2 nd Quarter 2012 Earnings Conference Call July 19, 2012 EXHIBIT 99.2 |

1 Certain statements contained in this release are forward-looking in nature. These include all statements about People's United Financial's plans, objectives, expectations and other statements that are not historical facts, and usually use words such as "expect," "anticipate," "believe" and similar expressions. Such statements represent management's current beliefs, based upon information available at the time the statements are made, with regard to the matters addressed. All forward-looking statements are subject to risks and uncertainties that could cause People's United Financial's actual results or financial condition to differ materially from those expressed in or implied by such statements. Factors of particular importance to People’s United Financial include, but are not limited to: (1) changes in general, national or regional economic conditions; (2) changes in interest rates; (3) changes in loan default and charge-off rates; (4) changes in deposit levels; (5) changes in levels of income and expense in non-interest income and expense related activities; (6) residential mortgage and secondary market activity; (7) changes in accounting and regulatory guidance applicable to banks; (8) price levels and conditions in the public securities markets generally; (9) competition and its effect on pricing, spending, third-party relationships and revenues; (10) the successful integration of acquired companies; and (11) changes in regulation resulting from or relating to financial reform legislation. People's United Financial does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Forward-Looking Statement |

2 Second Quarter 2012 Results Overview / 2Q 2012 vs. 1Q 2012 Operating earnings of $67.2 million or $0.20 per share, versus $0.18 per share in the prior quarter Net interest margin of 3.97%, down 4 bps Loan growth of $116 million, 2.3% annualized growth rate Deposit growth of $190 million, 3.6% annualized growth rate Non-interest income increased $3.3 million to $75.7 million Efficiency ratio improved to 61.5% from 63.2% TCE/TA ratio decreased to 11.5% from 11.7% as we have continued to efficiently deploy capital |

3 Continue to expand presence in the New York metro area Completed the acquisition of 57 Citizens branches Converted systems and rebranded all acquired Citizens branches over the weekend of June 22 nd New York metro footprint now includes approximately 100 branches Added seasoned in-market lending professionals over the last year and a half • Five C&I lenders and two ABL professionals Hired three senior lenders to lead our New York metro commercial real estate lending efforts Increased fee income generation particularly in cash management and brokerage services Repurchased 4.5 million shares, or $53.7 million, at a weighted average price of $11.93 per share Recent Initiatives |

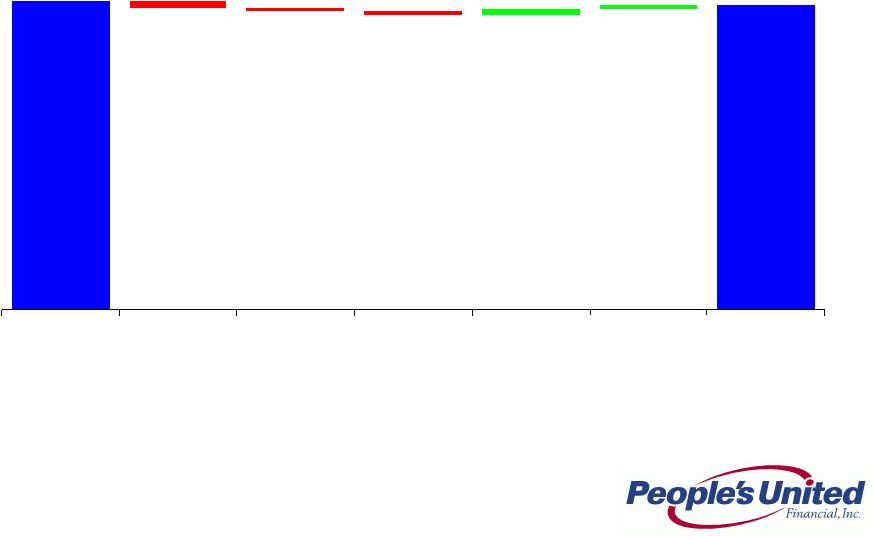

4 Net Interest Margin - Decrease from 1Q 2012 4.01% 3.97% 0.08% (0.08%) 0.05% (0.04%) (0.05%) 1Q 2012 Margin Lower Loan Yields Asset Mix FV Amort- Acquired CDs Cost Recovery Income Lower Funding Rates/ Mix 2Q 2012 Margin |

