As filed with the Securities and Exchange Commission on May 29, 2007

Registration No. 333-138916

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 4

TO

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Sabine Pass LNG, L.P.

(Exact name of registrant as specified in its charter)

| | | | |

| Delaware | | 2813 | | 20-0466069 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification Number) |

700 Milam Street, Suite 800

Houston, Texas 77002

(713) 375-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Don A. Turkleson

Chief Financial Officer

700 Milam Street, Suite 800

Houston, Texas 77002

(713) 375-5000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

Geoffrey K. Walker

Andrews Kurth LLP

600 Travis, Suite 4200

Houston, Texas 77002

(713) 220-4200

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this registration statement becomes effective.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 29, 2007

PROSPECTUS

SABINE PASS LNG, L.P.

Offer to Exchange

$550,000,000 of 7 1/4% Senior Secured Notes due 2013

that have been registered under the Securities Act of 1933

for

a like amount of 7 1/4% Senior Secured Notes due 2013

that have not been registered under the Securities Act of 1933

and

$1,482,000,000 of 7 1/2% Senior Secured Notes due 2016

that have been registered under the Securities Act of 1933

for

a like amount of 7 1/2% Senior Secured Notes due 2016

that have not been registered under the Securities Act of 1933

THE EXCHANGE OFFER WILL EXPIRE AT 5:00 PM, NEW YORK

CITY TIME, ON [ ], UNLESS WE EXTEND THE DATE

Terms of the Exchange Offer

| | • | | We are offering to exchange up to $2,032 million in aggregate principal amount of our outstanding 7 1/4% Senior Secured Notes due 2013 and 7 1/2% Senior Secured Notes due 2016, which were issued on November 9, 2006 in a transaction exempt from registration under the Securities Act of 1933, as amended, or the Securities Act, and which we refer to as the 2013 initial notes and the 2016 initial notes, respectively, and collectively the initial notes, for a like aggregate principal amount of our 7 1/4% Senior Secured Notes due 2013 and 7 1/2% Senior Secured Notes due 2016, which we refer to as the 2013 notes and the 2016 notes, respectively, and collectively the notes, the issuance of which will be registered under the Securities Act. The initial notes were issued, and the notes will be issued, under an indenture dated as of November 9, 2006. |

| | • | | We will exchange an equal principal amount of notes for all outstanding initial notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer. |

| | • | | The terms of the notes are substantially identical to those of the outstanding initial notes, except that the transfer restrictions and registration rights relating to the initial notes do not apply to the notes. |

| | • | | You may withdraw tenders of initial notes at any time prior to the expiration of the exchange offer. |

| | • | | The exchange of notes for initial notes will not be a taxable transaction for U.S. federal income tax purposes. |

| | • | | We will not receive any cash proceeds from the exchange offer. |

| | • | | The initial notes are, and the notes will be, fully and unconditionally guaranteed, jointly and severally, on a senior secured basis by all of our future domestic restricted subsidiaries. |

| | • | | There is no established trading market for the notes or the initial notes, and we do not intend to apply for listing of the notes on any national securities exchange or for quotation through any quotation system. However, the notes are expected to be eligible to trade in The PORTALSM Market, or PORTAL, a subsidiary of The Nasdaq Stock Market, Inc. |

Terms of the Notes

| | • | | We will pay interest on the notes on each May 30 and November 30, commencing May 30, 2007. |

| | • | | The 2013 notes and the 2016 notes will mature on November 30, 2013 and November 30, 2016, respectively. |

| | • | | We may redeem the 2013 notes and the 2016 notes, in whole or in part, at any time prior to maturity at the redemption prices described in this prospectus, which will include a make-whole premium. In addition, prior to November 30, 2009, we may redeem up to 35% of the 2013 notes and the 2016 notes with the net cash proceeds of one or more equity offerings. Redemption prices are set forth in this prospectus under “Description of Notes—Optional Redemption.” |

| | • | | There is no sinking fund for the notes. |

| | • | | The notes will be secured by a first-priority security interest (subject to certain permitted liens) in our equity interests and substantially all of our assets. The notes will be our senior secured obligations and will rankpari passu in right of payment with all of our existing and future senior indebtedness and senior in right of payment to all of our subordinated indebtedness. |

This investment involves risks. Please read “Risk Factors” beginning on page 17 for a discussion of certain risks that you should consider prior to tendering your outstanding initial notes in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Each broker-dealer that receives notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of notes received in exchange for initial notes where such initial notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of not less than 90 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. Please read “Plan of Distribution.”

The date of the prospectus is [ ].

TABLE OF CONTENTS

You should rely only on the information contained in this document. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may be accurate only on the date of this document.

i

SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that you should consider before making a decision to participate in the exchange offer. You should carefully read the entire prospectus, especially “Risk Factors” beginning on page 17 and our financial statements and the related notes, before deciding to participate in the exchange offer. Unless otherwise indicated, financial information included in this prospectus is presented on an historical basis. As used in this prospectus, unless we indicate otherwise or the context otherwise requires, the terms Sabine Pass LNG, “we,” “our,” “us” and similar terms refer to Sabine Pass LNG, L.P.

Overview

We are an indirect subsidiary of Cheniere Energy, Inc., or Cheniere, which owns a 90.6% interest in us, created to develop, own and operate the Sabine Pass liquefied natural gas, or LNG, receiving terminal currently under construction in western Cameron Parish, Louisiana on the Sabine Pass Channel. The entire 4.0 billion cubic feet per day, or Bcf/d, of regasification capacity that will be available at our LNG receiving terminal upon completion of construction has been fully reserved under three 20-year terminal use agreements, or TUAs, under which the customers are generally required to pay fixed monthly fees, whether or not they use the terminal. Provided our LNG receiving terminal has achieved the required level of commercial operation, which we expect will occur in the third quarter of 2008, these payments will be made as follows:

| | • | | Total LNG USA, Inc., or Total, has reserved approximately 1.0 Bcf/d of regasification capacity and has agreed to make monthly payments to us aggregating approximately $125 million per year for 20 years commencing April 1, 2009; |

| | • | | Chevron U.S.A., Inc., or Chevron, has reserved approximately 1.0 Bcf/d of regasification capacity and has agreed to make monthly payments to us aggregating approximately $125 million per year for 20 years commencing not later than July 1, 2009; and |

| | • | | Cheniere Marketing, Inc., or Cheniere Marketing, a wholly-owned subsidiary of Cheniere, has reserved approximately 2.0 Bcf/d of regasification capacity, is entitled to use any capacity not utilized by Total and Chevron and has agreed to make monthly payments to us aggregating approximately $250 million per year for at least 19 years commencing January 1, 2009. In addition, Cheniere Marketing has agreed to make payments of $5 million per month during an initial commercial operations ramp-up period in 2008 commencing on the date of commercial operations completion. |

Our LNG Receiving Terminal

In 2003, we were formed by Cheniere to develop our LNG receiving terminal. The initial phase, or Phase 1, of our LNG receiving terminal was designed, and permitted by the Federal Energy Regulatory Commission, or FERC, with a regasification capacity of 2.6 Bcf/d, three LNG storage tanks with an aggregate LNG storage capacity of 10.1 billion cubic feet, or Bcf, and two unloading docks capable of handling the largest LNG carriers currently being operated or built. In July 2006, we received approval from the FERC to increase the regasification capacity of our LNG receiving terminal from 2.6 Bcf/d to 4.0 Bcf/d by adding up to three additional LNG storage tanks, additional vaporizers and related facilities. We refer to the entire FERC-approved expansion as Phase 2. The first stage of the Phase 2 expansion will include the addition of a fourth and fifth LNG storage tank, additional vaporizers and related facilities, and will achieve a full operability at approximately 4.0 Bcf/d and an aggregate storage capacity of approximately 16.8 Bcf. We refer to this expansion as Phase 2 – Stage 1. We will conduct further Phase 2 expansion, if any, including construction of a potential sixth LNG storage tank, in one or more subsequent stages.

