Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-157550

PROSPECTUS

SENSATA TECHNOLOGIES B.V.

Offer to Exchange

THE SECURITIES LISTED BELOW FOR SUBSTANTIALLY IDENTICAL SECURITIES

THAT HAVE BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933:

€141,000,000 11.25% Senior Subordinated Notes due 2014

Material Terms of Exchange Offer

| • | We sold the outstanding notes on July 23, 2008 to placement agents who subsequently re-sold such securities to qualified institutional buyers under Rule 144A and non-U.S. persons under Regulation S. |

| • | The terms of the notes to be issued in the exchange offer described in this prospectus are substantially identical to the outstanding notes, except that the transfer restrictions and registration rights relating to the outstanding notes will not apply to the exchange notes. |

| • | Based on interpretations by the staff of the Securities Exchange Commission (“SEC”), we believe that, subject to some exceptions, the exchange notes may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act of 1933, as amended. |

| • | The outstanding notes are listed on the Luxembourg Stock Exchange. We have applied for listing of the exchange notes on the Luxembourg Stock Exchange. |

| • | The exchange offer expires at 5:00 p.m., London time, 12:00 p.m., New York City time, April 9, 2009, unless extended. |

| • | You may withdraw tenders of outstanding notes at any time prior to the expiration of the exchange offer. |

| • | You may tender your outstanding notes in integral multiples of €1,000. |

| • | We believe that the exchange of the notes will not be a taxable event for U.S. federal income tax purposes. |

| • | The exchange offer is subject to customary conditions, including that the exchange offer does not violate applicable law or any applicable interpretation of the staff of the SEC. |

| • | We will not receive any proceeds from the exchange offer. |

| • | The exchange notes will be fully and unconditionally guaranteed on an unsecured basis by certain of our subsidiaries in the U.S., the Netherlands, Mexico, Brazil, Japan, South Korea and Malaysia. |

We are not asking you for a proxy and you are not requested to send us a proxy.

For a discussion of certain factors that you should consider before participating in the exchange offer, see “Risk Factors” beginning on page 14 of this prospectus.

Neither the SEC nor any state securities commission has approved or disapproved of the notes to be distributed in the exchange offer, nor have any of these organizations determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is March 10, 2009.

Table of Contents

This prospectus incorporates business and financial information about Sensata Technologies B.V. that is not included in or delivered with this prospectus. This information is available free of charge to security holders upon written or oral request to: Sensata Technologies B.V., Kolthofsingel 8, 7602 EM Almelo, the Netherlands; (telephone 31-546-879-555). To obtain timely delivery, security holders must request this information no later than five business days before the date they must make their investment decision. Security holders must request this information by April 2, 2009.

| Page | ||

| 1 | ||

| 14 | ||

| 32 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 44 | ||

| 45 | ||

Selected Combined and Consolidated Historical Financial Data | 46 | |

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations | 49 | |

| 80 | ||

| 96 | ||

| 99 | ||

| 111 | ||

| 113 | ||

| 115 | ||

| 122 | ||

| 189 | ||

| 196 | ||

| 200 | ||

| 201 | ||

| 203 | ||

| 203 | ||

| 203 | ||

| 204 | ||

| F-1 |

Table of Contents

The following summary is qualified in its entirety by the more detailed information, including the section entitled “Risk Factors” and the consolidated and combined financial statements and related notes, included elsewhere in this prospectus. Because this is a summary, it may not contain all of the information that may be important to you. You should read the entire prospectus and the other documents to which we have referred you before deciding whether to invest in the notes.

Unless the context indicates otherwise, in this prospectus, the term “outstanding notes” refers to the €141.0 million of 11.25% senior subordinated notes due January 15, 2014, that we issued on July 23, 2008, the terms “exchange notes” or “Notes” refer to the €141.0 million of 11.25% senior subordinated notes due January 15, 2014, Series B, being offered hereby, and the term “notes” refers to both the outstanding notes and exchange notes.

Company Information

Sensata Technologies B.V., (“Sensata”) the issuer of the exchange notes, is a private company with limited liability incorporated under the laws of the Netherlands and was formed on February 8, 2006. The Sensors & Controls (“S&C”) business traces its origins to 1916 and was owned by Texas Instruments Incorporated (“TI”) between 1959 and April 26, 2006. Sensata is a direct, wholly-owned subsidiary of Sensata Technologies Intermediate Holding B.V., (“Sensata Intermediate Holding”). Sensata Intermediate Holding is a direct wholly- owned subsidiary of Sensata Technologies Holding B.V. (“Parent”) and Parent is a direct wholly-owned subsidiary of Sensata Investment Company S.C.A. (“Ultimate Parent”). The address of our corporate headquarters is Kolthofsingel 8, 7602 EM Almelo, the Netherlands, and the address of our primary U.S. operating subsidiary is 529 Pleasant Street, Attleboro, Massachusetts, and its telephone number is (508) 236-3800.

Our Sponsors

A company controlled by funds (the “Bain Capital Funds”) managed by advisers associated with Bain Capital LLC (“Bain Capital”) beneficially own approximately 90% of our ultimate parent. See “—Corporate Structure.”

Founded in 1984, Bain Capital is a leading global investment firm managing approximately $75 billion in assets through its affiliated investment advisers, including private equity, venture capital, high-yield debt and public equity, and has more than 300 investment professionals. Since its inception, Bain Capital’s private equity adviser, Bain Capital Partners, LLC, and its predecessors have raised 14 private equity funds and have made more than 300 investments and add-on acquisitions. Bain Capital Partners is uniquely positioned given its deep experience in a variety of industries and its strategy consulting background and expertise that enable the firm to provide its portfolio companies and management partners with significant strategic and operational guidance. Headquartered in Boston, Bain Capital also has offices in Chicago, New York, London, Munich, Hong Kong, Shanghai, Tokyo and Mumbai.

The 2006 Acquisition

On April 27, 2006, Bain Capital Funds completed the acquisition of the S&C business of TI for an aggregate purchase price of $3.0 billion, excluding fees and expenses. We refer to the 2006 Acquisition, together with the following related events, collectively as the “Transactions”:

| • | The payment of $3.0 billion in cash to TI for the S&C business. |

| • | A cash investment by funds managed by advisers associated with Bain Capital and co-investors of $985.0 million. |

1

Table of Contents

| • | A senior secured credit facility that includes term loan borrowings of $1.35 billion and a $150.0 million revolving credit facility, of which $10.0 million was drawn in connection with the 2006 Acquisition and repaid during fiscal year 2006. The senior term loan borrowings included $950.0 million of U.S. dollar denominated borrowings and €325.0 million ($400.1 million, at issuance) of Euro denominated borrowings. |

| • | The issuance and sale of $450.0 million aggregate principal amount of 8% senior notes due 2014 and €245.0 million ($301.6 million, at issuance) aggregate principal amount of 9% Euro denominated senior subordinated notes due 2016. |

Sensata and one of its subsidiaries are the borrowers under the Senior Secured Credit Facility and Sensata is the issuer of the outstanding notes, including the notes subject to the exchange offer. Sensata is an indirect wholly owned subsidiary of Parent, which is the ultimate holding company for the S&C business and which is owned indirectly by investment funds associated with or designated by the Sponsors and certain members of our senior management through a Luxembourg-based investment vehicle known as Sensata Investment Company S.C.A., as well as directly by certain members of our senior management through our equity incentive plan. See “—Corporate Structure.” The acquisition of the S&C business was effected through a number of subsidiaries of Sensata that collectively acquired the assets and assumed the liabilities being transferred in connection with the S&C business.

