Morgan Stanley 14 th Annual Global Electricity & Energy Conference Morgan Stanley 14 th Annual Global Electricity & Energy Conference March 14, 2007 New York Investor & Public Relations: Norelle Lundy, Vice President Hillarie Forister, Senior Analyst (713) 507-6466 ir@dynegy.com Filed by Dynegy Acquisition, Inc. Pursuant to Rule 425 of the Securities Act of 1933, as amended, and deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934, as amended Subject Company: Dynegy Inc. Commission File No: 001-15659 |

2 FORWARD-LOOKING STATEMENTS FORWARD-LOOKING STATEMENTS This presentation contains statements reflecting assumptions, expectations, projections, intentions or beliefs about future events that are intended as “forward-looking statements.” You can identify these statements, including those relating to Dynegy’s 2007 financial estimates and the proposed combination with LS Power, by the fact that they do not relate strictly to historical or current facts. Management cautions that any or all of Dynegy’s forward-looking statements may turn out to be wrong. Please read Dynegy’s annual, quarterly and current reports under the Securities Exchange Act of 1934, including its 2006 Form 10-K for additional information about the risks, uncertainties and other factors affecting these forward-looking statements and Dynegy generally. Dynegy’s actual future results may vary materially from those expressed or implied in any forward-looking statements. All of Dynegy’s forward-looking statements, whether written or oral, are expressly qualified by these cautionary statements and any other cautionary statements that may accompany such forward-looking statements. In addition, Dynegy disclaims any obligation to update any forward-looking statements to reflect events or circumstances after the date hereof. In connection with the LS Power transaction announced on September 15, 2006, Dynegy and Dynegy Acquisition, Inc. have filed a definitive proxy statement/prospectus with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO CAREFULLY READ THE IMPORTANT INFORMATION CONTAINED IN THE MATERIALS REGARDING THE PROPOSED TRANSACTION. THEY CONTAIN IMPORTANT INFORMATION ABOUT DYNEGY, LS POWER, THE NEW COMPANY AND THE PROPOSED TRANSACTION. Investors and security holders may obtain a copy of the definitive proxy statement/prospectus and other documents containing information about Dynegy and LS Power, free of charge, at the SEC’s web site at www.sec.gov and at Dynegy’s web site at www.dynegy.com. Copies of the definitive proxy statement/prospectus may also be obtained by writing Dynegy Inc. Investor Relations, 1000 Louisiana Street, Suite 5800, Houston, Texas 77002 or by calling 713-507-6466. Dynegy, LS Power and their respective directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies from Dynegy’s shareholders with respect to the proposed transaction. Information regarding Dynegy’s directors and executive officers is available in the company’s proxy statement for its 2006 Annual Meeting of Shareholders, dated April 3, 2006. Additional information regarding the interests of such potential participants is included in the definitive proxy statement/prospectus and other relevant documents filed with the SEC. Non-GAAP Financial Measures: We use the non-GAAP financial measures “EBITDA” and “free cash flow” in these materials. EBITDA is a non-GAAP financial measure. Consolidated EBITDA can be reconciled to Net income (loss) using the following calculation: Net income (loss) less Income tax benefit (expense), plus Interest expense and Depreciation and amortization expense equals EBITDA. Management and some members of the investment community utilize EBITDA to measure financial performance on an ongoing basis. However, EBITDA should not be used in lieu of GAAP measures such as net income and cash flow from operations. Free cash flow is a non-GAAP financial measure. Free cash flow can be reconciled to operating cash flow using the following calculation: Operating cash flow plus investing cash flow (consisting of asset sale proceeds less business acquisition costs, capital expenditures and changes in restricted cash) equals free cash flow. We use free cash flow to measure the cash generating ability of our operating asset-based energy business relative to our capital expenditure obligations. Free cash flow should not be used in lieu of GAAP measures with respect to cash flows and should not be interpreted as available for discretionary expenditures, as mandatory expenditures such as debt obligations are not deducted from the measure. |

3 2006 ANNUAL HIGHLIGHTS 2006 ANNUAL HIGHLIGHTS Generation EBITDA improved year-over-year 2006 benefited from strong execution of near-term commercial strategy and continued focus on reliable operations 2006 impacted by liability management costs and asset impairments, while 2005 included the gain on the sale of the Midstream business, offset by toll settlements and legal charges Completed comprehensive liability management plan, reducing debt and other obligations by more than $2.5 B Completed Rocky Road-West Coast Power asset exchange and Rockingham asset sale Announced agreement with state of Illinois to reduce mercury and other emissions, which is expected to create one of the cleanest-burning coal fleets in Illinois and U.S. Participated in Illinois auction process to supply a portion of Ameren’s full-requirements load Settled Enron trade credit litigation, resolving a major legacy legal claim Announced proposed LS Power combination and development joint venture Building a strong platform for future consolidation and growth |

4 INTEGRATION UPDATE INTEGRATION UPDATE Expiration of Hart-Scott-Rodino waiting period Filing of preliminary proxy statement/prospectus with SEC Presentation of 2007 combined company cash flow and earnings estimates Receipt of New York Public Service Commission approval Receipt of FERC approval Proxy statement and prospectus effective with the SEC and mailed to shareholders Pending: Special shareholder meeting and affirmative vote of at least 2/3 of Dynegy’s Class A shares; meeting scheduled for March 29, 2007 Pending: Transaction closing On track for transaction closing at end of 1Q 2007 |