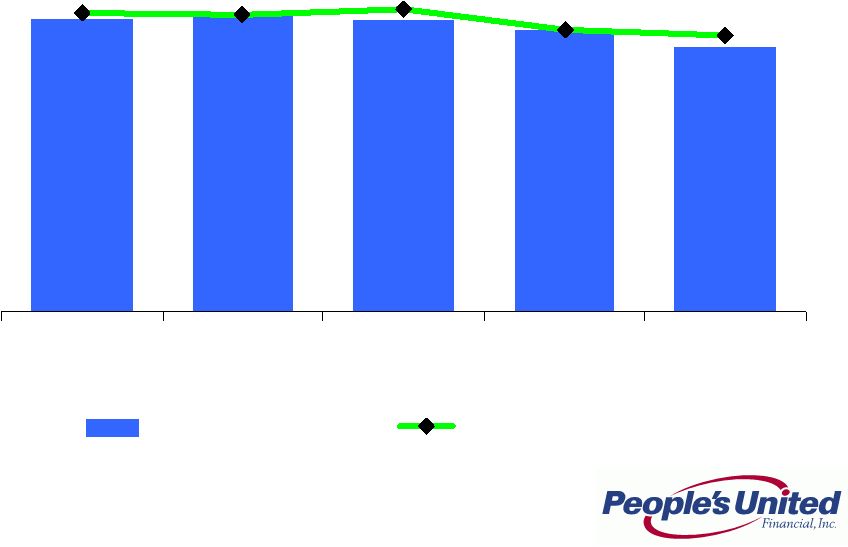

5 Net Interest Margin 4.09 4.11 4.07 4.01 3.89 4.13 4.11 4.16 4.01 3.97 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 Margin- Operating Margin- Reported |

