Exhibit 99.2

| Vantage Energy Services Company Presentation September 12, 2007 |

| Forward-Looking Statements Some of the statements in this presentation constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward looking statements contained in this presentation involve risks and uncertainties as well as statements as to: availability of investment opportunities; general volatility of the market price of our securities; changes in our business strategy; our ability to consummate an appropriate investment opportunity within given time constraints; availability of qualified personnel; changes in our industry, interest rates, the debt securities markets or the general economy; changes in governmental regulations, tax rates and similar matters; changes in generally accepted accounting principles by standard-setting bodies; and the degree and nature of our competition. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. These beliefs, assumptions and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, our business, financial condition, liquidity and results of operations may vary materially from those expressed in our forward-looking statements. |

| Introduction Paul Bragg – Chairman and CEO Christopher DeClaire – CFO John O’Leary – Member, Board of Directors Peter Espig – Senior Vice President, TMT |

| Delivering on our IPO Promise Acquire Four Baker Marine Pacific Class 375 Ultra-premium Jackups for $848 million $500 - $1,000 million initial target acquisition size Utilizing seller equity participation Utilizing credit facility Speculative newbuild market very attractive Capitalize on market expertise and expanding offshore & deepwater spending trends “Quick strike” first transaction Ability to compete against established players for acquisition opportunities Acquire Initial Platform (IPO promise) $848 million acquisition (approximately $1.5 billion including the drillship) Seller is taking $275 million in units $440 million credit facility pending Four Baker Marine Pacific Class 375 Ultra-premium Jackups; option on Ultra-deepwater drillship Professional relationships and industry contacts facilitated a quick transaction Seller refused competing bids from established players in choosing Vantage Establish strong foundation for future expansion |

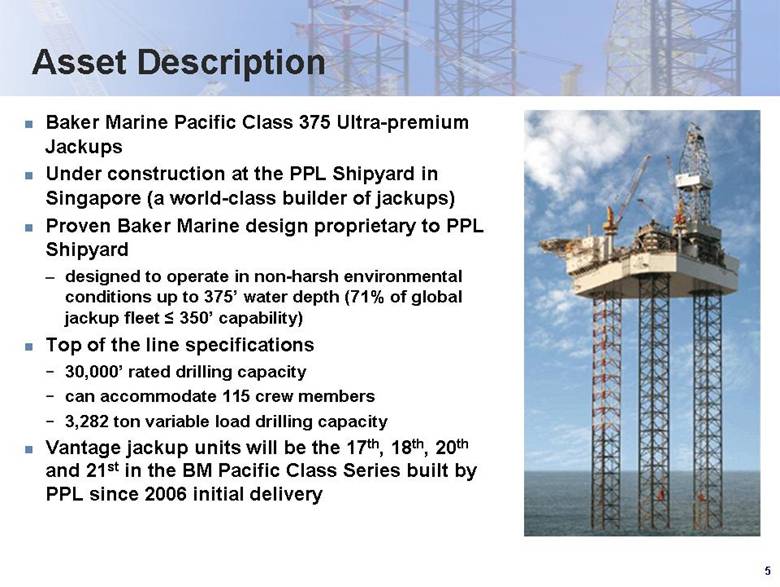

| Asset Description Baker Marine Pacific Class 375 Ultra-premium Jackups Under construction at the PPL Shipyard in Singapore (a world-class builder of jackups) Proven Baker Marine design proprietary to PPL Shipyard designed to operate in non-harsh environmental conditions up to 375’ water depth (71% of global jackup fleet ≤ 350’ capability) Top of the line specifications 30,000’ rated drilling capacity can accommodate 115 crew members 3,282 ton variable load drilling capacity Vantage jackup units will be the 17th, 18th, 20th and 21st in the BM Pacific Class Series built by PPL since 2006 initial delivery |

| TMT has previously partnered with a SPAC – Star Maritime – to successfully build value for investors. IPO investors in Star Maritime have experienced gains of over 60%(b) Strategic Partner – TMT Offshore drilling assets of TMT TMT is one of the world’s largest privately-owned shipping companies TMT will become a major shareholder of and strategic partner to Vantage consideration to TMT includes approximately $275 million in units(a) High strategic value to Vantage level of equity investment demonstrates commitment to the long-term growth of Vantage and the management team keen insight into important global markets, particularly Asia exceptional shipyard relationships (TMT is a global shipping owner and operator of approximately 100 vessels) shipping provider for essentially all major oil and gas and national oil companies (a) $275 million represents approximately a 41% ownership stake on a fully diluted basis. (b) Returns based on market price as of September 7, 2007 and Star Maritime’s December 16, 2005 IPO price. |

