Second Quarter 2010 Investor Presentation August 10, 2010 |

1 Forward Looking Statement Certain comments made in the course of this presentation by People's United Financial are forward-looking in nature. These include all statements about People's United Financial's operating results or financial position for periods ending or on dates occurring after June 30, 2010 and usually use words such as "expect", "anticipate", "believe", and similar expressions. These comments represent management's current beliefs, based upon information available to it at the time the statements are made, with regard to the matters addressed. All forward-looking statements are subject to risks and uncertainties that could cause People's United Financial's actual results or financial condition to differ materially from those expressed in or implied by such statements. Factors of particular importance to People’s United Financial include, but are not limited to: (1) changes in general, national or regional economic conditions; (2) changes in interest rates; (3) changes in loan default and charge-off rates; (4) changes in deposit levels; (5) changes in levels of income and expense in non-interest income and expense related activities; (6) residential mortgage and secondary market activity; (7) changes in accounting and regulatory guidance applicable to banks; (8) price levels and conditions in the public securities markets generally; (9) competition and its effect on pricing, spending, third-party relationships and revenues; (10) the successful integration of acquired companies; (11) success in addressing management succession issues in a timely and effective manner; and (12) possible changes in regulation resulting from or relating to recently enacted financial reform legislation. With respect to the recently announced transactions with Smithtown Bancorp, Inc. and LSB Corporation, factors of particular importance to People’s United Financial include, but are not limited to: (1) failure of the parties to satisfy the closing conditions in either merger agreement in a timely manner or at all; (2) failure of the shareholders of Smithtown Bancorp or LSB Corporation to approve the applicable merger agreement; (3) failure to obtain governmental approvals for one or both mergers; (4) disruptions to the parties’ businesses as a result of the announcement and pendency of one or both mergers; (5) costs or difficulties related to the integration of the businesses following one or both mergers; and (6) the risk that the anticipated benefits, cost savings and any other savings from either transaction may not be fully realized or may take longer than expected to realize. |

2 Corporate Overview Snapshot, as of June 30, 2010 1842 Founded: 4,582 Employees (FTE): >440 ATMs: ~300 Branches: $15.8 billion, #26 Deposits: $15.0 billion, #24 Loans: $21.9 billion, #25 Assets: $5.1 billion, #17 Market Capitalization (8/9/10) NASDAQ (PBCT) People’s United Financial, Inc. |

3 Diversified footprint with 333 branches and ~$18 billion in deposits across six states Considerable scarcity value as only major independent bank with presence across Northeast People’s United Pro Forma Footprint 0 #36 2 RiverBank 10 #36 29 Bank of Smithtown 2 #56 6 RiverBank 5 #7 32 ME 7 #4 33 NH * 9 #15 29 MA * 11 #35 34 NY * 14 #1 46 VT 30 #1 63 Fairfield, CT 54 #3 160 CT % of Deposits Market Share Branches PBCT SMTB LSBX De Novo Branches * Pending transaction completion |

4 Investment Thesis Prudently turning book value into earnings per share growth Organic loan & deposit growth including select de novo activity Well priced acquisitions Improving integration efficiency Share repurchases Committed to a strong dividend during capital deployment phase Significantly more asset sensitive than peers Multi-year de-leveraging process and tougher regulatory environment are encouraging consolidation People’s United is focused on increasing shareholder value |

5 0.58 0.24 -2.00 -1.50 -1.00 -0.50 0.00 0.50 1.00 1.50 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 PBCT Peers 3.68 3.33 4.16 2.50 3.00 3.50 4.00 4.50 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 PBCT Peers PBCT Core 1.30 2.01 0.46 1.13 2.58 1.84 4.67 3.20 0.00 1.00 2.00 3.00 4.00 5.00 6.00 NPAs / Assets NPAs / Loans + REO NCOs / Loans Allowance / Loans PBCT Peers Peer Comparison As of June 30, 2010 On most important measures, People’s United remains stronger than peers Net Interest Margin ** Return on Average Assets * Tangible Equity / Tangible Assets Asset Quality * For People’s United, Return on Average Assets reflects Operating Net Income/Average Assets annualized Peers reflect ROAA before extraordinary items according to SNL ** PBCT Core excludes excess capital 18.0 7.3 0.00 5.00 10.00 15.00 20.00 PBCT Peers |