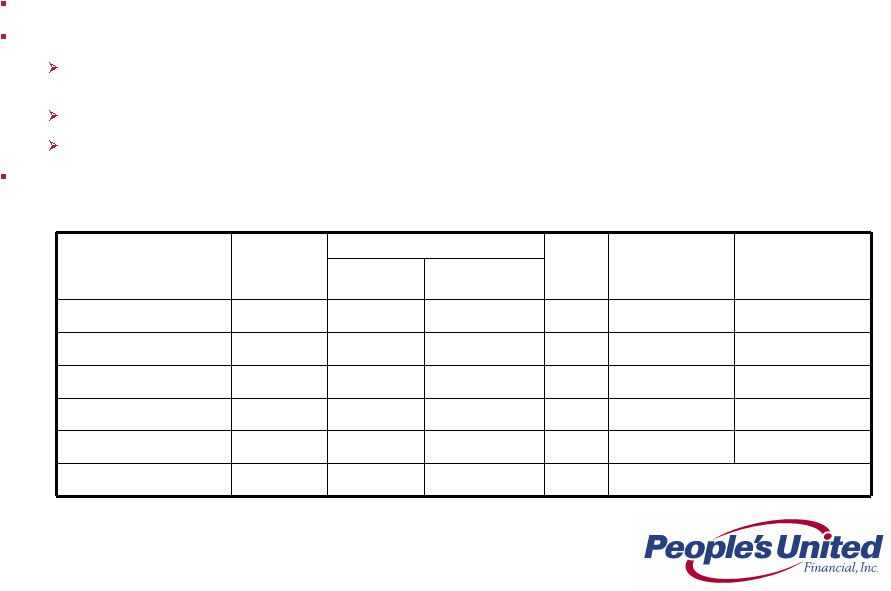

6 Acquired Loan Portfolio Actual Credit Experience vs. Expectations Acquired loans initially recorded at fair value (inclusive of related credit mark) without carryover of historical ALLL Accounting model is cash-flow based: Contractual cash flows (principal & interest) less Expected cash flows (principal & interest) = non-accretable difference (effectively utilized to absorb actual portfolio losses) Expected cash flows (principal & interest) less fair value = accretable yield Expected cash flows are regularly reassessed and compared to actual cash collections The following reclassifications from non-accretable difference to accretable yield during the period reflect better than anticipated credit performance: Butler: $6.5MM, Smithtown: $2.4MM As of 6/30/2012 (in $ millions) Carrying Amount a, b Carrying Amount Component b NPLs c Non-Accretable Difference/NPLs Charge-offs Incurred Since Acquisition Accretable Yield Non-Accretable Difference FinFed (2/18/10) $210.2 $12.8 $7.9 $36.5 22% $11.4 Butler (4/16/10) 68.2 27.1 16.4 11.4 144% 5.2 RiverBank (11/30/10) 319.7 105.9 11.1 25.3 44% 3.9 Smithtown (11/30/10) c 954.2 461.5 127.6 111.5 114% 115.8 Danvers (7/1/11) 1, 464.3 542.4 28.0 51.9 54% 8.1 Total $3,016.6 $1,149.7 $191.0 $236.6 (a) Initial carrying amounts of acquired portfolios are as follows: FinFed, $1.2BN; Butler, $141MM; RiverBank, $518MM; Smithtown, $1.6BN; and Danvers, $1.9BN. (b) Carrying amount and related components reflect loan sale, settlement and payoff activity which have occurred since acquisition. (c) Represent contractual amounts; loans meet People’s United Financial’s definition of a non-performing loan but are not subject to classification as non-accrual in the same manner as originated loans. Rather, these loans are considered to be accruing loans because their interest income relates to the accretable yield recognized at the pool level and not to contractual interest payments at the loan level. |

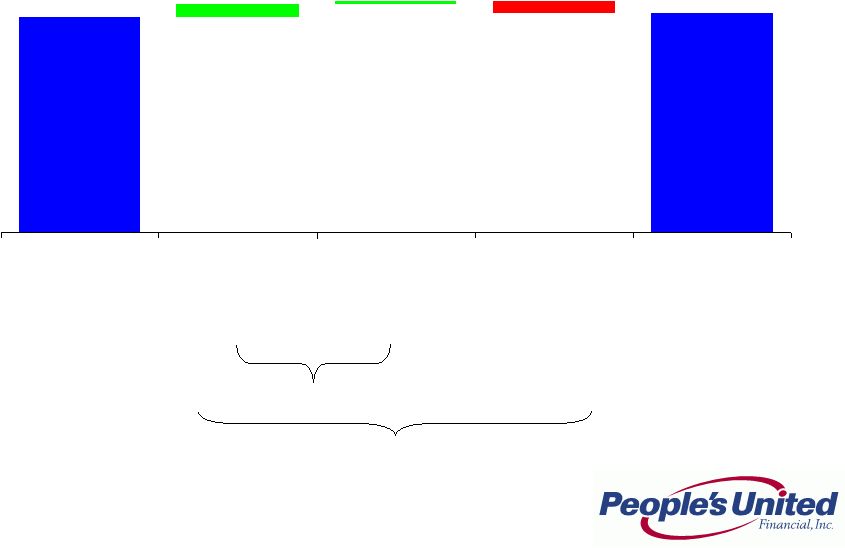

7 Acquired Loan Portfolio Amortization of Original Discount on Acquired Loan Portfolio Note: 1. Excluding FinFed, the weighted average coupon on the acquired loan portfolio is 5.20%. 2. Represents the difference between the outstanding balance of the acquired loan portfolio and the carrying amount of the acquired loan portfolio. $ in millions, except per share data Impact on Net Interest Margin Impact on Earnings Per Share 2Q12 Total Accretion (All interest income on acquired loans) 56 Interest Income from Amortization of Original Discount on Acq. Loan Portfolio 11.7 1Q12 Acquired Loan Portfolio Carrying Amount 3,377 2Q12 Effective Tax Rate 32% 2Q12 Acquired Loan Portfolio Carrying Amount 3,017 2Q12 Average Acquired Loan Portfolio 3,197 2Q12 Earnings from Amortiz. of Original Discount on Acq. Loan Portfolio 7.9 Effective Yield on Acquired Loan Portfolio 6.97% 2Q12 Weighted Average Shares Outstanding 340.7 Weighted Average Coupon on Acquired Loan Portfolio 5.51% 2Q12 EPS Impact from Amortiz. of Discount on Acq. Loan Portfolio $0.02 Incremental Yield Attributable to Amortiz. of Discount on Acq. Loan Portfolio 1.46% Incremental Interest Income from Amortiz. of Discount on Acq. Loan Portfolio 11.7 2Q12 Average Earning Assets 24,040 Add: Average unamortized loan discount 2 106 Adjusted 1Q12 Average Earning Assets 24,146 Impact on Overall Net Interest Margin (bps) 19 Operating Net Interest Margin 3.89% Adjusted Net Interest Margin 3.70% Amortization of Original Discount on Acquired Loan Portfolio Amortization of Original Discount on Acquired Loan Portfolio 1 |