Our Company

Sensata is a global designer and manufacturer of sensors and controls and has manufacturing operations in the Americas and Asia. We design, manufacture and market a wide range of customized, highly-engineered sensors and controls. We operate as two global business units: sensors and controls, based on differences in products included in each segment. We believe that we are one of the largest suppliers of sensors and controls in each of the key applications in which we compete and that we have developed our strong market position due to our technological expertise, long-standing customer relationships, broad product portfolio and competitive cost structure.

Our sensors business is a leading manufacturer of a variety of sensors used in automotive, commercial and industrial products. Our sensors products include pressure sensors and switches, as well as position, force and acceleration sensors. Our acquisition of the First Technology Automotive and Special Products (“FTAS” or “FTAS Acquisition”) business from Honeywell International Inc. (“Honeywell”) in December 2006 added steering position and fuel cut-off switch devices to our portfolio of products.

Our controls business is a leading manufacturer of a variety of engineered controls used in the industrial, aerospace, military, commercial and residential markets. Our controls products include motor and compressor protectors, circuit breakers, precision switches and thermostats, power-inverters and semiconductor burn-in test sockets (“BITS”). We market our controls products primarily under the Klixon®, Airpax® and Dimensions® brands. Our acquisition of the Airpax Holdings, Inc. (“Airpax” or “Airpax Acquisition”) business from William Blair Capital Partners VIII QP, L.P. (“William Blair”) in July 2007 further strengthened our customer positions in electrical protection and secured our position as a leading designer and manufacturer of sensing and electrical protection solutions for the industrial, heating, ventilation, air conditioning, military and mobile markets.

We are a global business with a diverse revenue mix. We have significant operations around the world, and we generated approximately 53% of our net revenue for fiscal year 2008 outside the Americas. In addition, our largest customer accounted for approximately 7% of our net revenue for fiscal year 2008, and our ten largest customers contributed a total of 40% of our net revenues during this period. Our fiscal year 2008 net revenues

2

Table of Contents

were derived from the following end markets; 17% from North American automotive, 34% from automotive outside of North America, 14% from appliances and heating, ventilating and air conditioning (“HVAC”), 14% from industrial, 7% from heavy vehicle/off road (“HVOR”), and 14% from other end-markets. Within many of our end-markets, we are a significant supplier to most or all major original equipment manufacturers, or “OEMs,” reducing our exposure to fluctuations in market share within individual end-markets.

We generated net revenue of $1,422.7 million during the year ended December 31, 2008. We have grown our net revenue at a compound annual rate of 8.9% from 2003 through 2008.

Our Strengths

Our strengths include:

| • | Leading Market Positions and Established Customer Relationships, |

| • | Leadership Position in Growing Applications, |

| • | Scaleable, Tailored Portfolio of Highly-Engineered Products for Critical Applications, |

| • | High Switching Costs and Significant Barriers to Competitive Entry, |

| • | Global Business with Diverse Revenue Mix, |

| • | Competitive Cost Manufacturer with Global Asset Base, |

| • | Significant Revenue Visibility, and |

| • | Experienced Management Team. |

Our Strategy

Our business strategy includes:

| • | Product Innovation and Expansion Into Growing Applications, |

| • | Develop and Strengthen Customer Relationships, |

| • | Build on Low-Cost Position, |

| • | Continue to Pursue Attractive Strategic Acquisitions, and |

| • | Recruiting, Retaining and Developing Talent. |

Airpax Acquisition

On July 27, 2007, we acquired Airpax for a purchase price of $277.3 million including fees and expenses. We believe the acquisition of Airpax provides us with leading customer positions in electrical protection for high-growth network power and critical, high-reliability mobile power applications, and further secures our position as a leading designer and manufacturer of sensing and electrical protection solutions for the industrial, heating, ventilation, air conditioning, military and mobile markets. The acquisition also adds new products such as power inverters and expands our customer end-markets to include growing network power applications where customers value high reliability and differentiated performance. In July 2007, we entered into a €141.0 million ($195.0 million, at issuance) senior subordinated term loan, issued as bridge financing, which, together with cash on hand, was used to finance the Airpax Acquisition.

We used the proceeds from the outstanding notes to repay amounts owed under this senior subordinated term loan.

3

Table of Contents

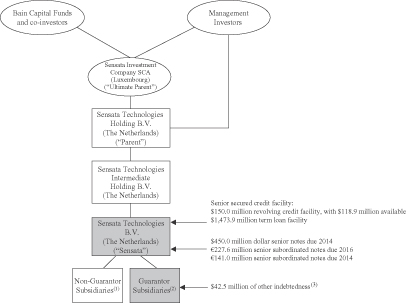

Corporate Structure

The following chart reflects our corporate structure and principal indebtedness as of December 31, 2008:

| (1) | Our non-guarantor subsidiaries include subsidiaries located in the following jurisdictions: Dominican Republic, United Kingdom, Bermuda, China, Taiwan, Germany, Italy, France, Spain, Singapore, India and Hong Kong, as well as certain of our subsidiaries in the United States, the Netherlands, Japan and Mexico. See “Risk Factors—Risk Factors Related To The Notes—The notes are structurally subordinated in right of payment to the indebtedness and other liabilities of those of our existing and future subsidiaries that do not guarantee the notes, and to the indebtedness and other liabilities of any guarantor whose guarantee of the notes is deemed to be unenforceable.” |

| (2) | Certain of our subsidiaries in the U.S. and the Netherlands, as well as certain subsidiaries in the following jurisdictions, guarantee the notes: Mexico, Brazil, Japan, South Korea and Malaysia. We own, directly or indirectly, 100% of the stock or other equity interests of each of our guarantor subsidiaries. For the year ended December 31, 2008, we and our guarantor subsidiaries represented 92.0% of our consolidated net revenue after elimination of inter-company sales, and substantially all of our profit from operations. As of December 31, 2008, we and our guarantor subsidiaries represented 92.4% and 97.7% of our consolidated total assets and liabilities, respectively, after elimination of intercompany balances. See “Risk Factors—Risk Factors Related To The Notes—The notes are structurally subordinated in right of payment to the indebtedness and other liabilities of those of our existing and future subsidiaries that do not guarantee the notes, and to the indebtedness and other liabilities of any guarantor whose guarantee of the notes is deemed to be unenforceable.” |

| (3) | Reflects capitalized lease obligations held by certain subsidiaries associated with our Attleboro facility and certain manufacturing equipment, and other financing obligations associated with our manufacturing facility in Kuala Lumpur, Malaysia and a warehouse in Mexico. |

We operate through subsidiaries with general corporate and manufacturing facilities and operations in the United States, Mexico, Brazil, the Dominican Republic, the Netherlands, Japan, South Korea, Malaysia and China and marketing and sales operations in Taiwan, Hong Kong, India, Singapore, Spain, France and Germany. Certain of our direct and indirect subsidiaries are guarantors under the notes offered hereby. See “Description of Other Indebtedness”, “Description of the Notes—Guarantees” and “Risk Factors—Risk Factors Related To The Notes—The notes are structurally subordinated in right of payment to the indebtedness and other liabilities of

4

Table of Contents

those of our existing and future subsidiaries that do not guarantee the notes, and to the indebtedness and other liabilities of any guarantor whose guarantee of the notes is deemed to be unenforceable.”

