Exhibit 99.01

$375 Million Credit Facilities Public Lenders' Presentation November 14, 2013 |  |

Statement on Forward-Looking Information Some of the following information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended, and is intended to come within the safe-harbor protection provided by those sections. Forward-Looking Statements Certain statements in this presentation are forward-looking as defined in the Private Securities Litigation Reform Act of 1995. These statements involve certain risks and uncertainties that may be beyond our control and may cause our actual future results to differ materially from our current expectations both in connection with the Chapter 11 filings Patriot announced on July 9, 2012 and our business and financial prospects. No assurance can be made that these events will come to fruition. Patriot undertakes no obligation (and expressly disclaims any such obligation) to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. Factors that could affect our results include, but are not limited to: (i) the ability of Patriot and its subsidiaries to continue as a going concern, (ii) the ability of Patriot and its subsidiaries to operate within the restrictions and liquidity limitations of the post-petition credit facilities authorized by the Bankruptcy Court, (iii) the ability of Patriot and its subsidiaries to obtain Bankruptcy Court approval with respect to motions in the Chapter 11 cases, (iv) the ability of Patriot and its subsidiaries to successfully complete a reorganization under Chapter 11 and emerge from bankruptcy, which is dependent upon, among other things, the ability to implement changes to wage and benefit programs and postretirement benefit obligations consensually or pursuant to section 1113 and 1114 of the Bankruptcy Code, to minimize liabilities upon emergence and to obtain post-bankruptcy financing, (v) the effects of the bankruptcy filing on Patriot and its subsidiaries and the interests of various creditors, equity holders and other constituents, (vi) Bankruptcy Court rulings in the Chapter 11 cases and the outcome of the cases in general, (vii) the length of time Patriot and its subsidiaries will operate under the Chapter 11 cases, (viii) risks associated with third-party motions in the Chapter 11 cases, which may interfere with the ability of Patriot and its subsidiaries to develop one or more plans of reorganization and consummate such plans once they are developed, (ix) the potential adverse effects of the Chapter 11 proceedings on Patriot's liquidity or results of operations, (x) the ability to execute Patriot's business and restructuring plans, (xi) increased legal costs related to Patriot's bankruptcy filing and other litigation, and (xii) the ability of Patriot and its subsidiaries to maintain contracts that are critical to their operation, including to obtain and maintain normal terms with their vendors, customers, landlords and service providers and to retain key executives, managers and employees. In the event that the risks disclosed in Patriot's public filings and those discussed above cause results to differ materially from those expressed in Patriot's forward-looking statements, Patriot's business, financial condition, results of operations or liquidity, and the interests of creditors, equity holders and other constituents, could be materially adversely affected. For additional information concerning factors that could cause actual results to materially differ from those projected herein, please refer to Patriot's Form 10-K and Form 10-Q reports. When considering any investment, each lender should always conduct its own legal and financial due diligence before making any investment decision. 1 |  |

Table of Contents 1. Introduction 3 2. Transaction Overview 4 3. Knighthead Capital Management, LLC 8 4. Company Overview 9 5. Marketing Overview 15 6. Credit Highlights 21 7. Financial Overview 29 8. Syndication 36 9. Public Qand A 2 |  |

Introduction |  |

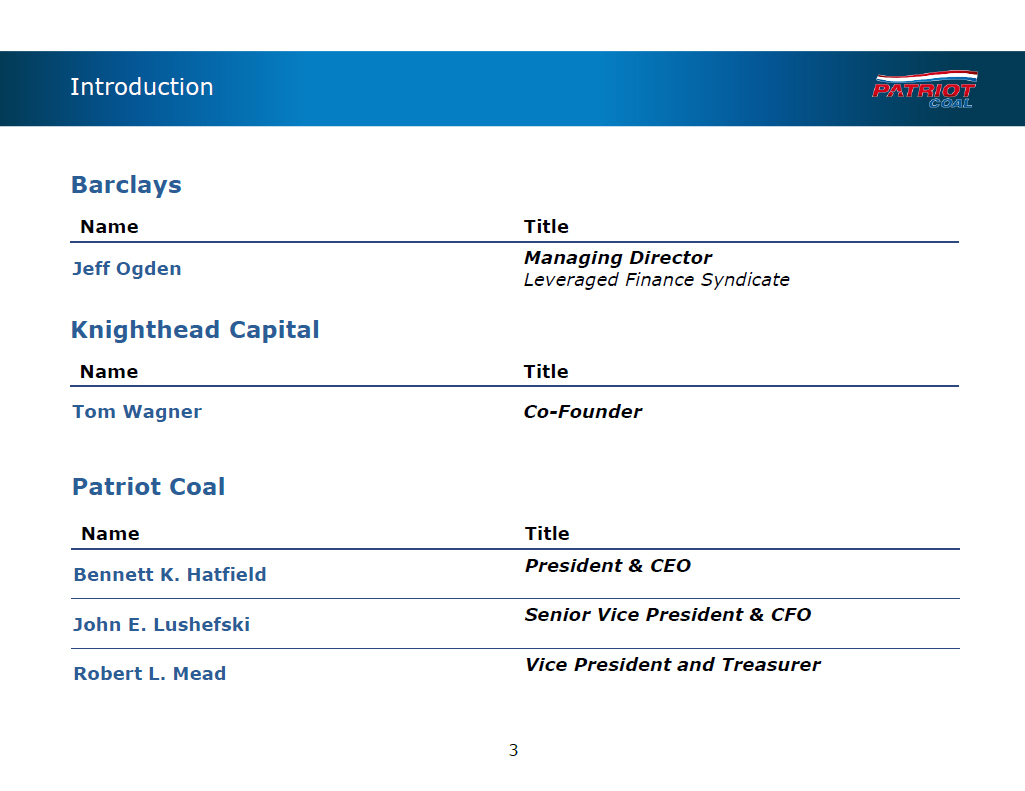

Introduction Barclays Name Title Managing Director Jeff Ogden Leveraged Finance Syndicate Knighthead Capital Name Title Tom Wagner Co-Founder Patriot Coal Name Title President and CEO Bennett K. Hatfield Senior Vice President and CFO John E. Lushefski Vice President and Treasurer Robert L. Mead |  |

Transaction Overview |  |

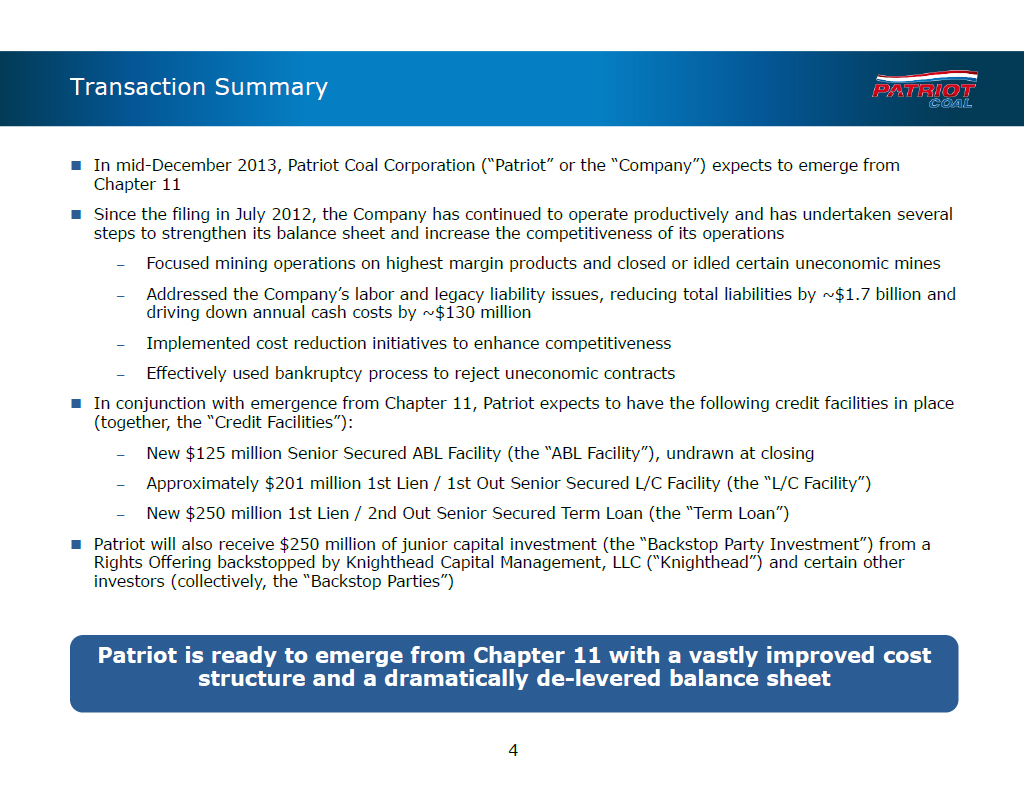

Transaction Summary

[] In mid-December 2013, Patriot Coal Corporation ("Patriot" or the "Company")

expects to emerge from Chapter 11 [] Since the filing in July 2012, the Company

has continued to operate productively and has undertaken several steps to

strengthen its balance sheet and increase the competitiveness of its operations

-- Focused mining operations on highest margin products and closed or idled

certain uneconomic mines

-- Addressed the Company's labor and legacy liability issues, reducing total

liabilities by ~$1.7 billion and driving down annual cash costs by ~$130

million

-- Implemented cost reduction initiatives to enhance competitiveness

-- Effectively used bankruptcy process to reject uneconomic contracts

[] In conjunction with emergence from Chapter 11, Patriot expects to have the

following credit facilities in place (together, the "Credit Facilities"):

-- New $125 million Senior Secured ABL Facility (the "ABL Facility"), undrawn

at closing

-- Approximately $201 million 1st Lien / 1st Out Senior Secured L/C Facility

(the "L/C Facility")

-- New $250 million 1st Lien / 2nd Out Senior Secured Term Loan (the "Term

Loan")

[] Patriot will also receive $250 million of junior capital investment (the

"Backstop Party Investment") from a Rights Offering backstopped by Knighthead

Capital Management, LLC ("Knighthead") and certain other investors

(collectively, the "Backstop Parties")

Patriot is ready to emerge from Chapter 11 with a vastly improved cost

structure and a dramatically de-levered balance sheet

|  |

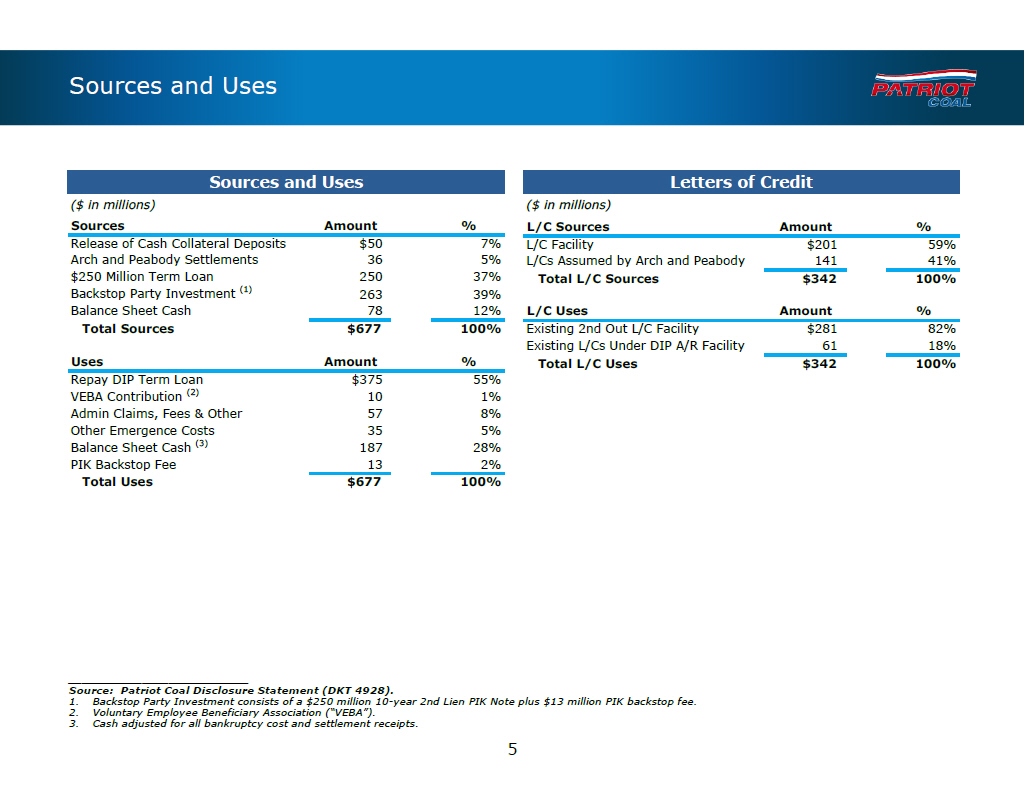

Sources and Uses

Sources and Uses Letters of Credit

($ in millions) ($ in millions)

Sources Amount % L/C Sources Amount %

Release of Cash Collateral Deposits $50 7% L/C Facility $201 59% Arch and

Peabody Settlements 36 5% L/Cs Assumed by Arch and Peabody 141 41% $250 Million

Term Loan 250 37% Total L/C Sources $342 100% Backstop Party Investment (1) 263

39% Balance Sheet Cash 78 12% L/C Uses Amount % Total Sources $677 100%

Existing 2nd Out L/C Facility $281 82% Existing L/Cs Under DIP A/R Facility 61

18%

Uses Amount % Total L/C Uses $342 100%

Repay DIP Term Loan $375 55% VEBA Contribution (2) 10 1% Admin Claims, Fees and

Other 57 8% Other Emergence Costs 35 5% Balance Sheet Cash (3) 187 28% PIK

Backstop Fee 13 2%

Total Uses $677 100%

___________________________

Source: Patriot Coal Disclosure Statement (DKT 4928).

1. Backstop Party Investment consists of a $250 million 10-year 2nd Lien PIK

Note plus $13 million PIK backstop fee.

2. Voluntary Employee Beneficiary Association ("VEBA").

3. Cash adjusted for all bankruptcy cost and settlement receipts.

5

|  |

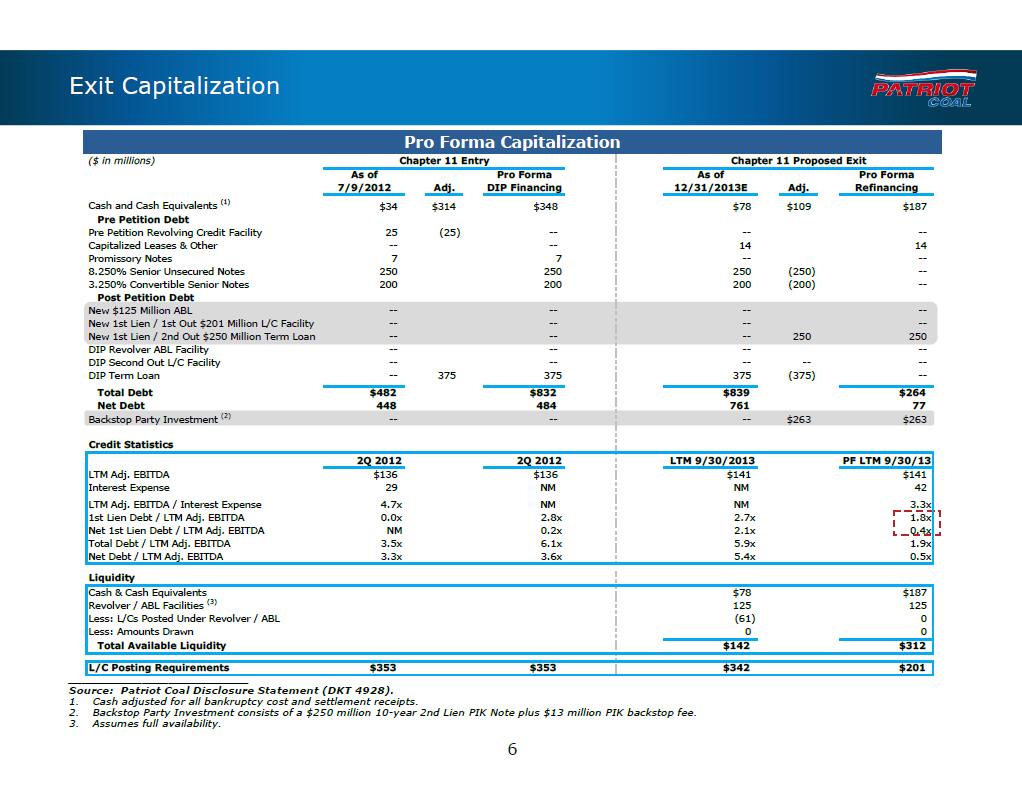

Exit Capitalization Pro Forma Capitalization ($ in millions) Chapter 11 Entry Chapter 11 Proposed Exit As of Pro Forma As of Pro Forma 7/9/2012 Adj. DIP Financing 12/31/2013E Adj. Refinancing Cash and Cash Equivalents (1) $34 $314 $348 $78 $109 $187 Pre Petition Debt Pre Petition Revolving Credit Facility 25 (25) -- -- --Capitalized Leases and Other -- -- 14 14 Promissory Notes 7 7 -- --8.250% Senior Unsecured Notes 250 250 250 (250) --3.250% Convertible Senior Notes 200 200 200 (200) -- Post Petition Debt New $125 Million ABL -- -- -- --New 1st Lien / 1st Out $201 Million L/C Facility -- -- -- --New 1st Lien / 2nd Out $250 Million Term Loan -- -- -- 250 250 DIP Revolver ABL Facility -- -- -- --DIP Second Out L/C Facility -- -- -- -- --DIP Term Loan -- 375 375 375 (375) -- Total Debt $482 $832 $839 $264 Net Debt 448 484 761 77 Backstop Party Investment (2) -- -- -- $263 $263 Credit Statistics 2Q 2012 2Q 2012 LTM 9/30/2013 PF LTM 9/30/13 LTM Adj. EBITDA $136 $136 $141 $141 Interest Expense 29 NM NM 42 LTM Adj. EBITDA / Interest Expense 4.7x NM NM 3.3x 1st Lien Debt / LTM Adj. EBITDA 0.0x 2.8x 2.7x 1.8x Net 1st Lien Debt / LTM Adj. EBITDA NM 0.2x 2.1x 0.4x Total Debt / LTM Adj. EBITDA 3.5x 6.1x 5.9x 1.9x Net Debt / LTM Adj. EBITDA 3.3x 3.6x 5.4x 0.5x Liquidity Cash and Cash Equivalents $78 $187 Revolver / ABL Facilities (3) 125 125 Less: L/Cs Posted Under Revolver / ABL (61) 0 Less: Amounts Drawn 0 0 Total Available Liquidity $142 $312 L/C Posting Requirements $353 $353 $342 $201 ___________________________ Source: Patriot Coal Disclosure Statement (DKT 4928). 1. Cash adjusted for all bankruptcy cost and settlement receipts. 2. Backstop Party Investment consists of a $250 million 10-year 2nd Lien PIK Note plus $13 million PIK backstop fee. 3. Assumes full availability. |  |

