UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

(Amendment No. )

| Filed by the Registrant [X] | |

| Filed by a Party other than the Registrant [ ] | |

| Check the appropriate box: | |

| [ ] | Preliminary Proxy Statement |

| [ ] | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| [ ] | Definitive Proxy Statement |

| [X] | Definitive Additional Materials |

| [ ] | Soliciting Material under §240.14a-12 |

| ALPINE TOTAL DYNAMIC DIVIDEND FUND | ||

| (Name of Registrant as Specified In Its Charter) | ||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||

| Payment of Filing Fee (Check the appropriate box): | ||

| [X] | No fee required. | |

| [ ] | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

| [ ] | Fee paid previously with preliminary materials. | |

| [ ] | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

- 2 -

On February 28, 2018, representatives of Alpine Total Dynamic Dividend Fund (the “Fund”) provided a presentation to representatives of Institutional Shareholder Services Inc. regarding the Fund. A copy of this presentation is filed herewith asExhibit I.

* * * * *

ADDITIONAL INFORMATION:

The Fund has filed its definitive proxy statement for the Special Meeting of Shareholders, to be held on March 14, 2018, together with itsWHITEproxy card, with the U.S. Securities and Exchange Commission. Shareholders can obtain free additional copies of the notice of the Special Meeting and proxy statement, including theWHITEproxy card, and other documents by calling AST, the Fund’s proxy solicitor, at 1-800-331-7543.

Reasons for the Transaction

| • | The Alpine Total Dynamic Divided fund (the “Fund”) has outperformed its benchmark since we restructured portfolio management in 2012. Over the last 5 years the Fund has paid out $373 million in distributions to shareholders. |

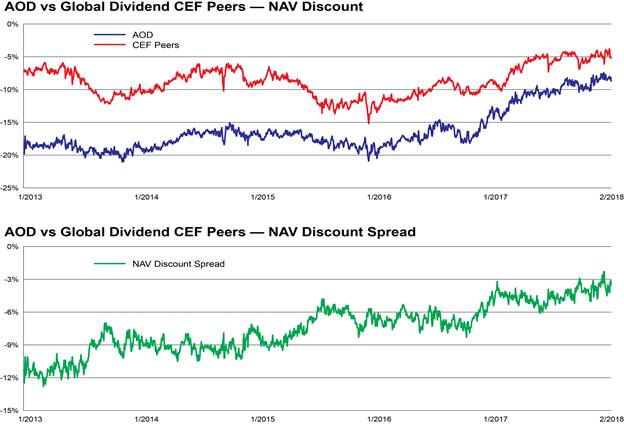

Please see the AOD Discount Data on Slide 7 indicating the improving trends on the Fund’s discount levels

| • | From inception (1/27/2007) the Fund has generated $210 million in fees and expenses. Of this number $35 million were Fund expenses, $35 million in underwriting fees with a net fee of $140 million paid to Adviser. The numbers do not reflect Adviser overhead expenses including personnel and infrastructure costs |

| • | Alpine Transaction — The Board’s Focus: How to Generate Investment Flow |

| • | The Board of Trustees of the Fund unanimously approved the proposed transaction with Alpine, including all of the independent trustees |

| • | Beginning 4 years ago Alpine hired consultants to review OEF and CEF opportunities and growth opportunities in today’s market |

| • | Met with distributors and asset managers on varying models we could implement by either partnering or in strategic transactions |

| • | Management and the Board undertook a thoughtful and expansive process, with management reporting quarterly to the Board on findings and analysis |

| • | Engaged the street and industry experts in dialogue in order to make best decision in the interest of shareholders |

| • | We are not exiting investment management, only the mutual fund space where scale is essential to be competitive |

| • | Hired UBS as financial advisor to assist in strategic solution for firm — multiple firms participated resulting in Aberdeen Standard Investments (‘ASI’) as the best partner |

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 2 |

Why Aberdeen Standard Investments?