1

Although we are still in the process of constructing our LNG receiving terminal, we have already entered into three TUAs, through which Total, Chevron and Cheniere Marketing have reserved, in aggregate, the entire 4.0

Bcf/d of LNG regasification capacity that will be available upon completion of Phase 1 and Phase 2 – Stage 1 of our LNG receiving terminal. Payment obligations under our TUAs have also been guaranteed by our customers’ respective parent companies, Total, S.A. (up to $2.5 billion of fees payable by Total), Chevron Corporation (up to 80% of fees payable by Chevron) and Cheniere (100% of fees payable by Cheniere Marketing).

Construction of our LNG receiving terminal began in March 2005. During the second quarter of 2008, we expect to complete construction and cool down of the first two tanks, to complete related equipment installation and specified checks and tests, and to achieve a sustained revaporized natural gas sendout at a significant rate for a preagreed period of time (currently provided to be a rate of at least 2.0 Bcf/d for a minimum sustained test period of at least 24 hours), which we refer to as Phase 1 Target Completion. We expect to complete construction and commissioning of the third tank and the rest of Phase 1, and to achieve the full 2.6 Bcf/d of Phase 1 regasification capacity, during the third quarter of 2008. LNG regasification operations relating to the Phase 2 – Stage 1 expansion are expected to commence by April 2009. We expect to complete all of Phase 2 – Stage 1, including construction and commissioning of the fourth and fifth tanks, and to achieve full operability at 4.0 Bcf/d and aggregate storage capacity of approximately 16.8 Bcf during the third quarter of 2009.

Our cost to construct Phase 1 of our LNG facility is currently estimated at approximately $900 million to $950 million, before financing costs. Phase 2 – Stage 1 is estimated to cost approximately $500 million to $550 million, before financing costs. Our cost estimates are subject to change due to such items as cost overruns, change orders, delays in construction, increased component and material costs, escalation of labor costs and increased spending to maintain our construction schedule. See “Description of Principal Project Documents.” As of March 31, 2007, we had paid $615.0 million and $73.5 million of Phase 1 and Phase 2 – Stage 1 construction costs, respectively.

Business Strategy

Our primary business objective is to generate stable cash flows by completing construction of our LNG receiving terminal so that terminal operations can commence and we can generate steady and reliable revenues under long-term TUAs.

Strengths

We believe that we have several strengths and advantages in pursuing our business strategy, including:

| | • | | our contracted and stable cash flows under three long-term TUAs; |

| | • | | our solid arrangements with Bechtel Corporation, or Bechtel, for the construction of our LNG receiving terminal; |

| | • | | what we believe is one of the best available North American sites for our LNG receiving terminal; |

| | • | | ample access, currently under development, to natural gas transmission pipelines; |

| | • | | economies of scale in operation of our LNG receiving terminal; |

| | • | | an environmentally sound and community friendly approach in developing our LNG receiving terminal; |

| | • | | our team of professionals with extensive experience in the LNG industry; |

| | • | | a comprehensive collateral package that benefits the notes; and |

| | • | | the availability of reserve funds that offer multiple sources of liquidity. |

2

Illustrative Cash Flow Summary

The information set forth below represents our anticipated results of operations, including the projected revenues under our 20-year TUAs with Total, Chevron and Cheniere Marketing, for 2010, the first full year of operating revenues under all three TUAs. In preparing this information, we have relied on assumptions regarding circumstances beyond the control of us or any other person. By their nature, the assumptions are subject to significant uncertainties and actual results will differ, perhaps materially, from those projected. We cannot give any assurance that these assumptions are correct or that this information will reflect actual results. Accordingly, this financial estimate is not intended to be a prediction of future results. If our actual results are materially less favorable than those shown, or if the assumptions used in preparing this information prove to be incorrect, our ability to make payments of principal and interest on the notes may be adversely affected. For additional information relating to these financial estimates, please read “Risk Factors—Risks Relating to the Exchange Offer and the Notes—Our financial estimates, including our illustrative cash flow summary, are based on certain assumptions that may not materialize.”

| | | | |

(Dollars in millions)

| | 2010

| |

TUA Revenues(1) | | | | |

Total TUA(2) | | $ | 125.5 | |

Chevron TUA(2) | | | 129.9 | |

Cheniere Marketing TUA | | | 255.7 | |

| | |

|

|

|

Aggregate TUA Revenues | | | 511.1 | |

Deferred revenues(2) | | | (4.0 | ) |

Operating expenses(3) | | | (36.7 | ) |

Assumed commissioning costs(4) | | | — | |

State and local taxes | | | (9.9 | ) |

| | |

|

|

|

EBITDA(5) | | $ | 460.5 | |

| | |

|

|

|

EBITDA/Interest(6) | | | 3.1x | |

Total Debt/ EBITDA(7) | | | 4.4x | |

| (1) | Fixed capacity reservation fees, including an operating fee component subject to adjustment for annual consumer price index inflation (assumed to be 2.5% annually). |

| (2) | TUA revenues include $2 million of annual non-cash deferred revenues during the first ten years under each of the Total and Chevron TUAs related to $20 million of advance capacity reservation fees previously received from each of Total and Chevron. |

| (3) | Combined operating expenses and maintenance capital expenditures are as estimated by us and the Independent Engineer. See “Summary of Independent Engineer’s Report,” below, for more information. Maintenance capital expenditures estimated by us at $1.5 million per year beginning in 2009, escalating with inflation at 2.5% annually thereafter, are not included in this table. |

| (4) | We anticipate that these commissioning costs will be paid before the third quarter of 2009. |

| (5) | Calculated as total TUA revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. See “—Non-GAAP Financial Measure,” below, for more information. |

| (6) | Assumes weighted-average fixed interest rate of 7.432% paid semi-annually. |

| (7) | Assumes total debt of $2,032 million. |

Assuming payments under the 20-year TUAs with Total, Chevron and Cheniere Marketing are made as contractually stipulated, we expect (i) the Total TUA to provide annual revenues of approximately $125 million for 20 years commencing April 1, 2009, (ii) the Chevron TUA to provide annual revenues of approximately $125 million for 20 years commencing July 1, 2009 and (iii) the Cheniere Marketing TUA to provide annual revenues of approximately $250 million for at least 19 years commencing January 1, 2009,plus initial revenues of $5

3

million per month during 2008 commencing on the date of commercial operations completion. The Independent Engineer has estimated that the total annual operating expenses for our LNG receiving terminal will be approximately $37 million per year to support the full 4.0 Bcf/d of receiving capacity. Based on these expected TUA revenues and operating expenses, we believe that our LNG receiving terminal will generate approximately $461 million in EBITDA in 2010.