On March 3, 2009, we announced the commencement of two separate cash tender offers, one to purchase the maximum aggregate principal amount of our 8% Senior Notes due 2014 (the “8% Senior Notes”) that we can purchase for $40.0 million (excluding accrued interest and subject to increase) at a purchase price per $1,000 principal amount determined in accordance with a modified Dutch auction procedure on the terms and conditions set forth in the Offer to Purchase dated March 3, 2009 (the “Offer to Purchase”) and the other to purchase the maximum aggregate principal amount of our 9% Senior Subordinated Notes due 2016 (the “9% Senior Subordinated Notes”) and our 11.25% Senior Subordinated Notes due 2014 (the “11.25% Senior Subordinated Notes” and, together with the 9% Senior Subordinated Notes, the “Senior Subordinated Notes”) that we can purchase for $10.0 million (excluding accrued interest and subject to increase, the “Maximum Euro Payment Amount”) at a purchase price per €1,000 principal amount determined in accordance with a modified Dutch auction procedure on the terms and conditions set forth in the Offer to Purchase. The Maximum Euro Payment Amount is limited by certain restrictive covenants contained in our Senior Secured Credit Facility.

The Tender Offers for 8% Senior Notes and Senior Subordinated Notes are scheduled to expire at 11:59 P.M., New York City time, on March 30, 2009, unless extended or earlier terminated by the Company.

Summary of the Exchange Offer

The Initial Offering of Outstanding Notes | We sold the outstanding notes on July 23, 2008 to Morgan Stanley & Co, Inc., Bank of America Securities LLC and Goldman, Sachs & Co. We refer to these parties in this prospectus collectively as the “initial purchasers.” The initial purchasers subsequently resold all or a portion of the outstanding notes: (i) to qualified institutional buyers pursuant to all or a portion of Rule 144A; or (ii) outside the United States in compliance with Regulation S, each as promulgated under the Securities Act of 1933, as amended (the “Securities Act”). |

Registration Rights Agreement | Simultaneously with the initial sale of the outstanding notes, we entered into a registration rights agreement for the exchange offer. In the registration rights agreement, we agreed, among other things, to use our reasonable best efforts to file a registration statement with the SEC within 240 days of issuing the outstanding notes, to have such registration statement declared effective within 360 days of issuing the outstanding notes, and to complete the exchange offer within 40 business days of the effectiveness of the registration statement. The exchange offer is intended to satisfy your rights under the registration rights agreement. After the exchange offer is complete, you will no longer be entitled to any exchange or registration rights with respect to your outstanding notes. |

Exchange Offer | We are offering to exchange the exchange notes for outstanding notes. The exchange notes have been registered under the Securities Act. All outstanding notes that are validly tendered and not validly withdrawn will be exchanged. We will issue exchange notes promptly after the expiration of the exchange offer. The outstanding notes may be tendered only in integral multiples of €1,000. |

5

Table of Contents

Resales | Based on interpretations by the staff of the SEC set forth in no-action letters issued to unrelated parties, we believe that the exchange notes issued in the exchange offer may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: |

| • | the exchange notes are being acquired in the ordinary course of your business; |

| • | you are not participating, do not intend to participate, and have no arrangement or understanding with any person to participate, in the distribution of the exchange notes issued to you in an exchange offer; and |

| • | you are not an affiliate of ours. |

| If any of these conditions are not satisfied and you transfer any exchange notes issued to you in an exchange offer without delivering a prospectus meeting the requirements of the Securities Act or without an exemption from registration of your exchange notes from these requirements, you may incur liability under the Securities Act. We will not assume, nor will we indemnify you against, any such liability. |

| Each broker-dealer that is issued exchange notes in an exchange offer for its own account in exchange for outstanding notes that were acquired by that broker-dealer as a result of market-making or other trading activities, must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act in connection with any resale of the exchange notes. A broker-dealer may use this prospectus for an offer to resell, resale or other retransfer of the exchange notes issued to it in an exchange offer. |

Record Date | We mailed this prospectus and the related exchange offer documents to registered holders of outstanding notes on March 11, 2009. |

Expiration Date | The exchange offer will expire at 5:00 p.m., London time, 12:00 p.m., New York City time, on April 9, 2009, unless we decide to extend it. |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, including that the exchange offer does not violate applicable law or any applicable interpretation of the staff of the SEC. |

Procedures for Tendering Outstanding Notes | We issued the outstanding notes as global securities. When the outstanding notes were issued, we deposited the global notes with the custodians for the book-entry depositary. The book-entry depositary issued depositary interests in respect of each global note to Euroclear or Clearstream, and then recorded such interests in their respective books and records in the name of the common depositary for Euroclear and Clearstream. All of the outstanding notes are held in book-entry form through Euroclear or Clearstream. You may tender your outstanding notes through the book-entry transfer systems of |

6

Table of Contents

Euroclear and Clearstream. See “Exchange Offer—Procedures for Tendering” for more information. |

Special Procedures for Beneficial Owners | If you are the beneficial owner of book-entry interests and your name does not appear on a security position listing of Euroclear and Clearstream as the holder of the book-entry interests or if you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender the book-entry interest or outstanding notes in an exchange offer, you should contact the person in whose name your book-entry interests or outstanding notes are registered promptly and instruct that person to tender on your behalf. |

Withdrawal Rights | You may withdraw the tender of your outstanding notes at any time prior to 5:00 p.m., London time, 12:00 p.m., New York City time, on April 9, 2009. |

Acceptance of Outstanding Notes and Delivery of Exchange Notes | If you fulfill all conditions required for proper acceptance of outstanding notes, we will accept any and all outstanding notes that you properly tender in an exchange offer on or before 5:00 p.m., London time, 12:00 p.m., New York City time, on the expiration date. We will return any outstanding notes that we do not accept for exchange to you without expense as promptly as practicable after the expiration date. We will deliver the exchange notes as promptly as practicable after the expiration date and acceptance of the outstanding notes for exchange. See “Exchange Offer—Terms of the Exchange Offer.” |

Use of Proceeds; Fees and Expenses | We will not receive any proceeds from the issuance of the exchange notes pursuant to the exchange offer. We will pay all of our expenses incident to the exchange offer. |

U.S. Federal Income Tax Considerations | We believe that the exchange of outstanding notes will not be a taxable event for U.S. federal income tax purposes. |

Exchange Agents | The Bank of New York Mellon is serving as the principal exchange agent in connection with the exchange offer. The Bank of New York (Luxembourg) S.A. is serving as the exchange agent in Luxembourg in connection with the exchange offer. |

7

Table of Contents

Summary of Terms of the Exchange Notes

The form and terms of the exchange notes are the same as the form and terms of the outstanding notes, except that the exchange notes will be registered under the Securities Act. As a result, the exchange notes will not bear legends restricting their transfer and will not contain the registration rights and liquidated damage provisions contained in the outstanding notes.

Issuer | Sensata Technologies B.V. |

Notes Offered | €141,000,000 aggregate principal amount of 11.25% Senior Subordinated Notes due January 15, 2014, Series B. |

Maturity | January 15, 2014. |

Interest | The exchange notes bear interest at 11.25% per annum, payable semi-annually in arrears on January 15 and July 15 of each year, beginning on January 15, 2009. |

Optional Redemption | We may redeem some or all of the exchange notes beginning on January 15, 2010, at the redemption prices listed under “Description of the Notes—Optional Redemption,” plus accrued interest. |

We may also redeem any of the exchange notes at any time prior to January 15, 2010, at a redemption price equal to 100% of the principal amount of the exchange notes to be redeemed, plus the Applicable Premium, defined under “Description of the Notes—Certain Definitions” as of, and accrued interest to, the redemption date.