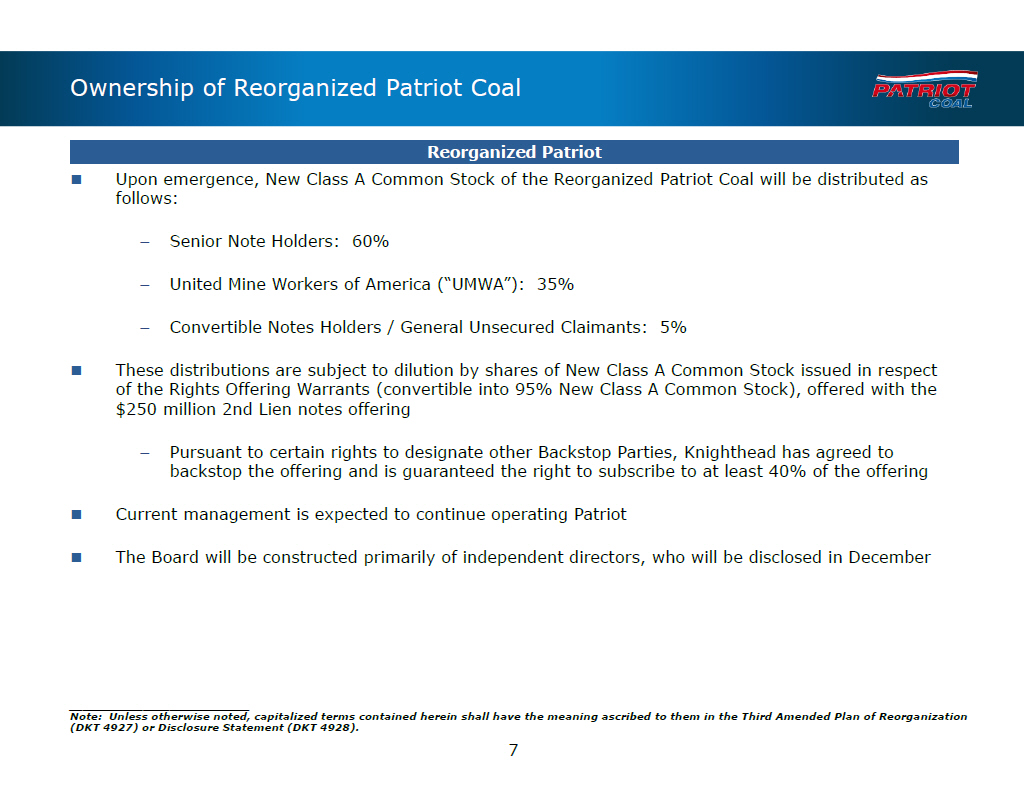

Ownership of Reorganized Patriot Coal

Reorganized Patriot

[] Upon emergence, New Class A Common Stock of the Reorganized Patriot Coal

will be distributed as follows:

-- Senior Note Holders: 60%

-- United Mine Workers of America ("UMWA"): 35%

-- Convertible Notes Holders / General Unsecured Claimants: 5%

[] These distributions are subject to dilution by shares of New Class A Common

Stock issued in respect of the Rights Offering Warrants (convertible into 95%

New Class A Common Stock), offered with the $250 million 2nd Lien notes

offering

-- Pursuant to certain rights to designate other Backstop Parties, Knighthead

has agreed to backstop the offering and is guaranteed the right to subscribe to

at least 40% of the offering

[] Current management is expected to continue operating Patriot

[] The Board will be constructed primarily of independent directors, who will

be disclosed in December

___________________________

Note: Unless otherwise noted, capitalized terms contained herein shall have the

meaning ascribed to them in the Third Amended Plan of Reorganization (DKT 4927)

or Disclosure Statement (DKT 4928).

|  |

Knighthead Capital Management, LLC |  |

Knighthead Capital Management, LLC Knighthead Capital Management, LLC [] Knighthead Capital Management, LLC is a New York-based registered investment adviser founded in 2008 [] The firm focuses on long-short investments and specializes in event driven, special situation opportunities across a broad array of industries [] Knighthead manages approximately $4.4 billion 8 |  |

Company Overview |  |

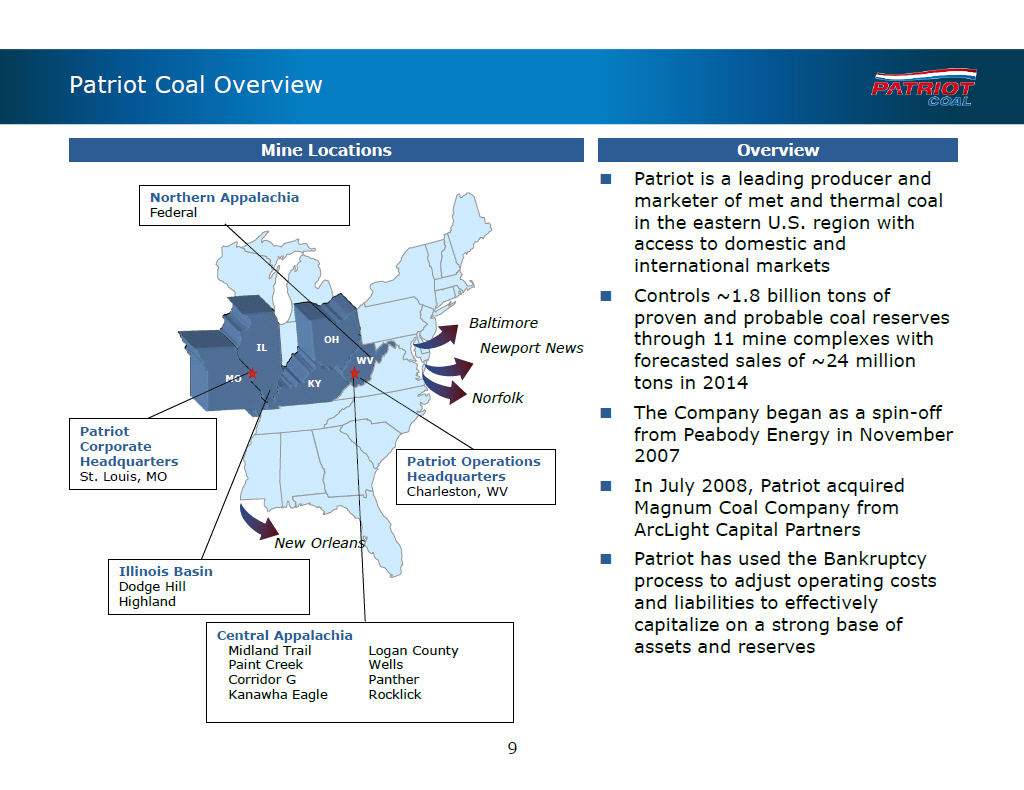

Patriot Coal Overview

Mine Locations Overview

[] Patriot is a leading producer and Northern Appalachia

marketer of met and thermal coal Federal in the eastern U.S. region with access

to domestic and international markets[] Controls ~1.8 billion tons of Baltimore

proven and probable coal reserves OH through 11 mine complexes with

IL Newport News

WV forecasted sales of ~24 million

MO

KY tons in 2014

Norfolk

[] The Company began as a spin-off Patriot

from Peabody Energy in November

Corporate 2007 Headquarters Patriot Operations

St. Louis, MO Headquarters

Charleston, WV [] In July 2008, Patriot acquired Magnum Coal Company from

ArcLight Capital Partners

New Orleans

[] Patriot has used the Bankruptcy Illinois Basin

process to adjust operating costs

Dodge Hill

Highland and liabilities to effectively capitalize on a strong base of

Central Appalachia

Midland Trail Logan County assets and reserves Paint Creek Wells Corridor G

Panther Kanawha Eagle Rocklick

9

|  |

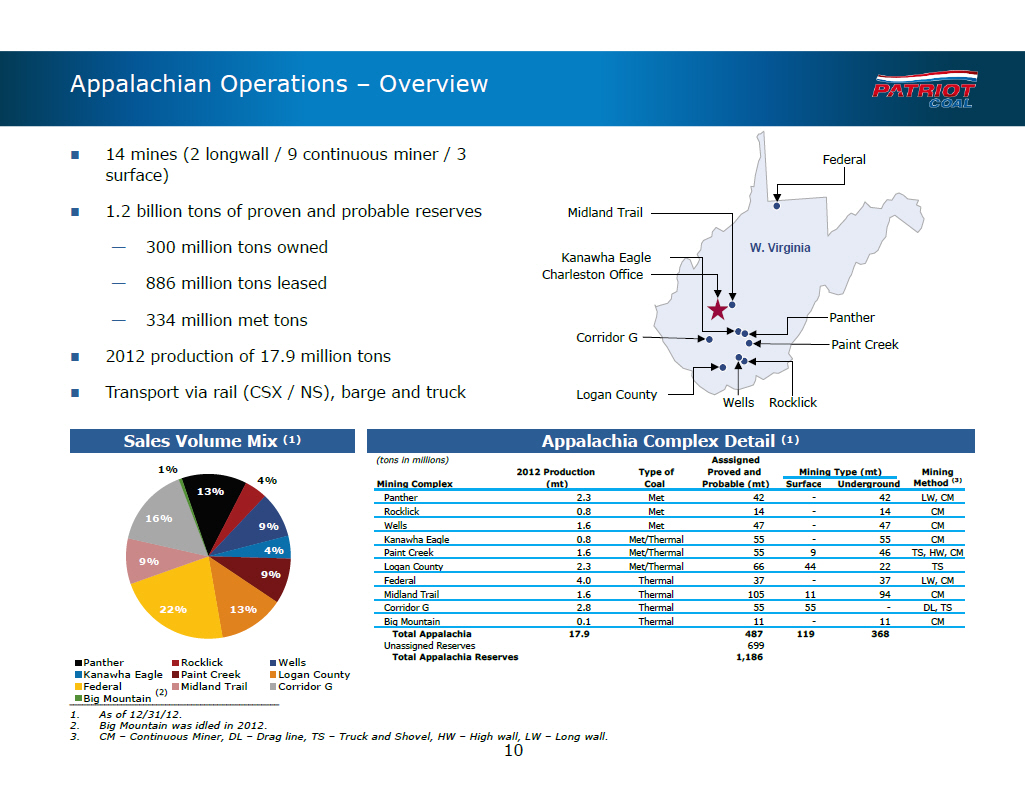

Appalachian Operations -- Overview

[] 14 mines (2 longwall / 9 continuous miner / 3 Federal surface)

[] 1.2 billion tons of proven and probable reserves Midland Trail

-- 300 million tons owned W. Virginia

Kanawha Eagle Charleston Office

-- 886 million tons leased

-- 334 million met tons Panther

Corridor G

Paint Creek

[] 2012 production of 17.9 million tons

[] Transport via rail (CSX / NS), barge and truck Logan County

Wells Rocklick

Sales Volume Mix (1) Appalachia Complex Detail (1)

(tons in millions) Asssigned

1% 2012 Production Type of Proved and Mining Type (mt) Mining

4% Mining Complex (mt) Coal Probable (mt) Surface Underground

Method (3) 13%

Panther 2.3 Met 42 - 42 LW, CM

Rocklick 0.8 Met 14 - 14 CM

16%

9% Wells 1.6 Met 47 - 47 CM

Kanawha Eagle 0.8 Met/Thermal 55 - 55 CM

4% Paint Creek 1.6 Met/Thermal 55 9 46 TS, HW, CM

9%

Logan County 2.3 Met/Thermal 66 44 22 TS

9%

Federal 4.0 Thermal 37 - 37 LW, CM

Midland Trail 1.6 Thermal 105 11 94 CM

22% 13% Corridor G 2.8 Thermal 55 55 - DL, TS Big Mountain 0.1 Thermal 11 - 11

CM

Total Appalachia 17.9 487 119 368

Unassigned

Reserves 699 Panther Rocklick Wells Total Appalachia Reserves 1,186

Kanawha Eagle Paint Creek Logan County Federal Midland Trail Corridor G

(2)

________________________________________________Big Mountain

1. As of 12/31/12.

2. Big Mountain was idled in 2012.

3. CM -- Continuous Miner, DL -- Drag line, TS -- Truck and Shovel, HW -- High

wall, LW -- Long wall.

10

|  |

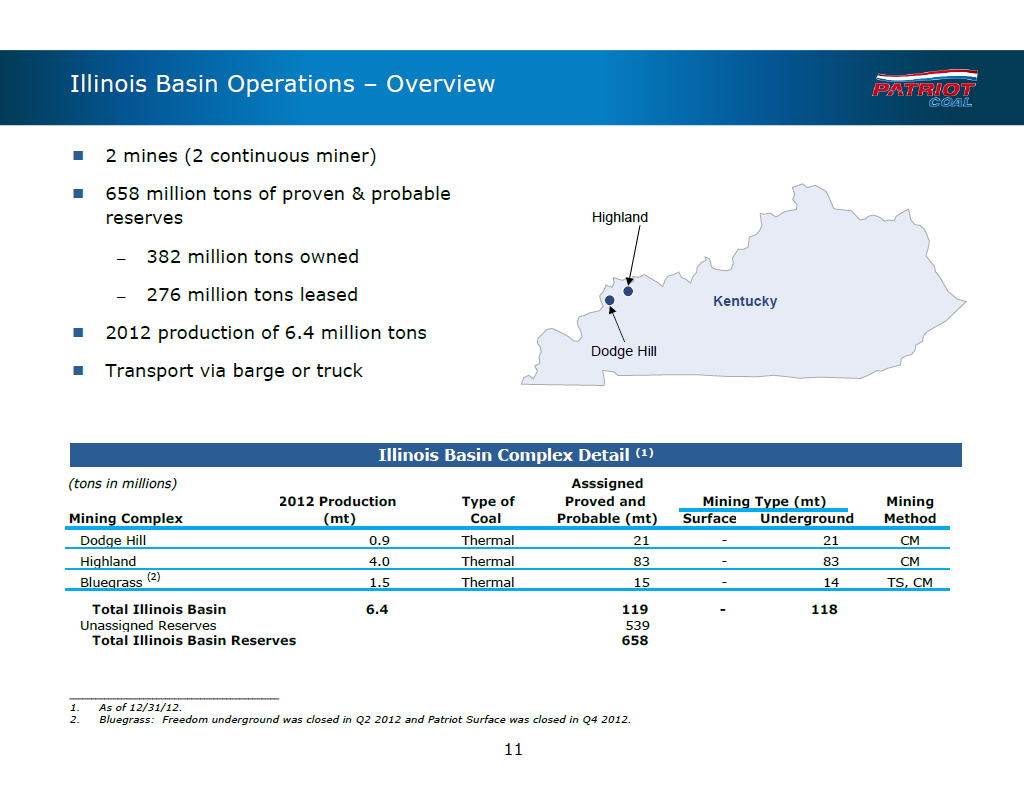

Illinois Basin Operations -- Overview

[] 2 mines (2 continuous miner) [] 658 million tons of proven and probable

reserves Highland

-- 382 million tons owned

-- 276 million tons leased Kentucky [] 2012 production of 6.4 million

tons

Dodge Hill

[] Transport via barge or truck

Illinois Basin Complex Detail (1)

(tons in millions) Asssigned

2012 Production Type of Proved

and Mining Type (mt) Mining Mining Complex (mt) Coal Probable (mt) Surface

Underground Method

Dodge Hill 0.9 Thermal 21 - 21 CM Highland 4.0 Thermal 83 - 83 CM Bluegrass (2)

1.5 Thermal 15 - 14 TS, CM

Total Illinois Basin 6.4 119 - 118

Unassigned Reserves 539

Total Illinois Basin Reserves 658

________________________________________________

1. As of 12/31/12.

2. Bluegrass: Freedom underground was closed in Q2 2012 and Patriot Surface was

closed in Q4 2012.