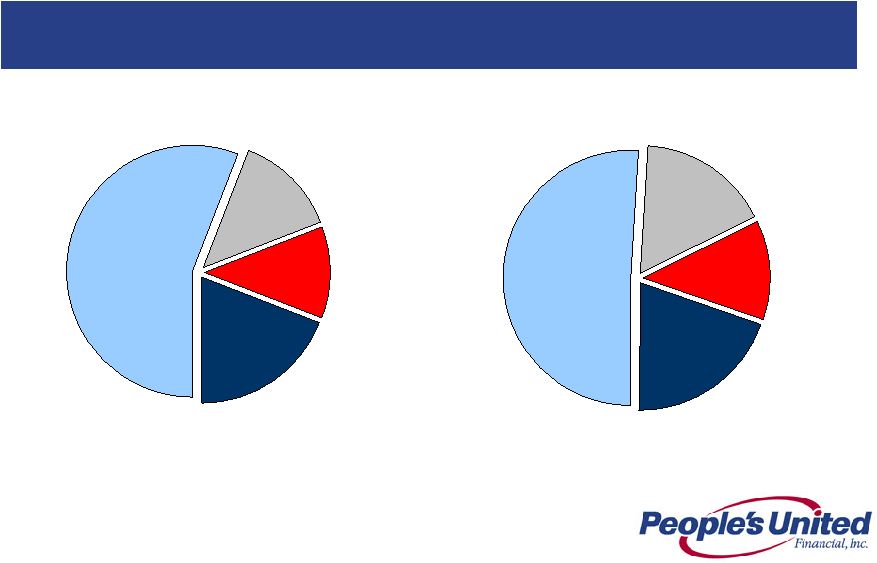

6 Average Earning Asset Mix 2Q 09 Home Equity 13% Securities & Investments 20% Commercial Banking 51% Residential Mortgage 16% 2Q 10 Securities & Investments 19% Home Equity 12% Commercial Banking 56% Residential Mortgage 13% We remain focused on growing core commercial and consumer lending, while excess capital is safely held in liquid investments $10,573 $2,537 $2,209 $3,630 $9,330 $2,989 $2,276 $3,615 |

7 Average Funding Mix Our assets are funded nearly entirely with deposits and equity 2Q 09 Interest- bearing Deposits 56% Demand Deposits 15% Stockholders’ Equity 25% 2Q 10 Interest- bearing Deposits 57% Stockholders’ Equity 25% Demand Deposits 15% Sub-debt / Other 3% $710 Sub-debt / Other 4% $711 Cost of Deposits = 0.74% Cost of Deposits = 1.26% $3,357 $5,458 $12,347 $5,162 $3,192 $11, 694 |

