EXHIBIT 99.1

Presentation Materials dated January 22, 2010

Fourth Quarter 2009 Earnings Review Conference Call dial-in (800) 561-2718, Passcode: 22269964 Friday, January 22, 2010, 11:00 AM ET Available through January 29 at (888) 286-8010, Passcode: 39025635 Also available on: www.peoples.com and www.streetevents.com |

1 Certain comments made in the course of this presentation by People's United Financial are forward- looking in nature. These include all statements about People's United Financial's operating results or financial position for periods ending or on dates occurring after December 31, 2009 and usually use words such as "expect", "anticipate", "believe", and similar expressions. These comments represent management's current beliefs, based upon information available to it at the time the statements are made, with regard to the matters addressed. All forward-looking statements are subject to risks and uncertainties that could cause People's United Financial's actual results or financial condition to differ materially from those expressed in or implied by such statements. Factors of particular importance to People’s United Financial include, but are not limited to: (1) changes in general, national or regional economic conditions; (2) changes in interest rates; (3) changes in loan default and charge-off rates; (4) changes in deposit levels; (5) changes in levels of income and expense in non-interest income and expense related activities; (6) residential mortgage and secondary market activity; (7) changes in accounting and regulatory guidance applicable to banks; (8) price levels and conditions in the public securities markets generally; (9) competition and its effect on pricing, spending, third-party relationships and revenues; and (10) the successful integration of acquired companies. People's United Financial does not undertake any obligation to update or revise any forward- looking statements, whether as a result of new information, future events or otherwise. Forward Looking Statement |

2 Fourth Quarter Results Operating earnings exclude non-recurring charges Operating net income of $28.0 million, or $0.08 per share excludes $3.1 million, or $0.01 per share of non-recurring charges. Net interest margin of 3.19% Net loan charge-offs of 0.38% of average loans NPAs to loans, REO & repossessed assets of 1.44% Tangible common equity ratio of 18.2% |

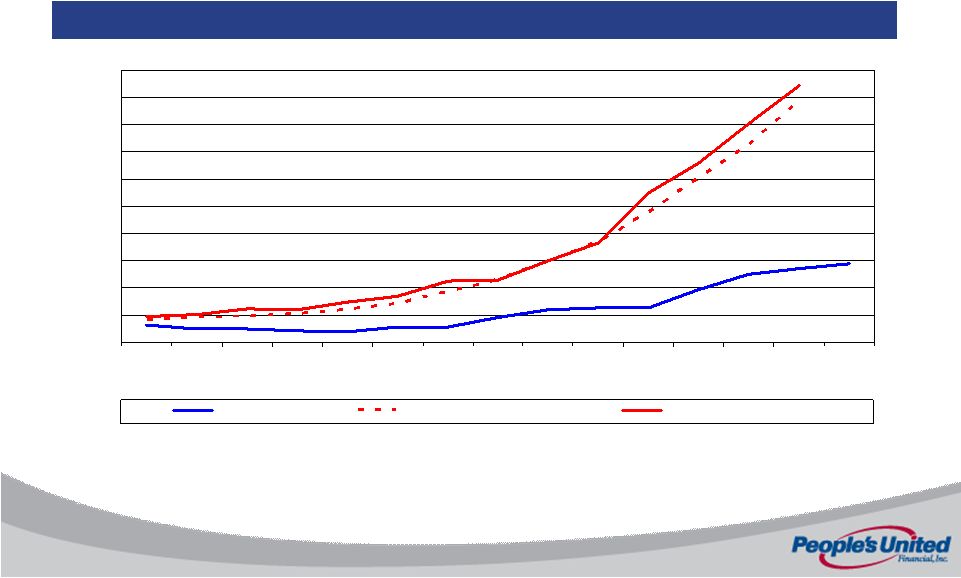

3 Net Interest Margin The core margin remained stable in 4Q as net repricing benefits of both assets and liabilities were offset by continued deposit growth . 4Q08 1Q09 2Q09 3Q09 4Q09 3.94% 3.66% 3.58% 3.65% 3.65% 3.55% 3.25% 3.12% 3.19% 3.19% 1.25% 0.78% 0.25% 0.25% 0.25% |

