JPMorgan Annual High Yield Conference 2007 JPMorgan Annual High Yield Conference 2007 January 23, 2007 Miami Beach Investor & Public Relations: Norelle Lundy, Vice President Hillarie Forister, Senior Analyst (713) 507-6466 ir@dynegy.com Exhibit 99.1 Filed by Dynegy Acquisition, Inc. Pursuant to Rule 425 of the Securities Act of 1933, as amended, and deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934, as amended Subject Company: Dynegy Inc. Commission File No: 001-15659 |

2 FORWARD-LOOKING STATEMENTS FORWARD-LOOKING STATEMENTS This presentation contains statements reflecting assumptions, expectations, projections, intentions or beliefs about future events that are intended as “forward- looking statements.” You can identify these statements, including those relating to Dynegy’s 2007 financial estimates, by the fact that they do not relate strictly to historical or current facts. Management cautions that any or all of Dynegy’s forward-looking statements may turn out to be wrong. Please read Dynegy’s annual, quarterly and current reports under the Securities Exchange Act of 1934, including its 2005 Form 10-K, as amended, and first, second and third quarter 2006 Form 10-Qs for additional information about the risks, uncertainties and other factors affecting these forward-looking statements and Dynegy generally. Dynegy’s actual future results may vary materially from those expressed or implied in any forward-looking statements. All of Dynegy’s forward-looking statements, whether written or oral, are expressly qualified by these cautionary statements and any other cautionary statements that may accompany such forward-looking statements. In addition, Dynegy disclaims any obligation to update any forward-looking statements to reflect events or circumstances after the date hereof. In connection with the LS Power transaction announced on September 15, 2006, Dynegy has filed a preliminary proxy statement/prospectus, as amended, with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO CAREFULLY READ THE IMPORTANT INFORMATION CONTAINED IN THE MATERIALS REGARDING THE PROPOSED TRANSACTION. THEY CONTAIN IMPORTANT INFORMATION ABOUT DYNEGY, LS POWER, THE NEW COMPANY AND THE PROPOSED TRANSACTION. Investors and security holders may obtain a copy of the preliminary proxy statement/prospectus, as amended, and other documents containing information about Dynegy and LS Power, free of charge, at the SEC’s web site at www.sec.gov and at Dynegy’s web site at www.dynegy.com. Copies of the preliminary proxy statement/prospectus, as amended, may also be obtained by writing Dynegy Inc. Investor Relations, 1000 Louisiana Street, Suite 5800, Houston, Texas 77002 or by calling 713-507-6466. Dynegy, LS Power and their respective directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies from Dynegy’s shareholders with respect to the proposed transaction. Information regarding Dynegy’s directors and executive officers is available in the company’s proxy statement for its 2006 Annual Meeting of Shareholders, dated April 3, 2006. Additional information regarding the interests of such potential participants is included in the preliminary proxy statement/prospectus, as amended, and other relevant documents filed with the SEC. Non-GAAP Financial Measures: We use the non-GAAP financial measures “EBITDA,” “free cash flow” and “free cash flow per share” in these materials. EBITDA is a non-GAAP financial measure. Consolidated EBITDA can be reconciled to Net income (loss) using the following calculation: Net income (loss) less Income tax benefit (expense), plus Interest expense and Depreciation and amortization expense equals EBITDA. Management and some members of the investment community utilize EBITDA to measure financial performance on an ongoing basis. However, EBITDA should not be used in lieu of GAAP measures such as net income and cash flow from operations. Free cash flow is a non-GAAP financial measure. Free cash flow can be reconciled to operating cash flow using the following calculation: Operating cash flow plus investing cash flow (consisting of asset sale proceeds less business acquisition costs, capital expenditures and changes in restricted cash) equals free cash flow. We use free cash flow to measure the cash generating ability of our operating asset-based energy business relative to our capital expenditure obligations. Free cash flow should not be used in lieu of GAAP measures with respect to cash flows and should not be interpreted as available for discretionary expenditures, as mandatory expenditures such as debt obligations are not deducted from the measure. Free cash flow per share is also a non-GAAP financial measure. Free cash flow per share can be reconciled to operating cash flow using the following calculation: Operating cash flow plus investing cash flow (consisting of asset sale proceeds less business acquisition costs, capital expenditures and changes in restricted cash) equals free cash flow, and free cash flow divided by the weighted-average number of shares of common stock outstanding during the period equals free cash flow per share. We use free cash flow per share to determine whether the cash generating ability of our operating asset-based energy business has improved period over period, relative to our capital expenditure obligations. Free cash flow per share should not be used in lieu of GAAP measures with respect to cash flows and should not be interpreted as an amount that is available for the direct benefit of our shareholders. |

3 LS POWER COMBINATION OVERVIEW LS POWER COMBINATION OVERVIEW ACCRETION Significant accretion to 2007 free cash flow metrics compared to Dynegy stand-alone GROWTH Consolidation benefits Development joint venture STABILITY Greater stability through diversity of geography, fuel, dispatch and sales strategy Diversification with Significant Scale and Scope in Key Regions Diversification with Significant Scale and Scope in Key Regions Dynegy baseload coal: Strong cash flow + Dynegy peaking: Significant leverage in market recovery Dynegy baseload coal: Strong cash flow + Dynegy peaking: Significant leverage in market recovery LS Power intermediate combined cycle gas: Contracted cash flow with market recovery upside LS Power intermediate combined cycle gas: Contracted cash flow with market recovery upside |