11

|  |

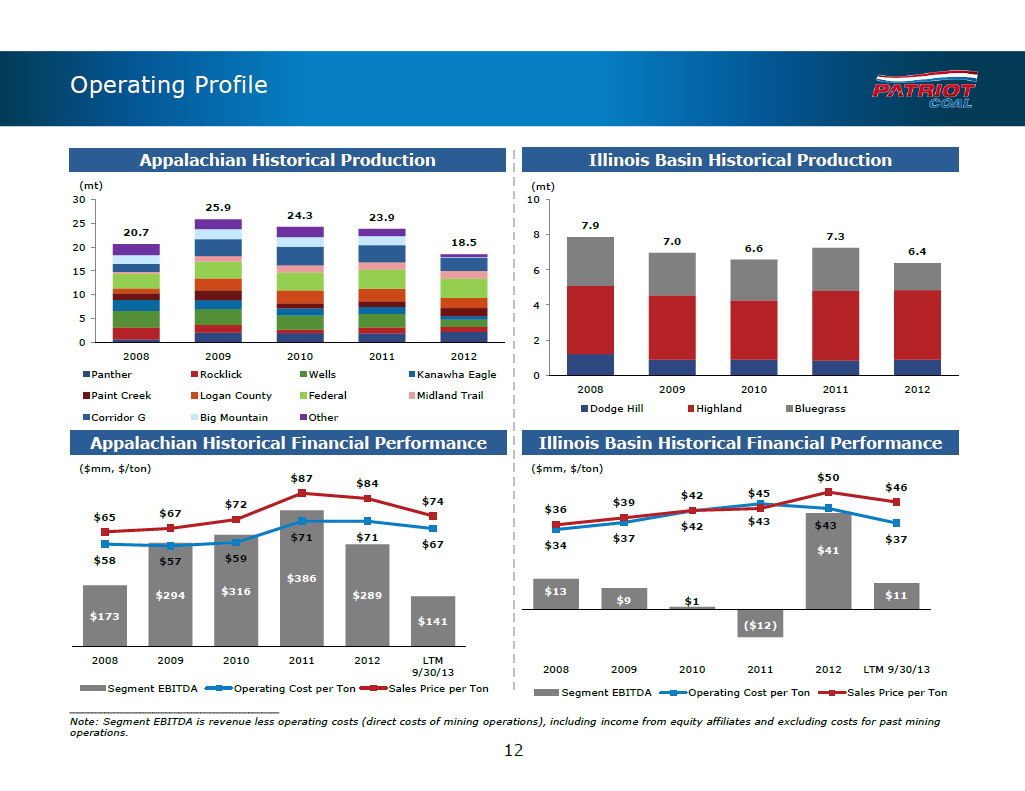

Operating Profile

Appalachian Historical Production Illinois Basin Historical Production

(mt) (mt)

30 10

25.9

24.3 23.9

25 7.9

20.7 8 7.3 18.5 7.0

20 6.6 6.4

15 6 10 4 5

0 2 2008 2009 2010 2011 2012 Panther Rocklick Wells Kanawha Eagle 0

2008 2009 2010 2011 2012 Paint Creek Logan County

Federal Midland Trail Dodge Hill Highland Bluegrass Corridor G Big Mountain

Other

Appalachian Historical Financial Performance Illinois Basin Historical

Financial Performance

($mm, $/ton) $100 ($mm, $/ton) $87 $50 $84 $90 $46 $42 $45 $72 $74 $80 $39 $67

$36 $65 $43 $70 $42 $43 $71 $71 $60 $37 $37 $67 $34 $41 $58 $57 $59 $50 $386

$40 $294 $316 $289 $30 $13 $11 $9 $1 $20 $173 $141 ($12) $10 $0 2008 2009 2010

2011 2012 LTM

9/30/13 2008

2009 2010 2011 2012 LTM 9/30/13 Segment EBITDA Operating Cost per Ton Sales

Price per Ton Segment EBITDA Operating Cost per Ton Sales Price per Ton

________________________________________________

Note: Segment EBITDA is revenue less operating costs (direct costs of mining

operations), including income from equity affiliates and excluding costs for

past mining operations.

12

|  |

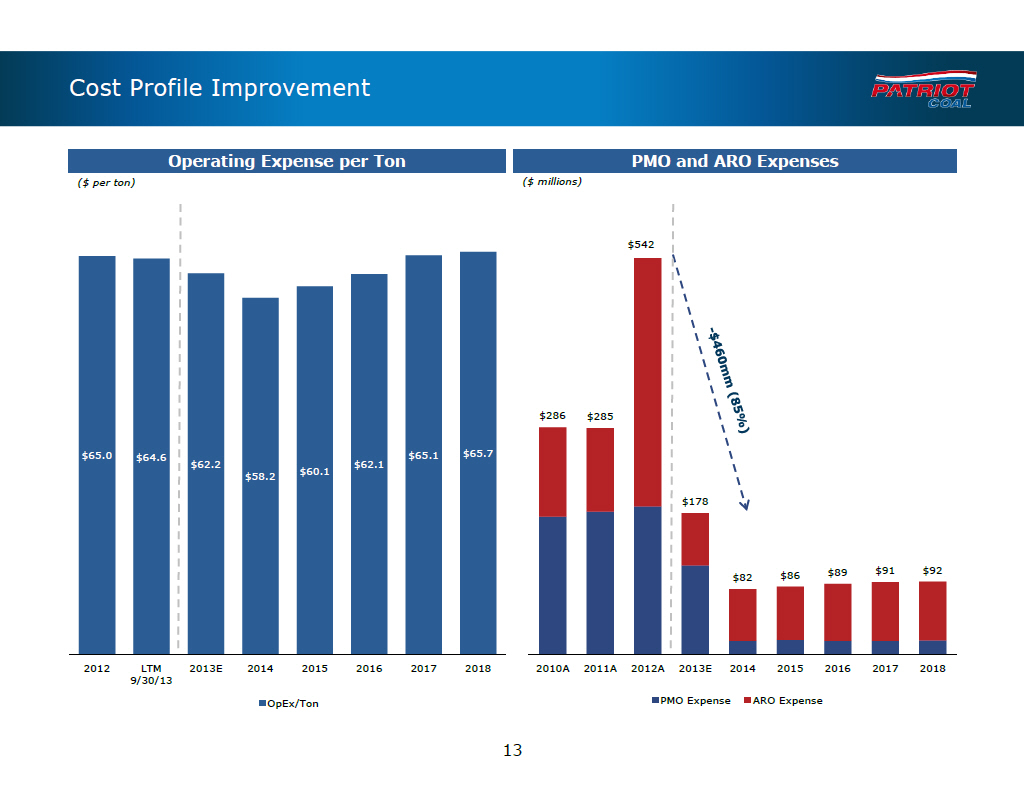

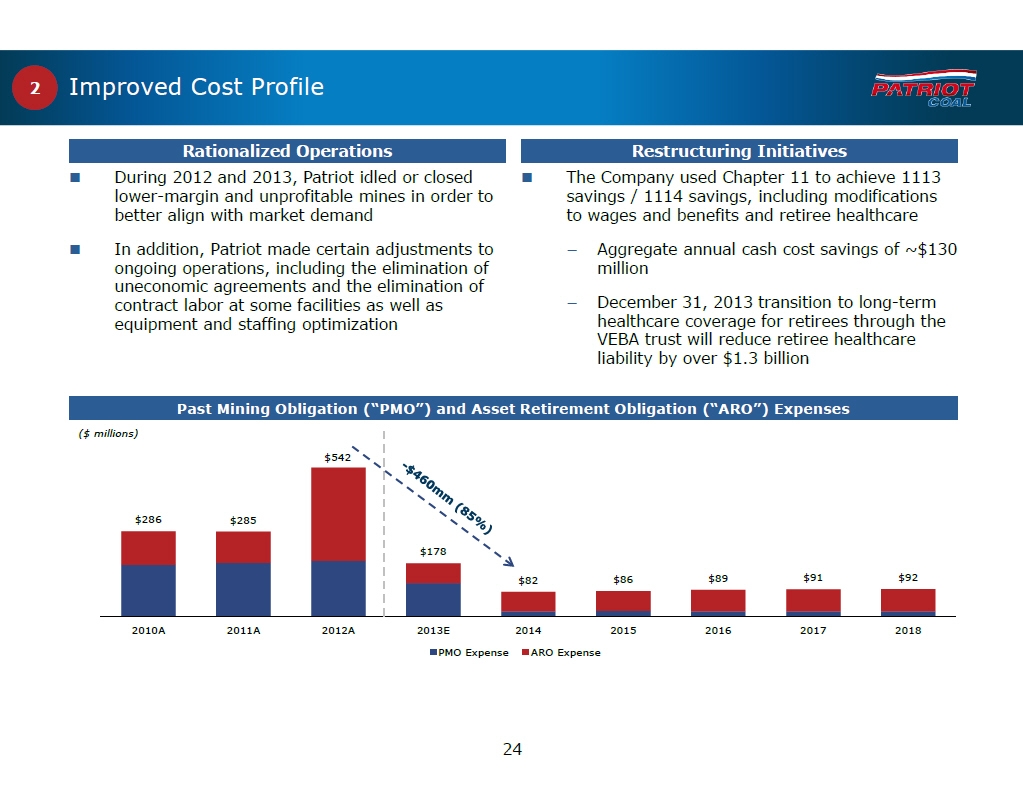

Cost Profile Improvement

Operating Expense per Ton PMO and ARO Expenses

($ per ton) ($ millions)

$542

$286 $285

$65.0 $64.6 $65.1 $65.7 $62.2 $62.1 $60.1 $58.2

$178

$86 $89 $91 $92 $82

2012 LTM 2013E 2014 2015 2016 2017 2018 2010A 2011A 2012A 2013E 2014 2015 2016

2017 2018 9/30/13 OpEx/Ton PMO Expense ARO Expense

13

|  |

Substantial Progress on Selenium Treatment Costs [] At 9/30/13 Patriot's total selenium remediation liability was estimated at $433 million, primarily based on outdated treatment methods in an area where technology is evolving quickly [] Successful negotiation of compliance deadline extensions has allowed Patriot to use new Selenium treatment technologies that are leading to major cost reductions -- The high-cost Fluidized Bed Reactor (FBR) technology applied at the Logan complex has been progressively replaced by GE's ABMet process, Iron Facilitated Selenium Reduction (IFSeR), and (most recently) by Bio-Chemical Reactor (BCR) -- BCR technology is projected to have a much lower capital and operating cost [] Within a 2-year timeframe, capital cost for a (900 gallons per minute, "gpm") treatment facility has dropped from $32 million for FBR to $17 million for ABMet and to $4 million for BCR [] Projected annual operating costs for a 900 gpm treatment facility have declined in similar fashion, from $2.4 million FBR to $1.5 million for ABMet and to $0.2 million for BCR [] Patriot's ARO Liability associated with Selenium is expected to decrease substantially as BCR and similar developing technologies are proven to be effective -- In Q3 2013, Patriot updated their liability to reflect BCR utilization only for the smallest category of outfalls (200 gpm or less), resulting in a $31.4 million reduction (to $433.1 million) -- We believe continued application and development of this emerging technology could lead to substantial reductions in the Company's Selenium liability 14 |  |

Marketing Overview |  |

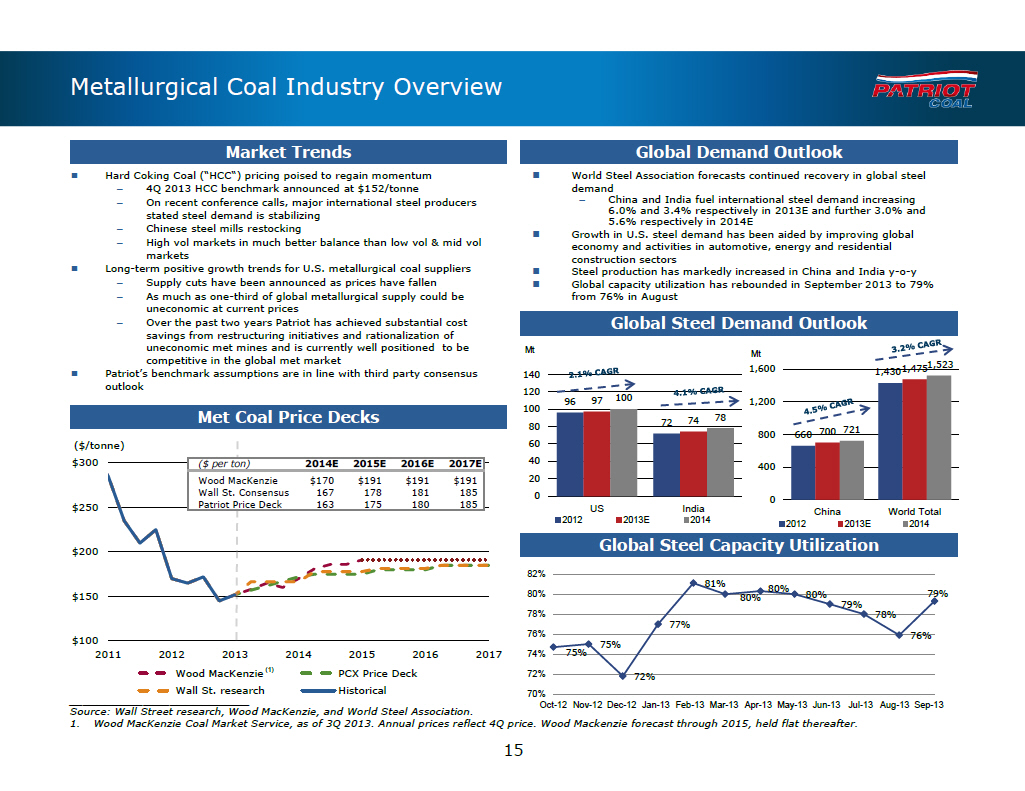

Metallurgical Coal Industry Overview

Market Trends Global Demand Outlook

[] Hard Coking Coal ("HCC") pricing poised to regain momentum [] World Steel

Association forecasts continued recovery in global steel

-- 4Q 2013 HCC benchmark announced at $152/tonne demand

-- On recent conference calls, major international steel producers -- China and

India fuel international steel demand increasing stated steel demand is

stabilizing 6.0% and 3.4% respectively in 2013E and further 3.0% and 5.6%

respectively in 2014E

-- Chinese steel mills restocking

[] Growth in U.S. steel demand has been aided by improving global

-- High vol markets in much better balance than low vol and mid vol

economy and activities in automotive, energy and residential markets

construction sectors [] Long-term positive growth trends for U.S. metallurgical

coal suppliers [] Steel production has markedly increased in China and India

y-o-y

-- Supply cuts have been announced as prices have fallen [] Global capacity

utilization has rebounded in September 2013 to 79%

-- As much as one-third of global metallurgical supply could be from 76% in

August uneconomic at current prices

-- Over the past two years Patriot has achieved substantial cost

Global Steel Demand Outlook savings from restructuring initiatives and

rationalization of uneconomic met mines and is currently well positioned to be

Mt Mt competitive in the global met market 1,523 Patriot's benchmark

assumptions are in line with third party consensus 1,600 1,430 1,475 [] 140

outlook 120

96 97 100 1,200 100

Met Coal Price Decks 74 78

80 72

800 700

721 660 ($/tonne) 60 $300 ($ per ton) 2014E 2015E 2016E 2017E 40 400 Wood

MacKenzie $170 $191 $191 $191 20 Wall St. Consensus 167 178 181 185 0 Patriot

Price Deck 163 175 180 185 0 $250 US India China World Total 2012 2013E 2014

2012 2013E 2014

$200 Global Steel Capacity Utilization

82%

81%

80%

$150 80% 80% 80% 79% 79% 78% 78% 77% 76% 76% $100 75% 2011 2012 2013 2014 2015

2016 2017 74% 75% Wood MacKenzie (1) PCX Price Deck 72% 72% Wall St. research

Historical 70%

___________________________ Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

May-13 Jun-13 Jul-13 Aug-13 Sep-13

Source: Wall Street research, Wood MacKenzie, and World Steel Association.

1. Wood MacKenzie Coal Market Service, as of 3Q 2013. Annual prices reflect 4Q

price. Wood Mackenzie forecast through 2015, held flat thereafter.

