UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

o Preliminary Proxy Statement

¨ Confidential, for Use of the Commission Only (as permitted by Rule14a-6(e)(2))

¨ Definitive Proxy Statement

x Definitive Additional Materials

o Soliciting Material Under Rule 14a-12

DENNY’S CORPORATION |

| (Name of Registrant as Specified in Its Charter) |

OAK STREET CAPITAL MASTER FUND, LTD. OAK STREET CAPITAL MANAGEMENT, LLC DAVID MAKULA PATRICK WALSH DASH ACQUISITIONS LLC JONATHAN DASH SOUNDPOST CAPITAL, LP SOUNDPOST CAPITAL OFFSHORE, LTD. SOUNDPOST ADVISORS, LLC SOUNDPOST PARTNERS, LP SOUNDPOST INVESTMENTS, LLC JAIME LESTER LYRICAL OPPORTUNITY PARTNERS II, L.P. LYRICAL OPPORTUNITY PARTNERS II, LTD. LYRICAL OPPORTUNITY PARTNERS II GP, L.P. LYRICAL CORP III, LLC LYRICAL PARTNERS, L.P. LYRICAL CORP I, LLC JEFFREY KESWIN PATRICK H. ARBOR |

| (Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

x No fee required.

¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

¨ Fee paid previously with preliminary materials:

¨ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

(1) Amount previously paid:

(2) Form, Schedule or Registration Statement No.:

(3) Filing Party:

(4) Date Filed:

The Committee to Enhance Denny’s (the “Committee”), together with the other Participants named herein, is filing materials contained in this Schedule 14A with the Securities and Exchange Commission (the “SEC”) in connection with the solicitation of proxies for the election of its slate of director nominees at the 2010 annual meeting of stockholders (the “Annual Meeting”) of Denny’s Corporation. The Committee has made a definitive filing with the SEC of a proxy statement and accompanying GOLD proxy card to be used to solicit votes for the election of its slate of director nominees at the Annual Meeting.

Item 1: The following materials were posted by the Committee to http://www.enhancedennys.com:

Enhance Denny’s

Important Notice

This website may contain forward-looking statements. These statements may be identified by the use of forward-looking terminology such as the words “expects,” “intends,” “believes,” “anticipates” and other terms with similar meaning indicating possible future events or actions relating to the business or stockholders of Denny’s Corporation (the “Company”). These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties that could cause actual results to differ materially. These risks and uncertainties include, among others, the ability to successfully solicit sufficient proxies to elect the director nominees (the “Nominees”) nominated by The Committee to Enhance Denny’s (the “C ommittee”) to the Company’s board of directors at the Company’s 2010 Annual Meeting of Stockholders (the “2010 Annual Meeting”), the ability of the Nominees to improve the corporate governance and performance of the Company and risk factors associated with the business of the Company, as described in the Company’s Annual Report on Form 10-K for the fiscal year ended December 30, 2009, and in other periodic reports of the Company, which are available at no charge at the website of the Securities and Exchange Commission (“SEC”) at http://www.sec.gov. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results.

This website may be deemed to constitute proxy solicitation material and is intended solely to inform stockholders so that they may make an informed decision regarding the election of directors at the 2010 Annual Meeting.

THE COMMITTEE, TOGETHER WITH THE OTHER PARTICIPANTS (AS DEFINED BELOW), HAS FILED WITH THE SEC A DEFINITIVE PROXY STATEMENT AND ACCOMPANYING PROXY CARD TO BE USED TO SOLICIT PROXIES FOR THE ELECTION OF ITS SLATE OF DIRECTOR NOMINEES AT THE 2010 ANNUAL MEETING.

THE COMMITTEE STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT BECAUSE IT CONTAINS IMPORTANT INFORMATION. SUCH PROXY STATEMENT IS AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THE SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR, MACKENZIE PARTNERS, INC., TOLL-FREE AT (800) 322-2885 OR COLLECT AT (212) 929-5500 OR VIA EMAIL AT ENHANCEDENNYS@MACKENZIEPARTNERS.COM.

THE PARTICIPANTS IN THE PROXY SOLICITATION ARE OAK STREET CAPITAL MASTER FUND, LTD., OAK STREET CAPITAL MANAGEMENT, LLC, DAVID MAKULA, PATRICK WALSH, DASH ACQUISITIONS LLC, JONATHAN DASH, SOUNDPOST CAPITAL, LP, SOUNDPOST CAPITAL OFFSHORE, LTD., SOUNDPOST ADVISORS, LLC, SOUNDPOST PARTNERS, LP, SOUNDPOST INVESTMENTS, LLC, JAIME LESTER, LYRICAL OPPORTUNITY PARTNERS II, L.P., LYRICAL OPPORTUNITY PARTNERS II, LTD., LYRICAL OPPORTUNITY PARTNERS II GP, L.P., LYRICAL CORP III, LLC, LYRICAL PARTNERS, L.P., LYRICAL CORP I, LLC, JEFFREY KESWIN AND PATRICK H. ARBOR (COLLECTIVELY, THE “PARTICIPANTS”).

THE PARTICIPANTS COLLECTIVELY OWN AN AGGREGATE OF 6,245,476 SHARES OF COMMON STOCK OF THE COMPANY.

This communication is not a solicitation of a proxy, which may be done only pursuant to a definitive proxy statement.

| I have read and agree to the terms of this website |

| I disagree (You will not gain access to this website without agreeing to the above terms). |

Use of this website and the information contained herein is subject to the restrictions and limitations described in Terms and Conditions. By accessing or retrieving information from this website, the user acknowledges and agrees to be bound by the terms specified in Terms and Conditions.

| The Committee to Enhance Denny’s The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions LLC, owns approximately 6.3% of the outstanding shares of Denny’s Corporation. We are seeking your support to elect our three highly qualified director nominees – Patrick Arbor, Jonathan Dash and David Makula – to the Denny’s board of directors at the 2010 Annual Meeting of Shareholders to be held on May 19, 2010. We created this website to serve as a forum to share our concerns regarding Denny’s and to present our nominees’ plans to create value for all shareholders. Our concerns include, but are not limited to, the following:

o Failure to grow system-wide restaurants o Ceding the #1 market position to International House of Pancakes o Unacceptable declines in key operating trends such as guest traffic o Inappropriately high general and administrative expenses o Expensive and ineffective marketing strategies o Imprudent capital allocation decisions o Lack of accountability for management at the board level o Marginalization of shareholders and franchisees, and o Extremely poor share price performance Denny’s is an iconic American brand and we believe shareholder value can be restored with the help of our highly qualified director nominees. If elected at the Annual Meeting, our nominees would seek to work with the other board members to address the concerns outlined above and discussed in further detail in our proxy statement, which has been posted to this website. We invite you to read the materials on this website to learn more about our campaign at Denny’s and how you can help. |  | ||

| |||

A MESSAGE FROM

THE COMMITTEE TO ENHANCE DENNY’S

VOTE YOUR GOLD PROXY CARD TODAY TO ELECT THE COMMITTEE’S THREE HIGHLY QUALIFIED DIRECTOR NOMINEES

April 13, 2010

Dear Denny’s Shareholder:

The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions LLC, owns approximately 6.3% of the outstanding shares of Denny’s. We are seeking your support to elect our three highly qualified, independent director nominees to the Denny’s board of directors at the Annual Meeting of Shareholders to be held on May 19, 2010. We are writing to share our concerns regarding Denny’s and to outline our nominees’ plans to create value for all shareholders.

Our proposed director nominees are Patrick Arbor, Jonathan Dash and David Makula – their bios can be found toward the end of this letter. They bring significant skills, experience, objectivity and judgment to the board and are committed to implementing a set of initiatives designed to increase long-term shareholder value. We are soliciting proxies to elect not only our three director nominees, but also the candidates who have been nominated by the Company other than Nelson J. Marchioli, Robert E. Marks and Debra Smithart-Oglesby. We believe it is critical to remove these long-tenured directors who we believe are most responsible for the current state of the Company. After reading this letter, you will have the information necessary to make an informed decision at the upcoming Annual Meeting and we are hopeful that you will understand why it is absolutely essential to elect our director nominees. We are counting on your support as each and every vote will matter as we seek to maximize value for all Denny’s shareholders.