The operating expenses set forth in the table above for 2010 may be higher in later years due to numerous factors, such as increased maintenance costs of our LNG receiving terminal as the facility ages. As a result, the EBITDA forecast for 2010 may not be indicative of our EBITDA in periods thereafter. In addition, approximately one-half of our forecast revenues are attributable to Cheniere Marketing, which is a small, developing company with virtually no operating history. See “Risk Factors—Risks Relating to Development and Operation of Our Business—If and when the applicable commercial start dates under the TUAs are achieved, we will become dependent upon our TUA counterparties, including cash flows from the Cheniere Marketing TUA, for substantially all of our revenues and cash flows.” We do not expect to generate sufficient cash flow from operations to repay the notes upon maturity without additional refinancing, which may not be available on terms reasonably acceptable to us or at all. See “Risk Factors—Risks Relating to the Exchange Offer and the Notes—To service our indebtedness, we will require significant amounts of cash. Our ability to generate cash will depend on many factors beyond our control.”

Our independent auditor has not reviewed the foregoing illustrative cash flow summary and, accordingly, does not express an opinion or any other form of assurance on it. Holders of the notes will not be provided with any revised illustrative cash flow summary. We expressly disclaim any duty to update the illustrative cash flow summary under any circumstances.

Non-GAAP Financial Measure

Our EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does not include depreciation expense and certain non-operating items. Because we have not forecasted such depreciation expense and non-operating items, we have not made any forecast of net income, which would be the most directly comparable financial measure under generally accepted accounting principles, or GAAP. As a result, we are unable to reconcile differences between forecasts of EBITDA and net income. EBITDA is used as a supplemental financial measure by management and by external users of our financial statements, such as commercial banks, to assess:

| | • | | the anticipated financial performance of our assets without regard to financing methods, capital structure or historical cost basis; |

| | • | | the ability of our assets to generate cash sufficient to pay interest on our indebtedness; and |

| | • | | our anticipated operating performance and return on invested capital compared to other comparable companies, without regard to their financing methods and capital structure. |

Our EBITDA should not be considered an alternative to net income, operating income, cash flows from operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. Our EBITDA excludes some, but not all, items that affect net income and operating income, and it does not include capital expenditures and other non-operating items that require capital expenditures. In addition, these expenditures excluded from EBITDA may, over time, be material to our business and may have a negative impact on the cash available to make interest payments on the notes and to repay our indebtedness. These EBITDA measures may vary among companies. Therefore, our EBITDA may not be comparable to similarly titled measures of other companies.

4

Summary of Independent Engineer’s Report

This prospectus contains a report by Stone & Webster Management Consultants, Inc., or the Independent Engineer. The Independent Engineer has prepared a report that analyzes certain technical, environmental and economic aspects of our LNG receiving terminal. This report includes, among other things, discussions of the technology used at the LNG receiving terminal, engineering and construction execution issues and costs, operating plans, environmental permitting status, and a technical review of the documents and agreements relating to our LNG receiving terminal. A copy of the report is attached as Appendix A to this prospectus and should be read in its entirety. The Independent Engineer is a leading consulting and engineering firm that devotes a substantial portion of its resources to providing services related to the technical, environmental and economic aspects of industrial facilities.

In the preparation of its report, the Independent Engineer has relied on assumptions regarding circumstances beyond the control of us or any other person. By their nature, these assumptions are subject to significant uncertainties and actual results will differ, perhaps materially, from those stated in the report. The persons responsible for the assumptions contained in the report cannot give any assurance that these assumptions will prove to be correct. If our actual results are materially less favorable than those shown in the Independent Engineer’s report, or if the assumptions prove to be incorrect, our ability to make payments of principal and interest on the notes may be adversely affected.

Our independent auditor has not reviewed the Independent Engineer’s report and, accordingly, does not express an opinion or any other form of assurance on it. Holders of the notes will not be provided with any revised report from the Independent Engineer. We expressly disclaim any duty to update the Independent Engineer’s report under any circumstances.

Below is a summary of the conclusions expressed by the Independent Engineer in its report. This is merely a summary and is subject to the information contained, and the assumptions made, in the Independent Engineer’s report. The Independent Engineer’s report should be read in its entirety in order for the reader to understand the basis of the conclusions and the assumptions upon which they are based.

Certain terms used in the summary below are defined in the Independent Engineer’s report. On the basis of its studies, analyses and investigations of our LNG receiving terminal and the assumptions set forth in the Independent Engineer’s report, the Independent Engineer is of the opinion that:

| | • | | The Phase 1 Project is technically viable; |

| | • | | The Phase 1 Project Budget is reasonable; |

| | • | | The Phase 1 Schedule is reasonable; |

| | • | | The Phase 1 Project has been approved by the FERC, indicating compliance with environmental regulations and that environmental risks are low; |

| | • | | The Phase 1 Project contracting strategy is reasonable and minimizes the strain on Sabine Pass LNG, which is a development stage company; |

| | • | | The Phase 1 EPC contract provides a suitable basis for contracting the required services; |

| | • | | The Phase 1 Project will provide ample availability to service the aggregate 2.0 Bcf/d export capacity requirements under the Total and Chevron TUAs; |

| | • | | The Phase 2 – Stage 1 Expansion of Sabine Pass poses negligible risk to the timely completion and operation of the Phase 1 Project; |

| | • | | The Phase 2 – Stage 1 Expansion is technically feasible and viable; |

5

| | • | | The Phase 2 – Stage 1 Budget is reasonable and generally consistent with that for the Phase 1 Project; |

| | • | | The Phase 2 – Stage 1 Schedule is reasonable; |

| | • | | The Phase 2 – Stage 1 Project has been approved by the FERC, indicating compliance with environmental regulations and that environmental risks are low; |

| | • | | The Phase 2 – Stage 1 Project contracting strategy provides Sabine Pass LNG with maximum flexibility in Phase 2 Project execution; |

| | • | | The Phase 2 – Stage 1 construction contracts provide a suitable basis for contracting the required services without impinging on the Phase 1 Project; and |

| | • | | The Phase 2 – Stage 1 Project will increase the overall export capacity to a maximum peak rate of 4.0 Bcf/d and a long-term sustainable capacity of at least approximately 3.5 Bcf/d. |

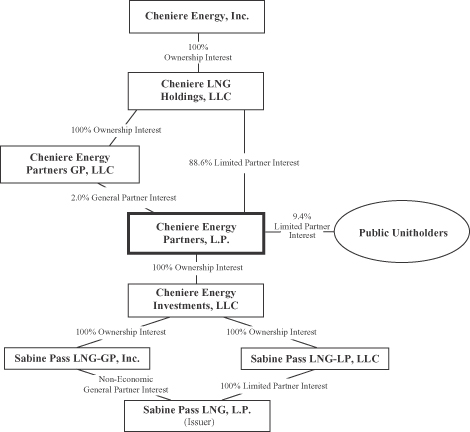

Organizational Structure

We are the operating subsidiary of Cheniere that was created to develop, own and operate the Sabine Pass LNG receiving terminal. Our general partner has sole responsibility and authority for conducting our business and for managing our operations. The directors and officers of our general partner are also officers of Cheniere, except for one independent director. See “Management.” The following chart shows the ownership of our partnership:

6

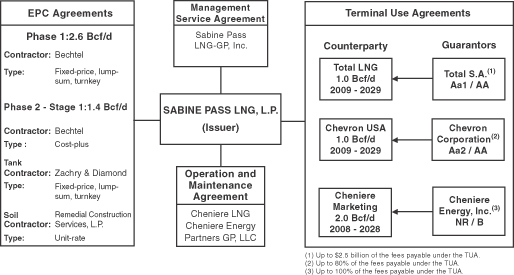

Contractual Relationships

The following chart illustrates several of our key contractual relationships. See “Description of Principal Project Documents” and “Certain Relationships and Related Transactions” for additional information regarding the agreements listed below.