15

|  |

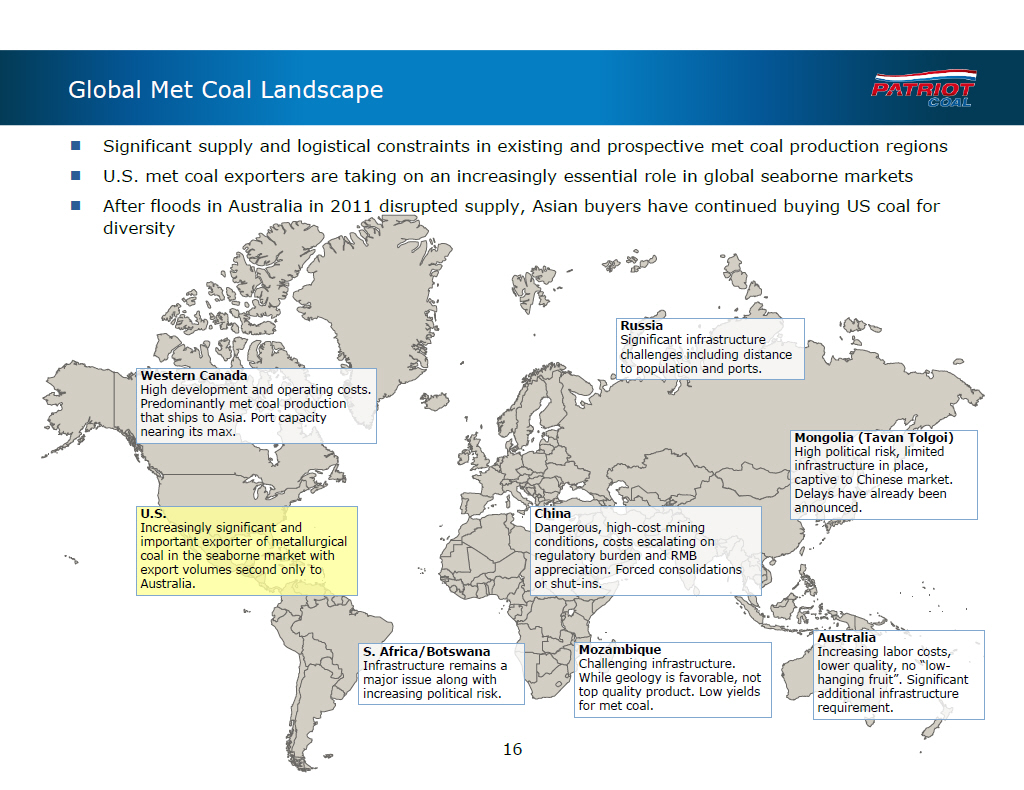

Global Met Coal Landscape [] Significant supply and logistical constraints in existing and prospective met coal production regions [] U.S. met coal exporters are taking on an increasingly essential role in global seaborne markets [] After floods in Australia in 2011 disrupted supply, Asian buyers have continued buying US coal for diversity Russia Significant infrastructure challenges including distance to population and ports. Western Canada High development and operating costs. Predominantly met coal production that ships to Asia. Port capacity nearing its max. Mongolia (Tavan Tolgoi) High political risk, limited infrastructure in place, captive to Chinese market. Delays have already been announced. U.S. China Increasingly significant and Dangerous, high-cost mining important exporter of metallurgical conditions, costs escalating on coal in the seaborne market with regulatory burden and RMB export volumes second only to appreciation. Forced consolidations Australia. or shut-ins. Australia S. Africa/Botswana Mozambique Increasing labor costs, Infrastructure remains a Challenging infrastructure. lower quality, no "low-major issue along with While geology is favorable, not hanging fruit". Significant increasing political risk. top quality product. Low yields additional infrastructure for met coal. requirement. 16 |  |

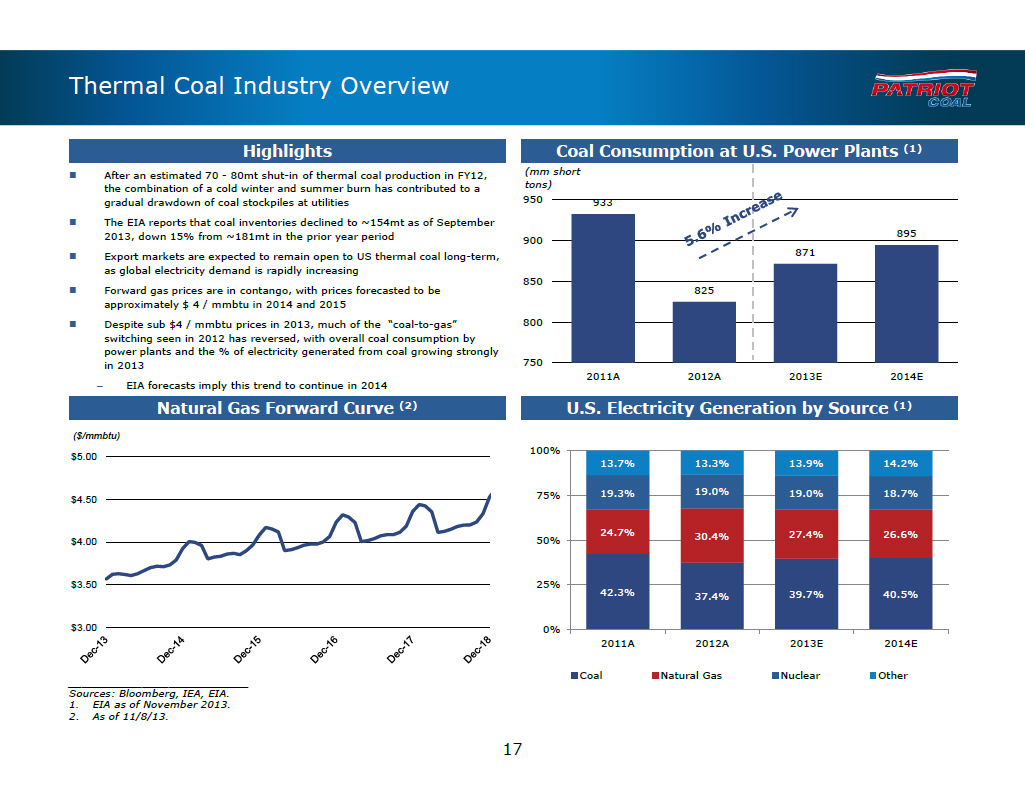

Thermal Coal Industry Overview

Highlights Coal Consumption at U.S. Power Plants (1)

[] After an estimated 70 - 80mt shut-in of thermal coal production in FY12, (mm

short the combination of a cold winter and summer burn has contributed to a

tons) gradual drawdown of coal stockpiles at utilities 950 933 [] The EIA

reports that coal inventories declined to ~154mt as of September

2013, down 15% from ~181mt in the prior year period 895 900[] Export

markets are expected to remain open to US thermal coal long-term, 871 as global

electricity demand is rapidly increasing 850[] Forward gas prices are in

contango, with prices forecasted to be 825 approximately $ 4 / mmbtu in 2014

and 2015 [] Despite sub $4 / mmbtu prices in 2013, much of the "coal-to-gas"

800 switching seen in 2012 has reversed, with overall coal consumption by power

plants and the % of electricity generated from coal growing strongly in 2013

750 2011A 2012A 2013E 2014E

-- EIA forecasts imply this trend to continue in 2014

Natural Gas Forward Curve (2) U.S. Electricity Generation by Source (1)

($/mmbtu)

100% $5.00

13.7% 13.3% 13.9% 14.2%

75% 19.3% 19.0% 19.0% 18.7% $4.50

24.7% 30.4% 27.4% 26.6% $4.00 50%

$3.50 25%

42.3% 37.4% 39.7% 40.5%

$3.00 0%

2011A 2012A 2013E 2014E

Coal Natural Gas Nuclear Other

___________________________ Sources: Bloomberg, IEA, EIA.

1. EIA as of November 2013.

2. As of 11/8/13.

17

|  |

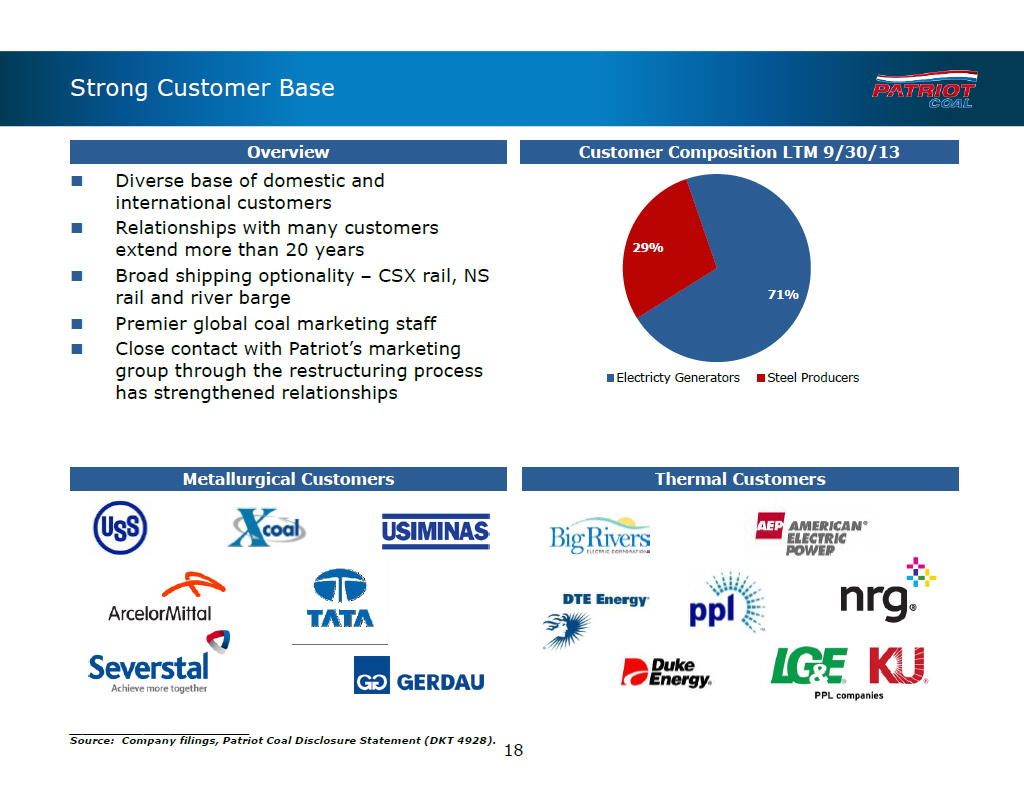

Strong Customer Base Overview Customer Composition LTM 9/30/13 [] Diverse base of domestic and international customers [] Relationships with many customers extend more than 20 years 29% [] Broad shipping optionality -- CSX rail, NS rail and river barge 71% [] Premier global coal marketing staff[] Close contact with Patriot's marketing group through the restructuring process Electricty Generators Steel Producers has strengthened relationships Metallurgical Customers Thermal Customers ___________________________ Source: (Company filings, Patriot Coal Disclosure Statement (DKT 4928).) 18 |  |

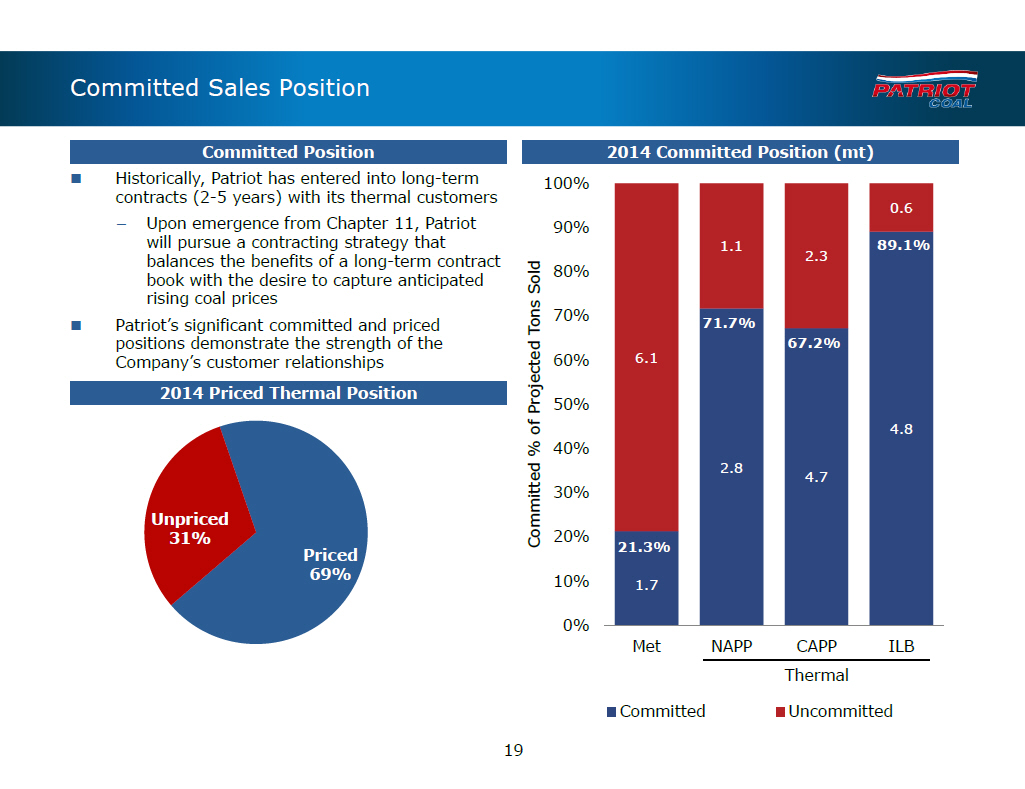

Committed Sales Position

Committed Position 2014 Committed Position (mt)

[] Historically, Patriot has entered into long-term 100% contracts (2-5 years)

with its thermal customers

0.6

-- Upon emergence from Chapter 11, Patriot 90% will pursue a contracting

strategy that 1.1 89.1% balances the benefits of a long-term contract 2.3 80%

book with the desire to capture anticipated rising coal prices 70% 71.7%

[] Patriot's significant committed and priced Tons Sold positions demonstrate

the strength of the Projected 67.2% Company's customer relationships 60% 6.1

2014 Priced Thermal Position

50%

4.8 % of 40% Committed 2.8 4.7 30%

Unpriced

31% 20%

21.3%

Priced 69% 10% 1.7

0%

Met NAPP CAPP ILB Thermal

Committed Uncommitted

19

|  |

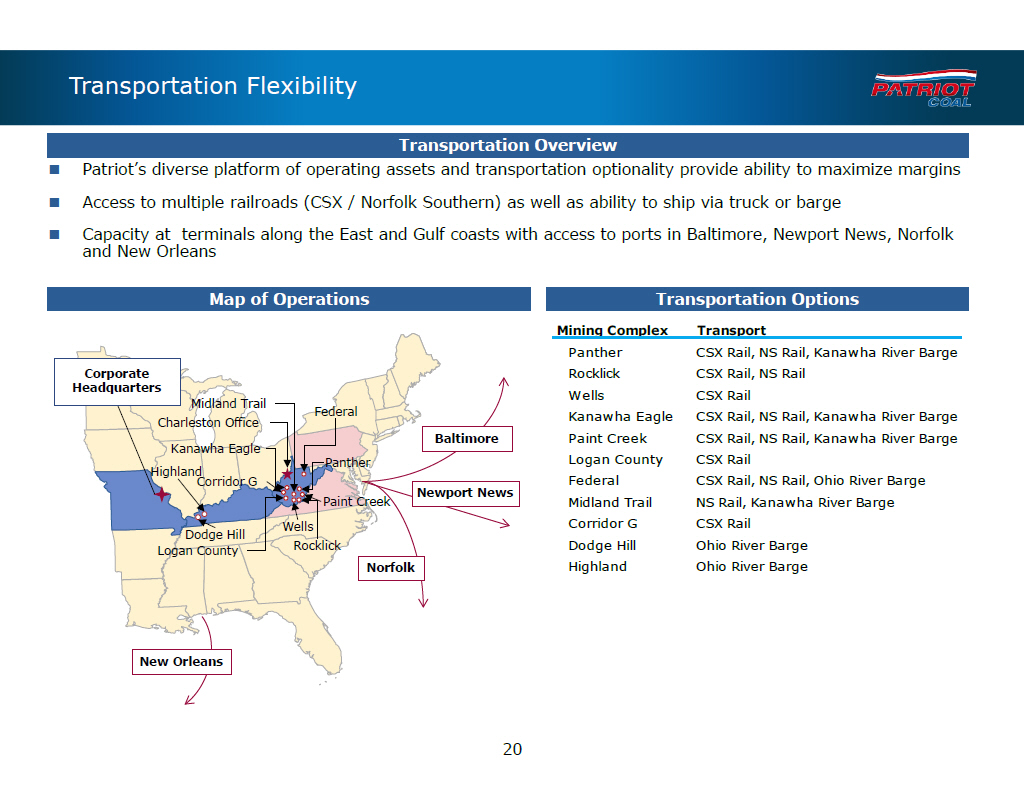

Transportation Flexibility

Transportation Overview

[] Patriot's diverse platform of operating assets and transportation

optionality provide ability to maximize margins [] Access to multiple railroads

(CSX / Norfolk Southern) as well as ability to ship via truck or barge []

Capacity at terminals along the East and Gulf coasts with access to ports in

Baltimore, Newport News, Norfolk and New Orleans

Map of Operations Transportation Options

Mining Complex Transport

Panther CSX Rail, NS Rail, Kanawha River Barge

Corporate Rocklick CSX Rail, NS Rail

Headquarters

Wells CSX Rail Midland Trail

Federal Kanawha Eagle CSX Rail, NS Rail,

Kanawha River Barge Charleston Office Baltimore Paint Creek CSX Rail, NS Rail,

Kanawha River Barge Kanawha Eagle Panther Logan County CSX Rail Highland

Corridor G Federal CSX Rail, NS Rail, Ohio River Barge

Newport News

Paint Creek Midland Trail NS Rail, Kanawha

River Barge Wells Corridor G CSX Rail Dodge Hill Logan County Rocklick Dodge

Hill Ohio River Barge Norfolk Highland Ohio River Barge

New Orleans

20

|  |

Credit Highlights |  |

|

1 Improved Credit and Liquidity Profile

Patriot has greatly improved its balance sheet by reducing debt and outstanding

obligations

Summary Improvements Total Liabilities (1)

[] Significantly lowered total liabilities ($ millions)

$3,391 $3,500 $378

[] Vastly reduced post-retirement benefit $3,000

$418 $2,500

obligations ("PRBOs") through the $474

$2,000 $1,701 $738

1113/1114 process $1,500 $391

$212

$1,000 $264

[] Increased liquidity and reduced debt $1,384

$500 $743 $91 $0 PRBOs AROs Total Debt A/P and Accrued Exp. Other

Total Liquidity (2) Total Debt (1)

($ millions) ($ millions) $350 $312 $500 $474 $300 $125 million $400 $250

ABL $200

$300 $264 $150 $200 $100 $187 million Cash $46 $100 $50 $0 $0

Pre-Petition Pro Forma Exit Pre-Petition Pro Forma Exit

___________________________

Source: Patriot Coal Disclosure Statement (DKT 4928).

Note: Pre-petition figures as of 6/30/12, assuming no availability under

pre-petition credit facilities. 1. Excluding Backstop Party Investment.

2. Adjusted for all bankruptcy cost and settlement receipts. Assumes full

availability under the $125mm ABL Facility.