INCUMBENT BOARD HAS PRESIDED OVER THE DESTRUCTION OF SUBSTANTIAL SHAREHOLDER VALUE

We believe Denny’s current board and management team have implemented and must take responsibility for a strategic and capital allocation plan that has destroyed significant shareholder value. The Denny’s board and management team have been given a sufficiently long period of time to implement their plans and create value for shareholders, and they have failed. As long-term shareholders are aware, Denny’s share price has declined by 76.9% between the Company’s emergence from bankruptcy in January 1998 and December 31, 2009, not accounting for the time value of money. Over the past five completed fiscal years alone, Denny’s share price has plummeted by 51.3%, an unacceptable outcome. While we acknowledge the market volatility associated with last year’s global economic decline, we believe Denny’s historically poor share price performance demonstrates the board’s and management’s inability to maximize shareholder value. If shareholders continue to accept the status quo, we are concerned that Denny’s future will look very much like its past. These abysmal results cannot be allowed to continue.

Price Performance Comparison

DENNY’S SHARE PRICE HAS INCREASED SIGNIFICANTLY SINCE WE FILED OUR INITIAL SCHEDULE 13D

Since disclosing our Denny’s position in our initial Schedule 13D filed on January 21, 2010, the share price has appreciated by approximately 70%1. This share price performance has been achieved in a period during which the Company reported continued deterioration in key operating metrics such as comparable store guest traffic. We believe the recent share price performance is reflective of a market view that change is needed at Denny’s. Nevertheless, we believe the current market value fails to reflect Denny’s full potential, a potential that can be realized with changes to the board of directors.

Our shareholder group is financially and constitutionally committed to improving the future direction of Denny’s. We have no interest in lingering on the sidelines while the board and management team attempt to figure out an effective strategic plan. Management’s track record spans both good and bad economic times, and the operating results of Denny’s closest competitors only serve to highlight management’s shortcomings.

Our concerns with the current Denny’s board and management can be summarized as follows:

| · | Failure to grow system-wide restaurants |

| · | Ceding the #1 market position to International House of Pancakes (“IHOP”) |

| · | Unacceptable declines in key operating trends such as guest traffic |

| · | Inappropriately high general and administrative expenses |

| · | Expensive and ineffective marketing strategies |

| · | Imprudent capital allocation decisions |

| · | Lack of accountability for management at the board level |

| · | Marginalization of shareholders and franchisees, and |

| · | Extremely poor share price performance |

| 1 | Based on closing price of $2.30 per share on January 21, 2010 and closing price of $3.89 per share on April 9, 2010. |

FAILURE TO GROW THE SYSTEM HAS

WEAKENED DENNY’S COMPETITIVE POSITION

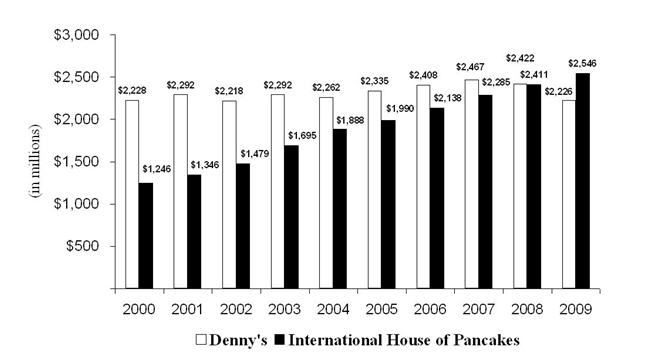

We believe the perennial decline in the number of system-wide restaurants has undermined Denny’s ability to stay competitive and has negatively impacted profitability. According to Denny’s public filings, the Company’s system-wide units peaked ten years ago, at 1,822 restaurants, shortly before Nelson Marchioli was appointed CEO in 2001. Over the past decade, the board oversaw a 15% decline in total system-wide restaurants to 1,551 units as of December 30, 2009. This stands in stark contrast to the Company’s closest competitor, IHOP, which during a similar time frame increased system-wide restaurants from 922 units to 1,456 units as of December 31, 2009.

Notably, we view IHOP as a similarly situated restaurant concept, with no fundamental competitive advantage other than its current leadership relative to Denny’s. IHOP presents an interesting case study of what can be accomplished in the family dining category when a quality leadership team is in charge. Since 2000, IHOP has more than doubled system-wide sales from $1.2B to over $2.5B for 2009, based on public filings. During this same time frame, Denny’s system-wide sales, on the other hand, have stagnated. The chart below contrasts system-wide sales performance for these closely related concepts since 2000.

System-Wide Sales Comparison

Source: SEC filings

GUEST CHECK INCREASES HAVE LED TO

UNACCEPTABLE GUEST TRAFFIC DECLINES

We believe management failed to improve key restaurant operating trends such as same store guest traffic – despite shrinking units by 15% since 2000. Since Mr. Marchioli assumed his role as CEO, we believe Denny’s same store guest traffic has been among the worst of its peers. In fact, Denny’s customer traffic has declined in seven of the last eight years.

Despite these persistent guest traffic declines, management responded by consistently raising prices year after year. We are deeply concerned that Denny’s pricing strategy only served to accelerate guest traffic declines, particularly during 2008 when management hiked prices in the face of lower commodity costs and an ailing U.S. consumer. The chart below illustrates the loss of customers under current management.

Denny’s Cumulative Decline in Guest Traffic

Source: SEC filings

Incidentally, the Denny’s board and management team have themselves acknowledged the importance of increasing guest counts based on their 2005 Annual Report which states:

“Our future success will be driven by increasing guest counts and capitalizing on the significant capacity for sales growth within our restaurants.”

Unfortunately, five years later, shareholders are still waiting for them to increase guest counts and fill excess restaurant capacity. If these guest traffic declines are allowed to persist, we strongly believe that the effect on shareholders and the franchisee base will be dire. We must act now.

EXCESS CORPORATE OVERHEAD

We believe the Denny’s board and management have not effectively controlled operating costs such as the Company’s general and administrative expenses. Management has refranchised or closed approximately 333 locations since 2002. Based on our research of the industry, we would expect substantial general and administrative expense savings to be associated with these refranchised or closed restaurants. However, the Company’s general and administrative expenses have actually increased by approximately $7.3 million since 2002. We believe this is attributable to a culture of wasteful spending at corporate headquarters. We believe shareholder value cannot be maximi zed unless general and administrative expenses are significantly reduced and aligned with Denny’s smaller base of company-owned restaurants. Our goal would be to reduce annual operating expenses by at least $15 million.

Denny’s G&A Expense Growth Versus Restaurant Unit Declines

($ in millions except store data) | 2002 | 2009 | % change |

| G&A Expense | $50.0 | $57.3 | 14.6% | |||

| Number of Company Owned stores | 566 | 233 | (58.8%) | |||

| Number of Franchise stores | 1,110 | 1,318 | 18.7% | |||

Total stores | 1,676 | 1,551 | (7.5%) |

Note: Store data as of 12/31/2002 and 12/31/2009

Source: SEC filings

Unfortunately, some of these excess general and administrative expenses are attributable to generous payments to the Denny’s board and management through cash compensation and stock option packages, despite poor stock and operating performance. The Company’s compensation packages have attracted strong criticism in the past. In a 2006 article, the New York Times highlighted Denny’s unusual practice of granting in-the-money stock options:

“… Denny’s shareholders would be hard pressed to discover that added part of their chief executive’s pay. Instead of writing Mr. Marchioli a check, Denny’s board handed him about 333,000 stock options that came with a built-in paper gain. The amount was not mentioned in Denny’s compensation committee report. It was not counted in the company’s summary compensation chart. Only by carefully studying a table, deep in the proxy statement from the year before, would an ordinary investor realize that Denny’s awarded those options last December with a “buy” price of $2.42 when Denny’s shares were selling for $3.91, a 38 percent discount.”

The full article can be found at:

http://www.nytimes.com/2006/04/29/business/29options.html?_r=1&pagewanted=all

ILL-CONCEIVED MARKETING STRATEGY

Denny’s purchase of three Super Bowl ads this year is one of the recent examples of management’s inability to execute an effective marketing strategy. We note that management ran one Super Bowl ad at great expense in 2009. While the ad produced a short-term increase in sales and traffic, we believe many of the customers attracted by the ad failed to return as traffic losses accelerated in the second half of 2009. This year, by purchasing three Super Bowl ads, the board and management have irresponsibly tripled down on an ineffective promotion. Our discussions with several IHOP franchisees confirm that they experienced a significant increase in traffic during the Denny’s promotion as many of Denny’s core customers were turned off by long wait times. In essence, the Super Bowl promotion encouraged many of Denny’s core customers to try out IHOP, while Denny’s gave away free food to customers who are unlikely to return! We believe Denny’s needs to refocus its marketing efforts on a consistent value message throughout the year, not on marketing gimmicks that send the wrong message and attract the wrong customer base. In summary, we agree with the assessment of a Fortune 500 CEO who labeled Super Bowl advertisements as the “last bastion of unaccountable spending in corporate America.”

