2011 Barclays Capital Global Financial Services Conference September 12, 2011 Exhibit 99.1 |

2 Corporate Overview Snapshot, as of June 30, 2011 People’s United Financial, Inc. NASDAQ (PBCT) Market Capitalization (9/8/11) $4.4 billion Assets: $25.3 billion Loans: $17.7 billion Deposits: $18.3 billion Branches: 341 ATMs: 518 Founded: 1842 |

3 Primary Objectives Optimize the existing business + Deploy capital in high risk-adjusted return initiatives Return the franchise to >1.25% Operating ROAA |

4 The Northeast Region is Best Commercial Banking Market in the United States Population density Limited amount of land available for development Construction entitlements are difficult to win Deep educational and healthcare sectors provide long-lasting infrastructure, attract talented young people, consistently spawn new businesses Significant “quiet wealth” which adds credit strength to the region Mega bank acquisitions of mid-size banks have left a void of relationship- based, service focused banks |

5 Deepening Presence in NYC Metro and Boston MSA People’s United (PBCT) Danvers Bancorp (DNBK) |

6 Strong Pro Forma Deposit Market Position Connecticut Branches $BN % 1 B of A 166 20.7 21.7 2 Webster 136 11.5 12.1 3 People's United 162 9.7 10.1 4 Wells Fargo 76 8.3 8.6 5 TD Bank 80 5.2 5.5 6 First Niagara 74 4.9 5.1 7 JPM Chase 49 3.9 4.0 8 Liberty 42 2.7 2.8 9 RBS 51 2.6 2.8 10 Citi 20 2.2 2.3 Massachusetts Vermont New York New Hampshire Maine Branches $BN % 1 B of A 280 44.2 24.2 2 RBS 257 24.5 13.4 3 Santander 230 13.6 7.4 4 TD Bank 159 8.7 4.8 5 Eastern 96 6.2 3.4 6 Independent 70 3.7 2.0 7 People's United 59 3.6 2.0 8 Middlesex 33 3.6 2.0 9 Boston Private 9 2.4 1.3 10 Berkshire Hills 37 2.0 1.2 Branches $BN % 1 People's United 46 2.6 24.3 2 TD Bank 37 2.0 18.5 3 Merchants 34 1.0 9.8 4 RBS 24 0.8 8.0 5 KeyCorp 13 0.8 7.7 6 Northfield 13 0.5 4.4 7 Community 14 0.4 3.6 8 Union 13 0.3 3.3 9 Passumpsic 7 0.3 3.1 10 Berkshire Hills 7 0.3 2.8 Branches $BN % 1 JPM Chase 811 287.4 34.3 2 Citi 261 66.6 7.9 3 HSBC 377 65.9 7.9 4 B of A 380 55.2 6.6 5 Capital One 290 32.6 3.9 6 M&T 278 23.5 2.8 7 Wells Fargo 87 20.4 2.4 8 TD Bank 203 18.9 2.3 9 KeyCorp 229 15.2 1.8 10 Astoria 85 11.2 1.3 37 People's United 38 2.2 0.3 Branches $BN % 1 RBS 82 6.9 26.3 2 TD Bank 74 4.8 18.2 3 B of A 35 4.6 17.5 4 People's United 33 1.4 5.2 5 LSB Financial 20 0.8 3.2 6 Santander 20 0.8 3.1 7 Northway 19 0.6 2.5 8 New Hamp. Thrift 19 0.6 2.3 9 Centrix 6 0.5 2.1 10 Meredith Village 11 0.5 1.8 Branches $BN % 1 TD Bank 57 3.2 15.0 2 KeyCorp 61 2.7 12.7 3 B of A 35 1.7 8.0 4 Bangor Bancorp 57 1.7 7.9 5 Camden National 38 1.6 7.3 6 First Bancorp 14 0.9 4.5 7 Machias 13 0.8 3.9 8 People's United 31 0.8 3.9 9 Norway 21 0.7 3.3 10 Bar Harbor 13 0.7 3.1 Deposits of $20.2BN #1 in Fairfield County, CT, 64 branches, $5.4BN, 17.8% market share #2 in Essex County, MA, 24 branches, $2.0BN, 12.3% market share Source: SNL Financial |