22

|  |

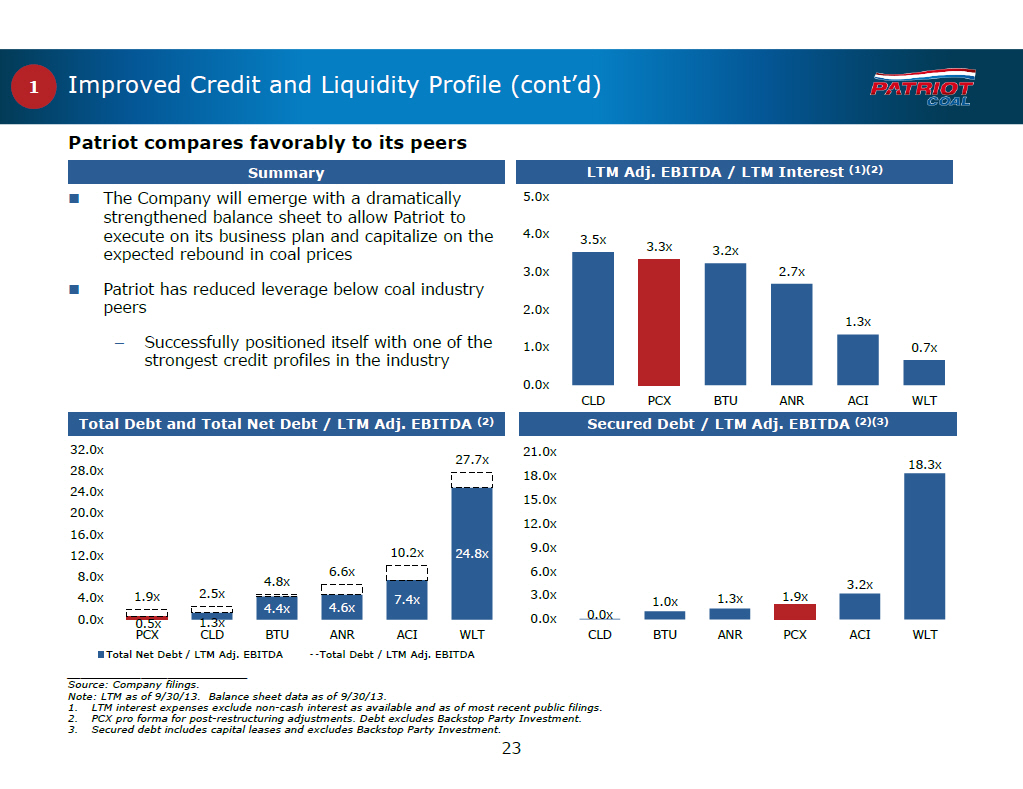

1 Improved Credit and Liquidity Profile (cont'd)

Patriot compares favorably to its peers

Summary LTM Adj. EBITDA / LTM Interest (1)(2)

[] The Company will emerge with a dramatically 5.0x strengthened balance sheet

to allow Patriot to execute on its business plan and capitalize on the 4.0x

3.5x

3.3x 3.2x

expected rebound in coal prices

3.0x 2.7x

[] Patriot has reduced leverage below coal industry peers 2.0x

1.3x

-- Successfully positioned itself with one of the 1.0x 0.7x strongest credit

profiles in the industry

0.0x

CLD PCX BTU ANR ACI WLT

Total Debt and Total Net Debt / LTM Adj. EBITDA (2) Secured Debt / LTM Adj.

EBITDA (2)(3)

32.0x 21.0x

27.7x 18.3x 28.0x 18.0x 24.0x 15.0x 20.0x 12.0x 16.0x 10.2x 9.0x 12.0x

24.8x 8.0x 6.6x 6.0x 4.8x 3.2x 4.0x 1.9x 2.5x 3.0x 1.3x 1.9x 7.4x 1.0x 4.4x

4.6x 0.0x 0.0x 0.0x 0.5x 1.3x PCX CLD BTU ANR ACI WLT CLD BTU ANR PCX ACI WLT

Total Net Debt / LTM Adj. EBITDA - - Total Debt / LTM Adj. EBITDA

___________________________ Source: Company filings.

Note: LTM as of 9/30/13. Balance sheet data as of 9/30/13.

1. LTM interest expenses exclude non-cash interest as available and as of most

recent public filings.

2. PCX pro forma for post-restructuring adjustments. Debt excludes Backstop

Party Investment.

3. Secured debt includes capital leases and excludes Backstop Party

Investment.

23

|  |

|

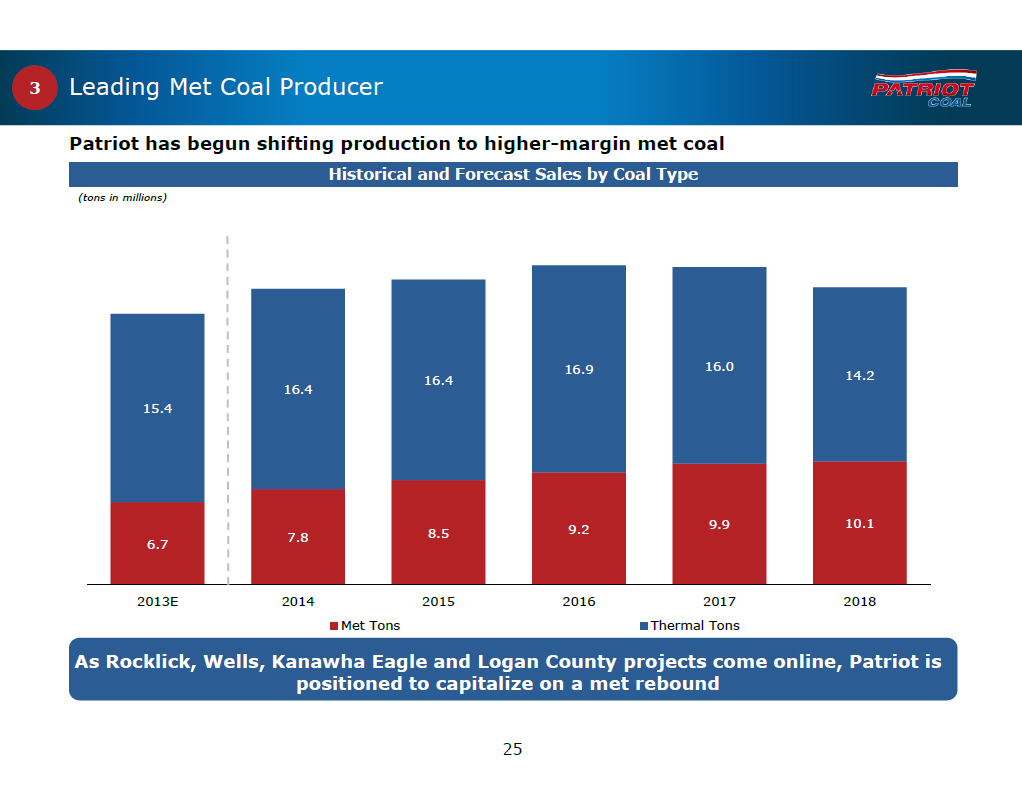

3 Leading Met Coal Producer

Patriot has begun shifting production to higher-margin met coal

Historical and Forecast Sales by Coal Type

(tons in millions)

16.9 16.0

16.4 14.2 16.4

15.4

9.2 9.9 10.1 7.8 8.5 6.7

2013E 2014 2015 2016 2017 2018 Met Tons Thermal Tons

As Rocklick, Wells, Kanawha Eagle and Logan County projects come online,

Patriot is positioned to capitalize on a met rebound

25

|  |

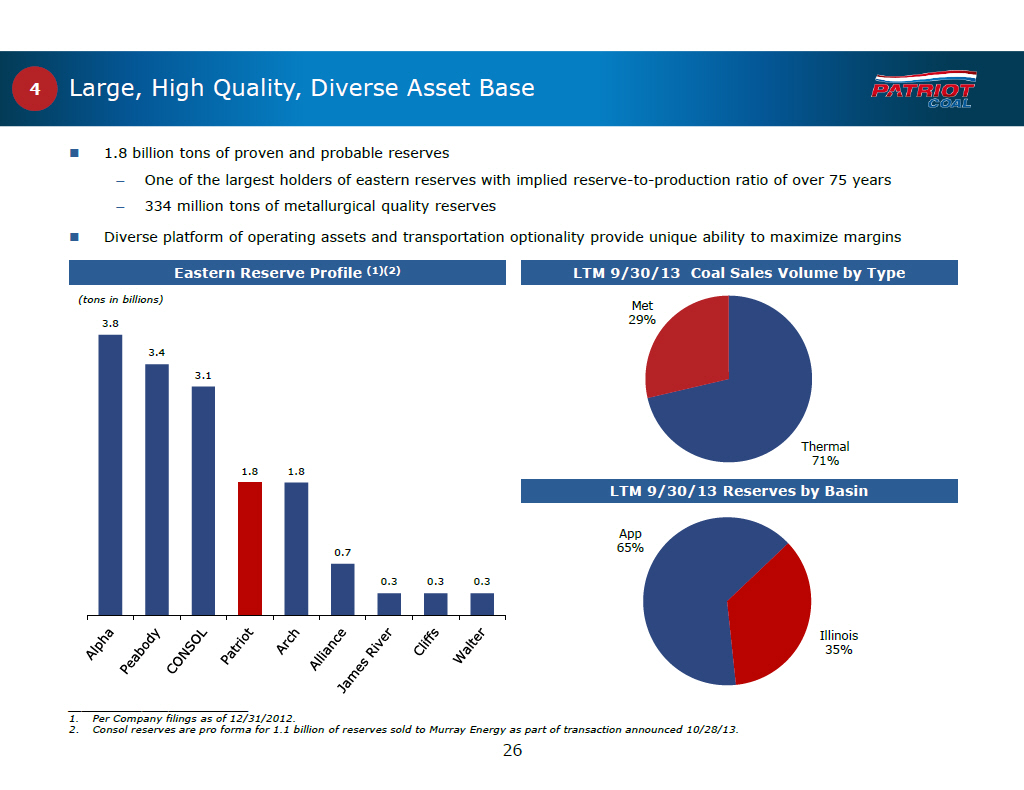

4 Large, High Quality, Diverse Asset Base

[] 1.8 billion tons of proven and probable reserves

-- One of the largest holders of eastern reserves with implied

reserve-to-production ratio of over 75 years

-- 334 million tons of metallurgical quality reserves

[] Diverse platform of operating assets and transportation optionality provide

unique ability to maximize margins

Eastern Reserve Profile (1)(2) LTM 9/30/13 Coal Sales Volume by Type

(tons in billions)

Met 3.8 29%

3.4 3.1

Thermal 71% 1.8 1.8

LTM 9/30/13 Reserves by Basin

App 0.7 65%

0.3 0.3 0.3

Illinois 35%

___________________________

1. Per Company filings as of 12/31/2012.

2. Consol reserves are pro forma for 1.1 billion of reserves sold to Murray

Energy as part of transaction announced 10/28/13.

26

|  |

5 Operational Flexibility Patriot's operational flexibility has allowed it to respond aggressively to difficult market conditions while maintaining the ability to ramp up quickly in response to increased demand Flexible Operating Platform Positioned for Market Rebound [] Patriot has a diverse product base with [] Patriot maintains the ability to react to the different grades and characteristics for met expected rebound in coal pricing and and thermal coal. This diversity of coal quickly ramp up production grades allows Patriot to address changing market needs as well ability to blend coal [] By utilizing its existing mining complexes, to customers' precise specifications Patriot is able to expand its met portfolio in a capital-efficient manner[] Patriot has idled or reduced production at mines with marginal returns and focused -- Rocklick: restart idled mines (high-vol on low-cost, higher-margin met and A met) thermal mines in its portfolio -- Replaced higher-cost contract mines -- Wells: shift production to new areas with lower-cost captive operations (high vol A met) -- Rationalized higher-cost production -- Kanawha Eagle: continue to develop sources throughout 2012 and 2013 and expand North Eagle operations -- Concentrated efforts at lower-cost complexes -- Idled certain uneconomic mines (with ability to start up when prices rebound) As market conditions improve, Patriot will continue to shift its production capacity to higher margin met coal mines and lower cost thermal mines ___________________________ Source: Company filings. 27 |  |

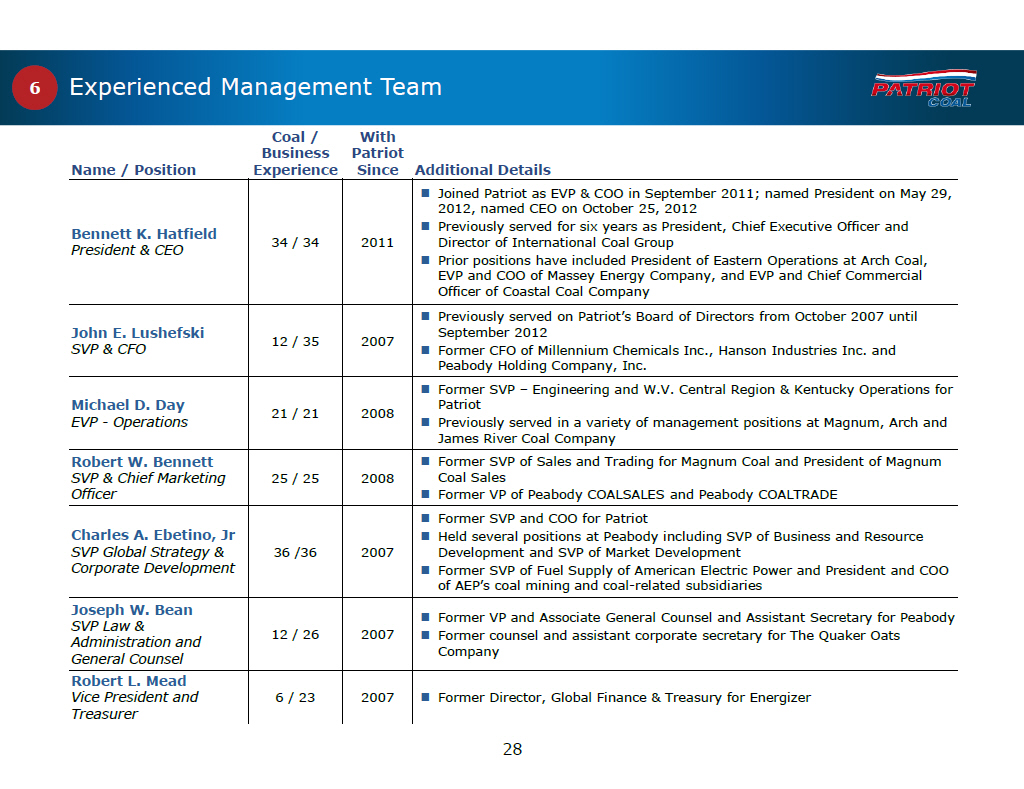

6 Experienced Management Team

Coal / With Business Patriot

Name / Position Experience Since Additional Details

[]

Joined Patriot as EVP and COO in September 2011; named President on

May 29, 2012,

named CEO on October 25, 2012 Bennett K. Hatfield [] Previously served for six

years as President, Chief Executive Officer and 34 / 34 2011 Director of

International Coal Group

President and CEO

[] Prior positions have included President of Eastern Operations at Arch Coal,

EVP and COO of Massey Energy Company, and EVP and Chief Commercial Officer of

Coastal Coal Company [] Previously served on Patriot's Board of Directors from

October 2007 until

John E. Lushefski September 2012 12 / 35 2007

SVP and CFO [] Former CFO of Millennium Chemicals Inc., Hanson Industries Inc.

and Peabody Holding Company, Inc.