4 NPAs/Loans & REO (%) 2006-2009 1.44 1.35 4.45 4.71 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks by Assets |

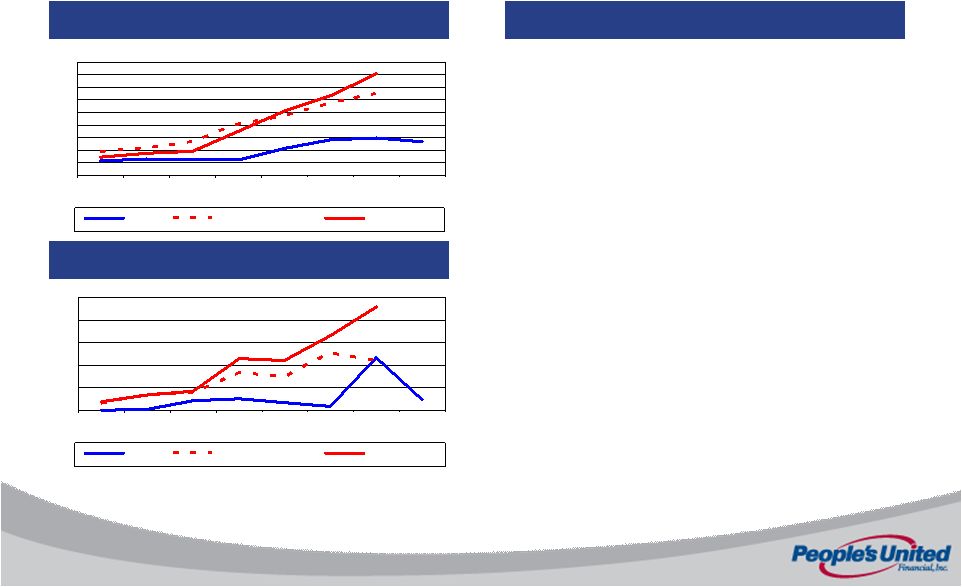

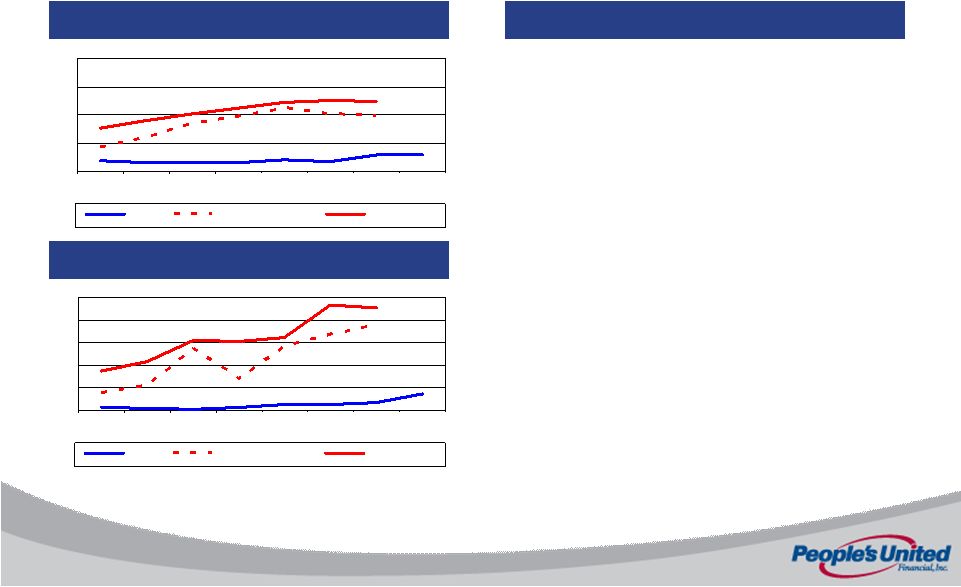

5 Commercial & Industrial Loans Historical Credit Performance NPLs (%) NCOs (%) Commentary • Portfolio remains well diversified • Continue to see growth in core middle market segment • Equipment Finance arm focused on mission critical equipment with good resale values • Core portfolio is all self-originated, with rigorous underwriting and ongoing credit administration 0.94 0.99 2.16 2.59 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks 0.82 0.35 2.16 2.68 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

6 Commercial Real Estate Loans Historical Credit Performance Commentary • CRE portfolio totals $5.4BN, 95% was originated by us, $270MM represents shared national credits, which we fully underwrote • All CRE loans are underwritten on a cash flow basis • Portfolio is well diversified • Construction portfolio down to $819MM down over 11% from $925MM at 12/31/08 • Florida construction represents less than $17MM of loans NPLs (%) NCOs (%) 1.34 1.49 3.26 4.05 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks 0.12 0.58 0.55 1.14 0.00 0.25 0.50 0.75 1.00 1.25 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