We are deeply concerned that Denny’s management lacks the attention to detail and judgment necessary to create an effective marketing strategy. In the past few months alone, Denny’s management oversaw two marketing blunders which caught the media’s attention. We believe these incidents speak volumes about management’s lack of judgment and oversight in deploying its marketing strategy. We encourage you to read the selected articles and excerpts at the website addresses below.

http://www.suntimes.com/business/2082931,CST-NWS-dennys04.article

http://www.facebook.com/pages/Dennys-Boycott-The-Irish-Demand-Respect/338126671783

“The spot, promoting an all-you-can-eat french fries and pancakes offer, drew plenty of complaints and threats of protests by Irish Americans, saying it made light of the 19th century famine that left more than a million people dead.”

http://mashable.com/2010/02/22/dennys-twitter/

“Denny’s dine-in menu invites customers to “Join the conversation!” and follow @Dennys on Twitter. The problem is that the account in question belongs to a Taiwanese Twitterer — Dennys Hsieh — and not the American restaurant chain, which manages two official accounts: DennysAllNightr and DennysGrandSlam.”

“The inaccurate menus … have been in circulation since October 2009 at more than 1,500 locations nationwide.”

POOR CAPITAL ALLOCATION

One of the main responsibilities of the board of directors is to ensure that capital is allocated productively. We believe Denny’s historical capital allocation record has been dismal. Since 2001, the Denny’s board approved approximately $307.6 million of capital expenditures. Given Denny’s poor comparable store guest traffic, shareholders have little to show for these investments. Since 2001, when Mr. Marchioli was appointed CEO and Director, shareholders have suffered negative cumulative free cash flow of $32.3 million.

Historical Cumulative Free Cash Flow

Cumulative | ||||||||||

($ in millions) | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | Since 2001 |

| Cash from operations | $8.2 | $8.8 | $26.6 | $30.1 | $57.3 | $40.2 | $50.3 | $20.5 | $33.3 | $275.3 |

| Capital expenditures | (41.1) | (41.7) | (32.0) | (36.1) | (47.2) | (32.3) | (30.9) | (27.9) | (18.4) | (307.6) |

| Free cash flow | ($32.9) | ($32.9) | ($5.4) | ($6.0) | $10.1 | $7.9 | $19.4 | ($7.4) | $14.9 | ($32.3) |

Source: SEC filings

Denny’s management often boasts of the reduction in debt over the past few years. Unfortunately for shareholders, debt reduction is not tantamount to shareholder value creation. This is particularly true when, in our opinion, management achieved the debt reduction by selling restaurants far too cheaply with respect to the restaurants’ cash flows. In addition, the board and management failed to implement, before selling, simple operational changes that would have significantly increased cash flow. In these cases, the benefits of turning around the restaurant operations were passed along to the franchisees that purchased the restaurants. Unfortunately, in these transactions, the franchisees’ gains come at the expense of shareholders. We urge the board and management to halt all company-restaurant sales until after the upcoming Annual Meeting. We believe prudent capital allocation decisions must be made on a go forward basis in order to maximize shareholder value.

LACK OF ACCOUNTABILITY AND LACK OF OWNERSHIP

We are concerned that many of Denny’s largest franchisees have lost faith in management’s ability to turn around the Company’s operating trends. The Denny’s Franchisee Association (“DFA”) has clearly expressed its disappointment with the current management to the Denny’s board. In a March 30, 2009 letter from the DFA to the Company, the DFA states that:

“The DFA Board hereby expresses our unanimous lack of confidence in the leadership of the Company and their leadership of our Brand ... While there are many approaches that can be deployed to create value within our Brand, it is clear that the strategic and tactical implementation by current Company leadership has not created sustainable, if any, value for the Brand, the franchise owners or Company stakeholders.”

Notwithstanding this strong criticism, the Denny’s board has continued to support management, despite management’s failure to create shareholder value or meaningfully improve operating trends. Shareholders must hold the board accountable for their unwavering support of this management team.

We are also concerned that the Denny’s board lacks a significant actual ownership interest in the Company and therefore lacks a meaningful economic interest in holding management accountable. The independent directors of the board (all directors other than Mr. Marchioli) own outright2 an aggregate of just 162,506 shares or 0.16% of the outstanding shares as of March 23, 2010. We believe this lack of significant actual ownership by members of the board may contribute to the board’s lack of commitment to maximizing shareholder value. In contrast, our Committee’s ownership stake of 6,245,476 shares or approximately 6.3% of the outstanding share s places us as one of Denny’s largest shareholders, closely aligning our interests with other shareholders.

WE BRING AN OWNERSHIP MENTALITY TO THE BOARD

We have nominated three highly qualified director nominees: Patrick Arbor, Jonathan Dash and David Makula. Each will bring a fresh perspective to the Denny’s board and a keen understanding of the strategic and financial miscues that have caused such a dramatic erosion of shareholder and brand value under the current management team. Mr. Arbor’s extensive experience having served as Chairman of the Chicago Board of Trade and as a director of a wide-range of other public and private companies has given him a strong understanding of corporate responsibility and corporate governance. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize the marketing, supply chain and research and development departments of The Steak n Shake Company.&# 160; Mr. Makula brings significant capital markets experience and he will work to address the Company’s capital allocation and other financial issues.

2 | Shares owned directly by the directors as opposed to shares issuable to the directors at a future date upon the exercise of stock options or through the conversion of deferred stock units, subject to vesting and other restrictions under the Company’s compensation plans. |

| · | Patrick H. Arbor is a director of Macquarie Futures USA Inc., a Futures Commission Merchant and clearing member of the Chicago Mercantile Exchange and other exchanges. Mr. Arbor is a long-time member of the Chicago Board of Trade, the world’s oldest derivatives exchange, and served as its Chairman from 1993 to 1999. During that period, Mr. Arbor also served on the board of directors of the National Futures Association. Prior to that, he served as Vice Chairman of the Chicago Board of Trade for three years and as a director of the Chicago Board of Trade for ten years. Mr. Arbor’s extensive experience serving on the board of directors of the Chicago Board of Trade and a wide-range of other public and private companies has given him a strong un derstanding of corporate responsibility and corporate governance. |

| · | Jonathan Dash is the President of Dash Acquisitions, an investment management firm. He served from 2006 to March 2010 as a director of Western Sizzlin Corporation, a restaurant chain with 102 restaurants. He served until recently as a consultant to The Steak n Shake Company, a publicly-traded restaurant chain with 485 restaurants. Mr. Dash, working under the Chairman and CEO, helped to revitalize the Steak n Shake brand and reverse a long history of negative sales comparisons and traffic declines that culminated in double digit positive same store sales comparisons and double digit guest traffic increases for the prior two fiscal quarters. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize t he marketing, supply chain and research and development departments of Steak n Shake. |

| · | David Makula is the Founder and Managing Member of Oak Street Management, an investment management firm. He was previously a Research Analyst with Coghill Capital Management, LLC, an investment management firm. He also served as an Investment Banker for Salomon Smith Barney, where he focused on mergers and acquisitions across a variety of sectors. Mr. Makula holds a CPA certificate from the State of Illinois. He brings significant capital markets experience and he will work to address the Company’s capital allocation and other financial issues. |

We believe that Denny’s is an iconic all-American brand that can be revitalized with the help of our highly qualified director nominees. If elected, our nominees will seek to work with the other board members to address the concerns outlined above.

GOALS OF OUR DIRECTOR NOMINEES

It is easy to criticize without offering a solution. Fortunately, our director nominees have a plan designed to reverse the erosion of shareholder value overseen by the current board. Our changes are intended to significantly improve Denny’s free cash flow per share, thus forming the basis for the market to revalue Denny’s share price. Our sole mission will be to increase Denny’s intrinsic value per share. A broad outline of our goals is as follows:

| · | Create a pay-for-performance culture that clearly and measurably aligns management’s interests with those of shareholders |

| · | Implement a cost structure that provides the Company with a source of competitive advantage, by sustainably reducing annual operating expenses by at least $15 million |

| · | Stop the declining trend in guest traffic and comp store sales with more effective marketing and an improved price-to-value relationship for the customer |

| · | Rationalize capital expenditures to an average of less than $10 million per year |

| · | Halt value-eroding sales of company-owned restaurant units at unreasonably low prices |

| · | Refocus marketing efforts on a consistent value message |

| · | Restore system-wide unit growth through franchisee development, while improving the Company’s relationship with its franchisees |

HELP US RETURN DENNY’S TO ITS RIGHTFUL PLACE

We ask for your support and urge you to vote for our director nominees so that we can work on your behalf to implement a plan to enhance shareholder value and return Denny’s to its rightful place as a leader in the family dining restaurant industry.