7

The Exchange Offer

On November 9, 2006, we completed a private offering of the initial notes. As part of the private offering, we entered into a registration rights agreement with the representative of the initial purchasers of the initial notes in which we agreed, among other things, to deliver this prospectus to you and to use our commercially reasonable efforts to cause the registration statement to be effective within 270 days of the issue date of the initial notes and to complete the exchange offer within 30 days thereafter. The following is a summary of the exchange offer.

Original Notes | $550 million aggregate principal amount of 7 1/4% Senior Secured Notes due 2013, which were issued in a private placement on November 9, 2006 |

| | $1,482 million aggregate principal amount of 7 1/2% Senior Secured Notes due 2016, which were issued on November 9, 2006 |

Notes | 7 1/4% Senior Secured Notes due November 30, 2013 and 7 1/2% Senior Secured Notes due November 30, 2016. The terms of the notes are substantially identical to those terms of the outstanding initial notes, except that the transfer restrictions, registration rights and provision for additional interest relating to the initial notes do not apply to the notes. |

Exchange Offer | We are offering to exchange up to $2,032 million aggregate principal amount of our notes ($550 million of 7 1/4% Senior Secured Notes due 2013 and $1,482 million of 7 1/2% Senior Secured Notes due 2016) that have been registered under the Securities Act for an equal amount of our outstanding initial notes that have not been registered under the Securities Act to satisfy our obligations under the registration rights agreement. |

| | The notes will evidence the same debt as the initial notes and will be issued under and be entitled to the benefits of the same indenture that governs the initial notes. Holders of the initial notes do not have any appraisal or dissenter rights in connection with the exchange offer. Because the notes will be registered, the notes will not be subject to transfer restrictions or the provisions for additional interest, and holders of initial notes that have tendered and had their initial notes accepted in the exchange offer will have no registration rights. |

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on [ ], unless we decide to extend it. We do not currently intend to extend the exchange offer. |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, which we may waive. Please read “The Exchange Offer—Conditions to the Exchange Offer” for more information regarding the conditions to the exchange offer. |

Procedures for Tendering Initial Notes | Unless you comply with the procedures described under the caption “The Exchange Offer—Procedures for Tendering—Guaranteed |

8

| | Delivery,” you must do one of the following on or prior to the expiration of the exchange offer to participate in the exchange offer: |

| | • | | tender your initial notes by sending the certificates for your initial notes, in proper form for transfer, a properly completed and duly executed letter of transmittal, with any required signature guarantees, and all other documents required by the letter of transmittal, to The Bank of New York, as registrar and exchange agent, at the address listed under the caption “The Exchange Offer—Exchange Agent”; or |

| | • | | tender your initial notes by using the book-entry transfer procedures described below and transmitting a properly completed and duly executed letter of transmittal, with any required signature guarantees, or an agent’s message instead of the letter of transmittal, to the exchange agent. In order for a book-entry transfer to constitute a valid tender of your initial notes in the exchange offer, The Bank of New York, as registrar and exchange agent, must receive a confirmation of book-entry transfer of your initial notes into the exchange agent’s account at The Depository Trust Company prior to the expiration of the exchange offer. For more information regarding the use of book-entry transfer procedures, including a description of the required agent’s message, please read the discussion under the caption “The Exchange Offer—Procedures for Tendering—Book-Entry Transfer.” |

Guaranteed Delivery Procedures | If you are a registered holder of the initial notes and wish to tender your initial notes in the exchange offer, but |

| | • | | the initial notes are not immediately available, |

| | • | | time will not permit your initial notes or other required documents to reach the exchange agent before the expiration of the exchange offer, or |

| | • | | the procedure for book-entry transfer cannot be completed prior to the expiration of the exchange offer, |

| | then you may tender your initial notes by following the procedures described under the caption “The Exchange Offer—Procedures for Tendering—Guaranteed Delivery.” |

Special Procedures for Beneficial Owners | If you are a beneficial owner whose initial notes are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your initial notes in the exchange offer, you should promptly contact the person in whose name the initial notes are registered and instruct that person to tender on your behalf. |

| | If you wish to tender in the exchange offer on your own behalf, prior to completing and executing the letter of transmittal and delivering the certificates for your initial notes, you must either make |

9

| | appropriate arrangements to register ownership of the initial notes in your name or obtain a properly completed bond power from the person in whose name the initial notes are registered. |

Withdrawal; Non-Acceptance | You may withdraw any initial notes tendered in the exchange offer at any time prior to 5:00 p.m., New York City time, on [ ]. If we decide for any reason not to accept any initial notes tendered for exchange, the initial notes will be returned to the registered holder at our expense promptly after the expiration or termination of the exchange offer. In the case of initial notes tendered by book-entry transfer into the exchange agent’s account at The Depository Trust Company, any withdrawn or unaccepted initial notes will be credited to the tendering holder’s account at The Depository Trust Company. For further information regarding the withdrawal of tendered initial notes, please read “The Exchange Offer—Withdrawal Rights.” |

U.S. Federal Income Tax Considerations | The exchange of notes for initial notes in the exchange offer will not be a taxable transaction for U.S. federal income tax purposes. Please read the discussion under the caption “Material United States Federal Income Tax Considerations” for more information regarding the tax consequences to you of the exchange offer. |

Use of Proceeds | The issuance of the notes will not provide us with any new proceeds. We are making this exchange offer solely to satisfy our obligations under the registration rights agreement. |

Fees and Expenses | We will pay all of the expenses incident to the exchange offer. |

Exchange Agent | We have appointed The Bank of New York as exchange agent for the exchange offer. You can find the address, telephone number and fax number of the exchange agent under the caption “The Exchange Offer—Exchange Agent.” |

Resales of Notes | Based on interpretations by the staff of the SEC, as set forth in no-action letters issued to third parties that are not related to us, we believe that the notes you receive in the exchange offer may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act so long as: |

| | • | | the notes are being acquired in the ordinary course of business; |

| | • | | you are not participating, do not intend to participate, and have no arrangement or understanding with any person to participate in the distribution of the notes issued to you in the exchange offer; |

| | • | | you are not our affiliate; and |

| | • | | you are not a broker-dealer tendering initial notes acquired directly from us for your account. |

10

| | The SEC has not considered this exchange offer in the context of a no-action letter, and we cannot assure you that the SEC would make similar determinations with respect to this exchange offer. If any of these conditions are not satisfied, or if our belief is not accurate, and you transfer any notes issued to you in the exchange offer without delivering a resale prospectus meeting the requirements of the Securities Act or without an exemption from registration of your notes from those requirements, you may incur liability under the Securities Act. We will not assume, nor will we indemnify you against, any such liability. Each broker-dealer that receives notes for its own account in exchange for initial notes, where the initial notes were acquired by such broker-dealer as a result of market-making activities or other trading activities, must acknowledge that it will deliver a prospectus in connection with any resale of such notes. Please read “Plan of Distribution.” |

| | Please read “The Exchange Offer—Resales of Notes” for more information regarding resales of the notes. |

Consequences of Not Exchanging Your Initial Notes | If you do not exchange your initial notes in this exchange offer, you will no longer be able to require us to register your initial notes under the Securities Act, except in the limited circumstances provided under the registration rights agreement. In addition, you will not be able to resell, offer to resell or otherwise transfer your initial notes unless we have registered the initial notes under the Securities Act, or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act. |

| | For information regarding the consequences of not tendering your initial notes and our obligation to file a registration statement, please read “The Exchange Offer—Consequences of Failure to Exchange Outstanding Securities” and “Description of Notes.” |

11

Description of Notes

The terms of the notes and those of the outstanding initial notes are substantially identical, except that the transfer restrictions and registration rights relating to the initial notes do not apply to the notes. As a result, the notes will not bear legends restricting their transfer and will not have the benefit of the registration rights and special interest provisions contained in the initial notes. The notes represent the same debt as the initial notes for which they are being exchanged. Both the initial notes and the notes are governed by the same indenture. When we use the term “notes” in this prospectus, unless the context otherwise requires, the term includes the initial notes and the notes issued pursuant to the exchange offer.