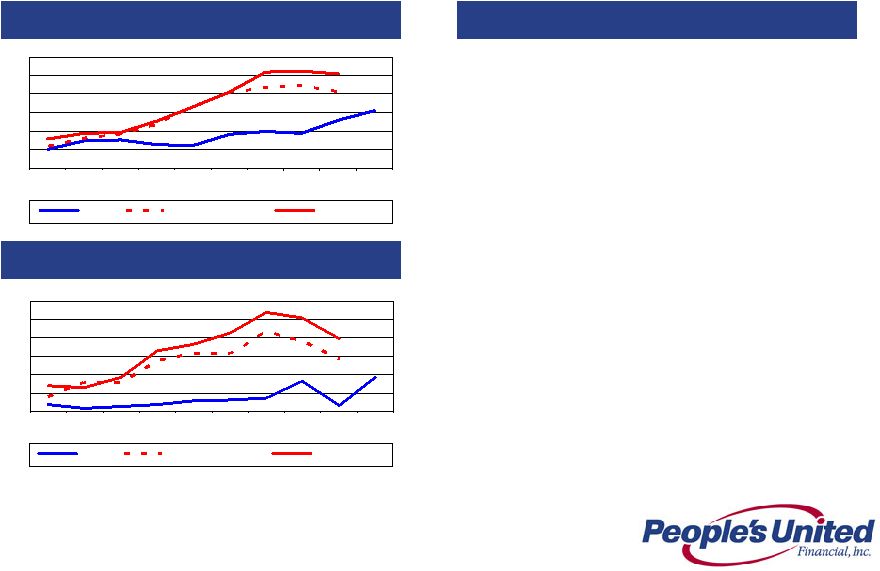

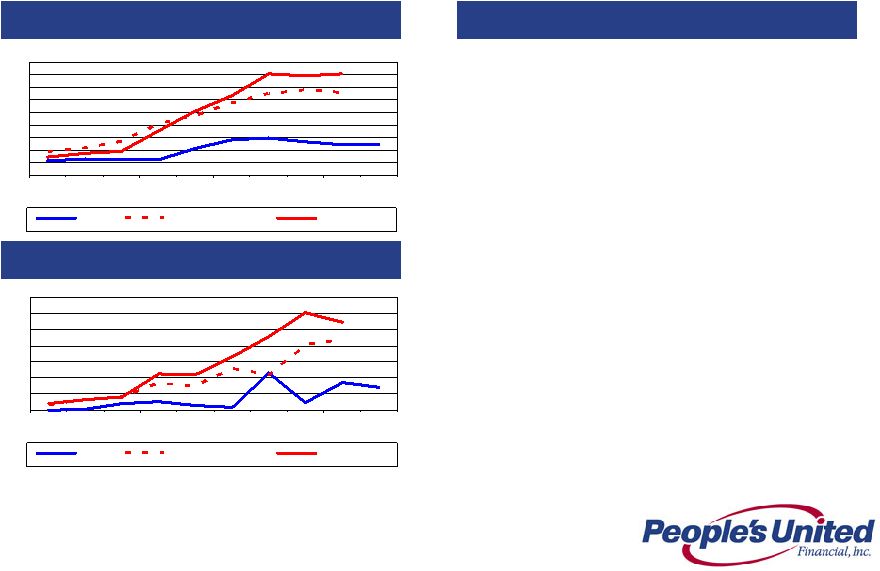

8 Commercial & Equipment Financing Historical Credit Performance NPLs * (%) NCOs (%) Commentary • Portfolio remains well diversified • Continue to see growth in core middle market segment • Core portfolio is self-originated, with rigorous underwriting and ongoing credit administration • Equipment Financing focused on mission critical equipment with good resale values 1.54 1.29 2.06 2.55 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks 0.92 0.15 1.40 1.97 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks * For People’s United, excludes acquired non-performing loans |

9 Commercial Real Estate Loans Historical Credit Performance Commentary • CRE portfolio totals $5.5BN • All CRE loans are underwritten on a cash flow basis • Portfolio is well diversified • Loss content is limited • Strong CRE portfolio growth opportunities continue to exist NPLs * (%) NCOs (%) 1.23 1.21 3.29 4.03 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks 0.35 0.43 1.08 1.37 0.00 0.25 0.50 0.75 1.00 1.25 1.50 1.75 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks * For People’s United, excludes acquired non-performing loans |

10 Retail & Small Business Relationship and service focus translates to low deposit rates Have begun originating first mortgages for portfolio (selling 30 year fixed mortgages) Highly developed retail model in southern New England #1 deposit market share in Fairfield County Multiple products and cross selling – 4.6 products per customer Continue to enhance retail model in northern New England Increase penetration from 3.0 products per customer Invested in licensing, product and sales training Westchester, NY expansion over the past 2 years now represents 5 branches and ~$330 million of deposits Will open two branches in downtown Boston before year end 2010 Deposit pricing discipline and high-quality consumer lending expansion will allow a continued focus on margin management |

11 Residential Loans Historical Credit Performance NPLs * (%) NCOs (%) Commentary • Resolution of NPLs is limited by a much slower foreclosure process • Low LTV at origination • 83% of NPLs have LTVs < 90%; should insure continued low loss content • Given attractive spreads, we began portfolioing some residential mortgages this quarter 3.40 2.70 3.01 3.45 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks 0.07 0.01 1.07 1.90 0.00 0.50 1.00 1.50 2.00 2.50 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks * For People’s United, excludes acquired non-performing loans |

12 Home Equity Historical Credit Performance Commentary NPLs * (%) NCOs (%) 0.03 0.17 1.37 1.93 0.00 0.50 1.00 1.50 2.00 2.50 3.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks • As of Q2 2010, Home Equity loans stood at $2.0BN, flat from Q1 2010 levels • Q2 2010 utilization rate was 48.2%, flat with Q1 2010 and Q4 2009 • Asset quality remains high, as measured by low NPLs and NCOs • Home Equity remains an important part of our retail relationships 0.44 0.35 0.91 1.33 0.00 0.50 1.00 1.50 2.00 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 PBCT Peer Group Mean Top 50 Banks * For People’s United, excludes acquired non-performing loans |

13 Wealth Management Delivering discount brokerage, full service brokerage, registered investment advisory, life insurance and long-term care services through one consolidated sales force Discount brokerage is a core competency and has attracted over $1 billion in assets Brokerage (discount and full-service) enhance PBCT deposit household profitability and retention We are committed to the RIA model growing fee-based business as opposed to competitors who are solely focused on up-front commission Life insurance sales up 60% YTD through July New opportunities: enhancing wealth management offering within Northern New England franchise, further penetrating the commercial insurance market Assets managed and administered totaled $16.4 billion What makes PBCT Wealth Management different from other bank models? |