4 INTEGRATION UPDATE INTEGRATION UPDATE Continued focus on: Enhancing flexibility, Minimizing costs, Protecting credit ratings, Optimizing portfolio Continued focus on: Enhancing flexibility, Minimizing costs, Protecting credit ratings, Optimizing portfolio Expiration of Hart-Scott-Rodino waiting period Filing of preliminary proxy statement/prospectus with SEC Presentation of 2007 combined company cash flow and earnings estimates Receipt of New York Public Service Commission approval Receipt of FERC approval Pending: Proxy statement and prospectus effective with the SEC and mailed to shareholders Pending: Special shareholder meeting and affirmative vote by holders of at least 2/3 of Dynegy’s Class A shares Pending: Transaction closing On track for transaction closing at end 1Q 2007 |

5 NEW DYNEGY’S BUSINESS STRUCTURE AND KEY FINANCIAL METRICS NEW DYNEGY’S BUSINESS STRUCTURE AND KEY FINANCIAL METRICS Baseload coal, combined cycle gas and gas-fired peakers MISO and PJM Baseload coal, combined cycle gas and dual-fuel NYISO and ISO-NE Midwest 9,495 MW West 6,740 MW Northeast 3,809 MW Other Combined cycle gas and gas-fired peakers West (CAISO, Meade, Palo Verde) and ERCOT G&A Development portfolio CRM Note: 2007 cash flow and earnings estimates are as presented 12/13/06. All indicated 2007 estimates include results of the combined enterprise after an assumed closing of the LS Power transaction expected at the end of 1Q 2007. The LS Power transaction remains subject to certain regulatory and shareholder approvals, the receipt of which cannot be guaranteed. 2007E OCF: $600-700 MM 2007E FCF: $415-515 MM 2007E EBITDA Mid-Point: ~$1.1 B 2007E Net Income: $190-255 MM 2007E EBITDA of $745-795 MM 2007E EBITDA of $215-235 MM 2007E EBITDA of $175-205 MM 2007E EBITDA of ($115-105) MM Cash Flow Measures Earnings Measures |

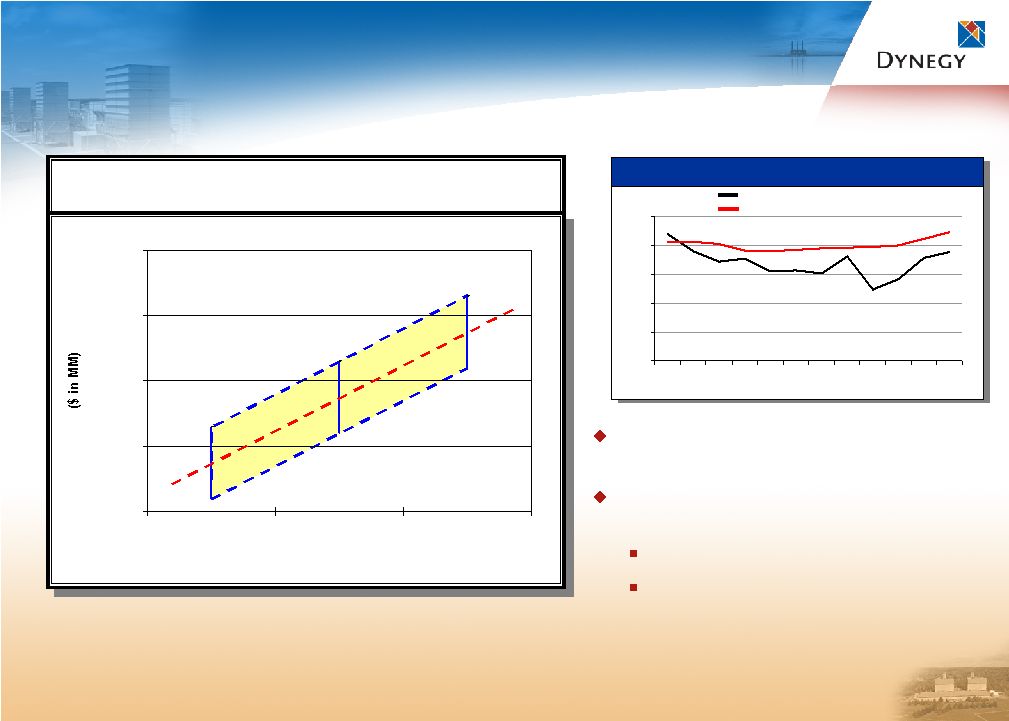

6 ACCRETION: INCREASED FREE CASH FLOW ACCRETION: INCREASED FREE CASH FLOW Dynegy-LS Power combination is accretive to 2007 free cash flow metrics Note: 2007 cash flow and earnings estimates are as presented 12/13/06. (1) Based on full-year estimates for existing Dynegy assets and 9 months of estimates for LS Power assets beginning 4/01/07. (2) Excludes free cash flow of $200-500 MM related to proceeds from potential Dynegy asset sales and $145 MM of LS Power cash consideration and transaction costs included in estimates as presented 12/13/06. (3) Calculated based on 500 MM shares outstanding for Dynegy stand-alone and 755 MM weighted-average shares outstanding for New Dynegy. (4) Full-year LS Power EBITDA estimates of $305-365 MM differ from previous full-year EBITDA estimates of $360-$400 MM as presented 9/15/06 primarily due to accounting treatment of financial contracts. EBITDA (1) Free Cash Flow (1)(2) Free Cash Flow Per Share (2)(3) Dynegy Stand-Alone New Dynegy $770- 830 MM $770- 830 MM $250- 300 MM $250- 300 MM $180- 230 MM $180- 230 MM $180- 230 MM $180- 230 MM $0.48- 0.61 $0.48- 0.61 $0.36- 0.46 $0.36- 0.46 LS Power Free Cash Flow Accretion Accretion 9 Months 1Q 2007 $250-300 MM $55 - 65 MM $305-365 MM (4) FY 2007E LS Power |

