Astellas Offer to Acquire OSI Investor Presentation Investor Presentation April 2010 April 2010 Exhibit (a)(5)(k) ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ******** ****** |

2 Executive Summary • • OSI’s share price has lagged that of its peers and its performance has OSI’s share price has lagged that of its peers and its performance has fallen short of Wall Street expectations fallen short of Wall Street expectations • • Astellas’ Astellas’ $52 per share offer reflects the potential for both Tarceva and $52 per share offer reflects the potential for both Tarceva and OSI’s pipeline products as well as the value of OSI's financial assets OSI’s pipeline products as well as the value of OSI's financial assets • • This offer represents a significant premium relative to comparable This offer represents a significant premium relative to comparable companies and relative to the value OSI is expected to achieve on its companies and relative to the value OSI is expected to achieve on its own, according to Wall Street estimates own, according to Wall Street estimates • • As evidenced by the CV Therapeutics process, Astellas is a disciplined As evidenced by the CV Therapeutics process, Astellas is a disciplined buyer that will not pay beyond its opinion of intrinsic value simply to win buyer that will not pay beyond its opinion of intrinsic value simply to win an asset an asset • • Astellas has recently signed a confidentiality agreement with OSI, Astellas has recently signed a confidentiality agreement with OSI, providing it access to confidential information, which may lead it to providing it access to confidential information, which may lead it to confirm, raise or lower its offer price confirm, raise or lower its offer price |

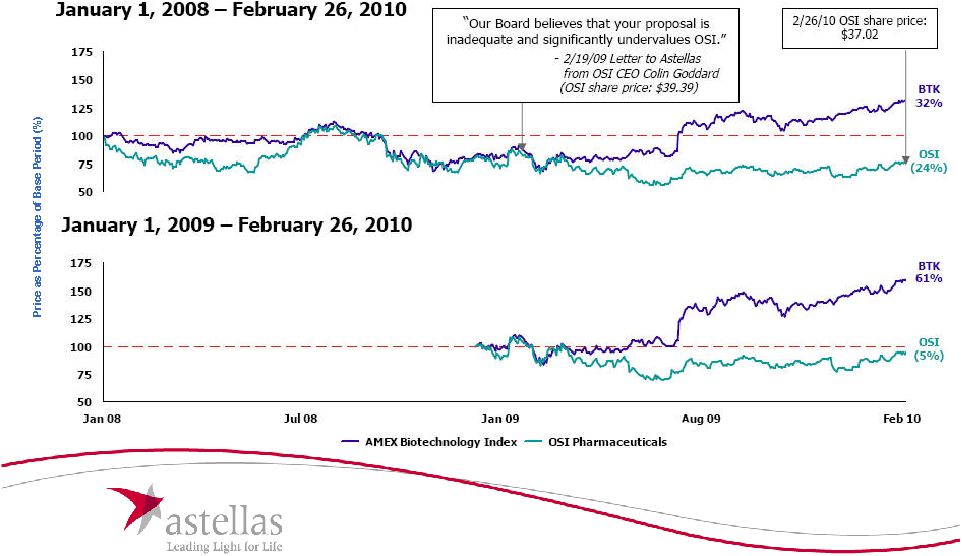

3 OSI’s Share Price Has Lagged Its Peers • Prior to the announcement of Astellas’ tender offer on March 1, 2010, OSI’s share price had significantly underperformed its peers in the AMEX Biotechnology (BTK) index over the last several years Note: February 26, 2010 was the last trading day prior to public announcement of Astellas’ tender offer. |