We may also redeem up to 40% of the exchange notes on or prior to January 15, 2010 from the proceeds of certain equity offerings and designated asset sales at a redemption price equal to 111.25% of the principal amount of the exchange notes, plus accrued interest, if any, to the date of redemption only if, after any such redemption, at least 50% of the aggregate principal amount of exchange notes remain outstanding. See “Description of the Notes—Optional Redemption.”

Additional Amounts; Tax Redemption | All payments in respect of the exchange notes will be made without withholding or deduction for any taxes or other governmental charges, except to the extent required by law. If withholding or deduction is required by law, subject to certain exceptions, we will pay additional amounts so that the net amount you receive is no less than what you would have received in the absence of such withholding or deduction. See “Description of the Notes—Additional Amounts.” |

If certain changes in the law of any relevant taxing jurisdiction become effective that would impose withholding taxes or other deductions on the payments on the exchange notes or the guarantees, we may redeem the exchange notes in whole, but not in part, at any time, at a redemption price of 100% of the principal amount, plus accrued and unpaid interest, if any, and additional amounts, if any, to the date of redemption.

8

Table of Contents

Change of Control | Upon a change of control, as defined under the section entitled “Description of the Notes—Certain Definitions,” we will be required to make an offer to purchase the exchange notes then outstanding at a purchase price equal to 101% of their principal amount, plus accrued interest to the date of repurchase. We may not have sufficient funds available at the time of any change of control to make any required debt repayment (including repurchases of the exchange notes). |

Guarantees | The exchange notes are guaranteed on a senior subordinated basis, jointly and severally by each of our existing and future wholly owned subsidiaries that is a guarantor under our Senior Secured Credit Facility, subject to certain exceptions. Our Parent has not guaranteed the exchange notes. See “Description of the Notes—Guarantees.” |

Ranking | The exchange notes are unsecured senior subordinated obligations and rank: |

| • | junior in right of payment to all of our existing and future senior indebtedness, including any indebtedness under our Senior Secured Credit Facility and our senior notes, and any guarantees thereof; |

| • | structurally junior to all of the obligations, including trade payables, of any subsidiaries that do not guarantee the exchange notes; |

| • | equally in right of payment with our existing senior subordinated notes and all of our future senior subordinated indebtedness, if any; |

| • | senior in right of payment to any of our future indebtedness, if any, that is expressly subordinated in right of payment to the exchange notes; and |

| • | effectively junior in right of payment to all our secured indebtedness, including any indebtedness under our senior secured credit facility, to the extent of the value of the assets securing that indebtedness. |

Similarly, the guarantee of each guarantor of the exchange notes ranks:

| • | junior in right of payment to all of such guarantor’s existing and future senior indebtedness, including its guarantee of our senior notes and its guarantee of borrowings under our senior secured credit facility; |

| • | structurally junior to all of the obligations, including trade payables, of any subsidiaries that do not guarantee the exchange notes; |

| • | equally in right of payment with such guarantor’s guarantee of our existing senior subordinated notes and any future senior subordinated indebtedness, if any, of such guarantor; |

| • | senior in right of payment to any future indebtedness, if any, of such guarantor that is expressly subordinated in right of payment to the guarantee of the exchange notes; and |

9

Table of Contents

| • | effectively junior in right of payment to all of such guarantor’s secured indebtedness, including its guarantee under our senior secured credit facility, to the extent of the value of the assets securing that indebtedness. |

Certain Covenants | The indenture governing the exchange notes contains certain covenants that limit our ability and the ability of our restricted subsidiaries to: |

| • | incur additional debt or issue preferred stock; |

| • | create liens; |

| • | create restrictions on our subsidiaries’ ability to make payments to Sensata; |

| • | pay dividends and make other distributions in respect of our capital stock; |

| • | redeem or repurchase our capital stock or prepay subordinated indebtedness; |

| • | make certain investments or certain other restricted payments; |

| • | guarantee indebtedness; |

| • | designate unrestricted subsidiaries; |

| • | sell certain kinds of assets; |

| • | enter into certain types of transactions with affiliates; or |

| • | effect mergers or consolidations. |

These covenants are subject to a number of important exceptions and qualifications. See “Description of the Notes.”

Trading and Listing | We have applied to list the exchange notes on the official list of the Luxembourg Stock Exchange and to trade the exchange notes on the Euro MTF market of such Exchange. However, the exchange notes are not yet listed. The exchange notes are a new issue of securities with no established trading market. |

Luxembourg Paying Agent and Transfer Agent | The Bank of New York (Luxembourg) S.A. will be the Luxembourg paying agent and Luxembourg transfer agent in respect of the exchange notes in the event they are listed on the Luxembourg Stock Exchange. The address and telephone number of the Luxembourg paying agent and Luxembourg transfer agent are set forth, on the inside back cover of this prospectus. |

Luxembourg Listing Agent | The Bank of New York (Luxembourg) S.A. is the Luxembourg listing agent in respect of the exchange notes. The address and telephone number of the Luxembourg listing agent are set forth, on the inside back cover of this prospectus. |

RISK FACTORS

Before making an investment decision, you should carefully consider all of the information in this prospectus, including the discussion under the caption “Risk Factors” beginning on page 14, for a discussion of certain risks of participating in the exchange offer.

10

Table of Contents

SUMMARY HISTORICAL FINANCIAL DATA

Set forth below is summary historical condensed combined financial data of the S&C business for the period from January 1, 2006 to April 26, 2006. The combined results are presented because the S&C business was under the common ownership and common management of TI for these periods. Set forth below is summary historical condensed consolidated financial data of Sensata for the period from April 27, 2006 to December 31, 2006 and the years ended December 31, 2007 and December 31, 2008. Prior to the 2006 Acquisition, the S&C business operated as a business unit of TI. As a result, the historical financial data for the S&C business included elsewhere in this prospectus does not necessarily reflect what our operations would have been had we operated the business as a separate, stand-alone entity during those periods. We sometimes refer to the S&C business as our “Predecessor.” The summary historical data of the S&C business for the period from January 1, 2006 to April 26, 2006 and of Sensata for the period from April 27, 2006 to December 31, 2006 and years ended December 31, 2007 and December 31, 2008 have been derived from the audited historical financial statements which are included elsewhere in this prospectus.

This information is only a summary and should be read in conjunction with the historical financial statements and the related notes thereto and other financial information appearing elsewhere in this prospectus, including “Capitalization,” “Selected Historical Combined and Consolidated Financial Data,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

11

Table of Contents

| Predecessor (combined) | Sensata Technologies B.V. (consolidated) | |||||||||||||||

| For the period | ||||||||||||||||

| (Amounts in thousands) | January 1 - April 26, 2006 | April 27 - December 31, 2006 | Year ended December 31, | |||||||||||||

| 2007 | 2008 | |||||||||||||||

Statement of Operations Data: | ||||||||||||||||

Net revenue | $ | 375,600 | $ | 798,507 | $ | 1,403,254 | $ | 1,422,655 | ||||||||

Operating costs and expenses: | ||||||||||||||||

Cost of revenue | 253,028 | 538,867 | 950,316 | 958,860 | ||||||||||||

Research and development | 8,635 | 19,742 | 33,900 | 38,270 | ||||||||||||

Selling, general and administrative | 39,752 | 175,107 | 291,556 | 308,216 | ||||||||||||

Impairment of goodwill | — | — | — | | 13,173 | | ||||||||||

Restructuring | 2,456 | — | 5,166 | 24,124 | ||||||||||||

Total operating costs and expenses | 303,871 | 733,716 | 1,280,938 | 1,342,643 | ||||||||||||

Profit from operations | 71,729 | 64,791 | 122,316 | 80,012 | ||||||||||||

Interest expense | (511 | ) | (165,160 | ) | (191,161 | ) | (197,840 | ) | ||||||||