7 GROWTH THROUGH CONSOLIDATION BENEFITS FOR INVESTORS GROWTH THROUGH CONSOLIDATION BENEFITS FOR INVESTORS Greater scale and scope without proportionate increase in costs Greater scale and scope without proportionate increase in costs New Dynegy’s competitive position enhanced through more assets under management Note: G&A estimates are as presented 12/13/06. (1) Excludes $55 MM pre-tax legal and settlement charges recorded in G&A. (2) Based on full-year estimates for Dynegy and 9 months of estimates for LS Power beginning 4/01/07, including certain acquisition-related expenditures. 0 5,000 10,000 15,000 20,000 25,000 Megawatts Estimated G&A ($ in MM) 2007 2006 $140 (1) $160 (2) 11,739 20,044 Megawatts increase 71%, while G&A up only 14% Megawatts increase 71%, while G&A up only 14% |

8 Combined portfolio is much less sensitive to commodity price changes New Dynegy expects to enter 2007 with approximately 50% of its estimated gross margin (3) contracted under forward sales commitments, which include: New Dynegy will actively manage forward sales commitments in response to market conditions GREATER STABILITY FOR INVESTORS GREATER STABILITY FOR INVESTORS (1) Percentage change for Dynegy calculated based on Generation EBITDA estimates of a range of $475-505 MM as presented 11/08/06. (2) Percentage change for New Dynegy calculated based on Generation EBITDA estimates of a range of $1,135-1,235 MM as presented 12/13/06. (3) Gross margin equals revenues less fuel and emission costs. Illinois auction sales (up to 1,400 MW) RMR contracts (approximately 1,400 MW in CA and CT) Tolling arrangements (approximately 3,000 MW in AZ, CA, and IL) Bilateral agreements for capacity and energy sales Financial forward sales contracts (including approximately 2,350 MW related to the LS assets) (1) (2) Dynegy New Dynegy Given +/- $1.00 MMBtu Gas +/- ~10% EBITDA +/- ~4% EBITDA Generation EBITDA Sensitivity |

9 2007 TOTAL EARNINGS SENSITIVITY TO NATURAL GAS 2007 TOTAL EARNINGS SENSITIVITY TO NATURAL GAS Full-year 2007 average natural gas price as of 11/01/06 = $8.05/MMBtu (Henry Hub) +/- $1/MMBtu change in natural gas is approximately equal to: +/- ~4% change (3) in generation EBITDA +/- ~$50 MM change in generation EBITDA Note: 2007 earnings estimates are as presented 12/13/06. EBITDA based on full-year estimates for existing Dynegy assets and 9 months of estimates for LS Power assets beginning 4/01/07. (1) Pricing as of 11/01/06. Prices reflect actual day ahead settlement prices for Jan. – Oct. and quoted forward monthly prices for Nov. – Dec. 2006. (2) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. (3) Percentage change calculated based on Generation EBITDA estimates of a range of $1,135-1,235 MM as presented 12/13/06. Expected 2007 Total EBITDA Ranges Given $/MMBtu Cost of Natural Gas (12-Month Average $/MMBtu) $900 $1,000 $1,100 $1,200 $1,300 $6.00 Gas $8.00 Gas $10.00 Gas $920 $1,030 $975 $1,020 $1,130 $1,120 $1,230 $1,175 $1,075 $0 $2 $4 $6 $8 $10 J F M A M J J A S O N D 2006A/F: $6.79 2007F: $8.05 ($/MMBtu) Natural Gas 2006 Actual/Forward as of 11/01/06 (1) 2007 Forward as of 11/01/06 (2) -- OR -- |

10 MAJOR MIDWEST ENVIRONMENTAL CAPITAL SPENDING MAJOR MIDWEST ENVIRONMENTAL CAPITAL SPENDING Historical capital expenditures made from 1998 to 2006 in connection with our efforts to achieve regulatory requirements totaled approximately $545 MM ~$280 MM for completion of PRB conversions at four Midwest facilities (Baldwin, Havana, Hennepin and Wood River) ~$210 MM for all other regulatory capital ~$55 MM for Consent Decree, including $25 MM for Vermilion PRB conversion Investments to date have resulted in 88% and 87% reduction in SO and NO x , respectively, while increasing production 22% Future capital expenditures related to the Consent Decree will vary, but risks are being mitigated with respect to: Labor (60% of Consent Decree cost) – Negotiating contract agreements for project construction, including consecutive staging of projects to retain labor force Materials (35% of Consent Decree cost) – Competitive contracts with several suppliers, with escalation rates built into contracts Engineering/Technology (5% of Consent Decree cost) – Using standardized designs and technology to minimize customization The multi-pollutant standard under the Illinois Mercury Rule is expected to reduce mercury emissions 90% by 2015 and provide for further reduction in SO NO x and particulate matter Dynegy in advanced position to meet all applicable regulatory requirements 1998-2006 2007 2008 2009 2010 2011 2012 TOTAL Consent Decree (1) 55 $ 90 $ 125 $ 150 $ 140 $ 85 $ 30 $ 675 $ Regulatory Capital 490 - - - - - - 490 Illinois Mercury (2) - - - 20 - - 5 25 Total 545 $ 90 $ 125 $ 170 $ 140 $ 85 $ 35 $ 1,190 $ Note: Actual capital expenditures may vary materially from these estimates, which may not be updated to reflect future changes. (1) Amounts presented are based on assumptions as of November 2006 and are intended solely as estimates for capital expenditures related to the Consent Decree. (2) Expected capital expenditures related to the Illinois Mercury Rule also include $50 MM and $45 MM in 2013 and 2014, respectively. 2, 2 |