[] Former SVP -- Engineering and W.V. Central Region and Kentucky Operations

for

Michael D. Day Patriot 21 / 21 2008

EVP - Operations [] Previously served in a variety of management positions at

Magnum, Arch and James River Coal Company Robert W. Bennett [] Former SVP of

Sales and Trading for Magnum Coal and President of Magnum SVP and Chief Marketing

25 / 25 2008 Coal Sales Officer[] Former VP of Peabody COALSALES and Peabody

COALTRADE

[] Former SVP and COO for Patriot

Charles A. Ebetino, Jr [] Held several positions at Peabody including SVP of

Business and Resource SVP Global Strategy and 36 /36 2007 Development and SVP

of

Market Development Corporate Development [] Former SVP of Fuel Supply of

American Electric Power and President and COO of AEP's coal mining and

coal-related subsidiaries

Joseph W. Bean

[] Former VP and Associate General Counsel and Assistant Secretary for Peabody

SVP Law and

12 / 26 2007 [] Former counsel and assistant corporate secretary for The Quaker

Oats

Administration and

Company

General Counsel

Robert L. Mead

Vice President and 6 / 23 2007 [] Former Director, Global Finance and Treasury

for Energizer

Treasurer

28

|  |

Financial Overview |  |

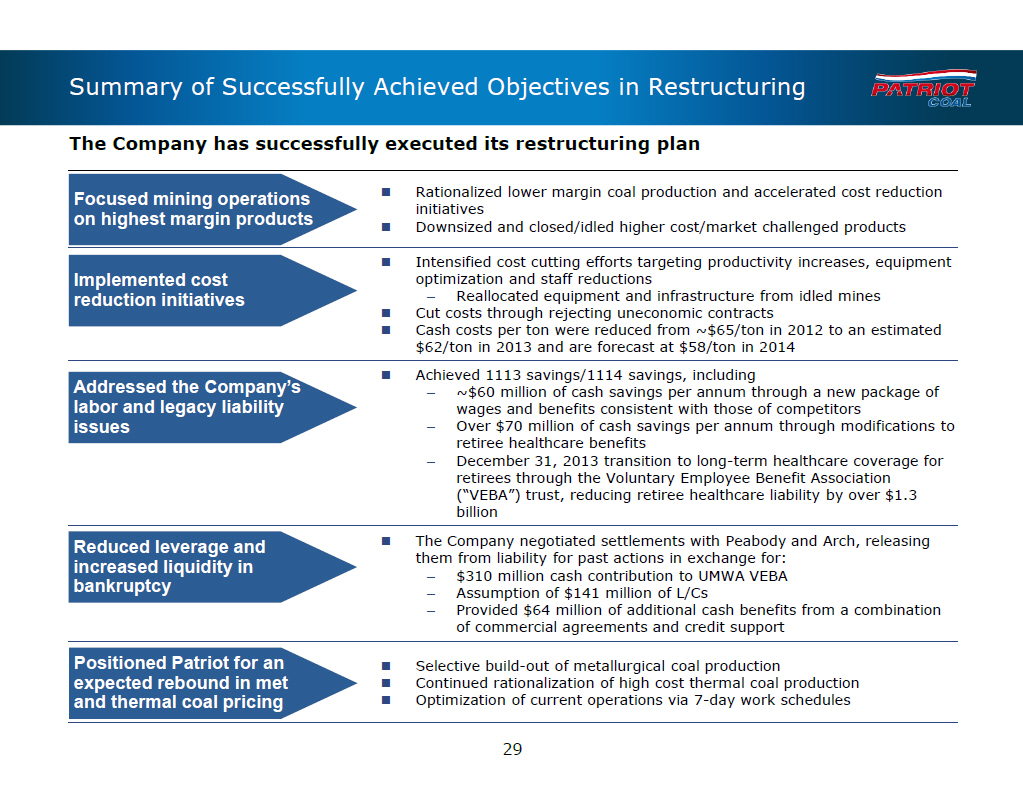

Summary of Successfully Achieved Objectives in Restructuring

The Company has successfully executed its restructuring plan

Focused mining operations [] Rationalized lower margin coal production and

accelerated cost reduction

on highest margin products initiatives

[] Downsized and closed/idled higher cost/market challenged products

[]

Intensified cost cutting efforts targeting productivity increases, equipment

Implemented cost optimization and staff reductions reduction initiatives --

Reallocated equipment and infrastructure from idled mines [] Cut costs through

rejecting uneconomic contracts [] Cash costs per ton were reduced from ~$65/ton

in 2012 to an estimated $62/ton in 2013 and are forecast at $58/ton in 2014 []

Achieved 1113 savings/1114 savings, including Addressed the Company's -- ~$60

million of cash savings per annum through a new package of labor and legacy

liability wages and benefits consistent with those of competitors issues --

Over $70 million of cash savings per annum through modifications to retiree

healthcare benefits

--

December 31, 2013 transition to long-term healthcare coverage for retirees

through the Voluntary Employee Benefit Association ("VEBA") trust, reducing

retiree healthcare liability by over $1.3 billion Reduced leverage and [] The

Company negotiated settlements with Peabody and Arch, releasing increased

liquidity in them from liability for past actions in exchange for: -- $310

million cash contribution to UMWA VEBA bankruptcy -- Assumption of $141 million

of L/Cs

-- Provided $64 million of additional cash benefits from a combination of

commercial agreements and credit support

Positioned Patriot for an [] Selective build-out of metallurgical coal

production expected rebound in met [] Continued rationalization of high cost

thermal coal production and thermal coal pricing [] Optimization of current

operations via 7-day work schedules

29

|  |

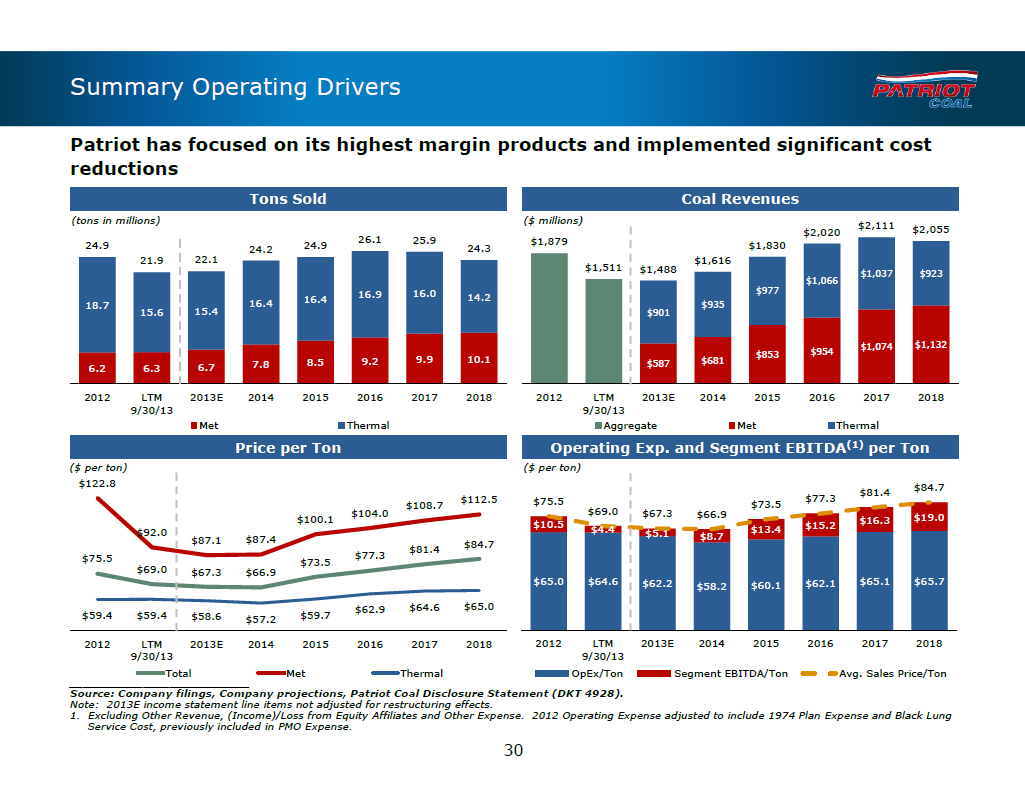

Summary Operating Drivers

Patriot has focused on its highest margin products and implemented significant

cost reductions

Tons Sold Coal Revenues

(tons in millions) ($ millions) $2,111 $2,020 $2,055 26.1 25.9 $1,879 24.9 24.2

24.9 24.3 $1,830 21.9 22.1 $1,616 $1,511 $1,488 $1,037 $923 $1,066 16.9 16.0

$977 16.4 14.2 18.7 16.4 $935 15.6 15.4 $901

$1,074 $1,132 $853 $954 8.5 9.2 9.9 10.1 $681 6.2 6.3 6.7 7.8 $587

2012 LTM 2013E 2014 2015 2016 2017 2018 2012 LTM 2013E 2014 2015 2016 2017 2018

9/30/13 9/30/13 Met Thermal Aggregate Met Thermal

Price per Ton Operating Exp. and Segment EBITDA(1) per Ton

($ per ton) ($ per ton) $122.8 $84.7 $81.4 $112.5 $75.5 $77.3 $108.7 $73.5

$104.0 $69.0 $67.3 $66.9 $100.1 $16.3 $19.0 $10.5 $4.4 $15.2 $92.0 $5.1 $13.4

$87.1 $87.4 $8.7 $84.7 $81.4 $75.5 $77.3 $73.5 $69.0 $67.3 $66.9 $65.0 $64.6

$62.2 $60.1 $62.1 $65.1 $65.7 $58.2 $62.9 $64.6 $65.0 $59.4 $59.4 $58.6 $57.2

$59.7 2012 LTM 2013E 2014 2015 2016 2017 2018 2012 LTM 2013E 2014 2015 2016

2017 2018 9/30/13 9/30/13 Total Met Thermal OpEx/Ton Segment EBITDA/Ton Avg.

Sales Price/Ton

___________________________

Source: Company filings, Company projections, Patriot Coal Disclosure Statement

(DKT 4928).

Note: 2013E income statement line items not adjusted for restructuring effects.

1. Excluding Other Revenue, (Income)/Loss from Equity Affiliates and Other

Expense. 2012 Operating Expense adjusted to include 1974 Plan Expense and Black

Lung Service Cost, previously included in PMO Expense.

30

|  |

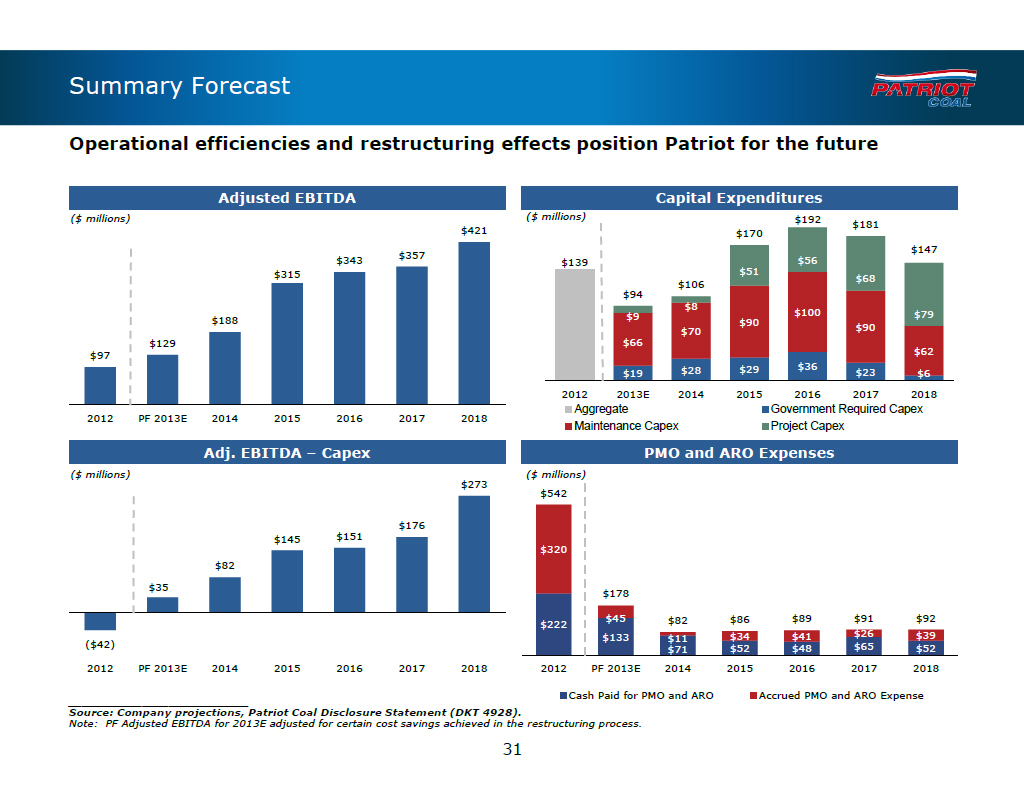

Summary Forecast

Operational efficiencies and restructuring effects position Patriot for the

future

Adjusted EBITDA Capital Expenditures

($ millions) ($ millions) $192 $181 $421 $170 $147 $357 $56 $343 $139 $315 $51

$68 $106 $94 $8 $9 $100 $79 $188 $90 $70 $90 $129 $66 $97 $62 $28 $29 $36 $19

$23 $6 2012 2013E 2014 2015 2016 2017 2018

Aggregate Government Required Capex

2012 PF 2013E 2014 2015 2016 2017 2018

Maintenance Capex Project Capex

Adj. EBITDA -- Capex PMO and ARO Expenses

($ millions) ($ millions) $273 $542

$176 $145 $151 $320 $82

$35 $178

$45 $82 $86 $89 $91 $92 $222 $133 $11 $34

$41 $26 $39 ($42) $52 $48 $65 $52 $71 2012 PF 2013E 2014 2015 2016 2017 2018

2012 PF 2013E 2014 2015 2016 2017 2018

Cash Paid for PMO and ARO Accrued PMO and ARO Expense

___________________________

Source: Company projections, Patriot Coal Disclosure Statement (DKT 4928).

Note: PF Adjusted EBITDA for 2013E adjusted for certain cost savings achieved

in the restructuring process.

31

|  |

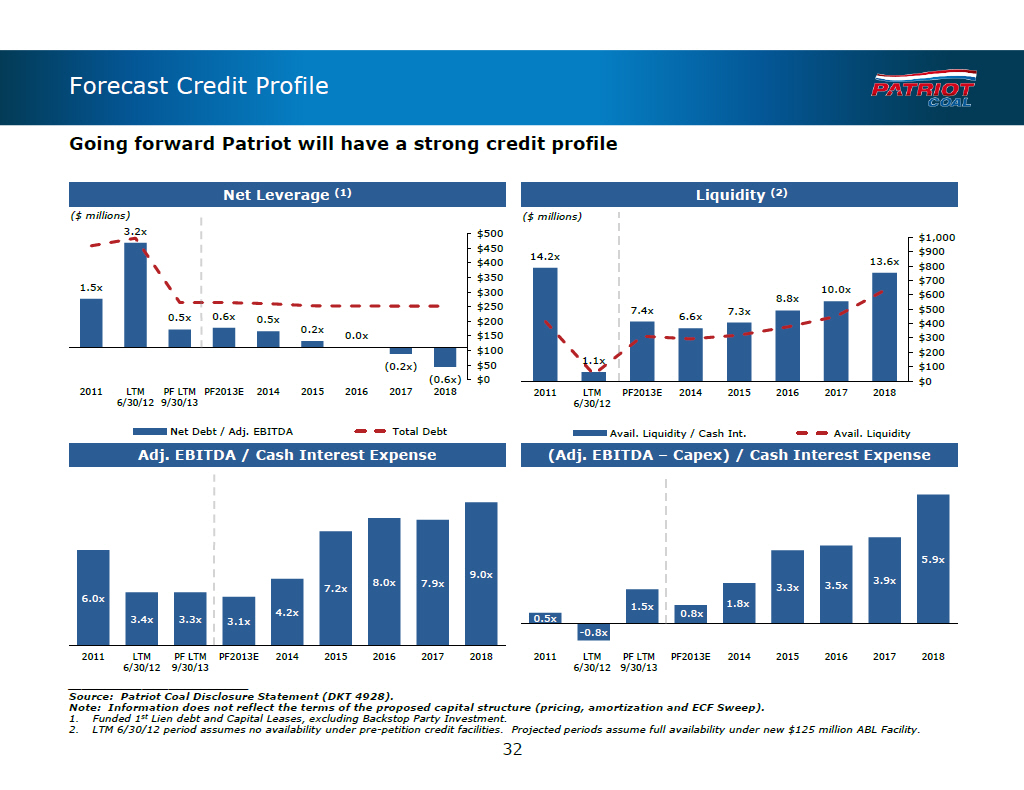

Forecast Credit Profile

Going forward Patriot will have a strong credit profile

Net Leverage (1) Liquidity (2)

($ millions) ($ millions)

3.2x $500 $1,000 $450 $900 14.2x 13.6x $400 $800 $350 $700 1.5x $300

10.0x 8.8x $600 $250 7.4x 7.3x $500 0.5x 0.6x 0.5x $200 6.6x $400 0.2x 0.0x

$150 $300 $100 $200 $50 1.1x (0.2x) $100 (0.6x) $0 $0 2011 LTM PF LTM PF2013E

2014 2015 2016 2017 2018 2011 LTM PF2013E 2014 2015 2016 2017 2018 6/30/12

9/30/13 6/30/12

Net Debt / Adj. EBITDA Total Debt Avail. Liquidity / Cash Int. Avail.

Liquidity

Adj. EBITDA / Cash Interest Expense (Adj. EBITDA -- Capex) / Cash Interest

Expense

5.9x 9.0x 8.0x 7.9x 3.5x 3.9x 7.2x 3.3x 6.0x 1.5x

1.8x 4.2x 0.8x 3.4x 3.3x 3.1x 0.5x -0.8x

2011 LTM PF LTM PF2013E 2014 2015 2016 2017 2018 2011 LTM PF LTM PF2013E 2014

2015 2016 2017 2018 6/30/12 9/30/13 6/30/12 9/30/13

___________________________

Source: Patriot Coal Disclosure Statement (DKT 4928).

Note: Information does not reflect the terms of the proposed capital structure

(pricing, amortization and ECF Sweep).

1. Funded 1(st) Lien debt and Capital Leases, excluding Backstop Party

Investment.

2. LTM 6/30/12 period assumes no availability under pre-petition credit

facilities. Projected periods assume full availability under new $125 million

ABL Facility.