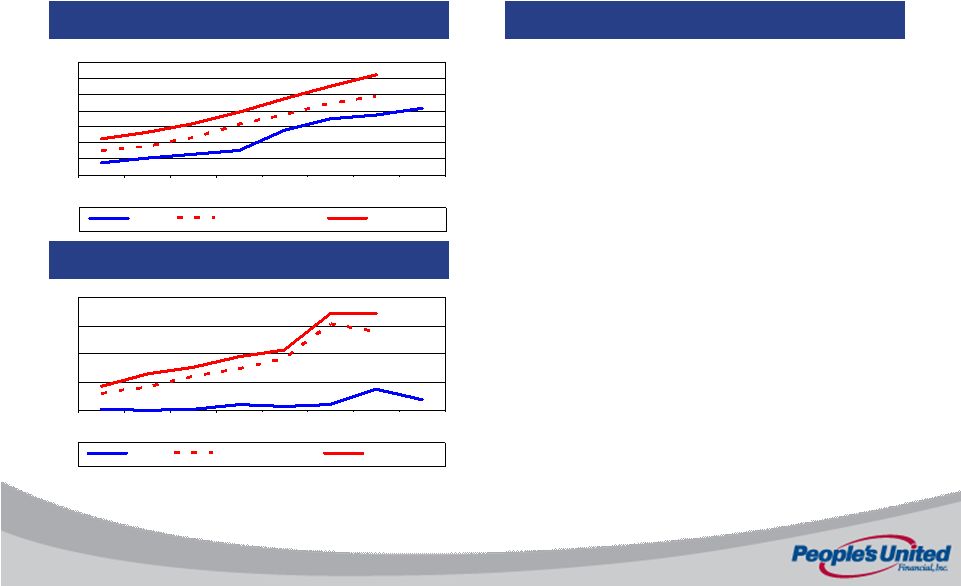

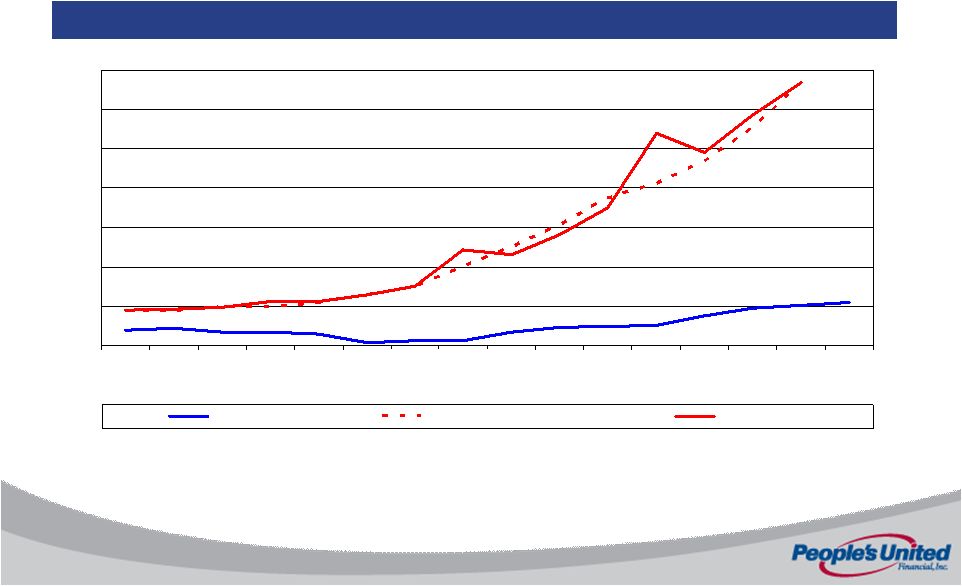

7 Residential Loans Historical Credit Performance NPLs (%) NCOs (%) Commentary • Low LTV at origination • Current FICO of 724 • Stopped portfolioing residential mortgages in 2006 • Of the $52.7MM in NPLs, approximately two-thirds have current LTV of <90% • Strength of original underwriting should continue to minimize loss content in NPAs 2.07 1.88 2.43 3.11 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks 0.18 0.37 1.39 1.72 0.00 0.50 1.00 1.50 2.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

8 Home Equity Historical Credit Performance Commentary NPLs (%) NCOs (%) 0.37 0.16 1.89 2.26 0.00 0.50 1.00 