7 7 Low Cost of Deposits Publicly Traded Northeast Banks, $5BN < Assets <$100BN Source: SNL Financial SNLTable Total Cost of Assets ($BN) Deposits (%) Company City State 2Q 2011 2Q 2011 1 M&T Bank Corporation Buffalo NY 77.7 0.30 2 First Niagara Financial Group, Inc. Buffalo NY 30.9 0.48 3 Boston Private Financial Holdings, Inc. Boston MA 6.0 0.55 4 NBT Bancorp Inc. Norwich NY 5.3 0.57 5 Community Bank System, Inc. De Witt NY 6.4 0.58 6 People's United Financial, Inc. Bridgeport CT 25.3 0.58 7 Webster Financial Corporation Waterbury CT 17.8 0.62 8 Fulton Financial Corporation Lancaster PA 16.0 0.70 9 Valley National Bancorp Wayne NJ 14.5 0.72 10 New York Community Bancorp, Inc. Westbury NY 40.6 0.72 11 National Penn Bancshares, Inc. Boyertown PA 8.6 0.73 12 F.N.B. Corporation Hermitage PA 9.9 0.75 13 Provident Financial Services, Inc. Iselin NJ 6.9 0.78 14 First Commonwealth Financial Corporation Indiana PA 5.7 0.79 15 Susquehanna Bancshares, Inc. Lititz PA 14.2 0.84 16 Signature Bank New York NY 13.1 0.87 17 Northwest Bancshares, Inc. Warren PA 8.1 1.06 18 CapitalSource Inc. Chevy Chase MD 9.3 1.13 19 Investors Bancorp, Inc. (MHC) Short Hills NJ 10.2 1.17 20 Astoria Financial Corporation Lake Success NY 17.1 1.25 21 Hudson City Bancorp, Inc. Paramus NJ 51.8 1.32 |

8 88,538 35,052 20,811 0 30,000 60,000 90,000 120,000 150,000 NY Metro* Boston Central CT** Bridgeport / Stamford < 20 Employees Commercial Market Opportunity by MSA Source: SBA firms and employment by MSA 2007 * NY Metro area includes New York, Northern New Jersey, and Long Island MSA ** Central Connecticut includes New Haven and Hartford MSAs 428,577 > 500 Employees 471,661 < 500 Employees 0.2% 2.4% 6.3% 17.8% 0.2% 2.4% 6.3% 17.8% 0.2% 2.4% 6.3% 17.8% Pro Forma Deposit Market Share Overall within identified MSA Number of firms by size People’s United is growing in NYC Metro and Boston Metro, areas rich with potential commercial, non-commodity relationships 101,633 40,880 23,630 0 30,000 60,000 90,000 120,000 150,000 NY Metro* Boston Central CT** Bridgeport / Stamford 4,184 2,605 2,118 1,027 0 900 1,800 2,700 3,600 4,500 NY Metro* Boston Central CT** Bridgeport / Stamford |

9 Capital Deployment Primary focus is to deploy capital via organic growth – “new markets, new products, cross-sell” Current dividend yield is ~5.4% (see Appendix for Dividends Per Share - Last 20 Years) Repurchased $191MM of stock in 2010 at a weighted average price of $13.35 Repurchased an additional $61MM of stock in 1Q11 at an average price of $13.09 Prohibited from repurchasing shares until the Danvers Bancorp deal closed Acquisitions Closed 4 deals in 2010: Financial Federal, Butler Bank, RiverBank, Smithtown Danvers Bancorp closed June 30 , effective July 1 Building relationships with banks $1BN - $20BN in asset size Maintaining price discipline in light of challenging industry conditions st th |