The following is a summary of the terms of the notes. It may not contain all of the information that is important to you. For a more detailed description of the notes, please read “Description of Notes.”

Issuer | Sabine Pass LNG, L.P. |

Notes Offered | $550 million aggregate principal amount of 7 1/4% Senior Secured Notes due 2013. |

| | $1,482 million aggregate principal amount of 7 1/2% Senior Secured Notes due 2016. |

Maturity Date | 2013 notes: November 30, 2013 |

| | 2016 notes: November 30, 2016 |

| | The notes will not amortize prior to the Maturity Date. |

Interest Payment Dates | May 30 and November 30 of each year, commencing on May 30, 2007. |

Interest | 7 1/4% per annum on the 2013 notes and 7 1/2% per annum on the 2016 notes, payable semiannually in arrears. Interest will be computed on the basis of a 360-day year comprised of twelve 30-day months. |

Guarantees | The notes will be guaranteed by all of our future domestic restricted subsidiaries. We currently have no subsidiaries. See “Description of Notes—The Note Guarantees.” |

Ranking | The notes are our senior secured obligations and: |

| | • | | rankpari passu in right of payment with all of our other existing and future senior indebtedness; and |

| | • | | rank senior in right of payment to all of our subordinated indebtedness. |

We have no indebtedness outstanding other than the initial notes.

Optional Redemption | At any time and from time to time, we may redeem some or all of the 2013 notes at a redemption price equal to 100% of the principal amount plus a make-whole premium, plus accrued and unpaid interest and additional interest, if any, to the redemption date. |

12

| | At any time and from time to time, we may redeem some or all of the 2016 notes at a redemption price equal to 100% of the principal amount plus a make-whole premium, plus accrued and unpaid interest and additional interest, if any, to the redemption date. |

| | Until November 30, 2009, we may redeem up to 35% of the principal amount of the 2013 notes and the 2016 notes originally issued with the net cash proceeds of one or more equity offerings by us with the proceeds that we retain or that are contributed to us, as applicable, at par plus a premium equal to the coupon, plus accrued and unpaid interest and additional interest, if any, as long as at least 65% of the aggregate principal amount of the notes remains outstanding immediately after such optional redemption and such optional redemption occurs within 90 days of the date of the closing of such equity offering. |

Mandatory Redemption | If we sell certain assets or experience certain events of loss, we must offer to purchase the notes at the prices determined as stated under “Description of Notes—Repurchase at the Option of Holders.” |

Change of Control | If a change of control of our general partner occurs, we are required to offer to repurchase all or a portion of such holder’s notes at a price equal to 101% of their principal amount, plus accrued and unpaid interest and additional interest, if any, as of the date of repurchase. |

Collateral | Our obligations under the notes are secured on a first-priority basis (subject to certain permitted liens) by a security interest in our equity interests and substantially all of our assets, including a pledge of the stock of our future subsidiaries (provided that the pledge of voting stock of our future foreign subsidiaries will be limited to 65% of the voting stock owned by us or any guarantor). See “Description of Notes—Security.” |

Construction Period Debt Service Reserve Account | We have deposited $335 million in a debt service reserve account, which will be withdrawn when necessary to pay the first five interest payments on the notes. |

Cash Waterfall | We have deposited approximately $887 million from the sale of the initial notes in a construction account, which, until Phase 1 Target Completion, will only be applied to pay construction and startup costs of the project and to pay other expenses incidental for us to complete construction of the project. Following Phase 1 Target Completion, any amount remaining in the construction account will be transferred to a revenue account. |

| | All revenues received by us will be deposited in a revenue account and will be applied as described in “Pre-Completion Account Flows” and “Post-Completion Account Flows” below. |

13

Pre-Completion Account Flows | Prior to Phase 1 Target Completion, revenues received by us will be applied in the following manner: |

| | • | | first, to pay obligations, if any, under the assumption agreement, as described under “Certain Relationships and Related Transactions—Assumption Agreement,” which we refer to as the assumption agreement; |

| | • | | second, to the extent that amounts on deposit in the debt service reserve account are not sufficient to pay interest on the notes on the next interest payment date, to such account in an amount sufficient to make such payment; and |

| | • | | third, to the construction account (i) to fund the construction and start-up costs of our LNG receiving terminal; (ii) to pay other expenses (including taxes) incidental for us to complete construction of our LNG receiving terminal; and (iii) to be transferred to other project accounts. |

Post-Completion Account Flows | After Phase 1 Target Completion, revenues received by us will be applied in the following manner: |

| | • | | first, to fund the operating account with amounts sufficient to cover the succeeding 45 days of operation and maintenance expenses, maintenance capital expenditures and obligations, if any, under the assumption agreement and a state tax sharing agreement; |

| | • | | second, 1/6th of the amount of interest due on the notes on the next interest payment date (plus any shortfall from any such month subsequent to the preceding interest payment date) will be transferred to a debt payment account; |

| | • | | third, to pay outstanding principal then due and payable on the notes; |

| | • | | fourth, to pay taxes payable by us or the guarantors and permitted payments in respect of taxes; |

| | • | | fifth, to replenish the debt service reserve account when such account is not funded with the amount (or acceptable letters of credit or acceptable guarantees in respect of such amount) required to make the next interest payment on the notes; and |

| | • | | sixth, for all other purposes permitted by the indenture including restricted payments, subject to the limitations contained in the indenture. |

Covenants | The indenture governing the notes contains covenants that, among other things, limit our ability and the ability of our restricted subsidiaries to: |

| | • | | incur additional indebtedness or issue preferred stock; |

| | • | | make certain investments or pay dividends or distributions on our capital stock or subordinated indebtedness or purchase or redeem or retire capital stock; |

| | • | | sell or transfer assets, including capital stock of our restricted subsidiaries; |

14

| | • | | restrict dividends or other payments by restricted subsidiaries; |

| | • | | enter into transactions with affiliates; |

| | • | | consolidate, merge, sell or lease all or substantially all of our assets; and |

| | • | | enter into sale and leaseback transactions. |

| | These covenants are subject to a number of important limitations and exceptions that are described later in this prospectus under the caption “Description of Notes—Certain Covenants.” |

Restricted Payments | We will be permitted to make payments on subordinated debt, make distribution to our partners, purchase any equity interest in an affiliate and make restricted investments with any amounts of available cash, which includes revenues available after payment of construction costs and other capital expenditures, payments of required principal and interest on indebtedness and payment of operation and maintenance expenses. Such payments can be made as long as no default or event of default under the indenture has occurred and is continuing; Phase 1 has been completed in accordance with the target completion date performance standards set forth in the EPC contract with Bechtel; we would be permitted to incur at least $1.00 of additional indebtedness at the time of the payment and after giving pro forma effect thereto; the operating period debt service reserve account has at least six months of interest funded; and the debt payment account has on deposit the amount required at such time. |

Transfer Restrictions; Absence of a Public Market for the Notes | The notes issued pursuant to this exchange offer will generally be freely transferable, but will also be new securities for which there will not initially be a market. There can be no assurance as to the development or liquidity of any market for the notes. |

Governing Law | The indenture, the notes and related security documents are governed by, and construed in accordance with, the laws of the State of New York, while the real property mortgage is governed by the laws of the State of Louisiana. |

Risk Factors

See “Risk Factors” for a discussion of certain factors that you should carefully consider before deciding to participate in the exchange offer.