8 Loans Linked Quarter Change (in $ millions) Annualized linked QTD change 12.7% 7.7% -42.7% Annualized linked QTD change- Originated 11.2% Annualized Linked QTD change- Total 2.3% 20,606 20,489 103 (360) 374 Mar 31, 2012 Commercial Banking Retail Acquired Jun 30, 2012 |

9 Deposits by Business Line Linked Quarter Change (in $ millions) * Retail includes Wealth Management deposits of $72MM at 3/2012 and $69MM at 6/2012 Total 21,268 21,458 Retail * Annualized linked QTD change 3.7% 3.3% Annualized Linked QTD change- Total 3.6% Commercial 15,959 16,105 5,353 5,309 146 44 Mar 31, 2012 Retail Commercial Jun 30, 2012 |

10 Loans Deposits Growing Future Earnings Per Share Loans and Deposits per Share $60.49 $14 $15 $16 $17 $18 $19 $20 $21 $22 2010Q2 2010Q4 2011Q2 2011 Q4 2012 Q2 $40 $45 $50 $55 $60 $65 Gross Loans ($BN) Loans per Share $62.99 $14 $15 $16 $17 $18 $19 $20 $21 $22 2010Q2 2010Q4 2011Q2 2011Q4 2012 Q2 $40 $45 $50 $55 $60 $65 Deposits ($BN) Deposits per share |

11 72.4 75.7 (0.2) (1.2) (0.8) 1.0 1.6 2.2 0.7 1Q 2012 Insurance Gain on Loan Sales- Residential Bank Service Charges Loan Prepayment Fees Operating Lease Income Gain on Loan Sales- Acquired Other 2Q 2012 Non-Interest Income Linked Quarter Change (in $ millions) |

12 Non-Operating Operating Total Non-Interest Expense Linked Quarter Change (in $ millions) 208.6 205.7 0.6 205.6 0.7 1.5 (5.0) (0.7) 202.1 3.0 3.6 1Q 2012 Non-Operating Citizens Operating Professional & Outside Svc Comp & Benefits Other 2Q 2012 |

13 Efficiency Ratio Last Five Quarters 64.9% 62.0% 61.8% 63.2% 61.5% 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 |

14 Acquired Citizens branches will add approximately $7.8MM of non-interest expenses on a quarterly basis In addition to the initiatives below, we are taking a longer-term view of cost planning, which will help us reduce the pro forma cost base Recent Initiatives Focused on Cost Reduction Initiatives Status Benchmarking business unit performance Benchmarking initiatives complete Right-sized our employee base following acquisitions FTE reduced by 276, even after staffing for revenue initiatives Consolidating 15 branches Consolidated 14 branches, completed sale of 1 branch Actively marketing unused facilities 20 properties identified (14 owned, 6 leased); 50% of cost savings anticipated from 3 locations Identify IT related savings $2 million of annual IT contractor and other consultant savings will be realized in 2012 Lower than anticipated rent and depreciation expense Estimated $900,000 positive impact in 2012 Savings in check processing charges and courier fees Estimated $900,000 positive impact in 2012 Savings in core processing costs Estimated $2.3 million positive impact in 2012 Purchasing initiatives and legal fee savings Estimated $500,000 positive impact in 2012 Other initiatives Identified approximately $9 million of other annual savings throughout the franchise |