11 VALUE PROPOSITION VALUE PROPOSITION Near-Term Near-Term Value Value Medium-Term Medium-Term Value Value Long-Term Long-Term Value Value Accretion through increased free cash flow More predictability with lower volatility Greater fuel, dispatch and geographic diversity in key regions Increased scale with minimal incremental costs Experienced development team Scaleable platform for future sector consolidation ENHANCED SCALE ENHANCED SCALE FUTURE GROWTH FUTURE GROWTH FINANCIAL STABILITY FINANCIAL STABILITY 1. Complete integration: Be “Day 1 Ready” 2. “Right-hand” side of balance sheet: Enhance flexibility, minimize costs and protect credit ratings 3. “Left-hand” side of balance sheet: Monetize selected assets |

Appendix |

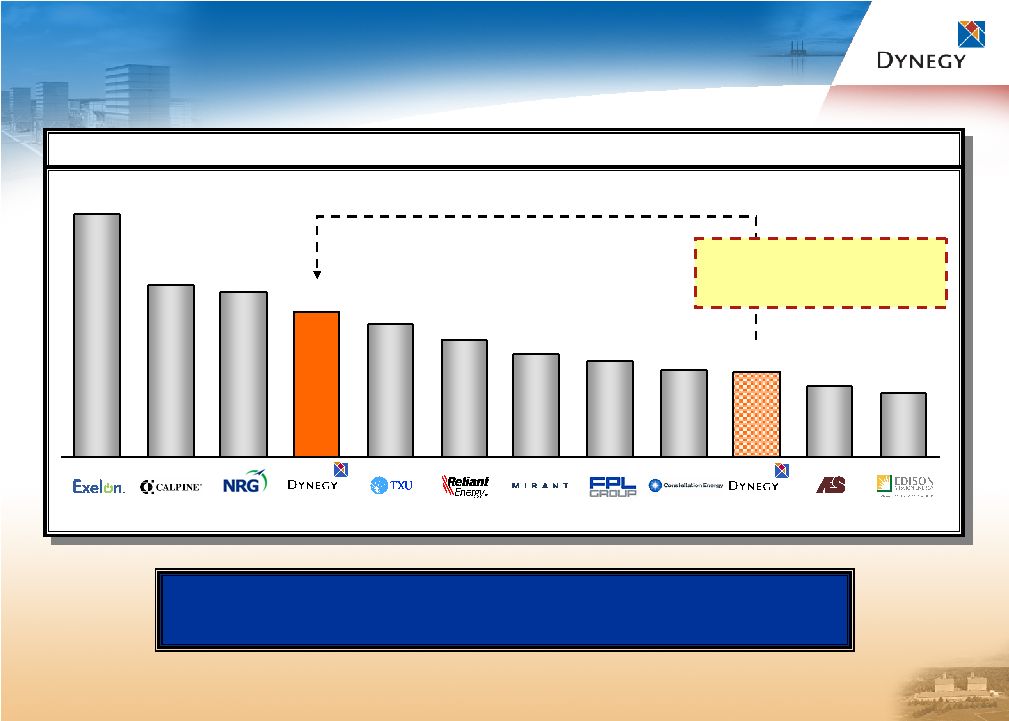

13 U.S. Unregulated Generation (Net MW) A TOP TIER MERCHANT GENERATOR A TOP TIER MERCHANT GENERATOR Note: Excludes announced development programs and potential divestitures. Increased scale and scope significantly enhances competitive position of our power generation business More sources of earnings and value without substantial cost increases More sources of earnings and value without substantial cost increases 11,739 9,749 8,834 22,584 20,044 18,300 13,158 15,934 33,290 23,676 11,856 Pro Forma 14,161 |

14 NEW DYNEGY PORTFOLIO NEW DYNEGY PORTFOLIO Scale and scope in key regions Primary Fuel Type Nameplate Capacity (MW) More than 900 MW 500 MW to 900 MW 150 MW to 500 MW Less than 150 MW LS Power - Operating Coal Gas Gas/Oil Wind LS Power - Development Dynegy Inc. Midwest 9,495 MW Northeast 3,809 MW Transmission Total 20,044 MW West 6,740 MW Note: Plum Point 1 currently under construction. MW totals exclude development and repowerings. |