VOTE THE GOLD PROXY CARD TODAY

Your vote is important, no matter how many or how few shares you own. If you have any questions or need any assistance voting your shares, please do not hesitate to contact our proxy solicitor, MacKenzie Partners, Inc., by toll-free telephone at 800-322-2885 or by e-mail at enhancedennys@mackenziepartners.com.

For additional information and updates on our solicitation, please visit our website at www.enhancedennys.com. Thank you for your support.

Sincerely,

The Committee to Enhance Denny’s

| Jonathan Dash | David Makula | Patrick Walsh |

| Co-Chairman | Co-Chairman | Co-Chairman |

For additional information and updates leading up to the Annual Meeting, please visit our website at www.enhancedennys.com or if you have any questions, need assistance voting your GOLD proxy card or need additional copies of the Committee’s proxy materials, please contact MacKenzie Partners, Inc. at the address, email or phone numbers listed below. 105 Madison Avenue New York, New York 10016 enhancedennys@mackenziepartners.com Call Collect: (212) 929-5500 or Toll-Free (800) 322-2885 |

Committee Chairmen

Patrick Walsh is a Partner of Oak Street Capital Management, LLC, an investment management firm. Previously, he was a vice president in the investment banking division at Deutsche Bank in New York, NY where he focused on mergers and acquisitions, recapitalizations, joint ventures, and equity and debt offerings. He also served as an equity research analyst focused on the Lodging and REIT sectors at Prudential Securities. Mr. Walsh earned the Chartered Financial Analyst designation in 2001. He holds a B.S. in Accountancy from the Boston College Carroll School of Management and has studied at Columbia Business School’s Value Investing Program. Jonathan Dash is the President of Dash Acquisitions LLC, an investment management firm. He served until recently as a director of Western Sizzlin Corporation, a restaurant chain with 102 restaurants. He served until recently as a consultant to the Steak n Shake Company (NYSE: SNS), a publicly-traded restaurant chain with 485 restaurants. Mr. Dash, working under the Chairman and CEO, helped to revitalize the Steak n Shake brand and reverse a long history of negative sales comparisons that culminated in double digit positive same store sales comparisons for the prior two fiscal quarters. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize the marketing, s upply chain and research and development departments of Steak n Shake. David Makula is the Founder and Managing Member of Oak Street Capital Management, LLC, an investment management firm. He was previously a Research Analyst with Coghill Capital Management, LLC, an investment management firm. He also served as an Investment Banker for Salomon Smith Barney, where he focused on mergers and acquisitions across a variety of sectors. Mr. Makula holds a CPA certificate from the State of Illinois. He brings significant capital markets experience and he will work to address Denny’s capital allocation and other financial issues. | | ||

| |||

Our Nominees

Patrick H. Arbor is a director of Macquarie Futures USA Inc., a Futures Commission Merchant and clearing member of the Chicago Mercantile Exchange and other exchanges. Mr. Arbor is a long-time member of the Chicago Board of Trade, the world’s oldest derivatives exchange, and served as its Chairman from 1993 to 1999. During that period, Mr. Arbor also served on the Board of Directors of the National Futures Association. Prior to that, he served as Vice Chairman of the Chicago Board of Trade for three years and as a director of the Chicago Board of Trade for ten years. Mr. Arbor’s extensive experience serving on the Board of Directors of the Chicago Board of Trade and a wide-range of other public and private compan ies has given him a strong understanding of corporate responsibility and corporate governance. Jonathan Dash is the President of Dash Acquisitions LLC, an investment management firm. He served until recently as a director of Western Sizzlin Corporation, a restaurant chain with 102 restaurants. He served until recently as a consultant to the Steak n Shake Company (NYSE: SNS), a publicly-traded restaurant chain with 485 restaurants. Mr. Dash, working under the Chairman and CEO, helped to revitalize the Steak n Shake brand and reverse a long history of negative sales comparisons that culminated in double digit positive same store sales comparisons for the prior two fiscal quarters. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize the marketing, supply chain and research and development departments of Steak n Shake. David Makula is the Founder and Managing Member of Oak Street Capital Management, LLC, an investment management firm. He was previously a Research Analyst with Coghill Capital Management, LLC, an investment management firm. He also served as an Investment Banker for Salomon Smith Barney, where he focused on mergers and acquisitions across a variety of sectors. Mr. Makula holds a CPA certificate from the State of Illinois. He brings significant capital markets experience and he will work to address Denny’s capital allocation and other financial issues.

| | ||

| |||

Press Releases o Record Date Press Release Dated March 9, 2010 [PDF] o Preliminary Proxy Press Release Dated March 16, 2010 [PDF]

o Shareholder Letter Press Release Dated April 13, 2010 [PDF] | | ||

| |||

FOR RELEASE 8:00 A.M. ET TUESDAY MARCH 9, 2010

Contact:

MacKenzie Partners, Inc.

Mark Harnett &

Bob Marese

212-929-5500

The Committee to Enhance Denny’s Alerts Denny’s Corporation Stockholders to March 23, 2010 Record Date For Denny’s 2010 Annual Meeting of Stockholders

Chicago, Illinois, March 9, 2010 - The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions LLC, noted today that Denny’s Corporation (NASDAQ: DENN) has set a record date of March 23, 2010 and a meeting date of May 19, 2010 for its upcoming 2010 Annual Meeting of Stockholders, according to its notice issued to Broadridge Financial Services, Inc.

The Committee, whose members own an aggregate of approximately 6.5% of Denny’s outstanding common stock, has notified the Company of its intention to nominate three highly qualified independent candidates – Patrick H. Arbor, Jonathan Dash and David Makula – for election to the Denny’s board at the upcoming Annual Meeting. The Committee anticipates filing its preliminary proxy statement with the Securities and Exchange Commission in the near future.

Patrick Walsh, Co-Chairman of the Committee, commented: “The Committee urges Denny’s stockholders to take the necessary steps with their custodial banks and brokerage firms to ensure they have the ability to vote at Denny’s upcoming Annual Meeting. Shares held in margin accounts may be loaned out by brokers and any shares that are subject to a stock loan cannot be voted by the beneficial owner at the upcoming Annual Meeting if they are loaned out as of the March 23 record date. In order to ensure that Denny’s stockholders have the ability to vote their shares, they should move their shares into a cash account in advance of the March 23 record date.”

Investors who are interested in adding to their ownership of Denny’s shares and having the ability to vote these shares at the upcoming Annual Meeting should complete any purchases by March 18, 2010 in order to allow for trade settlement by the record date.

# # #

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

The Committee to Enhance Denny’s (the “Committee”), together with the other Participants (as defined below), intends to make a preliminary filing with the Securities and Exchange Commission (“SEC”) of a proxy statement and accompanying proxy card to be used to solicit proxies for the election of its slate of director nominees at the 2010 annual meeting of stockholders of Denny’s Corporation (the “Company”).

THE COMMITTEE STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT WHEN IT IS AVAILABLE BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY STATEMENT WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THE SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR, MACKENZIE PARTNERS, INC., TOLL-FREE AT (800) 322-2885 OR COLLECT AT (212) 929-5500 OR VIA EMAIL AT ENHANCEDENNYS@MACKENZIEPARTNERS.COM.

The Participants in the proxy solicitation are anticipated to be Oak Street Capital Master Fund, Ltd. (“Oak Street Master”), Oak Street Capital Management, LLC (“Oak Street Management”), David Makula, Patrick Walsh, Dash Acquisitions LLC (“Dash Acquisitions”), Jonathan Dash, Soundpost Capital, LP (“Soundpost Onshore”), Soundpost Capital Offshore, Ltd. (“Soundpost Offshore”), Soundpost Advisors, LLC, Soundpost Partners, LP (“Soundpost Partners”), Soundpost Investments, LLC, Jaime Lester, Lyrical Opportunity Partners II, L.P. (“Lyrical Onshore”), Lyrical Opportunity Partners II, Ltd. (“Lyrical Offshore”), Lyrical Opportunity Partners II GP, L.P., Lyrical Corp III, LLC, Lyrical Partners, L.P., Lyrical Corp I, LLC, Jeffrey Keswin and Patrick H. Arbor (collectively, the “Participants”).