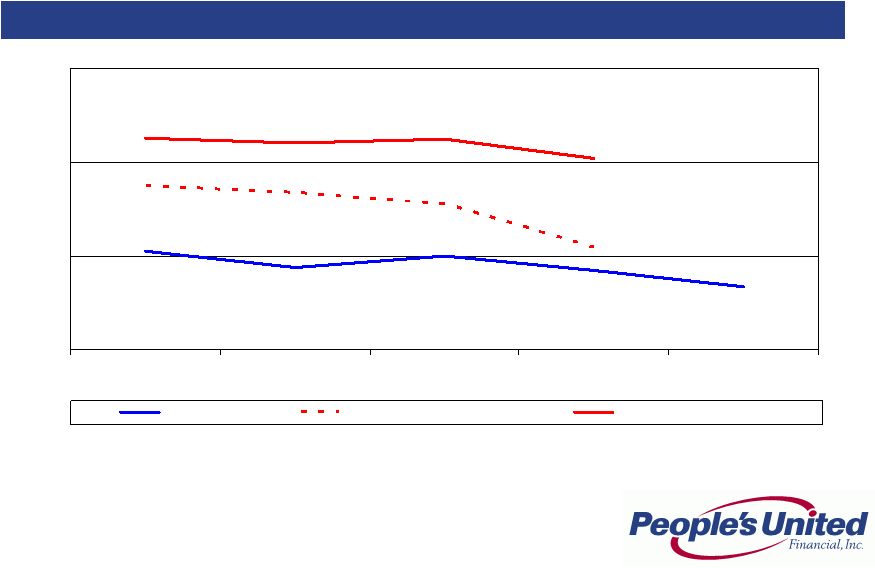

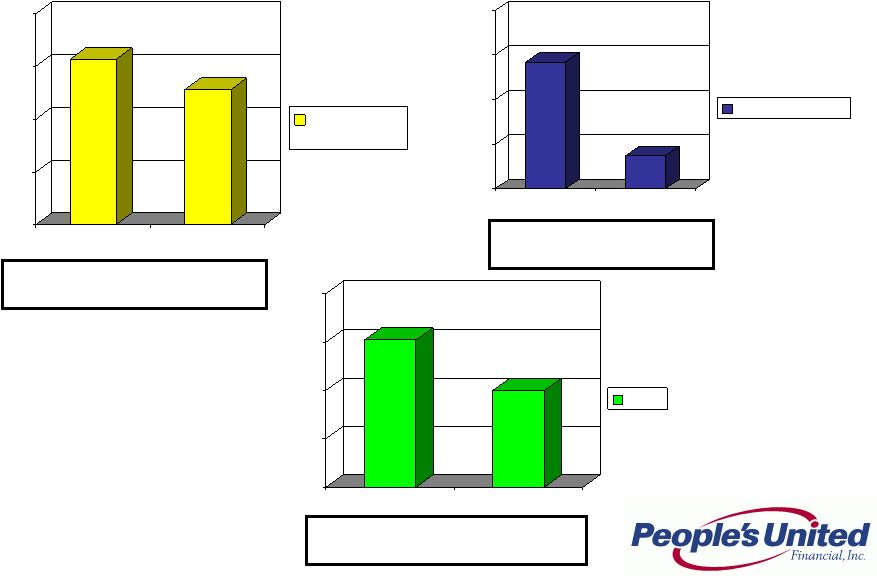

15 1.67 2.09 3.04 1.00 2.00 3.00 4.00 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 PBCT Peer Group Median Top 50 Banks by Assets Last Five Quarters Asset Quality NPAs / Loans & REO* (%) * Source: SNL Financial and Company filings Non-performing assets (excluding acquired non-performing loans) as a percentage of originated loans plus all REO and repossessed assets; acquired non-performing loans excluded as risk of loss has been considered by virtue of (i) our estimate of acquisition-date fair value, (ii) the existence of an FDIC loss sharing agreement, and/or (iii) allowance for loan losses established subsequent to acquisition |

16 Last Five Quarters 0.26 0.46 0.71 0.00 0.50 1.00 1.50 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 PBCT Peer Group Median Top 50 Banks Asset Quality Net Charge-Offs / Avg. Loans (%) Source: SNL Financial and Company filings |

17 Allowance for Loan Losses Originated Portfolio Coverage Detail (in $ millions) 1.57% 1.28% 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Commercial Banking 1.42% 0.37% 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Retail Banking Commercial ALLL - $155.5 million 82% of Commercial NPLs Retail ALLL - $20.0 million 26% of Retail NPLs Total ALLL - $175.5 million 66% of Total NPLs 1.52% 1.00% 0.00% 0.50% 1.00% 1.50% 2.00% NPLs:Loans ALLL:Loans Total |