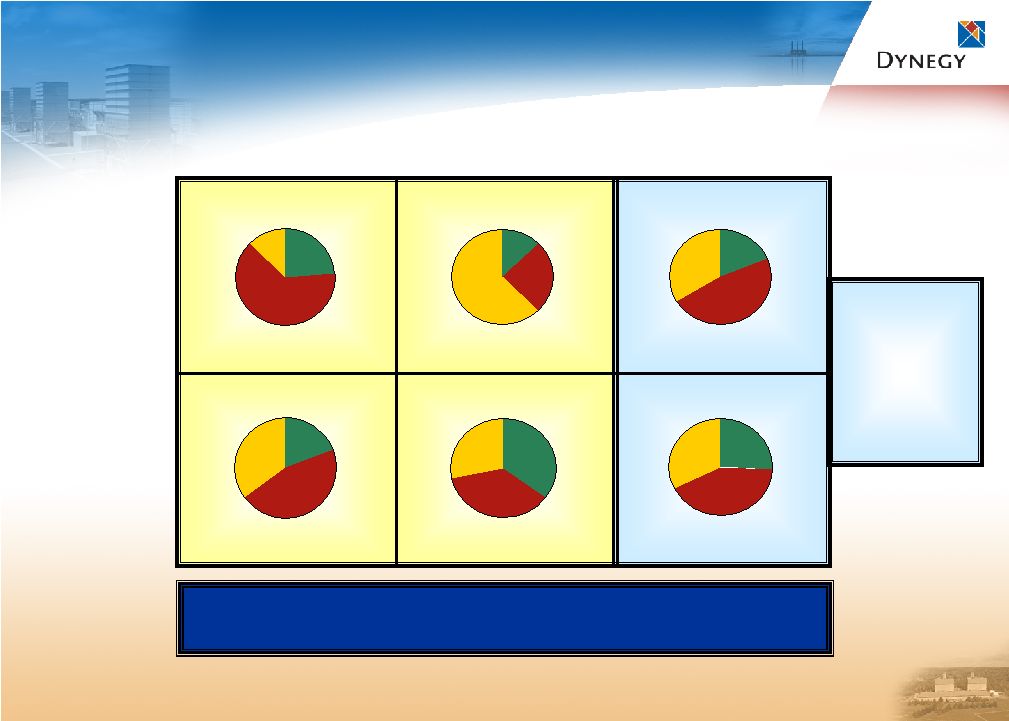

15 DIVERSIFIED AND BALANCED PORTFOLIO DIVERSIFIED AND BALANCED PORTFOLIO Northeast 23.4% Midwest 63.4% West 13.2% Northeast 12.9% Midwest 24.6% West 62.5% Northeast 19.0% Midwest 47.4% West 33.6% Intermediate 19.2% Peaking 45.3% Baseload 35.5% Intermediate 25.8% Peaking 41.7% Baseload 32.5% Peaking 36.5% Baseload 28.3% Intermediate 35.2% Fuel Diversity Coal/Oil 20.9% Dual Fuel 6.5% Gas - CCGT 33.4% Gas - Simple Cycle 39.2% Portfolio diversified through geographic locations, fuel and dispatch types Dynegy Capacity LS Power Capacity Combined Capacity Geographic Diversity Dispatch Diversity |

16 2007 COMMODITY PRICING ASSUMPTIONS AS OF 11/01/06 2007 COMMODITY PRICING ASSUMPTIONS AS OF 11/01/06 (1) Represents annual average. 2007E (1) Natural Gas - Henry Hub ($/MMBtu) 8.05 $ On-Peak Power ($/MWh) NI Hub/ComEd 58.00 $ PJM 73.00 $ Cinergy 59.00 $ NY - Zone G 89.00 $ NE - Mass 86.00 $ ERCOT 75.00 $ NP-15 75.00 $ West - PV 69.00 $ Coal ($/MMBtu) PRB Delivered to Baldwin 1.35 $ South American Delivered to Northeast 2.90 $ Fuel Oil #6 Delivered to Northeast ($/MMBtu) 8.85 $ Plant Heat Rates - Summertime (Btu/Net kWh) Midwest & New York Coal 10,000-12,000 Intermediate (CA, NV, NY) 9,500-11,000 Combined Cycle (AZ, CA, CT, IL, ME, NY, PA, TX) 7,000-8,200 Midwest & Southeast Peakers 9,500-12,000 Applicable Facilities Midwest Coal and Kendall Ontelaunee Moss Landing, Oakland Arlington Valley, Griffith Midwest Peakers Roseton, Danskammer Lyondell Bridgeport, Casco Bay |