Information regarding the Participants, including their direct or indirect interests in the Company, by security holdings or otherwise, is contained in the Schedule 13D initially filed by Oak Street Master with the SEC on January 21, 2010, as amended or may be amended from time to time (the “Schedule 13D”). The Schedule 13D is currently available at no charge on the SEC’s website at http://www.sec.gov. As of the date hereof, the Participants collectively own an aggregate of 6,245,476 shares of Common Stock of the Company, consisting of the following: (1) 1,826,333 shares owned directly by Oak Street Master, (2) 101,743 shares held in accounts managed by Oak Street Management, (3) 43,000 shares owned directly by Patrick Walsh, (4) 1,202,300 shares held in accounts managed by Dash Acquisitions, (5) 1,407,587 shares owne d directly by Soundpost Onshore, (6) 551,882 shares owned directly by Soundpost Offshore, (7) 340,531 shares held in accounts managed by Soundpost Partners, (8) 338,500 shares owned directly by Lyrical Onshore, (9) 368,600 shares owned directly by Lyrical Offshore and (10) 65,000 shares owned directly by Patrick H. Arbor.

FOR IMMEDIATE RELEASE

Contact:

MacKenzie Partners, Inc.

Mark Harnett &

Bob Marese

212-929-5500

THE COMMITTEE TO ENHANCE DENNY’S FILES PRELIMINARY PROXY STATEMENT IN CONNECTION WITH ITS NOMINATION OF THREE HIGHLY QUALIFIED NOMINEES FOR ELECTION TO DENNY’S BOARD

Chicago, Illinois, March 16, 2010 - The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions, LLC, announced today it has filed its preliminary proxy statement with the SEC in connection with the nomination of its three independent director nominees for election to the Board of Directors of Denny’s Corporation (NASDAQ: DENN) at its 2010 annual meeting of stockholders. The members of the Committee collectively own approximately 6.5% of Denny’s outstanding shares.

The Committee’s three director nominees are Patrick H. Arbor, Jonathan Dash and David Makula. The preliminary proxy statement discusses, among other things, the Committee’s concerns with the financial, operational and share price performance of Denny’s and the action plan the Committee’s nominees would seek to implement if they are elected at the annual meeting.

The Committee reminds investors and fellow stockholders that the record date for the annual meeting is March 23, 2010. Accordingly, the Committee urges Denny’s stockholders to take the necessary steps with their custodial banks and brokerage firms to ensure they have the ability to vote at the annual meeting. Investors who are interested in purchasing Denny’s shares and voting such shares at the annual meeting should complete any purchases by March 18 in order to allow for trade settlement by the record date.

# # #

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

The Committee to Enhance Denny’s (the “Committee”), together with the other Participants (as defined below), has made a preliminary filing with the Securities and Exchange Commission (“SEC”) of a proxy statement and accompanying proxy card to be used to solicit proxies for the election of its slate of director nominees at the 2010 annual meeting of stockholders of Denny’s Corporation (the “Company”).

THE COMMITTEE STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AS IT BECOMES AVAILABLE BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY STATEMENT IS AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THE SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR, MACKENZIE PARTNERS, INC., TOLL-FREE AT (800) 322-2885 OR COLLECT AT (212) 929-5500 OR VIA EMAIL AT ENHANCEDENNYS@MACKENZIEPARTNERS.COM.

The Participants in the proxy solicitation are anticipated to be Oak Street Capital Master Fund, Ltd. (“Oak Street Master”), Oak Street Capital Management, LLC (“Oak Street Management”), David Makula, Patrick Walsh, Dash Acquisitions LLC (“Dash Acquisitions”), Jonathan Dash, Soundpost Capital, LP (“Soundpost Onshore”), Soundpost Capital Offshore, Ltd. (“Soundpost Offshore”), Soundpost Advisors, LLC, Soundpost Partners, LP (“Soundpost Partners”), Soundpost Investments, LLC, Jaime Lester, Lyrical Opportunity Partners II, L.P. (“Lyrical Onshore”), Lyrical Opportunity Partners II, Ltd. (“Lyrical Offshore”), Lyrical Opportunity Partners II GP, L.P., Lyrical Corp III, LLC, Lyrical Partners, L.P., Lyrical Corp I, LLC, Jeffrey Keswin and Patrick H. Arbor (collectively, the “Participants”).

Information regarding the Participants, including their direct or indirect interests in the Company, by security holdings or otherwise, is contained in the Schedule 13D initially filed by Oak Street Master with the SEC on January 21, 2010, as amended or may be amended from time to time (the “Schedule 13D”). The Schedule 13D is currently available at no charge on the SEC’s website at http://www.sec.gov. As of the date hereof, the Participants collectively own an aggregate of 6,245,476 shares of Common Stock of the Company, consisting of the following: (1) 1,826,333 shares owned directly by Oak Street Master, (2) 101,743 shares held in accounts managed by Oak Street Management, (3) 43,000 shares owned directly by Patrick Walsh, (4) 1,202,300 shares held in accounts managed by Dash Acquisitions, (5) 1,407,587 shares owne d directly by Soundpost Onshore, (6) 551,882 shares owned directly by Soundpost Offshore, (7) 340,531 shares held in accounts managed by Soundpost Partners, (8) 338,500 shares owned directly by Lyrical Onshore, (9) 368,600 shares owned directly by Lyrical Offshore and (10) 65,000 shares owned directly by Patrick H. Arbor.

NEWS RELEASE

FOR RELEASE AT 8:00 A.M., NYC TIME, APRIL 13, 2010

Contact:

MacKenzie Partners, Inc.

Mark Harnett &

Bob Marese

212-929-5500

The Committee to Enhance Denny’s Issues Letter to Shareholders – Urges Vote On Gold Proxy Card FOR Election of its Three Highly Qualified Director Nominees

Chicago, Illinois, April 13, 2010 - - The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions LLC, issued the following letter to shareholders of Denny’s Corporation (NASDAQ: DENN) relating to the May 19, 2010 Annual Meeting:

A MESSAGE FROM

THE COMMITTEE TO ENHANCE DENNY’S

VOTE YOUR GOLD PROXY CARD TODAY TO ELECT THE COMMITTEE’S THREE HIGHLY QUALIFIED DIRECTOR NOMINEES

April 13, 2010

Dear Denny’s Shareholder:

The Committee to Enhance Denny’s, headed by Oak Street Capital Management, LLC and Dash Acquisitions LLC, owns approximately 6.3% of the outstanding shares of Denny’s. We are seeking your support to elect our three highly qualified, independent director nominees to the Denny’s board of directors at the Annual Meeting of Shareholders to be held on May 19, 2010. We are writing to share our concerns regarding Denny’s and to outline our nominees’ plans to create value for all shareholders.

Our proposed director nominees are Patrick Arbor, Jonathan Dash and David Makula – their bios can be found toward the end of this letter. They bring significant skills, experience, objectivity and judgment to the board and are committed to implementing a set of initiatives designed to increase long-term shareholder value. We are soliciting proxies to elect not only our three director nominees, but also the candidates who have been nominated by the Company other than Nelson J. Marchioli, Robert E. Marks and Debra Smithart-Oglesby. We believe it is critical to remove these long-tenured directors who we believe are most responsible for the current state of the Company. After reading this letter, you will have the information necessary to make an informed decision at the upcoming Annual Meeting and we are hopeful that you will understand why it is absolutely essential to elect our director nominees. We are counting on your support as each and every vote will matter as we seek to maximize value for all Denny’s shareholders.

INCUMBENT BOARD HAS PRESIDED OVER THE DESTRUCTION OF SUBSTANTIAL SHAREHOLDER VALUE

We believe Denny’s current board and management team have implemented and must take responsibility for a strategic and capital allocation plan that has destroyed significant shareholder value. The Denny’s board and management team have been given a sufficiently long period of time to implement their plans and create value for shareholders, and they have failed. As long-term shareholders are aware, Denny’s share price has declined by 76.9% between the Company’s emergence from bankruptcy in January 1998 and December 31, 2009, not accounting for the time value of money. Over the past five completed fiscal years alone, Denny’s share price has plummeted by 51.3%, an unacceptable outcome. While we acknowledge the market volatility associated with last year’s global economic decline, we believe Denny’s historically poor share price performance demonstrates the board’s and management’s inability to maximize shareholder value. If shareholders continue to accept the status quo, we are concerned that Denny’s future will look very much like its past. These abysmal results cannot be allowed to continue.

Price Performance Comparison

DENNY’S SHARE PRICE HAS INCREASED SIGNIFICANTLY SINCE WE FILED OUR INITIAL SCHEDULE 13D

Since disclosing our Denny’s position in our initial Schedule 13D filed on January 21, 2010, the share price has appreciated by approximately 70%1. This share price performance has been achieved in a period during which the Company reported continued deterioration in key operating metrics such as comparable store guest traffic. We believe the recent share price performance is reflective of a market view that change is needed at Denny’s. Nevertheless, we believe the current market value fails to reflect Denny’s full potential, a potential that can be realized with changes to the board of directors.