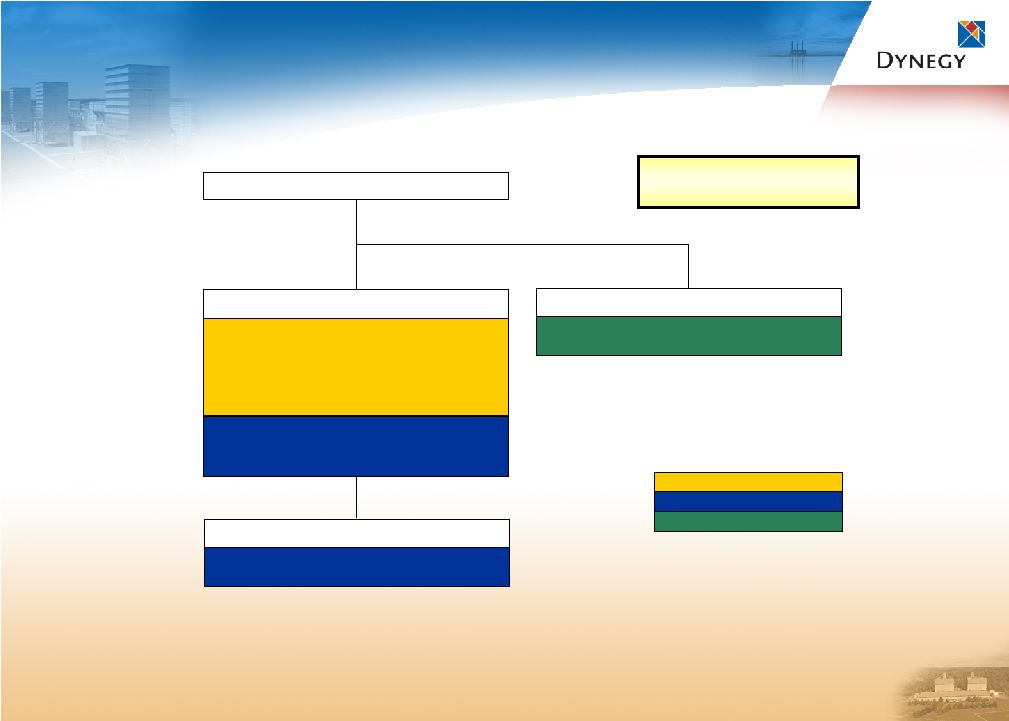

5 NEW DYNEGY’S PLANNED CAPITAL STRUCTURE PRO FORMA AS OF CLOSING ($ in MM) NEW DYNEGY’S PLANNED CAPITAL STRUCTURE PRO FORMA AS OF CLOSING ($ in MM) Dynegy Power Corp. Central Hudson (3) $820 Dynegy Holdings Inc. $750 Million Revolver (1) $275 Synthetic LC Facility (2) $500 Second Secured Notes $11 Sr. Unsec. Notes/Debentures $2,397 Subordinated Debentures $200 Secured Key Secured Non-Recourse Unsecured Dynegy Inc.. Sithe Energies Senior Debentures $428 LS Power Portfolio (4) 1st Lien $1,500 2nd Lien 200 Operating Assets $1,700 Plum Point, Net 202 Total $1,902 Note: Represents current capital structure expectations and assumptions as of February 2007, which have been adjusted to reflect balances expected as of 3/31/07. (1) Represents drawn amounts under the revolver upon expected closing of transaction. (2) Proceeds from this facility are expected to be drawn and fully collateralize the issuance of letters of credit. Includes $200 MM from original facility, $185 MM for LS Power parental support, $83 MM for Sithe debt reserve and $32 MM for miscellaneous developmental requirements. (3) Central Hudson lease payments are unsecured obligations of Dynegy Inc., but are a secured obligation of an unrelated third party (“lessor”) under the lease. DHI has guaranteed the lease payments on a senior unsecured basis. Amount reflects PV (10%) of future lease payments as of 3/31/07. (4) See the appendix for more details about the LS Power debt portfolio. |

6 2007 CASH FLOW ESTIMATES: GAAP BASIS 2007 CASH FLOW ESTIMATES: GAAP BASIS GEN OCF adjustment primarily related to cash received in 2006 for 2007 forward sales Other OCF adjustment due to timing of Sithe interest payment previously expected in 2006 Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 1/30/07 and assume closing of the LS Power transaction at end 1Q 2007. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Core business represents continuing operating results, excluding significant items. (1) Asset sale proceeds in the range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. Proceeds from the expected sale of Calcasieu are assumed to be received in early 2008. As Presented February 27, 2007; Based on Price Curves as of January 30, 2007 ($ in millions) GEN OTHER 2007 Total Previous GAAP OCF Estimates $ 1,170-1,260 $ (570-560) $ 600-700 Adjustments (Approximate): Timing of Receipts and Payments (80) (20) (100) New GAAP OCF Estimates $ 1,090-1,180 $ (590-580) $ 500-600 GAAP ICF Capex - Maintenance (155) (15) (170) Capex - Consent Decree (90) - (90) Capex - Plum Point Development (155) - (155) Investment in Development Portfolio - (10) (10) Proceeds from Asset Sales and Acquisition Costs, Net (1) 200 (145) 55 Change in Restricted Cash 155 30 185 Free Cash Flow $ 315-415 Add Back: Acquisition Costs 145 Less: Proceeds from Asset Sales (1) (200) Free Cash Flow - Core Business $ 260-360 |