Interest income | — | 1,567 | 2,574 | 1,503 | ||||||||||||

Currency translation (loss)/gain and other, net(1) | 115 | (63,633 | ) | (105,474 | ) | 55,455 | ||||||||||

Income (loss) from continuing operations before income taxes | 71,333 | (162,435 | ) | (171,745 | ) | (60,870 | ) | |||||||||

Provision for income taxes | 25,796 | 48,560 | 62,504 | 53,531 | ||||||||||||

Income (loss) from continuing operations | 45,537 | (210,995 | ) | (234,249 | ) | (114,401 | ) | |||||||||

Loss from discontinued operations, net of tax of $0 | (167 | ) | (1,309 | ) | (18,260 | ) | (20,082 | ) | ||||||||

Net income (loss) | $ | 45,370 | $ | (212,304 | ) | $ | (252,509 | ) | $ | (134,483 | ) | |||||

Other Financial Data: | ||||||||||||||||

Net cash provided by (used in): | ||||||||||||||||

Operating activities | $ | 40,599 | $ | 129,906 | $ | 155,278 | $ | 47,821 | ||||||||

Investing activities | (16,705 | ) | (3,142,543 | ) | (355,710 | ) | (38,713 | ) | ||||||||

Financing activities | (23,894 | ) | 3,097,390 | 175,736 | 8,551 | |||||||||||

Capital expenditures | 16,705 | 29,630 | 66,701 | 40,963 | ||||||||||||

EBITDA(2) | 81,286 | 111,037 | 187,850 | 315,508 | ||||||||||||

Ratio of earnings to fixed charges (unaudited)(3) | 63.4 | NM | NM | NM | ||||||||||||

| Sensata Technologies B.V. (consolidated) | ||||||||||||||||

| (Amounts in thousands) | As of December 31, | |||||||||||||||

| 2008 | ||||||||||||||||

Balance Sheet Data: | ||||||||||||||||

Cash and cash equivalents | $ | 77,716 | ||||||||||||||

Working capital(4) | 201,940 | |||||||||||||||

Total assets | 3,303,074 | |||||||||||||||

Total debt, including capital lease and other financing obligations | 2,511,187 | |||||||||||||||

Shareholder’s equity | 405,051 | |||||||||||||||

| (1) | Currency translation (loss)/gain and other, net in the period from April 27, 2006 to December 31, 2006 primarily includes currency translation loss associated with Euro denominated debt and the Deferred Payment Certificates (“DPCs”) of $65.5 million. Currency translation (loss)/gain and other, net for the years ended December 31, 2007 and 2008 primarily includes currency translation (loss)/gain associated with the Euro denominated debt of $(111.9) million and $53.2 million, respectively. |

12

Table of Contents

| (2) | EBITDA (earnings before interest, taxes, depreciation and amortization) is a non-GAAP financial measure. We believe that EBITDA provides investors with helpful information with respect to our operations. EBITDA is used by management and investors to evaluate our operating performance exclusive of financing costs and depreciation policies. In addition to its use to monitor performance trends, EBITDA provides a comparative metric to management and investors that is consistent across companies with different capital structures and depreciation policies. This enables management and investors to compare our performance to that of our peers. The use of EBITDA has limitations and you should not consider EBITDA in isolation from or as an alternative to GAAP measures such as net income. |

The following unaudited table summarizes the calculation of EBITDA and provides a reconciliation to net income (loss), the most directly comparable financial measure presented in accordance with GAAP, for the periods presented:

| Predecessor (combined) | Sensata Technologies B.V. (consolidated) | |||||||||||||||

| For the period | ||||||||||||||||

| January 1 - April 26, 2006 | April 27 - December 31, 2006 | Year ended December 31, | ||||||||||||||

| 2007 | 2008 | |||||||||||||||

Net income (loss) | $ | 45,370 | $ | (212,304 | ) | $ | (252,509 | ) | $ | (134,483 | ) | |||||

Provision for income taxes | 25,796 | 48,560 | 62,504 | 53,531 | ||||||||||||

Interest expense, net | 511 | 163,593 | 188,587 | 196,337 | ||||||||||||

Depreciation and amortization | 9,609 | 111,188 | 189,268 | 200,123 | ||||||||||||

EBITDA | $ | 81,286 | $ | 111,037 | $ | 187,850 | $ | 315,508 | ||||||||

| (3) | Ratio of earnings to fixed charges is calculated by dividing (1) “earnings” which consist of earnings from continuing operations and fixed charges, by (2) “fixed charges” which consist of interest expense and the estimated interest portion of rental payments on operating leases. Earnings were insufficient to cover fixed charges due to losses from continuing operations before taxes incurred of $(162,435), $(171,745) and $(60,870) for the period April 27, 2006 to December 31, 2006 and the years ended December 31, 2007 and December 31, 2008, respectively. Therefore, the ratio of earnings to fixed charges is not meaningful for those periods. Additional earnings of $162,435, $171,745 and $60,870, respectively, must be generated to achieve a coverage ratio of 1:1. |

| (4) | We define working capital as current assets less current liabilities. Prior to the Acquisition, we participated in TI’s centralized system for cash management, under which our cash flows were transferred to TI on a regular basis and netted against TI’s net investment account. Consequently, none of TI’s cash, cash equivalents, debt or interest expense has been allocated to our business in the Predecessor historical combined financial statements. |

13

Table of Contents

You should carefully consider the risks described below, and in the documents incorporated by reference, before making an investment decision. The risks described below are not the only ones facing us. Any of the following risks, and additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also materially and adversely affect our business, financial condition or results of operations. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your original investment.

Risks Factors Related To The Exchange Offer

Because there is no public market for the exchange notes, you may not be able to resell your exchange notes.

The exchange notes will be registered under the Securities Act, but will constitute a new issue of securities with no established trading market, and there can be no assurance as to:

| • | the liquidity of any trading market that may develop; |

| • | the ability of holders to sell their exchange notes; and |

| • | the price at which the holders would be able to sell their exchange notes. |

If a trading market were to develop, the exchange notes might trade at higher or lower prices than their principal amount or purchase price, depending on many factors, including prevailing interest rates, the market for similar securities and our financial performance.

We understand that the initial purchasers presently intend to make a market in the outstanding notes. However, they are not obligated to do so, and any market-making activity with respect to the notes may be discontinued at any time without notice. In addition, any market-making activity will be subject to the limits imposed by the Securities Act and the Securities Exchange Act of 1934, as amended, or the “Exchange Act,” and may be limited during the exchange offer or the pendency of an applicable shelf registration statement. There can be no assurance that an active trading market will exist for the notes or that any trading market that does develop will be liquid. We have applied to list the exchange notes on the Luxembourg Stock Exchange; however, we cannot assure you that a Luxembourg Stock Exchange listing will be obtained.

In addition, any outstanding note holder who tenders in the exchange offer for the purpose of participating in a distribution of the exchange notes may be deemed to have received restricted securities, and if so, will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. For a description of these requirements, see “Exchange Offer.”

Your outstanding notes will not be accepted for exchange if you fail to follow the procedures for the exchange offer and, as a result, your outstanding notes will continue to be subject to existing transfer restrictions and you may not be able to sell your outstanding notes.

We will not accept your outstanding notes for exchange if you do not follow the procedures for the exchange offer. We will issue exchange notes as part of the exchange offer only after a timely receipt of your outstanding notes and all other required documents. Therefore, if you want to tender your outstanding notes, please allow sufficient time to ensure timely delivery. If we do not receive your outstanding notes and other required documents by the expiration date of the exchange offer, we will not accept your outstanding notes for exchange. We are under no duty to give notification of defects or irregularities with respect to the tenders of outstanding notes for exchange. If there are defects or irregularities with respect to your tender of outstanding notes, we will not accept your outstanding notes for exchange.