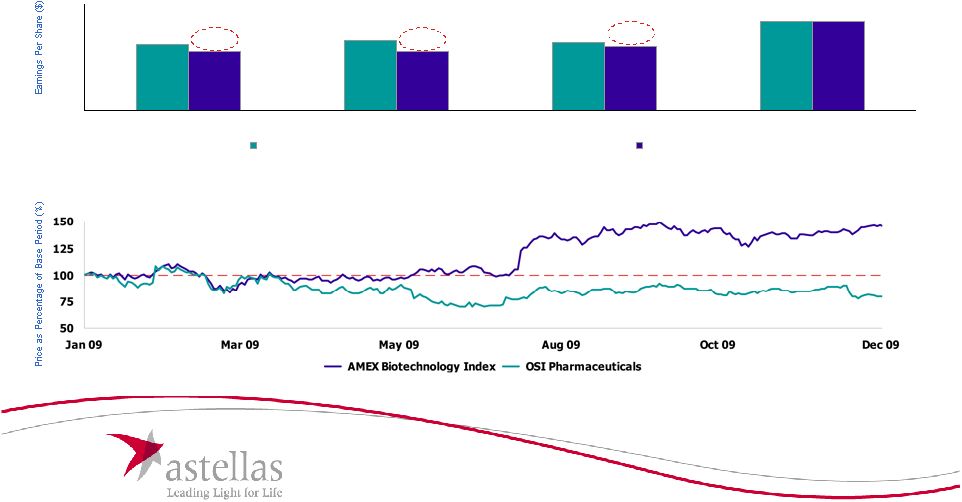

4 OSI’s 2009 Financial Results Contribute to Underperformance of Its Stock • • OSI’s continued inability to exceed Wall Street estimates caused it to OSI’s continued inability to exceed Wall Street estimates caused it to significantly underperform its peers in 2009 significantly underperform its peers in 2009 Wall Street EPS Consensus Estimates vs. Actual Results Share Price Performance (January 1, 2009 – December 31, 2009) $0.31 $0.33 $0.32 $0.42 $0.28 $0.28 $0.30 $0.42 0.00 0.10 0.20 0.30 0.40 0.50 1Q CY09 2Q CY09 3Q CY09 4Q CY09 Wall Street Mean Consensus OSI Actuals (20%) +46% -10% -15% -6% 0% (1) Denotes Wall Street mean consensus estimates for diluted EPS from continuing operations. (1) |

5 Astellas’ Current Offer Represents Full and Fair Value for OSI • • Based on information available to Astellas, $52 in cash per share Based on information available to Astellas, $52 in cash per share represents a full and fair value for OSI represents a full and fair value for OSI • • This represents both the value created by OSI to date as well as This represents both the value created by OSI to date as well as its future prospects its future prospects • • The offer stands in comparison to Wall Street research analysts The offer stands in comparison to Wall Street research analysts that had an average 12-month price target of only $40 prior to that had an average 12-month price target of only $40 prior to announcement of Astellas' offer announcement of Astellas' offer • • Astellas reduced the $55-57 per share offer it made in 2009 to Astellas reduced the $55-57 per share offer it made in 2009 to correspond with Astellas’ correspond with Astellas’ current, updated view of the value of all current, updated view of the value of all of OSI’s future prospects, including the remaining useful life of of OSI’s future prospects, including the remaining useful life of the Tarceva patents the Tarceva patents |

6 Wall Street Commentary on Tarceva Maintenance • • Astellas' offer attributes value to all of the potential label expansions for Astellas' offer attributes value to all of the potential label expansions for Tarceva, including maintenance approval. Wall Street research analysts Tarceva, including maintenance approval. Wall Street research analysts generally do not see significant value associated with maintenance generally do not see significant value associated with maintenance approval approval "The EU approval of Tarceva as first-line maintenance therapy (FLMT) is a positive surprise given the negative FDA ODAC panel...The commercial hurdle would likely be high for Tarceva, if approved....We estimate the sales potential of FLMT in the EU to be about $100-150 mm, representing about $1-$2 per share in NPV.” Goldman Sachs – March 19, 2010 "While today's news is an incremental positive, we see maintenance as a niche opportunity with peak potential of $50M to $100M in Europe...we estimate this could be worth an incremental $1.00/share to base business....We don't think this announcement supports a materially higher bid from current levels.” JP Morgan – March 19, 2010 “OSIP's confidence in its valuation is based on its discussions with FDA for the maintenance indication and ongoing clinical trials. We already have a high level of confidence that the FDA will approve Tarceva in the maintenance setting but believe there is likely only modest impact to sales as a result.” RBC – March 15, 2010 “We do remain skeptical on the maintenance setting, however, and believe that even under a best-case scenario, the FDA...gives Tarceva a restricted label that contraindicates use in the squamous cell and EGFR mutant populations – at which point, any competitive differentiation relative to Alimta, which has better data in non-squamous patients, becomes difficult.” Thomas Weisel – February 24, 2010 Source: Wall Street research. Note: Permission to use quotations was neither sought nor obtained. |