Our shareholder group is financially and constitutionally committed to improving the future direction of Denny’s. We have no interest in lingering on the sidelines while the board and management team attempt to figure out an effective strategic plan. Management’s track record spans both good and bad economic times, and the operating results of Denny’s closest competitors only serve to highlight management’s shortcomings.

Our concerns with the current Denny’s board and management can be summarized as follows:

| · | Failure to grow system-wide restaurants |

| · | Ceding the #1 market position to International House of Pancakes (“IHOP”) |

| · | Unacceptable declines in key operating trends such as guest traffic |

| · | Inappropriately high general and administrative expenses |

| · | Expensive and ineffective marketing strategies |

| · | Imprudent capital allocation decisions |

| · | Lack of accountability for management at the board level |

| · | Marginalization of shareholders and franchisees, and |

| · | Extremely poor share price performance |

| 1 | Based on closing price of $2.30 per share on January 21, 2010 and closing price of $3.89 per share on April 9, 2010. |

FAILURE TO GROW THE SYSTEM HAS

WEAKENED DENNY’S COMPETITIVE POSITION

We believe the perennial decline in the number of system-wide restaurants has undermined Denny’s ability to stay competitive and has negatively impacted profitability. According to Denny’s public filings, the Company’s system-wide units peaked ten years ago, at 1,822 restaurants, shortly before Nelson Marchioli was appointed CEO in 2001. Over the past decade, the board oversaw a 15% decline in total system-wide restaurants to 1,551 units as of December 30, 2009. This stands in stark contrast to the Company’s closest competitor, IHOP, which during a similar time frame increased system-wide restaurants from 922 units to 1,456 units as of December 31, 2009.

Notably, we view IHOP as a similarly situated restaurant concept, with no fundamental competitive advantage other than its current leadership relative to Denny’s. IHOP presents an interesting case study of what can be accomplished in the family dining category when a quality leadership team is in charge. Since 2000, IHOP has more than doubled system-wide sales from $1.2B to over $2.5B for 2009, based on public filings. During this same time frame, Denny’s system-wide sales, on the other hand, have stagnated. The chart below contrasts system-wide sales performance for these closely related concepts since 2000.

System-Wide Sales Comparison

Source: SEC filings

GUEST CHECK INCREASES HAVE LED TO

UNACCEPTABLE GUEST TRAFFIC DECLINES

We believe management failed to improve key restaurant operating trends such as same store guest traffic – despite shrinking units by 15% since 2000. Since Mr. Marchioli assumed his role as CEO, we believe Denny’s same store guest traffic has been among the worst of its peers. In fact, Denny’s customer traffic has declined in seven of the last eight years.

Despite these persistent guest traffic declines, management responded by consistently raising prices year after year. We are deeply concerned that Denny’s pricing strategy only served to accelerate guest traffic declines, particularly during 2008 when management hiked prices in the face of lower commodity costs and an ailing U.S. consumer. The chart below illustrates the loss of customers under current management.

Denny’s Cumulative Decline in Guest Traffic

Source: SEC filings

Incidentally, the Denny’s board and management team have themselves acknowledged the importance of increasing guest counts based on their 2005 Annual Report which states:

“Our future success will be driven by increasing guest counts and capitalizing on the significant capacity for sales growth within our restaurants.”

Unfortunately, five years later, shareholders are still waiting for them to increase guest counts and fill excess restaurant capacity. If these guest traffic declines are allowed to persist, we strongly believe that the effect on shareholders and the franchisee base will be dire. We must act now.

EXCESS CORPORATE OVERHEAD

We believe the Denny’s board and management have not effectively controlled operating costs such as the Company’s general and administrative expenses. Management has refranchised or closed approximately 333 locations since 2002. Based on our research of the industry, we would expect substantial general and administrative expense savings to be associated with these refranchised or closed restaurants. However, the Company’s general and administrative expenses have actually increased by approximately $7.3 million since 2002. We believe this is attributable to a culture of wasteful spending at corporate headquarters. We believe shareholder value cannot be maximi zed unless general and administrative expenses are significantly reduced and aligned with Denny’s smaller base of company-owned restaurants. Our goal would be to reduce annual operating expenses by at least $15 million.

Denny’s G&A Expense Growth Versus Restaurant Unit Declines

($ in millions except store data) | 2002 | 2009 | % change |

| G&A Expense | $50.0 | $57.3 | 14.6% | |||

| Number of Company Owned stores | 566 | 233 | (58.8%) | |||

| Number of Franchise stores | 1,110 | 1,318 | 18.7% | |||

Total stores | 1,676 | 1,551 | (7.5%) |

Note: Store data as of 12/31/2002 and 12/31/2009

Source: SEC filings

Unfortunately, some of these excess general and administrative expenses are attributable to generous payments to the Denny’s board and management through cash compensation and stock option packages, despite poor stock and operating performance. The Company’s compensation packages have attracted strong criticism in the past. In a 2006 article, the New York Times highlighted Denny’s unusual practice of granting in-the-money stock options:

“… Denny’s shareholders would be hard pressed to discover that added part of their chief executive’s pay. Instead of writing Mr. Marchioli a check, Denny’s board handed him about 333,000 stock options that came with a built-in paper gain. The amount was not mentioned in Denny’s compensation committee report. It was not counted in the company’s summary compensation chart. Only by carefully studying a table, deep in the proxy statement from the year before, would an ordinary investor realize that Denny’s awarded those options last December with a “buy” price of $2.42 when Denny’s shares were selling for $3.91, a 38 percent discount.”

The full article can be found at:

http://www.nytimes.com/2006/04/29/business/29options.html?_r=1&pagewanted=all

ILL-CONCEIVED MARKETING STRATEGY

Denny’s purchase of three Super Bowl ads this year is one of the recent examples of management’s inability to execute an effective marketing strategy. We note that management ran one Super Bowl ad at great expense in 2009. While the ad produced a short-term increase in sales and traffic, we believe many of the customers attracted by the ad failed to return as traffic losses accelerated in the second half of 2009. This year, by purchasing three Super Bowl ads, the board and management have irresponsibly tripled down on an ineffective promotion. Our discussions with several IHOP franchisees confirm that they experienced a significant increase in traffic during the Denny’s promotion as many of Denny’s core customers were turned off by long wait times. In essence, the Super Bowl promotion encouraged many of Denny’s core customers to try out IHOP, while Denny’s gave away free food to customers who are unlikely to return! We believe Denny’s needs to refocus its marketing efforts on a consistent value message throughout the year, not on marketing gimmicks that send the wrong message and attract the wrong customer base. In summary, we agree with the assessment of a Fortune 500 CEO who labeled Super Bowl advertisements as the “last bastion of unaccountable spending in corporate America.”

We are deeply concerned that Denny’s management lacks the attention to detail and judgment necessary to create an effective marketing strategy. In the past few months alone, Denny’s management oversaw two marketing blunders which caught the media’s attention. We believe these incidents speak volumes about management’s lack of judgment and oversight in deploying its marketing strategy. We encourage you to read the selected articles and excerpts at the website addresses below.

http://www.suntimes.com/business/2082931,CST-NWS-dennys04.article

http://www.facebook.com/pages/Dennys-Boycott-The-Irish-Demand-Respect/338126671783

“The spot, promoting an all-you-can-eat french fries and pancakes offer, drew plenty of complaints and threats of protests by Irish Americans, saying it made light of the 19th century famine that left more than a million people dead.”

http://mashable.com/2010/02/22/dennys-twitter/

“Denny’s dine-in menu invites customers to “Join the conversation!” and follow @Dennys on Twitter. The problem is that the account in question belongs to a Taiwanese Twitterer — Dennys Hsieh — and not the American restaurant chain, which manages two official accounts: DennysAllNightr and DennysGrandSlam.”

“The inaccurate menus … have been in circulation since October 2009 at more than 1,500 locations nationwide.”

POOR CAPITAL ALLOCATION

One of the main responsibilities of the board of directors is to ensure that capital is allocated productively. We believe Denny’s historical capital allocation record has been dismal. Since 2001, the Denny’s board approved approximately $307.6 million of capital expenditures. Given Denny’s poor comparable store guest traffic, shareholders have little to show for these investments. Since 2001, when Mr. Marchioli was appointed CEO and Director, shareholders have suffered negative cumulative free cash flow of $32.3 million.