7 2007 EARNINGS ESTIMATES: GAAP BASIS 2007 EARNINGS ESTIMATES: GAAP BASIS As Presented February 27, 2007; Based on Price Curves as of January 30, 2007 ($ in millions) Midwest West Northeast Total GEN OTHER 2007 Total EBITDA Estimates $ 745-795 $ 215-235 $ 175-205 $ 1,135-1,235 $ (115-105) $ 1,020-1,130 Depreciation (180) (45) (40) (265) (15) (280) Interest (435) Tax Expense (115-160) Net Income Applicable to Common Shareholders - GAAP $ 190-255 Earnings Per Share (1) $ 0.25-0.34 Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 1/30/07 and assume closing of the LS Power transaction at end 1Q 2007, excluding purchase accounting adjustments. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Reduced 2007 and forward EBITDA or free cash flow could result from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges. (1) Calculated based on 755 MM weighted-average shares outstanding. Other includes G&A costs of approximately $160 MM, primarily offset by interest income Interest expense of $435 MM includes approximately $30 MM for Plum Point Estimates exclude purchase accounting adjustments to be recorded upon closing of LS Power transaction Earnings may be more volatile as many of the forward sales commitments associated with the LS Power portfolio are marked-to-market under GAAP, which may create variances between earnings and cash flows in certain periods |

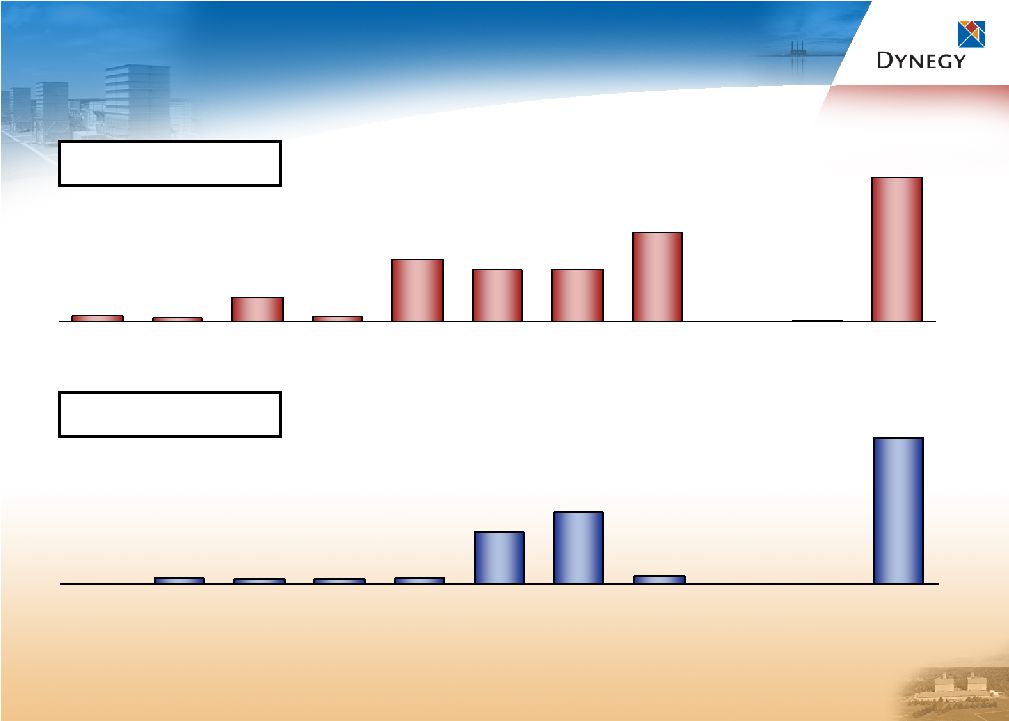

8 Expected 2007 Total EBITDA Ranges Given $/MMBtu Cost of Natural Gas 2007 TOTAL EARNINGS SENSITIVITY TO NATURAL GAS 2007 TOTAL EARNINGS SENSITIVITY TO NATURAL GAS Full-year 2007 average natural gas price as of 1/30/07 = $7.80/MMBtu (Henry Hub) +/- $1/MMBtu change in natural gas is approximately equal to: +/- ~4% change (3) in Generation EBITDA +/- ~$50 MM change in Generation EBITDA Note: EBITDA based on full-year estimates as presented 2/27/07 for existing Dynegy assets and 9 months of estimates for LS Power assets beginning 4/01/07. (1) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. (2) Pricing as of 1/30/07, which was the basis for estimates as presented 2/27/07. Prices reflect actual day ahead settlement prices for Jan. 1 – Jan. 30 and quoted forward monthly prices for Jan. 31 – Dec. 2007. (3) Percentage change calculated based on Generation EBITDA estimates of a range of $1,135-1,235 MM as presented 2/27/07. (12-Month Average $/MMBtu) $900 $1,000 $1,100 $1,200 $1,300 $6.00 Gas $8.00 Gas $10.00 Gas $920 $1,030 $975 $1,020 $1,130 $1,120 $1,230 $1,175 $1,075 $0 $2 $4 $6 $8 $10 J F M A M J J A S O N D 2006A: $6.74 2007F (Nov): $8.05 ($/MMBtu) Natural Gas 2006 Actual 2007 Forward as of 11/01/06 (1) -- OR -- 2007A/F (Jan): $7.80 2007 Actual/Forward as of 1/30/07 (2) |