14 Initiatives Growing into our capital base via high value activities February 2010 Converted Southern NE Franchise to new core system 2Q10 Repurchased $52MM in stock July 2010 Negotiated leases on 2 downtown Boston branches July 2010 Re-branded legacy Chittenden franchises to People’s United name July 2010 Converted Northern NE franchise to new core system Announced July 2010 Acquired Smithtown Bancorp (Bank of Smithtown) ~$2.4BN assets Long Island commercial bank Announced July 2010 Acquired LSB Corp (RiverBank) ~$800MM assets Greater Boston commercial bank Closed April 2010 Acquired Butler Bank ~$250MM assets Greater Boston commercial bank Closed February 2010 Acquired Financial Federal – ~$1.5BN assets national equipment finance company |

15 7 30 Branches 797 2,307 Assets ($MM) 543 1,978 Loans ($MM) 493 1,824 Deposits ($MM) 10 42 ATMs LSB Corp. * Smithtown Bancorp * Largest commercial bank headquartered on Long Island, NY operating as Bank of Smithtown High quality branch network Commercial bank headquartered in North Andover, MA operating as RiverBank Operates in attractive markets north of Boston Description Pending Acquisitions - Business Profiles * Financial data as of June 30, 2010 |

16 Pending Acquisitions - Strategic Rationale Expansion into densely populated, contiguous markets Expansion into attractive Long Island market Increases presence in Boston area Continuing to build the premier regional bank in the Northeast Provides platforms for increased market share in new markets Significant opportunity to lower deposit costs to PBCT levels Leverages excess capital Exceeds financial hurdles >15% IRR Significant operating EPS accretion in year 1 |

17 Pending Acquisitions - Pro Forma Impact >15% >15% Internal rate of return ~$0.10 ~$0.01 ~$0.09 2011 operating EPS accretion *** ~$9.65 $10.14 Tangible book value per share 30 1.8 2.0 2.3 SMTB* ~15.0% 18.0% Tangible common equity ratio 7 0.5 0.5 0.8 LSBX* 333 296 Branches 25.1 21.9 Assets ($Bn) 18.3 15.8 Deposits ($Bn) 17.6 15.2 Loans ($Bn) PBCT Pro Forma ** * Financial data as of June 30, 2010 ** Pro forma for purchase accounting adjustments. Assumes stock issued in SMTB transaction is repurchased *** Excludes one-time merger related expenses |

Appendix |

19 Appendix Management Committee Brian Dreyer Robert D’Amore Paul Burner David Bodor Jack Barnes People’s United Bank, FirstConstitution Bank, Bank of Boston 30+ 19 Senior Executive Vice President & Head of Commercial Banking People’s United Bank 27 27 Senior Executive Vice President & Head of Retail & Small Business People’s United Bank, CFO of Citibank North America, Citigroup 30+ 2 Senior Executive Vice President & Chief Financial Officer People’s United Bank, CenterBank, Bank of Boston 35+ 13 Executive Vice President & Chief Credit Officer People’s United Bank (SEVP, CAO), Chittenden Bank, FDIC 30+ 27 President & CEO Professional Experience Years in Banking Years with Organization Position Name |

20 Appendix Management Committee Robert Trautmann Chantal Simon Louise Sandberg David Norton People’s United Bank, Tyler Cooper and Alcorn 20 16 Senior Executive Vice President & General Counsel People’s United Bank, Chief Risk Officer Merrill Lynch Bank, Lazard Freres & Co. 20+ 1 Senior Executive Vice President & Chief Risk Officer People’s United Bank, Chittenden Bank 33 33 Senior Executive Vice President & Head of Wealth Management People’s United Bank, The New York Times, Starwood Hotels, PepsiCo 1 1 Senior Executive Vice President & Chief Human Resources Officer Professional Experience Years in Banking Years with Organization Position Name |

21 Appendix Peer Group Company Name Ticker State 1 Associated Banc-Corp ASBC WI 2 Astoria Financial Corporation AF NY 3 BOK Financial Corporation BOKF OK 4 City National Corporation CYN CA 5 Comerica Incorporated CMA TX 6 Commerce Bancshares, Inc. CBSH MO 7 Cullen/Frost Bankers, Inc. CFR TX 8 First Horizon National Corporation FHN TN 9 Flagstar Bancorp, Inc. FBC MI 10 Fulton Financial Corporation FULT PA 11 Hudson City Bancorp, Inc. HCBK NJ 12 M&T Bank Corporation MTB NY 13 Marshall & Ilsley Corporation MI WI 14 New York Community Bancorp, Inc. NYB NY 15 Synovus Financial Corp. SNV GA 16 TCF Financial Corporation TCB MN 17 Valley National Bancorp VLY NJ 18 Webster Financial Corporation WBS CT 19 Zions Bancorporation ZION UT |

For more information, investors may contact: Peter Goulding, CFA peter.goulding@peoples.com (203) 338-6799 |