Historical Cumulative Free Cash Flow

Cumulative | ||||||||||

($ in millions) | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | Since 2001 |

| Cash from operations | $8.2 | $8.8 | $26.6 | $30.1 | $57.3 | $40.2 | $50.3 | $20.5 | $33.3 | $275.3 |

| Capital expenditures | (41.1) | (41.7) | (32.0) | (36.1) | (47.2) | (32.3) | (30.9) | (27.9) | (18.4) | (307.6) |

| Free cash flow | ($32.9) | ($32.9) | ($5.4) | ($6.0) | $10.1 | $7.9 | $19.4 | ($7.4) | $14.9 | ($32.3) |

Source: SEC filings

Denny’s management often boasts of the reduction in debt over the past few years. Unfortunately for shareholders, debt reduction is not tantamount to shareholder value creation. This is particularly true when, in our opinion, management achieved the debt reduction by selling restaurants far too cheaply with respect to the restaurants’ cash flows. In addition, the board and management failed to implement, before selling, simple operational changes that would have significantly increased cash flow. In these cases, the benefits of turning around the restaurant operations were passed along to the franchisees that purchased the restaurants. Unfortunately, in these transactions, the franchisees’ gains come at the expense of shareholders. We urge the board and management to halt all company-restaurant sales until after the upcoming Annual Meeting. We believe prudent capital allocation decisions must be made on a go forward basis in order to maximize shareholder value.

LACK OF ACCOUNTABILITY AND LACK OF OWNERSHIP

We are concerned that many of Denny’s largest franchisees have lost faith in management’s ability to turn around the Company’s operating trends. The Denny’s Franchisee Association (“DFA”) has clearly expressed its disappointment with the current management to the Denny’s board. In a March 30, 2009 letter from the DFA to the Company, the DFA states that:

“The DFA Board hereby expresses our unanimous lack of confidence in the leadership of the Company and their leadership of our Brand ... While there are many approaches that can be deployed to create value within our Brand, it is clear that the strategic and tactical implementation by current Company leadership has not created sustainable, if any, value for the Brand, the franchise owners or Company stakeholders.”

Notwithstanding this strong criticism, the Denny’s board has continued to support management, despite management’s failure to create shareholder value or meaningfully improve operating trends. Shareholders must hold the board accountable for their unwavering support of this management team.

We are also concerned that the Denny’s board lacks a significant actual ownership interest in the Company and therefore lacks a meaningful economic interest in holding management accountable. The independent directors of the board (all directors other than Mr. Marchioli) own outright2 an aggregate of just 162,506 shares or 0.16% of the outstanding shares as of March 23, 2010. We believe this lack of significant actual ownership by members of the board may contribute to the board’s lack of commitment to maximizing shareholder value. In contrast, our Committee’s ownership stake of 6,245,476 shares or approximately 6.3% of the outstanding share s places us as one of Denny’s largest shareholders, closely aligning our interests with other shareholders.

WE BRING AN OWNERSHIP MENTALITY TO THE BOARD

We have nominated three highly qualified director nominees: Patrick Arbor, Jonathan Dash and David Makula. Each will bring a fresh perspective to the Denny’s board and a keen understanding of the strategic and financial miscues that have caused such a dramatic erosion of shareholder and brand value under the current management team. Mr. Arbor’s extensive experience having served as Chairman of the Chicago Board of Trade and as a director of a wide-range of other public and private companies has given him a strong understanding of corporate responsibility and corporate governance. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize the marketing, supply chain and research and development departments of The Steak n Shake Company.&# 160; Mr. Makula brings significant capital markets experience and he will work to address the Company’s capital allocation and other financial issues.

2 | Shares owned directly by the directors as opposed to shares issuable to the directors at a future date upon the exercise of stock options or through the conversion of deferred stock units, subject to vesting and other restrictions under the Company’s compensation plans. |

| · | Patrick H. Arbor is a director of Macquarie Futures USA Inc., a Futures Commission Merchant and clearing member of the Chicago Mercantile Exchange and other exchanges. Mr. Arbor is a long-time member of the Chicago Board of Trade, the world’s oldest derivatives exchange, and served as its Chairman from 1993 to 1999. During that period, Mr. Arbor also served on the board of directors of the National Futures Association. Prior to that, he served as Vice Chairman of the Chicago Board of Trade for three years and as a director of the Chicago Board of Trade for ten years. Mr. Arbor’s extensive experience serving on the board of directors of the Chicago Board of Trade and a wide-range of other public and private companies has given him a strong un derstanding of corporate responsibility and corporate governance. |

| · | Jonathan Dash is the President of Dash Acquisitions, an investment management firm. He served from 2006 to March 2010 as a director of Western Sizzlin Corporation, a restaurant chain with 102 restaurants. He served until recently as a consultant to The Steak n Shake Company, a publicly-traded restaurant chain with 485 restaurants. Mr. Dash, working under the Chairman and CEO, helped to revitalize the Steak n Shake brand and reverse a long history of negative sales comparisons and traffic declines that culminated in double digit positive same store sales comparisons and double digit guest traffic increases for the prior two fiscal quarters. Mr. Dash brings valuable experience in the restaurant business due to his significant roles in helping revitalize t he marketing, supply chain and research and development departments of Steak n Shake. |

| · | David Makula is the Founder and Managing Member of Oak Street Management, an investment management firm. He was previously a Research Analyst with Coghill Capital Management, LLC, an investment management firm. He also served as an Investment Banker for Salomon Smith Barney, where he focused on mergers and acquisitions across a variety of sectors. Mr. Makula holds a CPA certificate from the State of Illinois. He brings significant capital markets experience and he will work to address the Company’s capital allocation and other financial issues. |

We believe that Denny’s is an iconic all-American brand that can be revitalized with the help of our highly qualified director nominees. If elected, our nominees will seek to work with the other board members to address the concerns outlined above.

GOALS OF OUR DIRECTOR NOMINEES

It is easy to criticize without offering a solution. Fortunately, our director nominees have a plan designed to reverse the erosion of shareholder value overseen by the current board. Our changes are intended to significantly improve Denny’s free cash flow per share, thus forming the basis for the market to revalue Denny’s share price. Our sole mission will be to increase Denny’s intrinsic value per share. A broad outline of our goals is as follows:

| · | Create a pay-for-performance culture that clearly and measurably aligns management’s interests with those of shareholders |

| · | Implement a cost structure that provides the Company with a source of competitive advantage, by sustainably reducing annual operating expenses by at least $15 million |

| · | Stop the declining trend in guest traffic and comp store sales with more effective marketing and an improved price-to-value relationship for the customer |

| · | Rationalize capital expenditures to an average of less than $10 million per year |

| · | Halt value-eroding sales of company-owned restaurant units at unreasonably low prices |

| · | Refocus marketing efforts on a consistent value message |

| · | Restore system-wide unit growth through franchisee development, while improving the Company’s relationship with its franchisees |

HELP US RETURN DENNY’S TO ITS RIGHTFUL PLACE

We ask for your support and urge you to vote for our director nominees so that we can work on your behalf to implement a plan to enhance shareholder value and return Denny’s to its rightful place as a leader in the family dining restaurant industry.

VOTE THE GOLD PROXY CARD TODAY

Your vote is important, no matter how many or how few shares you own. If you have any questions or need any assistance voting your shares, please do not hesitate to contact our proxy solicitor, MacKenzie Partners, Inc., by toll-free telephone at 800-322-2885 or by e-mail at enhancedennys@mackenziepartners.com.

For additional information and updates on our solicitation, please visit our website at www.enhancedennys.com. Thank you for your support.

Sincerely,

The Committee to Enhance Denny’s

| Jonathan Dash | David Makula | Patrick Walsh |

| Co-Chairman | Co-Chairman | Co-Chairman |

# # #

Documents

o The Committee to Enhance Denny's Proxy Statement [PDF] o The Committee to Enhance Denny's GOLD Proxy Card [PDF] o The Committee to Enhance Denny's Shareholder Letter 4-13-10 [PDF] | | ||

| |||

Enhance Denny's

Terms and Conditions

This website, http://www.enhancedennys.com (the “Site”), sponsored by Oak Street Capital Management, LLC and Dash Acquisitions LLC (the “Sponsor”), is for informational purposes only. You may use the Site for non-commercial, lawful purposes only. Your access to and use of the Site is subject to and governed by these Terms and Conditions. By accessing and browsing the Site, you accept, without limitation or qualification, and agree to be bound by, these Terms and Conditions and all applicable laws.