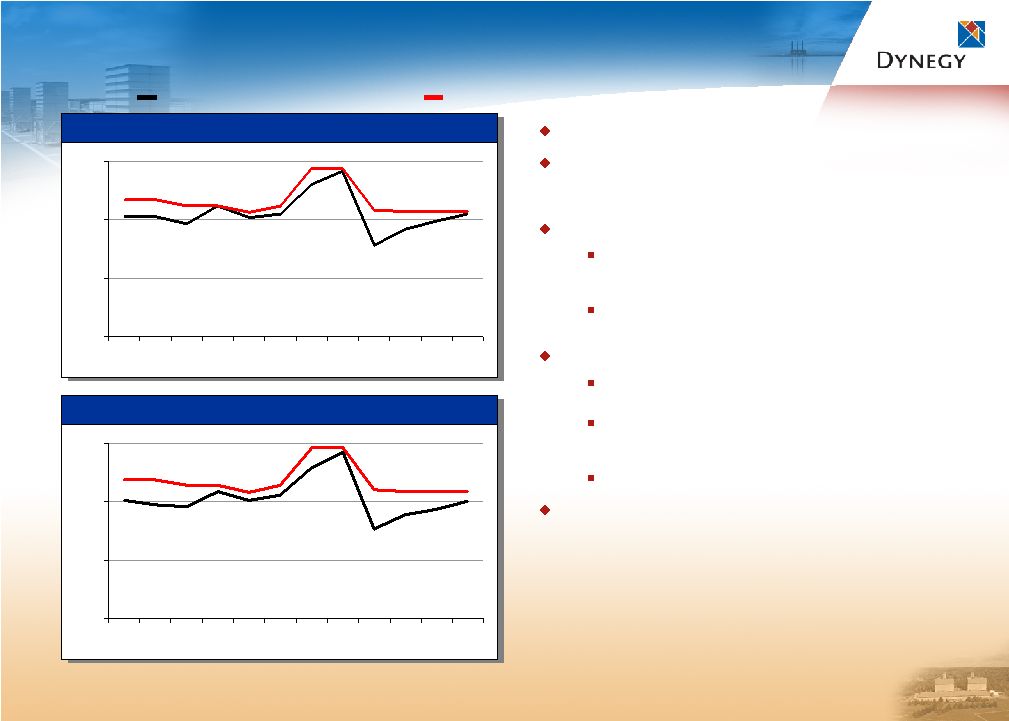

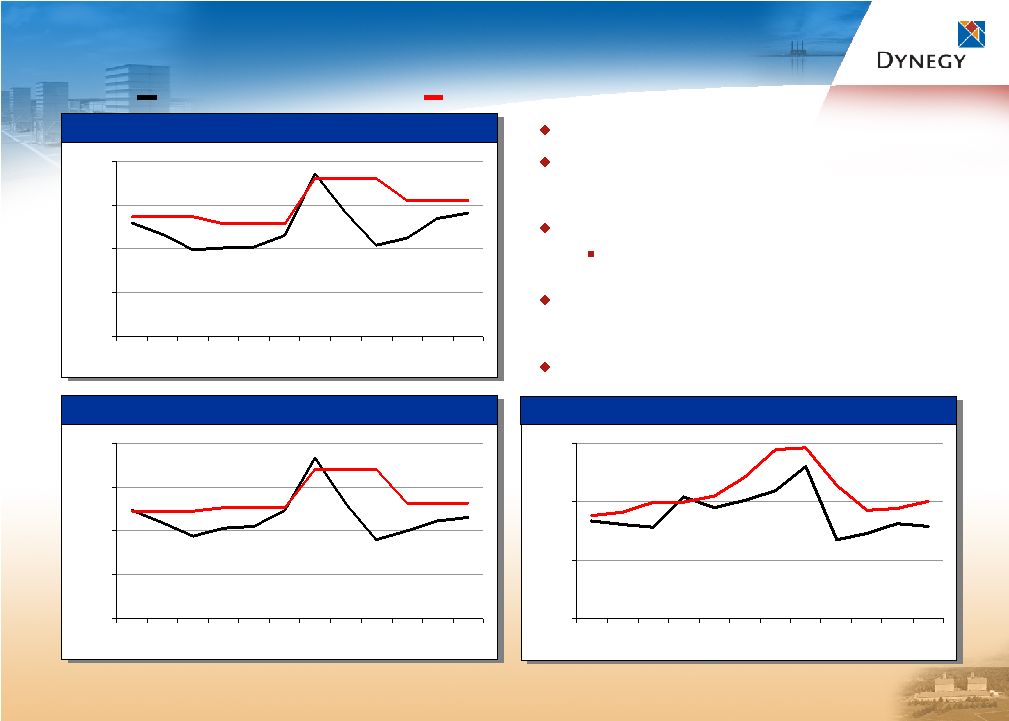

17 $0 $25 $50 $75 J F M A M J J A S O N D 2006A/F: $52.75 MIDWEST GENERATION: 2007 MIDWEST GENERATION: 2007 ($/MWh) 2006 Actual/Forward as of 11/01/06 (1) 2007 Forward as of 11/01/06 (2) $0 $25 $50 $75 J F M A M J J A S O N D NI Hub/ComEd 2007F: $58.04 Cinergy 2006A/F: $51.66 2007F: $59.04 Note: 2007 estimates are as presented 12/13/06. (1) Pricing as of 11/01/06. Prices reflect actual day ahead on-peak settlement prices for Jan.-Oct. and quoted forward on-peak monthly prices for Nov.-Dec. 2006. (2) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. 2007E sales volumes of 26-27 MM MWh EBITDA of $745-795 MM includes Illinois auction, bilateral and tolling agreements and financial forward sales contracts Primary market drivers include: MISO – Outright power price for uncontracted baseload volumes, and spark spread for gas-fired peaking units PJM – Spark spread for uncontracted gas-fired combined cycle units Long-term PRB coal and rail contracts Baldwin 2007E delivered price approximately $1.35/MMBtu Approximately 97% of coal requirements contracted through 2010, with 98% contracted at a fixed price through 2008 100% rail contracted through 2013 In-market availability assumed to be 90% |