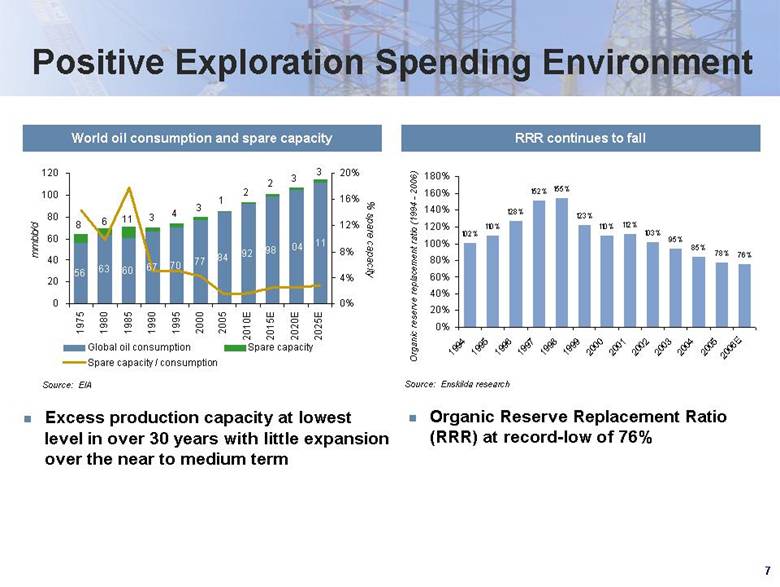

| Positive Exploration Spending Environment World oil consumption and spare capacity RRR continues to fall Source: EIA Source: Enskilda research Excess production capacity at lowest level in over 30 years with little expansion over the near to medium term Organic Reserve Replacement Ratio (RRR) at record-low of 76% 56 63 60 67 70 77 84 92 98 104 111 3 4 3 11 6 8 3 3 2 2 1 0 20 40 60 80 100 120 1975 1980 1985 1990 1995 2000 2005 2010E 2015E 2020E 2025E mmbb/d 0% 4% 8% 12% 16% 20% % spare capacity Global oil consumption Spare capacity Spare capacity / consumption |

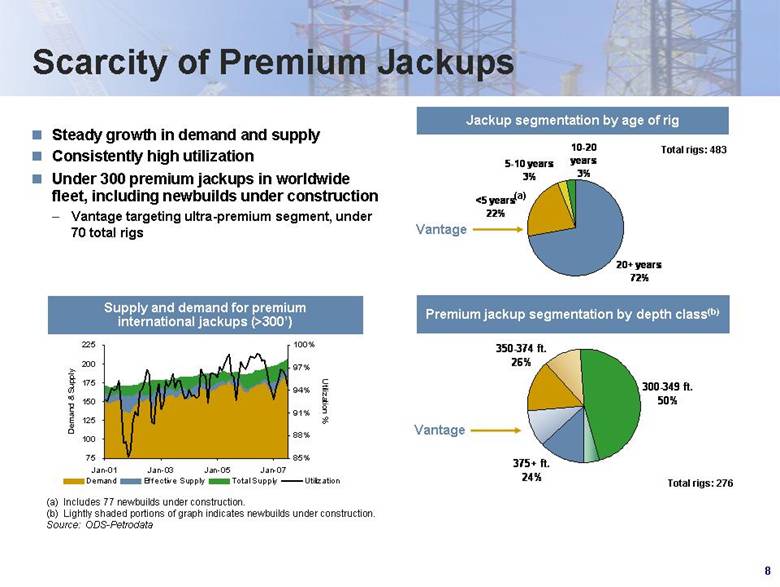

| Jackup segmentation by age of rig Scarcity of Premium Jackups Steady growth in demand and supply Consistently high utilization Under 300 premium jackups in worldwide fleet, including newbuilds under construction Vantage targeting ultra-premium segment, under 70 total rigs Premium jackup segmentation by depth class(b) (a) Includes 77 newbuilds under construction. (b) Lightly shaded portions of graph indicates newbuilds under construction. Source: ODS-Petrodata Supply and demand for premium international jackups (>300’) Total rigs: 276 Total rigs: 483 Vantage (a) 75 100 125 150 175 200 225 Jan-01 Jan-03 Jan-05 Jan-07 Demand & Supply 85% 88% 91% 94% 97% 100% Utilization % Demand Effective Supply Total Supply Utilization 20+ years 72% <5 years 22% 5-10 years 3% 10-20 years 3% |