Executive Offices

Our principal executive offices are located at 700 Milam Street, Suite 800, Houston, Texas 77002. Our telephone number is (713) 375-5000.

15

Summary Selected Historical Financial Data

The following tables set forth our selected financial data for the periods and at the dates indicated. The summary statement of operations data for the years ended December 31, 2004, 2005 and 2006, and the balance sheet information at December 31, 2005 and 2006 are derived from our audited financial statements, which are included elsewhere in this prospectus. The summary statement of operations data for the three months ended March 31, 2007 and 2006 and the balance sheet information at March 31, 2007 are derived from our unaudited financial statements, which are included elsewhere in this prospectus. The summary statement of operations data for the period from October 20, 2003 (inception) through December 31, 2003 and the summary balance sheet information at December 31, 2003 and 2004 have been derived from our audited financial statements, which are not included in this prospectus. Our past financial or operating performance is not a reliable indicator of our future performance (particularly anticipated revenues, debt costs and expenses), and you should not use our historical performance to anticipate results or future period trends.

We derived the information in the following tables from, and that information should be read together with and is qualified in its entirety by reference to, the financial statements and the accompanying notes included in this prospectus. The table should also be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| | | | | | | | | | | | | | | | | | | | | | | | |

(Dollars in thousands)

| | Period from

October 20, 2003 (inception) to

December 31, 2003

| | | Year ended

December 31,

| | | Three Months

Ended March 31,

| |

| | | 2004

| | | 2005

| | | 2006

| | | 2007

| | | 2006

| |

Revenues | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

Expenses | | | 2,763 | | | | 4,682 | | | | 4,711 | | | | 10,265 | | | | 1,860 | | | | 1,590 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Loss from operations | | | (2,763 | ) | | | (4,682 | ) | | | (4,711 | ) | | | (10,265 | ) | | | (1,860 | ) | | | (1,590 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Other income (expense)(1) | | | — | | | | 28 | | | | 456 | | | | (50,495 | ) | | | (11,050 | ) | | | 810 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net loss | | $ | (2,763 | ) | | $ | (4,654 | ) | | $ | (4,255 | ) | | $ | (60,760 | ) | | $ | (12,910 | ) | | $ | (780 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Ratio of earnings to fixed charges(2) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | |

(Dollars in thousands)

| | December 31,

| | March 31, 2007

|

| | 2003

| | 2004

| | 2005

| | 2006

| |

Cash and cash equivalents (unrestricted) | | $ | — | | $ | 21,822 | | $ | — | | $ | — | | $ | — |

Non-current restricted cash and cash equivalents | | | — | | | — | | | — | | | 982,613 | | | 882,919 |

Restricted cash and cash equivalents | | | — | | | — | | | 8,871 | | | 176,324 | | | 209,645 |

Total assets | | | 101 | | | 23,316 | | | 309,135 | | | 1,858,111 | | | 1,915,487 |

Long-term debt | | | — | | | — | | | 37,377 | | | 2,032,000 | | | 2,032,000 |

Deferred revenues | | | — | | | 22,000 | | | 40,000 | | | 40,000 | | | 40,000 |

Total other long-term liabilities | | | 2,864 | | | 17,418 | | | 120 | | | 1,149 | | | 1,154 |

| (1) | The year ended 2006 includes a $23.8 million loss related to the expensing of debt issuance costs and a $20.6 million derivative loss as a result of terminating interest rate swaps, both related to the termination of the Sabine Pass credit facility in November 2006. |

| (2) | The ratios were computed by dividing earnings by fixed charges. For this purpose, “earnings” represent the aggregate of (a) pre-tax income from continuing operations before adjustment for minority interests in consolidated subsidiaries or income or loss from equity investees, (b) fixed charges, (c) amortization of capitalized interest, (d) distributed income of equity investees and (e) our share of pre-tax losses of equity investees for which charges arising from guarantees are included in fixed charges, net of (a) interest capitalized and (b) the minority interest in pre-tax income of subsidiaries that have not incurred fixed charges. “Fixed charges” represent the sum of (a) interest expensed and capitalized, (b) amortized premiums, discounts and capitalized expenses related to indebtedness and (c) an estimate of the interest within rental expense. As a result of reported losses, earnings were inadequate to cover fixed charges, thereby resulting in a coverage deficiency of $2.8 million for the period from October 20, 2003 (inception) to December 31, 2003, $4.7 million, $9.7 million and $83.1 million for the years ended December 31, 2004, 2005 and 2006, respectively, and $25.8 million and $3.5 million for the three months ended March 31, 2007 and 2006, respectively. |

16

RISK FACTORS

Before deciding to participate in the exchange offer, you should carefully consider the following risk factors. We may encounter risks in addition to those described below. Additional risks and uncertainties not currently known to us, or that we currently deem to be immaterial, may also impair or adversely affect the development of our business, our assets, our contracts, our results of operations, our tax status, our financial condition and our prospects. As a result of any of these risks, known and unknown, you could lose all or part of your original investment in the notes.

The risk factors in this prospectus are grouped into the following categories:

| | • | | Risks Relating to Completion of our LNG Receiving Terminal, beginning on this page 17; |

| | • | | Risks Relating to Development and Operation of our Business, beginning on page 20; and |

| | • | | Risks Relating to the Exchange Offer and the Notes, beginning on page 27. |

Risks Relating to Completion of our LNG Receiving Terminal

Our inability to timely construct and commission our LNG receiving terminal would prevent us from commencing operations when anticipated and would prevent us from realizing anticipated cash flows.

We may not complete Phase 1 or Phase 2 – Stage 1 of our LNG receiving terminal in a timely manner, or at all, due to numerous factors, some of which are beyond our control. Factors that could adversely affect our planned completion include:

| | • | | failure by Bechtel or the other contractors to fulfill their obligations under their construction contracts, or disagreements with them over their contractual obligations; |

| | • | | our failure to enter into satisfactory additional agreements with contractors for the rest of Phase 2 – Stage 1; |

| | • | | shortages of materials or delays in delivery of materials; |

| | • | | cost overruns and difficulty in obtaining sufficient debt or equity financing to pay for such additional costs; |

| | • | | difficulties or delays in obtaining LNG for commissioning activities necessary to achieve commercial operability of our LNG receiving terminal; |

| | • | | failure to obtain all necessary governmental and third-party permits, licenses and approvals for the construction and operation of our LNG receiving terminal; |

| | • | | weather conditions, such as hurricanes and other catastrophes, such as explosions, fires, floods and accidents; |

| | • | | difficulties in attracting a sufficient skilled and unskilled workforce, increases in the level of labor costs and the existence of any labor disputes; |

| | • | | resistance in the local community to the development of our LNG receiving terminal due to safety, environmental or security concerns; and |

| | • | | local and general economic and infrastructure conditions. |

Our inability to timely complete our LNG receiving terminal, including as a result of any of the foregoing factors, could prevent us from commencing operations when anticipated, which could delay payments under the TUAs. As a result, we may not receive our anticipated cash flows on time or at all.