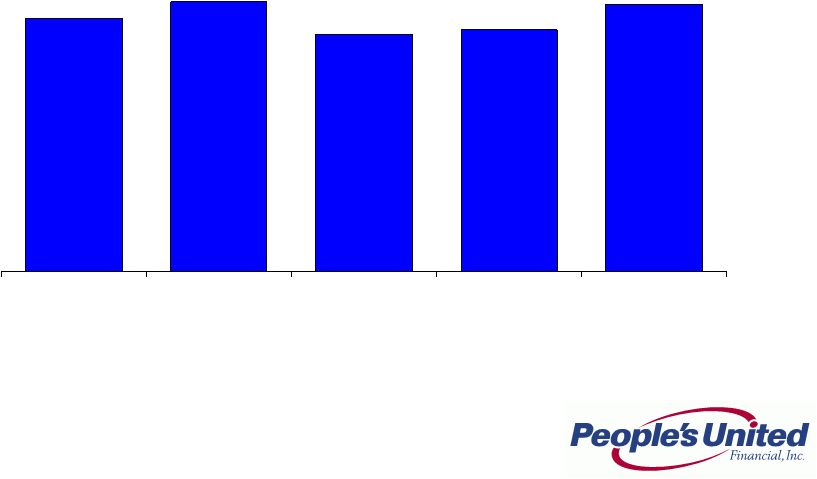

18 Operating ROAA Progress Last Five Quarters 0.92% 0.98% 0.86% 0.88% 0.97% 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 |

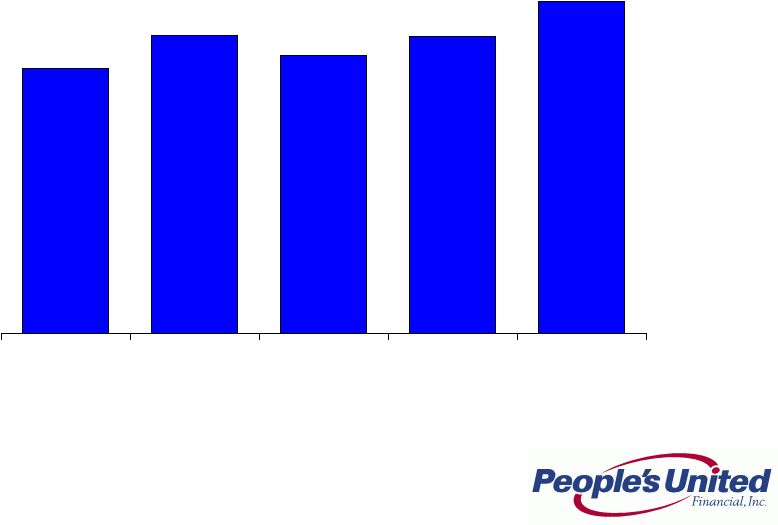

19 Operating ROATE Progress Last Five Quarters 7.1% 8.0% 7.4% 8.0% 8.9% 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 |

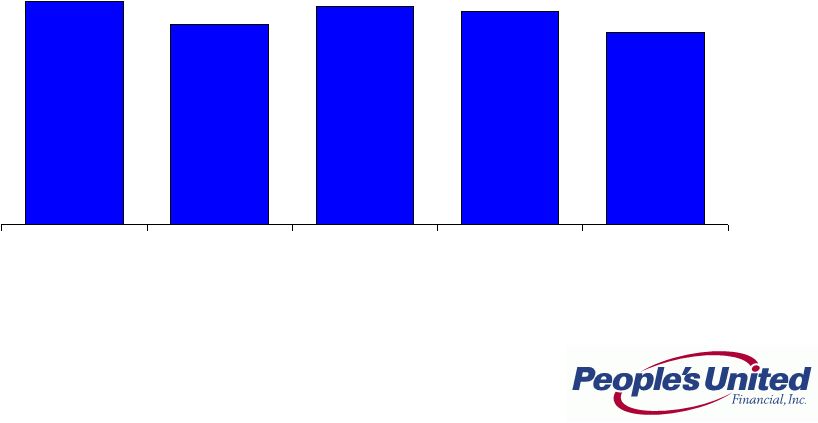

20 Operating Dividend Payout Ratio Last Five Quarters 95% 85% 93% 91% 82% 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 |