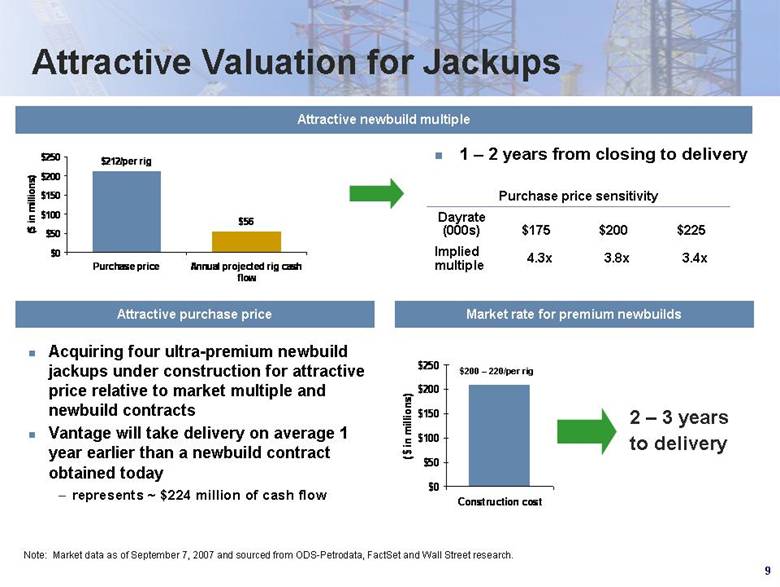

| Attractive Valuation for Jackups Attractive newbuild multiple 1 – 2 years from closing to delivery Attractive purchase price Market rate for premium newbuilds $200 – 220/per rig 2 – 3 years to delivery Note: Market data as of September 7, 2007 and sourced from ODS-Petrodata, FactSet and Wall Street research. 4.3x $175 3.4x 3.8x Implied multiple $225 $200 Dayrate (000s) Purchase price sensitivity Acquiring four ultra-premium newbuild jackups under construction for attractive price relative to market multiple and newbuild contracts Vantage will take delivery on average 1 year earlier than a newbuild contract obtained today represents ~ $224 million of cash flow $56 $212/per rig $0 $50 $100 $150 $200 $250 Purchase price Annual projected rig cash flow ($ in millions) $0 $50 $100 $150 $200 $250 Construction cost ($ in millions) |

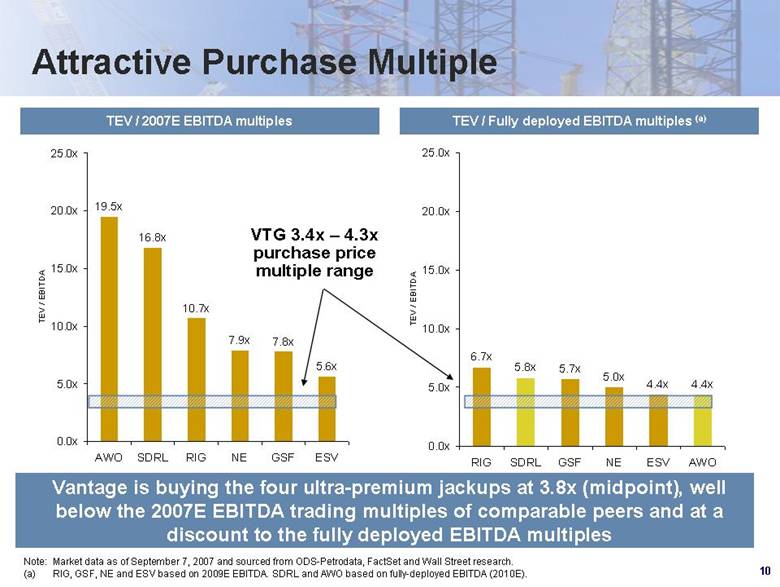

| Attractive Purchase Multiple Vantage is buying the four ultra-premium jackups at 3.8x (midpoint), well below the 2007E EBITDA trading multiples of comparable peers and at a discount to the fully deployed EBITDA multiples TEV / 2007E EBITDA multiples TEV / Fully deployed EBITDA multiples (a) Note: Market data as of September 7, 2007 and sourced from ODS-Petrodata, FactSet and Wall Street research. (a) RIG, GSF, NE and ESV based on 2009E EBITDA. SDRL and AWO based on fully-deployed EBITDA (2010E). VTG 3.4x – 4.3x purchase price multiple range 19.5x 16.8x 7.9x 7.8x 5.6x 10.7x 0.0x 5.0x 10.0x 15.0x 20.0x 25.0x AWO SDRL RIG NE GSF ESV TEV / EBITDA 6.7x 5.8x 5.7x 5.0x 4.4x 4.4x 0.0x 5.0x 10.0x 15.0x 20.0x 25.0x RIG SDRL GSF NE ESV AWO TEV / EBITDA |