Nothing on this Site is intended to be, nor should it be construed or used as, investment, tax, legal or financial advice, a recommendation whether or how to vote any proxy or any other kind of recommendation, an opinion of the appropriateness of any security or investment, nor intended to be an offer, or the solicitation of any offer, to buy or sell any security or investment. The Sponsor is not soliciting any action based upon the Site, is not responsible for any decision by any stockholder and the Site should not be construed as a solicitation to procure, withhold or revoke any proxy.

1. You should assume that everything you see or read on the Site is material owned or exclusively represented by the Sponsor and protected by copyright unless otherwise expressly noted, and may not be used except as provided in these Terms and Conditions or in the text of the Site without the Sponsor’s written permission. The Sponsor expressly neither warrants nor represents that your use of materials displayed on the Site will not infringe rights of third parties not owned by or affiliated with the Sponsor.

2. While the Sponsor endeavors to ensure that only accurate and up to date information is on the Site, the Sponsor makes no warranties or representations as to the accuracy of any of the posted information. The Sponsor assumes no liability or responsibility for any errors or omissions in the content of the Site.

3. The Site is provided “AS IS.” The Sponsor does not make any representations or warranties, whether express or implied, regarding or relating to the Site or any associated hardware or software, including the content or operations of either.

4. YOU EXPRESSLY ACKNOWLEDGE THAT USE OF THE SITE IS AT YOUR SOLE RISK. NEITHER THE SPONSOR OR ITS AFFILIATED COMPANIES NOR ANY OF THEIR RESPECTIVE EMPLOYEES, AGENTS, THIRD PARTY CONTENT PROVIDERS OR LICENSORS (COLLECTIVELY THE “SPONSOR PARTIES”) WARRANT THAT THE SITE WILL BE UNINTERRUPTED OR ERROR FREE, NOR DO THEY MAKE ANY WARRANTY AS TO THE RESULTS THAT MAY BE OBTAINED FROM USE OF THE SITE, OR AS TO THE ACCURACY, RELIABILITY OR CONTENT OF ANY INFORMATION, SERVICE, OR MERCHANDISE PROVIDED THROUGH THE SITE. THE SITE IS PROVIDED ON AN “AS IS” BASIS WITHOUT WARRANTIES OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, WARRANTIES OF TITLE OR IMPLIED WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE, OTHER THAN THOSE WARRANTIES WHICH ARE IMPLIED BY A ND INCAPABLE OF EXCLUSION, RESTRICTION OR MODIFICATION UNDER THE LAWS APPLICABLE TO THIS AGREEMENT.

THIS DISCLAIMER OF LIABILITY APPLIES TO ANY DAMAGES OR INJURY CAUSED BY ANY FAILURE OF PERFORMANCE, ERROR, OMISSION, INTERRUPTION, DELETION, DEFECT, DELAY IN OPERATION OR TRANSMISSION, COMPUTER VIRUS, COMMUNICATION LINE FAILURE, THEFT OR DESTRUCTION OR UNAUTHORIZED ACCESS TO, ALTERATION OF, OR USE OF RECORD, WHETHER FOR BREACH OF CONTRACT, TORTIOUS BEHAVIOR, NEGLIGENCE, OR UNDER ANY OTHER CAUSE OF ACTION. YOU SPECIFICALLY ACKNOWLEDGE THAT THE SPONSOR IS NOT LIABLE FOR THE DEFAMATORY, OFFENSIVE OR ILLEGAL CONDUCT OF OTHER USERS OR THIRD-PARTIES AND THAT THE RISK OF INJURY FROM THE FOREGOING RESTS ENTIRELY WITH YOU.

IN NO EVENT WILL THE SPONSOR, THE SPONSOR PARTIES, OR ANY PERSON OR ENTITY INVOLVED IN CREATING, PRODUCING OR DISTRIBUTING THE SITE BE LIABLE FOR ANY INDIRECT, INCIDENTAL, SPECIAL, CONSEQUENTIAL OR PUNITIVE DAMAGES ARISING OUT OF THE USE OF OR INABILITY TO USE THE SITE. YOU HEREBY ACKNOWLEDGE THAT THE PROVISIONS OF THIS SECTION SHALL APPLY TO ALL CONTENT ON THE SITE.

IN ADDITION TO THE TERMS SET FORTH ABOVE, NEITHER THE SPONSOR NOR THE SPONSOR PARTIES SHALL BE LIABLE REGARDLESS OF THE CAUSE OR DURATION, FOR ANY ERRORS, INACCURACIES, OMISSIONS, OR OTHER DEFECTS IN, OR UNTIMELINESS OR UNAUTHENTICITY OF, THE INFORMATION CONTAINED WITHIN THE SITE, OR FOR ANY DELAY OR INTERRUPTION IN THE TRANSMISSION THEREOF TO YOU, OR FOR ANY CLAIMS OR LOSSES ARISING THEREFROM OR OCCASIONED THEREBY. NONE OF THE FOREGOING PARTIES SHALL BE LIABLE FOR ANY THIRD-PARTY CLAIMS OR LOSSES OF ANY NATURE, INCLUDING, BUT NOT LIMITED TO, LOST PROFITS, PUNITIVE OR CONSEQUENTIAL DAMAGES AND THE AGGREGATE, TOTAL LIABILITY OF THE SPONSOR PARTIES TO YOU OR ANY END USER FOR ALL DAMAGES, INJURY, LOSSES AND CAUSES OF ACTION (WHETHER IN CONTRACT, TORT OR OTHERWISE) ARISING FROM OR RELATING TO THIS AGREEMENT OR THE USE OF OR INABILI TY TO USE THE SITE SHALL BE LIMITED TO PROVEN DIRECT DAMAGES IN AN AMOUNT NOT TO EXCEED ONE HUNDRED DOLLARS ($100).

SOME JURISDICTIONS DO NOT ALLOW THE LIMITATION OR EXCLUSION OF CERTAIN LIABILITY OR WARRANTIES, IN WHICH EVENT SOME OF THE ABOVE LIMITATIONS MAY NOT APPLY TO YOU. In such jurisdictions, the Sponsor’s liability is limited to the greatest extent permitted by law. You should check your local laws for any restrictions or limitations regarding the exclusion of implied warranties.

5. Artwork, images, names, and likenesses displayed on the Site are either the property of, or used with permission by, the Sponsor. The reproduction and use of any of these by you is prohibited unless specific permission is provided on the Site or otherwise. Any unauthorized use may violate copyright laws, trademark laws, privacy and publicity laws, and/or communications regulations and statutes.

6. The trademarks, service marks, logos, and other indicia, including of the Sponsor (collectively the “Trademarks”) which appear on the Site are registered and unregistered trademarks of the Sponsor and others. Nothing contained on the Site should be construed as granting, by implication or otherwise, any right, license or title to any of the Trademarks without the advance written permission of the Sponsor or such third party as may be appropriate. All rights are expressly reserved and retained by the Sponsor. Your misuse of any of the Trademarks displayed on the Site, or any other content on the Site, except as provided in these Terms and Conditions, is strictly prohibited. You are also advised that the Sponsor considers its intellectual property to be among i ts most valuable assets, and will aggressively enforce its intellectual property rights to the fullest extent of the law.

7. For your convenience, the Site may contain links to the websites of third parties on which you may be able to obtain content and/or download software. Except as otherwise noted, such websites, and such content and software are provided by companies which are not affiliated with and independent of the Sponsor. The Sponsor does not endorse or make any representations or warranties concerning such websites, and may have not reviewed such content or software. As such, the Sponsor makes no representation as to the accuracy or any other aspect of the information contained in or on such sites, sources or servers, nor does the Sponsor necessarily endorse such sites or sources.

8. If any provision of the Terms and Conditions or any application thereof is held to be invalid or unenforceable for any reason, that provision shall be deemed severable and the remainder of the Terms and Conditions and the application of that provision in other situations shall not be affected.

9. YOU AGREE TO INDEMNIFY, DEFEND AND HOLD HARMLESS THE SPONSOR FROM AND AGAINST ANY AND ALL THIRD PARTY CLAIMS, DEMANDS, LIABILITIES, COSTS OR EXPENSES, INCLUDING REASONABLE ATTORNEYS’ FEES, ARISING FROM OR RELATED TO ANY BREACH BY YOU OF ANY OF THE TERMS AND CONDITIONS OR APPLICABLE LAW, INCLUDING THOSE REGARDING INTELLECTUAL PROPERTY.

10. The Sponsor may at any time revise these Terms and Conditions by updating this posting. You are bound by any such revisions and should therefore periodically visit this page to review the then current Terms and Conditions to which you are bound.

11. The Sponsor knows that the privacy of your personal information is important to you. Therefore, the Sponsor has established a Privacy Policy governing the use of this information, which is located at http://www.enhancedennys.com/Notice.htm.