9 MARKET IMPLIED HEAT RATES MARKET IMPLIED HEAT RATES Market implied heat rates are derived from market gas and power prices, and are impacted by weather and outages in the short-term, and overall supply/demand balance in the longer-term Changes in market implied heat rates can affect plants in various ways: Impact to coal plants is primarily as a result of changes to margin based on the difference between power prices and production costs Roseton more sensitive to spreads based on fuel oil prices than spreads based on natural gas Impact to gas plants results from changes to margin and volume Facilities with forward sales commitments, RMR contracts, or tolling arrangements may not be as sensitive to changes in market implied heat rates In this example, ERCOT market implied heat rates reflect “on-peak” pricing, assuming constant natural gas price: Spark spread value changes depend on natural gas price assumptions Example: ~$8.00/MMBtu natural gas x .5 MMBtu/MWh heat rate change = $4.00 spark spread value OR ~$10.00/MMBtu natural gas x .5 MMBtu/MWh heat rate change = $5.00 spark spread value Note: Baseload coal sensitivity to heat rate changes does not apply if power prices are assumed constant with variable natural gas prices. (1) Average natural gas price as of 11/01/06, which was the basis for estimates as presented 12/13/06. + 500 Btu/MWh Base Case - 500 Btu/MWh On-Peak Power Price ($/MWh) $ 84 $ 80 $ 76 Natural Gas ($/MMBtu) (1) $ 8.05 $ 8.05 $ 8.05 Market Implied Heat Rate ~10,500 ~10,000 ~9,500 |

10 2007 TOTAL EARNINGS SENSITIVITY TO MARKET IMPLIED HEAT RATES 2007 TOTAL EARNINGS SENSITIVITY TO MARKET IMPLIED HEAT RATES Sensitivities based on “on-peak” power price changes Estimates based on full-year and nine months of earnings for Dynegy and LS Power assets, respectively Sensitivities apply only to 2007 earnings Assumes constant natural gas price of $8.05/MMBtu and heat rate changes are for a full year Coal and fuel-oil plant impacts primarily driven by changes in power prices Combined cycle sensitivities impacted by spark spread value and associated changes in run-time Peakers run when economical but have minimal impact in current pricing environment; however, if market implied heat rates continue to increase, peakers will add increased upside potential Market Implied Heat Rate Movement Coal/Fuel Oil Gas Total + 1,500 Btu/MWh $105 $125 $230 + 500 Btu/MWh $40 $35 $75 - 500 Btu/MWh -$25 -$30 -$55 - 1,500 Btu/MWh -$75 -$95 -$170 Generation EBITDA Sensitivity ($ in MM) Note: EBITDA calculations exclude purchase accounting adjustments, which will impact the value of the LS Power fleet when recorded upon transaction close. |

11 MARKET RECOVERY UPSIDE MARKET RECOVERY UPSIDE Market recovery upside refers to expected benefits resulting from tightening markets due to supply/demand balance and consolidation benefits Baseload – affected by increased outright power pricing, as run-times are currently at high levels and coal and rail costs are essentially flat in the near-term Intermediate – should benefit from both improved pricing/spreads, increased volumes and improved capacity markets Peakers – should benefit from both improved pricing/spreads, increased volumes and improved capacity markets Consolidation – results in G&A, O&M and financing cost savings due to Dynegy’s scalable platform and reduced duplication of overhead; this “Consolidation Benefit” is in addition to market recovery upside Price / Spread Volume Cost Savings Baseload Intermediate Peaker Consolidation = Areas for Potential Upside in Market Recovery |

12 Closing Price of Dynegy Common Stock Closing Price of DHI 8.375% Senior Unsecured Notes Due 2016 RECENT PRICE PERFORMANCE RECENT PRICE PERFORMANCE Dynegy common stock and unsecured bond prices have steadily risen since announcement of LS Power combination, illustrating, in part, both the equity and fixed income market’s favorable perception of the proposed merger Voting for the combination is important…a failure to vote is a vote “against” the deal $5 $6 $7 $8 9/15/06 10/15/06 11/15/06 12/15/06 1/15/07 2/15/07 $100 $103 $106 $109 9/15/06 10/15/06 11/15/06 12/15/06 1/15/07 2/15/07 9/15/06: $6.07 2/21/07: $8.00 9/15/06: $101.50 2/21/07: $108.25 |

13 UPCOMING EVENTS UPCOMING EVENTS Houston: Merrill Lynch Texas Power & Gas Day on March 20 Houston: Special Meeting of Shareholders on March 29 New Orleans: Howard Weil 35 th Annual Energy Conference on April 4 Special Meeting of Shareholders on March 29 VOTING “FOR” the Dynegy/LS Power Merger is Important A Failure to Vote is a Vote “Against” the Deal |

Appendix |

15 NEW DYNEGY PORTFOLIO NEW DYNEGY PORTFOLIO Scale and scope in key regions Note: Plum Point 1 currently under construction. MW totals exclude development and repowerings, opportunities for which exist at Bridgeport, Griffith, Morro Bay, Moss Landing, Oakland and South Bay. Dynegy has entered into an agreement to sell the 351-MW Calcasieu peaking facility in Louisiana, the closing of which is expected in early 2008. Primary Fuel Type Nameplate Capacity (MW) More than 900 MW 500 MW to 900 MW 150 MW to 500 MW Less than 150 MW LS Power - Operating Coal Gas Gas/Oil Wind LS Power - Development Dynegy Inc. Midwest 9,495 MW Northeast 3,809 MW Transmission Total 20,044 MW West 6,740 MW Dynegy Inc. – Potential Sale |