1.50 2.00 2.50 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks • As of Q4 2009, Home Equity loans stood at $2.0BN, flat from Q3 2009 levels • Q4 2009 utilization rate was 48.2%, compared to Q3 2009 rate of 47.5% • Asset quality in terms of both NPAs and NCOs remains low • While volume has slowed, Home Equity remains an important part of our retail relationships 0.29 0.28 0.99 1.24 0.00 0.50 1.00 1.50 2.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

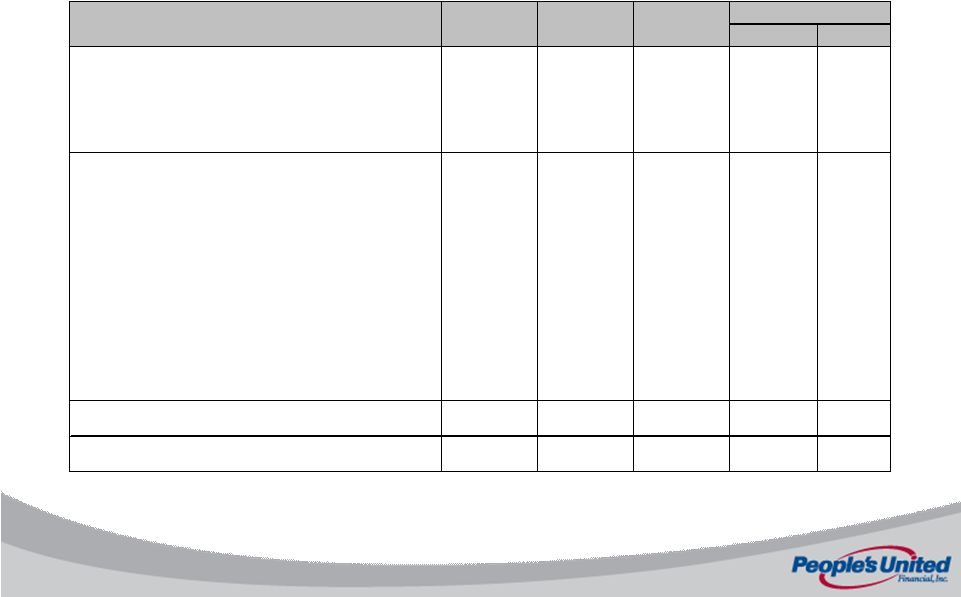

9 Net Charge-Offs/Average Loans (%) 2006-2009 0.38 0.44 2.00 2.68 -0.50 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007 Q3 2007 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