17

We may experience cost overruns and delays in the completion of Phase 1 or Phase 2 – Stage 1 of our LNG receiving terminal as well as difficulties in obtaining funding for any additional costs, which could have a material adverse effect on our results of operations.

Our construction costs for Phase 1 and Phase 2 – Stage 1 may be significantly higher than our current estimates as a result of cost overruns, change orders under existing or future construction contracts, increased component and material costs, escalating labor costs, limited availability of labor, delays in construction and increased spending to maintain construction schedules. We may also incur commissioning costs in excess of our forecast. As of April 30, 2007, change orders for $132.3 million had been approved under the Phase 1 EPC agreement with Bechtel. We do not have any prior experience in constructing LNG receiving terminals, and no LNG receiving terminal has been constructed and placed in service in the U.S. in almost 25 years, as a result of which there are limited benchmarks against which to compare our estimates.

Furthermore, in order to cover not only increased costs but also the cost of a sixth LNG storage tank if requested by Cheniere Marketing under its TUA, we may need to obtain additional funding. If we fail to obtain sufficient funding and we fail to complete Phase 1, our business plan could fail. If Phase 1 is satisfactorily completed but funding is not sufficient for completion of Phase 2 – Stage 1, we will be entitled to receive payments under the TUAs, including the Cheniere Marketing TUA, but Cheniere Marketing may not have access to regasification capacity or other resources or business opportunities sufficient to generate cash flow to fund its required payments to us under the Cheniere Marketing TUA. This could cause Cheniere Marketing to default on its obligations, which could have a material adverse effect on our business, results of operations, financial condition and prospects.

Our ability to obtain debt or equity financing that may be needed to provide additional funding to cover increased costs will depend, in part, on factors beyond our control, such as the status of various capital and industry markets at the time financing is sought. Accordingly, we may not be able to obtain financing on terms that are acceptable to us, or at all. Even if we are able to obtain financing, we may have to accept terms that are disadvantageous to us or that may have a material adverse effect on our current or future business, results of operations, financial condition and prospects.

We are dependent on Bechtel and other contractors for the successful completion of our LNG receiving terminal.

We have no experience constructing LNG receiving terminals and limited experience working with EPC contractors, including Bechtel, and with other construction contractors. Timely and cost-effective completion of our LNG receiving terminal in compliance with agreed specifications is central to our business strategy and is highly dependent on our contractors’ performance under their agreements with us. Our contractors’ ability to perform successfully under their contracts is dependent on a number of factors, including their ability to:

| | • | | design and engineer our LNG receiving terminal to operate in accordance with specifications; |

| | • | | engage and retain third-party subcontractors and procure equipment and supplies; |

| | • | | respond to difficulties such as equipment failure, delivery delays, schedule changes and failure to perform by subcontractors, some of which are beyond their control; |

| | • | | attract, develop and retain skilled personnel, including engineers; |

| | • | | post required construction bonds and comply with the terms thereof; |

| | • | | manage the construction process generally, including coordinating with other contractors and regulatory agencies; and |

| | • | | maintain their own financial condition, including adequate working capital. |

These risks are heightened for Phase 2 – Stage 1, which is still in the contracting phase. A substantial number of contracts, such as for performing portions of or supplying materials for Phase 2 – Stage 1, remain to

18

be negotiated for Phase 2 – Stage 1, and we may be unable to reach satisfactory arrangements for these contracts. As a result, the scope, design, timing and cost for Phase 2 – Stage 1 construction are not as well defined as they are for Phase 1, and therefore the risk of delays, cost overruns or non-completion is greater for Phase 2 – Stage 1 than for Phase 1.

Although some of our EPC contracts provide for liquidated damages, if the contractor fails to perform in the manner required with respect to certain of its obligations, the events that trigger a requirement to pay liquidated damages may delay or impair the operation of our LNG receiving terminal, and any liquidated damages that we receive may not be sufficient to cover the damages that we suffer as a result of any such delay or impairment. In addition, each contractor’s liability for liquidated damages is subject to a cap. Each of our material agreements with contractors is also subject to termination by the contractor prior to completion of construction under certain circumstances, including extended delays (of 100 days or more) caused byforce majeure events and our insolvency, breach of material obligations not subject to adjustment by change order, or failure to pay undisputed amounts. Please read “Description of Principal Project Documents” for further information.

Furthermore, we may have disagreements with our contractors about different elements of the construction process, which could lead to the assertion of rights and remedies under their contracts and increase the cost of the project or result in a contractor’s unwillingness to perform further work on the project. If any contractor is unable or unwilling to perform according to the negotiated terms and timetable of its respective agreement for any reason or terminates its agreement, we would be required to engage a substitute contractor. This would likely result in significant project delays and increased costs.

The failure of our contractors to perform under their contracts for any of the reasons described above may extend the date on which our TUA customers are required to begin making payments to us. This delay in payments could have a material adverse effect on our cash flows and results of operations and on our ability to make payments on the notes.

To commission our LNG receiving terminal, we must purchase and process LNG. We have not previously purchased or processed any LNG.

Our LNG receiving terminal must undergo a commissioning process for our storage tanks and other equipment before commencement of commercial operation. The commissioning process will require a substantial quantity of LNG as well as access to adequate LNG tankers to deliver the LNG.

Our construction cost estimates do not include the costs of acquiring this LNG (other than a minor portion we refer to as “heel” LNG) at our LNG receiving terminal, which we have projected will be approximately $157.5 million. Our actual cost to obtain LNG for the commissioning process could exceed our estimates, and the overrun could be significant.

We face several principal risks associated with this required purchase of LNG, including the following:

| | • | | we may be unable to enter into a contract for the purchase of the LNG needed for commissioning and may be unable to obtain tankers to deliver such LNG on terms reasonably acceptable to us or at all. Although we expect to contract with Cheniere Marketing to provide the LNG and the tankers, we have not negotiated any such contract at this time with Cheniere Marketing or any other third party; |

| | • | | we will bear the commodity price risk associated with purchasing the LNG, holding it in inventory for a period of time and selling the regasified LNG; and |

| | • | | we may be unable to obtain financing for the purchase and shipment of the LNG on terms that are reasonably acceptable to it or at all. |

Our failure to obtain LNG, tankers or both, or our inability to finance the purchase of LNG needed for commissioning, would impede commencement of commercial operation at our LNG receiving terminal, which

19

could delay the date on which our TUA customers are required to begin making payments to us. This delay in payments could have a material adverse effect on our business, results of operations, financial condition and prospects.

To commissionour LNG receiving terminal,we must obtain natural gas pipeline transportation access. The required pipeline infrastructure is under development by a Cheniere entity but has not yet been constructed.

The commissioning process for our LNG receiving terminal is dependent upon completion of pipeline infrastructure to supply natural gas for power generation units prior to delivery of cool down LNG and to take away natural gas produced in the commissioning process. We expect to obtain access to the natural gas required for the commissioning process from a four-inch diameter pipeline, approximately 5,000 feet in length, that we will construct from our LNG receiving terminal to a third-party pipeline. This pipeline infrastructure has not been constructed, and its timely completion is subject to numerous risks, such as weather delays, accidents and inability to obtain required rights-of-way and governmental approvals.

Failure to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the development of our LNG receiving terminal or related pipeline infrastructure could impede completion and have a material adverse effect on us.