16 DIVERSIFIED AND BALANCED PORTFOLIO DIVERSIFIED AND BALANCED PORTFOLIO Northeast 23.4% Midwest 63.4% South 13.2% Northeast 12.9% Midwest 24.6% West 62.5% Intermediate 19.2% Peaking 45.3% Baseload 35.5% Intermediate 25.8% Peaking 41.7% Baseload 32.5% Peaking 36.5% Baseload 28.3% Intermediate 35.2% Fuel Diversity Coal/Oil 20.9% Dual Fuel 6.5% Gas - CCGT 33.4% Gas - Simple Cycle 39.2% Portfolio diversified through geographic locations, fuel and dispatch types Dynegy Capacity LS Power Capacity Combined Capacity Geographic Diversity Dispatch Diversity Note: Includes MWs for assets to be sold or considered for divestiture. Dynegy has entered into an agreement to sell the 351-MW Calcasieu peaking facility in Louisiana, the closing of which is expected in early 2008. Other possible divestitures include the Bluegrass, Cogen Lyondell and Heard County generation facilities. Northeast 19.0% Midwest 47.4% South 7.5% West 26.1% |

17 GROWTH THROUGH CONSOLIDATION BENEFITS FOR INVESTORS GROWTH THROUGH CONSOLIDATION BENEFITS FOR INVESTORS Greater scale and scope without proportionate increase in costs Greater scale and scope without proportionate increase in costs New Dynegy’s competitive position enhanced through more assets under management Note: G&A estimates are as presented 2/27/07. (1) Excludes $55 MM pre-tax legal and settlement charges recorded in G&A. (2) Based on full-year estimates for Dynegy and 9 months of estimates for LS Power beginning 4/01/07, including certain acquisition-related expenditures. 0 5,000 10,000 15,000 20,000 25,000 Megawatts Estimated G&A ($ in MM) 2007 2006 $140 (1) $160 (2) 11,739 20,044 Megawatts increase 71%, while G&A up only 14% Megawatts increase 71%, while G&A up only 14% |

18 GREENFIELD DEVELOPMENT GREENFIELD DEVELOPMENT More than 7,600 MW in various stages of power generation development Sandy Creek Long Leaf White Pine/ Egan Elk Run Plum Point Unit 2 High Plains Five Forks West Deptford West Texas Texas Georgia Nevada Iowa Arkansas Colorado Virginia New Jersey Texas Coal/800 Coal/1,200 Coal/Wind 1,600/200 Coal/750 Coal/665 Coal/600 Coal/800 Coal/500 Natural Gas/500 Application Filed Permit Issued Application Filed Permit Issued Application Filed Permit Issued Location Solid Waste Permit Water Discharge Permit Air Permit Water Supply Secured/Available Fuel/MW Site Secured Zoning Approved/Not Required N/A N/A Note: Sandy Creek air permit appeal hearing scheduled for 1Q 2007. Draft Draft |