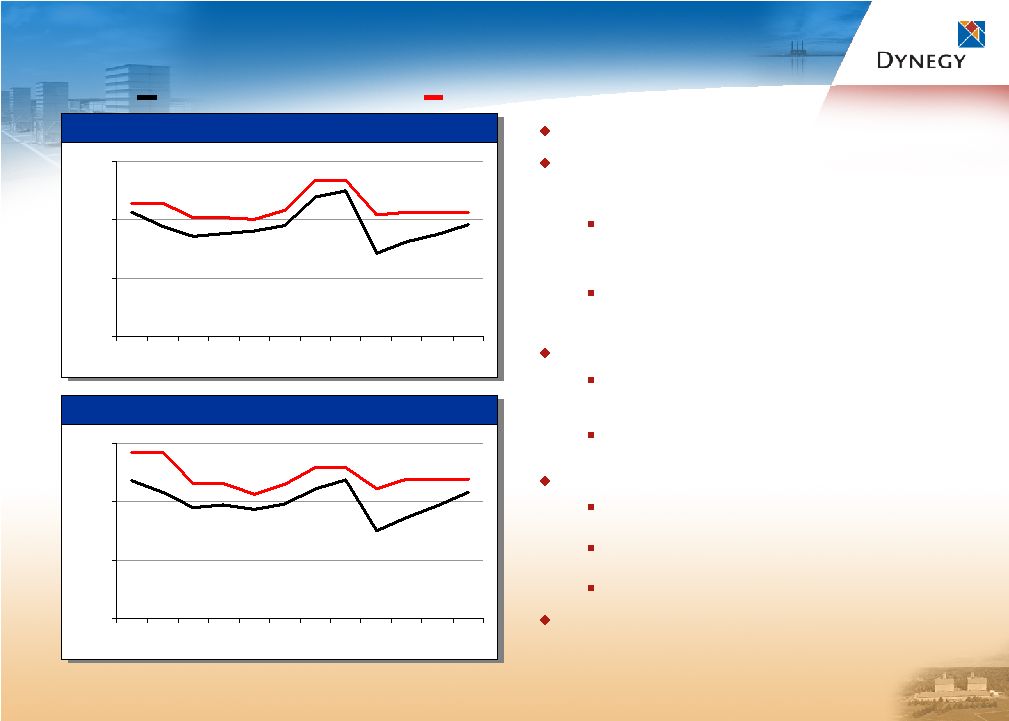

18 NORTHEAST GENERATION: 2007 NORTHEAST GENERATION: 2007 2007E sales volumes of 10-11 MM MWh EBITDA of $175-205 MM includes RMR contracts, bilateral capacity agreements and financial forward sales contracts EBITDA includes approximately $50 MM of Central Hudson lease expense, which is classified as operating expense; cash flow includes cash payments of $108 MM in 2007 Operating income from ConEd contract reflects approximately $50 MM net earnings; however, cash flow includes cash receipt of approximately $100 MM Primary market drivers include: NYISO – Spark spread for uncontracted combined cycle gas and fuel oil units, and outright power price for uncontracted baseload coal volumes ISO-NE – Spark spread for uncontracted combined cycle gas units Fuel supply 2007E South American coal delivered price ~$2.90/MMBtu 100% coal supply contracted at fixed price through 2007, with diversified suppliers and load ports 2007E fuel oil delivered price ~$8.85/MMBtu In-market availability assumed to be 90% $0 $35 $70 $105 J F M A M J J A S O N D $0 $40 $80 $120 J F M A M J J A S O N D New York Zone G Mass Hub 2006A/F: $75.83 2007F: $88.75 2006A/F: $70.26 2007F: $85.60 ($/MWh) 2006 Actual/Forward as of 11/01/06 (1) 2007 Forward as of 11/01/06 (2) Note: 2007 estimates are as presented 12/13/06. (1) Pricing as of 11/01/06. Prices reflect actual day ahead on-peak settlement prices for Jan.-Oct. and quoted forward on-peak monthly prices for Nov.-Dec. 2006. (2) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. |

19 WEST GENERATION: 2007 WEST GENERATION: 2007 2007E sales volumes of 15-16 MM MWh EBITDA of $215-235 MM includes RMR and steam contracts, tolling agreements and financial forward sales contracts Primary market drivers include: Spark spread for uncontracted gas-fired combined cycle and peaking units, and ancillary services Fuel price risk generally passed through on hedges and tolling agreements or purchased as needed at index-related prices In-market availability assumed to be 90% $0 $25 $50 $75 $100 J F M A M J J A S O N D $0 $25 $50 $75 $100 J F M A M J J A S O N D NP-15 Palo Verde 2006A/F: $61.70 2007F: $75.13 2006A/F: $57.82 2007F: $68.88 ($/MWh) 2006 Actual/Forward as of 11/01/06 (1) 2007 Forward as of 11/01/06 (2) $0 $35 $70 $105 J F M A M J J A S O N D ERCOT 2006A/F: $63.15 2007F: $75.47 Note: 2007 estimates are as presented 12/13/06. (1) Pricing as of 11/01/06. Prices reflect actual day ahead on-peak settlement prices for Jan.-Oct. and quoted forward on-peak monthly prices for Nov.-Dec. 2006. (2) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. |

20 2007 CASH FLOW ESTIMATES: GAAP BASIS 2007 CASH FLOW ESTIMATES: GAAP BASIS Development capex related to Plum Point of $155 MM expected to be funded from Plum Point’s restricted cash Net proceeds from asset sales and acquisition includes $200 MM from potential generation asset sales, offset by $100 MM cash paid to LS Power and $45 MM expected transaction costs Other OCF includes all interest payments, including Sithe interest previously recorded in GEN, as well as Plum Point cash interest of $30 MM funded from Plum Point’s restricted cash Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 11/01/06 and assume closing of the LS Power transaction at end 1Q 2007. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Core business represents continuing operating results, excluding significant items. (1) Asset sale proceeds in the range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. As Presented December 13, 2006; Based on Price Curves as of November 1, 2006 ($ in millions) GEN OTHER 2007 Total GAAP OCF $ 1,170-1,260 $ (570-560) $ 600-700 GAAP ICF Capex - Maintenance (155) (15) (170) Capex - Consent Decree (90) - (90) Capex - Plum Point Development (155) - (155) Investment in Development Portfolio - (10) (10) Proceeds from Asset Sales and Acquisition Costs, Net (1) 200 (145) 55 Change in Restricted Cash 155 30 185 Free Cash Flow $ 415-515 Add Back: Acquisition Costs 145 Less: Proceeds from Asset Sales (1) (200) Free Cash Flow - Core Business $ 360-460 |

21 2007 EARNINGS ESTIMATES: GAAP BASIS 2007 EARNINGS ESTIMATES: GAAP BASIS Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 11/01/06 and assume closing of the LS Power transaction at end 1Q 2007, excluding purchase accounting adjustments. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Reduced 2007 and forward EBITDA or free cash flow could result from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges. (1) Calculated based on 755 MM weighted-average shares outstanding. Other includes G&A costs of approximately $160 MM, primarily offset by interest income Interest expense of $435 MM includes approximately $30 MM for Plum Point Estimates exclude purchase accounting adjustments to be recorded upon closing of LS Power transaction Earnings may be more volatile as many of the forward sales commitments associated with the LS Power portfolio are marked-to-market under GAAP, which may create variances between earnings and cash flows in certain periods As Presented December 13, 2006; Based on Price Curves as of November 1, 2006 ($ in millions) Midwest West Northeast Total GEN OTHER 2007 Total EBITDA Estimates $ 745-795 $ 215-235 $ 175-205 $ 1,135-1,235 $ (115-105) $ 1,020-1,130 Depreciation (180) (45) (40) (265) (15) (280) Interest (435) Tax Expense (115-160) Net Income Applicable to Common Shareholders - GAAP $ 190-255 Earnings Per Share (1) $ 0.25-0.34 |

22 2007 GENERAL ASSUMPTIONS 2007 GENERAL ASSUMPTIONS LS Power combination assumed to close end 1Q 2007 LS Power combination consideration includes: 340 MM shares of new Class B common stock issued to LS Power; pro forma shares outstanding will be approximately 840 MM $275 MM junior subordinated note issued to LS Power with intent to repay in 2007 $100 MM cash paid to LS Power $45 MM anticipated transaction costs LS Power combination liquidity sources: $100 MM cash on hand Revolver capacity expected to be increased $200 MM in proceeds expected from asset sales (1) Dynegy not expected to be a cash taxpayer through 2010 Effective tax rate of 38%, substantially absorbed by ~$750 MM NOL carryforwards (2) and ~$250 MM AMT credits (2) Note: 2007 estimates are as presented 12/13/06. (1) Asset sale proceeds in a range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. (2) Estimated balance as of 12/31/06. |