If you do not exchange your outstanding notes, your outstanding notes will continue to be subject to the existing transfer restrictions and you may not be able to sell your outstanding notes.

We did not register the outstanding notes nor do we intend to do so following the exchange offer. Outstanding notes that are not tendered will therefore continue to be subject to the existing transfer restrictions and may be transferred only in limited circumstances under the securities laws. If you do not exchange your outstanding notes, you will lose your right to have such outstanding notes registered under the federal securities laws. As a result, if you hold outstanding notes after the exchange offer, you may not be able to sell your outstanding notes.

14

Table of Contents

Risk Factors Related To Our Business

Our operating results and financial condition have been and may continue to be adversely affected by the current financial crisis and worldwide economic conditions.

The current financial crisis affecting the banking system and financial markets and the uncertainty in global economic conditions has resulted in a significant tightening of the credit markets, a low level of liquidity in financial markets, decreased consumer confidence, and reduced corporate profits and capital spending. These conditions make it difficult for our customers, our vendors and us to accurately forecast and plan future business activities, and have caused, and may continue to cause, our customers to reduce spending on our products. We cannot predict the timing or duration of the global economic crisis or the timing or strength of a subsequent economic recovery. If the economy or markets in which we operate experience continued weakness at current levels or deteriorate further, our business, financial condition and results of operations would be materially and adversely affected.

Conditions in the automotive industry have had and may continue to have adverse effects on our results of operations.

51% of our sales are to customers in the automotive industry. Automakers and their suppliers globally have experienced significant difficulties from a weakened economy and tightening credit markets. General Motors, Chrysler and several U.S. tier 1 suppliers have sought government sponsored financial assistance to avoid bankruptcy proceedings. Globally, many automakers and their suppliers are in financial distress. Continued adverse developments in the automotive industry, including but not limited to continued sharp declines in demand, customer bankruptcies, and increased demands on us for pricing decreases, would have adverse effects on our results of operations and could impact our liquidity position and our ability to meet restrictive debt covenants. In addition, these same conditions could adversely impact certain of our vendors’ financial solvency resulting in potential liabilities or additional costs to us to ensure uninterrupted supply to our customers.

Continued fundamental changes in the industries in which we operate have had and could continue to have adverse effects on our businesses.

Our products are sold to automobile manufacturers and manufacturers of commercial and residential HVAC systems, as well as to manufacturers in the refrigeration, lighting, aerospace, telecommunications, power supply and generation and industrial markets, among others. These are global industries, and they are experiencing various degrees of growth and consolidation. Customers in these industries are located in every major geographic market. As a result, our customers are affected by changes in global and regional economic conditions, as well as by labor relations issues, regulatory requirements, trade agreements and other factors. This, in turn, affects overall demand and prices for our products sold to these industries. For example, the significant economic decline during the fourth quarter of 2008 has resulted in a reduction in automotive production and in the sales of many of the other products manufactured by our customers that use our products, and has had an adverse effect on our results of operations. This negative outlook is expected to continue throughout 2009. This may be more detrimental to us in comparison to our competitors due to our significant debt levels. In addition, many of our products are platform-specific—for example, sensors are designed for certain of our HVAC manufacturer customers according to specifications to fit a particular model. Our success may, to a certain degree, be connected with the success or failure of one or more of the industries to which we sell products, either in general or with respect to one or more of the platforms or systems for which our products are designed.

Our businesses operate in markets that are highly competitive, and competitive pressures could require us to lower our prices or result in reduced demand for our products.

Our businesses operate in markets that are highly competitive, and we compete on the basis of product performance, quality, service and/or price across the industries and markets we serve. A significant element of our competitive strategy is to manufacture high-quality products at low-cost, particularly in markets where low-cost country-based suppliers, primarily China with respect to the controls business, have entered our markets or increased their sales in our markets by delivering products at low-cost to local OEMs. Some of our competitors have

15

Table of Contents

greater sales, assets and financial resources than we do. In addition, many of our competitors in the automotive sensors market are controlled by major OEMs or suppliers, limiting our access to certain customers. Many of our customers also rely on us as their sole source of supply for the products we have historically sold to them. These customers may choose to develop relationships with additional suppliers or elect to produce some or all of these products internally, in each case in order to reduce risk of delivery interruptions or as a means of extracting pricing concessions. Competitive pressures such as these, and others, could affect prices or customer demand for our products, negatively impacting our profit margins and/or resulting in a loss of market share.

Continued pricing and other pressures from our customers may adversely affect our business.

Many of our customers, including automotive manufacturers and other industrial and commercial OEMs, have policies of seeking price reductions each year. Recently, many of the industries in which our products are sold have suffered from unfavorable pricing pressures in North America and Europe, which in turn has led manufacturers to seek price reductions from their suppliers. Our significant reliance on these industries subjects us to these and other similar pressures. While the precise effects of such instability on the industries in which we operate are difficult to determine, price reductions could impact our sales and profit margins. If we are not able to offset continued price reductions through improved operating efficiencies and reduced expenditures, those price reductions may have a material adverse effect on our results of operations and cash flows. In addition, our customers occasionally require engineering, design or production changes. In some circumstances, we may be unable to cover the costs of these changes with price increases. Additionally, as our customers grow larger, they may increasingly require us to provide them with our products on an exclusive basis, which could cause an increase in the number of products we must carry and, consequently, increase our inventory levels and working capital requirements. Certain of our customers, particularly domestic automotive manufactures, are increasingly requiring their suppliers to agree to their standard purchasing terms without deviation as a condition to engage in future business transactions. As a result, we may find it difficult to enter into agreements with such customers on terms that are commercially reasonable.

We are subject to risks associated with our non-U.S. operations, which could adversely impact the reported results of operations from our international businesses.

We generated approximately53% of our net revenue for fiscal year 2008 outside the Americas, and we expect sales from non-U.S. markets to continue to represent a significant portion of our total sales. International sales and operations are subject to changes in local government regulations and policies, including those related to tariffs and trade barriers, investments, taxation, exchange controls, and repatriation of earnings.

A portion of our revenues and expenses and receivables and payables are denominated in currencies other than U.S. dollars. We are therefore subject to foreign currency risks and foreign exchange exposure. Changes in the relative values of currencies occur from time to time and could affect our operating results. In our consolidated and combined financial statements, we remeasure certain local currency financial results into U.S. dollars based on average exchange rates prevailing during a reporting period (for purposes of reporting statements of operations data) or the exchange rate at the end of that period (for purposes of reporting balance sheet data). During times of a weakening U.S. dollar, our reported international sales and earnings will increase because the non-U.S. currency will translate into more U.S. dollars. Similiarly, during times of a strengthening U.S. dollar, our reported international sales and earnings will be reduced because the local currency will translate into fewer U.S. dollars.

There are other risks that are inherent in our non-U.S. operations, including the potential for changes in socio-economic conditions and/or monetary and fiscal policies, intellectual property protection difficulties and disputes, the settlement of legal disputes through certain foreign legal systems, the collection of receivables through certain foreign legal systems, exposure to possible expropriation or other government actions, unsettled political conditions and possible terrorist attacks against American interests. These and other factors may have a material adverse effect on our non-U.S. operations and therefore on our business and results of operations.

16

Table of Contents

We may not realize all of the revenue or achieve anticipated gross margins from products subject to existing purchase orders or for which we are currently engaged in development.