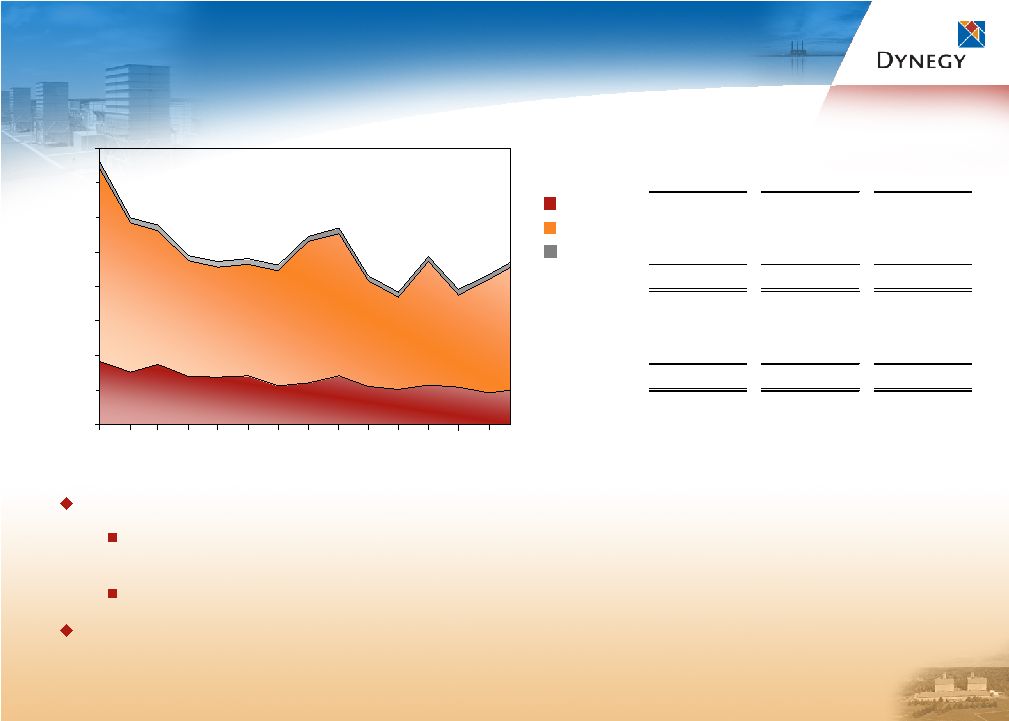

19 $0 $30 $60 $90 J F M A M J J A S O N D COMMODITY PRICING COMMODITY PRICING ($/MWh) 2006 Actual 2007 Forward as of 11/01/06 (1) 2007 Actual/Forward as of 1/30/07 (2) Cin Hub/Cinergy 2006A: $51.58 2007F (Nov): $59.04 2007A/F (Jan): $59.34 (1) Pricing as of 11/01/06, which was the basis for estimates as presented 12/13/06. Prices reflect quoted forward on-peak monthly prices for 2007. (2) Pricing as of 1/30/07, which was the basis for estimates as presented 2/27/07. Prices reflect actual day ahead on-peak settlement prices for Jan. 1 – Jan. 30 and quoted forward on-peak monthly prices for Jan. 31 – Dec. 2007. $0 $25 $50 $75 $100 $125 J F M A M J J A S O N D New York Zone G $0 $25 $50 $75 $100 $125 J F M A M J J A S O N D ERCOT ($/MWh) $0 $25 $50 $75 $100 J F M A M J J A S O N D ($/MWh) NP-15 ($/MWh) 2006A: $75.84 2007F (Nov): $88.75 2007A/F (Jan): $88.00 2006A: $63.09 2007F (Nov): $75.47 2007A/F (Jan): $74.87 2006A: $61.15 2007F (Nov): $75.13 2007A/F (Jan): $75.56 |

20 2007 CASH FLOW ESTIMATES: GAAP BASIS 2007 CASH FLOW ESTIMATES: GAAP BASIS Development capex related to Plum Point of $155 MM expected to be funded from Plum Point’s restricted cash Net proceeds from asset sales and acquisition includes $200 MM from potential generation asset sales, offset by $100 MM cash paid to LS Power and $45 MM expected transaction costs Other OCF includes all interest payments, including Sithe interest previously recorded in GEN, as well as Plum Point cash interest of $30 MM funded from Plum Point’s restricted cash Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 11/01/06 and assume closing of the LS Power transaction at end 1Q 2007. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Core business represents continuing operating results, excluding significant items. (1) Asset sale proceeds in the range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. As Presented December 13, 2006; Based on Price Curves as of November 1, 2006 ($ in millions) GEN OTHER 2007 Total GAAP OCF $ 1,170-1,260 $ (570-560) $ 600-700 GAAP ICF Capex - Maintenance (155) (15) (170) Capex - Consent Decree (90) - (90) Capex - Plum Point Development (155) - (155) Investment in Development Portfolio - (10) (10) Proceeds from Asset Sales and Acquisition Costs, Net (1) 200 (145) 55 Change in Restricted Cash 155 30 185 Free Cash Flow $ 415-515 Add Back: Acquisition Costs 145 Less: Proceeds from Asset Sales (1) (200) Free Cash Flow - Core Business $ 360-460 |

21 2007 EARNINGS ESTIMATES: GAAP BASIS 2007 EARNINGS ESTIMATES: GAAP BASIS Note: 2007 estimates are presented on a GAAP basis, are based on quoted forward commodity price curves as of 11/01/06 and assume closing of the LS Power transaction at end 1Q 2007, excluding purchase accounting adjustments. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Reduced 2007 and forward EBITDA or free cash flow could result from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges. (1) Calculated based on 755 MM weighted-average shares outstanding. Other includes G&A costs of approximately $160 MM, primarily offset by interest income Interest expense of $435 MM includes approximately $30 MM for Plum Point Estimates exclude purchase accounting adjustments to be recorded upon closing of LS Power transaction Earnings may be more volatile as many of the forward sales commitments associated with the LS Power portfolio are marked-to-market under GAAP, which may create variances between earnings and cash flows in certain periods As Presented December 13, 2006; Based on Price Curves as of November 1, 2006 ($ in millions) Midwest West Northeast Total GEN OTHER 2007 Total EBITDA Estimates $ 745-795 $ 215-235 $ 175-205 $ 1,135-1,235 $ (115-105) $ 1,020-1,130 Depreciation (180) (45) (40) (265) (15) (280) Interest (435) Tax Expense (115-160) Net Income Applicable to Common Shareholders - GAAP $ 190-255 Earnings Per Share (1) $ 0.25-0.34 |

22 DYNEGY STAND-ALONE 2007 ESTIMATES: GAAP BASIS DYNEGY STAND-ALONE 2007 ESTIMATES: GAAP BASIS Dynegy stand-alone expected to have positive net income and free cash flow in 2007 EBITDA includes G&A expenses of approximately $140 MM OCF adjustment primarily related to cash received in 2006 for 2007 forward sales Note: 2007 estimates are presented on a GAAP basis and are based on quoted forward commodity price curves as of 1/30/07. Actual results may vary materially from these estimates based on changes in commodity prices, among other things, including operational activities, legal settlements, financing or investing activities and other uncertain or unplanned items. Core business represents continuing operating results, excluding significant items. (1) Asset sale proceeds in a range of $200-500 MM are expected from potential divestitures of (a) non-core assets where the earnings potential is limited, or (b) assets where the value that can be captured through a divestiture is believed to outweigh the benefits of continuing to own or operate such assets. Divestitures could result in impairment charges and could reduce 2007 and forward EBITDA or free cash flow. Proceeds from the expected sale of Calcasieu are assumed to be received in early 2008. As Presented February 27, 2007; Based on Price Curves as of January 30, 2006 ($ in millions) 2007 Total ($ in millions) 2007 Total EBITDA Estimates $ 770-830 Previous GAAP OCF $ 410-460 Depreciation (230) Adjustments (Approximate) Interest (275) Timing of Receipts and Payments (100) Tax Expense (100-125) New GAAP OCF Estimates $ 310-360 Net Income Applicable to Common Shareholders - GAAP $ 165-200 GAAP ICF Capex - Maintenance (140) Capex - Consent Decree (90) Proceeds from Asset Sales (1) 200 Free Cash Flow $ 280-330 Less: Proceeds from Asset Sales (1) (200) Free Cash Flow - Core Business $ 80-130 |