23 2007 CAPITAL PLAN 2007 CAPITAL PLAN Capital expenditures of approximately $415 MM includes: $155 MM for generation maintenance, including approximately $20 MM for ongoing environmental requirements; $90 MM for Midwest fleet Consent Decree; $15 MM of other capex, primarily related to IT spending; and $155 MM for construction of Plum Point expected to be funded with restricted cash under the Plum Point credit facility Midwest Northeast West Other TOTAL Maintenance (1) 165 $ 100 $ 80 $ 40 $ 35 $ 15 $ 170 $ Consent Decree (2) 20 35 90 - - - 90 Development 10 10 155 - - - 155 Total 195 $ 145 $ 325 $ 40 $ 35 $ 15 $ 415 $ 2005A 2006E 2007E 2005 2006 2007 2008 2009 2010 2011 2012 TOTAL Consent Decree (2) 20 $ 35 $ 90 $ 125 $ 150 $ 140 $ 85 $ 30 $ 675 $ Note: 2007 estimates are as presented 12/13/06. (1) Includes ongoing environmental expenditures. (2) Amounts presented are based on assumptions as of November 2006 and are intended solely as estimates for future capital expenditures related to the Consent Decree; actual amounts may vary materially from these estimates, which may not be updated to reflect future changes. |

24 GREENFIELD DEVELOPMENT GREENFIELD DEVELOPMENT More than 7,600 MW in various stages of power generation development Sandy Creek Long Leaf White Pine/ Egan Elk Run Plum Point Unit 2 High Plains Five Forks West Deptford West Texas Texas Georgia Nevada Iowa Arkansas Colorado Virginia New Jersey Texas Coal/800 Coal/1,200 Coal/Wind 1,600/200 Coal/750 Coal/665 Coal/600 Coal/800 Coal/500 Natural Gas/500 Application Filed Permit Issued Application Filed Permit Issued Application Filed Permit Issued Location Solid Waste Permit Water Discharge Permit Air Permit Water Supply Secured/Available Fuel/MW Site Secured Zoning Approved/Not Required N/A N/A Note: Sandy Creek air permit appeal hearing scheduled for 1Q 2007. Draft Draft |

25 DYNEGY STAND-ALONE 2007 ESTIMATES: GAAP BASIS DYNEGY STAND-ALONE 2007 ESTIMATES: GAAP BASIS Dynegy stand-alone expected to have positive net income and free cash flow in 2007 EBITDA includes G&A expenses of approximately $140 MM Note: 2007 estimates are presented on a GAAP basis and are based on quoted forward commodity price curves as of 11/01/06. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Core business represents continuing operating results, excluding significant items. (1) Asset sale proceeds in a range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. As Presented December 13, 2006; Based on Price Curves as of November 1, 2006 ($ in millions) 2007 Total ($ in millions) 2007 Total EBITDA Estimates $ 770-830 GAAP OCF $ 410-460 Depreciation (230) GAAP ICF Interest (275) Capex - Maintenance (140) Tax Expense (100-125) Capex - Consent Decree (90) Proceeds from Asset Sales (1) 200 Net Income Applicable to Common Shareholders - GAAP $ 165-200 Free Cash Flow $ 380-430 Less: Proceeds from Asset Sales (1) (200) Free Cash Flow - Core Business $ 180-230 |

26 GENERATION ASSET LIST GENERATION ASSET LIST Net Primary Dispatch NERC Region/Facility (1) Location Capacity (2) Fuel Type Type Region MIDWEST Baldwin Baldwin, IL 1,800 Coal Baseload MISO Havana Units 1-5 Havana, IL 228 Oil Peaking MISO Unit 6 Havana, IL 441 Coal Baseload MISO Hennepin Hennepin, IL 293 Coal Baseload MISO Oglesby Oglesby, IL 63 Gas Peaking MISO Stallings Stallings, IL 89 Gas Peaking MISO Tilton Tilton, IL 188 Gas Peaking MISO Vermilion Units 1-2 Oakwood, IL 164 Coal/Gas Baseload MISO Unit 3 Oakwood, IL 12 Oil Peaking MISO Wood River Units 1-3 Alton, IL 119 Gas Peaking MISO Units 4-5 Alton, IL 446 Coal Baseload MISO Kendall Minooka, IL 1,200 Gas - CCGT Intermediate PJM Ontelaunee Ontelaunee Township, PA 580 Gas - CCGT Intermediate PJM Rocky Road (3) East Dundee, IL 330 Gas Peaking PJM Riverside/Foothills Louisa, KY 960 Gas Peaking PJM Rolling Hills Wilkesville, OH 965 Gas Peaking PJM Renaissance Carson City, MI 776 Gas Peaking MISO Plum Point (4) Osceola, AR 265 Coal Baseload SERC Bluegrass Oldham County, KY 576 Gas Peaking SERC Midwest Combined 9,495 NORTHEAST Independence Scriba, NY 1,064 Gas - CCGT Intermediate NYISO Roseton (5) Newburgh, NY 1,185 Gas/Oil Intermediate NYISO Bridgeport Bridgeport, CT 527 Gas - CCGT Baseload ISO-NE Casco Bay Veazie, ME 540 Gas - CCGT Baseload ISO-NE Danskammer Units 1-2 Newburgh, NY 123 Gas/Oil Peaking NYISO Units 3-4 (5) Newburgh, NY 370 Coal/Gas/Oil Baseload NYISO Northeast Combined 3,809 |

|