Our ability to generate revenues from sensors and controls subject to customer awards is subject to a number of important risks and uncertainties, many of which are beyond our control, including the number of products our customers will actually produce as well as the timing of such production. Many of our customer contracts provide for supplying a certain share of the customer’s requirements for a particular application or platform, rather than for manufacturing a specific quantity of products. As a result, in some cases we have no remedy if a customer chooses to purchase less than we expect, while in other cases customers do make minimum

volume commitments to us, but our remedy for their failure to meet those minimum volumes is limited to increased pricing on those products the customer does purchase from us or renegotiating other contract terms and there is no assurance that such price increases or new terms will offset a shortfall in expected revenue. In addition, some of our customers may have the right to discontinue a program or replace us with another supplier under certain circumstances, subject in some cases to a “break-up” fee that helps us defray our initial investment. As a result, products for which we are currently incurring development expenses may not be manufactured by customers at all, or may be manufactured in smaller amounts than currently anticipated. Therefore, our anticipated future revenue from sensors and controls relating to existing customer awards or product development relationships may not result in firm orders from customers for the same amount. We also incur capital expenditures and other costs, and price our products, based on estimated production volumes. If actual production volumes were significantly lower than estimated, our anticipated revenue and gross margin from those new products would be adversely affected. We cannot predict the ultimate demand for our customers’ products, nor can we predict the extent to which we would be able to pass through unanticipated per-unit cost increases to our customers.

The loss of one or more of our suppliers of finished goods or raw materials may interrupt our supplies and materially harm our business.

We purchase raw materials and components from a wide range of suppliers. However, for certain raw materials or components we may be dependent on sole source suppliers. Our ability to meet our customers’ needs depends on our ability to maintain an uninterrupted supply of raw materials and finished products from our third- party suppliers and manufacturers. Our business, financial condition or results of operations could be adversely affected if any of our principal third party suppliers or manufacturers experience production problems, lack of capacity or transportation disruptions. The magnitude of this risk depends upon the timing of the changes, the materials or products that the third party manufacturers provide and the volume of the production.

Our dependence on third parties for raw materials and components subjects us to the risk of supplier failure and customer dissatisfaction with the quality of our products. Quality failures by our third party manufacturers or changes in their financial or business condition which affect their production could disrupt our ability to supply quality products to our customers and thereby materially harm our business.

Increasing costs for manufactured components and raw materials may adversely affect our profitability.

We use a broad range of manufactured components and raw materials in the manufacture of our products, including copper, nickel, gold and silver, which may experience significant volatility in their prices. While we generally purchase raw materials at spot prices (except where we have enforceable long-term supply contracts), we first entered into hedge arrangements in 2007 and may continue to do so from time to time in the future. Such hedges might not be economically successful. In addition, the hedges might not qualify as an effective hedge in accordance with Generally Accepted Accounting Principles (“GAAP”) in the United States. Accordingly, there could be significant volatility in the results of operations from quarter to quarter. The availability and price of raw materials and manufactured components may be subject to change due to, among other things, new laws or regulations, global economic or political events including strikes, terrorist actions and war, suppliers’ allocations to other purchasers, interruptions in production by suppliers, changes in exchange rates and prevailing price

17

Table of Contents

levels. It is generally difficult to pass increased prices for manufactured components and raw materials through to our customers in the form of price increases. Therefore, a significant increase in the price of these items could materially increase our operating costs and materially and adversely affect our profit margins.

Non-performance by our suppliers may adversely affect our operations.

Because we purchase various types of raw materials and component parts from suppliers, we may be materially and adversely affected by the failure of those suppliers to perform as expected. This non-performance may consist of delivery delays or failures caused by production issues or delivery of non-conforming products. The risk of non-performance may also result from the insolvency or bankruptcy of one or more of our suppliers.

Our efforts to protect against and to minimize these risks may not always be effective. As we continually review the performance and price competitiveness of our suppliers, we may occasionally seek to engage new suppliers with which we have little or no experience.

Labor disruptions or increased labor costs could adversely affect our business.

As of December 31, 2008, we had9,278 employees, of whom approximately12% were located in the United States. None of our U.S. employees are covered by collective bargaining agreements. Approximately 1,062 employees at our manufacturing operations in Matamoros, Mexico are covered under collective bargaining agreements. In addition, in various countries, local law requires our participation in works councils. A material labor disruption or work stoppage at one or more of our manufacturing facilities could have a material adverse effect on our business. In addition, work stoppages occur relatively frequently in the industries in which many of our customers operate, such as the automotive industry. If one or more of our larger customers were to experience a material work stoppage, that customer may halt or limit the purchase of our products. This could cause us to shut down production facilities relating to those products, which could have a material adverse effect on our business, results of operations and financial condition.

We depend on third parties for certain transportation, warehousing and logistics services.

We rely primarily on third parties for transportation of the products we manufacture. In particular, a significant portion of the goods we manufacture are transported to different countries, requiring sophisticated warehousing, logistics and other resources. If any of the countries from which we transport products were to suffer delays in exporting manufactured goods, or if any of our third party transportation providers were to fail to deliver the goods we manufacture in a timely manner, we may be unable to sell those products at full value, or at all. Similarly, if any of our raw materials could not be delivered to us in a timely manner, we may be unable to manufacture our products in response to customer demand.

A material disruption at one of our manufacturing facilities could harm our financial condition and operating results.

If one of our manufacturing facilities were to be shut down, or certain of our manufacturing operations within an otherwise operational facility were to cease production unexpectedly, our revenue and profit margins would be adversely affected. Such a disruption could be caused by a number of different events, including:

| • | maintenance outages; |

| • | prolonged power failures; |

| • | an equipment failure; |

| • | fires, floods, earthquakes or other catastrophes; |

| • | potential unrest or terrorist activity; |

| • | labor difficulties; or |

| • | other operational problems. |

18

Table of Contents

In addition, most of our manufacturing facilities are located outside the United States. Serving a global customer base requires that we place more production in emerging markets to capitalize on market opportunities and maintain our best-cost position. Our international production facilities and operations could be particularly vulnerable to the effects of a natural disaster, labor strike, war, political unrest, terrorist activity or public health concerns, especially in emerging countries that are not well-equipped to handle such occurrences. Our manufacturing facilities abroad also may be more susceptible to changes in laws and policies in host countries and economic and political upheaval than our domestic facilities. If any of these or other events were to result in a material disruption of our manufacturing operations, our ability to meet our production capacity targets and satisfy customer requirements may be impaired.

We may not be able to keep up with rapid technological and other competitive changes affecting our industry.

The sensors and controls markets are characterized by rapidly changing technology, evolving industry standards, frequent enhancements to existing services and products, the introduction of new services and products and changing customer demands. Changes in competitive technologies may render certain of our products less attractive or obsolete, and if we cannot anticipate changes in technology and develop and introduce new and enhanced products on a timely basis, our ability to remain competitive may be negatively impacted. The success of new products depends on their initial and continued acceptance by our customers. Our businesses are affected by varying degrees of technological change, which result in unpredictable product transitions, shortened lifecycles and increased importance of being first to market with new products and services. We may experience difficulties or delays in the research, development, production and/or marketing of new products, which may negatively impact our operating results and prevent us from recouping or realizing a return on the investments required to bring new products to market.

As part of our on-going cost containment program designed to align our operations with economic conditions, we have had to make, and will likely continue to make, adjustments to both the scope and breadth of our overall research and development program. Such actions may result in choices that could adversely affect our ability to either take advantage of emerging trends or to develop new technologies or make sufficient advancements to existing technologies.