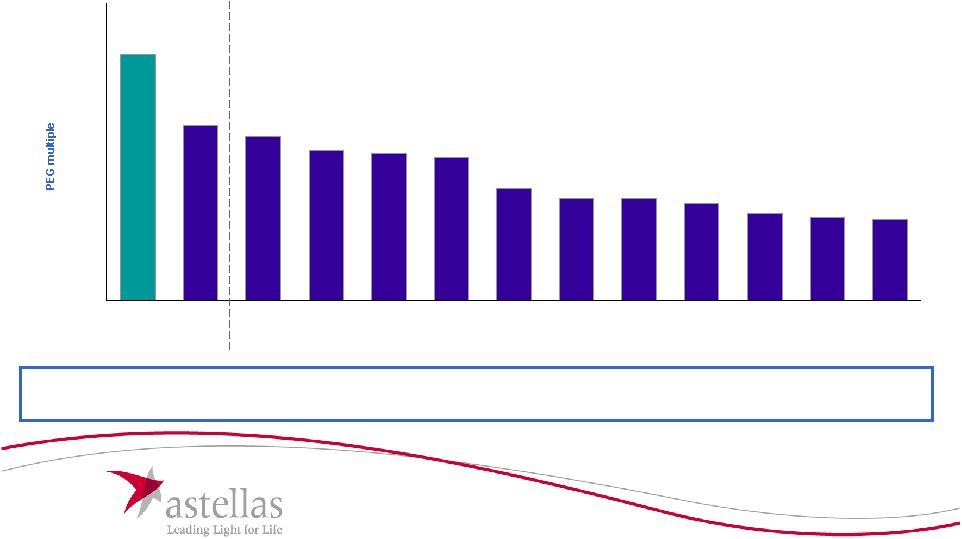

7 Comparable P/E and PEG multiples • • On a growth-adjusted basis, Astellas’ On a growth-adjusted basis, Astellas’ $52.00 per share offer is a $52.00 per share offer is a significant premium to other established pharmaceutical firms and firms significant premium to other established pharmaceutical firms and firms with higher growth expectations with higher growth expectations 2010E P/E LTG 33.6x 13.5% 12.4x 8.4% 19.5x 18.9% 10.9x 12.4% 12.6x 15.4% 16.7x 10.1% 20.7x 13.7% 33.2% 48.0x 24.1x 23.4% 11.6x 11.8% 13.6x 16.2% 23.9x 13.5% 11.7% 13.3x 2.5x 1.8x 1.7x 1.5x 1.5x 1.4x 1.1x 1.0x 1.0x 1.0x 0.9x 0.8x 0.8x 0.0 0.5 1.0 1.5 2.0 2.5 3.0x OSI: At $52 / share OSI: Before Offer Shire Allergan Biogen Idec Alexion King Genzyme Celgene Actelion Cephalon Cubist Gilead Source: Wall Street mean consensus research estimates. Note: Market data as of March 30, 2010. |