10 Loans Deposits Growing Future Earnings Per Share Loans and Deposits per Share * Pro forma for FIF acquisition ** Pro forma for SMTB & LSBX acquisitions *** Pro forma for DNBK acquisition $12.5 $14.0 $15.5 $17.0 $18.5 $20.0 2Q 2009 4Q 2009 * 2Q 2010 ** 4Q 2010 *** 2Q 2011 *** $35.00 $40.00 $45.00 $50.00 $55.00 Gross Loans ($Bn) Loans per share $12.0 $14.0 $16.0 $18.0 $20.0 $22.0 2Q 2009 4Q 2009 * 2Q 2010 ** 4Q 2010 *** 2Q 2011 *** $40.00 $42.50 $45.00 $47.50 $50.00 $52.50 $55.00 $57.50 Deposits ($Bn) Deposits per share |

11 Second Quarter 2011 Results Overview Operating income of $57.3 million or $0.17 per share Net interest margin of 4.13%; down 3 bps from 1Q 2011 Total loan growth of $164MM, 3.7% annualized Total deposit growth of $168MM, 3.7% annualized Operating efficiency ratio improved to 65.7% from 66.2% in 1Q 2011 NPAs as a percentage of originated loans, REO and repossessed assets increased to 2.05% up from 1.96% in 1Q 2011 as a result of a single credit |

12 0.02% 0.04% 0.03% 0.04% (0.16%) 4.13% 4.16% 1Q 2011 Margin 1Q Accretable Yield Reassessment 2Q Accretable Yield Reassessment Loan Yield & Mix Investment Yield & Mix Deposit/ Borrowing Rates 2Q 2011 Margin Total Impact of Decreased Loan Yields: (0.09%) Net Interest Margin Linked Quarter Change |

13 Net Interest Margin* (%) Last Five Quarters 13 3.69 3.74 3.87 4.00 4.09 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 * Excluding the impact of accretable yield reassessments |

14 Last Five Quarters 4.13 3.48 3.61 2.00 3.00 4.00 5.00 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 PBCT Peer Group Median Top 50 Banks Net Interest Margin Compared to Peers and Top 50 Banks Source: SNL Financial and Company filings |

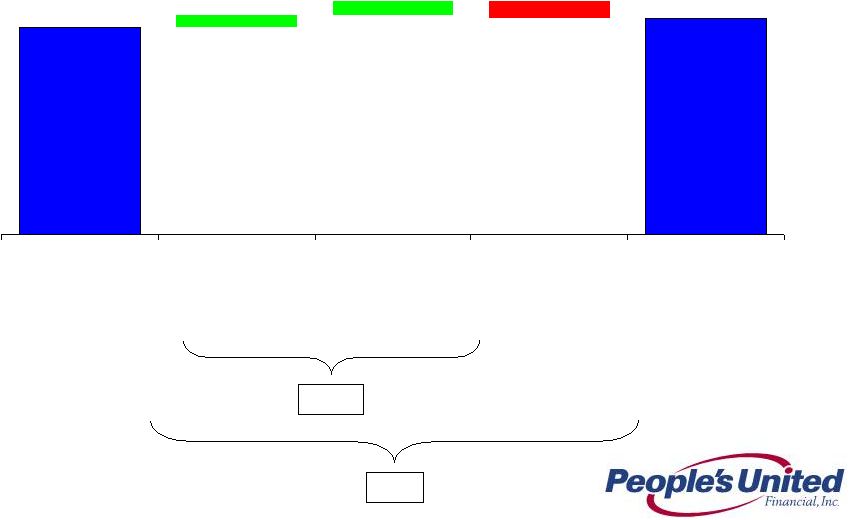

15 Loans Linked Quarter Change (in $ millions) 15 Annualized Linked Quarter Change: 18.7% 9.3% (43.1%) Originated Annualized Linked Quarter Change: 12.2% Total Annualized Linked Quarter Change: 3.7% 17,687 (288) 239 213 17,523 Mar 31, 2011 Retail Commercial Banking Acquired Jun 30, 2011 |

16 Deposits Linked Quarter Change (in $ millions) 16 Annualized Linked Quarter Change: 50.3% (4.9%) Total Annualized Linked Quarter Change: 3.7% 3.7% (30) 56 142 18,278 18,110 Mar 31, 2011 Legacy De Novo Acquired Jun 30, 2011 |