23 DEBT AND OTHER OBLIGATIONS CHART – AS OF 12/31/06 ($ in MM) DEBT AND OTHER OBLIGATIONS CHART – AS OF 12/31/06 ($ in MM) Dynegy Inc.. Dynegy Power Corp. Central Hudson (3) $801 Dynegy Holdings Inc. Revolver (1) $0 Synthetic LC Facility (2) $200 Second Secured Notes $11 Sr. Unsec. Notes/Debentures $2,397 Subordinated Debentures $200 Sithe Energies Senior Debentures (4) $447 Secured Key Secured Non-Recourse Unsecured (1) Represents drawn amounts under the revolver as of 12/31/06. (2) Proceeds from this facility have been drawn and fully collateralize the issuance of letters of credit. (3) Central Hudson lease payments are unsecured obligations of Dynegy Inc., but are a secured obligation of an unrelated third party (“lessor”) under the lease. DHI has guaranteed the lease payments on a senior unsecured basis. Amount reflects PV (10%) of future lease payments as of 12/31/06. (4) Includes approximately $19 MM as of 12/31/06 that was paid 1/02/07. Total: $4.1 B |

24 DEBT AND LEASE OBLIGATIONS ($ in MM) DEBT AND LEASE OBLIGATIONS ($ in MM) Net decrease from 12/31/05 to 12/31/06 primarily reflects the following: $1.7 B repayment of SPNs $225 MM repayment of convertible subordinated debentures $400 MM redemption of Series C preferred $419 MM elimination of Sithe subordinated debt, offset by $1,047 MM addition of senior unsecured notes due 2016 $200 MM addition of term credit facility due 2012 12/31/03 12/31/04 12/31/05 12/31/06 Secured Obligations 4,087 $ 2,536 $ 1,749 $ 211 $ Secured Non-Recourse Obligations - - 885 447 Unsecured Obligations 2,891 2,587 2,583 3,398 Preferred 411 400 400 - Total Obligations 7,389 $ 5,523 $ 5,617 $ 4,056 $ Cash on Hand 477 $ 628 $ 1,549 $ 371 $ Note: Debt includes par value debt obligations and obligations for Central Hudson. Debt as of 12/31/06: (1) includes approximately $19 MM of Sithe senior debt that was paid 1/02/07; and (2) excludes $470 MM revolving credit facility due 2009 as it is currently undrawn. $7,389 $5,523 $5,617 $4,056 12/31/03 12/31/04 12/31/05 12/31/06 |

25 DEBT MATURITY PROFILE ($ in MM) DEBT MATURITY PROFILE ($ in MM) $60 $40 $269 $57 $0 $1,584 $687 $568 $10 $575 $982 12/31/05: $4.8 B Note: Annual maturities reflect par value debt obligations, excluding Central Hudson lease payments. Debt as of 12/31/06: (1) includes $19 MM of Sithe senior debt in 2007 that was paid 1/02/07; (2) excludes $470 MM revolving credit facility due 2009 as it is currently undrawn; and (3) excludes LS Power debt of approximately $1.9 B expected to be assumed upon the closing of the transaction at end 1Q 2007. 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016+ $0 $59 $44 $57 $0 $1,597 $73 $568 $0 $775 $82 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016+ 12/31/06: $3.3 B |

26 COLLATERAL POSTED ($ in MM) COLLATERAL POSTED ($ in MM) Collateral reduced from year-end 2005 Decrease in generation business collateral due to decreased prices, expiration of certain hedge positions and West Coast Power sale completion CRM decrease due to price changes and contract expirations Increase in generation collateral from year-end 2006 primarily due to increased facility run-times $0 $50 $100 $150 $200 $250 $300 $350 $400 12/31/05 12/31/06 2/22/07 CRM 91 $ 54 $ 50 $ GEN 280 134 178 Other 10 7 7 Total 381 $ 195 $ 235 $ Cash 122 $ 38 $ 40 $ LCs 259 157 195 Total 381 $ 195 $ 235 $ 12/05 3/06 6/06 9/06 12/06 |

27 LIQUIDITY ($ in MM) LIQUIDITY ($ in MM) Decrease in cash on hand from 3/31/06 primarily due to liability management activities and repayment of debt obligations, offset by receipt of proceeds from issuance of new unsecured notes and equity offering Liquidity figure above excludes $38 MM cash collateral posted as of 12/31/06 Cash Availability $1,620 12/31/05 3/31/06 $1,913 9/30/06 $846 6/30/06 $864 12/31/06 $878 |

28 LS POWER DEBT AND OTHER OBLIGATIONS PRO FORMA AS OF 3/31/07 ($ in MM) LS POWER DEBT AND OTHER OBLIGATIONS PRO FORMA AS OF 3/31/07 ($ in MM) 1st Lien Debt $ 1,500 MM 2nd Lien Debt 200 MM Operating Assets $ 1,700 MM Plum Point, Net 202 MM Total $ 1,902 MM Total LS Power Amounts Outstanding Key Secured Non-Recourse Kendall 1st Lien LC Facility $0 1st Lien Term Loan $402 Ontelaunee 1st Lien Term Loan $95 2nd Lien Term Loan $50 LSP Gen Finance Co. 1st Lien Term Loans $933 2nd Lien Term Loan $150 $100 MM 1st Lien Revolver (1) $0 1st Lien LC Facilities (1) $0 Plum Point Energy Assoc. 1st Lien Term Loan (3) $356 2nd Lien Term Loan (3) $147 $50 MM 1st Lien Rev. (1) $0 Synthetic LC Facility (4) $0 Tax Exempt Notes (3) $100 Sub-Total $603 Less: Cash (5) ($401) Total, Net $202 LS Power Portfolio Griffith 1st Lien Facility (2) $70 Note: Represents pro forma debt balances as of 3/31/07. Plum Point is expected to be consolidated in Dynegy’s financial results, but the facility will be only net 40% owned by the new company. (1) Revolver facilities assumed to be undrawn as of 3/31/07. LSP Gen Finance Co. First Lien LC Facilities totaling $650 MM exclude $514 MM letters of credit posted as of January 2007. (2) First lien facility to be entered into upon expected closing of transaction. (3) Does not reflect a total of $401 MM restricted cash. (4) $102 MM Synthetic LC Facility is undrawn and collateralizes tax exempt notes. (5) Restricted cash expected to be approximately $401 MM as of 3/31/07. |