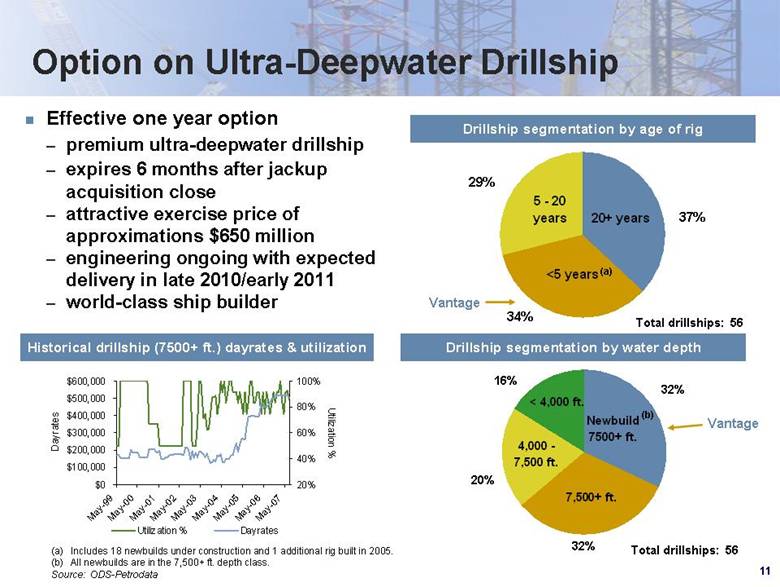

| 32% 32% 20% Vantage 16% Option on Ultra-Deepwater Drillship (a) Includes 18 newbuilds under construction and 1 additional rig built in 2005. (b) All newbuilds are in the 7,500+ ft. depth class. Source: ODS-Petrodata Effective one year option premium ultra-deepwater drillship expires 6 months after jackup acquisition close attractive exercise price of approximations $650 million engineering ongoing with expected delivery in late 2010/early 2011 world-class ship builder Historical drillship (7500+ ft.) dayrates & utilization 34% 29% 37% Vantage Drillship segmentation by age of rig (a) Total drillships: 56 Drillship segmentation by water depth Total drillships: 56 (b) Newbuild 7500+ ft. 7,500+ ft. 4,000 - 7,500 ft. < 4,000 ft. 20+ years <5 years 5 - 20 years $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 May-99 May-00 May-01 May-02 May-03 May-04 May-05 May-06 May-07 Dayrates 20% 40% 60% 80% 100% Utilization % Utilization % Dayrates |

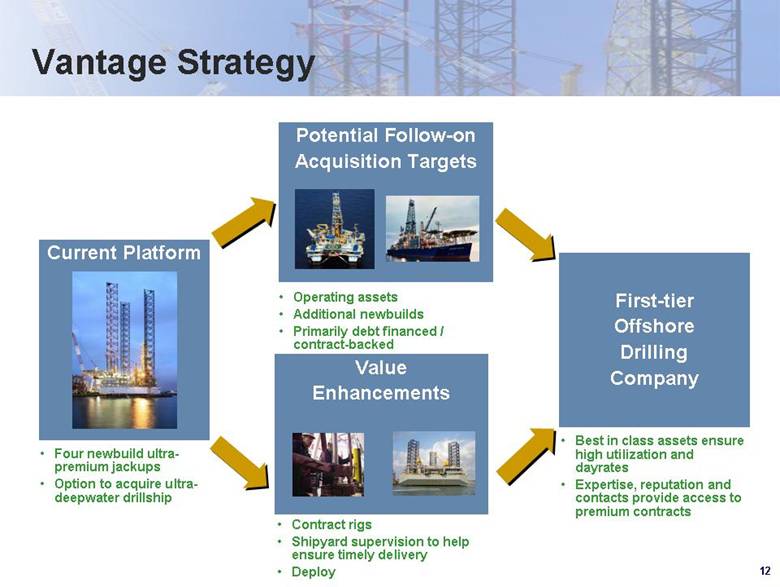

| Vantage Strategy Current Platform First-tier Offshore Drilling Company Four newbuild ultra-premium jackups Option to acquire ultra-deepwater drillship Best in class assets ensure high utilization and dayrates Expertise, reputation and contacts provide access to premium contracts Contract rigs Shipyard supervision to help ensure timely delivery Deploy Operating assets Additional newbuilds Primarily debt financed / contract-backed Value Enhancements Potential Follow-on Acquisition Targets |