32

|  |

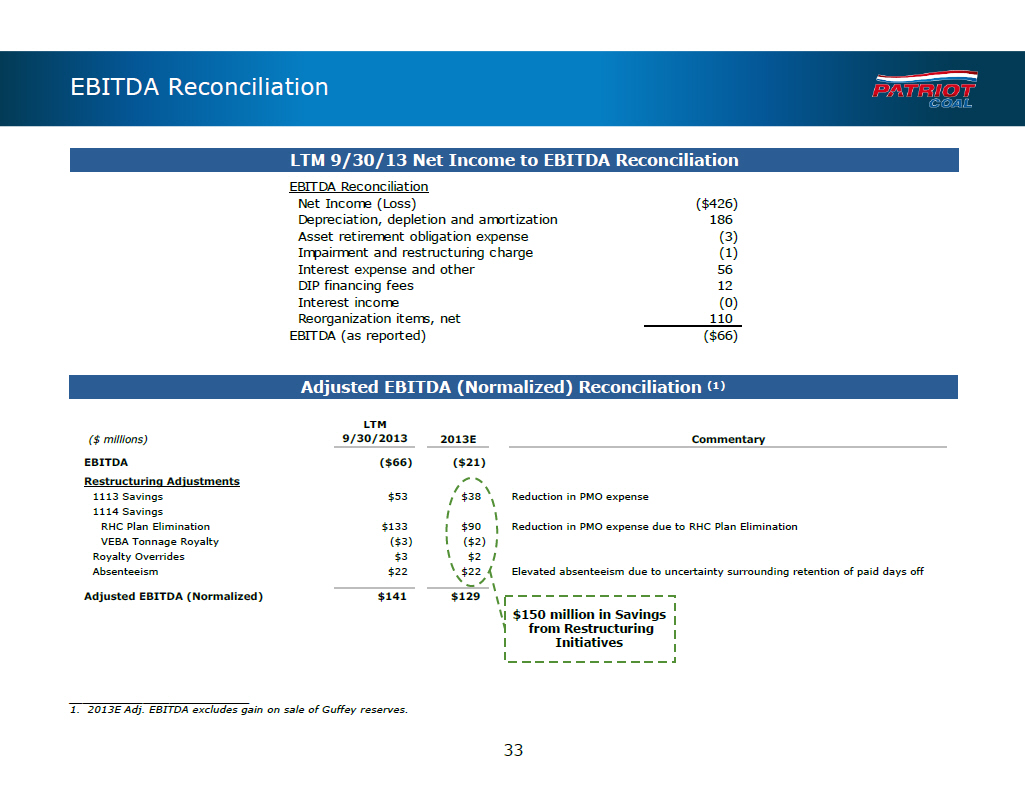

EBITDA Reconciliation LTM 9/30/13 Net Income to EBITDA Reconciliation EBITDA Reconciliation Net Income (Loss) ($426) Depreciation, depletion and amortization 186 Asset retirement obligation expense (3) Impairment and restructuring charge (1) Interest expense and other 56 DIP financing fees 12 Interest income (0) Reorganization items, net 110 EBITDA (as reported) ($66) Adjusted EBITDA (Normalized) Reconciliation (1) LTM ($ millions) 9/30/2013 2013E Commentary EBITDA ($66) ($21) Restructuring Adjustments 1113 Savings $53 $38 Reduction in PMO expense 1114 Savings RHC Plan Elimination $133 $90 Reduction in PMO expense due to RHC Plan Elimination VEBA Tonnage Royalty ($3) ($2) Royalty Overrides $3 $2 Absenteeism $22 $22 Elevated absenteeism due to uncertainty surrounding retention of paid days off Adjusted EBITDA (Normalized) $141 $129 $150 million in Savings from Restructuring Initiatives ___________________________ 1. 2013E Adj. EBITDA excludes gain on sale of Guffey reserves. 33 |  |

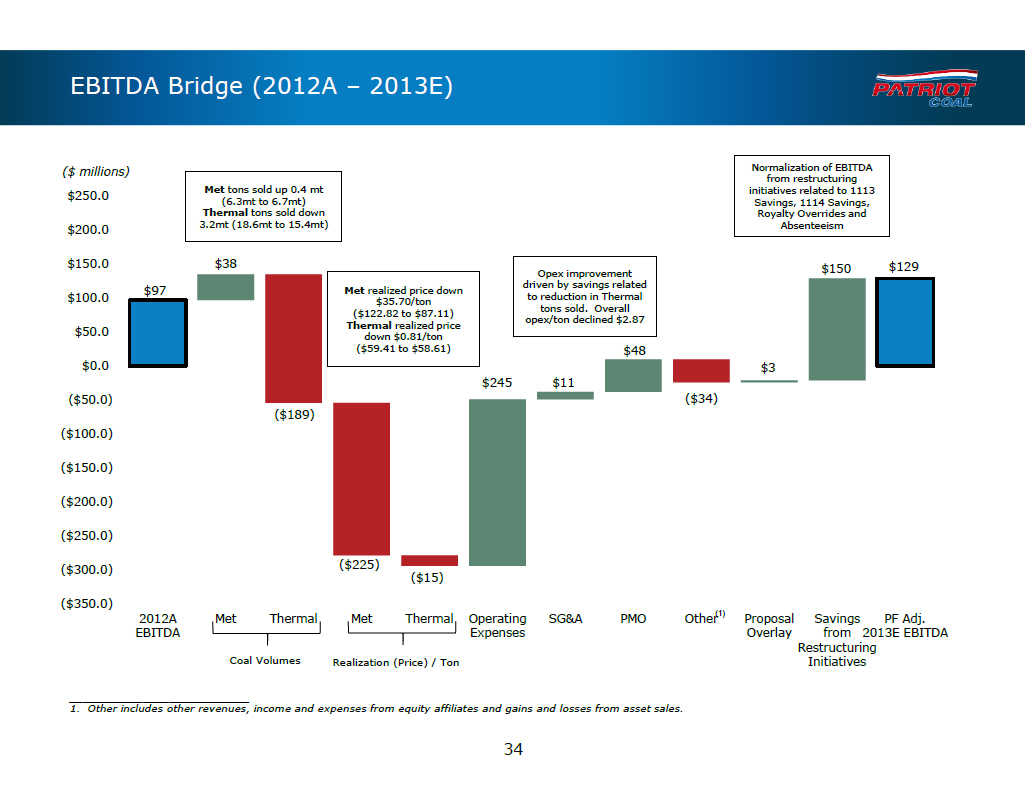

EBITDA Bridge (2012A -- 2013E)

($ millions) Normalization of EBITDA from restructuring Met tons sold up 0.4 mt

initiatives related to 1113 $250.0 (6.3mt to 6.7mt) Savings, 1114 Savings,

Thermal tons sold down Royalty Overrides and $200.0 3.2mt (18.6mt to 15.4mt)

Absenteeism

$150.0 $38 $150 $129 Opex improvement driven by savings related $97 Met

realized price down $100.0 to reduction in Thermal $35.70/ton tons sold.

Overall ($122.82 to $87.11) opex/ton declined $2.87 Thermal realized price

$50.0 down $0.81/ton ($59.41 to $58.61) $48 $0.0 $3 $245 $11 ($50.0) ($34)

($189) ($100.0)

($150.0) ($200.0) ($250.0)

($300.0) ($225)

($1

5) ($350.0)

2012A Met Thermal Met Thermal Operating SGand A PMO Other(1) Proposal Savings PF

Adj. EBITDA Expenses Overlay from 2013E EBITDA

Restructuring Coal Volumes

Realization (Price) / Ton Initiatives

___________________________

1. Other includes other revenues, income and expenses from equity affiliates

and gains and losses from asset sales.

34

|  |

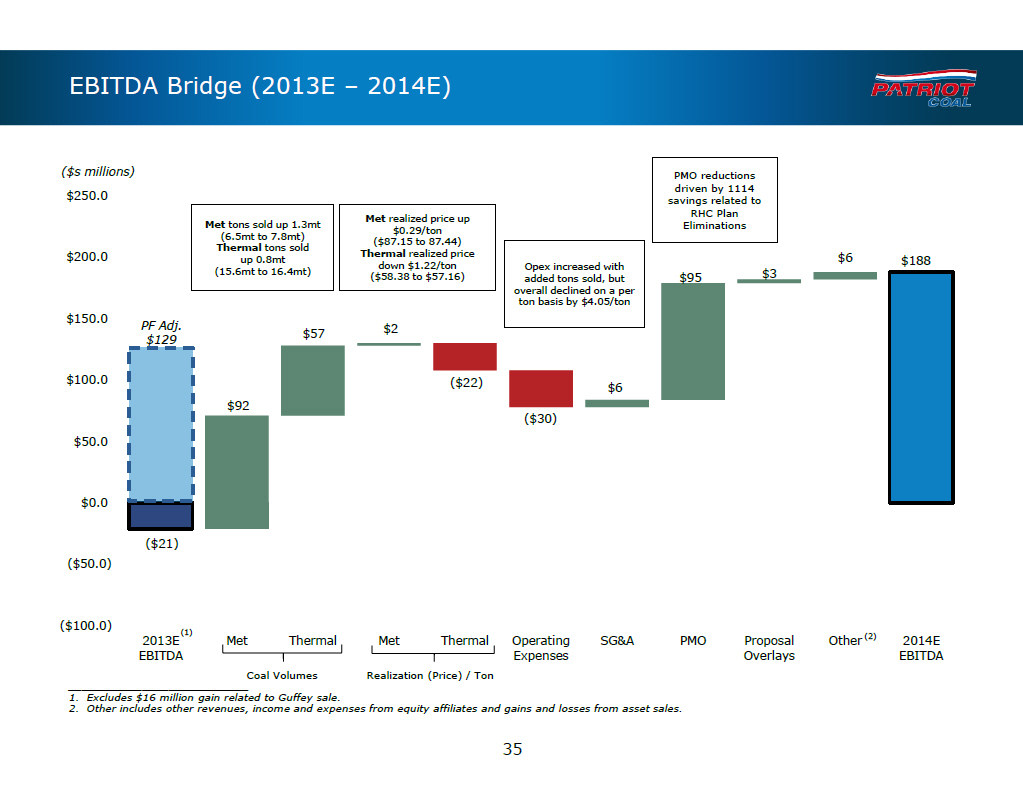

EBITDA Bridge (2013E -- 2014E)

($s millions) PMO reductions driven by 1114 $250.0 savings related to RHC Plan

Met realized price up Met tons sold up 1.3mt Eliminations $0.29/ton (6.5mt to

7.8mt) ($87.15 to 87.44) Thermal tons sold $200.0 Thermal realized price $6 up

0.8mt $188 down $1.22/ton Opex increased with (15.6mt to 16.4mt) $3 ($58.38 to

$57.16) added tons sold, but $95 overall declined on a per ton basis by

$4.05/ton $150.0

PF Adj. $2 $57 $129

$100.0 ($22) $6 $92 ($30) $50.0

$0.0

($21) ($50.0)

($100.0)

(1) (2)

2013E Met Thermal Met Thermal Operating SGand A PMO Proposal Other 2014E EBITDA

Expenses Overlays EBITDA

Coal Volumes Realization (Price) / Ton

___________________________

1. Excludes $16 million gain related to Guffey sale.

2. Other includes other revenues, income and expenses from equity affiliates

and gains and losses from asset sales.

35

|  |

Syndication |  |

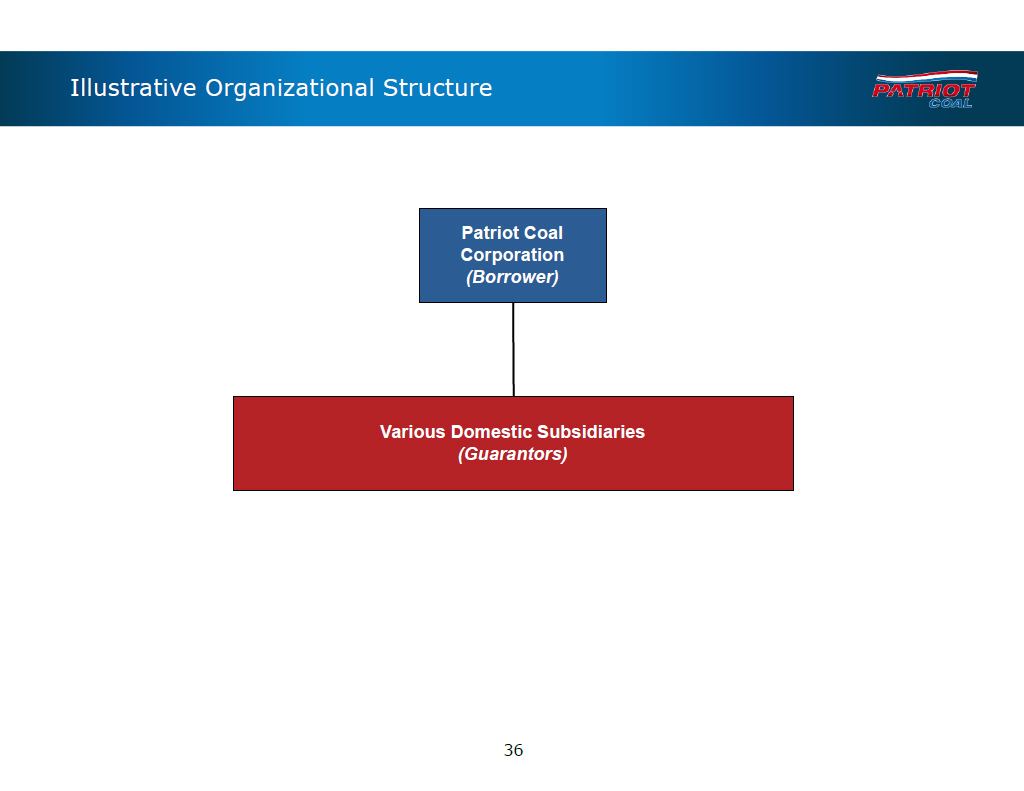

Illustrative Organizational Structure Patriot Coal Corporation (Borrower) Various Domestic Subsidiaries (Guarantors) 36 |  |

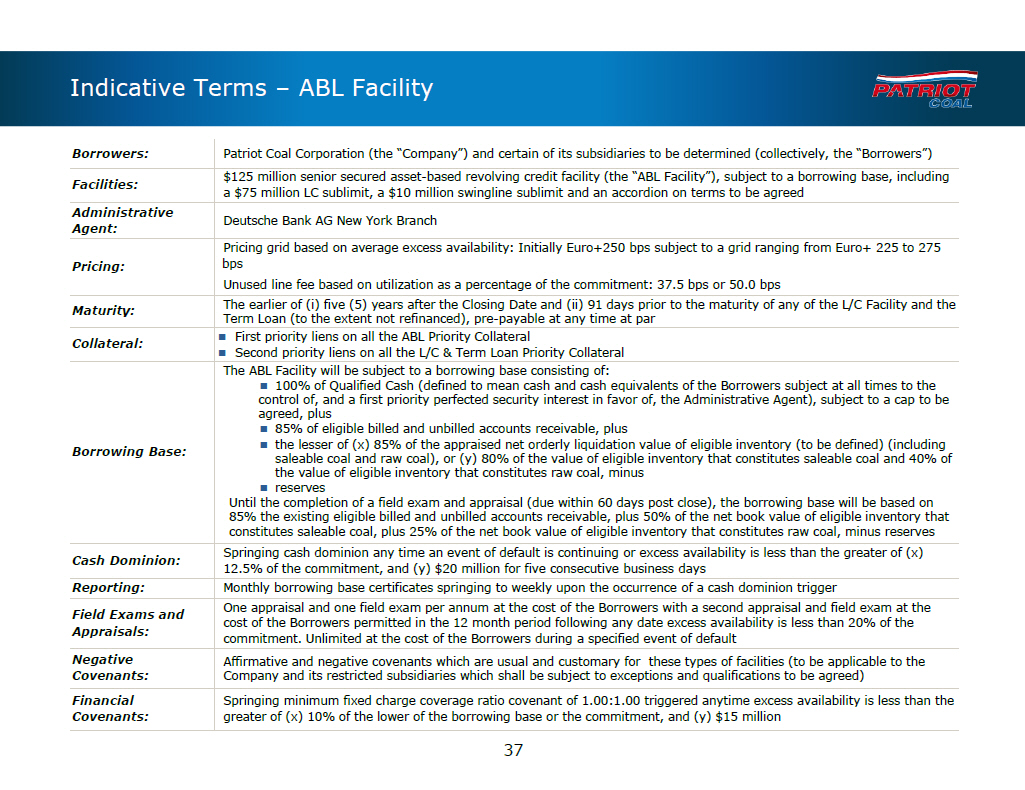

Indicative Terms -- ABL Facility

Borrowers: Patriot Coal Corporation (the "Company") and certain of its

subsidiaries to be determined (collectively, the "Borrowers") $125 million

senior secured asset-based revolving credit facility (the "ABL Facility"),

subject to a borrowing base, including

Facilities: a $75 million LC sublimit, a $10 million swingline sublimit and an

accordion on terms to be agreed

Administrative

Deutsche Bank AG New York Branch

Agent:

Pricing grid based on average excess availability: Initially Euro+250 bps

subject to a grid ranging from Euro+ 225 to 275

Pricing: bps

Unused line fee based on utilization as a percentage of the commitment: 37.5

bps or 50.0 bps

The earlier of (i) five (5) years after the Closing Date and (ii) 91 days prior

to the maturity of any of the L/C Facility and the

Maturity:

Term Loan (to the extent not refinanced),

pre-payable at any time at par Collateral: [] First priority liens on all the

ABL Priority Collateral [] Second priority liens on all the L/C and Term Loan

Priority Collateral The ABL Facility will be subject to a borrowing base

consisting of:

[] 100% of Qualified Cash (defined to mean cash and cash equivalents of the

Borrowers subject at all times to the control of, and a first priority

perfected security interest in favor of, the Administrative Agent), subject to

a cap to be agreed, plus [] 85% of eligible billed and unbilled accounts

receivable, plus [] the lesser of (x) 85% of the appraised net orderly

liquidation value of eligible inventory (to be defined) (including

Borrowing Base: saleable coal and raw coal), or (y) 80% of the value of

eligible inventory that constitutes saleable coal and 40% of the value of

eligible inventory that constitutes raw coal, minus[] reserves Until the

completion of a field exam and appraisal (due within 60 days post close), the

borrowing base will be based on 85% the existing eligible billed and unbilled

accounts receivable, plus 50% of the net book value of eligible inventory that

constitutes saleable coal, plus 25% of the net book value of eligible inventory

that constitutes raw coal, minus reserves Springing cash dominion any time an

event of default is continuing or excess availability is less than the greater

of (x)

Cash Dominion:

12.5% of the commitment, and (y) $20 million for five consecutive business days

Reporting: Monthly borrowing base certificates springing to weekly upon the

occurrence of a cash dominion trigger

One appraisal and one field exam per annum at the cost of the Borrowers with a

second appraisal and field exam at the

Field Exams and cost of the Borrowers permitted in the 12 month period

following any date excess availability is less than 20% of the

Appraisals: commitment. Unlimited at the cost of the Borrowers during a

specified event of default

Negative Affirmative and negative covenants which are usual and customary for

these types of facilities (to be applicable to the Covenants: Company and its

restricted subsidiaries which shall be subject to exceptions and qualifications

to be agreed) Financial Springing minimum fixed charge coverage ratio covenant

of 1.00:1.00 triggered anytime excess availability is less than the Covenants:

greater of (x) 10% of the lower of the borrowing base or the commitment, and

(y) $15 million

37

|  |

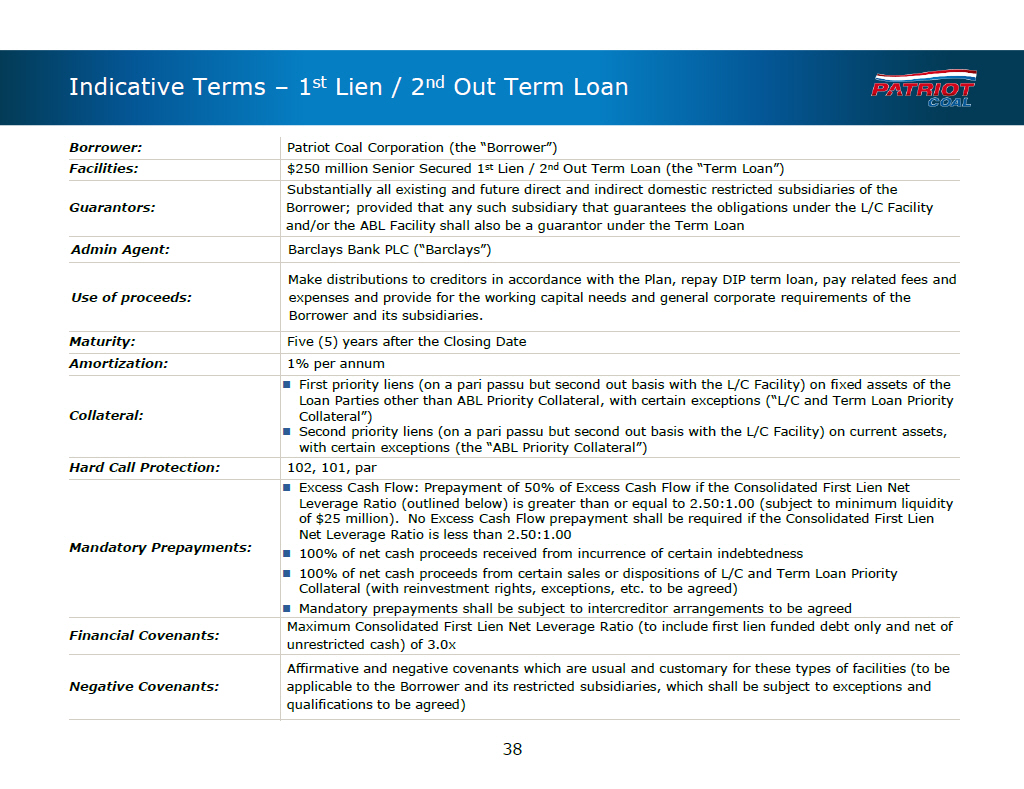

Indicative Terms -- 1(st) Lien / 2(nd) Out Term Loan

Borrower: Patriot Coal Corporation (the "Borrower")

Facilities: $250 million Senior Secured 1(st) Lien / 2(nd) Out Term Loan (the

"Term Loan") Substantially all existing and future direct and indirect domestic

restricted subsidiaries of the Guarantors: Borrower; provided that any such

subsidiary that guarantees the obligations under the L/C Facility and/or the

ABL Facility shall also be a guarantor under the Term Loan Admin Agent:

Barclays Bank PLC ("Barclays")

Make distributions to creditors

in accordance with the Plan, repay DIP term loan, pay related fees and Use of

proceeds: expenses and provide for the working capital needs and general

corporate requirements of the Borrower and its subsidiaries.

Maturity: Five (5) years after the Closing Date

Amortization: 1% per annum

[] First priority liens (on a

pari passu but second out basis with the L/C Facility) on fixed assets of the

Loan Parties other than ABL Priority Collateral, with certain exceptions ("L/C

and Term Loan Priority Collateral: Collateral") [] Second priority liens (on a

pari passu but second out basis with the L/C Facility) on current assets, with

certain exceptions (the "ABL Priority Collateral")

Hard Call Protection: 102, 101, par

[] Excess Cash Flow: Prepayment of 50% of Excess Cash Flow if the Consolidated

First Lien Net Leverage Ratio (outlined below) is greater than or equal to

2.50:1.00 (subject to minimum liquidity of $25 million). No Excess Cash Flow

prepayment shall be required if the Consolidated First Lien Net Leverage Ratio

is less than 2.50:1.00

Mandatory Prepayments:

[] 100% of net cash proceeds received from incurrence of certain indebtedness

[] 100% of net cash proceeds from certain sales or dispositions of L/C and Term

Loan Priority Collateral (with reinvestment rights, exceptions, etc. to be

agreed) [] Mandatory prepayments shall be subject to intercreditor arrangements

to be agreed Maximum Consolidated First Lien Net Leverage Ratio (to include

first lien funded debt only and net of

Financial Covenants: unrestricted cash) of 3.0x

Affirmative and negative

covenants which are usual and customary for these types of facilities (to be

Negative Covenants: applicable to the Borrower and its restricted subsidiaries,

which shall be subject to exceptions and qualifications to be agreed)

38

|  |

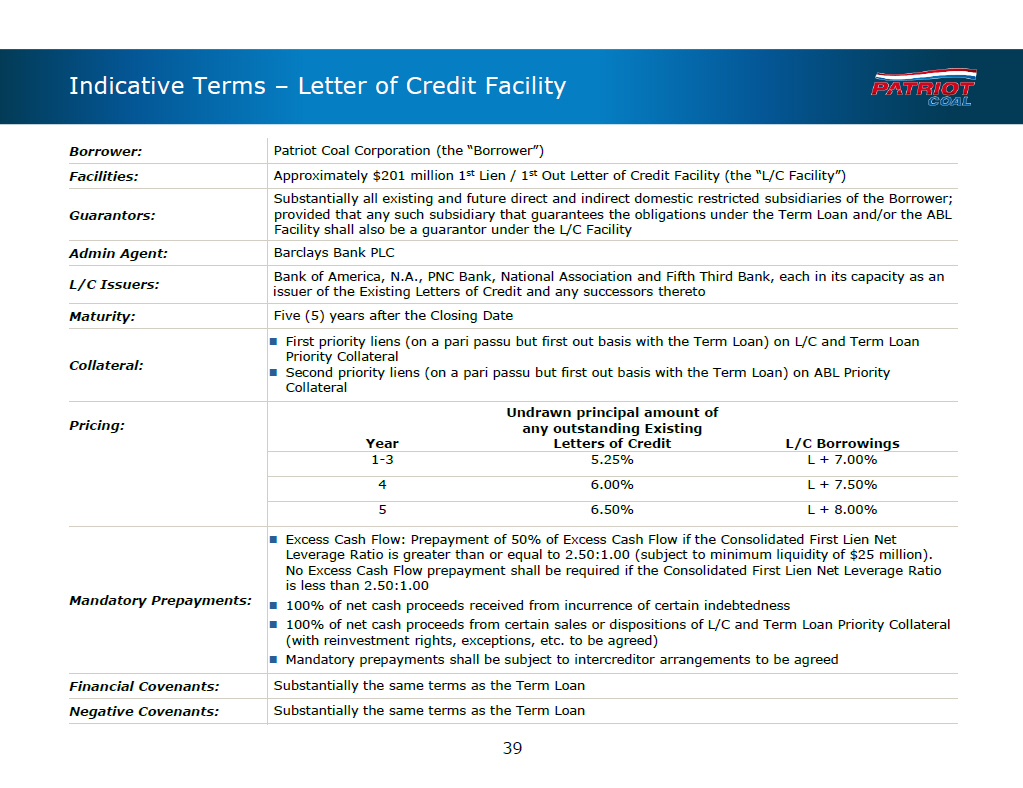

Indicative Terms -- Letter of Credit Facility

Borrower: Patriot Coal Corporation (the "Borrower")

Facilities: Approximately $201 million 1(st) Lien / 1(st) Out Letter of Credit

Facility (the "L/C Facility") Substantially all existing and future direct and

indirect domestic restricted subsidiaries of the Borrower; Guarantors: provided

that any such subsidiary that guarantees the obligations under the Term Loan

and/or the ABL

Facility shall also be a guarantor

under the L/C Facility Admin Agent: Barclays Bank PLC

Bank of America, N.A., PNC Bank, National Association and Fifth Third Bank,

each in its capacity as an

L/C Issuers: issuer of the Existing Letters of Credit and any successors

thereto Maturity: Five (5) years after the Closing Date

[] First priority liens (on a pari passu but first out basis with the Term

Loan) on L/C and Term Loan Priority Collateral

Collateral:

[] Second priority liens (on a pari passu but first out basis with the Term

Loan) on ABL Priority Collateral

Undrawn principal amount of Pricing: any outstanding Existing

Year Letters of Credit L/C Borrowings 1-3 5.25% L + 7.00%

4 6.00% L + 7.50%

5 6.50% L + 8.00%

[] Excess Cash Flow: Prepayment of 50% of Excess Cash Flow if the Consolidated

First Lien Net Leverage Ratio is greater than or equal to 2.50:1.00 (subject to

minimum liquidity of $25 million).

No Excess Cash Flow prepayment

shall be required if the Consolidated First Lien Net Leverage Ratio is less

than 2.50:1.00 Mandatory Prepayments: [] 100% of net cash proceeds received

from incurrence of certain indebtedness [] 100% of net cash proceeds from

certain sales or dispositions of L/C and Term Loan Priority Collateral (with

reinvestment rights, exceptions, etc. to be agreed) [] Mandatory prepayments

shall be subject to intercreditor arrangements to be agreed Financial

Covenants: Substantially the same terms as the Term Loan Negative Covenants:

Substantially the same terms as the Term Loan

39

|  |

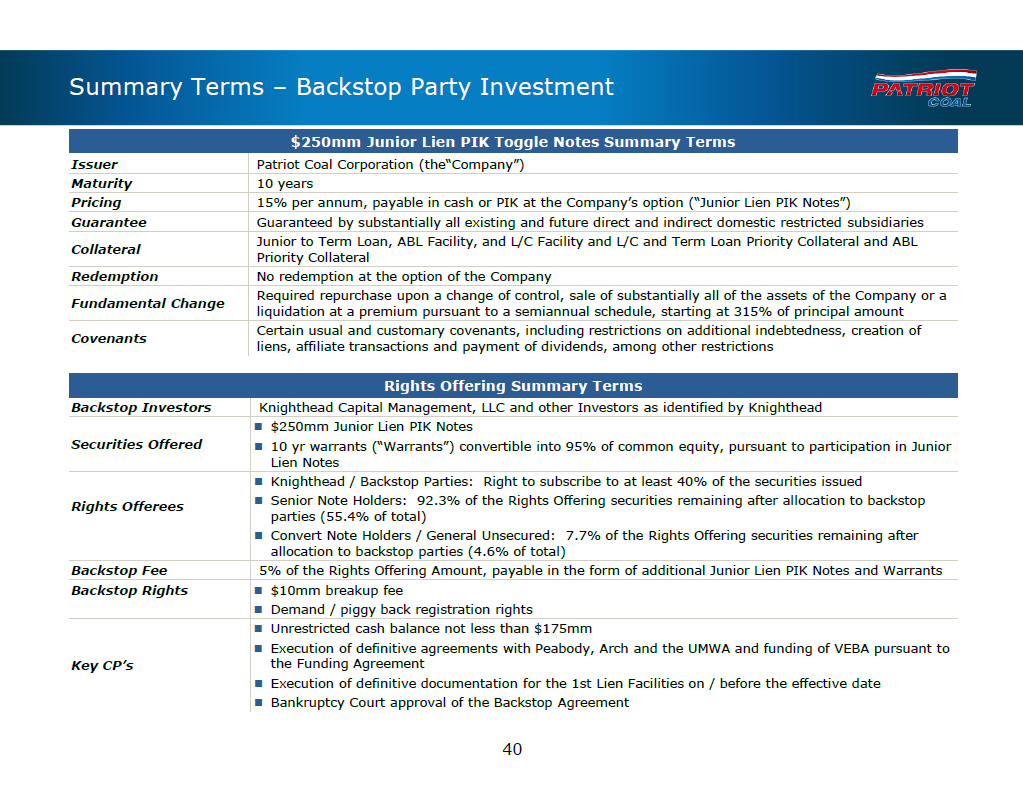

Summary Terms -- Backstop Party Investment

$250mm Junior Lien PIK Toggle Notes Summary Terms

Issuer Patriot Coal Corporation (the"Company")

Maturity 10 years

Pricing 15% per annum, payable in cash or PIK at the Company's option ("Junior

Lien PIK Notes") Guarantee Guaranteed by substantially all existing and future

direct and indirect domestic restricted subsidiaries Junior to Term Loan, ABL

Facility, and L/C Facility and L/C and Term Loan Priority Collateral and ABL

Collateral

Priority Collateral

Redemption No redemption at the option of the Company

Required repurchase upon a change of control, sale of substantially all of the

assets of the Company or a

Fundamental Change liquidation at a premium pursuant to a semiannual schedule,

starting at 315% of principal amount Certain usual and customary covenants,

including restrictions on additional indebtedness, creation of

Covenants liens, affiliate transactions and payment of dividends, among other

restrictions

Rights Offering Summary Terms

Backstop Investors Knighthead Capital Management, LLC and other Investors as

identified by Knighthead [] $250mm Junior Lien PIK Notes

Securities Offered [] 10 yr warrants ("Warrants") convertible into 95% of

common equity, pursuant to participation in Junior Lien Notes [] Knighthead /

Backstop Parties: Right to subscribe to at least 40% of the securities issued

Rights Offerees [] Senior Note Holders: 92.3% of the Rights Offering securities

remaining after allocation to backstop parties (55.4% of total) [] Convert Note

Holders / General Unsecured: 7.7% of the Rights Offering securities remaining

after allocation to backstop parties (4.6% of total) Backstop Fee 5% of the

Rights Offering Amount, payable in the form of additional Junior Lien PIK Notes

and Warrants Backstop Rights [] $10mm breakup fee [] Demand / piggy back

registration rights [] Unrestricted cash balance not less than $175mm []

Execution of definitive agreements with Peabody, Arch and the UMWA and funding

of VEBA pursuant to Key CP's the Funding Agreement [] Execution of definitive

documentation for the 1st Lien Facilities on / before the effective date []

Bankruptcy Court approval of the Backstop Agreement

40

|  |

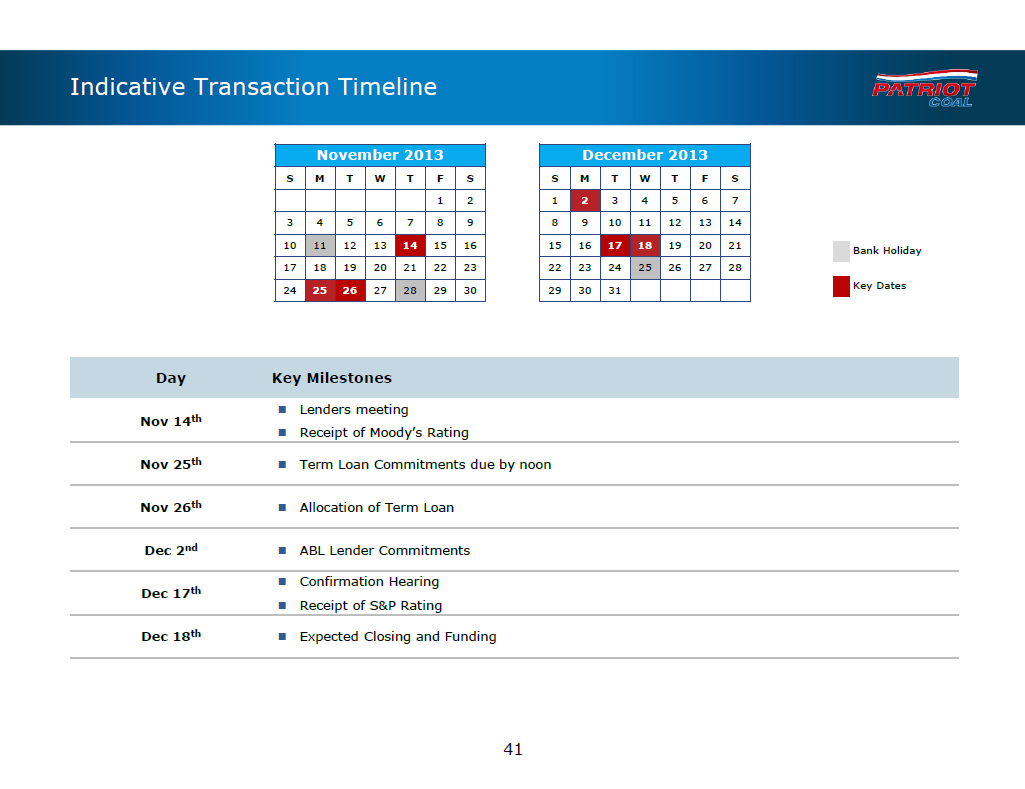

Indicative Transaction Timeline November 2013 December 2013 S M T W T F S S M T W T F S 1 2 1 2 3 4 5 6 7 3 4 5 6 7 8 9 8 9 10 11 12 13 14 10 11 12 13 14 15 16 15 16 17 18 19 20 21 Bank Holiday 17 18 19 20 21 22 23 22 23 24 25 26 27 28 24 25 26 27 28 29 30 29 30 31 Key Dates Day Key Milestones [] Lenders meeting Nov 14(th) [] Receipt of Moody's Rating Nov 25(th) [] Term Loan Commitments due by noon Nov 26(th)[] Allocation of Term Loan Dec 2(nd) [] ABL Lender Commitments [] Confirmation Hearing Dec 17(th) [] Receipt of S and P Rating Dec 18(th)[] Expected Closing and Funding 41 |  |

Public Q and A |  |