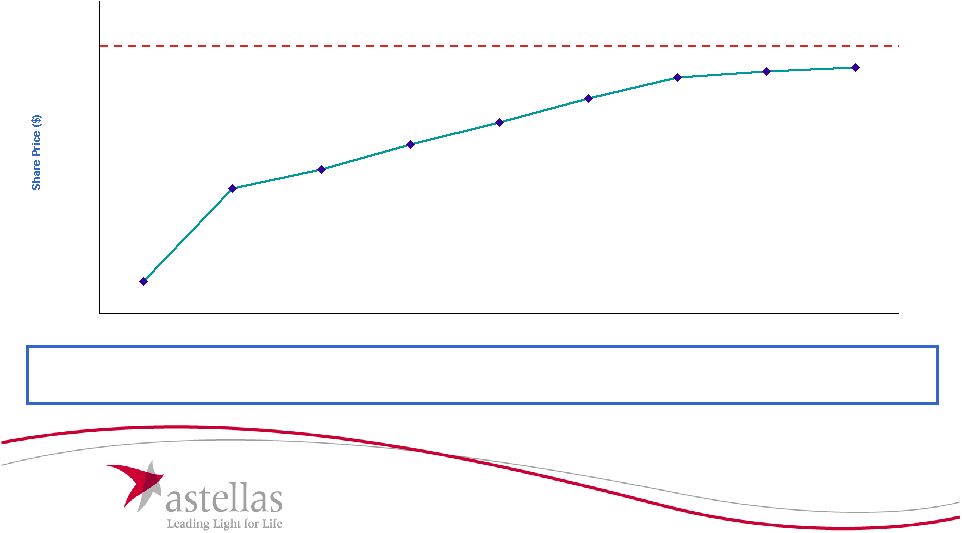

8 In Today’s Dollars, OSI Won’t Reach $52 Until After 2013 • Even if OSI’s shareholders believe the Company will successfully execute on its strategy for the next three and a half years, and achieve Wall Street’s earnings estimates, on a present value basis they still will not achieve the same value they could receive from Astellas today Forward EPS Multiple $1.55 23.9x 23.9x 23.9x 23.9x $1.84 $1.96 $2.11 (1) (2) 23.9x $2.26 23.9x $2.43 23.9x $2.59 23.9x $2.71 23.9x $2.84 Note: Prices calculated using an 8% discount rate. (1) Based on a rolling forward four quarter estimate of OSI’s EPS, according to Wall Street mean consensus estimates. (2) OSI’s forward P/E multiple based on a closing price of $37.02 and 2010 estimated EPS of $1.55 according to Wall Street research, as of February 26, 2010. $37.02 $50.80 $50.51 $50.13 $48.78 $47.25 $45.84 $44.26 $43.04 35.00 40.00 45.00 50.00 $55.00 2/26/10 6/30/10 12/31/10 6/30/11 12/31/11 6/30/12 12/31/12 6/30/13 12/31/13 Astellas’ Offer Price: $52.00 |

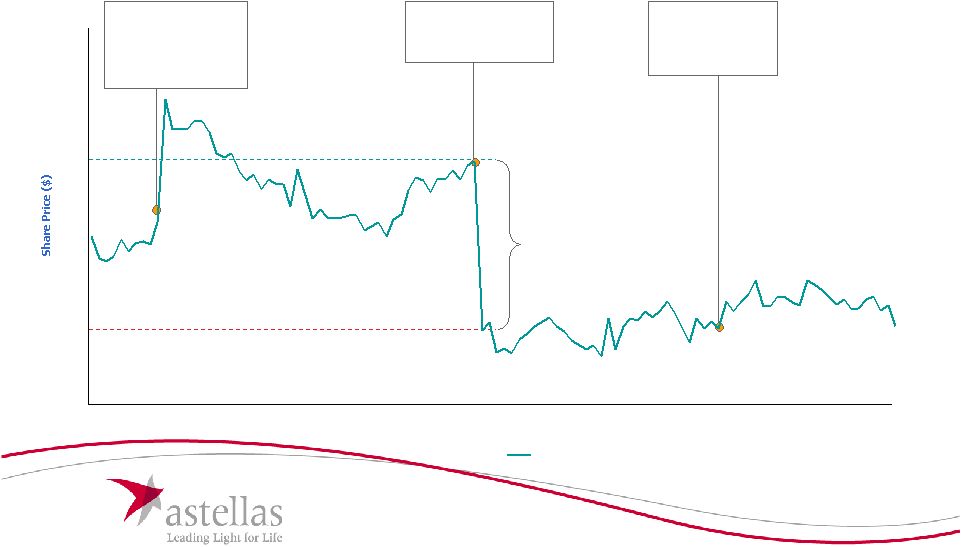

9 Biogen Idec’s Share Price History During Icahn’s Offer • • Biogen’s Biogen’s failed efforts to find a potential buyer resulted in share prices failed efforts to find a potential buyer resulted in share prices lower than pre-announcement levels lower than pre-announcement levels October 1, 2007 – March 1, 2008 Biogen Idec 10/13/07: Biogen announces it has commenced exploring alternatives after receiving an offer of $23bn from Icahn 12/12/07: Biogen ends its strategic review after the process failed to yield any definitive offers -24% -$5bn of market cap Market Cap: $17 bn Market Cap: $22 bn 1/28/08: Icahn sends a notice to Biogen seeking to nominate three members to the Board of Directors Oct 07 Nov 07 Dec 07 Jan 08 Feb 08 50 60 70 80 90 |

10 Outcome of Buyer Discussions Can Be Completed Quickly • • OSI’s Board of Directors instructed OSI’s management and OSI’s Board of Directors instructed OSI’s management and financial advisors to contact other parties to explore a transaction financial advisors to contact other parties to explore a transaction • • The sales process should not be used as a delay tactic The sales process should not be used as a delay tactic OSI has ample time to locate a bid greater than $52 that has the same certainty of value and completion as Astellas’ offer Considering (a) OSI has a straightforward business and assets and (b) the sophistication of the buyer universe, OSI should be able to complete the process expeditiously |

11 Conclusion • • If OSI does not announce a deal soon, shareholders will have to If OSI does not announce a deal soon, shareholders will have to choose: choose: Stay the course with OSI Realize immediate value from Astellas’ offer • • If they elect to stay the course with OSI, shareholders may face If they elect to stay the course with OSI, shareholders may face a rapid decline in OSI’s share price to pre-offer levels and Tarceva’s a rapid decline in OSI’s share price to pre-offer levels and Tarceva’s useful life will have continued to diminish useful life will have continued to diminish • • As evidenced by the CV Therapeutics process in 2009, Astellas is As evidenced by the CV Therapeutics process in 2009, Astellas is a a disciplined disciplined buyer buyer that that understands understands intrinsic intrinsic value, value, and and it it will will not not pay beyond that value simply to win an asset pay beyond that value simply to win an asset |