17 Non-Interest Income 1.7 (1.3) (2.0) 1.7 1.9 76.6 74.6 1Q 2011 Bank Service Charges Gain on Smithtown Loan Sales Gain on Residential Loan Sales Insurance Other 2Q 2011 |

18 Non-Interest Expense Non-operating increase from 1Q 202.8 3.3 2.8 (2.9) (2.2) 1.5 1.7 207.0 1Q 2011 Merger Related Executive Separation Comp & benefits Occupancy & Equipment Professional & Outside Svc Other 2Q 2011 |

19 Efficiency Ratio (%) Last Five Quarters 19 72.2% 71.2% 71.1% 66.2% 65.7% 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 |

20 Efficiency Ratio Initiatives How Do We Get There? Steady revenue growth, in-line with recent experience Completion of Smithtown conversion in June produces annual run-rate savings of ~$3MM As announced on our 2Q11 earnings call, changes to our retirement programs and other benefits (~$18MM) and headcount reductions, primarily in corporate positions (~$2MM), will reduce 2012 run-rate expenses by ~$20MM Danvers integration and system conversion produces 2012 run-rate savings of ~$30MM Additional opportunities: Leveraging of upgraded technology following conversion to FIS in mid-2010 Streamlining the organizational structure throughout the franchise Target: 55% run-rate Efficiency Ratio in 2013 |

21 Last Five Quarters 2.05 3.26 3.26 0.00 1.00 2.00 3.00 4.00 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 PBCT Peer Group Median Top 50 Banks by Assets Asset Quality NPAs / Loans & REO* (%) Source: SNL Financial and Company filings * Non-performing assets (excluding acquired non-performing loans) as a percentage of originated loans plus all REO and repossessed assets; acquired non-performing loans excluded as risk of loss has been considered by virtue of our estimate of acquisition-date fair value and/or the existence of an FDIC loss sharing agreement |

22 Last Five Quarters 0.35 0.72 1.09 0.00 0.50 1.00 1.50 2.00 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 PBCT Peer Group Median Top 50 Banks Asset Quality Net Charge-Offs / Avg. Loans (%) Source: SNL Financial and Company filings |

23 Acquired Smithtown Portfolio Workout Progress (in $ millions) Non-Performing Loans at Closing (11/30/2010) $268.7 New Non-Performing Loans 130.4 Sales, Settlements & Payoffs (125.3) Charge-Offs (74.9) Return to Accrual (20.4) Paydowns (9.4) Non-Performing Loans as of June 30, 2011 $169.1 Remaining Non-Accretable Difference (credit mark) $296.6 |

24 Allowance for Loan Losses Originated Portfolio Coverage Detail (in $ millions) 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Commercial Banking 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Retail Banking Commercial ALLL - $163.9 million 91% of Commercial NPLs Retail ALLL - $12.1 million 15% of Retail NPLs Total ALLL - $176.0 million 68% of Total NPLs 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Total |

25 Acquired Loan Portfolio Actual Credit Experience vs. Expectations Acquired loans initially recorded at fair value (inclusive of related credit mark) without carryover of historical ALLL Accounting model is cash-flow based: Expected cash flows are regularly reassessed and compared to actual cash collections As of 6/30/2011 (in $ millions) Carrying Amount Remaining Accretable Yield Remaining Non-Accretable Difference NPLs a Remaining Non-Accretable Difference/NPLs Charge-offs Incurred Since Acquisition FinFed (2/18/10) $485.4 $53.7 $21.1 $55.5 38.0% $9.8 Butler (4/16/10) 88.3 28.3 30.6 16.2 188.9% 3.3 RiverBank (11/30/10) 454.2 117.1 15.0 9.6 156.3% 1.8 Smithtown (11/30/10) b 1,359.3 702.7 296.6 169.1 175.4% 81.1 Total $2,387.2 $901.8 $363.3 $250.4 (a) Represent contractual amounts; loans meet People’s United Financial’s definition of a non-performing loan but are not subject to classification as non-accrual in the same manner as originated loans. Rather, these loans are considered to be accruing loans because their interest income relates to the accretable yield recognized at the pool level and not to contractual interest payments at the loan level. (b) Smithtown charge-offs include $8.2M and $17.7M incurred upon sale of acquired loans in Q211 and Q111, respectively. Cash flows are both acquisition and pool specific Better than expected credit experience results in reclass of non-accretable difference to accretable yield (prospective yield adjustment over the life of the loans) Contractual cash flows (principal & interest) less Expected cash flows (principal & interest) = non-accretable difference (utilized to absorb actual portfolio losses) Expected cash flows (principal & interest) less fair value = accretable yield |