10 NPAs/(Tangible Equity + LLR) (%) 2006-2009 5.5 5.1 33.4 33.4 0 5 10 15 20 25 30 35 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 PBCT Peer Group Mean Top 50 Banks |

11 2010 Outlook Our outlook for 2010 is based on a stable Federal Funds rate and a gradually improving credit environment Financial Federal (FIF) expected to close February 19, 2010 Growth in core commercial and HELOC loans (excluding FIF) mostly offset by continued reduction in Residential and Shared National Credits Average deposit growth of 4%, with continued modest reduction in deposit costs 2010 net interest margin to increase approximately 45 basis points due primarily to FIF Net loan charge-offs of approximately 0.30% Small increase in non-interest income excluding security gains Wealth Management Revenue up approximately 6% Headwinds from overdraft fee legislation Non-interest expenses will increase due to the addition of FIF, volume related expenses, as well as net new systems costs. Overall, quarterly operating expenses should average $185 mil in 2010. |

12 Summary Strong Balance Sheet with Significant Capital Surplus Tangible Capital Ratio of 18.2%, improving to 18.6% pro forma for Financial Federal No Wholesale Borrowings Exceptional credit quality Low level of non-performing assets of 1.44% Combined net charge-off ratio of 0.38% annualized for 4Q, and 0.29% for 2009 full year Significant and low cost deposit market share Cost of deposits continues to decline, at 0.94% for 4Q09 Deposits entirely fund loans Opportunities Abound! Actively evaluating acquisitions Drive organic growth Positioned to leverage earnings growth via our asset sensitive balance sheet We are excited about growth and confident in our position |

Appendix |

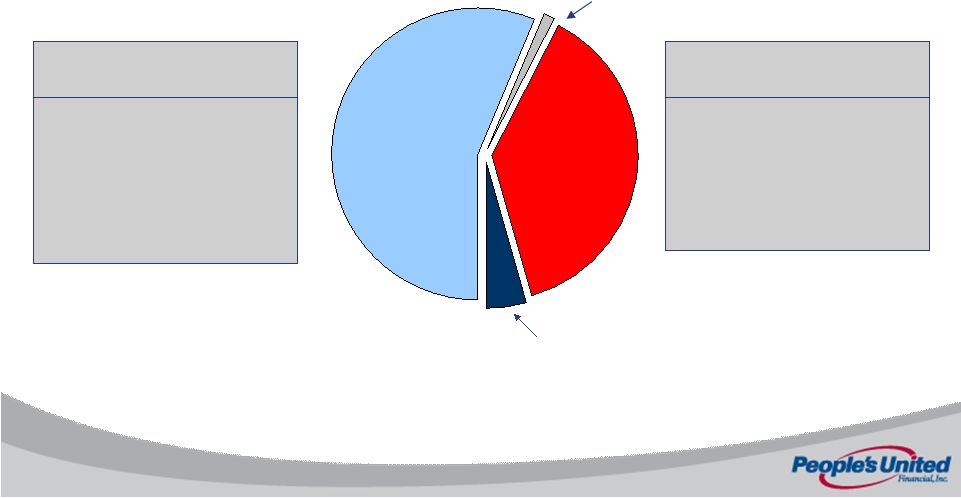

14 Average Earning Assets Earning asset increase due to deposit growth $ Inc/(Dec) % Commercial real estate 5,065 $ 4,992 $ 4,555 $ 73 $ 1 Commercial lending 3,712 3,744 3,703 (32) (1) Shared national credits 586 639 745 (53) (8) Total Commercial 9,363 9,375 9,003 (12) (0) Residential mortgage 2,609 2,809 3,190 (200) (7) Home equity and other loans 2,259 2,270 2,178 (11) (0) Total loans 14,231 14,454 14,371 (223) (2) Investments 4,351 3,887 3,003 464 12 Total earning assets 18,582 $ 18,341 $ 17,374 $ 241 $ 1 vs. Q3 2009 ($'s in millions) Q4 2009 Q3 2009 Q4 2008 |