We may incur material losses and costs as a result of product liability and warranty and recall claims that may be brought against us.

We have been and may continue to be exposed to product liability and warranty claims in the event that our products actually or allegedly fail to perform as expected or the use of our products results, or is alleged to result, in bodily injury and/or property damage. Accordingly, we could experience material warranty or product liability losses in the future and incur significant costs to defend these claims. In addition, if any of our products are, or are alleged to be, defective, we may be required to participate in a recall of the underlying end product, particularly if the defect or the alleged defect relates to product safety. Depending on the terms under which we supply products, an OEM may hold us responsible for some or all of the repair or replacement costs of these products under warranties, when the product supplied did not perform as represented. Our costs associated with providing product liabilities could be material.

Continued compliance with Section 404 of the Sarbanes-Oxley Act of 2002 (“Section 404”) may be costly with no assurance of maintaining effective internal control over financial reporting.

We will likely continue to experience significant operating expenses in connection with maintaining our internal control environment and Section 404 compliance activities. In addition, if we are unable to efficiently maintain effective internal control over financial reporting, our operations may suffer and we may be unable to obtain an attestation on internal control from our independent registered public accounting firm when required under the Sarbanes-Oxley Act of 2002. Recent cost reduction actions, including the loss of experienced finance

19

Table of Contents

and administrative personnel, may adversely effect our ability to maintain effective internal controls. This, in turn, could have a materially adverse impact on trading prices for our securities and adversely affect our ability to access the capital markets.

We may not be able to protect our intellectual property, including our proprietary technology and the Klixon®, Airpax® and Dimensions® brands.

Our success depends to some degree on our ability to protect our intellectual property and to operate without infringing on the proprietary rights of third parties. While we have been issued patents and have registered trademarks with respect to many of our products, if we fail to adequately protect our intellectual property, competitors may manufacture and market products similar to ours. While we have sought and may continue from time to time to seek to protect our intellectual property rights through litigation, these efforts might be unsuccessful in protecting such rights and may adversely affect our financial performance and distract our

management. We also cannot be sure that competitors will not challenge, invalidate or void the application of any existing or future patents that we receive or license. In addition, patent rights may not prevent our competitors from developing, using or selling products that are similar or functionally equivalent to our products. It is also possible that third parties may have or acquire licenses for other technology or designs that we may use or wish to use, so that we may need to acquire licenses to, or contest the validity of, such patents or trademarks of third parties. Such licenses may not be made available to us on acceptable terms, if at all, and we may not prevail in contesting the validity of third party rights.

In addition to patent and trademark protection, we also protect trade secrets, know-how and other confidential information, as well as brand names such as the Klixon®, Airpax® and Dimensions® brands under which we market many of the products sold in our controls business, against unauthorized use by others or disclosure by persons who have access to them, such as our employees, through contractual arrangements. These arrangements may not provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. Disputes may arise concerning the ownership of intellectual property or the applicability of confidentiality agreements, and we cannot be sure that our trade secrets and proprietary technology will not otherwise become known or that our competitors will not independently develop our trade secrets and proprietary technology. If we are unable to maintain the proprietary nature of our technologies, our sales could be materially adversely affected.

We may be subject to claims that our products or processes infringe the intellectual property rights of others, which may cause us to pay unexpected litigation costs or damages, modify our products or processes or prevent us from selling our products.

Although it is our intention to avoid infringing on or otherwise violating the intellectual property rights of others, third parties may nevertheless claim that our processes and products infringe on their intellectual property rights. Whether or not these claims have merit, we may be subject to costly and time-consuming legal proceedings, and this could divert our management’s attention from operating our business. If these claims are successfully asserted against us, we could be required to pay substantial damages and could be prevented from selling some or all of our products. We may also be obligated to indemnify our business partners or customers in any such litigation. Furthermore, we may need to obtain licenses from these third parties or substantially reengineer or rename our products in order to avoid infringement. In addition, we might not be able to obtain the necessary licenses on acceptable terms, or at all, or be able to reengineer or rename our products successfully. This could prevent us from selling some or all of our products.

20

Table of Contents

Export of our products are subject to various export control regulations and may require a license from either the U.S. Department of State, the U.S. Department of Commerce or the U.S. Department of the Treasury.

We must comply with the United States Export Administration Regulations (“EAR”), the International Traffic in Arms Regulations (“ITAR”), and the sanctions, regulations and embargoes administered by the Office of Foreign Assets Control. Certain of our products that have military applications are on the munitions list of the ITAR and require an individual validated license in order to be exported to certain jurisdictions. Any changes in export regulations may further restrict the export of our products, and we may cease to be able to procure export licenses for our products under existing regulations. The length of time required by the licensing process can vary, potentially delaying the shipment of products and the recognition of the corresponding revenue. Any restriction on the export of a significant product line or a significant amount of our products could cause a significant reduction in revenue.

We may be adversely affected by environmental, safety and governmental regulations or concerns.

We are subject to the requirements of environmental and occupational safety and health laws and regulations in the United States and other countries, as well as product performance standards established by

quasi governmental and industrial standards organizations. We cannot assure you that we have been or will be at all times in complete compliance with all of these requirements, or that we will not incur material costs or liabilities in connection with these requirements in excess of amounts we have reserved. In addition, these requirements are complex, change frequently and have tended to become more stringent over time. These requirements may change in the future in a manner that could have a material adverse effect on our business, results of operations and financial condition. We have made and will continue to make capital and other expenditures to comply with environmental requirements. In addition, certain of our subsidiaries are subject to pending litigation raising various environmental and human health and safety claims. We cannot assure you that our costs to defend and settle these claims will not be material.

Integration of acquired companies and any future acquisitions and joint ventures or dispositions may require significant resources and/or result in significant unanticipated losses, costs or liabilities.

We have grown and in the future we intend to grow by making acquisitions or entering into joint ventures or similar arrangements. Any future acquisitions will depend on our ability to identify suitable acquisition candidates, to negotiate acceptable terms for their acquisition and to finance those acquisitions. We will also face competition for suitable acquisition candidates that may increase our costs. In addition, acquisitions or investments require significant managerial attention, which may be diverted from our other operations. Furthermore, acquisitions of businesses or facilities, including those which may occur in the future, entail a number of additional risks, including:

| • | problems with effective integration of operations; |

| • | the inability to maintain key pre-acquisition customer, supplier and employee relationships; |

| • | increased operating costs; and |

| • | exposure to unanticipated liabilities. |

Subject to the terms of our indebtedness, we may finance future acquisitions with cash from operations, additional indebtedness and/or by issuing additional equity securities. In addition, we could face financial risks associated with incurring additional indebtedness such as reducing our liquidity and access to financing markets and increasing the amount of debt service. If conditions in the credit markets remain tight, the availability of debt to finance future acquisitions will be restricted and our ability to make future acquisitions will be limited.

21

Table of Contents

We may also seek to restructure our business in the future by disposing of certain of our assets. For example, the terms of the exchange notes allow us to dispose of our controls business and use the proceeds to either repay indebtedness, including the exchange notes , or make limited restricted payments to our stockholders, subject to certain conditions (including satisfying certain pro forma leverage ratios). There can be no assurance that any restructuring of our business will not adversely affect our financial position, leverage or results of operations. In addition, any significant restructuring of our business will require significant managerial attention which may be diverted from our operations and may require us to accept non-cash consideration for any sale of our assets, the market value of which may fluctuate.

We may not realize all of the anticipated operating synergies and cost savings from acquisitions, and we may experience difficulties in integrating these businesses, which may adversely affect our financial performance.