| • | Focused on Closed End Funds with 42 CEFs worldwide and $20bn AUM. Of which 14 Closed End Funds and $4.8bn are U.S. listed |

| • | Committed to U.S. CEF market since 2000 |

| • | Dedicated CEF marketing and relationship management personnel |

| • | Reduction in TERs forecast for all 3 CEFs due to economies of scale, this would no longer be the case if a material tender was offered |

| • | CEFs are a key focus even at highest levels of the organization — group CEO Martin Gilbert attends most quarterly U.S. CEF Board meetings in-person. ASI was originally born out of UK CEF |

| • | The current investment policies and strategies of the Fund are not expected to change if ASI is appointed as investment adviser, providing continuity of strategy for the Fund |

| • | ASI brings significant additional global equity income and global REIT investment management resources of benefit to all shareholders with a proven track record of successfully managing U.S. and UK CEF’s mandate and their structure such as Murray International, which has historically traded at a premium to NAV for many years. In addition, it is expected that there will be portfolio management continuity as existing portfolio management resources are integrated with ASI’s expertise |

| • | Shareholder friendly and good governance such as (1) first US CEFs to repay AMPS (2) offer up/down voting on Board members (3) currently consolidating 8 Emerging market funds into 1 with a shareholder tender of between 40–50% (4) committed to never doing a discounted rights offering to NAV |

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 3 |

Why Not Saba? They are Not Aligned with Shareholders

| • | Self-serving agenda with no meaningful proposal for shareholders |

| • | Saba’s arguments are flawed as we believe their information is factually incorrect with respect to fees and performance |

| • | We believe Hedge Funds like Saba are not aligned with shareholders and they are not concerned with stock portfolio growth — increasing the Fund’s net asset value (NAV) — because they are focused solely on shrinking of the discount (or spread) between market price and NAV |

| • | We believe Saba profits primarily when the discount narrows. Whereas most shareholders make money when NAV growth leads to market price moving higher |

| • | This is why Saba’s stated objective of derailing the vote is to force a purchase of shares at NAV, giving them “an opportunity to realize immediate gains,” even though this could hurt long-term shareholders, by impacting expense ratios |

| • | Saba is a short-term investor… the bulk of Saba’s shares were just purchased during 2017, so their view is not long term |

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 4 |

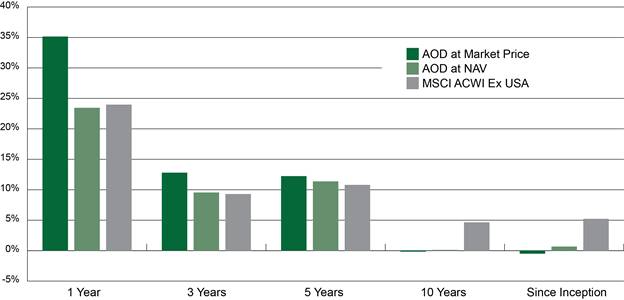

Morningstar Performance Data

| ONE YEAR | THREE YEARS | FIVE YEARS | TEN YEARS | SINCE INCEPTION | |||||||

| 2/1/2017 | 2/1/2015 | 2/1/2013 | 2/1/2008 | 1/26/2007 | |||||||

| 1/31/2018 | 1/31/2018 | 1/31/2018 | 1/31/2018 | 1/31/2018 | |||||||

| Group/Investment | Ticker | Return | Peer group percentile | Return | Peer group percentile | Return | Peer group percentile | Return | Peer group percentile | Return | Peer group percentile |

| AOD Category CY 2017 | |||||||||||

| Peer Group Median | 25.65 | 9.07 | 8.61* | 4.98 | 4.66 | ||||||

| Alpine Global Dynamic Dividend | AGD | 26.74 | 34 | 11.78 | 20 | 11.30 | 20 | 1.46 | 85 | 0.90 | 89 |

| Alpine Total Dynamic Dividend | AOD | 25.91 | 53 | 11.97 | 40 | 11.70* | 27 | 1.70 | 92 | 1.10 | 85 |

| BlackRock Enhanced Glbl Div Trust | BOE | 16.01 | 67 | 7.60 | 73 | 6.91 | 73 | 4.02 | 57 | 4.48 | 56 |

| Calamos Global Total Return | CGO | 28.81 | 20 | 11.57 | 27 | 8.83 | 47 | 6.93 | 15 | 7.33 | 12 |

| Clough Global Equity | GLQ | 33.11 | 7 | 8.40 | 67 | 8.39 | 53 | 5.26 | 29 | 5.24 | 34 |

| Cohen & Steers Glb Inc Builder | INB | 17.29 | 60 | 7.42 | 80 | 7.96 | 67 | 4.98 | 43 | ||

| EV Tax Adv Global Dividend Inc | ETG | 26.73 | 40 | 11.33 | 34 | 11.84 | 7 | 5.07 | 36 | 4.84 | 45 |