26 Capital Ratios 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 2Q 2011 Pro Forma PEOPLE’S UNITED FINANCIAL Tang. Com. Equity/Tang. Assets 18.0% 17.8% 14.1% 13.9% 13.9% 13.0% Leverage Ratio 1, 5 18.2% 18.0% 14.5% 14.6% 14.3% 13.1% Tier 1 Common 22.1% 22.3% 17.0% 17.2% 17.0% 15.5% Tier 1 Risk-Based Capital 3, 5 22.5% 22.7% 17.5% 17.7% 17.6% 16.2% Total Risk-Based Capital 4, 5 23.4% 23.6% 19.3% 19.4% 19.1% 17.6% PEOPLE’S UNITED BANK Leverage Ratio 1, 5 12.8% 13.0% 11.4% 11.5% 11.6% 10.3% Tier 1 Risk-Based Capital 3, 5 15.7% 15.4% 13.6% 13.9% 14.2% 12.8% Total Risk-Based Capital 4, 5 16.6% 16.4% 14.5% 14.8% 15.0% 13.6% 2 Leverage (core) Capital represents Tier 1 Capital (total stockholder’s equity, excluding: (i) after-tax net unrealized gains (losses) on certain securities classified as available for sale; (ii) goodwill and other acquisition-related intangibles; and (iii) the amount recorded in accumulated other comprehensive income (loss) relating to pension and other postretirement benefits), divided by Adjusted Total Assets (period end total assets less goodwill and other acquisition-related intangibles) Tier 1 Common represents total stockholder’s equity, excluding goodwill and other acquisition-related intangibles, divided by Total Risk-Weighted Assets Tier 1 Risk-Based Capital represents Tier 1 Capital divided by Total Risk-Weighted Assets Total Risk-Based Capital represents Tier 1 Capital plus subordinated notes and debentures, up to certain limits, and the allowance for loan losses, up to 1.25% of total risk weighted assets, divided by Total Risk-Weighted Assets Well capitalized limits for the Bank are: Leverage Ratio, 5%; Tier 1 Risk-Based Capital, 6%; and Total Risk Based Capital, 10%. 1. 2. 3. 4. 5. Notes: |

27 Operating ROAA Progress Last Five Quarters 0.58 0.50 0.64 0.87 0.92 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 |

Appendix |

29 Dividends Per Share Last 20 Years Notes: * Annualized $0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2H 2011* |

30 Peer Group Company Name Ticker State 1 Associated Banc-Corp ASBC WI 2 Astoria Financial Corporation AF NY 3 BOK Financial Corporation BOKF OK 4 City National Corporation CYN CA 5 Comerica Incorporated CMA TX 6 Commerce Bancshares, Inc. CBSH MO 7 Cullen/Frost Bankers, Inc. CFR TX 8 First Horizon National Corporation FHN TN 9 Flagstar Bancorp, Inc. FBC MI 10 Fulton Financial Corporation FULT PA 11 Hudson City Bancorp, Inc. HCBK NJ 12 M&T Bank Corporation MTB NY 13 Marshall & Ilsley Corporation MI WI 14 New York Community Bancorp, Inc. NYB NY 15 Synovus Financial Corp. SNV GA 16 TCF Financial Corporation TCB MN 17 Valley National Bancorp VLY NJ 18 Webster Financial Corporation WBS CT 19 Zions Bancorporation ZION UT |

For more information, investors may contact: Peter Goulding, CFA 203-338-6799 peter.goulding@peoples.com |