15 Average Funding Mix Annualized deposit growth of 6% from Q3 2009 $ Inc/(Dec) % Deposits: Non-interest-bearing 3,321 $ 3,223 $ 3,096 $ 98 $ 3 Savings/Now/PMA 7,145 6,798 6,144 347 5 Time 4,807 5,016 4,877 (209) (4) Total deposits 15,273 15,037 14,117 236 2 Sub-debt / Other borrowings 343 328 362 15 5 Total funding liabilities 15,616 15,365 14,479 251 2 Stockholders' equity 5,106 5,135 5,230 (29) (1) Total Funding 20,722 $ 20,500 $ 19,709 $ 222 $ 1 vs. Q3 2009 Q3 2009 Q4 2008 ($'s in millions) Q4 2009 |

16 Quarterly Income Statement vs. Q3 2009 $ Fav(Unf) % Inc/(Dec) Net Interest Income 147.5 $ 145.3 $ 153.3 $ 2.2 $ 2 Provision for Loan Losses 13.6 21.5 8.7 7.9 (37) Non-Interest Income 71.7 80.2 73.7 (8.5) (11) Non-Interest Expense 172.2 165.1 168.2 (7.1) 4 Income Before Taxes 33.4 38.9 50.1 (5.5) (14) Net Income 24.9 26.8 33.7 (1.9) (7) Earnings Per Share 0.07 0.08 0.10 (0.01) (13) ($'s in millions, except EPS) Q4 2009 Q3 2009 Q4 2008 |

17 Non-Interest Income $ Inc/(Dec) % Investment management fees 7.9 $ 8.4 $ 9.6 $ (0.5) $ (6) Insurance revenue 7.0 7.9 7.3 (0.9) (11) Brokerage commissions 2.9 2.8 3.2 0.1 4 Total wealth management 17.8 19.1 20.1 (1.3) (7) Bank service charges 32.2 33.3 31.5 (1.1) (3) Merchant services income 6.3 6.7 6.6 (0.4) (6) Net security gains (0.1) 4.7 0.2 (4.8) (102) Operating lease income 3.9 3.6 3.1 0.3 8 Gain on residential loan sales 3.0 5.2 0.8 (2.2) (42) Other non-interest income 8.6 7.6 11.4 1.0 13 Total non-interest income 71.7 $ 80.2 $ 73.7 $ (8.5) $ (11) Total non-interest income ex security gains 71.8 $ 75.5 $ 73.5 $ (3.7) $ (5) vs. Q3 2009 ($'s in millions) Q4 2009 Q3 2009 Q4 2008 |

18 Non-Interest Expense vs. Q3 2009 $ Inc/(Dec) % Compensation and benefits 89.2 $ 86.0 $ 83.2 $ 3.2 $ 4 Occupancy and equipment 28.0 27.5 26.5 0.5 2 Professional/outside service fees 10.0 11.6 12.8 (1.6) (14) Other non-interest expense 45.0 40.0 45.7 5.0 13 Total non-interest expense 172.2 $ 165.1 $ 168.2 $ 7.1 $ 4 Operating non-interest expense 167.7 $ 165.1 $ 168.2 $ 2.6 $ 2 Q4 2009 Q3 2009 Q4 2008 ($'s in millions) |

19 High Quality Consumer Portfolio Total Portfolio $4.8 billion (as of December 31, 2009) Residential Mortgage Portfolio Credit Statistics Weighted Average: Loan to value 51% FICO scores 724 Net charge-offs: 0.18% Non-accrual: 2.07% Home Equity Portfolio Credit Statistics Weighted Average: Combined LTV 55% FICO scores 751 Net charge-offs: 0.37% Non-accrual: 0.29% (1) Excludes the impact of the former Chittenden Corp. 1-4 Family Residential 53% Home Equity Loans & Lines 42% Indirect Auto 4% Other 1% 1 1 1 1 |