| JH Hedged Equity & Income Fund | HEQ | 15.19 | 80 | 9.10 | 47 | 8.27 | 60 | ||||

| JH Tax Advantaged Global Shareholder Yld | HTY | 14.22 | 86 | 5.10 | 93 | 6.01 | 86 | 4.98 | 50 | ||

| Lazard Glb Total Return & Income | LGI | 36.46 | 1 | 13.03 | 7 | 9.37 | 40 | 5.75 | 22 | 5.63 | 23 |

| Lazard World Dividend & Income | LOR | 26.23 | 47 | 5.78 | 86 | 4.43 | 93 | 3.85 | 64 | 3.62 | 67 |

| Nuveen Tax-Adv Div Growth | JTD | 28.43 | 27 | 11.86 | 14 | 11.38 | 14 | 8.53 | 8 | ||

| PIMCO Global StocksPLUS & Income | PGP | 30.29 | 14 | 17.40 | 1 | 13.77 | 1 | 13.89 | 1 | 12.24 | 1 |

| Virtus Total Return Fund Inc. | ZF | 13.90 | 93 | 9.04 | 53 | 10.32 | 34 | 2.24 | 78 | -2.78 | 100 |

| Voya Global Equity Dividend&Premium Opp | IGD | 15.85 | 73 | 8.71 | 60 | 6.87 | 80 | 3.78 | 71 | 3.40 | 78 |

| Wells Fargo Global Dividend Opportunity | EOD | 12.35 | 100 | 0.64 | 100 | 3.95 | 100 | 0.83 | 100 | ||

| Benchmark 1: S&P 500 TR USD | 26.41 | 14.66 | 15.91 | 9.78 | 8.71 | ||||||

| Number of investments ranked | 16 | 16 | 16 | 15 | 10 | ||||||

| * | Strong performance over 5 year period against peer group |

SOURCE: MORNINGSTAR DIRECT

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 5 |

Quarterly Performance Data

Performance over past 5 years periods has been strong

(Data as of 12/31/17)

Source: State Street

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 6 |

AOD Discount Data

Source: Bloomberg. Data as of 2/27/18

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 7 |

Aberdeen CEF Lineup Discounts

Aberdeen Standard Investments US Listed CEFs

| Ticker | Name | NAV Ticker | AUM ($mm) | NAV Discount |

| IAF | ABERDEEN AUSTRALIA EQUITY FD | XIAFX | 148 | -1.3% |

| FCO | ABERDEEN GLOBAL INCOME FUND | XFCOX | 81 | -4.6% |

| ACP | ABERDEEN INCOME CREDIT STRAT | XACPX | 199 | -7.5% |

| FEO | FIRST TRUST ABERDEEN EMG OPP | XFEOX | 95 | -8.2% |

| GRR | ASIA TIGERS FUND INC | XGRRX | 51 | -8.3% |

| IF | ABERDEEN INDONESIA FUND INC | XXIFX | 82 | -8.3% |

| CH | ABERDEEN CHILE FUND INC | XXCHX | 97 | -8.6% |

| LAQ | ABERDEEN LATIN AMERICAN EQTY | XLAQX | 240 | -8.6% |

| SGF | ABERDEEN SINGAPORE FUND INC | XSGFX | 109 | -8.7% |

| GCH | ABERDEEN GREATER CHINA FUND | XGCHX | 131 | -8.8% |

| ABE | ABERDEEN EMERGING MARKETS SM | XABEX | 161 | -9.0% |

| ISL | ABERDEEN ISRAEL FUND INC | XISLX | 91 | -9.5% |

| FAX | ABERDEEN ASIA-PAC INCOME FD | XFAPX | 1,383 | -10.8% |

| IFN | INDIA FUND INC | XIFNX | 857 | -11.7% |

| FAM | FIRST TRUST ABERDEEN GLOBAL | XFAMX | 169 | -11.8% |

| JEQ | ABERDEEN JAPAN EQUITY FUND I | XJEQX | 143 | -11.9% |

| Totals, Averages | 4,036 | -8.6% |

| Ticker | Name | NAV Ticker | AUM ($mm) | NAV Discount |

| MYI LN | MURRAY INTERNATIONAL TR-O | N/A | 2,099 | 5.6% |

| AOD | ALPINE TOTAL DYNAMIC DIVIDEN | XAODX | 1,116 | -8.1% |

Source: Bloomberg. NAVs as of 2/26/18

| www.AlpineFunds.com | Alpine Funds—Aligning capability with need | 8 |