Additional Information Further details related to this announcement can be found on www.oncologyleader.com Media Contacts Brunswick New York +1 212 333 3810 Stan Neve Sarah Lubman Brunswick Hong Kong +852 9850 5033 Joseph Lo Information Agent Georgeson + 1 212 440 9872 Thomas Gardiner About Astellas Astellas Pharma Inc., located in Tokyo, Japan, is a pharmaceutical company dedicated to improving the health of people around the world through the provision of innovative and reliable pharmaceuticals. Astellas has approximately 14,200 employees worldwide. The organization is committed to becoming a global category leader in urology, immunology & infectious diseases, neuroscience, DM complications & metabolic diseases and oncology. For more information on Astellas Pharma Inc., please visit our website at http://www.astellas.com/en. Important Additional Information This communication is for informational purposes only and does not constitute an offer to purchase or a solicitation of an offer to sell OSI Pharmaceuticals (“OSI”) common stock. The tender offer (the “Tender Offer”) is being made pursuant to a tender offer statement on Schedule TO (including the Offer to Purchase, Letter of Transmittal and other related tender offer materials) filed by Astellas Pharma Inc., Astellas US Holding, Inc. and Ruby Acquisition, Inc. (collectively, “Astellas”) with the Securities and Exchange Commission (“SEC”). These materials, as they may be amended from time to time, contain important information, including the terms and conditions of the Tender Offer, that should be read carefully before any decision is made with respect to the Tender Offer. Investors and security holders may obtain a free copy of these materials and other documents filed by Astellas with the SEC at the website maintained by the SEC at www.sec.gov. The Offer to Purchase, Letter of Transmittal and other related Tender Offer materials may also be obtained for free by contacting the information agent for the Tender Offer, Georgeson Inc., at (212) 440-9800 for banks and brokers and at (800) 213-0473 for persons other than banks and brokers. In connection with Astellas’ proposal to nominate directors at OSI’s annual meeting of stockholders, Astellas expects to file a proxy statement with the SEC. Investors and security holders of OSI are urged to read the proxy statement and other documents related to the solicitation of proxies filed with the SEC carefully in their entirety when they become available because they will contain important information. Stockholders of OSI and other interested parties may obtain, free of charge, copies of the proxy statement (when available), and any other documents filed by Astellas with the SEC in connection with the proxy solicitation, at the SEC's website as described above. The proxy statement (when available) and these other documents may also be obtained free of charge by contacting Georgeson Inc. at the numbers listed above. Astellas and certain of their directors and executive officers and the individuals to be nominated by Astellas for election to OSI’s board of directors may be deemed to be participants in the solicitation of proxies in connection with the proposed transaction. Information regarding these directors and executive officers and other individuals is available in the Schedule TO that was filed March 2, 2010, and other documents filed by Astellas with the SEC as described above. Further information will be available in any proxy statement or other relevant materials filed with the SEC in connection with the solicitation of proxies when they become available. No assurance can be given that the proposed transaction described herein will be consummated by Astellas, or completed on the terms proposed or any particular schedule, that the proposed transaction will not incur delays in obtaining the regulatory, board or stockholder approvals required for such transaction, or that Astellas will realize the anticipated benefits of the proposed transaction. Statement on Cautionary Factors Any statements made in this communication that are not statements of historical fact, including statements about Astellas’ beliefs and expectations and statements about Astellas’ proposed acquisition of OSI, are forward-looking statements and should be evaluated as such. Forward-looking statements include statements that may relate to Astellas’ plans, objectives, strategies, goals, future events, future revenues or performance, and other information that is not historical information. Factors that may materially affect such forward-looking statements include: Astellas’ ability to successfully complete the tender offer for OSI’s shares or realize the anticipated benefits of the transaction; delays in obtaining any approvals required for the transaction, or an inability to obtain them on the terms proposed or on the anticipated schedule; and the failure of any of the conditions to Astellas’ tender offer to be satisfied. Any information regarding OSI contained herein has been taken from, or is based upon, publicly available information. Although Astellas does not have any information that would indicate that any information contained herein is inaccurate or incomplete, Astellas has not had the opportunity to verify any such information and does not undertake any responsibility for the accuracy or completeness of such information. Astellas does not undertake, and specifically disclaims, any obligation or responsibility to update or amend any of the information above except as otherwise required by law. |