Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

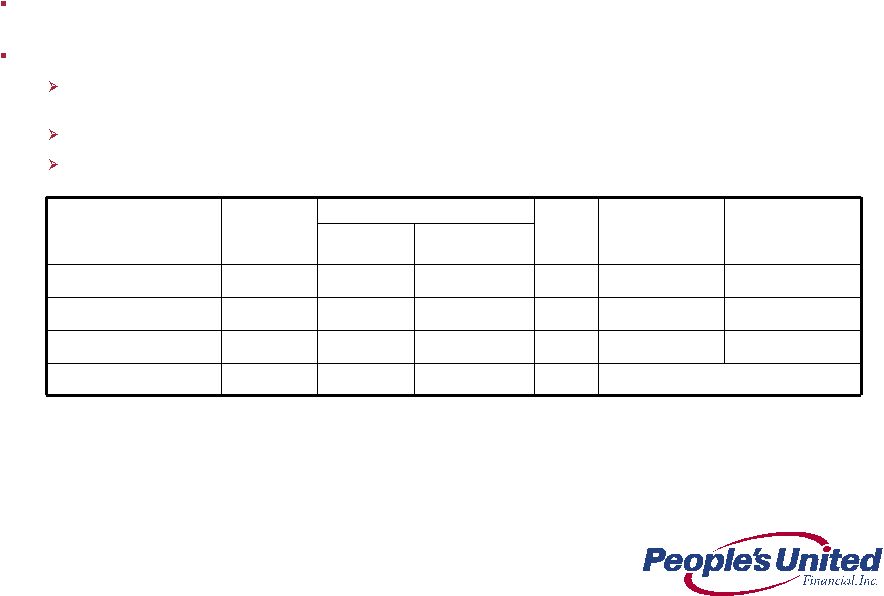

Filing tables

Filing exhibits

PBCT similar filings

- 10 Sep 13 Barclays Global Financial Services Conference

- 30 Jul 13 Certain statements contained in this release are forward-looking in nature. These include all statements

- 19 Jul 13 People’s United Financial Reports Second Quarter Operating Earnings and Net Income of $0.20 Per Share

- 13 Jun 13 Regulation FD Disclosure

- 13 May 13 Regulation FD Disclosure

- 19 Apr 13 Amendments to Articles of Incorporation or Bylaws

- 18 Apr 13 People’s United Financial Reports First Quarter Operating Earnings of $0.18 Per Share and Net Income of $0.16 Per Share; Announces Dividend Increase

Filing view

External links