29 GENERATION ASSET LIST GENERATION ASSET LIST Net Primary Dispatch NERC Region/Facility Location Capacity (1) Fuel Type Type Region MIDWEST Baldwin Baldwin, IL 1,800 Coal Baseload MISO Havana Units 1-5 Havana, IL 228 Oil Peaking MISO Unit 6 Havana, IL 441 Coal Baseload MISO Hennepin Hennepin, IL 293 Coal Baseload MISO Oglesby Oglesby, IL 63 Gas Peaking MISO Stallings Stallings, IL 89 Gas Peaking MISO Tilton Tilton, IL 188 Gas Peaking MISO Vermilion Units 1-2 Oakwood, IL 164 Coal/Gas Baseload MISO Unit 3 Oakwood, IL 12 Oil Peaking MISO Wood River Units 1-3 Alton, IL 119 Gas Peaking MISO Units 4-5 Alton, IL 446 Coal Baseload MISO Kendall Minooka, IL 1,200 Gas - CCGT Intermediate PJM Ontelaunee Ontelaunee Township, PA 580 Gas - CCGT Intermediate PJM Rocky Road (2) East Dundee, IL 330 Gas Peaking PJM Riverside/Foothills Louisa, KY 960 Gas Peaking PJM Rolling Hills Wilkesville, OH 965 Gas Peaking PJM Renaissance Carson City, MI 776 Gas Peaking MISO Plum Point (3) Osceola, AR 265 Coal Baseload SERC Bluegrass (4) Oldham County, KY 576 Gas Peaking SERC Midwest Combined 9,495 NORTHEAST Independence Scriba, NY 1,064 Gas - CCGT Intermediate NYISO Roseton (5) Newburgh, NY 1,185 Gas/Oil Intermediate NYISO Bridgeport Bridgeport, CT 527 Gas - CCGT Baseload ISO-NE Casco Bay Veazie, ME 540 Gas - CCGT Baseload ISO-NE Danskammer Units 1-2 Newburgh, NY 123 Gas/Oil Peaking NYISO Units 3-4 (5) Newburgh, NY 370 Coal/Gas/Oil Baseload NYISO Northeast Combined 3,809 |

30 GENERATION ASSET LIST (CONT.) GENERATION ASSET LIST (CONT.) Net Primary Dispatch NERC Region/Facility Location Capacity (1) Fuel Type Type Region WEST Moss Landing Units 1-2 Monterrey County, CA 1,020 Gas - CCGT Baseload CAISO Units 6-7 Monterrey County, CA 1,509 Gas Peaking CAISO Morro Bay (6) Morro Bay, CA 650 Gas Peaking CAISO South Bay Chula Vista, CA 706 Gas Peaking CAISO Oakland Oakland, CA 165 Oil Peaking CAISO Arlington Valley Arlington, AZ 585 Gas - CCGT Intermediate WECC Griffith Golden Valley, AZ 558 Gas - CCGT Intermediate WECC Calcasieu (7) Sulphur, LA 351 Gas Peaking SERC Heard County (4) Heard County, GA 539 Gas Peaking SERC Black Mountain (8) Las Vegas, NV 43 Gas Baseload WECC Cogen Lyondell (4) Houston, TX 614 Gas - CCGT Baseload ERCOT West Combined 6,740 TOTAL DYNEGY GENERATION 20,044 (8) Dynegy owns a 50% interest in this facility and the remaining 50% interest is held by Chevron. Total generating capacity of this facility is 85 MW. (1) Unit capabilities are based on winter capacity. (5) DYN entered into a $920 MM sale-leaseback transaction for the Roseton facility and units 3 and 4 of the Danskammer facility in 2001. Cash lease payments extend until 2029 and include $108 MM in 2007, $144 MM in 2008, $141 MM in 2009, $95 MM in 2010 and $112 MM in 2011. GAAP lease payments are $50.5 MM through 2030 and decrease until last GAAP lease payment in 2035. (3) Under construction. Represents net 40% ownership. (2) Excludes 28 MW of capacity for Unit 3, which is not available during cold weather because of winterization requirements. (6) Represents generating capacity of units 3 and 4. Units 1 and 2, with a combined net generating capacity of 352 MW, are currently in layup status and out of operation. (4) Dynegy is conducting a portfolio review and may consider divesting certain assets that (a) are primarily peaking in nature and generally operate in locations where market recovery is projected to occur much further in the future than in other regions in which the company will have a significant asset position, or (b) could present value propositions through potential dispositions not likely to be achieved through continued ownership and operation by the company. Based on this review, the Bluegrass, Cogen Lyondell and Heard County generation facilities could be targets for sale in 2007. (7) Dynegy has entered into an agreement to sell this generation facility, the closing of which is expected in early 2008. |