U.S. futures exchanges differ in certain respects from their U.S. counterparts. Importantly, non-U.S. futures exchanges are not subject to regulation by the CFTC, but rather are regulated by their home country regulator. In contrast to U.S. designated contract markets, some non-U.S. exchanges are principals’ markets, where trades remain the liability of the traders involved, and the exchange or an affiliated clearing organization, if any, does not become substituted for any party. Due to the absence of a clearing system, such exchanges are significantly more susceptible to disruptions. Further, participants in such markets must often satisfy themselves as to the individual creditworthiness of each entity with which they enter into a trade. Trading on non-U.S. exchanges is often in the currency of the exchange’s home jurisdiction. Consequently, USNG is subject to the additional risk of fluctuations in the exchange rate between such currencies and U.S. dollars and the possibility that exchange controls could be imposed in the future. Trading on non-U.S. exchanges may differ from trading on U.S. exchanges in a variety of ways and, accordingly, may subject USNG to additional risks.

Accountability Levels and Position Limits

The CFTC and U.S. designated contract markets have established accountability levels and position limits on the maximum net long or net short futures contracts in commodity interests that any person or group of persons under common trading control (other than a hedgor, which USNG is not) may hold, own or control. Among the purposes of accountability levels and position limits is to prevent a corner or squeeze on a market or undue influence on prices by any single trader or group of traders. The position limits currently established by the CFTC apply to certain agricultural commodity interests, such as grains (oats, barley, and flaxseed), soybeans, corn, wheat, cotton, eggs, rye, and potatoes, but not to interests in energy products. In addition, U.S. exchanges may set accountability levels and position limits for all commodity interests traded on that exchange. For example, the current accountability level for investments at any one time in the Benchmark Futures Contract is 12,000 contracts. The NYMEX also imposes position limits on contracts held in the last few days of trading in the near month contract to expire. Certain exchanges or clearing organizations also set limits on the total net positions that may be held by a clearing broker. In general, no position limits are in effect in forward or other over-the-counter contract trading or in trading on non-U.S. futures exchanges, although the principals with which USNG and the clearing brokers may trade in such markets may impose such limits as a matter of credit policy. For purposes of determining accountability levels and position limits USNG’s commodity interest positions will not be attributable to investors in their own commodity interest trading.

Daily Price Limits

Most U.S. futures exchanges (but generally not non-U.S. exchanges) limit the amount of fluctuation in some futures contract or options on futures contract prices during a single trading period by regulations. These regulations specify what are referred to as daily price fluctuation limits or more commonly, daily limits. The daily limits establish the maximum amount that the price of a futures or options on futures contract may vary either up or down from the previous day’s settlement price. Once the daily limit has been reached in a particular futures or options on futures contract, no trades may be made at a price beyond the limit. Positions in the futures or options contract may then be taken or liquidated, if at all, only at inordinate expense or if traders are willing to effect trades at or within the limit during the period for trading on such day. Because the daily limit rule governs price movement only for a particular trading day, it does not limit losses and may in fact substantially increase losses because it may prevent the liquidation of unfavorable positions. Futures contract prices have occasionally moved to the daily limit for several consecutive trading days, thus preventing prompt liquidation of positions and subjecting the trader to substantial losses for those days. The concept of daily price limits is not relevant to over-the-counter contracts, including forwards and swaps, and thus such limits are not imposed by banks and others who deal in those markets.