20 Well Balanced Commercial Portfolio Retail 26% Office 24% Industrial 12% Residential 14% Hospitality 10% Other 11% Land 3% As of December 31, 2009 Total Portfolio $9.4 billion $5.4 billion CRE * Includes the Commercial Real Estate portion of the Shared National Credit portfolio of $270 million CRE, By Sector General C&I 27% SNC 6% Commercial Real Estate 54% PCLC 13% 1 |

21 Construction Lending Detail Total Construction Portfolio $819 million As of December 31, 2009 Our construction exposure is modest at less than 6% of the total loan portfolio, and is a diverse mix of geographies and sectors. Residential 42% Land 11% Retail 22% Office 10% 15% Other Total Loans $14.2 billion By Geography By Sector Connecticut / New York 45% Other New England 33% 14% Other |

22 The Shared National Credits portfolio was initially established to expand geographic diversity in the loan portfolio, and has been in run-off mode since the beginning of 2008. This portfolio is now less than 4% of loans. Shared National Credits Outstandings, as of ($ in millions) 31-Dec-09 30-Sep-09 30-Jun-09 31-Mar-09 31-Dec-08 31-Dec-07 Commercial Lending 296.5 $ 308.2 $ 328.1 $ 398.2 $ 393.7 $ 456.3 $ Commercial Real Estate 270.3 306.0 310.8 294.9 289.8 284.2 Total loans 566.8 $ 614.2 $ 638.9 $ 693.1 $ 683.5 $ 740.5 $ Aggregate Exposure, as of ($ in millions) 31-Dec-09 30-Sep-09 30-Jun-09 31-Mar-09 31-Dec-08 31-Dec-07 Commercial Lending 681.3 $ 703.4 $ 711.4 $ 767.4 $ 784.8 $ 747.1 $ Commercial Real Estate 318.2 384.1 401.8 403.6 417.0 577.0 Total loans 999.5 $ 1,087.5 $ 1,113.2 $ 1,171.0 $ 1,201.8 $ 1,324.1 $ Current Maturity Schedule (based on Outstanding balances) 2010 2011 2012 2013 2014 + Commercial Lending 13% 16% 17% 7% 0% Commercial Real Estate 21% 21% 3% 0% 2% Total loans 34% 37% 20% 7% 2% |

Florida 6% Other (5% or less) 5% Louisiana 6% Arizona 7% Colorado 7% Other 9% Wholesale trade 4% Ent. 11% Professional services 11% Shared National Credits The portfolio is broadly diversified by both geography and industry CRE – Geography C&I – Industry $ 270.3 million $ 296.5 million Manufacturing 28% REITs 39% Washington 33% New York 21% Virginia 15% 23 |

24 Peer Group Company Name Ticker State Associated Banc-Corp ASBC WI Astoria Financial Corporation AF NY BOK Financial Corporation BOKF OK City National Corporation CYN CA Comerica Incorporated CMA TX Commerce Bancshares, Inc. CBSH MO Cullen/Frost Bankers, Inc. CFR TX First Horizon National Corporation FHN TN Flagstar Bancorp, Inc. FBC MI Fulton Financial Corporation FULT PA Hudson City Bancorp, Inc. HCBK NJ M&T Bank Corporation MTB NY Marshall & Ilsley Corporation MI WI New York Community Bancorp, Inc. NYB NY Synovus Financial Corp. SNV GA TCF Financial Corporation TCB MN Valley National Bancorp VLY NJ Webster Financial Corporation WBS CT Zions Bancorporation ZION UT |

For more information, investors may contact: Jared Shaw jared.shaw@peoples.com (203) 338-4130 |