The design, construction and operation of LNG receiving terminals are all highly regulated activities. The FERC’s approval under Section 3 of the Natural Gas Act of 1938, or NGA, as well as several other material governmental and regulatory approvals and permits, are required in order to construct and operate our LNG receiving terminal. Although we have obtained NGA Section 3 authorization to construct and operate our LNG receiving terminal, such authorization is subject to ongoing conditions imposed by the FERC. We also have not obtained several other material governmental and regulatory approvals and permits required in order to construct and operate Phase 2 – Stage 1 of our LNG receiving terminal, and third parties have not obtained approvals and permits to develop related pipeline infrastructure, including several under the Clean Air Act and the Clean Water Act from the U.S. Army Corps of Engineers and the Louisiana Department of Environmental Quality. We have no control over the outcome of the review and approval process. We do not know whether or when any such approvals or permits can be obtained, or whether or not any existing or potential interventions or other actions by third parties will interfere with our ability to obtain and maintain such permits or approvals. Failure to obtain and maintain any of these approvals and permits could have a material adverse effect on our business, results of operations, financial condition and prospects.

Hurricanes or other disasters could result in a delay in the completion of our LNG receiving terminal, higher construction costs and the deferral of the dates on which our TUA counterparties are obligated to begin making payments to us.

In August and September of 2005, Hurricanes Katrina and Rita and related storm activity, including windstorms, storm surges, floods and tornadoes, caused extensive and catastrophic damage to coastal and inland areas located in the Gulf Coast region of the U.S. (parts of Texas, Louisiana, Mississippi and Alabama) and certain other parts of the southeastern U.S. Construction at our LNG receiving terminal site was temporarily suspended in connection with Hurricane Katrina, as a precautionary measure. Approximately three weeks after the occurrence of Hurricane Katrina, the terminal site was again secured and evacuated in anticipation of Hurricane Rita, the eye of which made landfall to the east of the site. As a result of these 2005 storms and related matters, our LNG receiving terminal experienced construction delays and increased costs totaling approximately $36.0 million.

Future similar storms and related storm activity and collateral effects, or other disasters such as explosions, fires, floods or accidents, could result in damage to, delays or cost increases in construction of, or interruption of operations at, our LNG receiving terminal or related infrastructure.

20

Risks Relating to Development and Operation of our Business

We are a development stage company without any revenues, operating cash flows, operating history or experience constructing, operating or maintaining an LNG facility, and if we are unable to complete construction of our LNG receiving terminal or if our customers fail to perform under their contracts for whatever reason, our business will be materially and adversely affected and we may not be able to make payments on the notes.

We are a development stage company with no revenues, operating cash flows or operating history. We have had net losses of $85.3 million for the period from inception through March 31, 2007. We expect to continue to incur losses and experience negative operating cash flow through 2008 and to incur significant capital expenditures through completion of development of our LNG receiving terminal. Any delays beyond the expected development periods for our LNG receiving terminal would prolong, and could increase the level of, our operating losses and negative operating cash flows. Neither we nor Cheniere and its affiliates have ever managed the construction, operation or maintenance of an LNG facility.

We will be entirely dependent on Cheniere, including employees of Cheniere and its subsidiaries, for key personnel, and a loss of key personnel could have a material adverse effect on our business.

As of March 31, 2007, Cheniere and its subsidiaries had approximately 290 full-time employees, who, for the most part, were focused on the development of three LNG receiving terminals and other complementary businesses. As construction of our LNG receiving terminal progresses, we will have to hire or otherwise arrange with Cheniere affiliates for new onsite employees to manage the facility, which will increase the personnel needed to operate the facility from 34 as of March 31, 2007 to 65 in the first quarter of 2008, at an estimated annual cost of approximately $5.3 million. We will rely to a significant extent on the new personnel that we hire or otherwise arrange to perform these functions. As our operations expand, our general partner and other Cheniere subsidiaries will also have to expand their administrative staffs. If our general partner is not able to successfully manage the expansion of our business, our business, results of operations, financial condition and prospects could be materially adversely affected.

Our general partner’s executive officers are also officers of Cheniere and its affiliates. We do not maintain key person life insurance policies on any personnel. Although Cheniere has arranged agreements relating to compensation and benefits with certain of our general partner’s executive officers, our general partner does not have any employment contracts or other agreements with key personnel binding them to provide services for any particular term. The loss of the services of any of these individuals, including Messrs. Horton, Little and Turkleson, could have a material adverse effect on our business. In addition, our future success will depend in part on our general partner’s ability to engage, and Cheniere’s ability to attract and retain, additional qualified personnel.

We will have numerous contractual and commercial relationships, and conflicts of interest, with Cheniere and its affiliates, including Cheniere Marketing.

We have agreements to compensate and to reimburse expenses of affiliates of Cheniere. In addition, we have entered into a TUA with Cheniere Marketing, under which Cheniere Marketing will be able to derive substantially all of the economic benefits that may be generated by our LNG receiving facility beyond the payments to be received by us under our TUAs. Under its TUA, Cheniere Marketing may also require us to build a sixth LNG storage tank within four years after notification from Cheniere Marketing, provided that, among other things, we can obtain financing we consider to be reasonably acceptable. All of these agreements involve conflicts of interest between us, on the one hand, and Cheniere and its other affiliates, on the other hand.

We expect that there will be additional agreements or arrangements with Cheniere and its affiliates, including future interconnection and gas balancing agreements with one or more Cheniere-affiliated natural gas pipelines as well as other agreements and arrangements that cannot now be anticipated. In those circumstances

21

where additional contracts with Cheniere and its affiliates may be necessary or desirable, additional conflicts of interest will be involved.

The interests of Cheniere could conflict with your interest. For example, if we encounter financial difficulties or are unable to pay our debts as they mature, the interests of Cheniere, as an equity holder, might conflict with your interests as a noteholder.

We will be dependent for substantially all of our revenues and cash flows on the TUA counterparties. Cheniere Marketing has a limited operating history, limited capital, no credit rating and an unproven business strategy and may not be able to make payments to us under its TUA.

We will be dependent on the Chevron, Total and Cheniere Marketing TUAs for operating revenues and cash flows. Each of Chevron and Total will pay approximately $125 million annually when payments under those contracts commence, and Cheniere Marketing will pay approximately $250 million annually commencing in 2009. We are also exposed to the credit risk of the guarantors of our customers’ obligations under the TUAs in the event that we must seek recourse under a guaranty.

Cheniere Marketing has a limited operating history, limited capital, no credit rating and an unproven business strategy. Cheniere Marketing has no credit rating, and Cheniere has a non-investment grade corporate rating of B from Standard and Poor’s, indicating that Cheniere Marketing and Cheniere have a higher risk of being financially unable to perform on the Cheniere Marketing TUA than either Chevron or Total have with respect to their TUAs. Although each of our TUA counterparties faces a risk that it will not be able to enter into commercial arrangements for the use of its capacity at our LNG receiving terminal to support the payment of its obligations under its TUA, due to negative developments in the LNG industry or for other reasons, that risk is greater for Cheniere Marketing than for Total and Chevron. The principal risks attendant to Cheniere Marketing’s future ability to generate operating cash flow to support its TUA obligations include the following:

| | • | | Cheniere Marketing does not have unconditional agreements or arrangements for any supplies of LNG, for any vessels to transport LNG or for the utilization of capacity that it has contracted for under its TUA with us and may not be able to obtain such agreements or arrangements on economical terms, or at all; |