21 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 People’s United Financial Tang. Com. Equity/Tang. Assets 13.9% 12.5% 12.0% 11.7% 11.5% Leverage Ratio 1, 5 14.3% 12.7% 12.5% 12.2% 11.9% Tier 1 Common 2 17.0% 15.0% 14.3% 13.9% 13.6% Tier 1 Risk-Based Capital 3, 5 17.6% 15.2% 14.8% 14.5% 14.1% Total Risk-Based Capital 4, 5 19.1% 16.7% 16.2% 16.0% 15.6% People’s United Bank Leverage Ratio 1, 5 11.6% 11.8% 11.1% 11.0% 11.0% Tier 1 Risk-Based Capital 3, 5 14.2% 14.1% 13.1% 13.1% 13.1% Total Risk-Based Capital 4,5 15.0% 14.9% 14.0% 14.1% 14.0% Notes: 1. Leverage (core) Capital represents Tier 1 Capital (total stockholder’s equity, excluding: (i) after-tax net unrealized gains (losses) on certain securities classified as available for sale; (ii) goodwill and other acquisition-related intangibles; and (iii) the amount recorded in accumulated other comprehensive income (loss) relating to pension and other postretirement benefits), divided by Adjusted Total Assets (period end total assets less goodwill and other acquisition-related intangibles) 2. Tier 1 Common represents total stockholder’s equity, excluding goodwill and other acquisition-related intangibles, divided by Total Risk-Weighted Assets 3. Tier 1 Risk-Based Capital represents Tier 1 Capital divided by Total Risk-Weighted Assets 4. Total Risk-Based Capital represents Tier 1 Capital plus subordinated notes and debentures, up to certain limits, and the allowance for loan losses, up to 1.25% of total risk weighted assets, divided by Total Risk-Weighted Assets 5. Well capitalized limits for the Bank are: Leverage Ratio, 5%; Tier 1 Risk-Based Capital, 6%; and Total Risk-Based Capital, 10% Capital Ratios |

22 Summary Premium brand built over 170 years High quality Northeast footprint characterized by wealth, density and commercial activity Strong leadership team Solid net interest margin Superior asset quality Focus on relationship-based banking Growing loans and deposits within footprint - in two of the largest MSAs in the country (New York City, #1 and Boston, #10) Improving profitability Returning capital to shareholders Strong capital base as evidenced by robust Tangible Common Equity and Tier 1 Common ratios Sustainable Competitive Advantage |

Appendix |

24 We do not expect short-term interest rates to rise any time soon Given short-term interest rates are very low and are expected to remain low for the near term, we have added additional securities For 1Q 2012 we were more than twice as asset sensitive as the estimated median of our peer group, depending on the scenario For an immediate parallel increase of 100bps, our net interest income is projected to increase by ~$59MM on an annualized basis Yield curve twist scenarios confirm that we are reasonably well protected from bull flattener (short rates are unchanged, long rates fall) and benefit considerably from bear flattener environments (short rates rise, long rates are unchanged) Notes: 1. Analysis is as of 3/31/12 filings 2. Data as of 3/31/12 SEC filings, where exact +100bps shock up scenario data was not provided PBCT interpolated based on data disclosed 3. Data as of 3/31/12 filings, where exact +200bps shock up scenario data was not provided PBCT interpolated based on data disclosed Current Asset Sensitivity Net Interest Income at Risk 1 Analysis involves PBCT estimates, see notes below Change in Net Interest Income Scenario Lowest Amongst Peers Highest Amongst Peers Peer Median PBCT Multiple to Peer Median Shock Up 100bps ² -4.3% 5.8% 2.4% 2.6x Shock Up 200bps ³ -7.4% 11.7% 4.2% 3.3x |

25 Peer Group Firm Ticker City State 1 Associated ASBC Green Bay WI 2 BancorpSouth BXS Tupelo MS 3 City National CYN Los Angeles CA 4 Comerica CMA Dallas TX 5 Commerce CBSH Kansas City MO 6 Cullen/Frost CFR San Antonio TX 7 East West EWBC Pasadena CA 8 First Niagara FNFG Buffalo NY 9 FirstMerit FMER Akron OH 10 Fulton FULT Lancaster PA 11 Huntington HBAN Columbus OH 12 M&T MTB Buffalo NY 13 New York Community NYB Westbury NY 14 Signature SBNY New York NY 15 Susquehanna SUSQ Lititz PA 16 Synovus SNV Columbus GA 17 Valley National VLY Wayne NJ 18 Webster WBS Waterbury CT 19 Wintrust WTFC Lake Forest IL 20 Zions ZION Salt Lake City UT |

For more information, investors may contact: Peter Goulding, CFA 203-338-6799 peter.goulding@peoples.com |