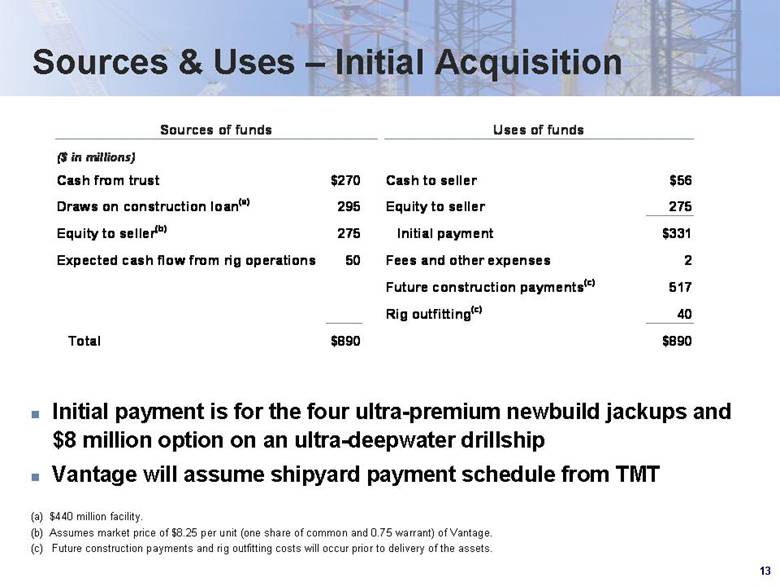

| Sources & Uses – Initial Acquisition Initial payment is for the four ultra-premium newbuild jackups and $8 million option on an ultra-deepwater drillship Vantage will assume shipyard payment schedule from TMT (a) $440 million facility. (b) Assumes market price of $8.25 per unit (one share of common and 0.75 warrant) of Vantage. (c) Future construction payments and rig outfitting costs will occur prior to delivery of the assets. Sources of funds Uses of funds ($ in millions) Cash from trust $270 Cash to seller $ 56 Draws on construction loan (a) 295 Equity to seller 275 Equity to seller (b) 275 $ 331 Expected cash flow from rig operations 50 Fees and other ex penses 2 Future construction payments ( c ) 517 Rig outfitting ( c ) 40 $ 890 $ 890 Total Initial payment |

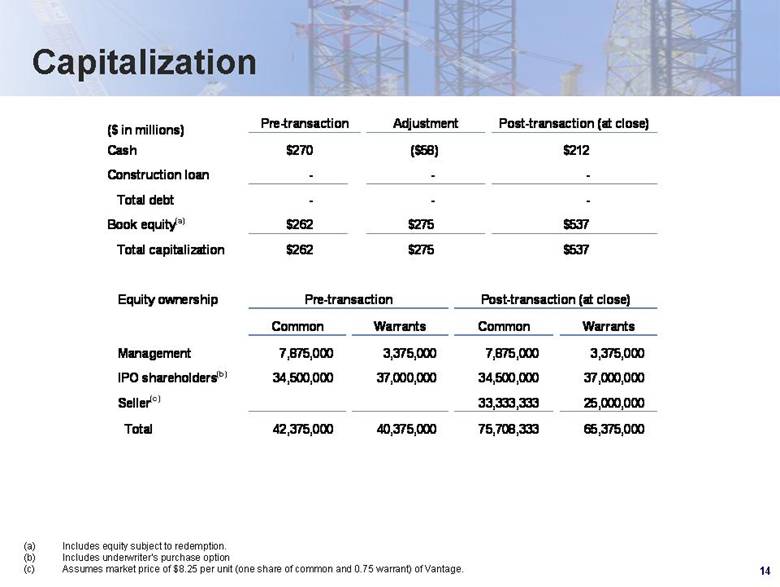

| Capitalization Includes equity subject to redemption. Includes underwriter’s purchase option Assumes market price of $8.25 per unit (one share of common and 0.75 warrant) of Vantage. ($ in millions) Pre - transaction Adjustment Post - transaction (at close) Cash $270 ($ 5 8 ) $2 1 2 Construction loan - - - - - - Book equit y (a) $ 262 $ 275 $ 537 $ 262 $ 275 $ 537 Equity ownership Pre - transaction Post - tr ansaction (at close) Common Warrants Common Warrants Management 7,875,000 3,375,000 7,875,000 3,375,000 IPO shareholders (b) 3 4 , 500 ,000 3 7 , 000 ,000 3 4 , 500 ,000 3 7 , 000 ,000 Seller ( c ) 33,333,333 25,000,000 4 2 , 375 ,000 40 , 375 ,000 75,708,333 65,375, 000 Total Total capitalization Total debt |